43

CONTINUING DISCLOSURE 2013 Annual Report for the City of Amesbury, Massachusetts Prepared by Financial Advisor

CONTINUING DISCLOSURE 2013

Annual Report for the

City of Amesbury, Massachusetts

Prepared by

Financial Advisor

1

THE CITY

The City of Amesbury was established in 1668 and has a population of approximately 16,500. The City is locatedon the Merrimack River in northern Essex County approximately 42 miles north of Boston. Amesbury is bordered bythe Town of Merrimac on the west, the Town of South Hampton, New Hampshire on the north, the Town of Salisburyon the east, the City of Newburyport and the Town of West Newbury on the south. Interstate Route 95 passes throughthe City from north to south and Interstate 495 intersects Interstate 95 at Amesbury in a southwesterly direction.

Services

The City provides general governmental services for the territory within its boundaries, including police and fireprotection, disposal of garbage and rubbish, public education in grades kindergarten through twelve, water and sewerservices, sewage disposal, street maintenance, library, parks and recreational facilities. The Whittier RegionalVocational School District provides vocational-technical training for students in grades nine through twelve. TheAmesbury Housing Authority provides housing for eligible low-income families, the elderly and handicapped persons.The City is a member of the Merrimack Valley Regional Transit Authority which provides fixed route service betweenneighboring communities.

Principal Municipal Facilities

The following is a list of the City’s principal facilities.

Assessed

Facility Date Built (Remodeled) Valuation

High School 1968 (2008) $22,617,000

Middle School 1946 (1967, 1996, 1998) 25,635,600

Amesbury Elementary School 1968 (1997) 5,893,100

Cashman Elementary School 1975 (1997, 2002, 2005) 7,915,600

Horace Mann School 1901 (1974) 847,300

Wastewater Treatment Plant 1974 (2005) 3,955,400

Water Treatment Plant 1985 (2012) 5,254,100

City Hall 1900 1,204,900

City Hall Ordway 1900 856,000

Public Library pre-1900's 1,022,500

Fire Stations Headquarters 1927 1,206,900

Elm Street Fire Station early 1900's 650,500

Public Works Garage 1939 253,400

Public Works Garage 2012 881,300

Police Station 1920's 1,076,500

Governing Bodies and Officers

The City voted on November 8, 2011 to adopt a new charter with a Council-Mayor form of government. Thelegislative branch is the City Council, which consists of nine councilors. There are six councilors, one from eachdistrict, and three councilors at large. The councilors are elected to serve two-year terms of office. The Mayor iselected for a two-year term of office to serve as the chief executive officer of the City. The Mayor also serves as theseventh member and chairperson of the six member elected school committee.

The water and sewer departments are managed by the superintendent of Public Works who is appointed by theMayor. Local taxes are assessed by a board of three assessors who are also appointed by the Mayor.

Local school affairs are administered by a committee of seven persons elected for staggered four-year terms.

2

Principal Executive Officers

The following is a list of the principal executive officers within the City.

Mayor Thatcher W. Kezer, III Elected 2 years 1/2/2014

City Council Anne R. Ferguson, President Elected 2 years 1/2/2014

Robert W. Lavoie Elected 2 years 1/2/2014

Allen R. Neale Elected 2 years 1/2/2014

James Kelcourse Elected 2 years 1/2/2014

Christian Scorzoni Elected 2 years 1/2/2014

Donna McClure Elected 2 years 1/2/2014

Robert L. Gilday Elected 2 years 1/2/2014

Joseph W. McMilleon Elected 2 years 1/2/2014

Derek T. Kimball Elected 2 years 1/2/2014

Chief Financial Officer Michael W. Basque Appointed 3 Years 9/30/2016

Treasurer/Collector Donna Cornoni Appointed Indefinite N/A

Assessor Jason DiScipio Appointed Indefinite N/A

City Clerk Bonnijo Kitchin Appointed Indefinite N/A

Superintendent of Schools Michelle Robinson Appointed 3 Years 6/30/2014

Director of Public Works Robert Desmerais Appointed Indefinite N/A

Director of Community Development Joseph Fahey Appointed Indefinite N/A

Town Counsel Kopelman & Paige Appointed Indefinite N/A

Collective Bargaining

City and town employees (other than managerial employees) are entitled to join unions and to bargain collectivelyby representatives of their choice on questions of wages, hours and other terms and conditions of employment. TheCity has approximately 425 full-time employees and 200 part-time employees of whom approximately 72 percent offull-time employees belong to unions or other collective bargaining groups. The following table sets forth thecollective bargaining groups.

Contract

Union Department Members Expires

AFL-CIO Local 939 Public Works 22 6/30/2015

AFL-CIO Local 1783 Fire 32 6/30/2015

Amesbury Police Officers Association Police 30 6/30/2015

AFL-CIO Local 1033 School - Teachers 163 8/31/2015

AFL-CIO Local 939 School - Cafeteria 2 8/31/2015

AFL-CIO Local 1033 School - Tutors 19 8/31/2015

AFL-CIO Local 1033 School - Custodian/Maintenance 10 6/30/2015

O.P.E.I.U. Local 6 Gen. Govt. Non-Dept. Heads 29 6/30/2015

Total: 307

Other Data

The following tables set forth income levels, age characteristics, housing characteristics, population trends, andemployment figures for the City of Amesbury, Essex County, and the Commonwealth of Massachusetts.

3

Per Capita Income

Amesbury Essex County Massachusetts

Year Amount % Change Amount % Change Amount % Change

2011 5-year estimates $41,142 70.7% $34,858 32.2% $35,051 35.1%

1999 24,103 56.3 26,358 49.9 25,952 50.7

1989 15,423 134.7 17,586 129.2 17,224 131.0

1979 6,571 0.0 7,673 0.0 7,457 0.0

% Below Poverty Level (2011 5-year estimates) 3.9% 10.6% 10.7%

_________________________

Source: U.S. Department of Commerce

Median Family IncomeAmesbury Essex County Massachusetts

Income for Families Families Percent Families Percent Families Percent

Less than $10,000 39 0.9% 6,967 3.7% 57,867 3.6%

10,000 - 24,999 149 3.4 16,759 8.9 133,136 8.3

25,000 - 49,999 537 12.3 31,735 16.8 264,129 16.5

50,000 - 74,999 719 16.4 29,924 15.8 261,052 16.3

75,000 - 99,999 836 19.1 27,348 14.5 242,747 15.1

100,000 - 149,999 1,286 29.4 38,706 20.5 330,690 20.6

150,000 or more 811 18.5 37,741 19.9 314,319 19.6

Total 4,377 100.0% 189,180 100.0% 1,603,940 100.0%

Median Income $94,946 $83,047 $83,371

_________________________

Source: U.S. Department of Commerce

Household Income

Amesbury Essex County Massachusetts

Income for Households Households Percent Households Percent Households Percent

Less than $10,000 217 3.3% 18,505 6.5% 164,071 6.5%

10,000 - 24,999 722 11.0 39,124 13.7 341,431 13.5

25,000 - 49,999 1,016 15.5 55,088 19.3 477,788 18.9

50,000 - 74,999 1,124 17.2 45,724 16.0 416,286 16.5

75,000 - 99,999 1,049 16.0 36,987 13.0 337,712 13.4

100,000 - 149,999 1,481 22.6 46,878 16.5 418,394 16.6

150,000 or more 934 14.3 42,634 15.0 366,727 14.5

Total 6,543 100.0% 284,940 100.0% 2,522,409 100.0%

Median Income $79,293 $65,785 $65,981

_________________________

Source: U.S. Department of Commerce

4

Median AgeAmesbury Essex County Massachusetts

Age Number Percent Number Percent Number Percent

Under 5 Years 1,040 6.4% 43,451 5.9% 367,252 5.6%

5 Years to 19 Years 2,808 17.3 149,387 20.2 1,262,333 19.4

20 Years to 64 Years 10,545 64.8 442,904 59.9 3,991,339 61.3

65 Years and Over 1,874 11.5 103,763 14.0 891,303 13.7

Total 16,267 100.0% 739,505 100.0% 6,512,227 100.0%

Median Age 41 40 39

Median Age (2000) 36.7 37.5 36.5

_________________________

Source: U.S. Department of Commerce

Median Value Owner - Occupied Housing Units

Amesbury Essex County Massachusetts

Units Number Percent Number Percent Number Percent

Less than $100,000 147 3.1% 4,880 2.6% 49,369 3.1%

100,000 - 199,999 542 11.4 15,335 8.3 189,878 11.8

200,000 - 299,999 1,291 27.1 41,247 22.3 389,385 24.3

300,000 - 499,999 2,164 45.4 78,886 42.6 627,185 39.1

500,000 - 999,999 577 12.1 38,719 20.9 291,521 18.2

1,000,000 or more 46 1.0 5,918 3.2 57,135 3.6

Total 4,767 100.0% 184,985 100.0% 1,604,473 100.0%

Median Value $327,200 $362,300 $343,500

_________________________

Source: U.S. Department of Commerce

Age of Housing Units

Amesbury Essex County Massachusetts

Year Built Number Percent Number Percent Number Percent

2000 or later 543 7.7% 19,563 6.4% 187,003 6.7%

1980 to 1999 1,404 19.8 53,184 17.4 508,434 18.2

1940 to 1979 2,324 32.8 112,969 36.9 1,111,838 39.7

1939 or Earlier 2,808 39.7 120,301 39.3 992,082 35.4

Total 7,079 100.0% 306,017 100.0% 2,799,357 100.0%

_________________________

Source: U.S. Department of Commerce

Unemployment

Unemployment Rate

Calendar Year(1) Labor Force Employment City County State US

2013 (August) 8,951 8,359 6.6% 7.2% 6.8% 7.3%

2012 8,761 8,226 6.1 7.1 6.7 8.1

2011 8,671 8,074 6.9 7.8 6.8 8.9

2010 8,849 8,112 8.3 8.9 8.5 9.6

2009 8,731 8,032 8.0 8.8 8.2 9.3

_________________________

Source: Massachusetts Department of Employment & Training

(1) Full year averages except for 2013 which is for the month indicated.

5

Population

Amesbury Essex County Massachusetts

Year Number % Change Number % Change Number % Change

2012 estimate 16,535 1.5% 755,618 1.7% 6,646,144 1.5%

2010 16,283 -1.0 743,159 2.7 6,547,629 3.1

2000 16,450 9.7 723,419 8.0 6,349,097 5.5

1990 14,997 7.3 670,080 5.8 6,016,425 4.9

1980 13,972 0.0 633,632 0.0 5,737,037 0.0

_________________________

Source: U.S. Department of Commerce for actuals and estimates,

Massachusetts Institute for Social & Economic Research for projections.

Employment and Payrolls

Calendar Year Average

Employment by Industry 2012 2011 2010 2009 2008

Construction & Natural Resources 293 262 249 309 347

Manufacturing 690 668 668 770 882

Trade, Transportation & Utilities 675 658 671 639 635

Financial Activities 179 170 173 170 172

Professional & Business Services 531 563 496 485 427

Education & Health Services 822 804 822 641 568

Leisure & Hospitality 593 614 567 556 564

Information & Other Services 263 269 249 223 261

Public Administration -0- -0- -0- -0- -0-

Total Employment 4,778 4,730 4,707 4,587 4,657

Number of Establishments 462 466 474 468 453

Total Annual Wage (000) $204,238 $194,073 $192,049 182,984 $185,474

Average Weekly Wage 822 789 785 767 766

_________________________

Source: Massachusetts Department of Employment & Training

Community Development

Over four decades ago Amesbury introduced a program of revitalization and economic development. During thoseyears, over three hundred thousand square feet of mill space has been redeveloped into commercial, office, residentialand manufacturing uses. The Central Business District (CBD) received a $4.4 million reconstruction includingroadways, sidewalks and utility work. Period lighting, street trees, brick sidewalks, a plaza and park were addedthrough that effort. Concurrently, using City and grant funds, a neighborhood rehabilitation effort was begun updatingthe infrastructure including streets and sidewalks in the neighborhoods surrounding the CBD. Well over $3,000,000has been spent on this program and work continues to this day.

During that time, a mill complex of eight buildings with over one hundred fifty thousand square feet of space hasbeen renovated into a mixed use complex of residential, office, restaurant and commercial spaces. This area, referredto as the Upper Millyard, spurred the redevelopment effort throughout the CBD which has included the construction ofthree new multi story, mixed use buildings and the renovation of several others.

With the success of the Upper Millyard, the City began work on another complex of mills to the southeast of theCBD, referred to as the Lower Millyard. Redevelopment is already underway in the area spurred by the sale of tax titleproperties to developers who have created residential loft housing, office, and artisan live-work space. After lobbyingby the City, the Merrimac Valley Regional Transit Authority (MVRTA) agreed to locate a regional transportationcenter in the Lower Millyard. Construction on the $5.8 million facility has been completed and the facility houses theCity’s Senior Center among other City offices.

6

New zoning has been approved for the area in order to facilitate the redevelopment effort. That zoning resulted inone property owner proposing a mixed use project valued at over fifty million dollars upon completion. Interesteddevelopers continue to approach the property owner on the project which will include over two hundred units ofhousing.

Another property owner has renovated over seventy thousand square feet of Mill space into office space and isleasing to over 22 small businesses including R&D, design and computer programming companies. That owner is inthe process of designing and permitting a thirty thousand square foot $4.5 million addition.

Also within the Lower Millyard, a developer has purchased a forty thousand (40,000) sq. ft. mill building and hasreceived permits to rehabilitate it into forty five residential units estimated to be valued at 7 million dollars. In order tosupport the interest in the redevelopment effort, the City has undertaken improvements in the area to further encourageprivate investment. A dilapidated cluster of buildings being used by the Public Works Department is proposed for saleto a private developer. To realize that goal, the City has appropriated $5.9 million to move the DPW to a new locationfor the facility. A portion of the vacated DPW property is planned for a $1.2 million Heritage Park which will includea canoe and kayak launch which the State has committed to fund. In addition, engineering and design funding has beensecured for the expansion of the above ground parking deck servicing the area. The City is also completing a $1.4million reconstruction of Elm Street, the major access route to the Lower Millyard. This project is funded through theState funded MassWorks program.

In another area of the City, adjacent to Interstates 495 and 95, lie 135 acres of land zoned for mixed development.Several years ago, the City completed a $100,000 study of the land identifying opportunities and constraints todevelopment. Since that time the City has re-zoned the area and approved an MGL 43G designation as a prioritydevelopment site with an expedited permitting process. Under that provision the City has approved a permitapplication for a ninety unit hotel, a retail building and most recently a regional veterinarian hospital and clinic.

Finally, along the Route 110 corridor, plans were submitted and approved for a new CVS Pharmacy, and a mixed-use building which have been built. The City has also permitted a large expansion for a food distribution business andthe installation of a commercial solar array in that area, while a real estate investment company continues to convert ahundred thousand square foot manufacturing building into rental space for high tech tenants.

Overall, through zoning, planning, infrastructure improvement and professional planning, the City is wellpositioned for expanded economic development opportunity in the future.

Principal Employers

The following table lists the largest employers in the City of Amesbury and the approximate number of employeesof each, exclusive of the City itself.

Current

Company Nature of Business Employees

Cardocaire/Munters Dehumidification units 314

Harborside Health Care Nursing and rehabilitation center 154

Super Stop and Shop Grocery store 151

Mariner Health Care Long-term care and rehabilitation facility 148

ARC Tech Microwave absorbable materials 130

Amesbury Health Center Healthcare 113(1)

Maptech, Inc. Navigation software, digital and paper data 82

Shaheen Bros., Inc. Grocery store 68

LeBaron Bonney Company/Hampton Coach Auto upholstery/materials/hardware 65

Innovative Technologies Glove box systems 62

TEK-Coating Company, Inc. Powder coating, spray painting, silkscreen 57

printing

Amesbury Chair Company Manufacturer/distributor of wood furniture 25

(1) Does not include private physician offices.

7

Building Permits

Below is a list of the building permits issued and their estimated values for the following calendar years.

For Calendar Year

2013(1) 2012 2011 2010 2009

Residential:

Number…………………… 430 502 382 418 445

Value……………………… $ 7,898,417 $ 9,567,667 $ 5,533,053 $ 14,326,728 $ 5,249,756

Non-Residential:

Number…………………… 34 38 75 74 28

Value……………………… $ 4,576,604 $ 3,830,592 $ 1,888,347 $ 5,808,945 $ 484,861

(1) Through September 2013.

Public School Facilities

The City operates two elementary schools (Pre-K through four), one middle school (grades five through eight) anda senior high school (grades nine through twelve). In 1997, the City completed various remodeling and repair projectstotaling $1,500,000 to the Cashman and Amesbury Elementary schools. A $19,850,000 project for the construction ofan addition to and remodeling of the middle school was completed and the City issued general obligation bonds inSeptember 1998. The City completed a construction and remodeling project totaling $5,000,000 to the CashmanElementary School in calendar year 2005.

The City also authorized a project totaling $29,070,000 for planning, constructing an addition to and forremodeling, reconstructing and making extraordinary repairs to the Amesbury High School which has been completed.The following tables list public school facilities, current and projected enrollment figures, and student - teacher ratiosfor the City as of the most recent October 1.

Date Added to Current

Name Grade Built (Remodeled) Capacity Enrollment(1)

Amesbury Elementary PreK-4 1968 (1997) 630 427

Charles Cashman Elementary PreK-4 1975 (1997, 2002, 2005) 700 538

Amesbury Middle 5-8 1946 1967 (1998) 1,000 731

Amesbury High 9-12 1968 (2005-2008) 900 643

Totals: 3,230 2,339

(1) As of October 1, 2013.

Public School EnrollmentsActual(1)

2005-06 2006-07 2007-8 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Elementary 992 973 1,004 1,006 987 995 969 969 965

Middle 766 751 714 722 763 751 749 730 731

High 745 709 697 679 674 640 610 637 643

Totals: 2,503 2,433 2,415 2,407 2,424 2,386 2,328 2,336 2,339

___________________________

(1) Source: Massachusetts Department of Education - As of October 1, each school year.

8

Student-Teacher Ratios

Elementary - 13:1 Middle - 13:1 High - 15:1

Total Number of Teachers & Teachers Aides 254

Total Number of Administrative Staff 8

Total: 262

Educational AttainmentAmesbury Essex County Massachusetts

Years of School Completed Number Percent Number Percent Number Percent

Less than 9th Grade 276 2.4% 27,306 5.4% 215,977 4.9%

9th to 12th Grade, No Diploma 470 4.1 31,039 6.2 274,938 6.2

High School Graduate 3,158 27.3 133,751 26.6 1,161,382 26.3

Some College, No Degree 1,913 16.5 86,497 17.2 718,047 16.2

Associate's Degree 970 8.4 41,006 8.2 337,921 7.6

Bachelor's Degree 2,944 25.4 110,083 21.9 977,354 22.1

Graduate or Professional Degree 1,851 16.0 72,862 14.5 733,672 16.6

Total 11,582 100.0% 502,544 100.0% 4,419,291 100.0%

High School Graduate or Higher 10,836 93.6% 444,199 88.4% 3,928,376 88.9%

Bachelor's Degree or Higher 4,795 41.4 182,945 36.4 1,711,026 38.7

_________________________

Source: U.S. Department of Commerce

9

INDEBTEDNESS

The general debt limit of the City of Amesbury consists of a normal debt limit and a double debt limit. The normaldebt limit is 5.0 percent of the valuation of taxable property as last equalized by the State Department of Revenue. TheCity can authorize up to $98,036,995 without state approval and up to twice this amount ($196,073,990 – double debtlimit) with the approval of the Municipal Finance Oversight Board composed of the State Treasurer, the State Auditor,the Attorney General and the Director of Accounts.

There are many categories of general obligation debt which are exempt from and do not count against the GeneralDebt Limit. Among others, these exempt categories include revenue anticipation notes and grant anticipation notes;emergency loans; loans exempted by special laws; certain school bonds, sewer bonds, solid waste disposal facility bondsand economic development bonds supported by tax increment financing; and subject to special debt limits, bonds for water(limited to 10 percent of equalized valuation), housing, urban renewal and economic development (subject to various debtlimits), and electric, gas, community antenna television systems, and telecommunications systems (subject to separatelimits). Revenue bonds are not subject to these debt limits. The General Debt Limit and the special debt limit for waterbonds apply at the time the debt is authorized. The other special debt limits generally apply at the time the debt is incurred.

As of November 1, 2013, the City of Amesbury had total outstanding and authorized unissued general obligationdebt of $50,720,199, of which $30,695,715 was outside, and $20,024,484 was subject to its general debt limit. Theadditional debt which could be authorized within the normal 5.0 percent debt limit was $78,012,511. The additionaldebt which could be authorized within the double debt limit was $176,049,506.

Authorization of General Obligation Bonds and Notes

Bonds and notes are generally authorized on behalf of the City by vote of two-thirds of all the members of theCity Council with the approval of the Mayor. Provision is made for a referendum on the filing of a petition bearing therequisite number of signatures. Borrowings for certain purposes require state administrative approval. Temporaryloans in anticipation of current revenues and certain state and county reimbursements are generally authorized bymajority vote but provision is made for temporary loans in anticipation of federal grants and for other purposes incertain circumstances without City Council authorization.

Refunding bonds and notes are authorized by the City Council. Borrowings for some purposes require Stateadministrative approval.

When serial bonds or notes have been authorized, bond anticipation notes may be issued by the officers authorized toissue the serial bonds or notes. Temporary debt in anticipation of the revenue of the fiscal year in which the debt is incurredor in anticipation of authorized federal and state aid generally may be incurred by the treasurer with the approval of themayor.

Types of Obligations

General Obligations. Massachusetts cities and towns are authorized to issue general obligation indebtedness of thesetypes:

Serial Bonds and Notes. These are generally required to be payable in annual principal amounts beginning no laterthan the end of the next fiscal year commencing after the date of issue and ending within the terms permitted by law. Alevel debt service schedule, or a schedule that provides for a more rapid amortization of principal than level debt service, ispermitted. The principal amounts of certain economic development bonds supported by tax increment financing may bepayable in equal, diminishing or increasing amounts beginning within 5 years after the date of issue. The maximum termsof serial bonds and notes vary from one year to 40 years, depending on the purpose of the issue. The maximum termspermitted are set forth in the statutes. In addition, for many projects, the maximum term may be determined in accordancewith useful life guidelines promulgated by the State Department of Revenue (“DOR”). Serial bonds and notes may beissued for the purposes set forth in the statutes. In addition, serial bonds and notes may be issued for any other public workimprovement or asset not specifically listed in the Statutes that has a useful life of at least 5 years. Bonds or notes may bemade callable and redeemed prior to their maturity, and a redemption premium may be paid. Refunding bonds or notesmay be issued subject to the maximum applicable term measured from the date of the original bonds or notes and mustproduce present value savings over the debt service of the refunded bonds. Generally, the first required annual payment ofprincipal of the refunding bonds cannot be later than the first principal payment of any of the bonds or notes being refunded

10

thereby, however, principal payments made before the first principal payment of any of the bonds or notes being refundedthereby may be in any amount.

Serial bonds may be issued as “qualified bonds” with the approval of the state Municipal Finance Oversight Boardcomposed of the State Treasurer, the State Auditor, the Attorney General and the Director of Accounts, subject to suchconditions and limitations (including restrictions on future indebtedness) as may be required by the Board. Qualified bondsmay mature not less than 10 nor more than 30 years from their dates and are not subject to the amortization requirementsdescribed above. The State Treasurer is required to pay the debt service on qualified bonds and thereafter to withhold theamount of the debt service paid by the State from state aid or other state payments; administrative costs and any loss ofinterest income to the State are to be assessed upon the city or town.

Tax Credit Bonds or Notes. Subject to certain provisions and conditions, the officers authorized to issue bonds ornotes may designate any duly authorized issue of bonds or notes as “tax credit bonds” to the extent such bonds and notes areotherwise permitted to be issued with federal tax credits or other similar subsidies for all or a portion of the borrowing costs.Tax credit bonds may be made payable without regard to the annual installments required by any other law, and a sinkingfund may be established for the payment of such bonds. Any investment that is part of such a sinking fund may mature notlater than the date fixed for payment or redemption of the applicable bonds.

Bond Anticipation Notes. These generally must mature within two years of their original dates of issuance but may berefunded from time to time for a period not to exceed five years from their original dates of issuance, provided that for eachyear that the notes are refunded beyond the second year they must be paid in part from revenue funds in an amount at leastequal to the minimum annual payment that would have been required if the bonds had been issued at the end of the secondyear. For certain school projects, however, notes may be refunded from time to time for a period not to exceed seven yearswithout having to pay any portion of the principal of the notes from revenue funds. The maximum term of bonds issued torefund bond anticipation notes is measured (except for certain school projects) from the date of the original issue of thenotes.

Revenue Anticipation Notes. These are issued to meet current expenses in anticipation of taxes and other revenues.They must mature within one year but, if payable in less than one year, may be refunded from time to time up to one yearfrom the original date of issue.

Grant Anticipation Notes. These are issued for temporary financing in anticipation of federal grants and state andcounty reimbursements. Generally, they must mature within two years but may be refunded from time to time as long asthe municipality remains entitled to the grant or reimbursement.

Revenue Bonds. Cities and towns may issue revenue bonds for solid waste disposal facilities, for projects financedunder the Commonwealth’s Water Pollution Abatement or Drinking Water Revolving Loan Programs and for certaineconomic development projects supported by tax increment financing. In addition, cities and towns having electricdepartments may issue electric revenue bonds and notes in anticipation of such bonds, subject to the approval of the StateDepartment of Telecommunications and Energy.

Revenue Anticipation Borrowing

Revenue anticipation notes are issued to meet current expenses in anticipation of taxes and other revenues. Theamount borrowed in each fiscal year by the issue of revenue anticipation notes is limited to the tax levy of the prior fiscalyear, together with the net receipts in the prior fiscal year from the motor vehicle excise and certain payments made by theCommonwealth in lieu of taxes. The fiscal year ends on June 30. Notes may mature in the following fiscal year, and notesmay be refunded into the following fiscal year to the extent of the uncollected, unabated current tax levy and certain otheritems, including revenue deficits, overlay deficits, final judgments and lawful unappropriated expenditures, which are to beadded to the next tax levy, but excluding deficits arising from a failure to collect taxes of earlier years. (See “Taxation toMeet Deficits” under “Property Tax” below.) In any event, the period from an original borrowing to its final maturitycannot exceed one year. The City has not issued revenue anticipation notes in the last five fiscal years.

11

Debt SummaryAuthorized

Unissued

Outstanding Bonds

11/1/2013 11/1/2013

Long-Term Indebtedness (1)(2)(3)(4)

Within the General Debt Limit:

Sewers & Drains ……………………… $ 2,862,808 $ 29,500(5)

Land Acquisition ……………………… 95,000 -0-

Schools ………………………………… 5,651,290 79,886(5)

Other Building ………………………… 80,000 10,356,000(6)

Architectural & Engineering Services … -0- 450,000(7)

Athletic & Recreational Facilities …….. 90,000 -0-

Other Inside General ………………….. -0- 330,000(7)

Total Within the General Debt Limit …… $ 8,779,098 $ 11,245,386

Outside the General Debt Limit:

Sewers ………………………………… $ 6,715,531 $ 2,079,979(8)

Schools ……………………………….. 3,877,120 -0-

Other Outside General ……………….. 12,744 -0-

Water …………………………………. 15,018,342 2,992,000(9)

Total Outside the General Debt Limit ….. $ 25,623,737 $ 5,071,979

Total Long-Term Indebtedness …………. $ 34,402,834 $ 16,317,365

Outstanding

Outstanding After This

11/1/2013 Issue Maturity

Short-Term Indebtedness

Revenue Anticipation Notes ………….. $ -0- $ -0-

Grant Anticipation Notes …………….. -0- -0-

Bond Anticipation Notes ……………… 7,678,000 7,474,000 9/12/14; 12/12/14

Total Short-Term Indebtedness …………. $ 7,678,000 $ 7,474,000

_________________________

(1) Principal amount only. Excludes lease and installment purchase obligations, overlapping debt, unfunded pension liability

and other post employment benefit liabilities.

(2) At the present time the normal General Debt Limit is $98,036,995 and the Double General Debt Limit is $196,073,990.

(3) $ 9,169,864 has been exempted from the provisions of Proposition 2 1/2.

(4) $24,471,760 is self-supporting.

(5) This amount is not expected to be issued.

(6) Of this amount, $4,400,000 is included in this issue. $2,400,000 for public safety buildings, $5,900,000 for the DPW building

and $1,500,000 for leasehold improvements will be permanently financed in fiscal year 2015. The balance of $556,000 for

remodeling to the public safety buildings will be permanently financed in December 2013.

(7) Included in this issue of Notes.

(8) Amount remaining from a completed sewer project totaling $15,788,000 and this balance is not expected to be issued

(9) Of this amount, $1,654,000 will be permanently financed in December 2013, $1,203,000 is included in this issue of Notes and

the balance of $135,000 will be paid with available funds.

Authorized Unissued Bonds and Prospective Financing

The City has $16,317,365 outstanding in authorized unissued debt. A total amount of $2,189,365 representingunexpended balances of authorized and completed projects for water and school are not expected to be issued. TheCity expects to permanently finance $2,188,000 for water projects in December 2013. The City will have outstandingafter this issue a total of $7,474,000 bond anticipation notes; $1,600,000 for DPW facility construction, $1,203,000 forwater projects, $1,500,000 for leasehold improvements, $2,400,000 for public safety buildings remodeling, $330,000for parking garage and snow dump projects and $441,000 for planning and design. The City expects to proceed withconstruction in the spring of the remaining $4,300,000 for the DPW facility. The remaining balance of $166,000represents principal payments for various projects to be paid on December 13, 2013.

12

Five Years Outstanding DebtAs of June 30

2013 2012 2011 2010 2009

Long-Term Indebtedness(1)

Within the General Debt Limit:

Sewers & Drains ……………………… $ 3,143,873 $ 3,510,148 $ 3,870,788 $ 4,229,224 $ 4,584,356

Land Acquisition ……………………… 110,000 125,000 140,000 155,000 170,000

Schools ……………………………….. 6,166,190 6,686,090 7,205,990 7,726,960 8,249,100

Other Building ………………………… 90,000 104,950 119,923 134,771 149,683

Athletic & Recreational Facilities …….. 135,000 180,000 225,000 279,842 334,815

Other Inside General …………………. -0- -0- -0- 105,000 210,000

Total Within the General Debt Limit …… $ 9,645,063 $ 10,606,188 $ 11,561,701 $ 12,630,797 $ 13,697,954

Outside the General Debt Limit:

Sewers ………………………………… 7,372,455 8,010,788 8,641,530 9,261,365 9,874,466

Schools ……………………………….. 4,852,960 5,833,060 6,817,615 7,815,405 8,826,440

Other Outside General ……………….. 15,294 17,844 20,393 22,943 25,493

Water …………………………………. 15,943,452 16,460,422 7,139,154 3,954,102 4,356,352

Total Outside the General Debt Limit ….. $ 28,184,160 $ 30,322,114 $ 22,618,693 $ 21,053,815 $ 23,082,751

Total Long-Term Indebtedness ……….. $ 37,829,223 $ 40,928,302 $ 34,180,393 $ 33,684,612 $ 36,780,705

Short-Term Indebtedness

Revenue Anticipation Notes ………….. $ -0- $ -0- $ -0- $ -0- $ -0-

Grant Anticipation Notes …………….. -0- -0- -0- -0- -0-

Bond Anticipation Notes ……………… 7,678,000 5,740,000 10,311,481 4,401,000 3,452,000

Total Short-Term Indebtedness ……….. $ 7,678,000 $ 5,740,000 $ 10,311,481 $ 4,401,000 $ 3,452,000

Total Outstanding Indebtedness ……..… $ 45,507,223 $ 46,668,302 $ 44,491,874 $ 38,085,612 $ 40,232,705

_________________________

(1) Principal amount only. Excludes lease and installment purchase obligations, overlapping debt and unfunded pension liability.

Bonded Debt vs. Population, Valuations and IncomeAs of June 30

2013 2012 2011 2010 2009

Amount (1) ……………………………… $37,829,223 $40,928,302 $34,180,393 $33,684,612 $36,780,705

Per Capita (2) ……………………………. 2,287.83 2,475.25 2,082.77 2,068.70 2,201.38

Percent of Assessed Valuation (3) ………. 2.13% 2.22% 1.85% 1.77% 1.86%

Percent of Equalized Valuation (4) ……… 1.93 1.97 1.64 1.49 1.62

Per Capita as a percent of

Personal Income (2) per capita ………… 5.56 6.02 5.06 5.03 5.35

_________________________

(1) Principal amount only. Excludes lease and installment purchase obligations, overlapping debt and unfunded pension liability.

(2) Source: U.S. Department of Commerce, Bureau of the Census - Latest applicable actuals or estimates.

(3) Source: Board of Assessors - Assessed valuation as of the prior January 1.

(4) Source: Massachusetts Department of Revenue - Equalized valuation in effect for that fiscal year

(equalized valuations are established for January 1 of each even-numbered year).

13

Principal Repayment ScheduleBonds Estimated Total Total Cumulative

Fiscal Outstanding 11/01/13 (1)(2)(3) Dated Bond Debt MSBA Net Debt % Principal

Year Principal Interest 12/3/2013 Interest (4) Service Payments (5) Service Retired

2014 $ 74,740 $ 617,363 $ -0- $ 35,555 $ 727,659 $ -0- $ 727,659 0.2%

2015 3,536,851 1,125,998 183,000 68,136 4,913,984 766,765 4,147,219 10.4

2016 3,566,198 973,072 170,000 62,400 4,771,671 766,765 4,004,906 20.6

2017 3,455,875 822,418 160,000 57,038 4,495,331 766,765 3,728,566 30.5

2018 3,371,547 689,615 155,000 51,919 4,268,080 766,765 3,501,315 40.1

2019 2,439,312 591,732 155,000 46,881 3,232,925 -0- 3,232,925 47.2

2020 2,119,799 490,333 140,000 42,088 2,792,220 -0- 2,792,220 53.4

2021 2,153,114 420,178 140,000 37,538 2,750,830 -0- 2,750,830 59.6

2022 2,171,713 352,190 140,000 32,988 2,696,891 -0- 2,696,891 66.0

2023 2,180,601 270,073 140,000 28,438 2,619,112 -0- 2,619,112 72.3

2024 1,614,786 202,183 140,000 23,888 1,980,857 -0- 1,980,857 77.1

2025 1,244,273 161,673 140,000 19,338 1,565,284 -0- 1,565,284 80.9

2026 1,259,071 125,764 135,000 14,869 1,534,704 -0- 1,534,704 84.7

2027 834,183 98,832 130,000 10,562 1,073,577 -0- 1,073,577 87.3

2028 794,606 81,607 130,000 6,338 1,012,551 -0- 1,012,551 89.8

2029 805,370 64,295 130,000 2,112 1,001,777 -0- 1,001,777 92.4

2030 771,470 47,901 -0- -0- 819,372 -0- 819,372 94.5

2031 787,914 32,307 -0- -0- 820,222 -0- 820,222 96.7

2032 604,140 18,387 -0- -0- 622,527 -0- 622,527 98.6

2033 617,270 6,173 -0- -0- 623,443 -0- 623,443 100.0

Total $ 34,402,834 $ 7,192,094 $ 2,188,000 $ 540,088 $ 44,323,016 $ 3,067,060 $ 41,255,956

_________________________

(1) Excludes revenue anticipation notes, grant anticipation notes, bond anticipation notes, lease and installment purchase obligations,

overlapping debt, unfunded pension liability and other post employment benefits liability.

(2) Principal totaling $9,169,864 and interest totaling $1,913,126 has been exempted from the provisions of Proposition 2 ½, subject to

the provisions of Chapter 44, Section 20 of the General Laws.

(3) Principal totaling $24,471,760 and interest totaling $5,174,811 is self-supporting.

(4) Interest for this issue is estimated at 3.25%.

(5) Annual appropriation of debt service reimbursement from the Massachusetts School Building Authority.

Overlapping Debt

In addition to direct debt, the City is indirectly liable for a portion of the debt and other expenses incurred by variousoverlapping governmental authorities and agencies.

Counties. County expenses including debt service on county bonds are assessed upon the cities and towns within thecounty in proportion to their taxable valuation as last equalized by the State Commissioner of Revenue. (The expenses ofSuffolk County are borne by the City of Boston alone.) Legislation was enacted in 1997 abolishing the county governmentsof Franklin and Middlesex counties as of July 1, 1997, with their assets, functions, debts and other obligations beingassumed by the Commonwealth. The abolishment of the Middlesex county government was in part in response to defaultby the county in the payment of general obligation notes of the county. The legislation also abolished the countygovernments of Hampden and Worcester counties as of July 1, 1998. Legislation enacted in 1998 abolishes the countygovernments of Hampshire, Essex and Berkshire counties as of January 1, 1999, July 1, 1999 and July 1, 2000,respectively. The legislation also requires the state secretary for administration and finance to establish a plan to recover theCommonwealth’s expenditures for the liabilities and other debts assumed and paid by the Commonwealth on behalf of anabolished county. Unless these provisions are changed by further legislation, the state treasurer shall assess upon each cityand town within the jurisdiction of an abolished county an amount not to exceed or equal to the county tax paid by eachsuch city and town for the fiscal year immediately prior to the abolishment of the county until such expenditures by theCommonwealth are recovered. It is possible that similar legislation will be sought to provide for the abolishment of countygovernment in all the remaining counties.

Regional School Districts. Towns may organize regional school districts to carry out general or specialized educationalfunctions. Pursuant to special laws a number of cities may also participate in regional school districts, primarily forvocational education. The operating expenses and debt service of regional school districts are apportioned among the

14

member municipalities in accordance with the agreements establishing the districts subject to the provisions of theEducation Reform Act of 1993.

The City is a member of the Whittier Regional Vocational Technical School District. The Whittier RegionalVocational Technical School District has no outstanding bonded debt as of October 15, 2013. The City’s assessment forfiscal year 2014 is $829,206, which represents approximately 6.5% of the District’s operating budget. The other membertowns in the District are Haverhill, Newburyport, Merrimac, Georgetown, Ipswich, Groveland, West Newbury,Newbury, Rowley and Salisbury.

The City is not a member of the Essex North Shore Agricultural and Technical School District, and as a result is notapportioned and is not responsible for the District’s debt. The City’s payment for tuition-in students for fiscal year 2014 is$125,532.

Regional Transit Authorities. These are transportation authorities which have been established outside the Boston area.It has been state practice in recent years to provide a portion of their net cost of service, including debt service on theirbonds. In addition to the other sources of funds provided by Massachusetts General Laws Chapter 161B from which theregional transit authorities may obtain monies for the payment of the principal of and interest on their obligations, suchpayment will be further secured by the Commonwealth, which is required to pay to the regional transit authorities amountsduly certified by the administrator of the authority as necessary to pay any principal or interest due or about to come due forsuch purpose. The remainder of the net cost of service is assessed upon the member cities and towns in proportion to theamount of the net cost incurred on routes within each city or town. The aggregate amount of such assessments is generallynot permitted to increase by more than 2.5 percent per year. The City pays an annual assessment to the Merrimack ValleyRegional Transit Authority. The budgeted amount for fiscal year 2014 is $221,901. The City’s 1.65% share is based onmileage incurred by the MVRTA buses operating in Amesbury versus the system’s total mileage charged to the City.Membership in the MVRTA includes the City and fourteen other communities. Financing of $2,000,000 for theMcGovern Transportation Center was obtained through the Massachusetts Development and Finance Agency in theform of a revenue bond dated July 1, 2004 payable through July 2025. The bond is secured by all net revenuesgenerated by the parking garage. The MVRTA issued $12,000,000 Revenue Anticipation Notes dated June 21, 2013maturing June 20, 2014 to meet operating expenses for the fiscal year beginning July 1, 2014 pending the receipt ofrevenues of the MRVTA including the payment of Federal Transit Administration operating subsidies and state net costof service payments.

Other Regional Districts. Regional districts that include cities and towns, or parts thereof, may be organized under theGeneral Laws for certain other purposes, including water pollution abatement and solid waste disposal. Regional districtshave also been established under special laws for sewer and water purposes. The apportionment of operating expenses anddebt service of such districts is sometimes prescribed specifically by the laws under which they are organized; for othersuch districts the apportionment is determined in accordance with the agreements establishing the districts.

Capital Improvement Program

The City has a capital improvements program providing for annual financing of capital requests. The following isa list of capital outlay projects completed and those anticipated over the following fiscal years.

Fiscal Year

Department/Project 2014 2015 2016 2017 2018

General Government………. $ 239,720 $ 50,290 $ 47,090 $ 50,000 $ 50,000

Engineering………………… 780,000 2,300,000(1) 150,000 50,000 50,000

Fire………………………. 152,000 282,000 82,000 682,000 100,000

Community & Economic Dev. 40,000 125,000 100,000 100,000 100,000

Police…………………….. 240,000 210,000 140,000 150,000 150,000

Public Works……………… 1,600,000 5,300,000(2) 2,646,250(3) 1,020,250 916,100

Schools……………………. 149,300 360,000 135,000 150,000 500,000

Totals: $ 3,201,020 $ 8,627,290 $ 3,300,340 $ 2,202,250 $ 1,866,100

(1) $1,500,000 is for the replacement of a structurally deficient bridge.

(2) $2,000,000 is for the construction of the Riverwalk pedestrian path expected to be funded by state and federal grants. $3,300,000

is for the reconstruction of Hillside Avenue which is expected to be funded by state and federal grants.

(3) Includes various road maintenance projects, vehicle purchases and $861,000 for a replacement main along Market St.

15

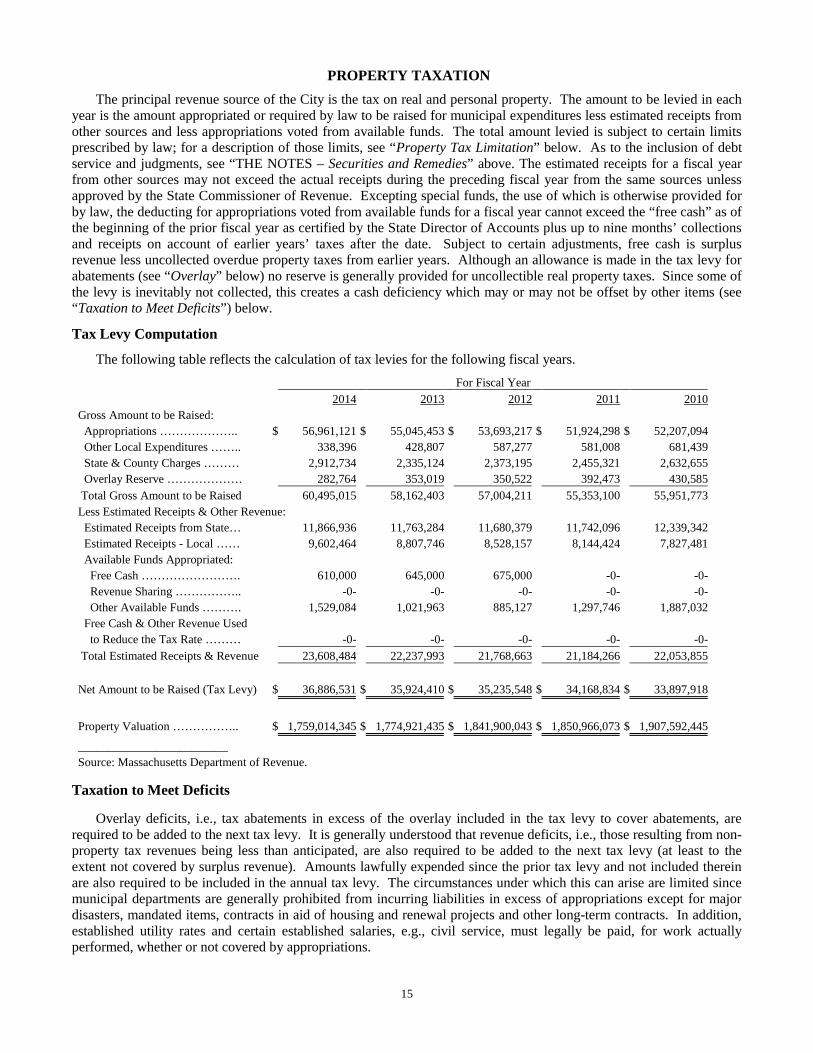

PROPERTY TAXATION

The principal revenue source of the City is the tax on real and personal property. The amount to be levied in eachyear is the amount appropriated or required by law to be raised for municipal expenditures less estimated receipts fromother sources and less appropriations voted from available funds. The total amount levied is subject to certain limitsprescribed by law; for a description of those limits, see “Property Tax Limitation” below. As to the inclusion of debtservice and judgments, see “THE NOTES – Securities and Remedies” above. The estimated receipts for a fiscal yearfrom other sources may not exceed the actual receipts during the preceding fiscal year from the same sources unlessapproved by the State Commissioner of Revenue. Excepting special funds, the use of which is otherwise provided forby law, the deducting for appropriations voted from available funds for a fiscal year cannot exceed the “free cash” as ofthe beginning of the prior fiscal year as certified by the State Director of Accounts plus up to nine months’ collectionsand receipts on account of earlier years’ taxes after the date. Subject to certain adjustments, free cash is surplusrevenue less uncollected overdue property taxes from earlier years. Although an allowance is made in the tax levy forabatements (see “Overlay” below) no reserve is generally provided for uncollectible real property taxes. Since some ofthe levy is inevitably not collected, this creates a cash deficiency which may or may not be offset by other items (see“Taxation to Meet Deficits”) below.

Tax Levy Computation

The following table reflects the calculation of tax levies for the following fiscal years.

For Fiscal Year

2014 2013 2012 2011 2010

Gross Amount to be Raised:

Appropriations ……………….. $ 56,961,121 $ 55,045,453 $ 53,693,217 $ 51,924,298 $ 52,207,094

Other Local Expenditures …….. 338,396 428,807 587,277 581,008 681,439

State & County Charges ……… 2,912,734 2,335,124 2,373,195 2,455,321 2,632,655

Overlay Reserve ………………. 282,764 353,019 350,522 392,473 430,585

Total Gross Amount to be Raised 60,495,015 58,162,403 57,004,211 55,353,100 55,951,773

Less Estimated Receipts & Other Revenue:

Estimated Receipts from State… 11,866,936 11,763,284 11,680,379 11,742,096 12,339,342

Estimated Receipts - Local …… 9,602,464 8,807,746 8,528,157 8,144,424 7,827,481

Available Funds Appropriated:

Free Cash ……………………. 610,000 645,000 675,000 -0- -0-

Revenue Sharing …………….. -0- -0- -0- -0- -0-

Other Available Funds ………. 1,529,084 1,021,963 885,127 1,297,746 1,887,032

Free Cash & Other Revenue Used

to Reduce the Tax Rate ……… -0- -0- -0- -0- -0-

Total Estimated Receipts & Revenue 23,608,484 22,237,993 21,768,663 21,184,266 22,053,855

Net Amount to be Raised (Tax Levy) $ 36,886,531 $ 35,924,410 $ 35,235,548 $ 34,168,834 $ 33,897,918

Property Valuation …………….. $ 1,759,014,345 $ 1,774,921,435 $ 1,841,900,043 $ 1,850,966,073 $ 1,907,592,445

_________________________

Source: Massachusetts Department of Revenue.

Taxation to Meet Deficits

Overlay deficits, i.e., tax abatements in excess of the overlay included in the tax levy to cover abatements, arerequired to be added to the next tax levy. It is generally understood that revenue deficits, i.e., those resulting from non-property tax revenues being less than anticipated, are also required to be added to the next tax levy (at least to theextent not covered by surplus revenue). Amounts lawfully expended since the prior tax levy and not included thereinare also required to be included in the annual tax levy. The circumstances under which this can arise are limited sincemunicipal departments are generally prohibited from incurring liabilities in excess of appropriations except for majordisasters, mandated items, contracts in aid of housing and renewal projects and other long-term contracts. In addition,established utility rates and certain established salaries, e.g., civil service, must legally be paid, for work actuallyperformed, whether or not covered by appropriations.

16

Cities and towns are authorized to appropriate sums, and thus to levy taxes, subject to any overall limits on taxlevies, to cover deficits arising from other causes, such as “free cash” deficits arising from a failure to collect taxes.This is not generally understood, however, and it has not been the practice to levy taxes to cover free cash deficits.Except to the extent that such deficits have been reduced or eliminated by subsequent collections of uncollected taxes(including sales of tax titles and tax possessions), lapsed appropriations, non-property tax revenues in excess ofestimates, other miscellaneous items or funding loans authorized by special act, they remain in existence.

Property Tax Limitation

Chapter 59, Section 21C of the General Laws, known as “Proposition 2 ½”, imposes two separate limits on theannual tax levy of a city or town.

The primary limitation is that the tax levy cannot exceed 2½ percent of the full and fair cash value. If a city ortown exceeds the primary limitation, it must reduce its tax levy by at least 15 percent annually until it is in compliance,provided that the reduction can be reduced in any year to not less than 7½ percent by majority vote of the voters, or toless than 7½ percent by two-thirds vote of the voters.

For cities and towns at or below the primary limit, a secondary limitation is that the tax levy cannot exceed themaximum levy limit for the preceding fiscal year as determined by the State Commissioner of Revenue by more than2½ percent, subject to exceptions for property added to the tax rolls or property which has had an increase, other thanas part of a general revaluation, in its assessed valuation over the prior year’s valuation.

This “growth” limit on the tax levy may be exceeded in any year by a majority vote of the voters, but an increasein the secondary or growth limit under this procedure does not permit a tax levy in excess of the primary limitation,since the two limitations apply independently. In addition, if the voters vote to approve taxes in excess of the “growth”limit for the purpose of funding a stabilization fund, such increased amount may only be taken into account forpurposes of calculating the maximum levy limit in each subsequent year if the board of selectmen of a City or theMunicipal Council of a city votes by a two-thirds vote to appropriate such increased amount in such subsequent year tothe stabilization fund.

The applicable tax limits may also be reduced in any year by a majority vote of the voters.

The State Commissioner of Revenue may adjust any tax limit “to counterbalance the effects of extraordinary,non-recurring events which occurred during the base year”.

The statute further provides that the voters may exclude from the taxes subject to the tax limits and from thecalculation of the maximum tax levy (a) the amount required to pay debt service on bonds and notes issued beforeNovember 4, 1980, if the exclusion is approved by a majority vote of the voters, and (b) the amount required to pay debtservice on any specific subsequent issue for which similar approval is obtained. Even with voter approval, the holders ofthe obligations for which unlimited taxes may be assessed do not have a statutory priority or security interest in the portionof the tax levy attributable to such obligations. It should be noted that Massachusetts General Laws Chapter 44, Section 20requires that the taxes excluded from the levy limit to pay debt service on any such bonds and notes be calculated based onthe true interest cost of the issue. Accordingly, the Department of Revenue limits the amount of taxes which may be leviedin each year to pay debt service on any such bonds and notes to the amount of such debt service, less a pro rata portion ofany original issue premium received by the city or town that was not applied to pay costs of issuance.

Voters may also exclude from the Proposition 2½ limits the amount required to pay specified capital outlayexpenditures or for the city or town’s apportioned share for certain capital outlay expenditures by a regional governmentalunit. In addition, the Municipal Council of a city, with the approval of the mayor if required, or the board of selectmen orthe Municipal Council of a City may vote to exclude from the Proposition 2½ limits taxes raised in lieu of sewer or watercharges to pay debt service on bonds or notes issued by the municipality (or by an independent authority, commission ordistrict) for water or sewer purposes, provided that the municipality’s sewer or water charges are reduced accordingly.

In addition, Proposition 2½ limits the annual increase in the total assessments on cities and towns by any county,district, authority, the Commonwealth or any other governmental entity (except regional school districts, the MWRA andcertain districts for which special legislation provides otherwise) to the sum of (a) 2½ percent of the prior year’sassessments and (b) “any increases in costs, charges or fees for services customarily provided locally or for servicessubscribed to at local option”. Regional water districts, regional sewerage districts and regional veterans districts mayexceed these limitations under statutory procedures requiring a two-thirds vote of the district’s governing body and either

17

approval of the local appropriating authorities (by two-thirds vote in districts with more than two members or by majorityvote in two-member districts) or approval of the registered voters in a local election (in the case of two-member districts).Under Proposition 2½ any State law to take effect on or after January 1, 1981 imposing a direct service or cost obligation ona city or town will become effective only if accepted or voluntarily funded by the city or town or if State funding isprovided. Similarly, State rules or regulations imposing additional costs on a city or town or laws granting or increasinglocal tax exemptions are to take effect only if adequate State appropriations are provided. These statutory provisions do notapply to costs resulting from judicial decisions.

Analysis of Property Tax Levies and Levy Limits

The following table reflects the calculation of levy limits for the following fiscal years.

For Fiscal Year

2014 2013 2012 2011 2010

Primary Levy Limit (1) ………… $ 43,975,359 $ 44,373,036 $ 46,047,501 $ 46,274,152 $ 47,689,811

Prior Fiscal Year Levy Limit …… $ 36,591,777 $ 35,387,755 $ 34,095,111 $ 32,642,326 $ 31,595,764

2.5% Levy Growth ……………. 914,794 884,694 852,378 816,058 789,894

New Growth (2) ……………….. 360,140 319,328 440,266 636,727 256,668

Overrides ………………………. -0- -0- -0- -0- -0-

Growth Levy Limit ……………. 37,866,711 36,591,777 35,387,755 34,095,111 32,642,326

Debt Exclusions ………………… 1,094,002 1,172,074 1,244,439 1,317,296 1,401,696

Capital Expenditure Exclusions … -0- -0- -0- -0- -0-

Other Adjustments …………….. -0- -0- -0- -0- -0-

Tax Levy Limit ………………… $ 38,960,713 $ 37,763,851 $ 36,632,194 $ 35,412,407 $ 34,044,022

Tax Levy ……………………….. 36,886,531 35,924,410 35,235,548 34,168,834 33,897,918

Unused Levy Capacity (3) …….. $ 2,074,182 $ 1,839,441 $ 1,396,646 $ 1,243,573 $ 146,104

Unused Primary Levy Capacity (4) $ 6,108,648$ 7,781,259$ 10,659,746$ 12,179,041$ 15,047,485

_________________________

Source: Massachusetts Department of Revenue.

(1) 2.5% of assessed valuation.

(2) Allowed increase for new valuations (or required reduction) - certified by the Department of Revenue.

(3) Tax Levy Limit less Tax Levy.

(4) Primary Levy Limit less Growth Levy Limit.

Pledged Taxes

Taxes on certain property in designated development districts may be pledged for the payment of costs of economicdevelopment projects within such districts and may therefore be unavailable for other municipal purposes (see “TAXINCREMENT FINANCING FOR DEVELOPMENT DISTRICTS” below).

Initiative Petitions

Various proposals have been made in recent years for legislative amendments to the Massachusetts Constitution toimpose limits on state and local taxes. To be adopted such amendments must be approved by two successive legislaturesand then by the voters at a state election.

Tax Rates and Valuations

Property is classified for the purpose of taxation according to its use. The legislature has in substance created threeclasses of taxable property: (1) residential real property, (2) open space land, and (3) all other (commercial, industrial andpersonal property). Within limits, cities and towns are given the option of determining the share of the annual levy to beborne by each of the three categories. The share required to be borne by residential real property is at least 50 per cent of itsshare of the total taxable valuation. The effective rate for open space must be at least 75 per cent of the effective rate forresidential real property and the share of commercial, industrial and personal property was limited to not more than 175 percent of their share of the total valuation. A city or town may also exempt up to 20 percent of the valuation of residential real

18

property (where used as the taxpayer’s principal residence) and up to 10 percent of the valuation of commercial realproperty (where occupied by certain small businesses). Property may not be classified in a city or town until the StateCommissioner of Revenue certifies that all property in the city or town has been assessed at its fair cash value. Suchcertification must take place every three years or pursuant to a revised schedule as may be issued by the Commissioner.

Related statutes provide that certain forest land, agricultural or horticultural land (assessed at the value it has for thesepurposes) and recreational land (assessed on the basis of its use at a maximum of 25 percent of its fair cash value) are all tobe taxed at the rate applicable to commercial property. Land classified as forest land is valued for this purpose at fivepercent of fair cash value but not less than ten dollars per acre. The following table reflects the breakdown of assessedvaluation by classification for the following fiscal years.

For Fiscal Year

2014 2013 2012 2011 2010

Real Property(1) ………………. $ 1,697,886,640 $ 1,712,518,670 $ 1,774,630,440 $ 1,789,017,540 $ 1,871,450,780

Personal Property(1) …………… 61,127,705 62,402,765 67,269,603 61,948,533 36,141,665

Total ………………………….. $ 1,759,014,345 $ 1,774,921,435 $ 1,841,900,043 $ 1,850,966,073 $ 1,907,592,445

Equalized Value(2) …………….. $ 1,960,739,900 $ 1,960,739,900 $ 2,078,441,100 $ 2,078,441,100 $ 2,266,894,100

Percent of Total Assessed

to Equalized Valuation ……….. 89.7% 90.5% 88.6% 89.1% 84.2%

_________________________

Source: Massachusetts Department of Revenue.

(1) As of the prior January 1st.

(2) Based on the equalized valuation in effect for each year.

In order to determine appropriate relative values for the purposes of certain distributions to and assessments uponcities and towns, the Commissioner of Revenue biennially makes his own redetermination of the fair cash value of thetaxable property in each municipality. This is known as the “equalized value”.

The following table reflects the trend in assessed valuations, equalized valuations and percentage of total assessedvaluation to equalized for the following fiscal years.

Fiscal 2014 % of Total Fiscal 2013 % of Total Fiscal 2012 % of Total

Assessed Assessed Assessed Assessed Assessed Assessed

Type of Property Valuation Valuation Valuation Valuation Valuation Valuation

Residential ……. $ 1,464,593,499 83.3% $ 1,478,695,853 83.3% $ 1,543,369,026 83.8%

Open Space …… -0- 0.0 -0- 0.0 -0- 0.0

Commercial …… 138,203,916 7.9 138,642,632 7.8 136,957,354 7.4

Industrial ……… 95,089,225 5.4 95,180,185 5.4 94,304,060 5.1

Personal ………. 61,127,705 3.5 62,402,765 3.5 67,269,603 3.7

Total $ 1,759,014,345 100.0% $ 1,774,921,435 100.0% $ 1,841,900,043 100.0%

_________________________

Source: Massachusetts Department of Revenue.

The following shows the actual rates per $1,000 of assessed valuation, and the full value rate as follows:

For Fiscal Year

Type of Property 2014 2013 2012 2011 2010

Residential and Open Space…..…… $20.97 $20.24 $19.13 $18.46 $17.77

Commercial, Industrial and Personal.. 20.97 20.24 19.13 18.46 17.77

Average Tax Rate …………….. $20.97 $20.24 $19.13 $18.46 $17.77

Full Value Tax Rate(1) …………. $18.81 $18.32 $16.95 $16.44 $14.95

_________________________

Source: Massachusetts Department of Revenue.

(1) Based on the equalized valuation in effect for each year.

19

Largest Taxpayers

The following is a list of the ten largest taxpayers for fiscal year 2013. All taxpayers are current in their taxpayments.

2013 % of

Assessed Amount Assessed

Name Nature of Business Valuation of Tax Valuation

New England Power Utility $ 27,143,410 $ 549,383 1.53%

National Grid Utility 15,656,170 316,881 0.88

Carriagetown Market Place Strip Mall 15,236,180 308,380 0.86

Ernest Cherry Residential Apartments 11,510,230 232,967 0.65

Ashley Abbot Residential Apartments 11,281,811 228,344 0.64

RRAB LTD Industrial 9,300,000 188,232 0.52

Zell Riverwalk Residential Apartments 8,374,110 169,492 0.47

New England Tel Telecom 7,524,100 152,288 0.42

Cargocaire Engineering Industrial 7,415,050 150,081 0.42

Henry Gagnon Residential Apartments 7,044,861 142,588 0.40

Total: $ 120,485,922 $ 2,438,636 6.79%

Tax Levies and Collections

The taxes for each fiscal year generally are due in two installments on November 1 (subject to deferral if tax billsare sent out late) and May 1. The City has accepted a statute, providing for quarterly tax payments; under that statute,preliminary tax payments are to be due on August 1, and November 1, with payment of the actual tax bill (after credit isgiven for the preliminary payments) in installments on February 1 and May 1 if actual tax bills are mailed by December31. Interest accrues on delinquent taxes currently at the rate of 14 percent per annum from the due date. Real property(land and buildings) is subject to a lien for the taxes assessed upon it (subject to any paramount federal lien and subjectto bankruptcy and insolvency laws). If the property has been transferred an unenforced lien expires on the fourthDecember 31, after the end of the fiscal year to which the tax relates. If the property has not been transferred by thefourth December 31, an unenforced lien expires upon a later transfer of the property. Provision is made, however, forcontinuation of the lien where it could not be enforced because of legal impediment. The persons against whom real orpersonal property taxes are assessed are personally liable for the tax (subject to bankruptcy and insolvency laws). Inthe case of real property, this personal liability is effectively extinguished by sale or taking of the property.

The following table reflects the total tax levy, the reserve for abatements, the net tax levy, and the amount of levycollected during the fiscal year payable. The total tax levy for fiscal year 2014 is expected to be $37,058,608, with anoverlay reserve for abatements of $350,000 resulting in the net tax levy of $36,708,608.

For Fiscal Year

2013 2012 2011 2010 2009

Total Tax Levy ………………… $ 35,924,410 $ 35,235,548 $ 34,168,834 $ 33,897,918 $ 32,683,452

Overlay Reserve for Abatements 353,019 350,522 392,473 430,585 411,631

Net Tax Levy(1) ……………… $ 35,571,391 $ 34,885,026 $ 33,776,361 $ 33,467,333 $ 32,271,822

Amount Collected

During Fiscal Year Payable(2) … $ 35,105,368 $ 33,988,254 $ 33,015,570 $ 32,843,410 $ 31,768,664

Percent of Net Tax Levy ……….. 98.7% 97.4% 97.7% 98.1% 98.4%

_________________________

(1) Net after deductions of overlay reserve for abatements.

(2) Actual collections of levy less refunds and amounts refundable but including proceeds of tax titles

and tax possessions attributed to such levy but not including abatements or other credits.

Overlay

The City is authorized by law to increase each tax levy by an amount approved as reasonable by the StateCommissioner of Revenue for an “overlay” to provide for tax abatements. If abatements are granted in excess of the

20

applicable overlay reserve, the resultant “overlay deficit” is required to be added to the next tax levy. Abatements aregranted where real or personal property has been overvalued or disproportionately valued. The assessors may alsoabate uncollectible personal property taxes. They may abate real and personal property taxes on broad grounds(including inability to pay) with the approval of the State Commissioner of Revenue. Uncollectible real property taxesare ordinarily not written off until they become municipal tax titles (either by purchase at the public sale or by taking),at which time the tax is written off in full by reserving the amount of tax and charging surplus. The following tablereflects the total tax levy, the reserve for abatements, the amount of abatements granted during the fiscal year of thelevy.

For Fiscal Year

2013 2012 2011 2010 2009

Total Tax Levy ………………… $ 35,924,410 $ 35,235,548 $ 34,168,834 $ 33,897,918 $ 32,683,452

Overlay Reserve for Abatements 353,019 350,522 392,473 430,585 411,631

Percent of Tax Levy(1) ……… 1.0 % 1.0 % 1.1 % 1.3 % 1.3 %

Abatements Granted:

During Fiscal Year Payable(2) … $ 155,703 $ 147,322 $ 231,948 $ 229,790 $ 295,537

Percent of Tax Levy ……….. 0.4 % 0.4 % 0.7 % 0.7% 0.9%

_________________________

(1) Net after deductions of overlay reserve for abatements.

(2) Actual collections of levy less refunds and amounts refundable but including proceeds of tax titles

and tax possessions attributed to such levy but not including abatements or other credits.

Taking and Sale

Massachusetts law permits a municipality either to sell by public sale (at which the municipality may become thepurchaser) or to take real property for non-payment of taxes thereon. In either case the property owner can redeem theproperty by paying the unpaid taxes, with interest and other charges, but if the right of redemption is not exercisedwithin six months (which may be extended an additional year in the case of certain installment payments) it can beforeclosed by petition to the land court. Upon foreclosure, a tax title purchased or taken by the municipality becomes a“tax possession” and may be held and disposed of like any land held for municipal purposes. Cities and Citys areauthorized to sell delinquent property tax receivables by public sale or auction, either individually or in bulk.

Taxes Outstanding

Massachusetts law permits a municipality either to sell by public sale (at which the municipality may become thepurchaser) or to take real property for non-payment of taxes thereon. In either case the property owner can redeem theproperty by paying the unpaid taxes, with interest and other charges, but if the right of redemption is not exercisedwithin six months (which may be extended an additional year in the case of certain installment payments) it can beforeclosed by petition to the land court. Upon foreclosure, a tax title purchased or taken by the municipality becomes a“tax possession” and may be held and disposed of like any land held for municipal purposes. Cities and towns areauthorized to sell delinquent property tax receivables by public sale or auction, either individually or in bulk. Thefollowing table sets forth the amount of overdue property taxes, tax titles and possessions outstanding at the end of thelast five fiscal years.

The following table sets forth the amount of overdue property taxes, tax titles and possessions outstanding at theend of the last five fiscal years.

For Fiscal Year

2013 2012 2011 2010 2009

Aggregate(1) ………………………. $ 976,850 $ 1,012,321 $ 837,397 $ 764,488 $ 950,039

Tax Titles …………………………. 1,607,159 1,434,972 1,408,653 1,489,363 1,118,219

Tax Possessions (2)……………….. 990,827 956,781 891,196 897,347 890,681

Tax Anticipation Notes Outstanding -0- -0- -0- -0- -0-________________________________________________

(1) Excludes tax titles, tax possessions and abated taxes. Includes taxes in litigation, if any.

(2) The City has taken real property for nonpayment of taxes and foreclosed by petition to the Land Court. Upon foreclosure, the tax

title becomes a tax possession which the City may sell by public sale or dispose of in the same manner as other land held for

municipal purposes.

21

Community Preservation Act

The Massachusetts Community Preservation Act (the “CPA”) permits cities and towns that accept its provisions tolevy a surcharge on its real property tax levy and to receive state matching funds for the acquisition, creation,preservation, rehabilitation and restoration of open space, historic resources and affordable housing. The provisions ofthe CPA must be accepted by the voters of the city or town at an election after such provisions have first been acceptedby either a vote of the legislative body of the city or town or an initiative petition signed by 5% of its registered voters.

A city or town may approve a surcharge of up to 3% of the real property tax levy, and it may accept one or moreexemptions to the surcharge under the CPA, including an exemption for low-income individuals and families and forlow and moderate-income senior citizens, an exemption for $100,000 of the value of each taxable parcel of residentialreal property, and an exemption for commercial and industrial properties in cities and towns with classified tax rates.The surcharge is not counted in the total taxes assessed for the purpose of determining the permitted levy amount underProposition 2½ (see “Tax Limitations” under “PROPERTY TAXATION” above). A city or town may revoke itsacceptance of the provisions of the CPA at any time after 5 years from the date of such acceptance and may change theamount of the surcharge or the exemptions to the surcharge at any time, provided that any such revocation or changemust be approved pursuant to the same process as acceptance of the CPA.

Any city or town that accepts the provisions of the CPA will receive annual state matching grants to supplementamounts raised by its surcharge on the real property tax levy. The state matching funds are raised from certainrecording and filing fees of the registers of deeds. Those amounts are deposited into a state trust fund and aredistributed to cities and towns that have accepted the provisions of the CPA, which distributions are not subject toannual appropriation by the state legislature. The amount distributed to each city and town is based on a statutoryformula which requires that 80% of the amount in the state trust fund be used to match an equal percentage of theamount raised locally by each city and town, and that the remaining 20% of the amount in the fund be distributed onlyto those cities and towns that levy the maximum 3% surcharge based on a formula which takes into account equalizedproperty valuation and population, resulting in larger distributions to those communities with low valuations and smallpopulations. The total state distribution made to any city or town may not, however, exceed 100% of the amount raisedlocally by the surcharge on the real property tax levy.

The amounts raised by the surcharge on real property taxes and received in state matching funds are required to bedeposited in a dedicated community preservation fund. Each city or town that accepts the provisions of the CPA isrequired to establish a community preservation committee to study the community preservation needs of thecommunity and to make recommendations to the legislative body of the city or town regarding the communitypreservation projects that should be funded from the community preservation fund. Upon the recommendations of thecommittee, the legislative body of the city or town may appropriate amounts from the fund for permitted communitypreservation purposes or may reserve amounts for spending in future fiscal years, provided that at least 10% of the totalannual revenues to the fund must be spent or set aside for open space purposes, 10% for historic resource purposes and10% for affordable housing purposes.

The CPA authorizes cities and towns that accept its provisions to issue bonds and notes in anticipation of thereceipt of surcharge revenues to finance community preservation projects approved under the provisions of the CPA.Bonds and notes issued under the CPA are general obligations of the city or town and are payable from amounts ondeposit in the community preservation fund. In the event that a city or town revokes its acceptance of the provisions ofthe CPA, the surcharge shall remain in effect until all contractual obligations incurred by the city or town prior to suchrevocation, including the payment of bonds or notes issued under the CPA, have been fully discharged. The City ofAmesbury has not accepted the provisions of the Community Preservation Act.

22

ADDITIONAL INFORMATION

Budget and Appropriation Process

Within one hundred seventy days after the annual organization of the City government (normally on the first day ofthe year), the Mayor submits to the Municipal Council the annual budget in the form of a statement of the amountsrecommended for the proposed expenditures of the City for the next fiscal year. The annual budget is classified anddesignated so as to show separately with respect to each officer, department or undertaking for which an appropriationis recommended.

The Municipal Council may by majority vote make appropriations for the purpose recommended and may reduceor reject any amount recommended but, except on recommendation of the Mayor, may not increase any amount in orthe total of the annual budget, nor add thereto any amount for the purpose not included therein (except by two-thirdsvote for certain purposes deemed necessary by the Council no earlier than seven days after the Council has taken aformal vote requesting the inclusion of said addition).

If the Council fails to take action with respect to any amount recommended in the annual budget, either byapproving, reducing or rejecting the same, within forty five days after the receipt of the budget, such amount withoutany action of the Council becomes a part of the appropriations for the year and is available for the purpose specified.

If, upon the expiration of one hundred seventy days after the annual organization of the City government, theMayor has not submitted the annual budget, the Municipal Council is authorized to prepare said budget.

The school budget is limited to the total amount appropriated by the Municipal Council, but the school committeeretains full power to allocate the funds appropriated.

State and county assessments, the overlay for abatements in excess of overlays, principal and interest not otherwiseprovided for and final judgments are included in the tax levy whether or not included in the budget. Revenues are notrequired to be set forth in the budget but estimated non-tax revenues are taken into account by the assessors in fixingthe tax levy. (See “Property Taxation” above).

Operating Budget Trends

The following table sets forth the operating budgets for the following fiscal years as voted by the MunicipalCouncil. As such, said budgets reflect neither revenues nor state and county assessments and other mandatory itemsnor supplemental budget appropriations. See “Budget and Appropriation Process” above. Similarly, the budgetssummarized below exclude expenditures for “non-operating” or extraordinary items authorized by additional orders ofthe municipal council.

Water and Sewer operations are being accounted for in separate enterprise accounts and are excluded from thetable below.

Appropriated Appropriated Appropriated Appropriated Appropriated

Fiscal Year Fiscal Year Fiscal Year Fiscal Year Fiscal Year

2014 2013 2012 2011 2010

General Government…………….… $ 2,504,994 $ 3,033,239 $ 2,466,182 $ 2,504,438 $ 2,526,959

Public Safety………………………. 6,946,468 6,846,825 6,656,939 6,486,146 6,540,318

Health and Sanitation……………… 1,040,897 1,153,908 1,132,079 1,115,861 955,597

Public Works……………………… 1,583,277 1,534,547 1,488,091 1,474,200 1,380,605

Schools……………………………. 28,177,702 27,217,686 26,636,105 25,657,976 25,758,055

Library……………………………. 768,713 707,994 691,213 642,036 595,047

Parks and Recreation……………… 304,684 293,463 265,627 236,376 236,376

Veterans…………………………… 441,360 406,005 372,649 340,652 307,916

Debt and Interest…………………. 2,251,222 2,321,861 2,317,094 2,448,187 2,548,871

Insurance………………………….. 278,300 278,300 278,300 278,300 278,360

Employee Benefits……………….. 4,805,967 4,678,822 4,990,146 4,504,938 4,463,885