Problem One and Solution Issue – FFIEC had no guidelines of market risk based potential for federal regulators Housed and modeled a credit agencies master file of over 300 STAG and demographics for each individual in US, creating segmentation models targeting mortgages, refinance-home equity, credit cards, personal, and auto loans. Testified before congressional banking sub-committee and sold business to credit agency. Details – Financial Modeling Concepts had a joint venture with Bear Stearns for CRA Securitization and partially owned by Trans Union. Co-Founder, Partner and Chief Scientist – Financial Modeling Concepts Solution – Recoded and Lifestage Trans Unions Master Credit and Demographic File Scored TU Master file against existing COOP of 5MM+ CRA loans by product Filtered by Current FICO and geography against current housing stock Provided FFIEC Bank examiners expected local area potential, sold banks pre-qualified prospects

Transcript

Problem One and SolutionIssue – FFIEC had no guidelines of market risk based potential for federal regulators

Housed and modeled a credit agencies master file of over 300 STAG and demographics for each individual in US, creating segmentation models targeting mortgages, refinance-home equity, credit cards, personal, and auto loans. Testified before congressional banking sub-committee and sold business to credit agency.

Details – Financial Modeling Concepts had a joint venture with Bear Stearns for CRA Securitization and partially owned by Trans Union.

Co-Founder, Partner and Chief Scientist – Financial Modeling Concepts

Solution – Recoded and Lifestage Trans Unions Master Credit and Demographic File

Scored TU Master file against existing COOP of 5MM+ CRA loans by product

Filtered by Current FICO and geography against current housing stock

Provided FFIEC Bank examiners expected local area potential, sold banks pre-qualified prospects

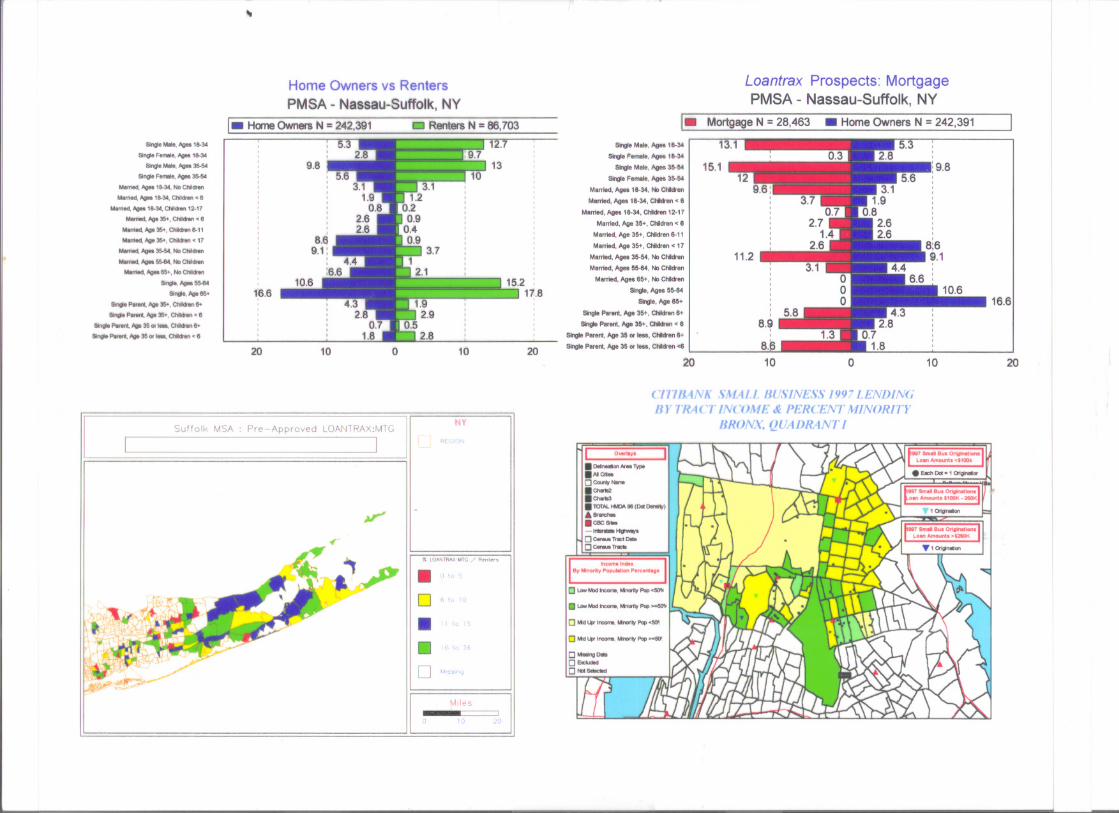

Definitions : Using a combination of data from TU, the Government, and several Client banks, a series of algorithms where developed that identified Prospects for various financial products ( New Mortgage, Refinance, Home Improvement, Installment, & Automobile). All data were Aggregated to Tract level geography. Using a GAP analyses approach each area was segmented based upon the current presence and potential. Essentially a spreadsheet and map were provided that was capable of demonstrating each clients performance.

Specifics : The essentials of the LOANTRAX Algorithms consist of pre-processing the TU master file which created a single Lifestage dimension from several raw variables, householded the file to create a single last name-street address combination, eliminated and audited anomalies found with the data, tagged and classified records according to FFIEC definitions. In addition all bank sourced data was matched to this file and coded to be used in the modelling.

Data Mart

Loantrax Algorithms

Raw Files from CPUS System 2/1997 Demographic lrecl = 384 & Credit lrecl=786

from FFIEC lrecl=836 N=46,641from List & Insurance Services Combined single file lrecl=930 N=127,030,251

RecodesCreates Matchkey (Household versus Individuals - Single Address-Last Name Combo)Lifestage (Age-DOB&Infered, Sex, Marital Status, Kids)Owner (Credit and Demo side with Opendate for LOR)Geocodes (Classification into LMI / MUI)

Bank Sourced CIFFirst Chicago = 918,571 AccountsFleet Boston = 833,523 Accounts

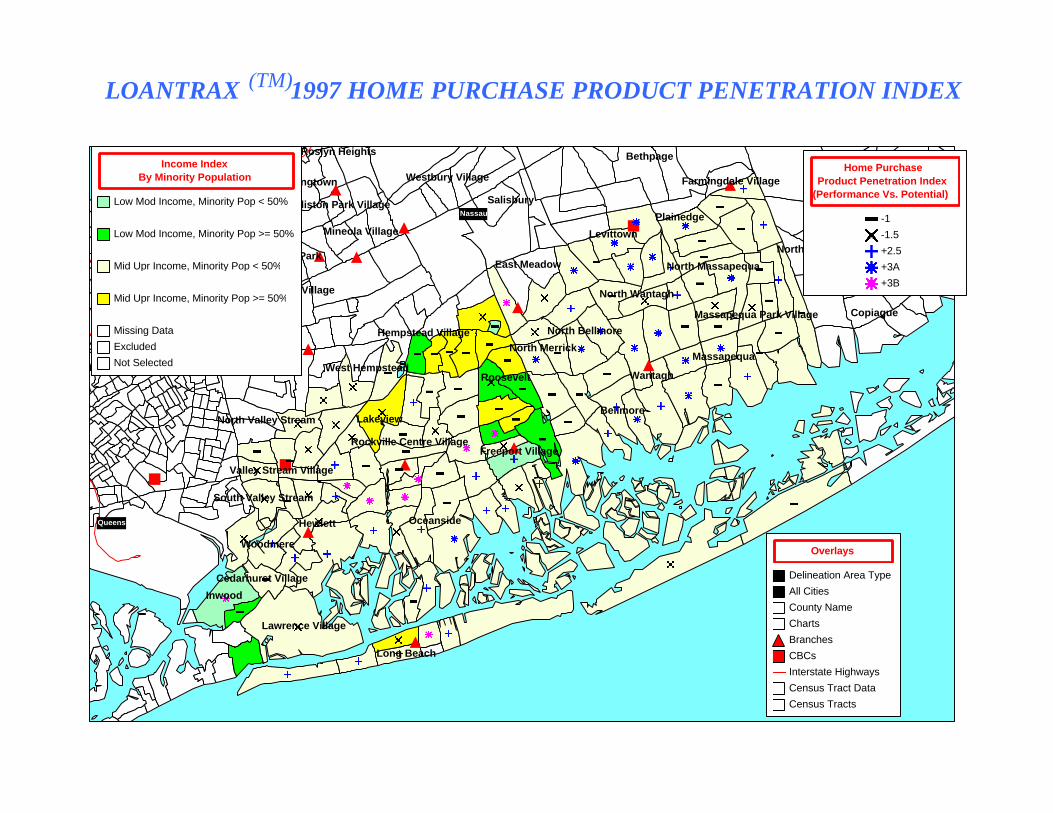

LOANTRAX 1997 HOME PURCHASE PRODUCT PENETRATION INDEX(TM)

Nassau

Hempstead Village

Levittown

Valley Stream Village

Oceanside

Freeport Village

Elmont

East Meadow Lindenhurst Village

West BabylonWest Islip

Hicksville

Plainview

Dix Hills

Huntington Station

Deer Park

Brentwood

Central Islip

Commack

Smithtown

Holbrook

Centereach

Coram

Hewlett

North Valley Stream

New Hyde Park Village

North New Hyde Park

Manhasset

Port Washington

Williston Park Village

Albertson

East Hills Village

Glen Cove

Bayville Village

Roosevelt

Bellmore

Wantagh

North Wantagh

North Massapequa

East Massapequa

Salisbury

New Cassel

Jericho

Syosset

Old Bethpage

Farmingdale Village

Melville

Wyandanch Bay Shore

Islip

Oyster Bay

West Hills

Huntington

Centerport

Elwood Hauppauge

East Northport

Fort Salonga

Kings Park St. James

Islip Terrace Oakdale

Bohemia

Nesconset

Sayville

Patchogue Village

Holtsville

Lake Grove Village

Stony Brook

Setauket-East Setauket

Terryville

Medford

East Patchogue

North Bellport

Yaphank

Middle Island

Overlays

Delineation Area Type

All Cities

County Name

Charts

Branches

CBCs

Interstate Highways

Census Tract Data

Census Tracts

Income IndexBy Minority Population

Low Mod Income, Minority Pop < 50%

Low Mod Income, Minority Pop >= 50%

Mid Upr Income, Minority Pop < 50%

Mid Upr Income, Minority Pop >= 50%

Missing Data

Excluded

Not Selected

Home PurchaseProduct Penetration Index

(Performance Vs. Potential)

-1

-1.5

+2.5

+3A

+3B

LOANTRAX 1997 HOME PURCHASE PRODUCT PENETRATION INDEX(TM)

Queens

Nassau

Hempstead Village

Levittown

Long Beach

Valley Stream Village

Oceanside

Freeport Village

Elmont

East Meadow Lindenhurst Village

West Babylon

Inwood

Lawrence Village

Cedarhurst Village

Woodmere

South Valley Stream

Hewlett

Floral Park Village

North Valley Stream Lakeview

Rockville Centre Village

West Hempstead

New Hyde Park Village

North New Hyde Park

Great Neck Plaza Village

Williston Park Village

Searingtown

Roslyn Heights

Mineola Village

Roosevelt

Bellmore

North Merrick

North Bellmore

Wantagh

Massapequa

North Wantagh

North Massapequa

Massapequa Park Village

North Amityville

Westbury Village

Salisbury

Plainedge

Bethpage

Farmingdale Village

Copiague

North Lindenhurst

Overlays

Delineation Area Type

All Cities

County Name

Charts

Branches

CBCs

Interstate Highways

Census Tract Data

Census Tracts

Income IndexBy Minority Population

Low Mod Income, Minority Pop < 50%

Low Mod Income, Minority Pop >= 50%

Mid Upr Income, Minority Pop < 50%

Mid Upr Income, Minority Pop >= 50%

Missing Data

Excluded

Not Selected

Home PurchaseProduct Penetration Index

(Performance Vs. Potential)

-1

-1.5

+2.5

+3A

+3B

Performance Context QuantificationUsing these Maps and the accompanied spreadsheets, BankExaminers could quickly and effectively assess the Real MarketPotential in an area and see the banks performance, product byproduct. Potential was now defined by Lifestage appropriateness and Risk/Credit worthiness. Banks could now address the exact locationswhere the potential was high yet the current presence was low.CRA was one application based upon FFIEC defined Geographies. HMDA issues where another application based upon Census countsby race concentrations. Both laws could now be quantitativelymeasured and defended by client banks.