24

Consumer Confidence Survey GB Q4, 2010 Survey field dates 10 th November to 1 st December 2010

Consumer Confidence Survey GB Q4, 2010

Survey field dates 10th November to 1st December 2010

2

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

Topline Summary Nielsen/BRC Consumer Confidence Survey December 2010

• Consumer Confidence ended 2010 lower than at the start, Q4 did however see a marginal improvement on Q3.

• Latest quarters, Consumer Confidence saw a slight improvement as consumers felt slightly more positive about their job prospects and their personal finances. Les negativity around willingness to spend likely to be a seasonal fluctuation.

• Top 6 GB concerns all impact household income.

• The proportion of consumers who have ‘no spare cash’ has increased from 26% in Q3 to 27% in Q4. This is at an all time high.

• Putting spare cash into savings or paying off debts is higher up shoppers agendas than spending on discretionary items.

• With rising food costs and falling disposable incomes, switching to cheaper grocery brands is an established strategy for staying within budget.

3

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

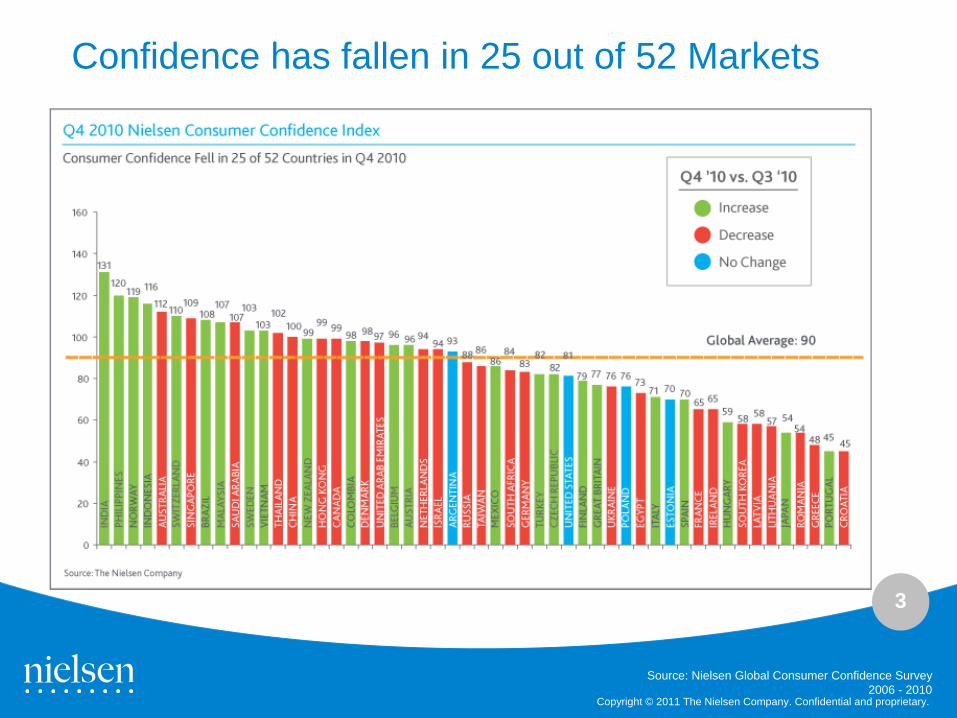

Confidence has fallen in 25 out of 52 Markets

Source: Nielsen Global Consumer Confidence Survey 2006 - 2010

4

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

Global Consumer Confidence remained unchanged from Q3 at 90, but finished the year 2 index points lower than the start. GB Consumer Confidence improved on

Q3 but also ended the year lower than the start.

94

8491 94

7974

6572 75 77

80 7875 77

8479 80

70

61 60 6067 67 68

6367 65

106100

83 82 80 8084 85

81

9090

77

8286 87

92 9399

889797

8182

108

87

40

60

80

100

120

Q3, 06 Q1, 07 Q3, 07 Q1, 08 Q3, 08 Q1, 09 Q2, 09 Q3, 09 Q4, 09 Q1, 10 Q2, 10 Q3, 10 Q4, 10

Global* Average GB France USA

GB Consumer Confidence Index versus Global Average, Neighbouring Countries & USA

Source: Nielsen Global Consumer Confidence Survey 2006 - 2010

*June/December global index based on sub-set of 28/9 countries

5

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

58

84 8589

58

8286 87

56

8479

88

57

82 84 86

Global Average GB France USA

Q1, 2010 Q2, 2010 Q3, 2010 Q4, 2010

“Do you think your country is in an economic recession at the moment?”

% answered “yes”

The proportion of global population believing we are in recession remains polarised, as the Asia Pacific economies are booming and Europe continues to be

hit by escalating concerns over debt.

Source: Nielsen – Global Consumer Confidence Survey 2008 - 2010 - GB results

Optimism continues to be driven by Asia Pacific where the economies of China, Australia, Hong Kong, Singapore are all in growth, whilst Europe continues to struggle especially those close to bankruptcy collectively known as PIIGS*.

*PIIGS Portugal, Ireland, Italy, Greece, Spain

Great Britain

Consumer Confidence Q4, 2010

7

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

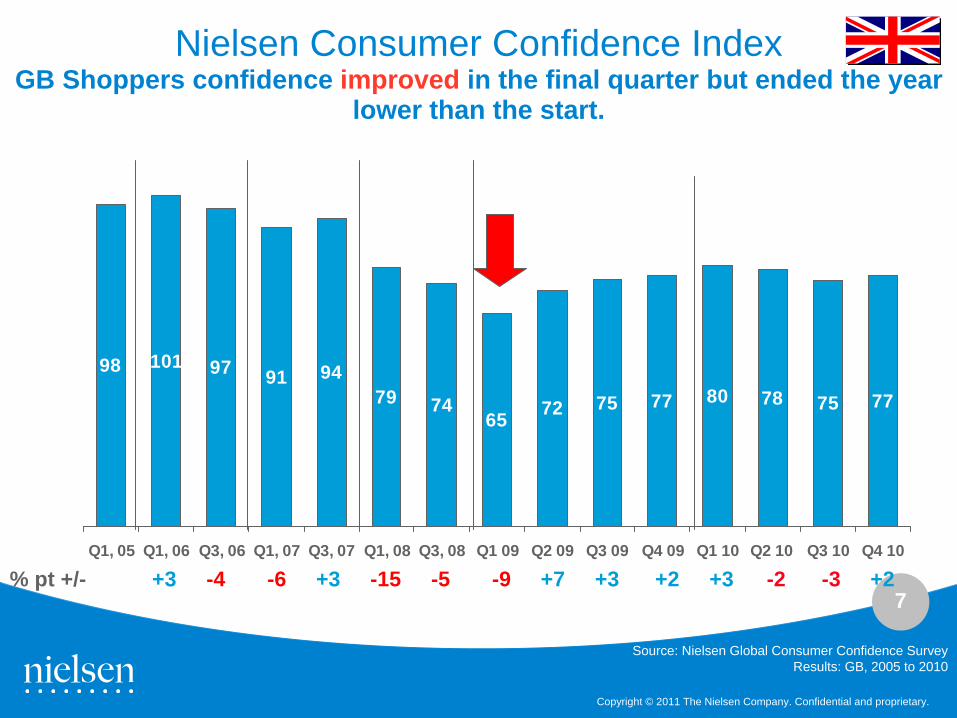

Nielsen Consumer Confidence Index GB Shoppers confidence improved in the final quarter but ended the year

lower than the start.

Source: Nielsen Global Consumer Confidence SurveyResults: GB, 2005 to 2010

98 101 97 91 9479 74

65 72 75 77 80 78 75 77

Q1, 05 Q1, 06 Q3, 06 Q1, 07 Q3, 07 Q1, 08 Q3, 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10

% pt +/- +3 -4 -6 +3 -15 -5 -9 +7 +3 +2 +3 -2 -3 +2

8

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

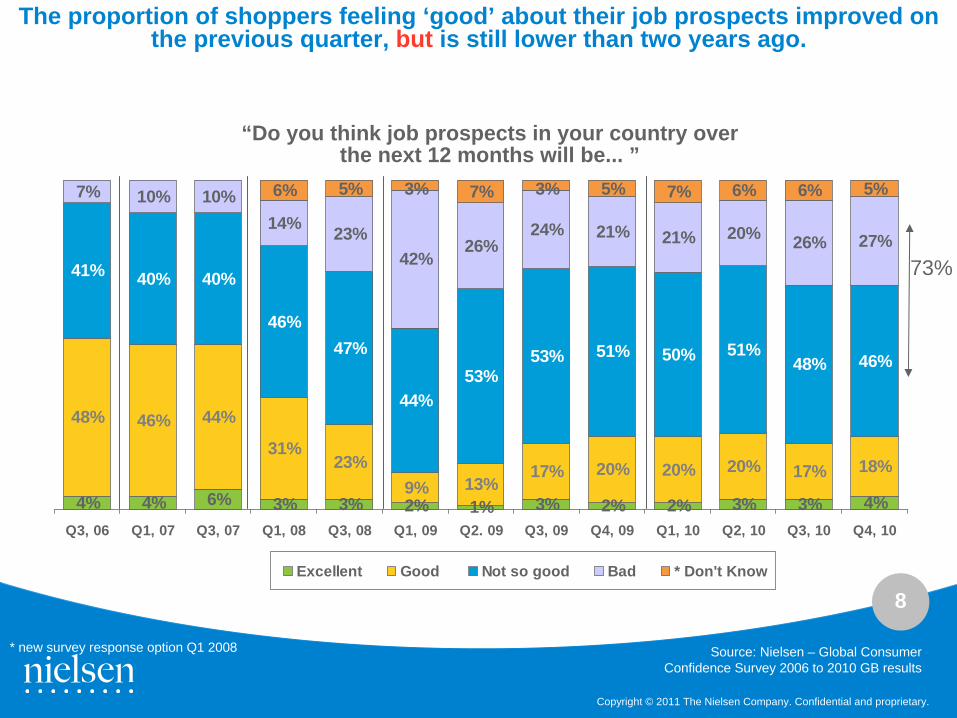

4% 4% 6% 3% 3% 2% 1% 3% 2% 2% 3% 3% 4%

48% 46% 44%

31%23%

9% 13%17% 20% 20% 20% 17% 18%

41% 40% 40%

46%47%

44%53%

53% 51% 50% 51%48% 46%

7% 10% 10%14% 23%

42%26%

24% 21% 21% 20% 26% 27%

6% 5% 3% 7% 3% 5% 7% 6% 6% 5%

Q3, 06 Q1, 07 Q3, 07 Q1, 08 Q3, 08 Q1, 09 Q2. 09 Q3, 09 Q4, 09 Q1, 10 Q2, 10 Q3, 10 Q4, 10

Excellent Good Not so good Bad * Don't Know

“Do you think job prospects in your country over the next 12 months will be... ”

Source: Nielsen – Global Consumer Confidence Survey 2006 to 2010 GB results

* new survey response option Q1 2008

The proportion of shoppers feeling ‘good’ about their job prospects improved on the previous quarter, but is still lower than two years ago.

73%

9

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

4% 4% 5% 2% 1% 1% 2% 3% 3% 2% 2% 4% 3%

47% 46% 49%37% 34% 28% 32% 33% 36% 39% 39% 30% 32%

41% 37% 38%

44% 46%49%

49% 46% 42% 45% 42%48% 47%

7% 12% 8%13% 14% 17% 12% 12% 14% 9% 12% 13% 13%

4% 4% 4% 6% 5% 5% 5% 5% 5% 5%

Q3, 06 Q1, 07 Q3, 07 Q1, 08 Q3, 08 Q1, 09 Q2. 09 Q3, 09 Q4, 09 Q1, 10 Q2, 10 Q3, 10 Q4, 10

Excellent Good Not so good Bad * Don't Know

“Do you think the state of your own personal finances over the next 12 months will be..”

* new survey response option H1 2008

Compared to the start of 2010, the proportion of shoppers feeling good about their personal finances has fallen from 41% to 35%, as income has not kept pace with rising household

costs, there was however a slight improvement on the previous quarter.

Source: Nielsen – Global Consumer Confidence Survey 2006 to 2010 - GB results

60%

10

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

3% 2% 3% 2% 1% 3% 2% 2% 3% 3% 1% 3% 3%

41% 36% 36%23% 27% 26% 27% 31% 30% 31% 30% 29% 29%

46%47% 46%

51% 46% 47% 49% 41% 45% 48%46% 42% 48%

10% 15% 15%22% 23% 23% 18% 23% 19% 16% 19% 22% 16%

2% 2% 1% 3% 3% 4% 2% 4% 4% 4%

Q3, 06 Q1, 07 Q3, 07 Q1, 08 Q3, 08 Q1, 09 Q2. 09 Q3, 09 Q4, 09 Q1, 10 Q2, 10 Q3, 10 Q4, 10

Excellent Good Not so good Bad * Dont' Know

“Considering the cost of things today and your own personal finances, would you say at this moment the time to buy the things you want and need is...”

* new survey response option H1 2008

GB has ended Q4 as it started, with a third of the population able and willing to spend discretionary income but two thirds are reluctant over spending

Source: Nielsen – Global Consumer Confidence Survey 2006 to 2010 - GB results

64%

11

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

11%

12%

12%

10%

10%

5%

6%

5%

5%

2%

5%

4%

2%

14%

13%

12%

12%

7%

6%

6%

5%

5%

4%

2%

2%

2%

Increasing utility bills

The economy

Debt

Job security

Increasing food prices

Increasing fuel prices

Health

Immigration

Work/life balance

Terrorism

Childrens' education and/or welfare

Crime

Parents' welfare and happiness

Q3, 10

Q4, 10

“What is your biggest concern over the next 6 months?”

Top 6 GB concerns all impact household income and 4 of these have increased since October ..

Source: Nielsen – Global Consumer Confidence Survey Q3 2010 - GB results

12

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

14%

13%

7%

12%

12%

6%

6%

5%

5%

4%

2%

2%

2%

13%

13%

13%

7%

6%

7%

6%

5%

4%

5%

5%

4%

3%

27%

26%

20%

19%

18%

13%

12%

10%

9%

9%

7%

6%

5%

Increasing utility bills

The economy

Increasing food prices

Job security

Debt

Increasing fuel prices

Health

Immigration

Work/life balance

Terrorism

Childrens' education and/or welfare

Crime

Parents' welfare and happiness

Main ConcernSecondary Concern

“What are your biggest concerns over the next 6 months?”

Increasing utility bills has become the number 1 concern, overtaking the economy. Increasing fuel prices have not gone unnoticed.

Source: Nielsen – Global Consumer Confidence Survey Q3 2010 - GB results

vs Q3, 10

==

=

=

13

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

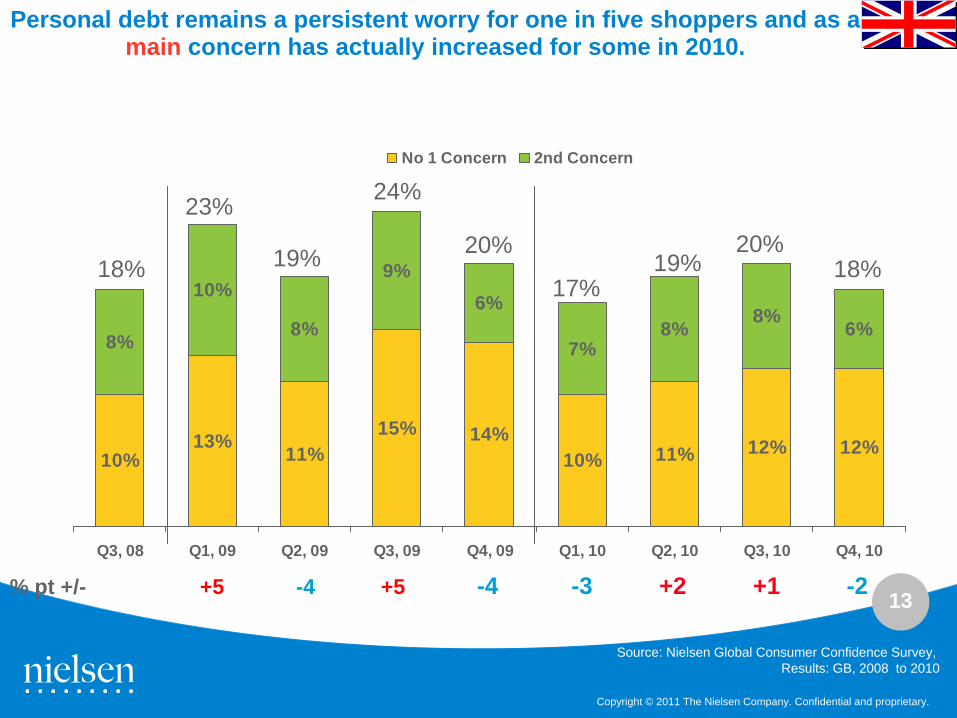

Personal debt remains a persistent worry for one in five shoppers and as a main concern has actually increased for some in 2010.

Source: Nielsen Global Consumer Confidence Survey, Results: GB, 2008 to 2010

10%13% 11%

15% 14%10% 11% 12% 12%

8%

10%

8%

9%6%

7%8% 8% 6%

Q3, 08 Q1, 09 Q2, 09 Q3, 09 Q4, 09 Q1, 10 Q2, 10 Q3, 10 Q4, 10

No 1 Concern 2nd Concern

% pt +/- +5 -4 +5 -4 -3 +2 +1 -2

18%

23%

19%

24%

20%

17%19%

20%18%

14

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

4 out of 5 shoppers still believe GB to be in economic recession and a diminishing proportion expect to be out of it in the next 12 months

94 9584 82 84 82

27 2429

17 2014

Q3, 09 Q4, 09 Q1, 10 Q2, 10 Q3, 10 Q4, 10

Do you think your country is in an economic recession at the moment? (Yes)

Do you think your country will be out ofeconomic recession in the next 12 months? (Yes)

of those who think we are in a recession

Source: Nielsen – Global Consumer Confidence Survey 2009 - 2010 - GB results

15

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

28%24%31%27%26%30%30%29%28%27%

58%56%

52%44%50%

51%48%50%48%51%

14%20%17%29%24%19%21%21%24%22%

GB Q4, 10GB Q3, 10GB Q2, 1OGB Q1, 10GB Q4 09GlobalAverageQ4, 10

GlobalAverageQ3, 10

GlobalAverageQ2, 10

GlobalAverageQ1, 10

GlobalAverageQ4, 09

Yes

No

Don'tknow

Source: Nielsen – Global Online Survey 2009-2010Consumer Confidence

“Do you think your country will be out of an economic recession in the next 12 months?”

Proportion of GB shoppers anticipating a double dip recession are increasing .....

16

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

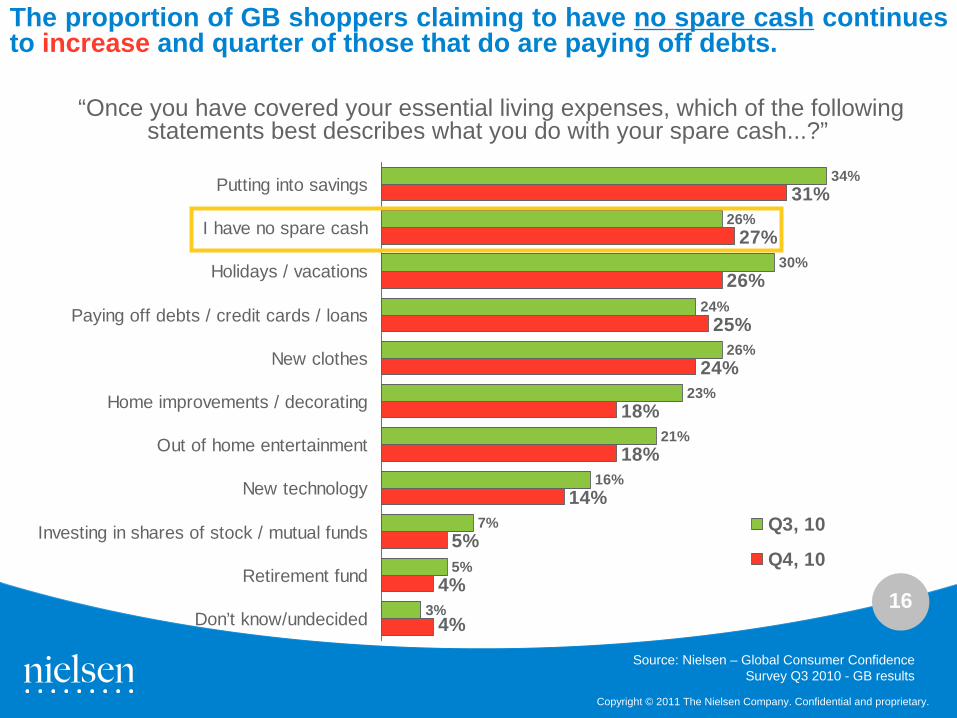

34%

26%

30%

24%

26%

23%

21%

16%

7%

5%

3%

31%

27%

26%

25%

24%

18%

18%

14%

5%

4%

4%

Putting into savings

I have no spare cash

Holidays / vacations

Paying off debts / credit cards / loans

New clothes

Home improvements / decorating

Out of home entertainment

New technology

Investing in shares of stock / mutual funds

Retirement fund

Don’t know/undecided

Q3, 10

Q4, 10

The proportion of GB shoppers claiming to have no spare cash continues to increase and quarter of those that do are paying off debts.

“Once you have covered your essential living expenses, which of the following statements best describes what you do with your spare cash...?”

Source: Nielsen – Global Consumer Confidence Survey Q3 2010 - GB results

17

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

68% of GB shoppers are making savings to stay within budget.

62%

66%

68%

71%

63%

64%

70%

62%

France

USA

GB

Global Average

Q3, 10Q4, 10

“Compared to this time last year, have you changed your spending to save on household expenses?”

% answered “yes”

Source: Nielsen – Global Consumer Confidence Survey Q3 2010 - GB results

18

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

59%

65%

60%

60%

50%

42%

37%

38%

37%

31%

31%

32%

24%

34%

13%

65%

65%

61%

57%

51%

42%

42%

40%

37%

29%

29%

28%

28%

23%

15%

Spend less on new clothes

Try save on gas and electricity

Cut down on take-away meals

Switch to cheaper grocery brands

Cut down on out-of-home entertainment

Cut down on holidays / short breaks

Cut down on telephone expenses

Delay replacement of major household items

Delay upgrading technology, eg. PC, Mobile

Use my car less often

Cut out annual vacation

Look for better deals on loans, insurance, credit cards

Cut down on at-home entertainment

Cut down on or buy cheaper brands of alcohol

Cut down on smoking

Q3, 10Q4, 10

“Compared to this time last year, which of the following actions would you take in order to stay within your budget?”

*results from a sub-set of those who have said yes, they have changed the way they shop to save money

Reigning in expenditure on new clothes is further evidence that shoppers are once again feeling the pinch and this strategy has moved back up the savings

hierarchy to joint first place with ‘bills’.

Source: Nielsen – Global Consumer Confidence Survey Q4 2010 - GB results

Of those householdslooking to stay withinbudget.

19

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

56%

39%

31%

29%

24%

24%

25%

21%

13%

14%

14%

19%

10%

10%

11%

54%

38%

30%

30%

28%

23%

19%

18%

18%

18%

17%

14%

12%

12%

11%

Try to save on gas and electricity

Cut down on take-away meals

Switch to cheaper grocery brands

Spend less on new clothes

Cut down on telephone expenses

Cut down on out-of-home entertainment

Look for better deals on home loans, insurance, credit cards ..

Use my car less often

Cut down on holidays / short breaks

Delay the replacement of major household items

Delay upgrading technology, eg. PC, Mobile, etc

Cut down on or buy cheaper brands of alcohol

Cut out annual vacation

Cut down on smoking

Cut down on at-home entertainment

Q3, 10Q4, 10

“When economic conditions do improve, which of these do you expect you will continue to do?”

Shoppers will continue to make savings by switching to cheaper grocery brands.

Source: Nielsen – Global Consumer Confidence Survey Q4 2010 - GB results

The continued poor exchange rates for GB shoppers may explain the increase in those looking cut back on holidays.

*results from a sub-set of those who have said yes, they have changed the way they shop to save money

20

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

65%

61%

65%

57%

42%

51%

28%

29%

42%

40%

37%

23%

15%

29%

28%

54%

38%

30%

30%

28%

23%

19%

18%

18%

18%

17%

14%

12%

12%

11%

Try to save on gas and electricity

Cut down on take-away meals

Spend less on new clothes

Switch to cheaper grocery brands

Cut down on telephone expenses

Cut down on out-of-home entertainmentLook for better deals on home loans, insurance, credit

cards etcUse my car less often

Cut down on holidays/short breaks

Delay the replacement of major household items

Delay upgrading technology, eg. PC, Mobile etc

Cut down on or buy cheaper brands of alcohol

Cut down on smoking

Cut out annual vacation

Cut down on at-home entertainment

NowPost Economic Crisis

“Compared to this time last year, which of the following actions would you take in order to stay within your budget?”

of those HHlooking to stay within budget

Saving on household essentials such as bills, groceries and discretionary items: clothes and take-aways are established strategies to save money

Source: Nielsen – Global Consumer Confidence Survey Q4 2010 - GB results*results from a sub-set of those who have said yes, they

have changed the way they shop to save money

Outlook for 2011

22

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

GDP declined 0.5% in the final quarter of 2010. Worst December weather on record has been widely blamed, as hotels and restaurants contributed most to the decline.

GDP Growth UK output decreases by 0.5%

Real GDP quarterly growth

Source: ONS January 26th 2011

Negative growth will re-ignite fears that GB is heading for a double dip recession, analysts have reworked GDP accounting for the weather and suggest the final quarter would have come in at zero.

23

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

Bleak GB Outlook for 2011• Negative GDP in Q4 will re-ignite fears that GB is heading for a double dip

recession.

• Nielsen’s Consumer Confidence survey has identified a diminishing proportion of shoppers believing GB will be out of recession in 12 months

• There is significant evidence that Shoppers are already feeling the impact of falling disposable income ...

– Unit growths remain weak– Promotions remain at an all time high– Shoppers are not willing to spend on discretionary categories such as

general merchandise

• Despite GB Consumer Confidence improving in the final quarter, it ended the year weaker than at the start.

• Discretionary expenditure is expected to be squeezed harder in 2011 as household income for most shoppers is unlikely to keep pace with the cost of living.

24

Copyright © 2011 The Nielsen Company. Confidential and proprietary.

Retail Outlook for 2011

• An increasing proportion of shoppers have no spare cash, those that do are more likely to put into savings or pay off debts than spend on discretionary items.

• For many homeowners there is an anticipation that interest rates will rise in the second half of 2011, putting another squeeze on discretionary spend.

• Looking ahead Grocery Retailers will need to find new incentives to encourage shoppers to spend, as shoppers will have to manage on LESS household income.

![Insperity Business Confidence Survey: Q4 2014 [Infographic]](https://static.documents.pub/doc/80x56/55a700761a28abf75e8b4787/insperity-business-confidence-survey-q4-2014-infographic.jpg)