56

INTRODUCTION

Retail means selling goods and services in small quantities directly to customers. Retailing

consists of all activities involved in marketing of goods and services directly to consumer for

their personnel family and household use.

The Indian retailing industry is becoming intensely competitive, as more and more payers are

Vying for the same set of customers. The major retail players are Pantaloon Retail, Shoppers

Stop, Reliance, etc.,

Retailing is one of the biggest sectors and it is witnessing revolution in India. The new entrant in

retailing in India signifies the beginning of retail revolution. India's retail market is expected to

grow tremendously in next few years. According to AT Kearney, The Windows of Opportunity

shows that Retailing in India was at opening stage in 1995 and now it is in peaking stage in 2006.

India's retail market is expected to grow tremendously in next few years. India shows US$330

billion retail market that is expected to grow 10% a year, with modern retailing just beginning.

India ranks first in 2005. In fact, in 2005 and 2006, India is the most compelling opportunity for

retailers, because now India is in peaking stag

OBJECTIVES

Analyse the customer satisfaction in Big Bazaar

Understand the consumer perception about Big Bazaar

Understand the consumer welfare measurement taken by Big Bazaar

RESEARCH METHODOLOGY

MEANING OF RESEARCH- Research is an active, diligent, and systematic process of inquiry

aimed at discovering, interpreting, and revising facts. This intellectual investigation produces a

greater knowledge of events, behaviors, theories, and laws and makes practical applications

possible. The term research is also used to describe an entire collection of information about a

particular subject, and is usually associated with the output of science and the scientific method

SAMPLE SIZE:

Three hundred respondents were randomly selected .

SAMPLE DESIGN- Simple random method

SOURCES OF DATA COLLECTION- Data collected in this project is both collected both

from both primary and secondary sources of data collection which are as follows-

PRIMARY DATA - The Primary data collection is done through a structured

questionnaire(open & closed) and interview

SECONDARY DATA - Secondary sources are the other important sources through which the

data were collected. Includes internet, websites, journals, articles, and the reports maintained by

BIGBAZAR.

Limitations

Time was the major constraint, which prevented me to put in more effort.

Some people left few questions unanswered.

Some of the respondents were not ready to fill the questionnaire.

Not all the respondents were cooperative thus it was difficult to convince them for filling

up the questionnaire.

Some of the respondents might have got biased while filling up the questionnaire.

INDUSTRY PROFILE

INTRODUCTION Retail means selling goods and services in small quantities directly to customers. Retailing

consists of all activities involved in marketing of goods and services directly to consumer for

their personnel family and household use.

The Indian retailing industry is becoming intensely competitive, as more and more payers are

Vying for the same set of customers. The major retail players are Pantaloon Retail, Shoppers

Stop, Reliance, etc.,

Retailing is one of the biggest sectors and it is witnessing revolution in India. The new entrant in

retailing in India signifies the beginning of retail revolution. India's retail market is expected to

grow tremendously in next few years. According to AT Kearney, The Windows of Opportunity

shows that Retailing in India was at opening stage in 1995 and now it is in peaking stage in 2006.

India's retail market is expected to grow tremendously in next few years. India shows US$330

billion retail market that is expected to grow 10% a year, with modern retailing just beginning.

India ranks first in 2005. In fact, in 2005 and 2006, India is the most compelling opportunity for

retailers, because now India is in peaking stage.

Sector details

1. Introduction to retail industries.

2. Retail word is derived French word retailer means to cut off a piece.

3. Retailing includes all the activities involved in selling goods or services to the final customer

for personnel or non-business use.

4. Supermarket is a retailing of a wide variety of consumer products under one roof, ample stock,

stock of several brands & extended business hours.

History of retailing

Retail concept is old in India. World‟s first departmental store started in Rome. Today‟s kirana

stores are based on Manusmriti & Kautilya‟s arthshastra.Haats, Melas, Mandis & door to door

salesmen are traditional Indian retail.

Vishal Mega Mart is a retail sector, which is providing good quality of products in very

reasonable price than its competitors. Retailing and wholesaling consist of many organizations

designed to bring goods and services from the point of production to the point of use.

Retailing includes all the activities involved in selling goods or services directly to final

consumers for their personal, non-business use. Retailers can be classified in terms of store

retailers, non-store retailing, and retail organizations.

Store retailers include many types, such as specialty stores, department stores, supermarkets,

convenience stores, superstores, combination stores, hypermarkets, discount stores, warehouse

stores, and catalog showrooms. These store forms have had different longevities and are at

different stages of the retail life cycle. Depending on the wheel-of-retailing, some will go out of

existence because they cannot compete on a quality, service, or price basis.

Non-store retailing is growing more rapidly than store retailing. It includes direct selling (door-

to-door, party selling), direct marketing, automatic vending, and buying services. Much of

retailing is in the hands of large retail organizations such as corporate chains, voluntary chain

and retailer cooperatives, consumer cooperatives, franchise organizations, and merchandising

conglomerates. More retail chains are now sponsoring

Diversified retailing lines and forms instead of sticking to one form such as the department store.

Retailers, like manufacturers, must prepare marketing plans that include decisions on target

markets, product assortment and services, store atmosphere, pricing, promotion, And place.

Retailers are showing strong signs of improving their professional management and their

productivity, in the face of such trends as shortening retail life cycles, new retail forms,

increasing intertype competition, and polarity of retailing, new retail technologies, and many

others.

Wholesaling includes all the activities involved in selling goods or services to those who are

buying for the purpose of resale or for business use. Wholesalers help manufacturers deliver their

products efficiently to the many retailers and industrial users across the nation. Wholesalers

perform many functions, including selling and promoting, buying and assortment-building, bulk-

breaking, warehousing, transporting, financing, risk bearing, supplying market information, and

providing management services and

Counseling. Wholesalers fall into four groups. Merchant wholesalers take possession of the

goods and include full-service wholesalers (wholesale merchants, industrial distributors) and

limited-service wholesalers (cash-and- carry wholesalers, truck wholesalers, drop shippers, rack

jobbers, producers' cooperatives, and mail-order wholesalers). Agents and brokers do not take

possession of the goods but are paid a commission for facilitating buying and selling.

Manufacturers' and retailers' branches and offices are wholesaling operations conducted by non-

wholesalers to bypass the wholesalers. Miscellaneous wholesalers include agricultural

assemblers, petroleum bulk plants and terminals, and auction companies.

Wholesalers, too, must make decisions on their target market, product assortment and services,

pricing, promotion, and place. Wholesalers who fail to carry adequate assortments and inventory

and provide satisfactory service are likely to be bypassed by manufacturers. Progressive

wholesalers, on the other hand, are adapting marketing concepts and streamlining their costs of

doing business.

CURRENT SCENARIO

India rank first in terms of emerging market potential in retail sector. Current retail market is US

$ 215 billion. Growth rate of retail sector in India is 8-10% per annum. Near about 12 million

retail outlets are spread across India.

FDI in retail sector increases from US $ 3.1 billion in 2003 to over US $7.6 billion in

2009.

TYPES OF RETAILERS

Retailers are broadly classified into 3 categories

Food Retailers.

General Merchandise Retailers.

Service Retailers.

OTHER SERVICES PROVIDED BY RETAILERS

Retail not only provides products to the customer but also gives different types of services like:

Airlines & travel agents

Banks

Health clubs

Hotel & Restaurants

Movie theatres

TECHNOLOGIES USED IN RETAILING SECTOR

In-store technologies-

Interactive kiosks

Virtual display case

Radio Frequency identification tags

Self-scanning & self-checkout system

Body scanning

Online technology-

Online display of products

Online shopping

CHALLENGES

Largely urban phenomenon, pace of growth is still slow.

Not being recognized as an industry in India so availability of finance is low to new

market players.

High cost of real estate.

High stamp duties.

Lack of infrastructure.

Multiple & complex taxation system.

Protest against retail sector.

FUTURE STRATEGY

It is projected that up to 2010 retail sector will be worth around US $ 300 billion.

FDI is going to increase rapidly, up to 2010 retail sector will become biggest industry in India.

Retail sector is expected to create 2 million jobs up to 2010.

According to Indian Retail Report top 10 players in modern retail trade are going to invest US $

18-20 billion in next five years.

Sector Details

In India, the most of the retail sector is unorganized. In India, the retail business contributes

around 10 percent of GDP. Of this, the organized retail sector accounts only for about 5 percent

share, and the expected annual growth rate is 5% per annum and remaining share is contributed

by the unorganized sector. The main challenge facing the organized sector is the competition

from unorganized sector. Unorganized retailing has-been there in India for centuries, theses are

named as mom-pop stores. The main advantage in unorganized retailing is consumer familiarity

that runs from generation to generation. It is a low cost structure, they are mostly operated by

owners, has very low real estate and labor costs and has low taxes to pay. And it also gives 8%

Employment to the country annually.

In late 1990's the retail sector has witnessed a level of transformation. Retailing is being

perceived as a beginner and as an attractive commercial business for organized business i.e. the

pure retailer is starting to emerge now. Organized retail business in India is very small but has

tremendous scope. The total in 2005 stood at $225 billion, accounting for about 10% of GDP. In

this total market, the organized retail accounts for only $8 billion

of total revenue. According to A T Kearney, the organized retailing is expected to be more than

$23 billion revenue by 2010.

In organized retailing will grow faster than unorganized sector and the growth speed will be

responsible for its high market share, which is expected to be $ 17 billion by 2010-11.

The organized sector is expected to grow faster than GDP growth in next few years driven by

favorable demographic patterns, changing lifestyles, and strong income growth. This organized

retail sector mix includes supermarkets, hypermarkets discounted stores and specialty stores,

departmental stores. For example, Spencer network has 69 stores, which includes seven Spencer

hypermarkets, three Spencer super markets and 49 Spencer Daily‟s. Now the company is

planning to open 20 stores in 10 cities in six months. The top 10 retailers account only for 2% of

total market, today modern retailing is expected to enter a boom phase, which has major players

and these players might capture 10% of total market, within next five years. The retail sales in

India for future are shown below (data from 2005-2008 is based on estimates)

The trend in the Industry

1. Low share of organized retailing

2. Falling real estate prices

3. Increase in disposable income and customer aspiration

Increase in expenditure for luxury items (CHART)

Another credible factor in the prospects of the retail sector in India is the increase in the young

working population. In India, hefty pay packets, nuclear families in urban areas, along with

increasing working-women population and emerging opportunities in the services sector. These

key factors have been the growth drivers of the organized retail sector in India which now boast

of retailing almost all the preferences of life - Apparel &

Accessories, Appliances, Electronics, Cosmetics and Toiletries, Home & Office Products, Travel

and Leisure and many more. With this the retail sector in India is witnessing rejuvenation as

traditional markets make way for new formats such as departmental stores, hypermarkets,

supermarkets and specialty stores.

Existing competition

Reliance fresh.

Aditya Birla group.

Shopper‟s Shoppe.

Subhiksha.

Big bazaar.

Mark and Spencer‟s.

The untapped scope of retailing has attracted superstores like Wal-Mart into India, leaving

behind the kiranas that served us for years. Such companies are basically IT based. The other

important participants in the Indian Retail sector are Bata, Big Bazaar, Pantaloons, Archies, Cafe

Coffee Day, landmark, Khadims, Crossword, to name a few.

Evolution of Indian Retail Industry

Indian Retail Industry is standing at its point of inflexion, waiting for the boom to take place.

The inception of the retail industry dates back to times where retail stores were found in the

village fairs, Mela‟s or in the weekly markets. These stores were highly unorganized. The

maturity of the retail sector took place with the establishment of retail stores in the locality for

convenience. With the government intervention the retail industry in India took a new shape.

Outlets for Public Distribution System, Cooperative

stores and Khadi stores were set up. These retail Stores demanded low investments for its

establishment. International Brand Outlets, Hyper or Super markets, shopping malls and

departmental stores

Retailing in India: a forecast

Future of organized retail in India looks bright. According to recent researches it is projected to

grow at a rate of about 37% in 2007 and at a rate of 42% in 2008. It will capture a share of 10%

of the total retailing by the end of 2010.

INDIA: A Hot Spot

India retail industry is the largest industry in India, with an employment of around 8% and

contributing to over 10% of the country's GDP. Retail industry in India is expected to rise 25%

yearly being driven by strong income growth, changing lifestyles, and favorable demographic

patterns.

It is expected that by 2016 modern retail industry in India will be worth US$ 175- 200 billion.

India retail industry is one of the fastest growing industries with revenue expected in 2007 to

amount US$ 320 billion and is increasing at a rate of 5% yearly. A further increase of 7-8% is

expected in the industry of retail in India by growth in consumerism in urban areas, rising

incomes, and a steep rise in rural consumption. It has further been predicted that the retailing

industry in India will amount to US$ 21.5 billion by 2010 from the current size of US$ 7.5

billion.

Shopping in India has witnessed a revolution with the change in the consumer buying behavior

and the whole format of shopping also altering. Industry of retail in India which have become

modern can be seen from the fact that there are multi- stored malls, huge shopping centers, and

sprawling complexes which offer food, shopping, and entertainment all under the same roof.

India retail industry is expanding itself most aggressively; as a result a great demand for real

estate is being created. Indian retailers preferred means of expansion is to expand to other

regions and to increase the number of their outlets in a city. It is expected that by 2010, India

may have 600 new shopping centers.

In the Indian retailing industry, food is the most dominating sector and is growing at a rate of 9%

annually. The branded food industry is trying to enter the India retail industry and convert Indian

consumers to branded food. Since at present 60% of the Indian grocery basket consists of non-

branded items.

As the contemporary retail sector in India is reflected in sprawling shopping centers, multiplex-

malls and huge complexes offer shopping, entertainment and food all under one roof, the concept

of shopping has altered in terms of format and consumer buying behavior, ushering in a

revolution in shopping in India. This has also contributed to large- scale investments in the real

estate sector with major national and global players investing in developing the infrastructure

and construction of the retailing business.

Growth Drivers

Growth drivers in India for retail sector

Rising incomes and improvements in infrastructure are enlarging consumer markets and

accelerating the convergence of consumer tastes.

Liberalization of the Indian economy

Increase in spending Per capital Income.

Advent of dual income families also helps in the growth of retail sector.

Shift in consumer demand to foreign brands like McDonalds, Sony, Panasonic, etc.

·Consumer preference for shopping in new environs

The Internet revolution is making the Indian consumer more accessible to the growing influences

of domestic and foreign retail chains. Reach of satellite T.V.

Channels are helping in creating awareness about global products for local markets.

About 47% of India's population is under the age of 20; and this will increase to 55% by 2015.

This young population, which is technology-savvy, watch more than 50 TV satellite channels,

and display the highest propensity to spend, will immensely contribute to the growth of the retail

sector in the country.

Availability of quality real estate and mall management practices

Foreign companies' attraction to India is the billion-plus population.

Employment opportunities in retail sector in India

India's retail industry is the second largest sector, after agriculture, which provides employment.

According to Associated Chambers of Commerce and Industry of India (ASSOCHAM), the

retail sector will create 50,000 jobs in next few years.

Retail companies are starting retail management courses in partnership with management

institutes, roping in talent from other sectors and developing comprehensive career growth and

loyalty plans for existing employees.

Top players like Pantaloon Retail India Limited, Trent, Shopper's Stop, RPG Group and ebony

are virtually on their toes.

Consider the plans of largest player, The Pantaloon Retail India Ltd, the company has developed

a comprehensive strategy, where in it expects that in 2years, it will not recruit any new managers

from outside.

"The estimated need is 1 lakh of employees till 2011", said Mr. Sanjoy Jog, HR Head at

Pantaloon Retail India Ltd. Pantaloon has the concept of partnership with educational Institute to

run retail courses across the entire chain. Trent has also started in-house learning programmers

and now goes to under graduate colleges to recruit students.

Since, the job market is hugely receptive to this with more and more business schools focusing

on the sector and large retailers setting up retail academics.

Challenges of Retailing in India

In India the Retailing industry has a long way to go, and to become a truly flourishing industry,

retailing needs to cross the following hurdles:

The first challenge facing the organized retail sector is the competition from unorganized sector.

In retail sector, Automatic approval is not allowed for foreign investment.

Taxation, which favors small retail businesses.

Developed supply chain and integrated IT management is absent in retail sector.

Lack of trained work force.

· Low skill level for retailing management.

· Intrinsic complexity of retailing- rapid price changes, threat of product obsolescence and low

margins.

Organized retail sector has to pay huge taxes, which is negligible for small retail business. Many

agencies have estimated differently about the size of organized retail market in 2010. The one

thing that is common amongst these estimates is that Indian organized retail market will be very

big in 2010. The status of the retail industry will depend mostly on external factors like

Government regulations and policies and real estate prices, besides the activities of retailers and

demands of the customers also show impact on retail industry.

Competition in retail

India Retail attempts to capture excitement of Retail Business in India by aggregating the best in

news, views, research, analysis, trends, technology, and competition dents retail sector growth.

The performance of the retail sector in the last quarter of financial year 2008-09 has been a

gloomy one. Not only has the quarter-on-quarter growth declined by 700 basis point, on year-on-

year (YoY) basis, sales growth fell drastically from 67.8% to 49.1%. Including the recently listed

Koutons and Vishal Retail, all big retailers continue to be on an aggressive expansion mode. This

kind of competition is having a negative impact on margins of retailers, as the target audience for

all of them, more or less, remains the same.

The slowdown has triggered a volume game in the industry. Strategies like promotional

campaigns, freebies, promoting private labels and online discounts are just some of the avenues

that retailers are looking at to lure customers. According to analysts, this is a knee-jerk reaction

by the industry to fight the inflation-induced dent in the purchasing power of customers. As they

say, retail is a number game, so, big retailers are trying to push volumes. For some, it comes at

the cost of profit. Meanwhile, in contrast to YoY sales growth of 49% for the sector, the interest

cost has registered a whopping 96% growth. Though growing at a lesser 39%, depreciation cost

has also been impacting margins.

The cost factor too is adding to the woes. For instance, during the quarter, Shoppers Stop opened

its new stores in various formats. Provogue and Pantaloon followed soon. The companies are

increasing their geographical presence in the wake of increasing competition. Launch of new

formats continues to catch the attention of these retailers. In fact, a couple of these new formats

are already generating profit at the operating level, thus showing a positive sign towards growth.

Like for Shoppers Stop, the average transaction size increased by about 7% for the current

quarter over the same quarter in the previous year. Players like Provogue and Pantaloons too

have witnessed a similar upward movement. Also, though growth in total expenses as a whole

has almost been equivalent to the growth in sales at about 47%, some individual cost items like

staff costs, selling and administration costs are under control. On a YoY basis, staff cost has

grown at 26% against 44% in the corresponding quarter of the previous year.

Nonetheless, raw material cost continues to remain high - it grew by 66% in the last quarter and

now is equivalent to 74% of the industry's aggregate net sales. This is the reason why operating

margins have reduced to 4.8% of the revenue sale compared with 5.7% during the corresponding

quarter of the previous year.

Among individual retailers, Pantaloon Retail continues to outgrow the industry – it recorded 57%

a YoY growth in net sales during March 2008 quarter. Although it is lower compared with the

63% growth recorded during the December quarter, momentum continues to favour the

company. New stores drove the growth in value-for-money format - strategies such as KB's Fair

Price and online shopping are picking up. Their home store division has also been doing well.

Next on growth charts is Provogue, which grew 40% in the last quarter, similar to the previous

quarter.

In short, setting up of new stores has resulted in higher working capital funding, which has raised

the industry's interest outgo. For Pantaloon, interest cost has almost doubled during the current

quarter - as a proportion of sales, it has increased from 2.7% to 3.2% on a YoY basis. Provogue

seems to be an exception in this as it recorded the highest increase of 100 basis points in interest

cost for March 2008. Overall, the profitability margin has seen a sharp decline.

Only Shoppers Stop has registered some profit compared with its performance in the

corresponding quarter of the previous year. The company's net profit margin now stands at 0.7%

of net sales as compared to -1% in March 2007 quarter. It can be concluded that margins of retail

companies seem to have been hit by costs related to their ambitious expansion programmer.

Expansion plans for some of them are running behind schedule. It has led to higher interest cost,

yet retail companies are trying hard to cut costs by keeping inventory and carrying costs under

control.

Big retailers at loggerheads with MNCs over brands

A serious conflict is brewing between Indian retailers and multinationals over imports of global

brands. To stay afloat in the dog-eat-dog world of retail, local retailers have reached

arrangements with overseas players to bring in some international brands, rattling many MNCs

who manufacture or market these products locally. In some cases, these brands have not yet been

introduced in India.

Several major MNCs with a long presence in India are invoking the Intellectual Property Rights

(imported goods) Enforcement Rules 2007 to stop retailers from importing foreign brands.

Hindustan Unilever, L‟Oreal, Lancôme Perfumes, Oakley Inc, Nivea and Mico have already

registered several brands with the Customs department. Sources said other MNCs are expected to

follow suit.

Market circles perceive this as a move to prevent Indian retailers from getting first access to

these brands. Some of the retailers are debating plans to legally contest the move, since they

possess a free sale certificate from the source of import. Retailers like Big Bazaar & Food

Bazaar, Reliance Retail, Spencer‟s and Sankalp Retail (MyDollarStore), among others, have

begun importing sizeable consignments of leading consumer brands and their variants for better

fill rates, product variety and higher margins.

However, the multinationals are not amused, and claim that it leads to loss of business

opportunity, unfair competition and product cannibalization. The fundamental issue here,

according to analysts, is that the Indian arms of the leading FMCG companies would like to

control the way their brands are marketed and sold. They would also like to determine when new

products and variants of existing products should be introduced in India.

A key reason for retailers to step up imports is bottom lines. Profit margins on imported products

are around 20% more than local brands, where producers and retailers are at loggerheads over

sharing margins.

“We are concerned over issues like protecting the properties of our brands, including quality and

consumer perception. Such unplanned imports create brand confusion in the minds of consumers,

since the properties of an imported brand are completely different from the domestic ones, which

are localized to suit the specific region‟s requirements. An unpleasant experience may work

against our brand,” said a high-ranking official in a leading multinational, which makes personal

care products.

Retailers claim they are creating „demand in advance‟ for the multinationals, which would

otherwise have to invest heavily in marketing and ad spends to promote the brands. Analysts say

the developments are the natural effects of a globalize market that India is moving towards,

which upsets the conventional distribution and trade practices.

State of Competition in the Wholesale and Retail Sector

The study assesses the state of competition in the Philippine wholesale and retail sector, focusing

on the distribution of specialized goods and pharmaceutical products. It uses the traditional tools

of analysis like concentration ratios and price-cost margins in determining the competitive state

of the sector. The study also analyzes the other dimensions in retail competition like price,

geographical location, and retail product and retail service. Industry data from the National

Statistics Office were used in the analysis, aided by a small-scale survey conducted in the Metro

Manila area.

The department store and grocery sub sector appears to operate in a competitive environment

despite the presence of two big dominating firms in the market. No price or quantity leader-

follower behavior was observed, as validated by the tools used in the analysis. On the other hand,

one firm, whose strategic advantages include economies of scope and space, retail image and

consumer loyalty, dominates the distribution of pharmaceutical products. Potential market

entrants face these forms of challenges-- factors that are not regarded as anti-competitive and are

welfare enhancing to the general public.

The need for competition policy is recommended to guard against possible merger of the giant

firms in the department store and grocery sub sector. Any possible collusion between the big

firms could result to a monopolistic outcome.

The study observes that the apparent high price of pharmaceutical products is mainly attributed

to the manufacturing process, and not at the distribution of these goods. Hence, it is

recommended that a study analyzing the state of competitiveness of manufacturing

pharmaceutical products be conducted. Thing else that is timely, authentic Electronics retail

sector could get new competition

Types of Retailing

There are several types we can see in Retailing. They are like:

Specialty Store:

Narrow product line with deep assortment, viz apparel stores, book stores etc. A clothing store

would be a single line store, men's clothing store would be limited line store &men's custom-

shirt store would be a super specialty store.

Example: The limited, The Body Shop.

Departmental Store:

Several products lines-typically clothing, household goods, home furnishings- with each line

operated as a separate department managed by specialist buyers or merchandisers.

Example: Sears, Bloomingdale's.

Supermarkets:

Relatively large, low-cost, low-margin, high volume, self-service operation designed to serve

total needs for food, laundry & household maintenance products.

Example: Kroger, Safeway.

Convenience Stores:

Relatively small store located near residential area, open long hours, seven days a week and

carrying a limited line of high-turnover convenience products at slightly higher prices.

Example: 7-Eleven, Circle K.

Discount Store:

Standard merchandise sold at lower prices with lower margins and higher volumes. True

discount stores regularly sell merchandise at lower prices and offer mostly national brands.

Example: Wal-Mart, Kmart.

Off-price retailer:

Merchandise bought at less than regular wholesale prices & sold at less than retail; often leftover

goods, overruns and irregulars obtained at reduced prices from manufacturers or other retailers.

Factory outlets are owned and operated by manufacturers and normally carry the manufacturer's

surplus, discontinued or irregular goods.

Example: Mikasa (dinnerware), Dexter (shoes)

Independent off-price retailers are owned & run by entrepreneurs or by divisions of larger retail

corporations.

Example: T.J.Maxx, Filene's Basement.

Superstore:

Averages 35,000 square feet of selling space traditionally aimed at meeting consumers' total

needs for routinely purchased food and non-food items. Usually offer services such as laundry,

dry cleaning, shoe repair, check cashing & bill paying.

A new group called "category killers" carries a deep assortment in a particular category & a

knowledgeable staff.

Example: Borders books & Music, IKEA.

Combination stores are a diversification of the supermarket store into the growing drug and-

prescription field. Combination food & drug stores average 55,000 square feet of selling space.

Example: Jewel & Osco stores.

Hypermarkets range between 80,000 and 220,000 square feet and combine supermarket, discount

& warehouse retailing principles. Product assortment goes beyond routinely purchased goods &

includes furniture, large & small appliances, clothing items and many other items. Bulk display

& minimum handling by store personnel with discounts offered to customers who are willing to

carry heavy appliances and furniture out of the store.

Hypermarkets originated in France.

Example: Carrefour and Casino (France), Pyrca, Continente and Alcampo (Spain).

Emerging trends in Indian organized retail sector

BPO industry in India

BPO (Business Process outsourcing) is one of the fastest growing segments of the Information

Technology Enabled Services (ITES) industry in India. Business Process Outsourcing refers to

the delegation of one or more IT-intensive business process to an external provider that in turn

owns administers and manages the selected process based on defined and measurable

performance criteria. The Indian BPO industry is constantly growing and a lot of fortune 500

companies are outsourcing services to India. There are several reasons for India‟s emergence as

one of leading outsourcing destinations. India is very rich in educated and talented human

resource. India is one of the pioneers in software development. India has an excellent technical

facilities and infrastructure for setting up call centers. Time zone difference between India and

America has also worked to the advantage of Indian BPO industry. India has an 8-12 hour time

zone difference with respect to the US and other developed markets. Most of the Indian cell

centers servicing American customers have timings between 5:30 pm to 9:30 am this time zone

difference allows Indian companies BPO‟s to service American clients by working in the nights.

last but not the least India has huge pool of English speaking workforce that provides excellent

voice based services at extremely competitive costs resulting in huge savings for companies.

Some of the leading BPO companies in India are

GE capital.

Converges

Wipro Spectra mind.

Dell

ICICI One Source

MphasiS.

Inflation in India

Inflation in India is at an acceptable level and remains much lower than in many other

developing countries. But off late prices of essential commodities such as food grain, edible oil,

vegetables etc have risen sharply and in the process driving up the inflation rate.

Inflation is defined as a sustained increase in the general level of prices for goods and services. It

is measured as an annual percentage increase. As inflation rises the value of currency goes down.

The current rise in inflation has its roots in supply-side factors. There was shortfall in domestic

production vis-à-vis domestic demand and hardening of international pieces, prices of primary

commodities, mainly food items. Wheat, pulses, edible oils, fruits and vegetables, and

condiments and spices have been the major contributors to the higher inflation rate of primary

articles. The inflation was also accompanied by buoyant growth of money and credit. While

GDP growth zoomed to 9.0 per cent per annum, the board money (M3) grew by more than 20

per cent.

Inflation is calculated on the bases of Wholesale Price Index (WPI) while in other countries it is

calculated on Consumer Price Index (CPI).

The emerging trends in the Indian organized retail sector would help the economic growth in

India.

There is a fantastic rise in the Indian organized retail sector in a very short period of time

between 2001 and 2006. Eventually, out of the shadows of the unorganized retail sector, India

has a chance of tremendous economic growth, both in India and abroad.

The emerging trends in the Indian organized retail sector are also adding up to the development

of the Indian organized retail sector. The relaxation by the government on regulatory controls on

foreign direct investments has added to the process of the growth of the Indian organized retail

sector.

The infrastructure of the retail sector will evolve radically in the recent future. The emergences

of shopping malls are increasing at a steady pace in the metros and there are further plans of

expansion which would lead to 150 new ones coming up in India by 2008. As the count of super

markets is going up much faster than rate of growth in retail sector, it is taking the lion‟s share in

food trade.

The growth of the Indian organized retail sector is anticipated to be heavier than the growth of

the gross domestic product. Alterations in people's lifestyle, growth in income levels, and

encouraging conventions of demography are proving favorable for the new emerging trends in

the Indian organized retail sector.

The success of this retail sector would also lie in the degree of penetration into the lower income

strata to tap the possible customers in the lowest levels of society. The demands of the buyers

would also be enhanced by more access to credit facilities. With the arrival of the Transnational

Companies (TNC), the Indian retail sector will undergo a transformation. At present the Foreign

Direct Investments (FDI) is not encouraged in the Indian organized retail sector but once the

TNC'S get in they inevitably try to oust their Indian counterparts. This would be challenging to

the retail sector in

India.

The trends to follow in the future:

The Indian Organized retail sector will grow up to 10% of total retailing by 2010.

No one single format can be assumed, as there is a huge difference in cultures regionally.

The most encouraging format now would be the hyper marts.

The hyper mart format would be further encouraged with the entry of the MNCs

Current Scenario

· A glimpse of the International Retail

· One of the world's largest industries exceeding US$ 9 trillion

· 47 global fortune companies & 25 of Asia's top 200 companies are retailers

· Dominated by developed countries

· US, EU & Japan constitute 80% of world retail sales.

· Biggest player in India is Pantaloon Retail India Limited.

Percentage of Organized Retail

USA - 85%

Taiwan - 81%

Malaysia - 55%

Thailand - 40%

Brazil - 36%

Indonesia - 30%

Poland - 20%

China - 20%

India - 3%

Key players

The existing players like Big Bazaar, More Retail outlay, Vishal Mega Mart,

Shoppers' Stop, Pyramid are expanding to smaller towns and cities. Many other business houses

are planning to enter the retail sector either on their own or through partnerships. New entrants

like Reliance Retail Ltd and Wal Mart are going to enter the market soon. Even rural areas will

provide a huge opportunity to be explored.

COMPANY PROFILE

Pantaloon Retail (India) Limited, is India‟s leading retailer that operates multiple retail formats

in both the value and lifestyle segment of the Indian consumer market. Headquartered in

Mumbai (Bombay), the company operates over 10 million square feet of retail space, has over

1000 stores across 61 cities in India and employs over 30,000 people.

The company‟s leading formats include Pantaloons, a chain of fashion outlets, Big Bazaar, a

uniquely Indian hypermarket chain, Food Bazaar, a supermarket chain, blends the look, touch

and feel of Indian bazaars with aspects of modern retail like choice, convenience and quality and

Central, a chain of seamless destination malls. Some of its other formats include, Depot, Shoe

Factory, Brand Factory, Blue Sky, Fashion Station, all, Top 10, m Bazaar and Star and Sitara.

The company also operates an online portal, futurebazaar.com.A subsidiary company, Home

Solutions Retail (India) Limited, operates Home Town, a large-format home solutions store,

Collection i, selling home furniture products and E-Zone focused on catering to the consumer

electronics segment.

Pantaloon Retail was recently awarded the International Retailer of the Year 2007 by the US-

based National Retail Federation (NRF) and the Emerging Market Retailer of the Year 2007 at

the World Retail Congress held in Barcelona. Pantaloon Retail is the flagship company of

Future Group, a business group catering to the entire Indian consumption space.

Future Group is one of the country‟s leading business groups present in retail, asset

management, consumer finance, insurance, retail media, retail spaces and logistics. The group‟s

flagship company, Pantaloon Retail (India) Limited operates over 10 million square feet of retail

space, has over 1,000 stores and employs over 30,000 people.

Future Group is present in 61 cities and 65 rural locations in India. Some of its leading retail

formats include, Pantaloons, Big Bazaar, Central, Food Bazaar, Home Town, e Zone, Depot,

Future Money and online retail format, futurebazaar.com

Future Group companies includes, Future Capital Holdings, Future Generally India Indus

League Clothing and Galaxy Entertainment that manages Sports Bar, Brew Bar and Bowling Co.

Future Capital Holdings, the group‟s financial arm, focuses on asset management and consumer

credit. It manages assets worth over $1 billion that are being invested in developing retail real

estate and consumer-related brands and hotels.

The group‟s joint venture partners include Italian insurance major, Generally, French retailer

ETAM group, US-based stationary products retailer, Staples Inc and UK-based Lee Cooper and

India-based Talwalkar‟s, Blue Foods and Liberty Shoes.

Future Group‟s vision is to, “deliver Everything, Everywhere, Every time to Every Indian

Consumer in the most profitable manner.” The group considers „Indian-ness‟ as a core value and

its corporate credo is - Rewrite rules, Retain values.

Futurebazaar.com is owned and operated by Future Bazaar India Ltd., a subsidiary of

Pantaloon Retail (India) Limited.

Future Group Manifesto:

“Future” – the word which signifies optimism, growth, achievement, strength, beauty, rewards

and perfection. Future encourages us to explore areas yet unexplored, write rules yet unwritten;

create new opportunities and new successes. To strive for a glorious future brings to us our

strength, our ability to learn, unlearn and re-learn our ability to evolve.

We, in Future Group, will not wait for the Future to unfold itself but create_futurescenarios in

the consumer space and facilitate consumption because consumption is development. Thereby,

we will effect socio-economic development for our customers, employees, shareholders,

associates and partners.

Our customers will not just get what they need, but also get them where, how and when they

need. We will not just post satisfactory results, we will write success stories. We will not just

operate efficiently in the Indian economy, we will evolve it.

We will not just spot trends; we will set trends by marrying our understanding of the Indian

consumer to their needs of tomorrow.

It is this understanding that has helped us succeed. And it is this that will help us succeed in the

Future. We shall keep relearning. And in this process, do just one thing.

Rewrite Rules and Retain Values

Group Vision:

Future Group shall deliver Everything, Everywhere, Every time for Every Indian Consumer in

the most profitable manner.

Group Mission:

We share the vision and belief that our customers and stakeholders shall be served only by

creating and executing future scenarios in the consumption space leading to economic

development.

We will be the trendsetters in evolving delivery formats, creating retail realty, making

consumption affordable for all customer segments – for classes and for masses.

We shall infuse Indian brands with confidence and renewed ambition. We shall be efficient, cost-

conscious and committed to quality in whatever we do.

We shall ensure that our positive attitude, sincerity, humility and united determination shall be

the driving force to make us successful.

Core Values:

Indianness: confidence in ourselves.

Leadership: to be a leader, both in thought and business.

Respect & Humility: to respect every individual and be humble in our conduct.

Introspection: leading to purposeful thinking.

Openness: to be open and receptive to new ideas, knowledge and information.

Valuing and Nurturing Relationships: to build long term relationships.

Simplicity & Positivity: Simplicity and positivity in our thought, business and action.

Adaptability: to be flexible and adaptable, to meet challenges.

Flow: to respect and understand the universal laws of nature.

Lines of Business

E-TAILING

FOOD

BOOKS/MUSIC

FASHION

TELECOM/IT

HOME/ELECTRONICS

GENERAL MERCHANDISE

LEISURE/ENTERTAINMENT

Stock Information

Listed on: Bombay Stock Exchange

Stock Code: BOM:523574

Company Timeline

Major Milestones

1987: Company incorporated as Manz wear Private Limited. Launch of Pantaloons, India‟s first

formal trouser brand.

1991: Launch of BARE, the Indian Jeans brand.

1992: Initial public offer(IPO) was made in the month of May.

1994; The Pantaloon Shoppe – an exclusive men‟s wear store in franchise format launched

across the nation. The company starts the distribution of branded garments through multi brand

retail outlets across the nation.

1995: John Miller – Formal shirt brand launched.

1997: Company enters modern retail with the launch of the first 8000 square feet store,

Pantaloons in Kolkata.

2001: Three Big Bazaar stores launched within a span of 22 days in Kolkata, Bangalore and

Hyderabad.

2002: Food Bazaar, the supermarket chain was launched.

2004: Central – India‟s first seamless mall was launched in Bangalore.

2005 :Group moves beyond retail, acquires stakes in Galaxy Entertainment, Indus League

Clothing and Planet Retail. Sets up India‟s first real estate investment fund Kshitij to build a

chain of shopping malls.

2006; Future Capital Holdings, the company‟s financial is formed to manage over $ 1.5 billion in

real estate, private equity and retail infrastructure funds. Plans forays into retaining of consumer

finance products.

Home Town, a home building and improvement products retail chain was launched along

with consumer durables format, E zone and furniture chain, Furniture Bazaar.

Future group enters into joint venture agreements to launch insurance products with

Italian insurance major, Generali.

Forms joint ventures with US office stationery retailer, staples.

2007 Future Group crosses $1billion mark.

Specialized companies in retail media, logistics, IPR, and brand development and retailed

technology services become operational.

Pantaloon retail wins the International retailer of the year at US- based National Retail

Federation convention in New York and Emerging Retailer of the year award at the

World Retain Congress held in Barcelona.

Futurebazaar.com becomes India‟s most popular shopping portal.

2008 Future Capital Holdings becomes the second group company to make a successful Initial

Public Offering in the Indian capital markets.

Big Bazaar crosses the 100 store mark, marking one of the fastest ever expansion of a

Hypermarket anywhere in the world.

Total operational retail space crosses 10 million square feet mark.

Future Group acquires rural retail chain, Aadhar present in 65 rural locations

Big Bazaar:

Big Bazaar is a chain of department stores in India, currently with 92 stores. It is owned by

the Pantaloon Retail India Ltd, Future Group. It works on the same economy model as Wal-Mart

and has considerable success in many Indian cities and small towns.

The goods are supplied from the Bangalore branch of Big Bazaar. The Big Bazaar, Chennai

branch consists of 200 employees. It has 19 departments.

The functional areas in Big Bazaar are Human resource, marketing, IT, admin, commercial,

tailoring and logistics.

The departments are given below.

Medicine bazaar (thulasi)

NBD(glasses,watches,car accessories,helmet,cosmetics)

Mobile bazaar

Men‟s wear

Women‟s wear

Kids wear

Foot wear

Luggage‟s

Electronics bazaar

Furniture‟s

Home linen& Home décor

Depot

Crockery

Utensils

Future money

Plastics

Toys

Food Bazaar

Customer service desk

The sales persons working there are well trained to serve the customers. They are getting

promotion as team leader for their best performance with increase in salary and incentives are

also given. Employee discount cards are given to every employee for their purchasing in Big

Bazaar.

The idea was pioneered by entrepreneur Kishore Biyani, the CEO of Future Group.

It is the biggest and the fastest growing chain of department store and aims to have 150 by June

2009 and 350 stores by the end of year 2010. Currently Big Bazaar stores are located only in

India.

Big Bazaar is not just another hypermarket. It caters to every need of a family. Where Big

Bazaar scores over other stores is its value for money proposition for the Indian consumers.

At Big Bazaar, we can get the best products at the best prices - that‟s what they guarantee.

With the ever increasing array of private labels, it has opened the doors into the world of fashion

and general merchandise including home furnishings, utensils, crockery, cutlery, sports goods

and much more at prices that will surprise you. And this is just the beginning. Big Bazaar plans

to add much more to complete your shopping experience.

Many Big Bazaar stores have a grocery department and vegetable section called the Food

Bazaar. Big Bazaar stores in Metros have a gaming area and kids' play area for entertainment.

These have proven to be very popular as a hang-out area for people of all age groups.

Board of Directors:

Kishore Biyani is the Managing Director of Pantaloon Retail (India) Limited and the Group

Chief Executive Officer of Future Group. He has led Pantaloon Retail‟s emergence as the India‟s

leading retailer operating multiple retail formats that now cater to almost the consumption basket

of a large section of Indian consumers.

Kishore Biyani led the company‟s foray into organized retail with the opening up of the

Pantaloons family store in 1997. This was followed in 2001 with the launch of Big Bazaar, a

uniquely Indian hypermarket format that democratized shopping in India. It blends the look,

touch and feel of Indian bazaars with aspects of modern retail like choice, convenience and

quality. This was followed by a number of other formats including Food Bazaar, Central and

Home Town.

The year, 2006 marked the evolution of Future Group, that brought together the multiple

initiatives taken by group companies in the areas of Retail, Brands, Space, Capital, Logistics and

Media. Kishore Biyani advocates „Indianness‟ as the core value driving the group. The group‟s

corporate credo is „Rewrite Rules, Retain Values.‟

Kishore Biyani was awarded the Ernst & Young Entrepreneur of the Year 2006 in the Services

Sector and the Lakshmipat Singhania - IIM Lucknow Young Business Leader Award by Prime

Minister, Dr. Manmohan Singh in 2006. He was also awarded the CNBC First Generation

Entrepreneur of the Year 2006.

Kishore Biyani was born in August, 1961 and is married to Sangita and they have two

daughters. He recently authored a book, „It Happened In India‟ that captures his entrepreneurial

journey and the growth of modern retailing in India.

Mr. Gopikishan Biyani – Wholetime Director

Mr. Rakesh Biyani – Wholetime Director

Mr. Ved Prakash Arya – Director

Mr. Shailesh Haribhakti – Independent Director

Mr. S. Doreswamy – Independent Director

Dr. D.O. Koshy – Independent Director

Ms. Anju Poddar – Independent Director

Ms. Bala Deshpande – Independent Director

Mr. Anil Harish – Independent Director

Awards and Recognition:

Coca-Cola Golden Spoon Awards 2008

Most Admired Food & Grocery Retail Visionary of the Year: Kishore Biyani

Most Admired Food & Grocery Retailer of the Year – Supermarkets: Food Bazaar

Most Admired Food & Grocery Retailer of the Year - Hypermarkets: Big Bazaar

Most Admired Retailer of the Year - Dynamic Growth in Network Expansion across

Food, Beverages & Grocery: Future Group

Most Admired Food & Grocery Retailer of the Year - Consumer's Choice: Big Bazaar

Coca-Cola Golden Spoon Awards 2008, were given away for the first time as a culmination of

the „Food Forum India 2008‟ – a two day convention which saw the participation of leading

brands, retailers & retail support organizations from across the globe. The awards were presented

to honour enterprise, innovation and achievement in the food retailing business as a benchmark

of excellence.

The Reid & Taylor Awards For Retail Excellence 2008

Retail Leadership Award: Kishore Biyani

Retail Best Employer of the Year: Future Group

Retailer of The Year: Home Products and Office Improvements: HomeTown

The Reid & Taylor Awards for Retail Excellence are an important feature of the Asia Retail

Congress - Asia‟s single most important global platform to promote world-class retail practices -

and are aimed at honouring the best, in Asian Retail scenario. India played host to Asia Retail

Congress 2008.

DATA ANALYSIS

AND

INTERPRETATION

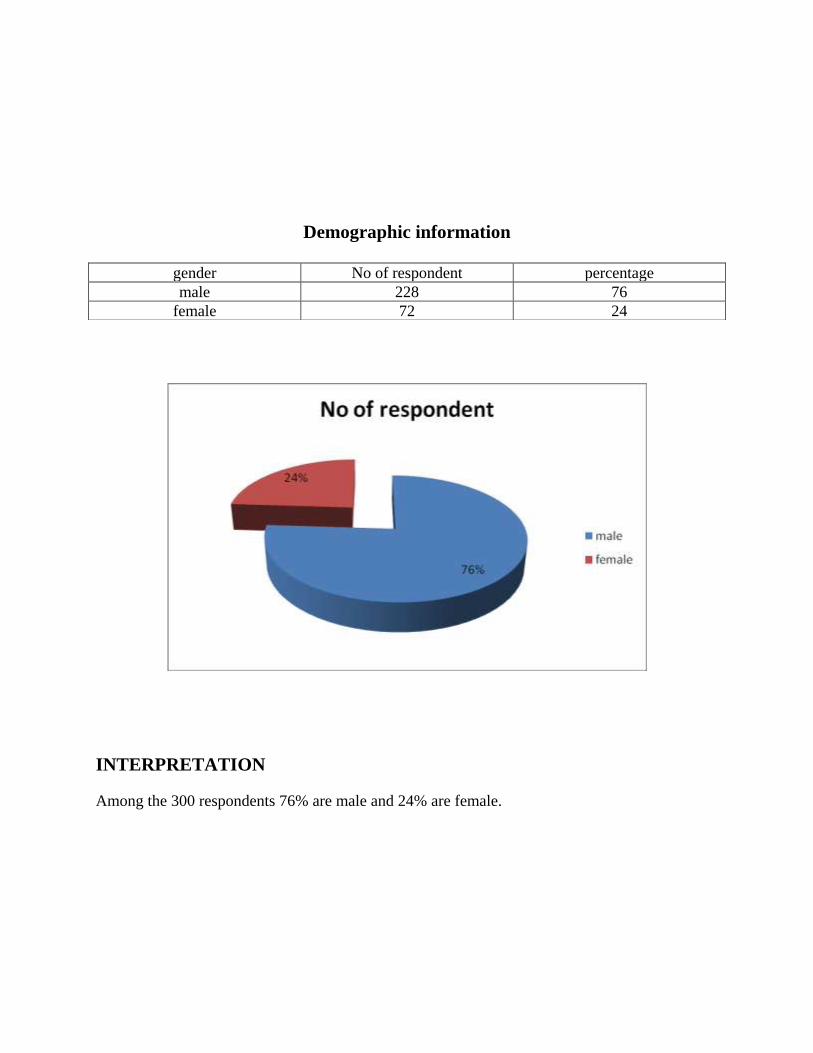

Demographic information

INTERPRETATION

Among the 300 respondents 76% are male and 24% are female.

gender No of respondent percentage

male 228 76

female 72 24

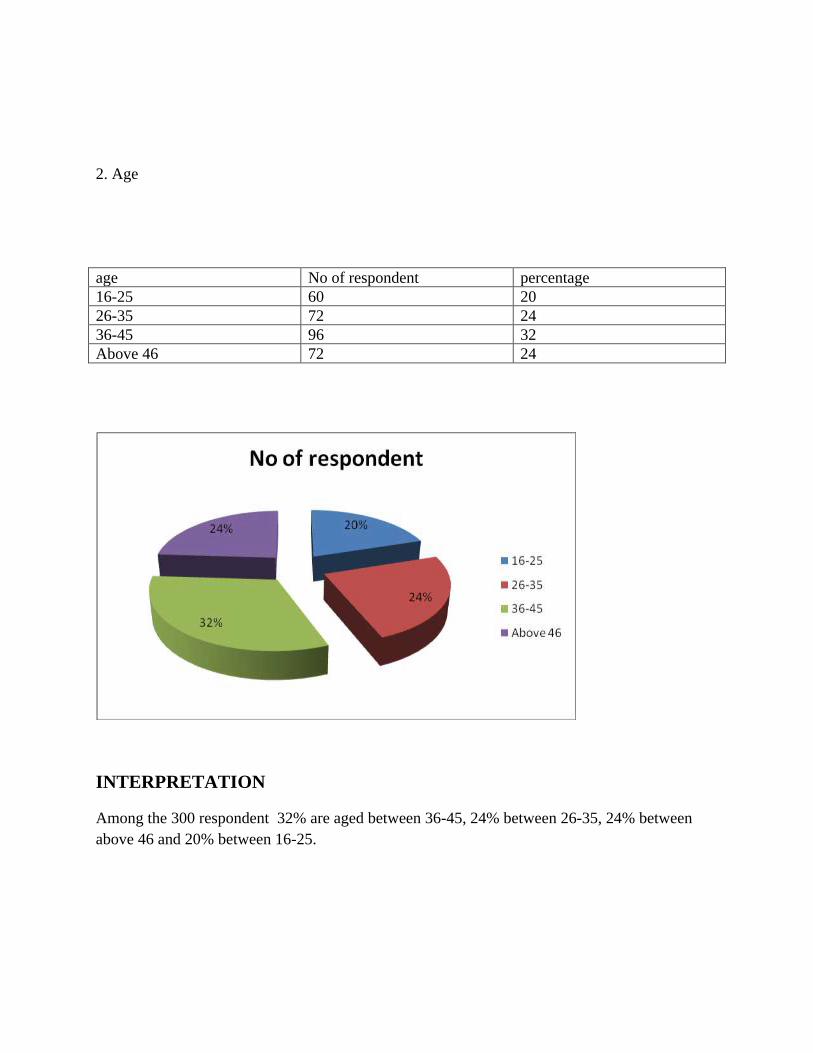

2. Age

age No of respondent percentage

16-25 60 20

26-35 72 24

36-45 96 32

Above 46 72 24

INTERPRETATION

Among the 300 respondent 32% are aged between 36-45, 24% between 26-35, 24% between

above 46 and 20% between 16-25.

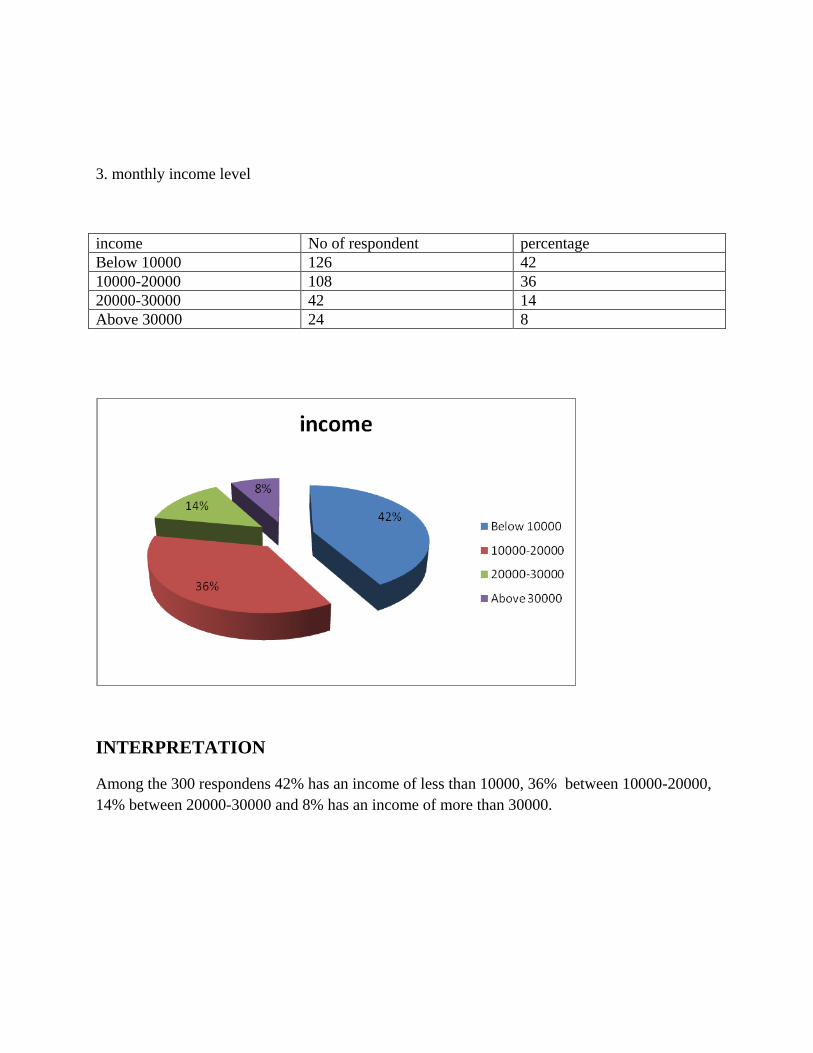

3. monthly income level

income No of respondent percentage

Below 10000 126 42

10000-20000 108 36

20000-30000 42 14

Above 30000 24 8

INTERPRETATION

Among the 300 respondens 42% has an income of less than 10000, 36% between 10000-20000,

14% between 20000-30000 and 8% has an income of more than 30000.

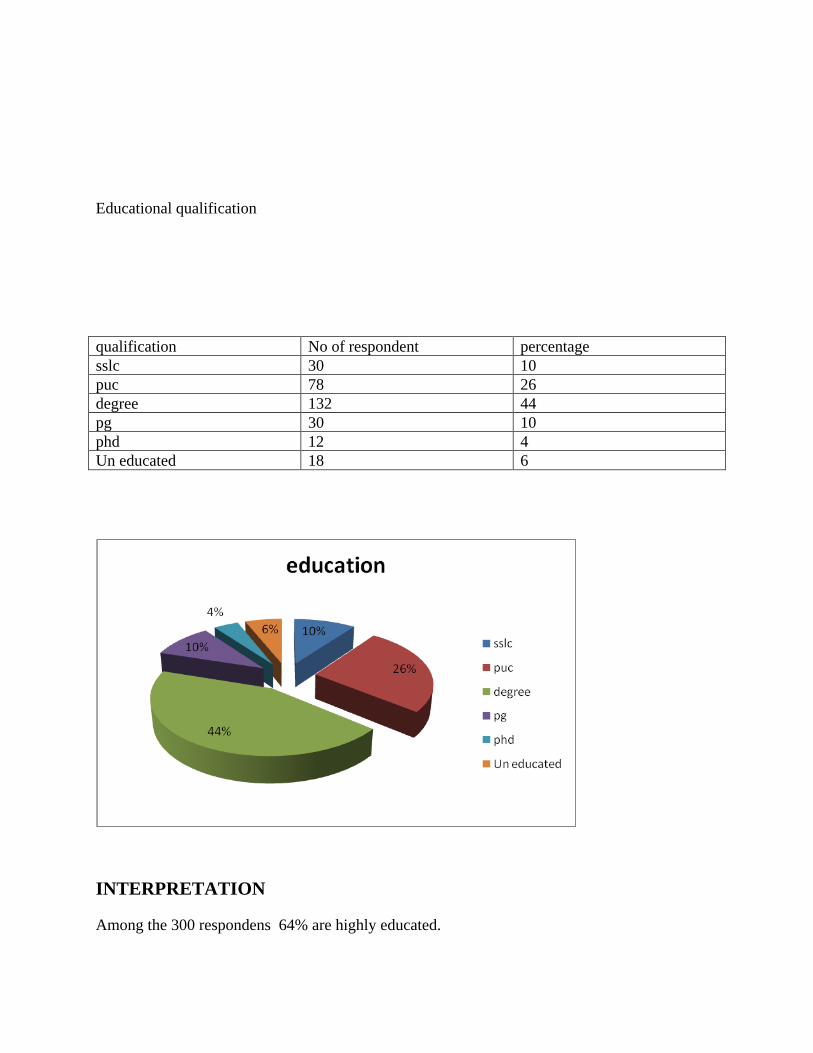

Educational qualification

qualification No of respondent percentage

sslc 30 10

puc 78 26

degree 132 44

pg 30 10

phd 12 4

Un educated 18 6

INTERPRETATION

Among the 300 respondens 64% are highly educated.

Questions

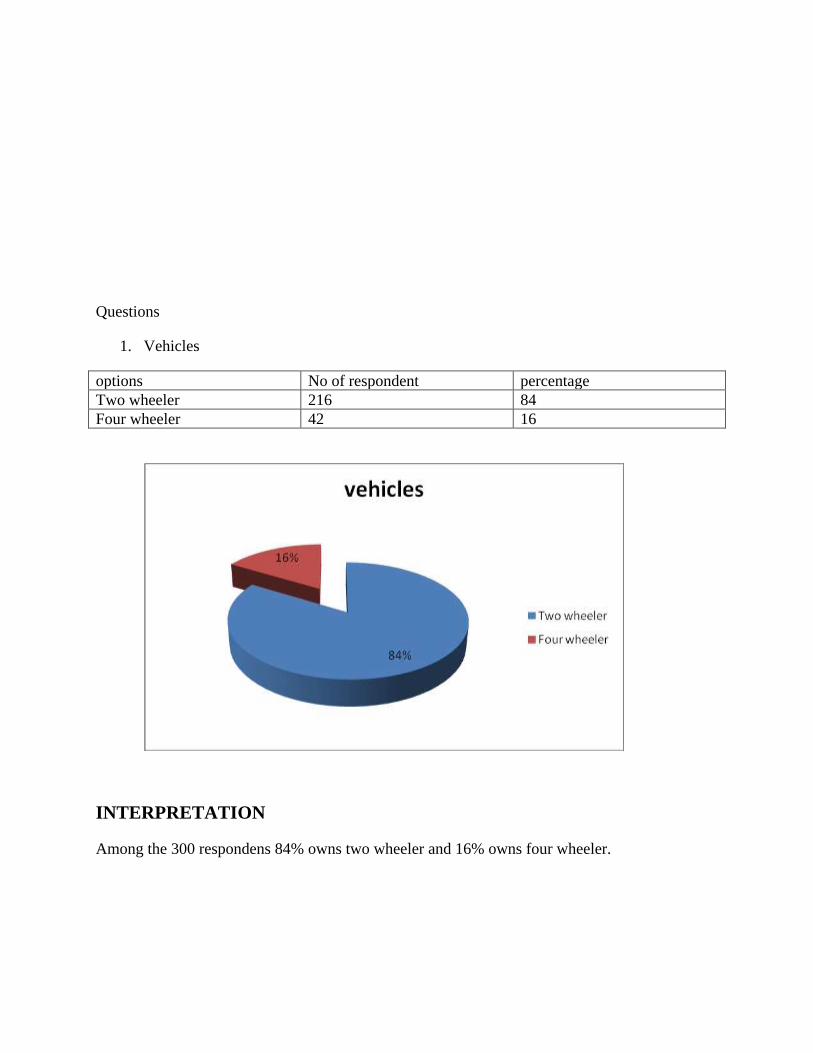

1. Vehicles

options No of respondent percentage

Two wheeler 216 84

Four wheeler 42 16

INTERPRETATION

Among the 300 respondens 84% owns two wheeler and 16% owns four wheeler.

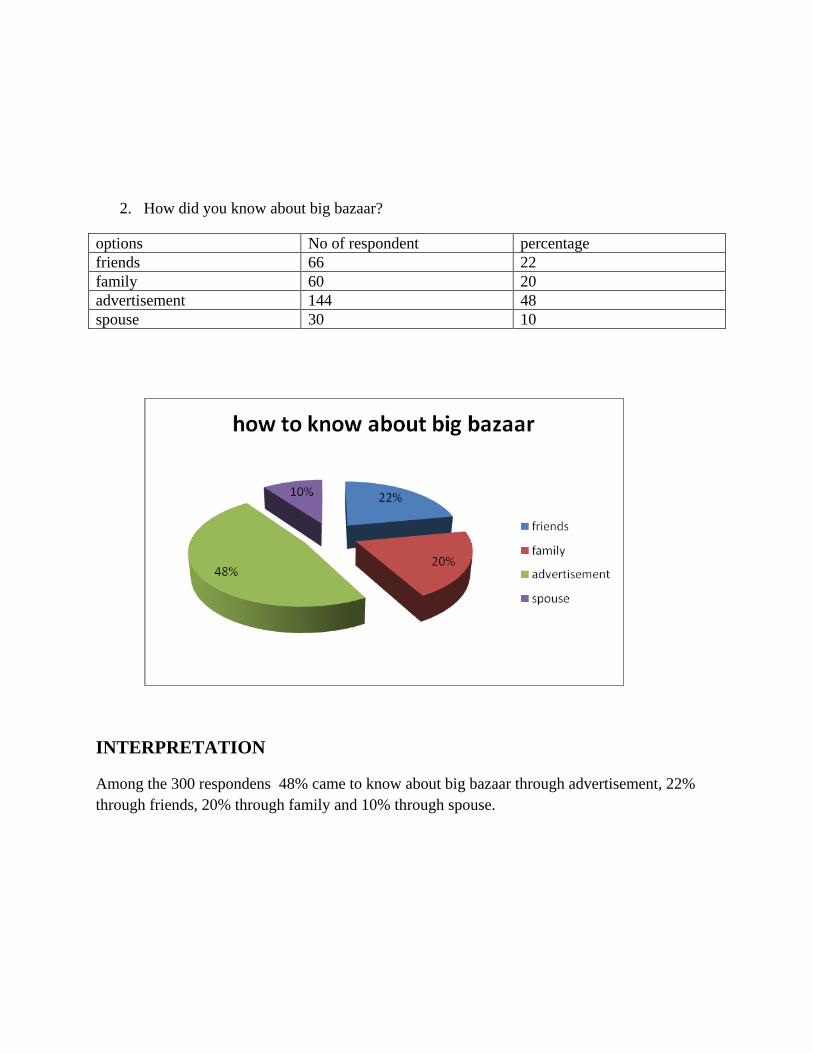

2. How did you know about big bazaar?

options No of respondent percentage

friends 66 22

family 60 20

advertisement 144 48

spouse 30 10

INTERPRETATION

Among the 300 respondens 48% came to know about big bazaar through advertisement, 22%

through friends, 20% through family and 10% through spouse.

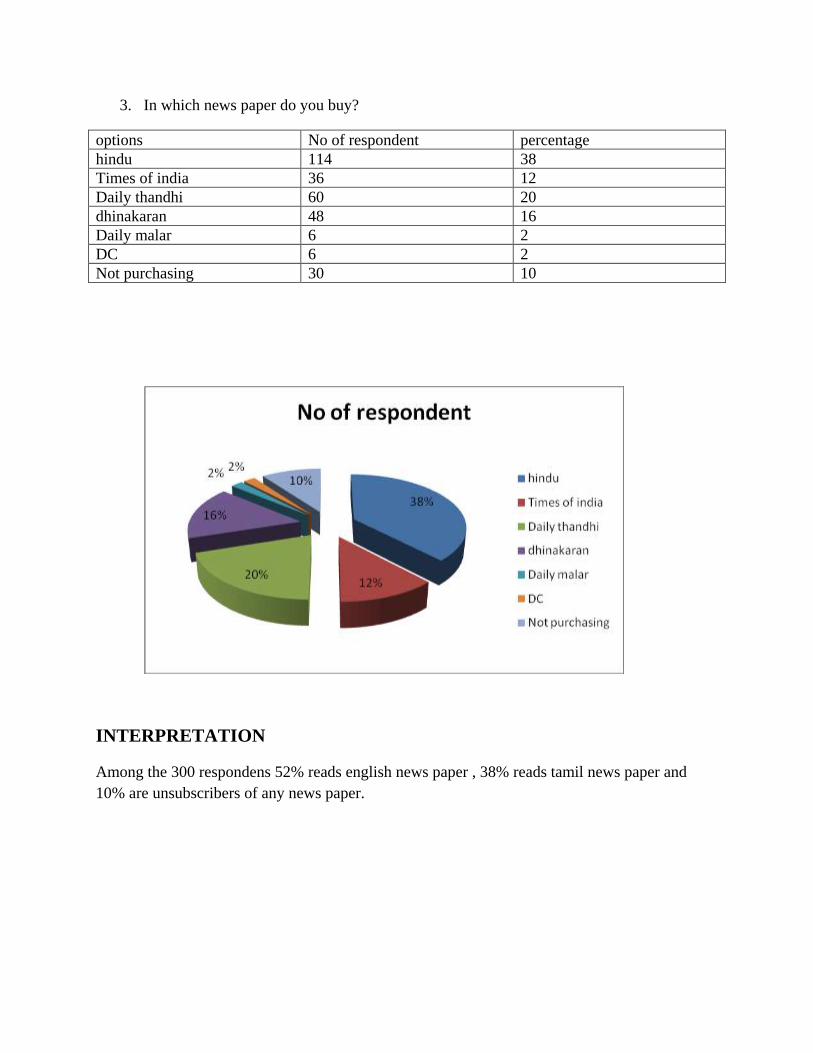

3. In which news paper do you buy?

options No of respondent percentage

hindu 114 38

Times of india 36 12

Daily thandhi 60 20

dhinakaran 48 16

Daily malar 6 2

DC 6 2

Not purchasing 30 10

INTERPRETATION

Among the 300 respondens 52% reads english news paper , 38% reads tamil news paper and

10% are unsubscribers of any news paper.

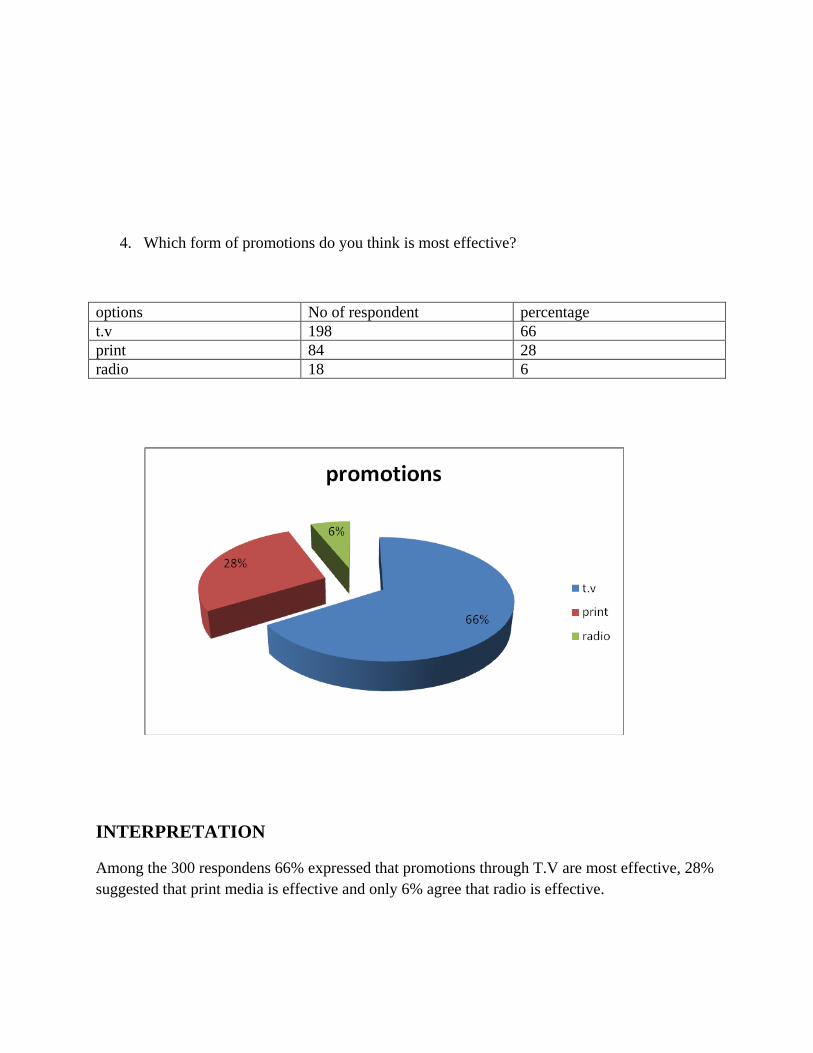

4. Which form of promotions do you think is most effective?

options No of respondent percentage

t.v 198 66

print 84 28

radio 18 6

INTERPRETATION

Among the 300 respondens 66% expressed that promotions through T.V are most effective, 28%

suggested that print media is effective and only 6% agree that radio is effective.

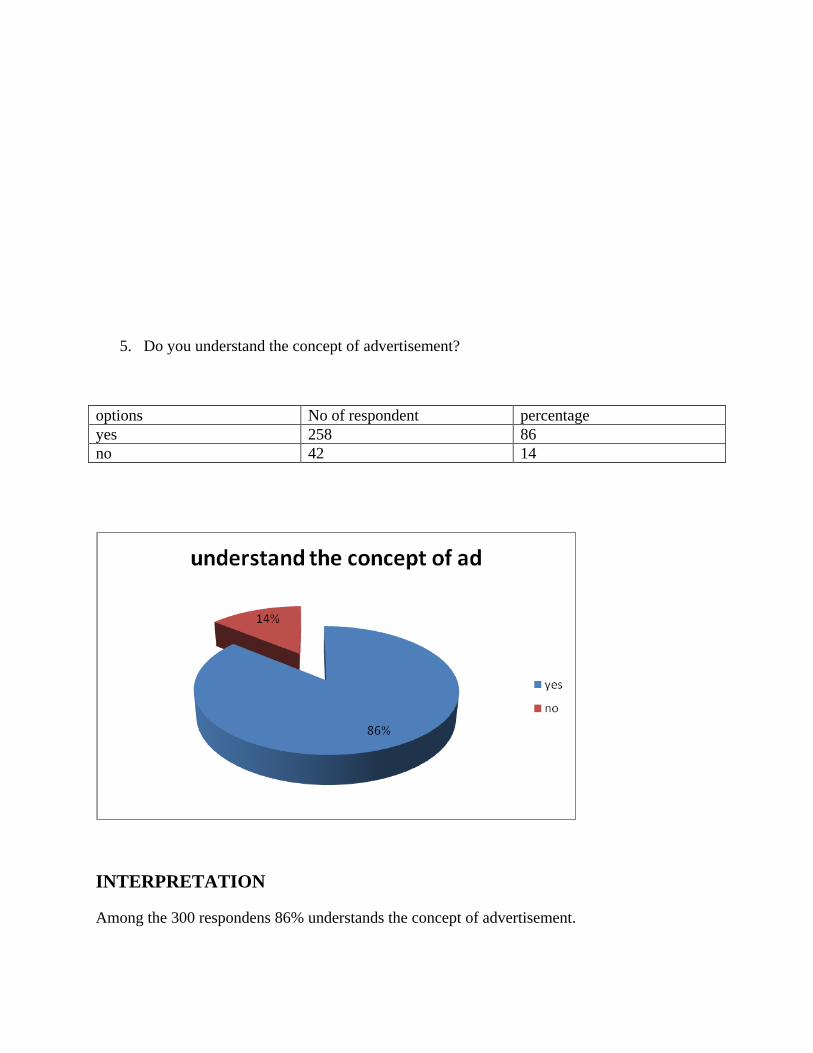

5. Do you understand the concept of advertisement?

options No of respondent percentage

yes 258 86

no 42 14

INTERPRETATION

Among the 300 respondens 86% understands the concept of advertisement.

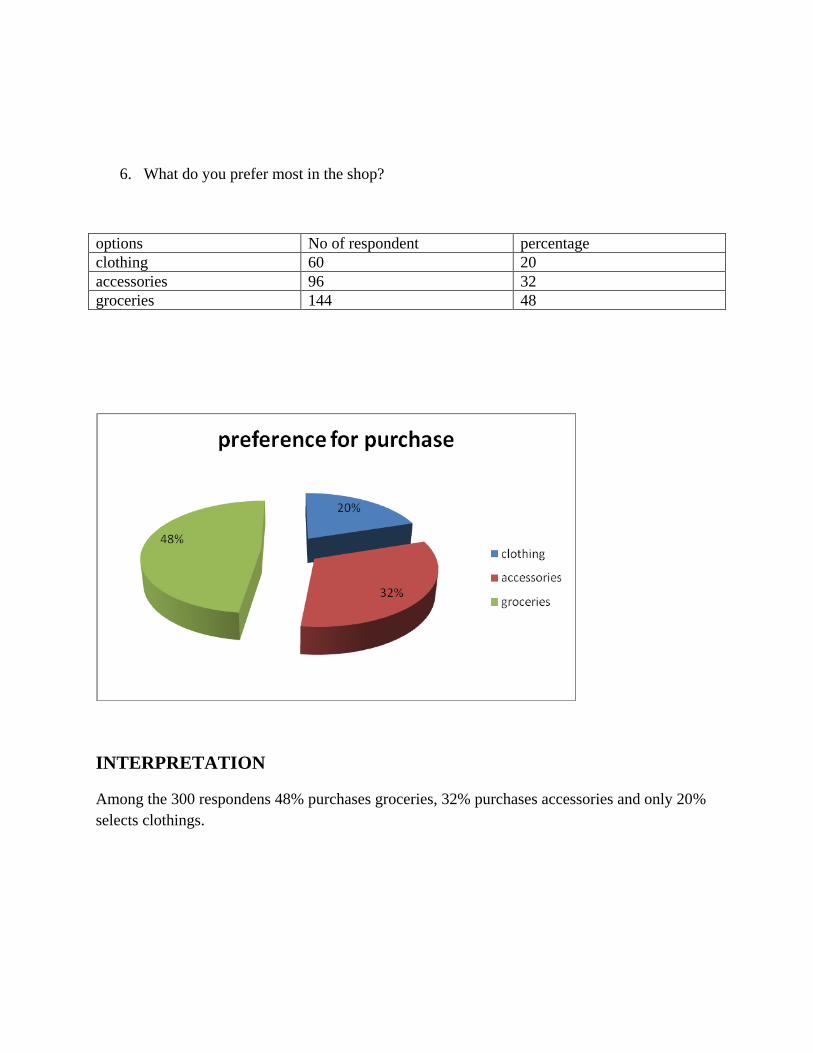

6. What do you prefer most in the shop?

options No of respondent percentage

clothing 60 20

accessories 96 32

groceries 144 48

INTERPRETATION

Among the 300 respondens 48% purchases groceries, 32% purchases accessories and only 20%

selects clothings.

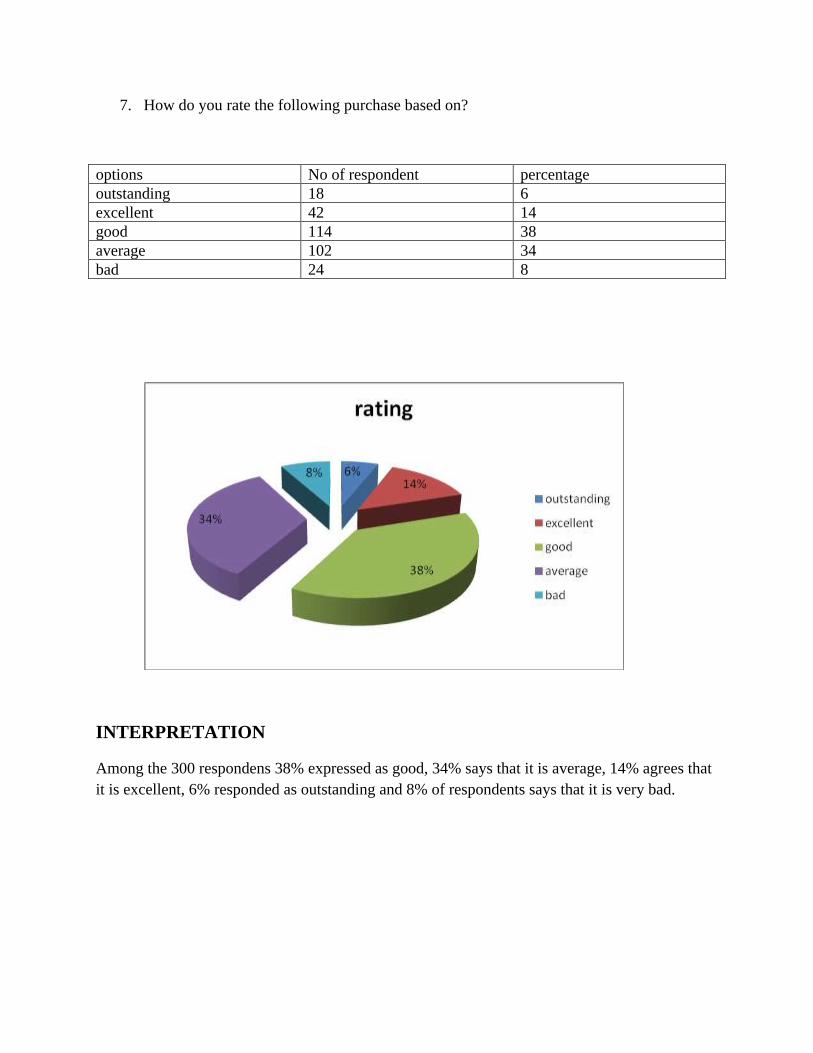

7. How do you rate the following purchase based on?

options No of respondent percentage

outstanding 18 6

excellent 42 14

good 114 38

average 102 34

bad 24 8

INTERPRETATION

Among the 300 respondens 38% expressed as good, 34% says that it is average, 14% agrees that

it is excellent, 6% responded as outstanding and 8% of respondents says that it is very bad.

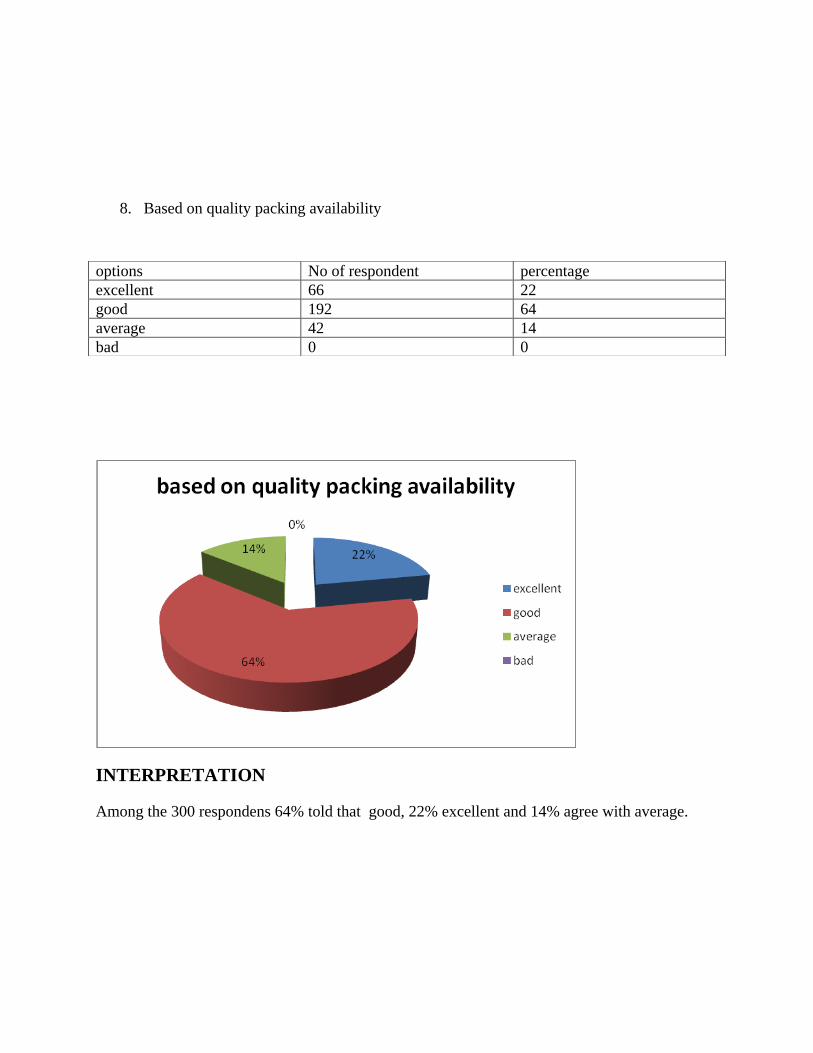

8. Based on quality packing availability

INTERPRETATION

Among the 300 respondens 64% told that good, 22% excellent and 14% agree with average.

options No of respondent percentage

excellent 66 22

good 192 64

average 42 14

bad 0 0

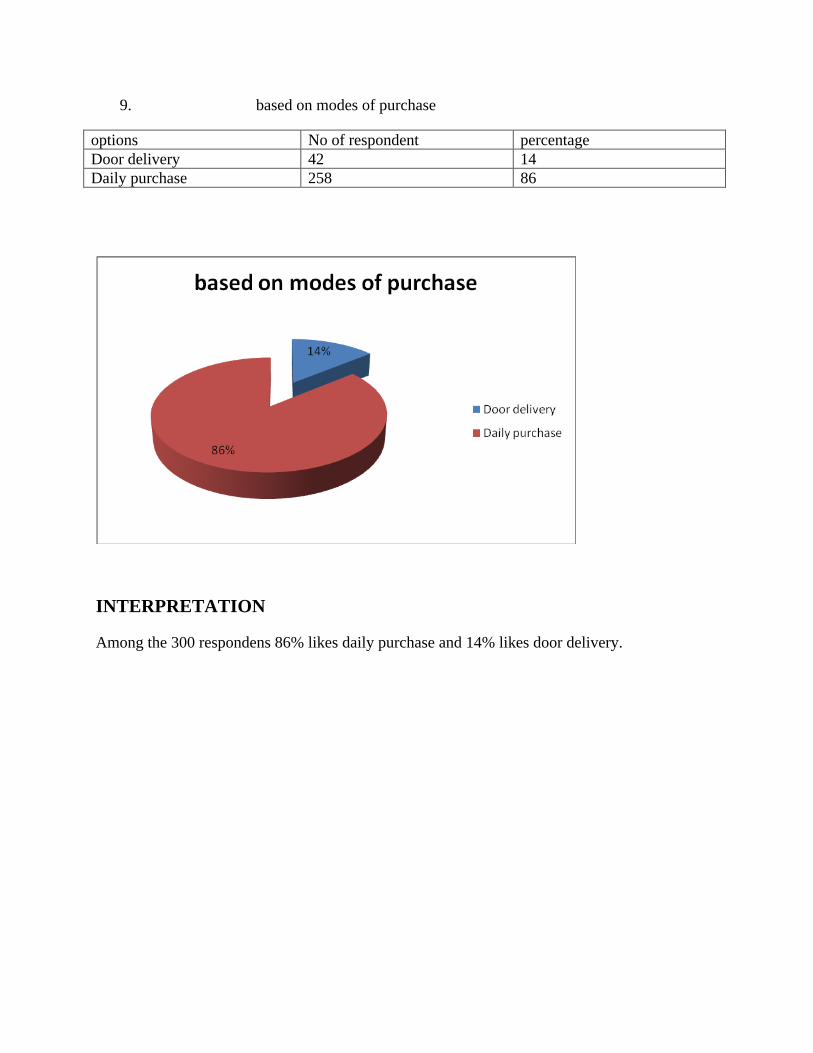

9. based on modes of purchase

options No of respondent percentage

Door delivery 42 14

Daily purchase 258 86

INTERPRETATION

Among the 300 respondens 86% likes daily purchase and 14% likes door delivery.

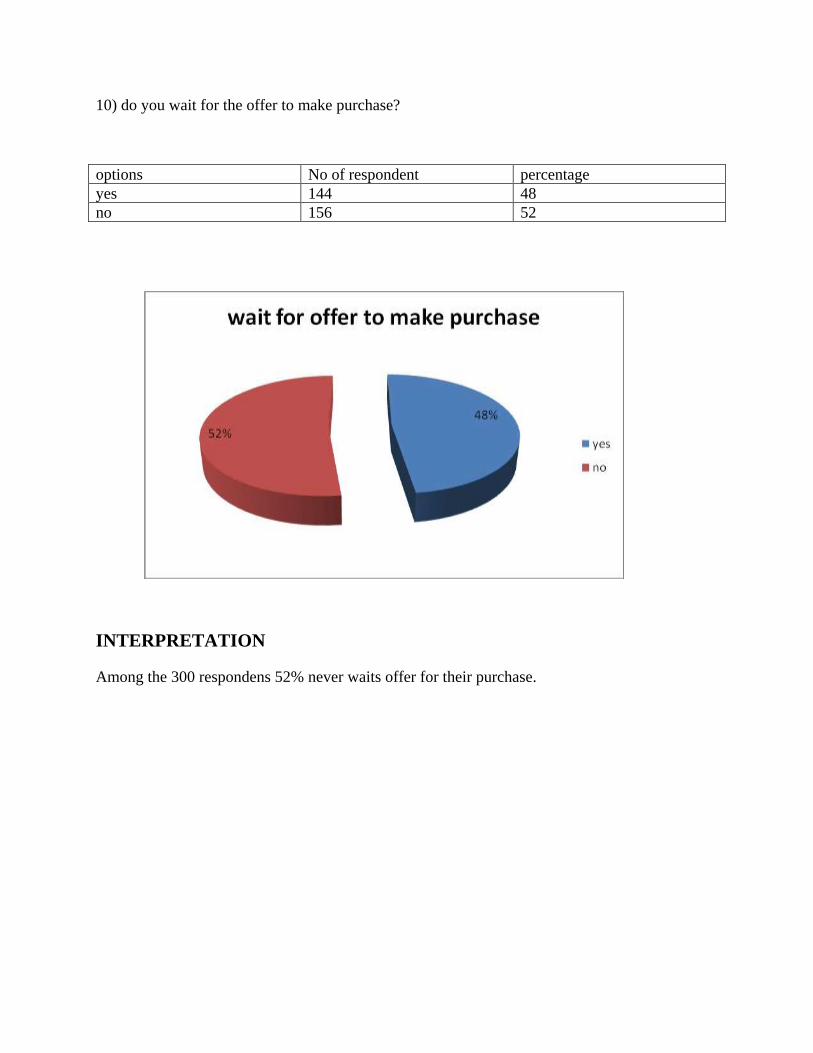

10) do you wait for the offer to make purchase?

options No of respondent percentage

yes 144 48

no 156 52

INTERPRETATION

Among the 300 respondens 52% never waits offer for their purchase.

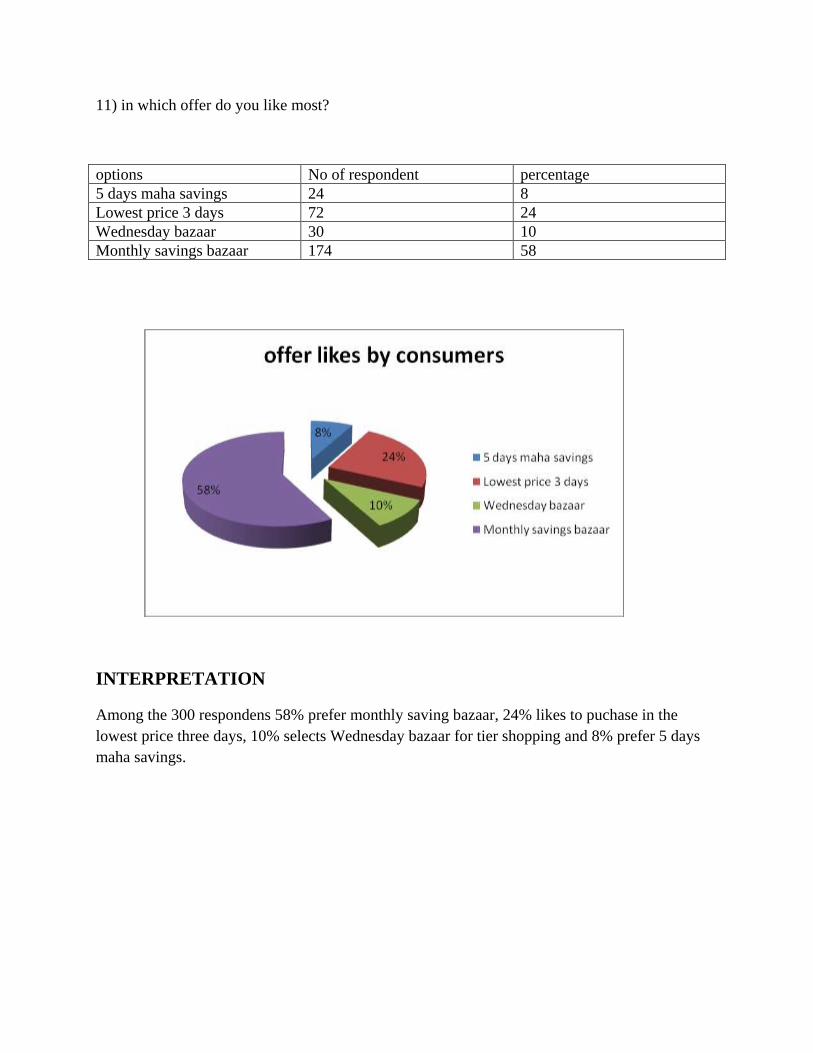

11) in which offer do you like most?

options No of respondent percentage

5 days maha savings 24 8

Lowest price 3 days 72 24

Wednesday bazaar 30 10

Monthly savings bazaar 174 58

INTERPRETATION

Among the 300 respondens 58% prefer monthly saving bazaar, 24% likes to puchase in the

lowest price three days, 10% selects Wednesday bazaar for tier shopping and 8% prefer 5 days

maha savings.

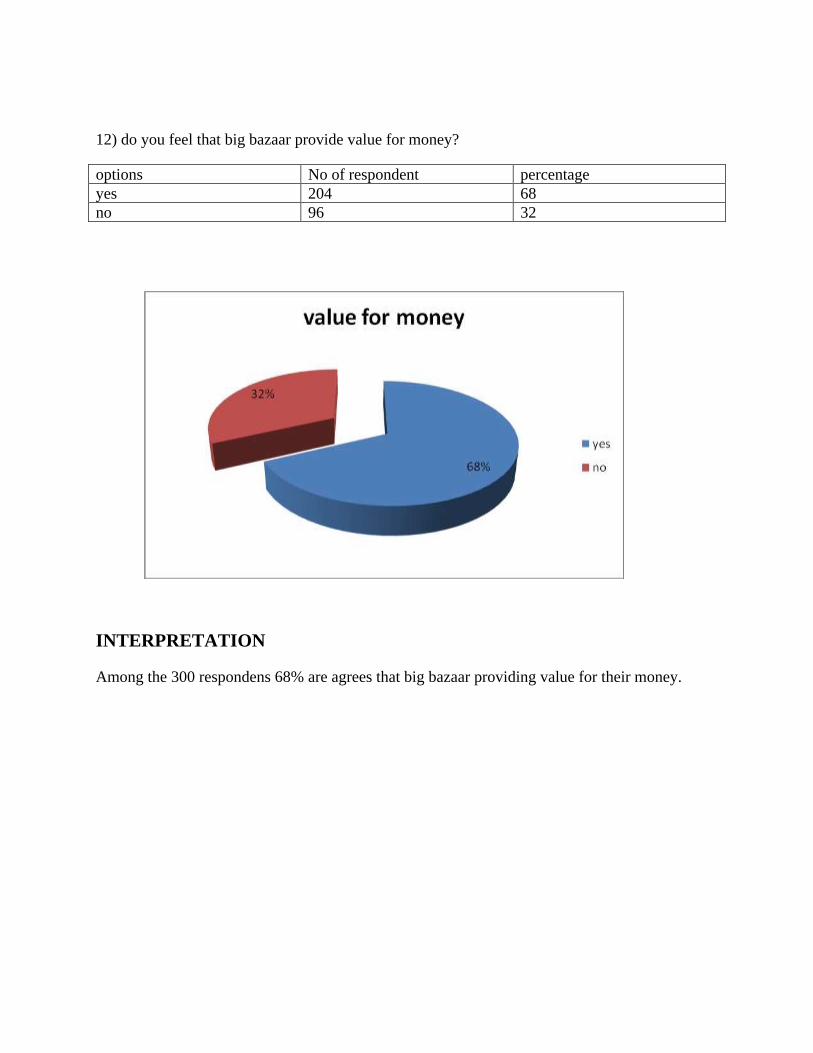

12) do you feel that big bazaar provide value for money?

options No of respondent percentage

yes 204 68

no 96 32

INTERPRETATION

Among the 300 respondens 68% are agrees that big bazaar providing value for their money.

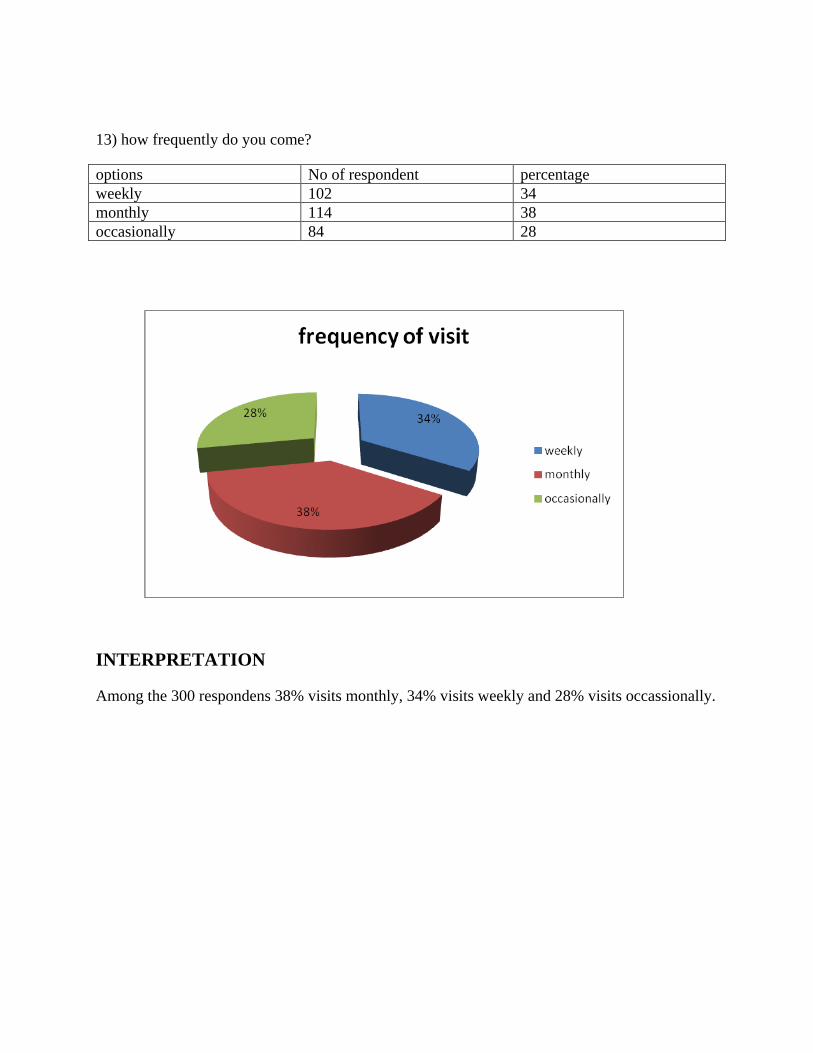

13) how frequently do you come?

options No of respondent percentage

weekly 102 34

monthly 114 38

occasionally 84 28

INTERPRETATION

Among the 300 respondens 38% visits monthly, 34% visits weekly and 28% visits occassionally.

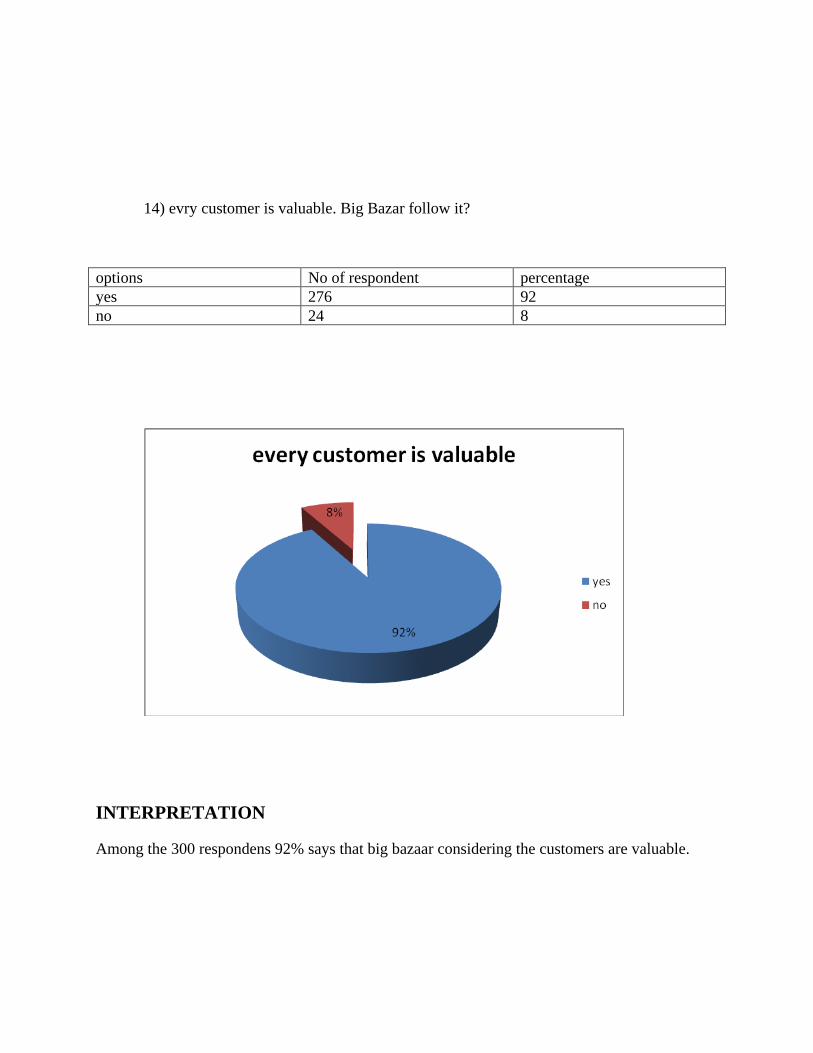

14) evry customer is valuable. Big Bazar follow it?

options No of respondent percentage

yes 276 92

no 24 8

INTERPRETATION

Among the 300 respondens 92% says that big bazaar considering the customers are valuable.

FINDINGS

Majority of the customers are male

Most of the people visiting big bazaar comes the age of between 36-45

The highest numbers of people have less than an income of 10000.

Majority of the people are highly educated

Most of the respondents own a two wheeler.

The highest number of people came to know about big bazaar through

advertisement

Majority of the people read English news paper

Most of the people likes promotion through television

Most of the respondents are able to understand the concept of advertisement.

The highest number of people purchasing groceries from big bazaar

Most of the people rate big bazaar as a good retail shop

Most of the respondents likes interactive purchase

Majority of the respondents never waits for offer to make purchase

Large number of people likes the monthly savings bazaar.

The highest number of people agrees that big bazaar providing value for their

money

Most of the people visits big bazaar on a monthly basis

Majority of the consumers are satisfied by the service provided by big bazaar.

SUGGESTIONS

Increase the advertisement

Include route map to big bazaar Royapuram in pamphlets, hoardings and

boards.

Reduce the price of apparels and include more models

Include some branded products especially in apparels

Encourage the customer service

Convey the offers regularly to customers and provoke them to visit the

store regularly

Arrange a bus stop in front of the store, because the nearest bus stops are

too far from the store.

![Customer Satisfaction Level in a Retail Outlet With Reference to Big Bazaar Research Report[1]](https://static.documents.pub/doc/80x56/577cdd881a28ab9e78ad3899/customer-satisfaction-level-in-a-retail-outlet-with-reference-to-big-bazaar.jpg)