24

1 Cocoa Sector Overview Risks and Opportunities as an introduction to: Managing Risk in Côte d’Ivoire’s Cocoa Sector ARD Week 2009 Peter van Grinsven, Mars Incorporated

1

Cocoa Sector Overview Risks and Opportunities

as an introduction to: Managing Risk in Côte d’Ivoire’s Cocoa Sector

ARD Week 2009 Peter van Grinsven, Mars Incorporated

2

Contents of Presentation General • Mars Incorporated • Chocolate Market and Market Outlook, Cocoa Price History • Price Risk Management by Industry • Cocoa Production and Shifts of Production • The Importance of Cocoa to various producing countries

Cocoa Sustainability: • Awareness of Risk of Availability (Supply) in addition to Price Risk • Identify Supply Challenges and Solutions through use of

appropriate Science, capacity building and Pilot Programs conducted in “farmers’ fields”

• Develop Key Partnerships

3

Introduction of Mars Incorporated Mars Incorporated is a family owned business that was founded in the USA in

1911 and we are a world leader in branded Snack foods, Main meal and Pet care products

Today, Mars Incorporated is a US$25 billion business operating in over 70 countries with 60,000 associates and 120 factories

Throughout our history the business has been guided by the Five Principles of Mars: Quality Responsibility Mutuality Efficiency Freedom

Mars Incorporated and Cocoa Sustainability: for Mars, cocoa beans are a key raw material and supply of affordable, good quality cocoa beans is important

Mars commits itself to help bring about necessary changes to transform the cocoa sector into a sustainable industry, focusing on economic, social and environmental wellbeing of all stakeholders

4

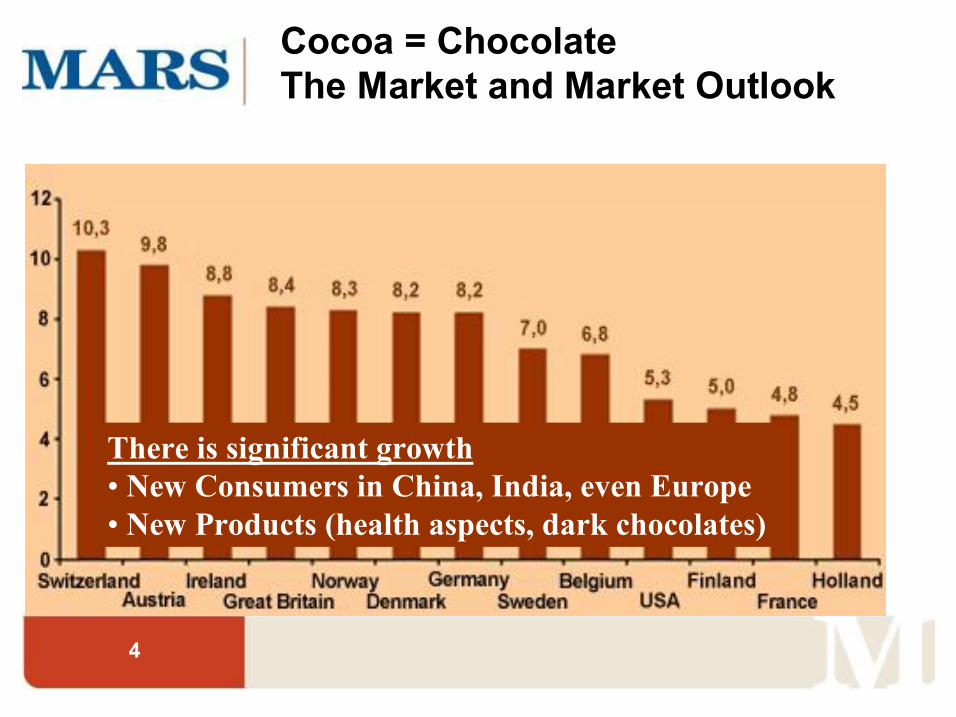

Cocoa = Chocolate The Market and Market Outlook

There is significant growth • New Consumers in China, India, even Europe • New Products (health aspects, dark chocolates)

5

Cocoa Prices: History 1979 – 2008 London Market

•Prices fluctuate •Long term price trend is rather flat

6

Monthly Average NY Cocoa 2nd Futures Price

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000 195301

195408

195603

195710

195905

196012

196207

196402

196509

196704

196811

197006

197201

197308

197503

197610

197805

197912

198107

198302

198409

198604

198711

198906

199101

199208

199403

199510

199705

199812

200007

200202

200309

Dollars/MT 1960‛s: Crop

Forecasts, Weather

Innovative Change & Cost Advantage

1970‛s Risk Management Importance

1980‛s Risk Mgt complex: Beans & Products, currency, politics etc.

Historical “Industry Focus”: Price Risk Management

Late 90‛s Geo Political Risk, awareness of non Sustainability

New: Health issues? Flavor? Reputation?

7

Production mondiale de cacao par continent

0

500

1000

1500

2000

2500

3000

3500

30 60 90 années

tonnes

Afrique Amérique Asie + océanie

Global Cocoa Production: Last 100 years

source

Consumption

8

0

200

400

600

800

1000

1200

1400

1950 1954 1958 1962 1966 1970 1974 1978 1982 1986 1990 1994 1998 2003

Year 1950 to 2005

Metric

Ton

per Yea

r Brazil Ghana Nigeria ICMalaysia Indonesia

Ghana: policy, farm income, capsids

Brazil: Witches’ Broom, low prices, currency

Indonesia: Pest (cocoa pod borer),

Malaysia: Major economic growth, cocoa price, alternatives

Nigeria: policy (oil), farm income, capsid & black pod

Issues with Cocoa Production in country: Last 60 years

9

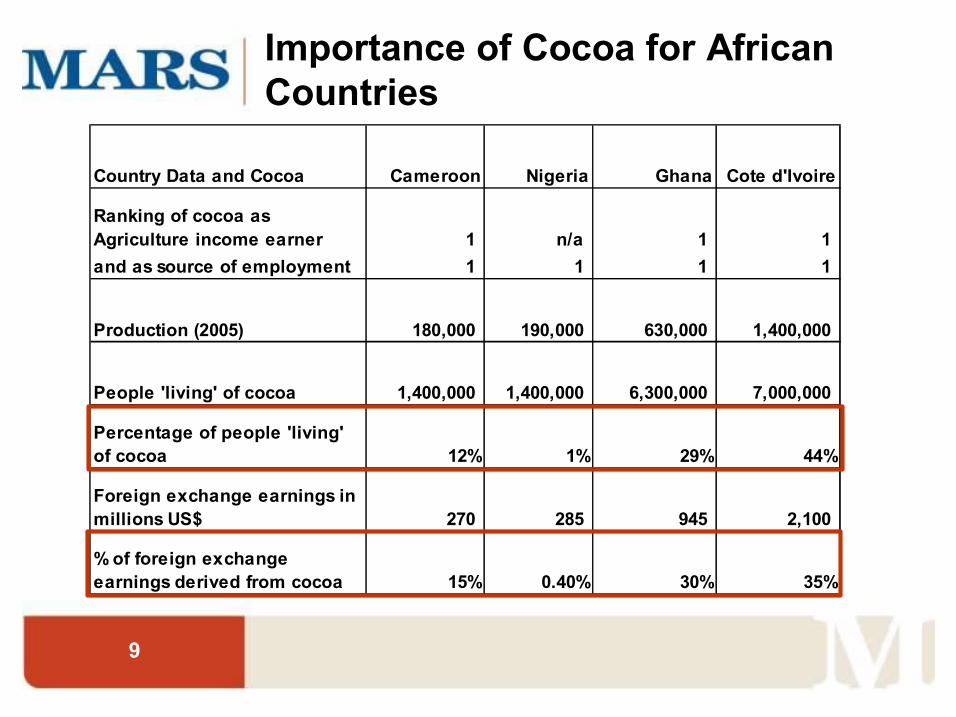

Importance of Cocoa for African Countries

Country Data and Cocoa Cameroon Nigeria Ghana Cote d'Ivoire

Ranking of cocoa as Agriculture income earner 1 n/a 1 1 and as source of employment 1 1 1 1

Production (2005) 180,000 190,000 630,000 1,400,000

People 'living' of cocoa 1,400,000 1,400,000 6,300,000 7,000,000

Percentage of people 'living' of cocoa 12% 1% 29% 44%

Foreign exchange earnings in millions US$ 270 285 945 2,100

% of foreign exchange earnings derived from cocoa 15% 0.40% 30% 35%

10

Awareness of Risk of Availability (Supply) in addition to Price Risk

Industry knows how to manage price risk • But managing price risk is not enough if there will not be

sufficient supply of affordable, good quality beans

Mars’ Commitment to Cocoa Sustainability • Understand situation (Risk analysis) • Identify Supply Challenges and Solutions; use, linking and

Sharing of Science • Capacity building in producing countries and • Pilot Programs conducted in “farmers’ fields” • Develop Partnerships

11

Challenges in the Current Cocoa Supply Chain

Economic issues Low Yields Poor agronomic practices, pest and disease problems, ageing

farms, inadequate planting materials, poor soil management and use of farm inputs

Economic issues Other Land Tenure rights, Inadequate infrastructure and landuse

planning, poor market information systems and quality signals, absence of crop diversification, no credit systems

Environmental issues Weather anomalies and trends, soil erosion, deforestation, water

stress, global warming, monoculture issues Social Issues

Poverty, lack of education, diseases, vulnerable rural livelihoods, labor conditions i.e. WFCL

The longterm supply of cocoa is at risk

12

Missed production potential due to Pest and Disease and Soil Fertility

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

1,800,000,000

Fertility

Black Pod

Mirids

Rodents

CPB W

B FPR

Loss US$ value

Cote d'Ivoire Ghana Nigeria Cameroun Indonesia Latin America

Lost potential in US$ by Issue

Low income due to avoidable losses

13 When productivity and income decline due to avoidable soil nutrient depletion, land is abandoned….

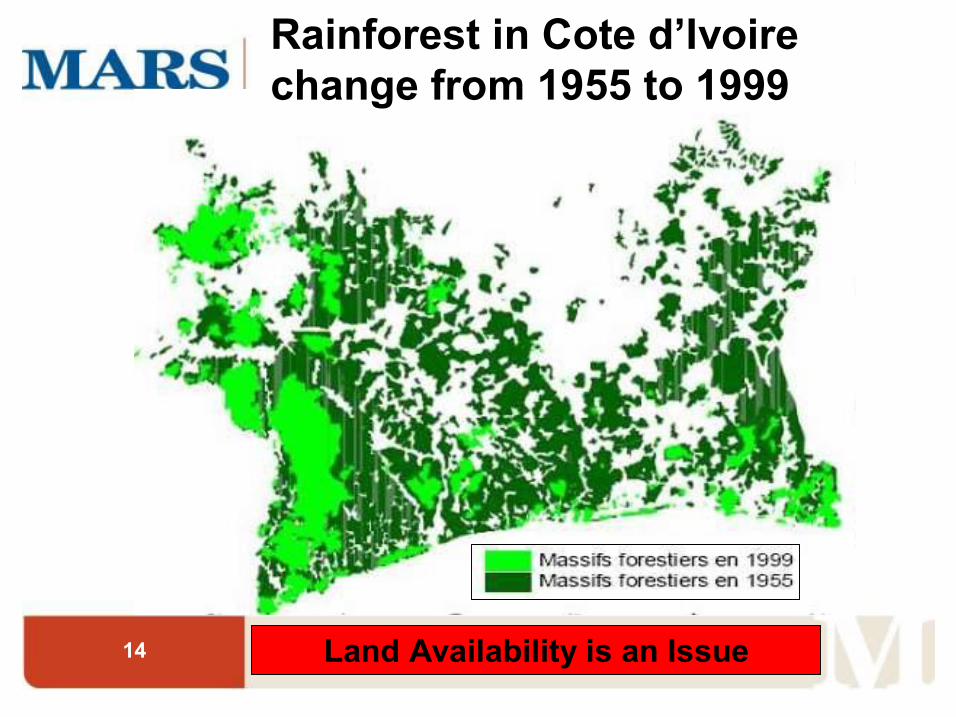

14 Land Availability is an Issue

Rainforest in Cote d’Ivoire change from 1955 to 1999

15

Challenges of a sustainable cocoa supply chain Downstream

Inadequate Marketing systems No or inadequate price information systems and low farm gate price compared to FOB and World Market price, poor price/quality signals to farmers, boom/bust cycles etc.

Cocoa and Chocolate Market far away from Farmer Not enough direct contact and feedback to farmers, market forces at farmers’ end very different than those at consumers’ end

Consumer Needs and Demands Good Quality but affordable product, pressure to improve human and environmental conditions for all stakeholders in chain

Corporate Social Responsibility The image of a business, a product

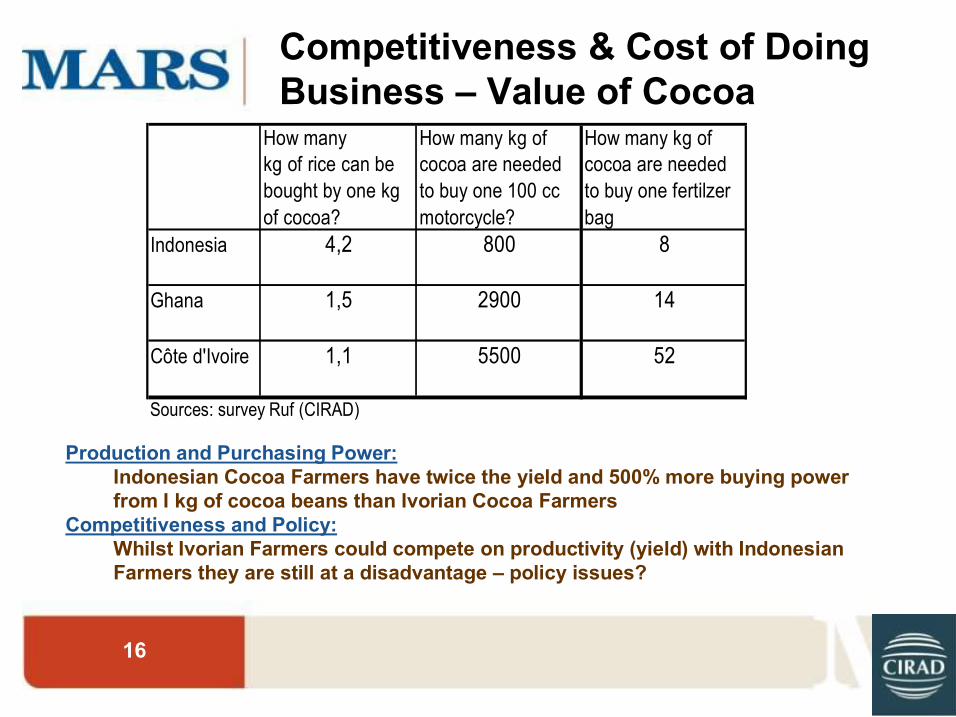

16

How many How many kg of How many kg of kg of rice can be cocoa are needed cocoa are needed bought by one kg to buy one 100 cc to buy one fertilzer of cocoa? motorcycle? bag

Indonesia 4,2 800 8

Ghana 1,5 2900 14

Côte d'Ivoire 1,1 5500 52

Sources: survey Ruf (CIRAD)

Competitiveness & Cost of Doing Business – Value of Cocoa

Production and Purchasing Power: Indonesian Cocoa Farmers have twice the yield and 500% more buying power from I kg of cocoa beans than Ivorian Cocoa Farmers

Competitiveness and Policy: Whilst Ivorian Farmers could compete on productivity (yield) with Indonesian Farmers they are still at a disadvantage – policy issues?

17

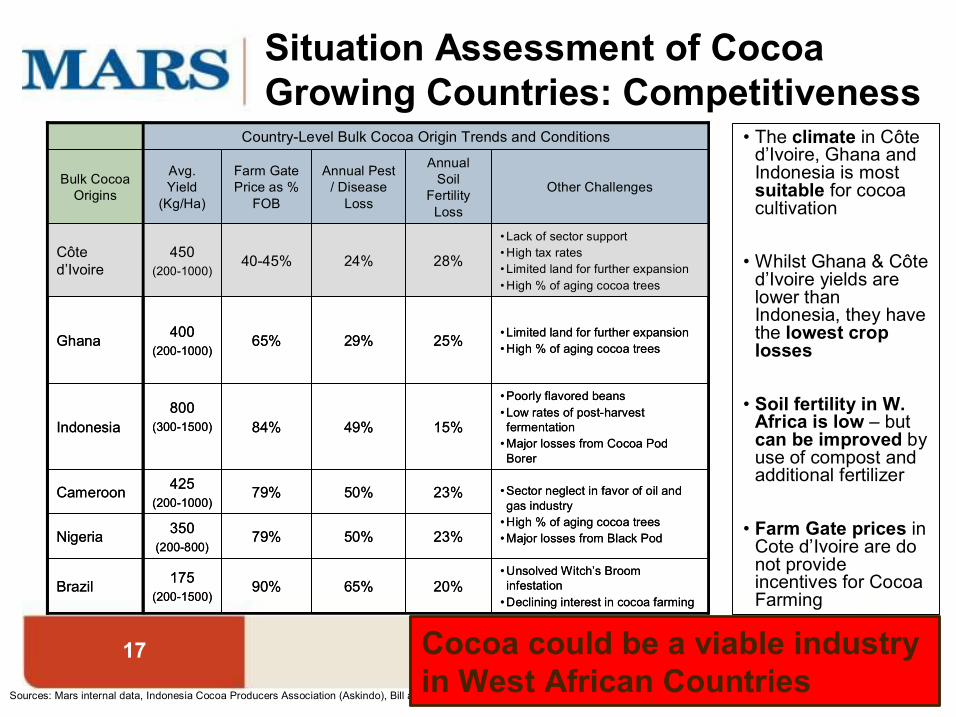

Situation Assessment of Cocoa Growing Countries: Competitiveness

Sources: Mars internal data, Indonesia Cocoa Producers Association (Askindo), Bill and Melinda Gates Foundation Presentation, COPAL, WCF

• The climate in Côte d’Ivoire, Ghana and Indonesia is most suitable for cocoa cultivation

• Whilst Ghana & Côte d’Ivoire yields are lower than Indonesia, they have the lowest crop losses

• Soil fertility in W. Africa is low – but can be improved by use of compost and additional fertilizer

• Farm Gate prices in Cote d’Ivoire are do not provide incentives for Cocoa Farming

CountryLevel Bulk Cocoa Origin Trends and Conditions

•Unsolved Witch’s Broom infestation •Declining interest in cocoa farming

•Sector neglect in favor of oil and gas industry •High % of aging cocoa trees •Major losses from Black Pod

•Poorly flavored beans • Low rates of postharvest fermentation •Major losses from Cocoa Pod Borer

• Limited land for further expansion •High % of aging cocoa trees

• Lack of sector support •High tax rates • Limited land for further expansion •High % of aging cocoa trees

Other Challenges

175 (2001500)

350 (200800)

425 (2001000)

800 (3001500)

400 (2001000)

450 (2001000)

Avg. Yield

(Kg/Ha)

Annual Soil

Fertility Loss

Annual Pest / Disease Loss

Farm Gate Price as %

FOB

Bulk Cocoa Origins

28% 24% 4045% Côte d’Ivoire

20% 65% 90% Brazil

23% 50% 79% Nigeria

23% 50% 79% Cameroon

15% 49% 84% Indonesia

25% 29% 65% Ghana

CountryLevel Bulk Cocoa Origin Trends and Conditions

•Unsolved Witch’s Broom infestation •Declining interest in cocoa farming

•Sector neglect in favor of oil and gas industry •High % of aging cocoa trees •Major losses from Black Pod

•Poorly flavored beans • Low rates of postharvest fermentation •Major losses from Cocoa Pod Borer

• Limited land for further expansion •High % of aging cocoa trees

• Lack of sector support •High tax rates • Limited land for further expansion •High % of aging cocoa trees

Other Challenges

175 (2001500)

350 (200800)

425 (2001000)

800 (3001500)

400 (2001000)

450 (2001000)

Avg. Yield

(Kg/Ha)

Annual Soil

Fertility Loss

Annual Pest / Disease Loss

Farm Gate Price as %

FOB

Bulk Cocoa Origins

28% 24% 4045% Côte d’Ivoire

20% 65% 90% Brazil

23% 50% 79% Nigeria

23% 50% 79% Cameroon

15% 49% 84% Indonesia

25% 29% 65% Ghana

Cocoa could be a viable industry in West African Countries

18

Summary of Issues

The Solution to current problems in the Cocoa Producing countries lies in

• Competitiveness (price, productivity, infrastructure) • Intensification (germplasm, rehabilitation, P&D control, fertility) + • Crop Diversification (farmers cultivating several crops)

Whilst Mars and other Cocoa Industry stakeholders understand ‘cocoa issues’ such as competitiveness and intensification, more expertise is needed for ‘crop diversification’

19

Luzon

Cocoa under Coconut

Coconut and Cocoa Farm Cocoa under Fruit

Cocoa in Mixed Farm

Farm Diversification: Mixing of Crops or Several Single Crops

20

Mutually Achieving Goals through Development of Sustainable Cocoa Goals Mars, Inc. (and others World Bank, Producer Organizations

in the cocoa and Governments of and Small Farmers chocolate industry) Producer Countries, NGO’s

Long Term A socially, environmentally Poverty reduction and economic Predictable yield, allowing and economically sustainable growth through a market and trade investment in land and equipment; cocoa industry with motivated oriented agriculture agroforestry systems that will farmers and assured supplies expand the economy

Medium Term Better quality and more reliable Sustainability and high quality Increased yield and income; supply of cocoa from Asia by technical support implemented reduced labor cost/acre combating CPB at little incremental cost

Short Term Opportunities in trading; Global access to worldclass Improved understanding of infrastructure, training knowledge and advanced farming techniques; improved

technical innovations planting materials

Partnerships: Mutual and Complementary Goals

21

Cocoa Sustainability Mars Incorporated Initiatives

Mars Inc. focuses on our Expertise, i.e. – Analysis: both inhouse and external – Science: e.g. Cocoa Genome – Implementation: Mars Cocoa Development Centres, iMPACT – Supply Chain: Certification through Rainforest Alliance, Utz Certified

Mars Inc. works in Partnerships and Collaboration with: – Research Institutes – Government , Public and Civil Society Institutes – Private industry

22

1 2 3 4 9 10 0 cT cCIR253

2,8 cT cCIR83 3,2 gT cCIR104 3,6 gT cCIR115 4,2 C168

12 cT cCIR238

14,7 cT cCIR1

17,7 mTcCIR15 17,8 cT cCIR79

23 cT cCIR77 23,6 gT cCIR127

27,4 C75 28,7 C66

31,1 cT cCIR46 31,5 ADH 33,6 33,9 cot448 35,7 AFLP17/5 35,9 rOPM7/1.4 36,3 AFLP14/5 36,3 AFLP3/1 39,1 cT cCIR78 40,7 mTcCIR54 42,5 AFLP18/9 43,9 mTcCIR29 46,1 AFLP18/6 46,6 AFLP17/1 47,4 AFLP1/12 48,3 AFLP9/8 50,9 AFLP14/9 51,2 C55 51,6 AFLP5/9 52,1 AFLP15/3 52,3 AFLP5/11 52,6 rOPP14/.9 52,7 AFLP17/3 52,7 AFLP6/2 53,1 AFLP8/10 54,6 rOPK15/,6 54,6 AFLP11/1 55,7 cT cCIR19 56,6 AFLP12/4 59,4 AFLP5/19 60,8 cT cCIR48 61,3 AFLP6/6 61,9 AFLP6/10 62,8 gT cCIR144 63,2 rOPD14/1 64,8 cT cCIR218 66,7 cT cCIR215 68,4 AFLP1/2 73,9 cT cCIR3 74,6 C138 78,3 rTcC IR132 79,4 AFLP6/16 80 C157

83,8 AFLP10/15 86,2 rOPR19/.4

89,8 cT cCIR72

96,1 gT cCIR120

100,2 mTcCIR22

0 AFLP4/3 1,8 gT cCIR147 2,5

8,6 9 gT cCIR135 10 mTcCIR19

11,4 AFLP20/3 11,5 gT cCIR110 12,3 14,5 cT cCIR235 14,6 AFLP10/8 19,3 mTcCIR3 20,9 N1072 22 AFLP8/3

23,4 gT cCIR161 24,8 25,5 cT cCIR252 25,6 AFLP19/4

30,7

42,1 rOPR16/.9

46,6 48 cT cCIR43

50,1 cT cCIR249

56,3 mTcCIR60 56,9 AFLP1/13 58,5 rOPM3/0.8 60,3 AFLP16/10 60,4 AFLP9/5 60,5 AFLP1/15 63,4 rTcCIR133 64,4 cT cCIR74 64,5 AFLP12/5 65,4 C119 65,5 cT cCIR86 66 AFLP3/4

68,9 gT cCIR149 69,6 cT cCIR23 70,3 AFLP6/9 71,6 CA18 72 mTcCIR48

72,7 C37 74,8 PGM/H 77,4 gT cCIR156 81,1 cT cCIR76 82,5 AFLP1/7 84,6 cT cCIR211 85,6 cT cCIR250 87,5 cT cCIR213 87,5 AFLP8/13

92,8 mTcCIR11

96 rOPR8/ .5

105 rOPQ4/1.8

109,1 gT cCIR151

0 1,4

cT cCIR230

cot3932

gT cCIR141

mTcCIR44

gT cCIR140

cT cCIR53

cT cCIR246

cT cCIR90 cT cCIR99

5 AFLP8/9 5,2 mTcCIR49 5,9 cT cCIR69 8,5 cT cCIR80 9,8 gT cCIR108 11,2 mTcCIR21 12,1 cT cCIR61 12,6 CA39 13,4 gT cCIR121a 13,7 AFLP6/11 15,1 cot3089 15,4 mTcCIR40 15,6 rOPQ4/.75 15,7 cT cCIR47 16,2 mTcCIR62 16,6 AFLP3/2 18,2 AFLP17/6 19,9 AFLP6/15 20,2 AFLP14/8 21,8 AFLP5/17 22,5 AFLP8/15 24 AFLP10/5

24,7 rOPL10/.8 25,3 cT cCIR62 25,5 C6 5 27,3 AFLP8/12 28 AFLP9/9

30,7 AFLP16/7 38,1 AFLP10/9 42,2 cT cCIR51

44,6 gT cCIR107

48 gT cCIR143 48,1 cT cCIR32 49,4 AFLP6/5 49,5 C4 2 52,5 AFLP7/1 53 rTcCIR131

54,5 AFLP3/3

64,1 AFLP10/1 66 AFLP5/7

72 AFLP10/11 73,9 gT cCIR118 74,1 cT cCIR66

78,3 gT cCIR122 78,5 C4 1 79,5 cT cCIR49

82,7 AFLP2/1

95,6 cT cCIR237

0 rOPF3/2,5

10,1 IDH 12,3 TEL139/HIND 12,5 AFLP17/8 13,4 C104 14,7 gT cCIR146 17,3 gT cCIR112

24 AFLP8/2 25,2 AFLP6/14 26 AFLP6/1

26,2 AFLP6/13 26,5 N1102 27,4 AFLP5/5 28,4 AFLP10/2 28,5 mTcCIR39 29,3 AFLP9/1 30 mTcCIR18

31,7 AFLP7/10 32,6 AFLP8/14 33 AFLP17/2

33,7 AFLP5/14 34,5 mTcCIR17 35,3 AFLP1/17 36,2 AFLP5/15 36,3 gT cCIR128 36,8 cT cCIR232 38,2 AFLP5/18 38,4 AFLP20/2 38,7 AFLP1/16 39,3 AFLP5/16 39,5 AFLP1/11 40,9 cT cCIR224 41,4 rOPF12/1 41,4 AFLP16/11 43,4 gT cCIR119 45,6 N1388 46,4 mTcCIR12 47,2 mTcCIR43 49,1 AFLP4/5 53,1 cT cCIR243 54,9 mTcCIR32 55,1 gT cCIR136 57,3 AFLP15/6 57,5 AFLP19/1 59,8 AFLP13/2 60 rOPO16/.7

60,4 cT cCIR212 61,2 mTcCIR33 64,1 MDH/A 68,9 mTcCIR57 69,8 AFLP1/3 74 cT cCIR214

74,4 gT cCIR129 77,3 C3 78,7 cT cCIR251 79,9 AFLP1/8 80 gT cCIR154 85 cT cCIR205

TEL139/BGL

0

2

5,9 6,7 7,8 9

9,6 12,4

14,8 16,2 17,6

20,8 21,2 21,6 23

23,5 24

24,5 25,3 25,6 25,8 25,9 26,2 27,2 27,5 27,5 28,5 29,4 30,6 33,4 35,3 40

40,5 41,1 44,2 46,1 47,8 49,2 51

51,2 54,5 56,2 58,4 60,7 61,9 62,8 63,5 64,2 66,4 66,6

5 6 7 8 HistoneB

gT cCIR106

cT cCIR202 gT cCIR148 AFLP18/5 HistoneA rOPD14/.6 cT cCIR73

cT cCIR85 AFLP5/10 cT cCIR88

gT cCIR139 a AFLP8/4 AFLP9/6 AFLP8/5 AFLP16/4 mTcCIR10 gT cCIR101 rOPO15 AFLP7/5 CA24 AFLP11/8 cT cCIR55 mTcCIR2 mTcCIR51 mTcCIR47 mTcCIR42 5S AFLP4/1 AFLP16/5 cT cCIR56 cT cCIR58b AFLP7/2 rOPM17/1.4 5 cT cCIR68 AFLP10/14 cT cCIR229 AFLP10/13 AFLP10/12 N1333 gT cCIR145 C164 cT cCIR81 cT cCIR2 cT cCIR216 mTcCIR36 rOPS 8/.55 cT cCIR231 cT cCIR89 cT cCIR234

0 AFLP1/6

10,5 mTcCIR6 11,9 AFLP5/3 12,1 AFLP17/10 13,6 cT cCIR247 15,5 mTcCIR16

20,9 AFLP7/6 21,4 AFLP5/1 22,9 mTcCIR53 23,2 AFLP6/8 23,2 gT cCIR160 23,8 AFLP12/3 24,1 AFLP15/5 24,3 AFLP10/6 25,2 AFLP2/5 25,9 mTcCIR50 26,5 AFLP9/3 26,7 AFLP9/2 26,8 cT cCIR245 27,8 AFLP5/13 28,2 rOPR3/ .75 28,3 AFLP9/4 29,6 AFLP11/4 30,3 AFLP2/6 32,8 cT cCIR223 36,8 gT cCIR130 42,5 cT cCIR12 45 cT cCIR54

45,2 mTcCIR25 46,5 cT cCIR241 48,9 AFLP7/3

56,5 cT cCIR225

61,3 gT cCIR116 61,4 AFLP5/4

65,4 cT cCIR222

68,2 mTcCIR52

73,3 mTcCIR9 75 cT cCIR93

75,9 cT cCIR240 76,2 gT cCIR139b 76,4 AFLP1/5

0 AFLP7/7 1,2 C173 3,2 AFLP1/14

7,3 AFLP16/13

10,2 AFLP10/7 12 gT cCIR138

15,2 gT cCIR152 16,3 gT cCIR155 16,9 N1081 18,2 gT cCIR125 18,4 rOPP 14/.7 19 N1077

21,8 AFLP4/4 24,1 cT cCIR71 26,2 mTcCIR46

28,3 AFLP11/5 28,4 mTcCIR7

32,7 AFLP10/4 33,1 AFLP10/3 34,5 mTcCIR56 36,7 mTcCIR55 38,3 AFLP6/17

41,6 AFLP14/10 43,1 cT cCIR59 43,2 AFLP14/11 44,1 AFLP14/4 44,9 rOPM20 44,9 AFLP18/8 45,7 AFLP5/12 47,8 AFLP8/11 48,3 cT cCIR94 48,7 AFLP16/3 48,9 AFLP19/2 50,5 rDNA PTA71 51,4 AFLP18/3 51,7 AFLP18/2 52,2 cT cCIR204 56,2 cT cCIR244 56,4 AFLP18/4 59,6 rOPM4/.7 63,2 AFLP15/7 65,8 rOPM5/.75

76,5 cT cCIR96

0 mTcCIR1

2,6 AFLP12/6 4,4 AFLP12/7

12,4 PGI

15,7 AFLP6/12 17,1 AFLP16/14

26 cT cCIR21

30,5 gT cCIR124 30,9 gT cCIR114 32,5 gT cCIR111

35 AFLP15/1

39,2 mTcCIR26

43,9 rOPP14/.4

47,1 rOPF15/,4 48,7 AFLP2/4

50,9 AFLP15/2 50,9 cT cCIR63 51,1 cT cCIR92 51,6 AFLP1/10 51,6 N1111 51,6 cT cCIR98 52,4 AFLP17/7 53,4 AFLP11/7 53,5 cT cCIR201 58,2 AFLP17/9 60,8 mTcCIR45 62,6 cT cCIR203 65,6 AFLP19/3 67,5

78,9 TEL139/HI

0 gT cCIR117 0 cT cCIR206

5 gT cCIR109

14,6 cT cCIR45

22,8 mTcCIR30 24,4 gT cCIR157 25,2 AFLP5/2 26,4 cT cCIR11 28,3 AFLP12/1 28,7 AFLP12/2 29 cT cCIR39

29,9 AFLP4/2 31,6 cT cCIR58a 31,7 mTcCIR24 32,1 cT cCIR95 32,1 AFLP1/4 32,2 gT cCIR134 33,5 cT cCIR207 36,7 AFLP6/7 37,6 AFLP8/8 38 ACP

38,3 AFLP8/7 38,3 mTcCIR35 39 AFLP8/6

42,4 rOPF15/18 46 AFLP3/5

48,5 AFLP2/8 49,4 AFLP3/6 49,6 AFLP4/6 49,9 AFLP1/9 50,3 gT cCIR150 50,4 AFLP11/3 50,4 mTcCIR63 50,5 AFLP16/1 50,7 AFLP11/9 50,8 rOPR19/.5 51,3 AFLP16/6 51,5 rOPF3/1,6 52,1 mTcCIR8 52,4 AFLP13/1 52,8 AFLP5/20 53,4 rOPQ10/2.1 54,1 cT cCIR208 54,6 AFLP5/6 54,8 cT cCIR228 55,3 AFLP2/3 57,9 AFLP3/7 59,7 gT cCIR102 60,9 mTcCIR58 65,1 cT cCIR87 71,8 AFLP5/22 73,4 AFLP14/7 78,2 AFLP18/1 85,3 AFLP11/2

91,1 cT cCIR236

94 C106 94,4 AFLP11/6 95,4 AFLP14/2

103,9 AFLP7/8

108 gT cCIR159

110,4 AFLP1/1

0 AFLP9/7 0,7 gT cCIR105

6,1 gT cCIR126 8,2 rOPP9/.35 9,7 cT cCIR239 11,3 cT cCIR254 11,6 cT cCIR50 12,8 cT cCIR219

29,7 AFLP6/3 30,5 mTcCIR31 32,6 cT cCIR217

34,7 HistoneC

41,8 gT cCIR113 43,4 cT cCIR233 45 AFLP14/3

46,5 mTcCIR41 46,8 mTcCIR38 46,9 mTcCIR61 47,6 AFLP16/8 48,5 cT cCIR252/2 50,6 gT cCIR137 51,8 cT cCIR75 54,3 gT cCIR103

60,9 AFLP2/7

63,6 AFLP5/21 65,5 cT cCIR209 66,2 AFLP14/1 67,3 AFLP14/6 68,8 mTcCIR59 68,9 mTcCIR37 69,9 mTcCIR34

75,2 AFLP2/2

84,8 AFLP10/10

88,6 AFLP11/10

Example of Mars leading Science: Molecular genetics at USDA

Mars waives IP rights on this research

23

Example of application of Science in a Mars Cocoa Development Centre

top grafting

Results from grafting rehabilitation

Side grafting

24 Thank You