No sooner has the UK construction industry thrown off the recessionary shackles than an industrial dispute among crane drivers threatens to undermine a recovery that is growing in momentum. At the time of writing, major construction sites are set for severe disruption on three consecutive Fridays (starting November 7th) as crane drivers employed by HTC Plant Limited begin industrial action. The company’s 180 plus crane drivers have overwhelmingly voted in favour of strike action in a dispute over pay. A large number of sites across London and the rest of England are set to be affected including: Crossrail, the London Bridge redevelopment, Nova Square Victoria, the Elephant and Castle redevelopment and the Atomic Weapons Establishment at Aldermarston. Major construction contractors set to be affected include: Kier, Lend Lease, Bam, Costain, Mace and Vinci. According to industry union UCATT, since the recession in 2008 crane drivers at HTC have experienced several pay freezes and their pay has plummeted in real terms. UCATT had previously attempted to undertake pay negotiations with HTC but the company did not table an offer that came close to the expectations of members. Steve Murphy, General Secretary of construction union UCATT, said: “Construction sites are facing massive disruption because HTC have failed to make a realistic pay offer to our members.” construction inside NOVEMBER 2014 Established 2011 Issue No. 27 Powered by BCLIVE.co.uk Please visit The Builders’ Conference website www.buildersconference.co.uk/newsandevents Construction sites set for shutdown on Friday as crane drivers begin strike action. Recovery Threatened by Crane Dispute

Transcript

No sooner has the UK constructionindustry thrown off the recessionaryshackles than an industrial disputeamong crane drivers threatens toundermine a recovery that isgrowing in momentum.

At the time of writing, majorconstruction sites are set for severe

disruption on three consecutiveFridays (starting November 7th) ascrane drivers employed by HTCPlant Limited begin industrial action.

The company’s 180 plus cranedrivers have overwhelmingly voted infavour of strike action in a disputeover pay.

A large number of sites acrossLondon and the rest of England areset to be affected including:Crossrail, the London Bridgeredevelopment, Nova SquareVictoria, the Elephant and Castleredevelopment and the AtomicWeapons Establishment atAldermarston.

Major construction contractors set tobe affected include: Kier, LendLease, Bam, Costain, Mace andVinci.

According to industry union UCATT,since the recession in 2008 cranedrivers at HTC have experiencedseveral pay freezes and their payhas plummeted in real terms. UCATThad previously attempted toundertake pay negotiations withHTC but the company did not tablean offer that came close to theexpectations of members.

Steve Murphy, General Secretary ofconstruction union UCATT, said:“Construction sites are facingmassive disruption because HTChave failed to make a realistic payoffer to our members.”

constructioninsi

de

NOVEMBER 2014 Established 2011 Issue No. 27Powered by BCLIVE.co.uk

Please visit The Builders’ Conference website www.buildersconference.co.uk/newsandevents

Construction sites set for shutdown on

Friday as crane drivers begin strike action.

Recovery Threatenedby Crane Dispute

A Downturn

THE INSIDER

In The Event OfTo BeOpened

Ever since Bing Crosby and the writers of

White Christmas received their first annual

royalty cheque, the music industry has been

adept at planning ahead and setting aside a

little something for the future.

It was 1982 that Prince penned 1999, safe in the knowledgethat 17 years hence – and regardless of his career trajectory- he was due a cash windfall. Jarvis Cocker followed suit in1995 with the release of Disco 2000 five years before Y2K;five years before Robbie Williams assailed eardrums andspoiled John Barry’s “You Only Live Twice” riff forever withhis “Millennium” dirge.

Tying your words to a significant yet inevitable future event isnot just financially astute; it speaks to a mythical prescience.And, let’s face it, there is very little more satisfying than throwingopen one’s arms to address the predicted vista whilst wearing asmug smile that says “see, I told you so.”

In this spirit, I have penned this column to our future industry inthe hope that it will offer some insight, guidance and comfortwhen the next inevitable downturn happens:

There are just

a few things you

can do to make the

transition from

recession to recovery

just that little

bit smoother

Dear ConstructionIndustry

If you are reading this, the chancesare that you find yourselves staringdown the barrel of what us old-timersused to call a “recession” (you mighthave coined a new phrase for this bynow; if so, I hope it’s something fluffyand less filled with foreboding).

Regardless, the important part of theword recession is the “re” at thebeginning; you know, like repeat,reimagine, regain. In other words, itrefers to something that has happenedbefore. (That said, I don’t think wecalled the first industry downturn a“cession” but I digress).

You have probably been told by nowthat your industry is cyclical. But, intruth, the industry behaves far morelike a rubber ball dropped from agreat height – Each low is followedby a high, which is followed by alow, which is….well, you get theidea. And if history has taught usanything it is that the more thingschange, the more things stay thesame or “plus ça change, plus c’estla même chose” as they say inFrance. Yes, France, that slightlyodd-smelling country the other side ofthe tunnel boarded up when TheGrand Wizard Farage swept topower in the great UKIP uprising (ornot, as the case may be).

In short, what I am trying to sayto you from beyond thegrave/care homeperimeter wall is that thedarkest hour is just beforethe dawn. Things mightlook bleak now but youare almost certainly justweeks/months/years*(*delete as applicable)from the next upturn.

Until then, there arejust a few things youcan do to make thetransition fromrecession to recoveryjust that little bitsmoother:Do your best tomaintain training levels

– The first thing you are going to needwhen the upturn comes are peoplethat can actually do the work.

Keep your systems up to date –Assuming that computers haven’t beenreplaced just yet, keep your softwareup to date. Computer systems havea nasty habit of becoming obsoletewhile you’re worrying about wherethe next cheque is coming from.

Nail your cash-flow – As cash hasprobably been replaced byplastic/hologram by now, this maysound like an archaic term, but the rulesstill apply. The first sign of a truerecession is that formerly reliable payersbecome less reliable. (For the record,the second sign of a true recession isthat even those that have no intention ofpaying will stop buying).

If the recession means you’re notworking for your business, work ONyour business – Experience tells usthat those most likely to survive adownturn are those that are lean andmean, quick to diversify and to seize

and that his revolutionbegan and ended with abook of that name, you

probably still have to toil underpoliticians. If yours are anything likeours, they know nothing. The onlytime they have ever set foot on aconstruction site is to deliver a scriptedsound-bite whilst wearing a hard hat(you still have those, right?)

I realise that this will be of scantconsolation to you right now as youstruggle to afford your next loaf of 3D-

printed bread/economy flight to AlphaCentauri, but things will get better.

Oh, and just so you know, yes, therereally was a time when a nation ofmillions used to huddle around aplastic box to watch other peoplemake cakes; there was a time whenthere was real music made by peoplethat could sing or play musicalinstruments, not just that prescribed byCowell the Merciless andOmnipotent; and there really was atime when West Ham (the footballteam that played at the OlympicStadium before it was turned intoVirgin Galactic’s spaceship dock)were fourth in the Premier League.

They were simpler times.

Yours Sincerely

(2014)The Insider

The first thing you are going to

need when the upturn comes are

people that can actually

do the work

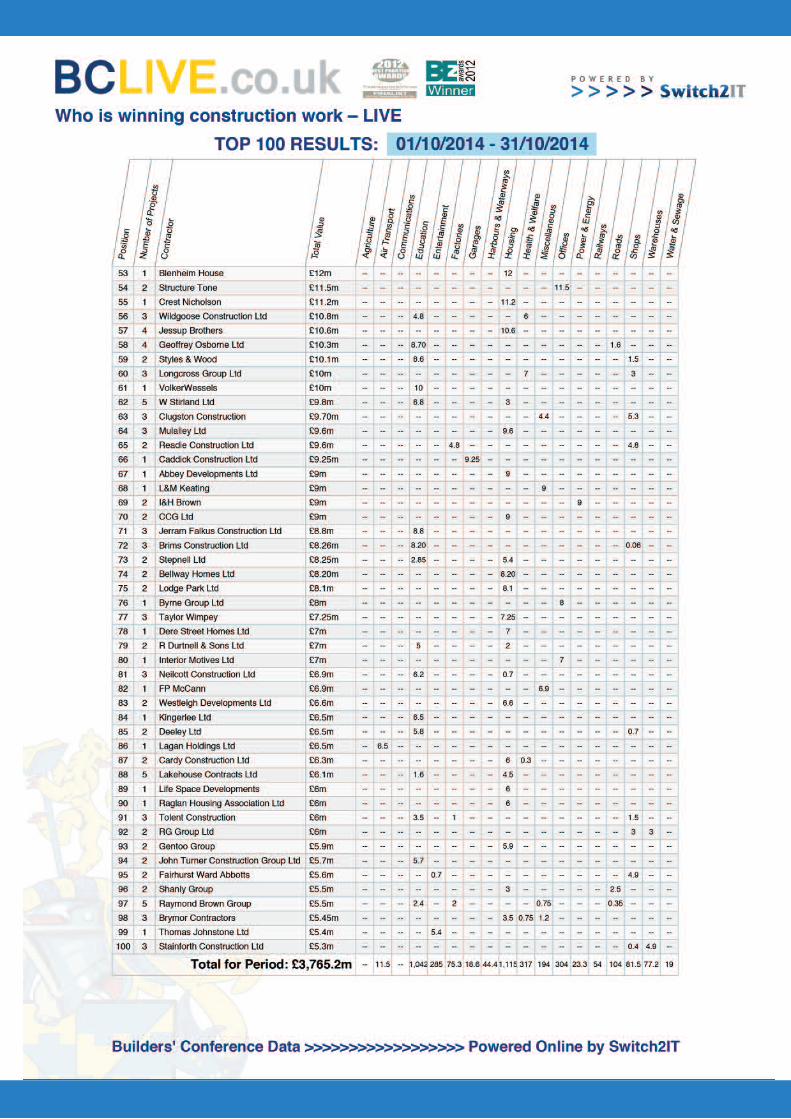

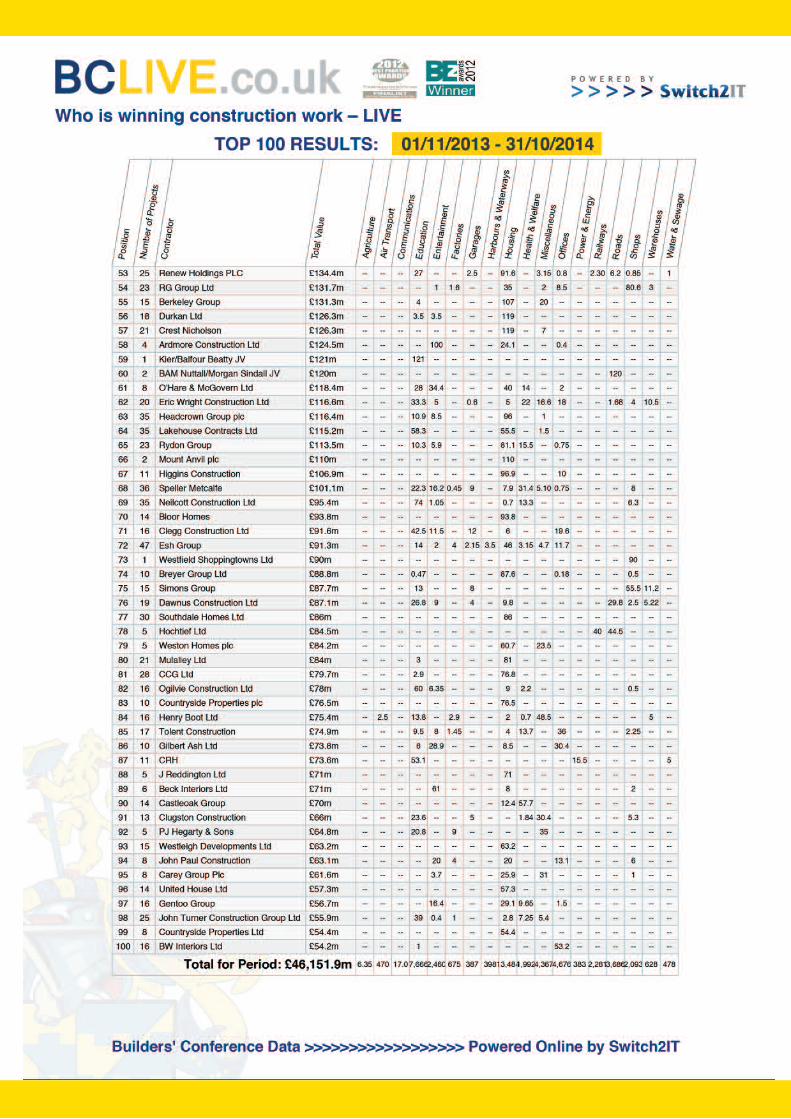

The BCLive league table for Octoberwas never likely to replicate the highsof the preceding month. But with atotal value of almost £3.8 billion, thesigns are that the recovery remainson track, according to The Builders’Conference CEO Neil Edwards.

October traditionally marks thebeginning of the winter slowdown inconstruction circles. So nobodyexpected the BCLive league table toreplicate the astonishing performance oflast month. And yet, with a combinedvalue of almost £3.8 billion spreadacross a total of 775contracts, the industry’srecovery remains verymuch on an upwardtrajectory. Of course,compared to theanomalous £5.7billion total achieved inSeptember, this lookslike a near £2 billionslide in the wrongdirection. Butfactoring inseasonality, thisremains a strong andencouraging set of

figures; a set of figures, incidentally,that is around £1.6 billion up on thesame month last year. Thiscontribution also keeps the rolling yearfigures nicely on track and just over the£46 billion mark.

It was notable once again that all of thecompanies in the BCLive Top 10 eachsecured more than £100 million ofwork again this month. It is similarlypleasing to note that Keepmoat madethe list again for the first time in a while,and that McAleer & Rushe Groupachieved a creditable 8th place.

Top of the pile, however, was Skanskawhich boasted a haul of just over£257 million including a £165 millioncontract to design, build, finance andoperate a new biomedical campus atPapworth Hospital in Cambridgeshire.

Laing O’Rourke maintained itsseemingly permanent place in theBCLive top tier courtesy of a £150million refurbishment and repairframework contract across sevenYorkshire schools for the EducationFunding Agency.

A £100 million housing refurbishmentand repair contract for NottinghamCommunity Housing Associationpropelled Keepmoat into fourth place,while Redrow Homes laid claim to sixthspot thanks largely to a £115 millionnew build housing contract inColchester.

In a month that saw Morgan Sindallmanaging director Graham Shennandepart the company, it is interesting tonote that, once again, the groupalong with Kier Group top the list ofcompanies with the most contractssecured with hauls of 20 & 21respectively for a combined values of

£127.7 & £160.4 million.

From a regional perspective,Yorkshire contributed morethan £300 million worth ofwork with East Anglia andthe South West followingclose behind with £277 and£267 million respectively.But – and it goes largelywithout saying – GreaterLondon once again made thegreatest contribution with£726 million across morethan 130 contracts.

Still On TrackThe BCLive league table might have

taken a seasonal dip in October, but the

long-awaited recovery remains very much

on track according to The Builders’

Conference chief executive Neil Edwards.

Commentary From Neil EdwardsChief Executive - The Builders' Conference Trade Association

Lack of FM

Almost £1 BillionConducted by the Royal Institutionof Chartered Surveyors (RICS), theresearch found that around 26percent of organisations in the UKare still not taking a strategicapproach when it comes to FM – abusiness discipline that involves theco-ordination of space, people,resources and property within anorganisation. It suggests that thoseorganisations using FM in astrategic capacity could be savingthemselves as much as £120,000on average.

As a result of its findings, the RICSsuggests that a reluctance to investin, and embed a dedicated FMprogramme within an organisation –an approach it calls ‘Strategic FM’(SFM) – means that many businessesand public sector organisationscould be missing out on huge costsaving opportunities.

The research conducted with 707small, medium and largeorganisations from across the public(203) and private sectors (504), alsoshows the positive impact SFM hason those organisations that alreadyadopt the approach. Half of thoseinterviewed who use SFM said that ithas saved their organisation money– with many of those in the privatesector reporting the positive impact ithas had on their profitability (39percent) and turnover (48 percent).

What’s more, of those questionedwho use SFM, three in five (59

Research suggests that UK businesses

could be losing out on savings of nearly

£1 billion, as a result of their failure to

adopt a more effective approach to

facilities management (FM).

RICS research highlights the business

cost of ineffective facilities management

Could Cost UK

percent) said that theirorganisation had seen anincrease in overallproductivity, with 49percent saying that theattractiveness of theirorganisation to clients orcustomers had beenboosted by it. In addition,around a fifth (21 percent)said that employeeabsence in theirorganisation haddecreased as a result of SFM.

Of those questioned specifically inthe Government sector, the tangiblebenefits of a more strategic approachto FM were even higher with 70percent of those respondents that useSFM saying that they had seen anoverall increase in productivity, witha further 71 percent stating that theyhad also seen an increase inemployee engagement.

“It’s clear from our research thatrecognising FM as a strategicdiscipline has the ability to bringabout tangible business benefits fororganisations of all shapes, sizesand sectors. With nearly £1 billionbeing wasted by thoseorganisations without SFM in place,our research clearly demonstratesthat more needs to be done to getleaders in the private and publicsectors on board with the newapproach. By recognising FM as animportant strategic discipline,businesses could reap the hugebusiness benefits it promotes,” says

Johnny Dunford, GlobalCommercial PropertyDirector at RICS.

“To supportprofessionals indeveloping SFM in theirown organisation, RICShas developed avaluable suite ofinformation, resourcesand services whichincludes our recently

launched SFM Guidance bookletand accompanying CaseStudies booklet. What’s more,the RICS is helping toprofessionalise the FM sectorthrough its Chartered FacilitiesManagement Surveyor(MRICS) and Associate(AssocRICS) qualifications.”

To accompany their findingsand to support professionalsin implementing SFM intheir own organisation, theRICS has developed aseries of top tips:

• Ensure that you arefully aware of yourorganisation’s overallmission statement andbusiness objectives witha view to developing anSFM approach thatsupports in theirdelivery.

• Put measures in placeto capture accurate data

which will enhance strategicdecision making when it comes toFM – data on operating costs, repaircosts, utilisation levels andenvironmental performance are key.

• Ensure that FM is represented at astrategic level when organisationalpolicies and frameworks are beingdeveloped – this will ensure that theright facilities can be provided in theright locations at the right cost andquality, supporting organisations inmeeting key objectives.

• Use internal communicationsnetworks to get a view of theoperational requirements of yourorganisation and build relationshipswith key operational managers whocan help you deliver an effective FMstrategy.

• Access the abundance of resources,information and qualifications that areout there – all geared towards theprofessionalising of FM andenhancing of its vital importance as

a strategic discipline.

With nearly £1 billion being

wasted by those organisations

without SFM in place, our research

clearly demonstrates that more

needs to be done

Johnny Dunford, GlobalProperty Director at RICS

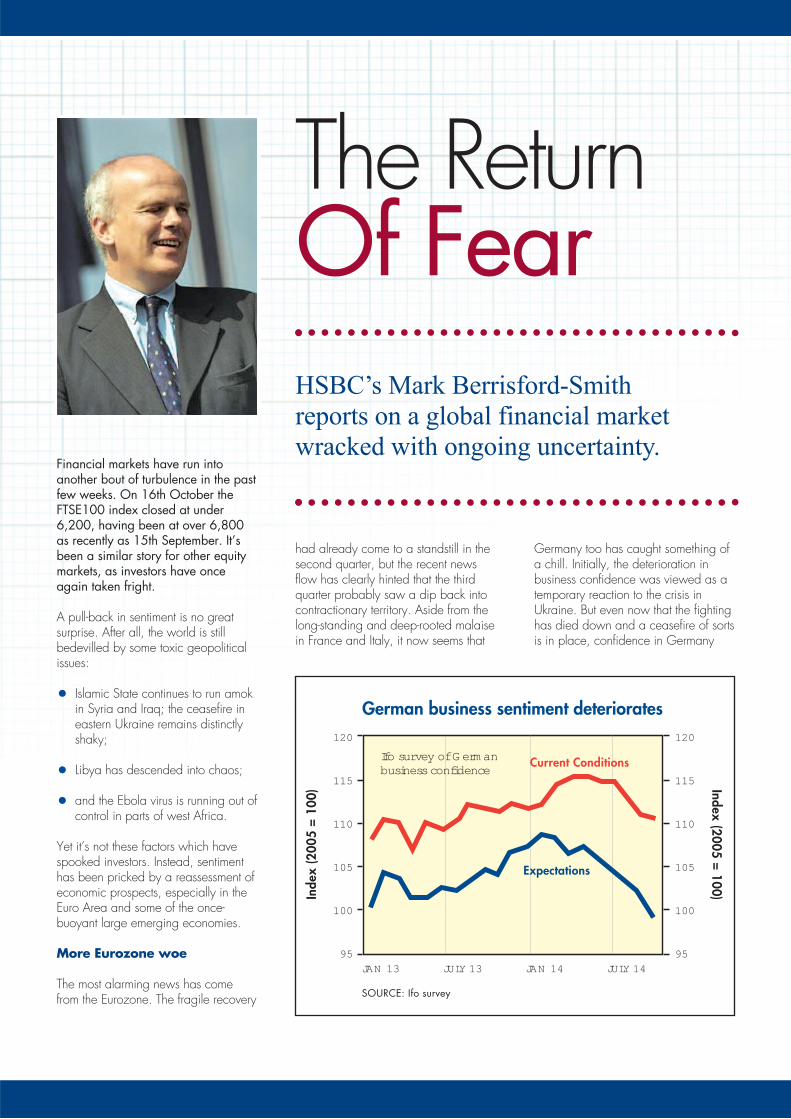

The ReturnOf Fear

Financial markets have run intoanother bout of turbulence in the pastfew weeks. On 16th October theFTSE100 index closed at under6,200, having been at over 6,800as recently as 15th September. It’sbeen a similar story for other equitymarkets, as investors have onceagain taken fright.

A pull-back in sentiment is no greatsurprise. After all, the world is stillbedevilled by some toxic geopoliticalissues:

• Islamic State continues to run amokin Syria and Iraq; the ceasefire ineastern Ukraine remains distinctlyshaky;

• Libya has descended into chaos;

• and the Ebola virus is running out ofcontrol in parts of west Africa.

Yet it’s not these factors which havespooked investors. Instead, sentimenthas been pricked by a reassessment ofeconomic prospects, especially in theEuro Area and some of the once-buoyant large emerging economies.

More Eurozone woe

The most alarming news has comefrom the Eurozone. The fragile recovery

had already come to a standstill in thesecond quarter, but the recent newsflow has clearly hinted that the thirdquarter probably saw a dip back intocontractionary territory. Aside from thelong-standing and deep-rooted malaisein France and Italy, it now seems that

Germany too has caught something ofa chill. Initially, the deterioration inbusiness confidence was viewed as atemporary reaction to the crisis inUkraine. But even now that the fightinghas died down and a ceasefire of sortsis in place, confidence in Germany

HSBC’s Mark Berrisford-Smith

reports on a global financial market

wracked with ongoing uncertainty.

German business sentiment deteriorates

SOURCE: Ifo survey

JAN 13 JULY 13 JAN 14 JULY 14

120

115

110

105

100

95

120

115

110

105

100

95

Inde

x (2

005

= 10

0)

Expectations

Index (2005 = 100)

Current ConditionsIfo survey of G erm anbusiness confidence

has continued to wilt. In particular,there were some dreadful datareleases from the industrial sector inAugust, which showed sharp falls inindustrial orders, manufacturingproduction, and merchandise exports.These might be partly explained bychanges to the timings of schoolholidays and factory shutdowns, butthere is a widely-held suspicion thatsomething more sinister is going on.

Some of the Eurozone’s once-strickenperipheral economies are now doingmuch better, with Spain responsiblefor half of the Eurozone’s (admittedlypaltry) job creation in the past year.But these countries can’t pull the trainon their own, and investors and othersfret that the policy response, whetherfrom the EU or the ECB, or fromnational governments, won’t add upto very much.

With the annual rate of consumer priceinflation in the Eurozone having drifteddown to just 0.3%, the ECB is clearlykeen to ward off the pernicious threat ofdeflation. Interest rates have been cuttwice in recent months, but with the refirate now at just five basis points, there isno more conventional ammunition left.That leaves only the various forms ofcredit easing and quantitative easing,where the experience of other centralbanks suggests that the economicbenefits are modest rather than dramatic.The ECB is finally embarking on aprogramme of asset purchases, but isnot yet ready to launch outrightquantitative easing by buyinggovernment bonds in the secondarymarkets. Instead, it hopes to use acombination of Targeted Long-TermRefinancing Operations, and purchasesof covered bonds and asset backedsecurities, to restore its balance sheet tothe size it was back in early 2012, atthe height of the debt crisis. It appearsthat most of the ECB’s GoverningCouncil, especially those from Germany,would sooner endure root canaltreatment rather than indulge in whatcritics often term ‘debt monetisation’. Yetthey may eventually have no choice,and HSBC still expects a programme ofgovernment bond purchases to beunveiled some time in 2015.

Sticking to the fiscal rules

The prospect that the Eurozone mightfall into a triple-dip recession has stirredsome of the demons from the debtcrisis. Peripheral bond yields haveagain spiked, especially in the case ofGreece, while the results of the ECB’sAsset Quality Reviews and stress testsof the Eurozone’s major banks, due tobe published at lunchtime this comingSunday, will be awaited withtrepidation.

Meanwhile, the European Commissionhas the unenviable task of deciding

whether to reject some of the draftnational budgets for 2015. France willprove to be something of a test casefor the new Fiscal Compact. The EUhad already granted an extension to2015 for the French government to cutits deficit to below the 3% of GDPceiling. But the latest budget proposalsnow envisage that this won’t happenuntil 2017. The Commission will haveto decide whether it is prepared to riskpushing economies back into recessionfor the sake of fiscal probity, orwhether it can sit back while a coachand horses are driven through thenewly-enhanced fiscal framework.

The Commission will have to

decide whether it is prepared to

risk pushing economies back into

recession for the sake of fiscal probity, or

whether it can sit back while a coach and

horses are driven through the

newly-enhanced fiscal framework

A rollercoaster ride for the FTSE 100

SOURCE: Thomson Datastream

JAN 13 JULY 13 JAN 14 JULY 14

7200

7000

6800

6600

6400

6200

6000

5800

7200

7000

6800

6600

6400

6200

6000

5800

FTSE

100

Inde

x

FTSE 100

FTSE 100 Index

For the public at large, the

HS2 project will deliver

faster journey times between

London, Birmingham,

Manchester and Leeds.

For the logistics sector, it

spells the end of restricted

freight capacity.

But to the construction

industry and the equipment

manufacturers that serve

it, HS2 represents the

UK’s largest infrastructure

project this century.

-- So Much MoreHS2

Than Fast

It has been a long while – possiblysince the completion of the core ofthe nation’s motorway network –since the UK construction industrystood on the brink of such a hugeand visible project as HS2. Surewe had the Channel Tunnel but, asis the way with tunnels, it was outof sight and largely out of mindfor all but the conservationists andthe anti-French lobby. And yes,we have witnessed theconstruction of The Shard, TheGherkin, The Walkie Talkie, TheCheese Grater and countless otherhigh profile London skyscraperswith equally ridiculous nicknames.

But in terms of magnitude, these aremere trifles when compared to themammoth undertaking that isscheduled to link London with theMidlands and the North of England,rewriting the nation’s economicgeography and alleviating the strainon an existing West Coast MainLine (WCML) rail service that willsoon have 50 percent more trainpassengers than it has seats.Indeed, the estimates surroundingthe HS2 truly boggle the mind. It isanticipated that the construction ofthe country’s second high speed railnetwork will generate 50,000 jobsper year during its construction. Itwill also support an additional100,000 jobs in and around thestations, and a further 400,000across the Midlands and theNorth (Core Cities Group).

But this will be a bi-productof a construction project ofunimaginable scale. HS2will require the constructionof 350 miles of railway.Requiring a total funding ofaround £42.6 billion, HS2will be built in two phasesand include nine dedicatedHS2 stations. Around 50percent of the line will passthrough cuttings, tunnels,bridges and viaductsincluding around 100 thatwill be built as part of theproject. The project willrequire 55 million m3 ofexcavation; four million m3concrete; 973 kilometres of

rail line; 700,000 m3 of surfacingmaterials and almost a milliontonnes of rebar. At the height ofconstruction activity, the project willbe utilising an unprecedented fleetof more than 500 articulateddumptrucks together with around600 eight-wheel tippers. Andthese haulers won’t load themselves,so excavators will also be in hugedemand.

Of course, in keeping with a projectthat is huge in every sense of theword, the timeline from inception todelivery and line opening is equallylarge and long. Although theproject has rarely been out of the

national headlines since it wasmooted in 2009, Royal Assent forthe project’s first phase is notexpected until 2016, quicklyfollowed by the required enablingworks. Experts anticipate thatconstruction will commence inearnest in 2017 with the lineopening nine years later.

This edition of Hard Data is drawnfrom a presentation given to thelatest CEA Conference by JohnCarroll, Head of Construction andLogistics, Hybrid Bill team, HS2 Ltd.

Around 50 percent of the

line will pass through

cuttings, tunnels, bridges and

viaducts including around 100 that

will be built as part

of the project

The past month has seen renewedturbulence on financial markets,with sharp falls in equity pricesand heightened volatility of majorexchange rates. The geopoliticalfactors which were tending todampen sentiment during thesummer are still active, with IslamicState still running amok across Iraqand Syria, while the ceasefirebetween Ukraine and Russia isshaky at best, and the Ebola virusis causing economic dislocation toWest Africa. Yet it is the outlookfor the global economy and theprospect of imminent rate hikes bythe Federal Reserve which havedone most to unsettle the markets.

Not for the first time, it is theEurozone which has beenresponsible for most of thedownbeat economic news flow ofthe past few months. While datareleased in early August showedthat GDP had stalled in the secondquarter, this was partly ascribed toa loss of confidence on the part ofGerman businesses resulting fromthe fighting in Ukraine. But the

ceasefire agreed in earlySeptember has done little to restoresentiment, while the latest data andsurvey reports suggest that the thirdquarter could have been evenworse than the second quarter.

More Eurozone woe

In particular, there were somedreadful numbers out of Germanyfor August, with a sharp fall inindustrial orders; a fall of nearly 5%in the volume of manufacturingproduction; and a decline of morethan 5% in the value of goodsexported. Changes to the timings ofschool holidays and factoryclosures are partly to blame, withSeptember’s figures likely to showsomething of a bounce-back. But

there is a widely-held suspicion thatAugust’s data pointed to anunderlying deterioration in theEurozone’s largest economy. Thatwould be bad news indeed,especially as numbers 2 and 3 –France and Italy – continue tolanguish on the cusp of recession.Of the ‘big four’ only Spain ismaking meaningful progress,reporting modest growth of 0.5% inthe second quarter, and is also theonly one of the four where the rateof unemployment is falling to ameaningful extent, albeit from avery high level.

So even before the recent dose ofmarket jitters HSBC had cut itsgrowth forecast for the Euro Area,with GDP now expected to expand

Another BumpInThe Road

Financial markets have run into another

bout of turbulence as economic

conditions have deteriorated in the Euro

Area and in some large emerging

economies, particularly Brazil, Russia,

and Turkey. Mark Berrisford-Smith,

Head of Economics, UK Commercial

Banking, HSBC Bank plc, reports.

by only 0.7% this year (previously0.9%), and by just 1% in 2015. Thedire state of the Eurozone economyhas galvanised the ECB into furtheraction. At its policy meeting inSeptember interest rates were cutone last time, taking the refi ratedown to just 0.05%, while aprogramme of asset purchases wasannounced. These purchases,together with the targeted long-termrefinancing operations (TLTROs)which also got underway inSeptember, are aimed at increasingthe size of the ECB’s balance sheetback to where it was, relative toGDP, at the start of 2012. Thisimplies that the ECB aims to achievean expansion of around one trillioneuros. For now, the asset purchasesare confined to covered bonds andasset-backed securities; but, with theannual rate of consumer priceinflation having eased to just 0.3%in September, a move to outrightquantitative easing (QE) involvingpurchases of government bonds inthe secondary markets is still on thecards for 2015.

When will US interest rates rise?

The other factor which hasdisturbed financial markets in recent

weeks is the approaching date ofthe first rate hike in the UnitedStates. Having been gently taperingits programme of asset purchasessince last autumn, the Fed willformally call a halt to QE later thismonth, and although the statementswhich follow each policy meetingstill talk of a ‘considerable’ timebetween the end of QE and the firstincrease in the fed funds rate, it isnow clearly the next decision thatwill be made. Moreover, while the

Eurozone economy is once againflat on its back, the US economycontinues to expand at a decentpace. It’s certainly not a re-run ofthe so-called ‘goldilocks’ years ofthe late 1990s, but jobs continue tobe created at a healthy pace, withmonthly gains in non-farm payrollsaveraging 224,000 during thethird quarter and the unemploymentrate in September falling below 6%for the first time since 2008.

The result of this trans-Atlantic tug ofwar has been a resurgence of thedollar. Nothing like this has beenseen since the dotcom days of thelate 1990s, and HSBC expects thatthe greenback’s strength still hasfurther to run.

Having traded at close toUSD/EUR 1.40 in the spring, therate is now down in the mid 1.20s,with HSBC expecting it to end nextyear at USD/EUR 1.19.

Lower oil prices

Given that geopolitical risks fromIslamic State and theRussia/Ukraine conflict haven’tgone away, it may seem somewhatsurprising that the price of oil hastumbled, rather than climbed. Bylate September Brent crude was

The housing market comes off the boil

SOURCE: Bank of England; RICS Housing Market Survey

2012 2013 2014

75

50

25

0

-25

80

70

60

50

40

House Prices(L Axis)

RICS

Hou

se P

rice

Bal

ance

Mortgage Approvals(R Axis)

Monthly M

ortgage Approvals (000s)

The result of this trans-Atlantic

tug of war has been a resurgence

of the dollar. Nothing like this has been

seen since the dotcom days of the late

1990s, and HSBC expects that the

greenback’s strength

still has further to run

trading at just $88 a barrel, areduction of a fifth since the spring.A number of factors are at playhere, including the dollar’srebound, with a strong greenbackusually being associated with aweakening of commodity prices,many of which are priced indollars. The oil price has also beenundermined by the deterioratingeconomic outlook, especially thedowngrades to forecasts by majorinternational bodies, such as theIMF and the OECD. There is also abattle for market share going onamong the world’s major oilproducers. With the United Statessoon likely to become the world’slargest producer, Saudi Arabia and other producers have beenprepared to drop their prices ratherthan lose share.

Geopolitics plays secondfiddle

If nothing else, the marketturbulence of recent weeks hasdemonstrated that the long-established link between geopoliticsand the price of energy has beenseverely weakened. The OPECcartel now accounts for less thantwo fifths of global output while theshale revolution has put the UnitedStates in a powerful marketposition.

The present bout of market jittersisn’t being stoked up bygeopolitics, but instead by theprospect of the Fed tighteningmonetary policy. Emergingeconomies are especiallyvulnerable to a normalisation ofmonetary conditions in the UnitedStates, with a rising fed funds targetrate threatening to suck liquidityback to America, while thedepreciation of currencies inrelation to the dollar tends to boostdomestic inflation rates on accountof the higher price of manyimported goods. So apart from thedowngrade to the Eurozone, themost notable changes to HSBC’sforecasts compared with theprevious quarter relate to emergingeconomies.

A brighter outlook for India’seconomy

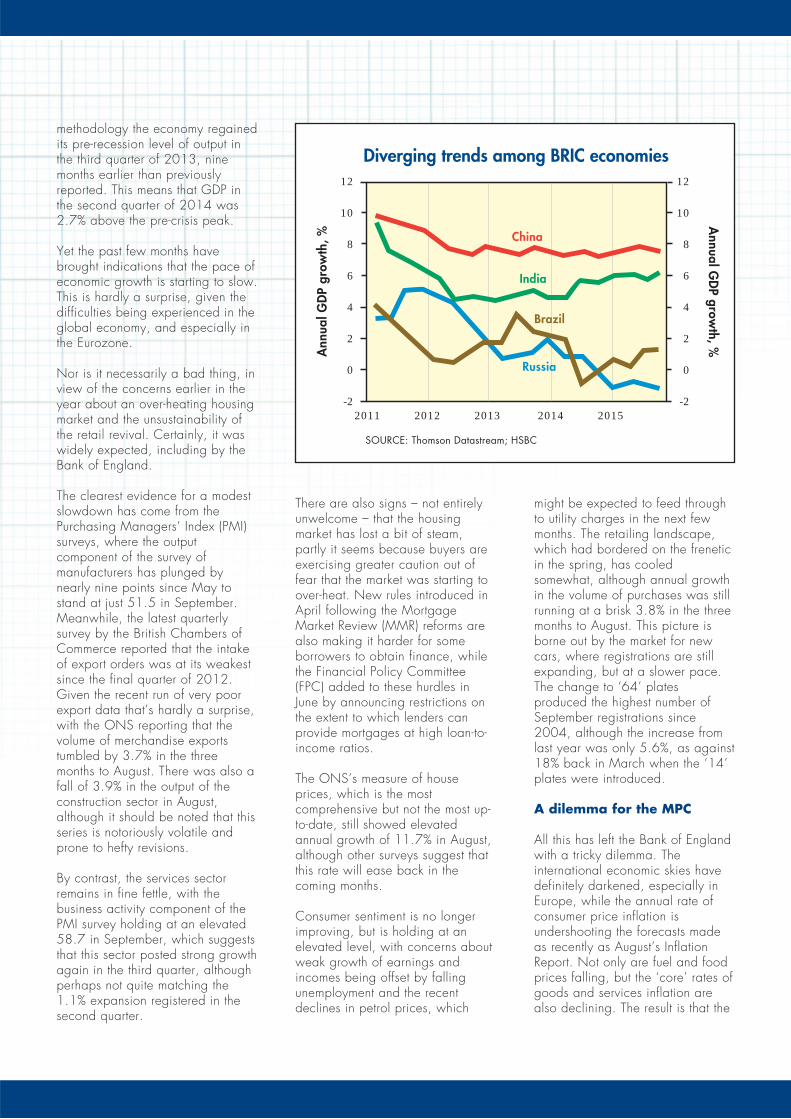

China continues to plough along ata growth rate slightly below theofficial target of 7.5% per annum,although recent statements fromthink-tanks linked to the governmentsuggest that this target rate couldsoon be trimmed.

Meanwhile, the Indian economyappears to have perked up sincethe election of Narendra Mohdi asPrime Minister in May, with matters

being helped by easing domesticinflation, which has brought an endto the tightening of monetary policyby the Reserve Bank of India.India’s growth rate is expected totop 6% in 2015, and could well beonly a touch shy of China’s.

In contrast to the relative resilienceof India and China, several of theother large emerging economiescontinue to struggle, with Brazilhaving slipped into a mildrecession, the Turkish economycontracting in the second quarter,and the Russian economy slowingsharply thanks to a combination oftit-for-tat sanctions, deterioratingbusiness sentiment, and theplunging oil price. HSBC nowexpects that the Russian economywill contract by 1% in 2015, withBrazil achieving only negligiblegrowth. Yet the overall impact onthe group of emerging economies ismodest thanks to the improvingprospects for India.

Britain has enjoyed a solidrecovery

The UK continues to be one of themost buoyant advanced economies,with growth for 2014 as a wholeexpected to come in at slightlyabove 3%. GDP expanded by abrisk 0.9% in the second quarter,with the annual growth rate comingin at 3.2%.

With the national accounts beingheavily rejigged to meet the newEuropean System of Accounts 2010(ESA2010) methodology, therehave been thorough-going revisionsgoing back to the late 1990s.These have had the effect ofsmoothing out the peaks andtroughs of the past decade to amodest degree – in other words,the pre-crisis boom wasn’t quite asbig; the recession not quite assteep; and the revival a littlestronger. Nonetheless, the peak-to-trough decline in GDP was still6.0%, as against the previousfigure of 7.2%. The otherconsequence is that under this new

Brazil having slipped into a mild

recession, the Turkish economy

contracting in the second quarter, and the

Russian economy slowing sharply thanks

to a combination of tit-for-tat sanctions,

deteriorating business sentiment,

and the plunging oil price

methodology the economy regainedits pre-recession level of output inthe third quarter of 2013, ninemonths earlier than previouslyreported. This means that GDP inthe second quarter of 2014 was2.7% above the pre-crisis peak.

Yet the past few months havebrought indications that the pace ofeconomic growth is starting to slow.This is hardly a surprise, given thedifficulties being experienced in theglobal economy, and especially inthe Eurozone.

Nor is it necessarily a bad thing, inview of the concerns earlier in theyear about an over-heating housingmarket and the unsustainability ofthe retail revival. Certainly, it waswidely expected, including by theBank of England.

The clearest evidence for a modestslowdown has come from thePurchasing Managers’ Index (PMI)surveys, where the outputcomponent of the survey ofmanufacturers has plunged bynearly nine points since May tostand at just 51.5 in September.Meanwhile, the latest quarterlysurvey by the British Chambers ofCommerce reported that the intakeof export orders was at its weakestsince the final quarter of 2012.Given the recent run of very poorexport data that’s hardly a surprise,with the ONS reporting that thevolume of merchandise exportstumbled by 3.7% in the threemonths to August. There was also afall of 3.9% in the output of theconstruction sector in August,although it should be noted that thisseries is notoriously volatile andprone to hefty revisions.

By contrast, the services sectorremains in fine fettle, with thebusiness activity component of thePMI survey holding at an elevated58.7 in September, which suggeststhat this sector posted strong growthagain in the third quarter, althoughperhaps not quite matching the1.1% expansion registered in thesecond quarter.

There are also signs – not entirelyunwelcome – that the housingmarket has lost a bit of steam,partly it seems because buyers areexercising greater caution out offear that the market was starting toover-heat. New rules introduced inApril following the MortgageMarket Review (MMR) reforms arealso making it harder for someborrowers to obtain finance, whilethe Financial Policy Committee(FPC) added to these hurdles inJune by announcing restrictions onthe extent to which lenders canprovide mortgages at high loan-to-income ratios.

The ONS’s measure of houseprices, which is the mostcomprehensive but not the most up-to-date, still showed elevatedannual growth of 11.7% in August,although other surveys suggest thatthis rate will ease back in thecoming months.

Consumer sentiment is no longerimproving, but is holding at anelevated level, with concerns aboutweak growth of earnings andincomes being offset by fallingunemployment and the recentdeclines in petrol prices, which

might be expected to feed throughto utility charges in the next fewmonths. The retailing landscape,which had bordered on the freneticin the spring, has cooledsomewhat, although annual growthin the volume of purchases was stillrunning at a brisk 3.8% in the threemonths to August. This picture isborne out by the market for newcars, where registrations are stillexpanding, but at a slower pace.The change to ‘64’ platesproduced the highest number ofSeptember registrations since2004, although the increase fromlast year was only 5.6%, as against18% back in March when the ‘14’plates were introduced.

A dilemma for the MPC

All this has left the Bank of Englandwith a tricky dilemma. Theinternational economic skies havedefinitely darkened, especially inEurope, while the annual rate ofconsumer price inflation isundershooting the forecasts madeas recently as August’s InflationReport. Not only are fuel and foodprices falling, but the ‘core’ rates ofgoods and services inflation arealso declining. The result is that the

Diverging trends among BRIC economies

SOURCE: Thomson Datastream; HSBC

2011 2012 2013 2014 2015

12

10

8

6

4

2

0

-2

12

10

8

6

4

2

0

-2

Ann

ual G

DP

grow

th, %

Annual G

DP grow

th, %

China

India

Brazil

Russia

annual rate of CPI inflation came inat a five-year low of just 1.2% inSeptember, 0.8 percentage pointsshort of the official target. But whilethese developments might pointtowards the MPC staying its handin starting to raise Bank Rate,falling unemployment still points toan economy that might soon haveused up all its spare capacity. Onlya year ago, the Bank of England’sfirst attempt at forward guidancestated that interest rates wouldn’t beraised until the unemployment ratehad declined to 7%.

Now that it’s come down to 6.0%,and still falling, it is getting harderfor the Committee to keep sitting onits hands without losing credibility.So even assuming that employmentincreases in the months ahead at aless blistering pace than in the pastyear or so, HSBC still expects thatthe first increase in Bank Rate willbe announced in February 2015.

Things may become a bit clearerwhen the November InflationReport is published, which willhave to deal with the significantundershoot of inflation against theBank’s own expectations.

The pound comes underpressure

Sterling has settled down after theroller-coaster ride in the run-up tothe Scottish independencereferendum, but is now trading atjust above USD/GBP1.60, having spent the first half of thisyear trading at closer toUSD/GBP1.70. So while Britishfirms selling to the United Statesand the other countries whosecurrencies are linked to the dollarmay enjoy some competitiverespite, those exporting to theEurozone have seen the exchange rate move a little furtheragainst them.

While the element of political riskarising from the Scottish referendumhas now abated, it hasn’taltogether gone away, withlingering concerns about futureconstitutional changes, and theprospect of a referendum on EUmembership in 2017, dependingon the outcome of next May’sgeneral election. Moreover, the UKis no longer consistentlyoutperforming market expectations,as it did during 2013 and the firsthalf of this year.

There is also the long-standingconcern about the size of thecurrent account deficit and freshworries about the stubbornness ofthe government’s budget shortfall.Taken together with the dollar’sgeneral resurgence, these factorspoint to sterling shedding a littlemore of its value, with HSBC nowexpecting a decline to USD/GBP1.55 by the end of 2015.

UCATT

• 2 in 5 construction apprentices arepaid below the minimum wage

• The number of young workers onzero hours contract is soaring

• Young people have beenadversely affected by Governmentcuts which have fallen oneducational maintenanceallowance (EMA) and also careersAdvice Services such asConnexions. Welfare benefit cutshave also affected people underthe age of 25 and university tuitionfees have been raised.

• Young people are targeted bylegal loan sharks to take out highinterest loans and then get trappedin debt.

UCATT officials frequently assistapprentices and young workers whohave been exploited or mistreated inthe workplace.

Recent examples include an apprenticein the North West who was laid off for7 weeks from their workplace andrisked losing their college placement ashe couldn’t complete part of his course.Once UCATT became involved theylearned that the reason the apprenticehad been laid off was because theyhad turned 18 and the employer wasobliged to pay £40 a day rather than£20 a day. UCATT was able to findthe apprentice a new employer.

In the Birmingham area UCATTassisted apprentices being paid belowthe minimum wage who were

employed by a social housing repairsorganisation. UCATT secured a payrise for the workers in that area and forall apprentices working for thecompany nationally.

Steve Murphy,General Secretaryof UCATT, said:“Too oftenapprentices aremistreated andexploited in

construction. Employers often thinkapprentices are cheap short-termlabour, rather than a long-termasset. It is essential that youngconstruction workers join UCATT asthis is the best way to protectthemselves.”

All UCATT regions will be taking partand organising events to informapprentices of their rights throughoutNovember.

HighlightsApprentice ExploitationConstruction union UCATT will be

highlighting the exploitation and

mistreatment of apprentices and young

workers throughout November, which

the TUC have designated as young

workers month.

Examples of particular concern include:

with Feminine SideOut Of Touch

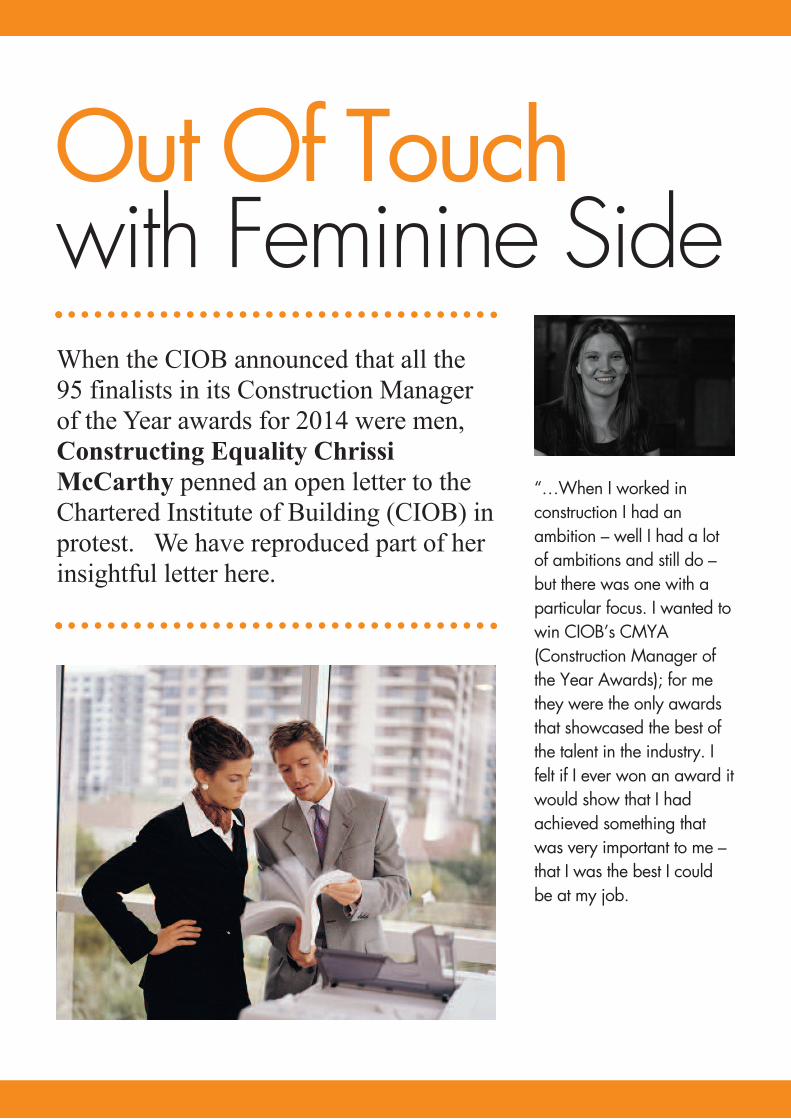

When the CIOB announced that all the

95 finalists in its Construction Manager

of the Year awards for 2014 were men,

Constructing Equality Chrissi

McCarthy penned an open letter to the

Chartered Institute of Building (CIOB) in

protest. We have reproduced part of her

insightful letter here.

“…When I worked inconstruction I had anambition – well I had a lotof ambitions and still do –but there was one with aparticular focus. I wanted towin CIOB’s CMYA(Construction Manager ofthe Year Awards); for methey were the only awardsthat showcased the best ofthe talent in the industry. Ifelt if I ever won an award itwould show that I hadachieved something thatwas very important to me –that I was the best I couldbe at my job.

The awards played another part in mycareer – when I decided to leave sitemanagement as a profession to focuson how to change the sector to makeit better for the people within it, I didone last thing before I closed the doorjust to check I wasn’t making a terriblemistake – one last thing before I leftbehind a career that had been animportant part of my identity for about15 years.

I looked up. I looked at CEOs,industry presidents and, of courseprobably most importantly, the CMYAfinalists. I looked up to see if therewere any women there – to see ifwomen could make it if we only triedhard enough.

What I saw confirmed my worst fears– women were not present at the topof the industry.

This was back in 2007, and thingshave changed – my ambition is nowto gain a PhD, help the industryimprove and grow a successfulbusiness. RICS, RIBA, CIOB, ICE andIStructE have all had their first femalepresidents, Laing O’Rourke and Mitieboth have female CEOs and CITBappointed its first female boardmember.

Some things have changed for theworse – the number of women in theindustry has fallen from 13 percentdown to 11 percent and the CMYA2014 had no female nominations outof 95 finalists – and nowhere on thewebsite does it even raise the issue.

So why does this matter?

Women in construction aren’t daft.

In fact, on average women in thesector are bright and ambitious. That’susually because we haven’t ‘fallen’into the industry, rather we haveworked hard to work to find our placehere (if you fell in, had an easy timeand are a woman; good for you andlong may it continue). But the problemis that our industry asks a lot of sitemanagers – a hell of a lot more thanmost industries – averages of 60-hourweeks, dangerous environments and

not as much respect as we deserve. Ifwe don’t give the bright, ambitiouspeople real opportunities forpromotion and progression they mightstart to think it’s not worth the hassle,no matter how much they love the job.And they might do as I did – check tosee if anyone else made it beforemaking the decision to close the door.

Neither are the men.

Increasingly the men I talk to in theindustry worry about how valued theirsoft skills are. Many tell me that theyfeel they have to “toughen up” theirapproach even where they feel this isdetrimental to the job. As oneremarked to me earlier this month, itsays a lot if women who arerenowned for their soft skills don’teven get a look in – what does thatsay about what we value inconstruction?

Or the young folk.

I don’t need to point out that theindustry has an image problem, orthat a lot of the things associated withthis problem are linked to machostereotypes. What then do we think isthe message we send to our youngentrants about the industry when wesay “this is the best our industry has tooffer” and there is not a single womanin sight?

Or our clients.

It just cannot look good to be one ofthe only industry awards to be so verymale dominated – how do wechange an image that we insist onreinforcing?

But we might all be.

We need to really address theseissues. We can’t keep waiting forthings to improve, because theyhaven’t – not in the last 30 years. Ifwe want improvement we need astrategic plan that understandsgender, wider equalities, theconstruction sector at large and thereal experience of working on site.Anything without this breadth ofknowledge is likely to fall by thewayside.

I’m not saying CIOB are the worstoffenders or that everyone else hastheir house in order, but I am sayingthat due to the project-based nature ofwork in the construction industry, themale dominance in CIOB relatedareas and the prevalence of the ‘oldboys club’ style of promotion andrecognition there is currently a genderbias towards men in industry andCIOB needs to take responsibility forthe part it plays in this.

It isn’t just that there were no femalefinalists in the CMYA 2014, therewere no female nominations – notone. Whilst our membership ofwomen maybe small at 3.41 percent it still should have beenrepresentative – we should have seen3.5 women if the system was fair.Even if you only went off of the datafor fellows alone, there should havebeen 1.7 percent representation fromwomen within the nominees.

This is not happening. I believe it isincumbent upon the CIOB toreconsider its practices…”

To read Chrissi McCarthy’s openletter in full, please visit:http://tinyurl.com/kqo37ph

What I saw

confirmed my worst

fears – women were

not present at the

top of the

industry

Umbrella

Construction union

UCATT’s new report

The Umbrella

Company Con-Trick

won strong support

from MPs when it

was launched in

Parliament

The report’s author Jamie Elliott described how umbrellacompanies operate. He focussed on how a worker agrees arate with an agency but that money is paid to the umbrellacompany and not the worker. He said in effect the umbrellacompany: “can do what they like with the money”. They takea cut (£20-£30 a week) for their costs, charge the worker bothemployers’ and employees’ national insurance contributions,only pay the worker the minimum wage, roll-up holiday pay inthe rate and then re-boost wages through dubious expenses.

Emma Lewell-Buck Labour MP for South Shields, describedhow she had met with constituents who were being paid viaumbrella companies and were losing out sustainably. Theworkers were given no option of being paid in any otherway, “If they didn’t sign then there was no work for them.”

Ms Lewell-Buck had also been pursuing the Treasury to find out what actionthey were taking against umbrella companies. “Best I have heard is that theHMRC are working on improving guidance. All this means is that the workerswill know how they are being conned.”

Steve Murphy, General Secretary of UCATT, said of umbrellacompanies: “They are unscrupulous sharks who are using theconstruction industry to make as much money as quickly aspossible to the detriment of construction workers.”

Shabana Mahmood MP, the Shadow ExchequerSecretary, said that Labour was committed to introducingdeeming into construction. This would mean that workerswould be considered employees unless they met strict criteria to prove they were self-employed. She also said thatLabour was committed to cracking down on the use of

expenses by umbrella companies, which would make suchschemes less attractive.

Company Report

UCATT Unveils

If you wish to advertise in this magazine please contact Neil Edwards on 020 8770 0111

Designed by www.delaneygoss.co.uk Edited by Mark Anthony Publicity Powered online by Switch2IT Distributed by – Eljays44 Ltd

The information on BCLive league table comesdirectly from The Builders’ Conference tradeassociation and can also be found on the front pageof their website www.buildersconference.co.uk

BCLive league table is merely a top level display ofwhich companies have won which contracts andtheir relative values during October 2014 howeverif you go to the website www.bclive.co.uk and clickon an individual business you can quickly viewwhat contracts combine to make the total, whichmarket sectors the contracts were won in and theirgeographical location.

The Builders’ Conference trade association makesevery effort to ensure BCLive league table for maincontractors is a fair representation of the industryhowever if your company has secured a project orprojects and you believe they have not made thetable then please telephone 020 8770 0111 or goto www.buildersconference.co.uk press on the tableand in the top left hand of the screen you will finda button where you will be directed to complete avery simple form which is automatically forwardedto this office upon submission.

Our address book has your name as a contact andtherefore we would be grateful if you could forwardthis e-mail within your company to persons, whomay also find this information of interest and value.

Please do not hesitate in contacting this officeshould you have any queries or require greater in-depth analysis of the construction industry,alternatively if you do not wish to receive this digitalinformation please send an email [email protected]

![Professional Entomology - Extension Entomologyexpensive in dollars, in destruction of animal life, and in . controversial content [Graham 1970].) assailed unfairly on . loss of public](https://static.documents.pub/doc/80x56/5f2ddf9737d48d6e5d4fa50f/professional-entomology-extension-entomology-expensive-in-dollars-in-destruction.jpg)