Overview of Southeast Bank Limited Southeast Bank Limited is a scheduled commercial bank in the private sector established under the ambit of Bank Company Act, 1991 and incorporated as a Public Limited Company under Companies Act, 1994 on March 12, 1995. The Bank started commercial banking operations on May 25, 1995. During this short span of time the Bank is successful in positioning itself as a progressive and dynamic financial institution in the country. The bank had been widely acclaimed by the business community, from small entrepreneurs to large traders and industrial conglomerates, including the top-rated corporate borrowers for its forward – looking business outlook and innovative financial solutions. Thus within this very short period of time it has been able to create an image and earn significant reputation in the country’s banking sector as a Bank with Vision. Presently, it has 41 branches. Southeast Bank Limited has been licensed by the Government of Bangladesh as a Scheduled commercial bank in the private sector in pursuance of the policy of liberalization of banking and financial services and facilities in Bangladesh. In view of the above, the Bank within a period of 10 years of its operation achieved a remarkable success and met up capital adequacy requirement of Bangladesh Bank. It has been growing fast as one of the leaders of the new generation banks in the private sector in respect of business and profitability as it is evident from the financial statements for the last 10 years. Southeast Bank Limited emerged as a new commercial bank to provide efficient banking services and to contribute socio-economic development of the country. . Southeast Bank Limited(SEBL) was established on 17th April, 1995 with an Authorized Capital of Tk. 1000 Million and Paid up Capital of Tk. 100 Million (raised to Tk. 200 Million in 1997) by a group of highly successful entrepreneurs from various fields of economic activities such as shipping, oil, finance, garments, textiles and insurance etc. It is a full licensed scheduled Commercial Bank set up in the private sector in pursuance of the policy of the Government to liberalize Banking & Financial services. The Chairman of the Bank, Mr. Md. Nader Khan is a renowned business elite of Chittagong. He is also the Chairman of Drum Kulshi Girls High School, Fatikchari, Chittagong and Vice- President of the Governing Body of CIDER International School and also a member of the CIDER Trust. He has also been elected as Vice-District Governor of Lion District 315 B4 for the year 1999-2000.

Transcript

Overview of Southeast Bank Limited

Southeast Bank Limited is a scheduled commercial bank in the private sector established

under the ambit of Bank Company Act, 1991 and incorporated as a Public Limited Company

under Companies Act, 1994 on March 12, 1995. The Bank started commercial banking

operations on May 25, 1995. During this short span of time the Bank is successful in positioning

itself as a progressive and dynamic financial institution in the country. The bank had been

widely acclaimed by the business community, from small entrepreneurs to large traders and

industrial conglomerates, including the top-rated corporate borrowers for its forward – looking

business outlook and innovative financial solutions. Thus within this very short period of time

it has been able to create an image and earn significant reputation in the country’s banking

sector as a Bank with Vision. Presently, it has 41 branches.

Southeast Bank Limited has been licensed by the Government of Bangladesh as a Scheduled

commercial bank in the private sector in pursuance of the policy of liberalization of banking

and financial services and facilities in Bangladesh. In view of the above, the Bank within a

period of 10 years of its operation achieved a remarkable success and met up capital adequacy

requirement of Bangladesh Bank. It has been growing fast as one of the leaders of the new

generation banks in the private sector in respect of business and profitability as it is evident

from the financial statements for the last 10 years.

Southeast Bank Limited emerged as a new commercial bank to provide efficient banking

services and to contribute socio-economic development of the country. . Southeast Bank

Limited(SEBL) was established on 17th April, 1995 with an Authorized Capital of Tk. 1000

Million and Paid up Capital of Tk. 100 Million (raised to Tk. 200 Million in 1997) by a group of

highly successful entrepreneurs from various fields of economic activities such as shipping,

oil, finance, garments, textiles and insurance etc. It is a full licensed scheduled Commercial

Bank set up in the private sector in pursuance of the policy of the Government to liberalize

Banking & Financial services.

The Chairman of the Bank, Mr. Md. Nader Khan is a renowned business elite of Chittagong.

He is also the Chairman of Drum Kulshi Girls High School, Fatikchari, Chittagong and Vice-

President of the Governing Body of CIDER International School and also a member of the

CIDER Trust. He has also been elected as Vice-District Governor of Lion District 315 B4 for

the year 1999-2000.

The former Government of the Bangladesh Bank Mr. Lutfar Rahman Sarkar was the first

Managing Director of the Bank. The Bank is being managed by highly professional people

having wide experience in domestic and international Banking.

The present Managing Director Mr. Kazi Abdul Mazid has long experience in domestic and

international Banking. The Bank has made significant process within a very short time due to

its very competent Board of Directors, dynamic management and introduction of various

customer friendly deposit and loan products. The Authorized Capital of the Bank is Tk. 3000

million and the Paid -up Capital is Tk. 1199.12 million.

The Bank provides a broad range of financial services to its customers and corporate clients.

The Board of Directors consists of eminent personalities from the realm of commerce and

industries of the country.

The Bank is manned and managed by qualified and efficient professionals. The name of the

honorable chairman is Md. Abdul jalil, Mr. Shah Md. Nurul Alam is the Managing Director and

CEO of the bank. He brings with him a wealth of experience of managing private sector banks

in the country.

The Bank is not depending only on interest earnings; rather it strives hard to go for fee-based

income from non-fund activities of the bank. This type of business include capital market

operations like underwriting, portfolio management, mutual fund management, investors’

account as well as commission based business like Letter Of Guarantee, Inland remittance,

Foreign remittance etc. These businesses usually do not involve Bank’s fund, but on the

contrary, offer immense opportunity and scope to expand bank services to the members of

public at large. The head office of the Bank is situated at 61, Dilkusha Commercial Area, Dhaka

1000.

Board of Directors:

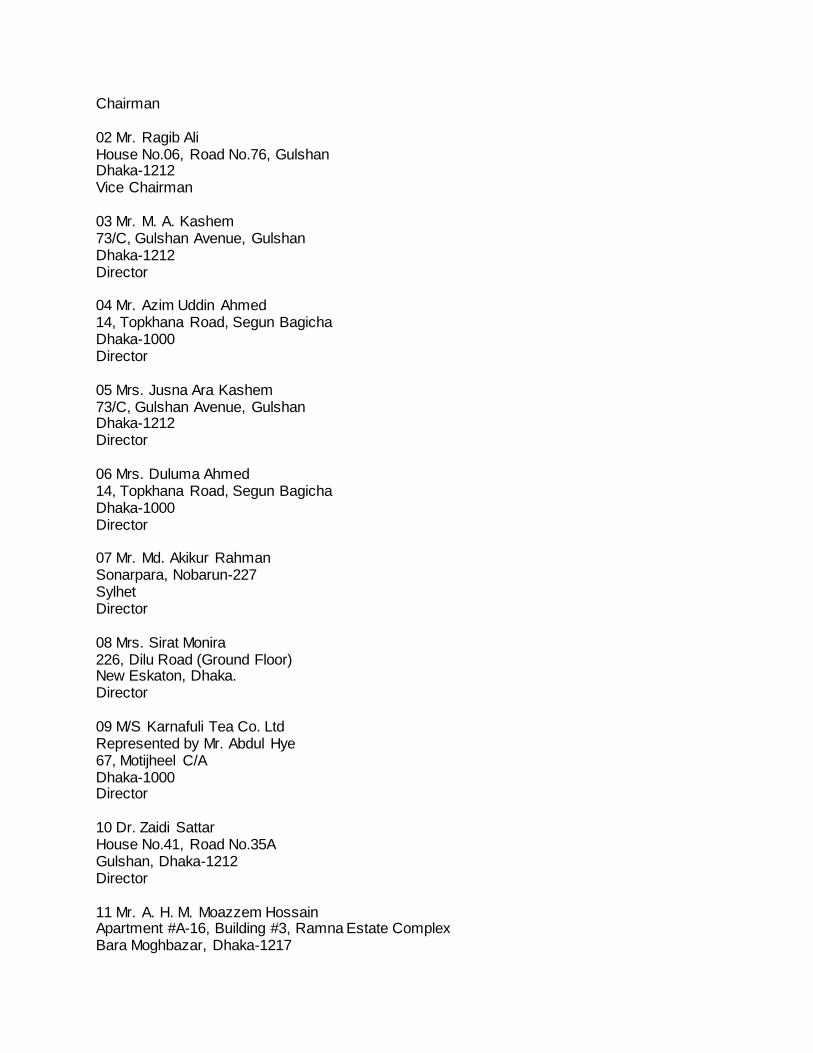

List of Directors:

01 Mr. Alamgir Kabir, FCA. 226, Dilu Road, New Eskaton. Dhaka.

Chairman 02 Mr. Ragib Ali House No.06, Road No.76, Gulshan Dhaka-1212 Vice Chairman 03 Mr. M. A. Kashem 73/C, Gulshan Avenue, Gulshan Dhaka-1212 Director 04 Mr. Azim Uddin Ahmed 14, Topkhana Road, Segun Bagicha Dhaka-1000 Director 05 Mrs. Jusna Ara Kashem 73/C, Gulshan Avenue, Gulshan Dhaka-1212 Director 06 Mrs. Duluma Ahmed 14, Topkhana Road, Segun Bagicha Dhaka-1000 Director 07 Mr. Md. Akikur Rahman Sonarpara, Nobarun-227 Sylhet Director 08 Mrs. Sirat Monira 226, Dilu Road (Ground Floor) New Eskaton, Dhaka. Director 09 M/S Karnafuli Tea Co. Ltd Represented by Mr. Abdul Hye 67, Motijheel C/A Dhaka-1000 Director 10 Dr. Zaidi Sattar House No.41, Road No.35A Gulshan, Dhaka-1212 Director 11 Mr. A. H. M. Moazzem Hossain Apartment #A-16, Building #3, Ramna Estate Complex Bara Moghbazar, Dhaka-1217

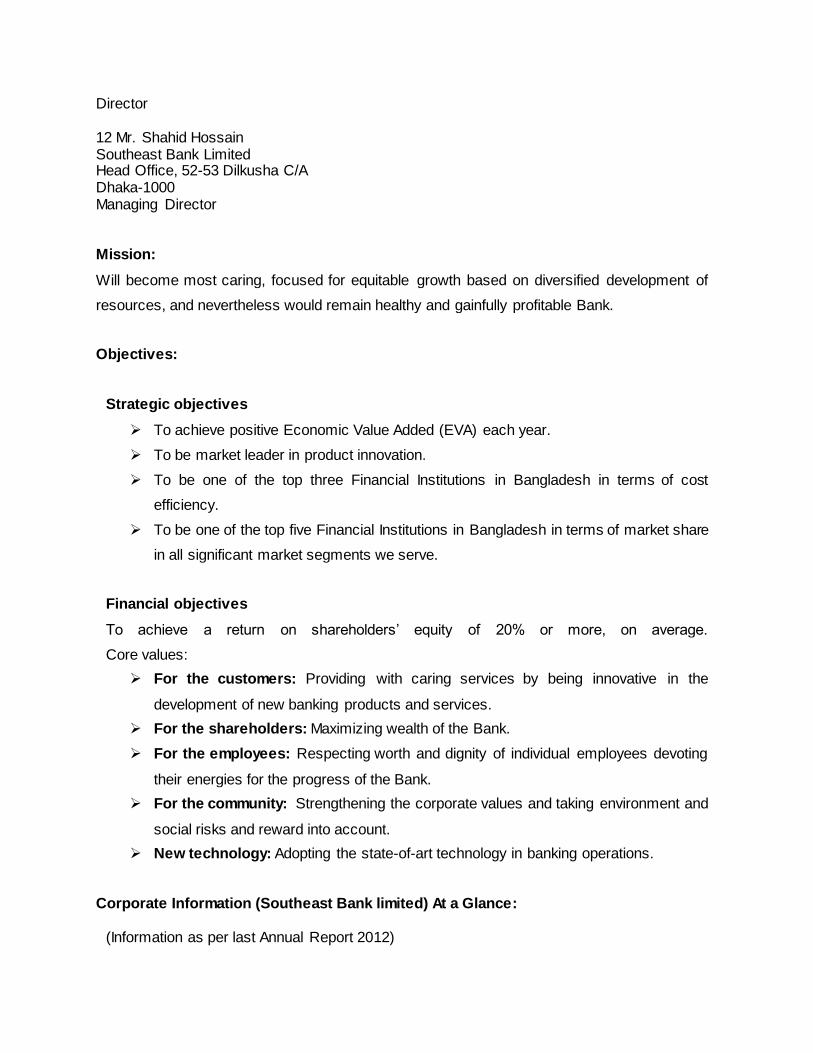

Director 12 Mr. Shahid Hossain Southeast Bank Limited Head Office, 52-53 Dilkusha C/A Dhaka-1000 Managing Director

Mission:

Will become most caring, focused for equitable growth based on diversified development of

resources, and nevertheless would remain healthy and gainfully profitable Bank.

Objectives:

Strategic objectives

To achieve positive Economic Value Added (EVA) each year.

To be market leader in product innovation.

To be one of the top three Financial Institutions in Bangladesh in terms of cost

efficiency.

To be one of the top five Financial Institutions in Bangladesh in terms of market share

in all significant market segments we serve.

Financial objectives

To achieve a return on shareholders’ equity of 20% or more, on average.

Core values:

For the customers: Providing with caring services by being innovative in the

development of new banking products and services.

For the shareholders: Maximizing wealth of the Bank.

For the employees: Respecting worth and dignity of individual employees devoting

their energies for the progress of the Bank.

For the community: Strengthening the corporate values and taking environment and

social risks and reward into account.

New technology: Adopting the state-of-art technology in banking operations.

Corporate Information (Southeast Bank limited) At a Glance: (Information as per last Annual Report 2012)

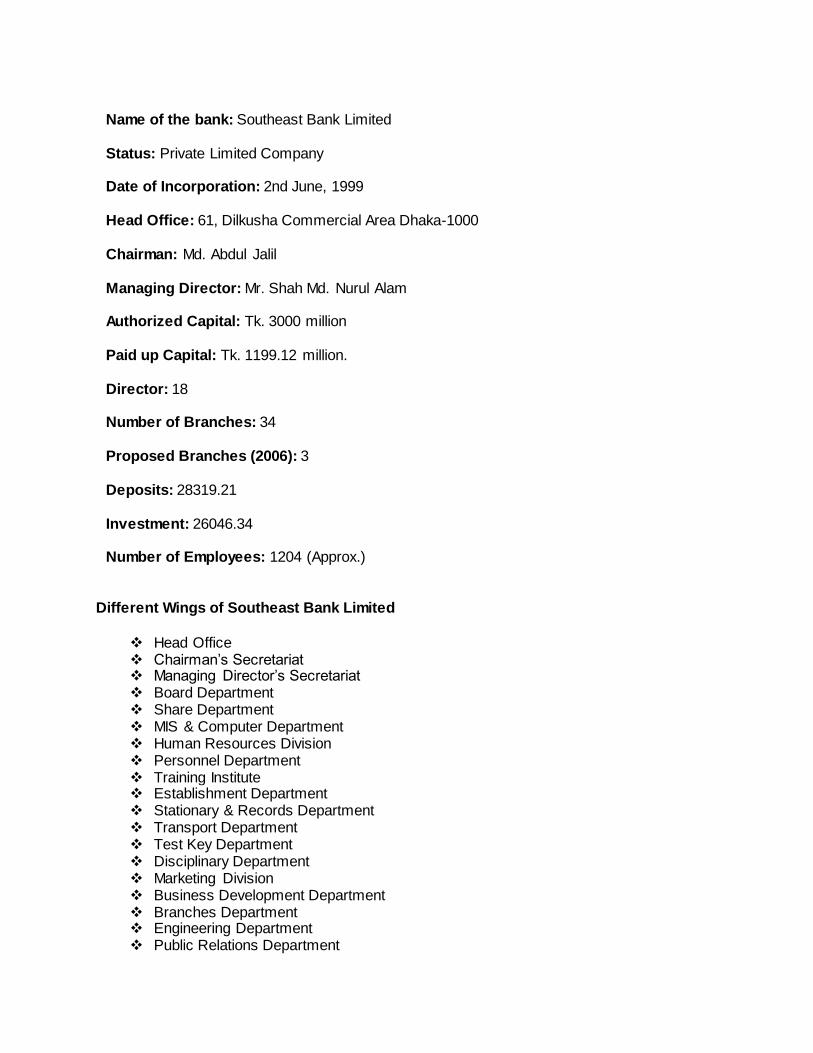

Name of the bank: Southeast Bank Limited

Status: Private Limited Company Date of Incorporation: 2nd June, 1999

Head Office: 61, Dilkusha Commercial Area Dhaka-1000

Chairman: Md. Abdul Jalil

Managing Director: Mr. Shah Md. Nurul Alam Authorized Capital: Tk. 3000 million

Paid up Capital: Tk. 1199.12 million.

Director: 18

Number of Branches: 34

Proposed Branches (2006): 3

Deposits: 28319.21

Investment: 26046.34 Number of Employees: 1204 (Approx.)

Different Wings of Southeast Bank Limited

Head Office Chairman’s Secretariat Managing Director’s Secretariat Board Department Share Department MIS & Computer Department Human Resources Division Personnel Department Training Institute Establishment Department Stationary & Records Department Transport Department Test Key Department Disciplinary Department Marketing Division Business Development Department Branches Department Engineering Department Public Relations Department

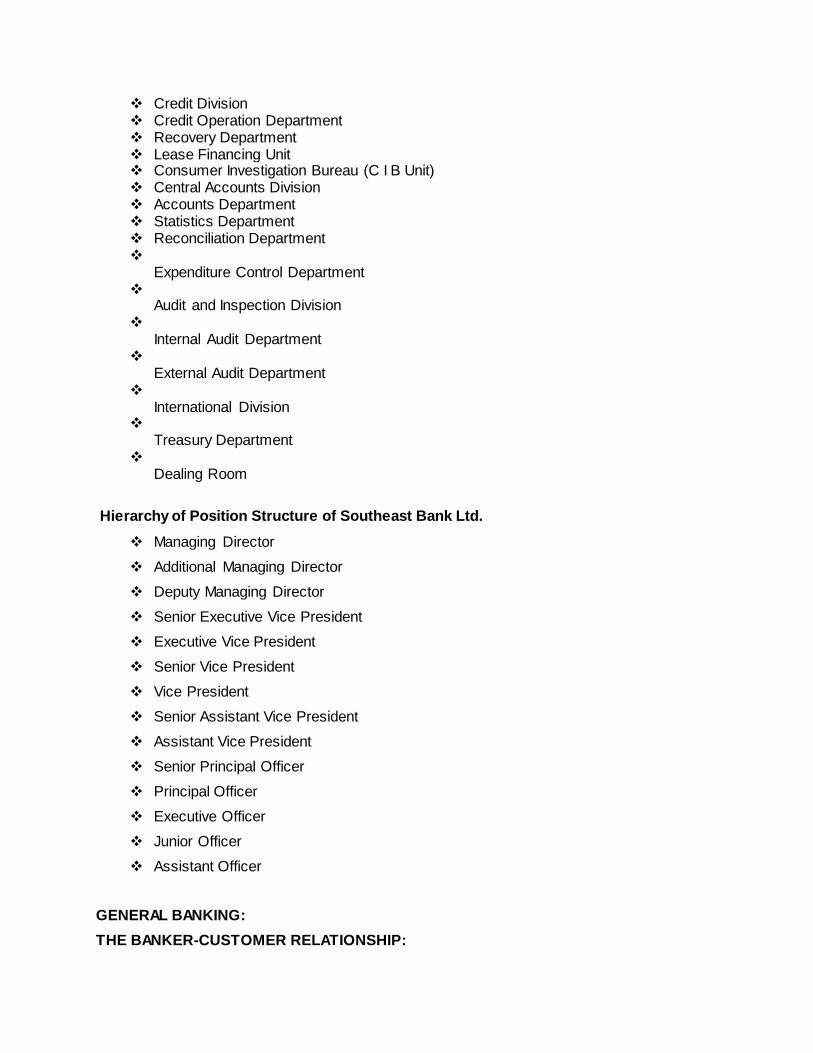

Credit Division Credit Operation Department Recovery Department Lease Financing Unit Consumer Investigation Bureau (C I B Unit) Central Accounts Division Accounts Department Statistics Department Reconciliation Department

Expenditure Control Department

Audit and Inspection Division

Internal Audit Department

External Audit Department

International Division

Treasury Department

Dealing Room

Hierarchy of Position Structure of Southeast Bank Ltd.

Managing Director

Additional Managing Director

Deputy Managing Director

Senior Executive Vice President

Executive Vice President

Senior Vice President

Vice President

Senior Assistant Vice President

Assistant Vice President

Senior Principal Officer

Principal Officer

Executive Officer

Junior Officer

Assistant Officer

GENERAL BANKING:

THE BANKER-CUSTOMER RELATIONSHIP:

The Banker-Customer relationship is essentially a debtor-creditor contractual relationship. This

relationship may be divided into two categories: Legal relationship & Behavioral relationship

after the contractual relationship is established between the banker and customer, they have

to avoid by some implied conditions of the contract as well as practices of the bank.

Some of the conditions and practices are as follows:

Customer is to use cheque books while demanding payment from his account.

Customer should keep cheque books in his safe custody.

Customer must inform the bank on time for any loss of cheque leaf or cheque books.

Customer while depositing money or presenting cheque, they must do that during

business hour of the bank.

Banker also should give necessary banking advice and help the customer in various

banking activities.

Rights of the Customer and Bank

Rights of a customer Duties & obligations of a bank

Right to deposit money in his A/C on time must credit the deposited amount to the

customer’s A/C.

Right to demand repayment by issuing cheque or written order properly in proper time

and place must honor cheque if otherwise in order

Right to get pass book/statement of A/C Must supply pass book/statement of A/C as

demanded

Right to stop payment on his cheque Must abide by the stop payment order

Right to give standing instructions Must abide by the instructions

Right to claim interest of his deposit balance in the interest bearing account Must

pay/credit interest as per rule

Right to have secrecy of his account must maintain secrecy of customer’s A/C if the

banker’s not bound to disclose it under certain conditions

Right to claim damages of any loss and for defamation due to wrongful/willful dishonor

of cheque by the bank must compensate the loss

Right to demand the proceeds of the instrument deposited for collection and collected

accordingly must collect the proceeds of the instrument in customer’s A/C and honor the

cheque drown against the amount

Right to claim money paid by bank from his A/C wrongly or payment is not made in due

courses. Payment should be made in due courses in good faith and without negligence

Right to return deposit if not in proper manner and time must deposit the amount properly

and in time.

Right to return the cheque if not drown properly or in time or for some other reason Must

demand payment by issuing cheque or written order properly

Termination of Banker-Customer Relationship:

The legal relation between banker and customer may be terminated with a notice given by

both of them with a view to close the account. Besides, there are some reasons for termination

of legal relationship. Some of these are stated below:

After the death of customer

When a customer declared insolvent by the court

When a customer become lunatic etc.

Forms of Deposit, Opening and Operation of Deposit Accounts and their legal Aspects:

The relationship between the banker and the customer begins with the opening of an account

by the customer. Initially all the accounts are opened with a deposit money by the customer and

hence these accounts are called deposit account. Actually in our country the bank deposits take

three different forms:

Current or Demand Deposit

Savings Deposit

Fixed or Time Deposit

Current or Demand Deposit:

Current account is purely a demand deposit account. It is a running and active account, which

may be operated upon any number and the amount of withdrawal from a current account. It is

noted that the bank does not provide any interest on current account. The special characteristic

of a current account are as follows:

The primary objective of current account is to save big customers as big

businessman, joint stock companies, private limited companies, public limited

companies etc. from the risk of handling cash themselves.

The cost of providing current account facilities is considerable to the bank since they

undertake to make payments and collects the bills, drafts, cheques for any number

of times daily. The bank therefore does not pay interest on current deposit while on

the other hand some banks charge for incidental charges on such account.

For opening of a current account minimum deposit of Taka 1000/= is required.

Introductory reference is also required for opening of such account.

DOCUMENTATION:

PROPRIETORSHIP:

Trade License

Photograph

PARTNERRSHIP;

Trade License

Photograph

Partnership Deed

PRIVATE LIMITED:

Trade License

Photograph of Directors

Certified copy of Memorandum and Articles of Association

Certificate of incorporation

List of Directors as per return of joint stock company with signature

Resolution for opening account with the bank

PUBLIC LIMITED:

Trade License

Photograph of Directors

Certified copy of Memorandum and Articles of Association

Certificate of incorporation

Certificate of commencement of business

List of Directors as per return of joint stock Company with signature

Resolution for opening account with the bank.

FORMALITIES:

Application on the prescribed form:

The person desiring to open a current account with the bank has to make application in the

prescribed form. This form must be properly filled up and signed by the applicants.

Introduction of the application

The applicant also required to furnish in the application form the names of the referees

from whom the banker may make inquiries regarding the character, integrity and

respectability of the applicants. In most cases the introduction is done by the customer

of the bank of some other person known to the bank by signing on the application form

with his/her account number (if any).

Specimen Signature

Every customer is required to supply to the bank with one or more specimens of his/her

signature. These signatures are taken on cards, which are preserved by the bank, and

the signature of the account holder on the cheques is compared with the specimen

signature.

Mandate for operation of the account by an agent

In case a customer desires to get his/her account operated upon by another person

then the bank will obtain a mandate in writing to that effects as well as the specimen

signature of the person in whose favor the mandate is given.

Opening and operating the account

After the above formalities are over, the banker opens an account in the name of applicant.

Generally the minimum amount to be deposited initially is Taka 1000.00 for opening a current

account. Then the bank provides the customer with:

A Pay-in-Slip/Deposit Book: With a view to facilitate the receipt of credit items paid in by a

customer, the bank will provide him/her pay-in-slip either loose or in a book forms. The

customer has to fill up the pay-in-slip at the time of depositing the money to the bank. The

cashier with his/her initials and stamps will return the counterfoil to the customer on the receipt

of the money.

Cheque book: To facilitate withdrawals and payment to third parties by the customer, the bank

will also provide a Chequebook to the customer. But it is noted that to get a Chequebook, the

customer has to dully fill up the cheque requisition slip to the banker.

SAVINGS ACCOUNT (SB)

Savings Bank (SB) Account is designed for individual savers who want to save a small part of

their income which may be used in the near future and also intend to have some profitable

returns on such savings. They can deposit a small amount and can withdraw whenever they

desire but the total numbers of withdrawals over a period of time are limited.

Features and Benefits:

Bank pays attractive interest.

Personalized MICR Cheque Book is available.

Nominal service charge.

Any branch banking facility (Cash withdrawal and deposit from any branch).

Bank accepts Standing Instructions from A/C holders.

Nomination facility is available to nominate beneficiary for account proceeds.

Interest is payable on half yearly basis.

Charge free statement of A/C, Balance Confirmation Certificate twice in a year on half

yearly basis.

Option is available to collect e - Statement on monthly basis.

Eligibility

Age: 18 years or above.

Single/Joint account can be opened.

Minor account can be opened under the supervision of his / her / their guardian.

Requirements

Applicants must satisfy the following documentation requirements for Personal Banking:

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License;

Two copies of recent passport size photograph duly attested by the introducer.

The account requires an introduction by an existing account holder with satisfactory

transaction records in Southeast Bank Limited.

Tin Certificate.

Proof of communication address: Photocopy of an Electricity Bill / Gas Bill / Wasa Bill /

Telephone Bill.

Initial deposit of Tk 2,000/- for urban clients and Tk 1,000/- for rural clients.

Nominee form and photograph of nominee(s) (signature attested by the account holder).

In case of minor nominee, copy of the birth certificate and photograph required;

Personal Information Form.

Transaction Profile.

KYC Form.

Account Opening Form to be duly filled in and signed by A/C holder and to be

authenticated by Bank’s authorized officials.

Rate of Interest & Fees

Rate of Interest: Currently 6.00% (below Tk 1.00 lac), 6.50% (Tk 1.00 lac and above)

which is subject to change from time to time.

Fees and Charges: As per existing schedule of charges which is separately

displayed/shown on the web site.

Current Deposit (CD) Account

Current Deposit (CD) Account is a transactional account where there is no restriction on

number of transactions in the account. Current Deposit (CD) Account can be opened for

individuals and business concerns including non-profit organizations.

Features and Benefits:

Unlimited transactions (both deposit and withdrawals) are allowed.

Personalized MICR Cheque Book is available.

No withdrawal notification required.

Nominal service charge.

Any branch banking facility (Cash withdrawal and deposit from any branch).

Bank accepts Standing Instructions from A/C holders.

Nomination facility is available to nominate beneficiary for account proceeds.

Charge free statement of A/C, Balance Confirmation Certificate twice in a year on half

yearly basis.

Option is available to collect e - Statement on monthly basis.

Eligibility:

CD Account can be opened both for Individuals and Firms/Corporate/ Autonomous

Bodies etc.

CD Account can be opened both for resident and non - resident Bangladeshi Nationals.

Age bar for Personal CD Account: 18 years or above.

Single/Joint account can be opened.

Minor account can be opened under the supervision of his / her / their guardian.

Account can be opened in the name of Trust / Club / Association / Societies / Non -

Trading Concerns.

Requirements:

Applicants must satisfy the following documentation requirements:

Personal Banking:

For resident of Bangladesh:

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License.

Two copies of recent passport size photograph duly attested by the introducer.

Certified document(s) for source of income.

Tin Certificate.

Proof of communication address: Photocopy of an Electricity Bill / Gas Bill / Wasa Bill

/ Telephone Bill.

The account requires an introduction by an existing and satisfactory account holder of

Southeast Bank Limited.

Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients.

Nominee form and photograph of nominee(s) (signature attested by the account

holder). In case of minor nominee, a copy of the birth certificate and photograph

required;

Personal Information Form.

Transaction Profile.

KYC Form.

Account Opening Form to be duly filled in and signed by A/C holder and to be

authenticated by Bank’s authorized officials.

Additional Requirement for Non - resident of Bangladesh:

As per existing Foreign Exchange guidelines of Bangladesh Bank.

Photocopy of passport with valid visa and work permit attested by their respective

Embassy / Mission authority.

Two copies of passport size photograph duly attested by their respective Embassy /

Mission authority.

Tax Certificate issued by foreign country.

Form QA-22

Corporate Banking:

Sole Proprietorship Concern:

Copy of valid Trade License;

Permission of Board of Investment required for FC (Foreign Currency) Account;

Declaration for opening foreign currency account duly filled in and signed;

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License.

Two copies of recent passport size photograph duly attested by the introducer.

Certified document(s) for source of income.

Tin Certificate.

Proof of communication address: Photocopy of an Electricity Bill / Gas Bill / Wasa Bill /

Telephone Bill.

The account requires an introduction by an existing and satisfactory account holder of

Southeast Bank Limited.

Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients.

Nominee form and photograph of nominee(s) (signature attested by the account holder).

In case of minor nominee, a copy of the birth certificate and photograph required;

Personal Information Form.

Transaction Profile.

KYC Form.

Account Opening Form to be duly filled in and signed by A/C holder and to be

authenticated by Bank’s authorized officials.

Partnership Concern:

Copy of Partnership Deed of the Firm (Registered / At least notarized);

Firm Registration Certificate (if registered);

List of Partners with their addresses;

Copy of valid Trade License;

Permission of Board of Investment required for FC (Foreign Currency) Account;

Recent passport size photograph(s) of signatory / signatories attested by the

introducer. (Photograph(s) of the signatory / signatories of non - residents of

Bangladesh shall be attested by their respective Embassy / Mission authority);

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License.

(Photocopy of valid Passport of the signatory of non - residents of Bangladesh shall be

attested by the their respective Embassy / Mission authority);

Resolution of the partners of the firm for opening the account and authorization for its

operation duly certified by managing partner of the firm;

Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients.

Official Seal;

Tin Certificate (If Any);

Personal Information Form.

Transaction Profile;

KYC Form

Account Opening Form to be dully filled in and signed by A/C holder and to be

authenticated by Bank’s authorized officials.

Private Limited Company:

Certified true copy of Certificate of incorporation;

Certified true copy of the Memorandum & Articles of Association of the Company duly

attached;

Certified true copy of Form XII of the company;

Permission of Board of Investment required for FC (Foreign Currency) Account;

Extract of the Resolution of the Board Meeting of the Company for opening the account

and authorization of its operation duly certified by the Chairman / Managing Director of

the Company;

Recent passport size photograph(s) of signatory / signatories attested by the introducer.

(Photograph(s) of the signatory / signatories of non - residents of Bangladesh shall be

attested by the their respective Embassy / Mission authority);

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License.

(Photocopy of valid Passport of the signatory of non-residents of Bangladesh shall be

attested by the their respective Embassy / Mission authority);

List of Directors with addresses;

Copy of valid Trade License;

Official Seal with designation;

Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients.

Tin Certificate;

Personal Information Form.

Account Opening Form to be dully filled in and signed by A/C holder and to be

authenticated by Bank’s authorized officials.

Public Limited Company:

Certified true copy of Certificate of incorporation;

Certified true copy of certificate of commencement;

Certified true copy of the Memorandum & Articles of Association of the Company duly

attached;

Certified true copy of Form XII of the company;

Permission of Board of Investment required for FC (Foreign Currency) Account;

Extract of the Resolution of the Board Meeting of the Company for opening the account

and authorization of its operation duly certified by the Chairman / Managing Director of

the Company;

Recent passport size photograph(s) of signatory / signatories attested by the introducer.

(Photograph(s) of the signatory / signatories of non - residents of Bangladesh shall be

attested by the their respective Embassy / Mission authority);

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License.

(Photocopy of valid Passport of the signatory of non - residents of Bangladesh shall be

attested by the their respective Embassy / Mission authority);

List of Directors with addresses;

Copy of valid Trade License;

Official Seal with designation;

Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients.

Tin Certificate;

Personal Information Form.

Account Opening Form to be dully filled in and signed by A/C holder and to be

authenticated by Bank’s authorized officials.

Trusts / Clubs / Associations / Societies / Co - operatives / NGO / Non - trading Concerns:

Certified true copy of the constitution / By - Laws / Trust Deed / Memorandum and

Articles of Association;

Certificate of Registration of the Association / Club / Charity / Trust / Society / Co-

operative / NGO / Non - trading concern for inspection and return (along with a duly

certified photocopy for Bank’s records);

List of members of the Governing Body / Executive Committee of the Association / Club

/ Charity / Trust / Society / Co-operative / NGO / Non - trading concern with their

addresses;

Extract of Resolution of the Association / Club / Charity / Trust / Society / Co - operative

/ NGO / Non-trading concern for opening the account and authorization of its operation

duly certified by the Chairman / Secretary of the Association / Club / Charity / Trust /

Society / Co - operative / NGO / Non - trading concern etc.

Recent passport size photograph(s) of signatory / signatories attested by the introducer.

(Photograph(s) of the signatory / signatories of non - residents of Bangladesh shall be

attested by the their respective Embassy / Mission authority);

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License.

(Photocopy of valid Passport of the signatory of non - residents of Bangladesh shall be

attested by the their respective Embassy / Mission authority);

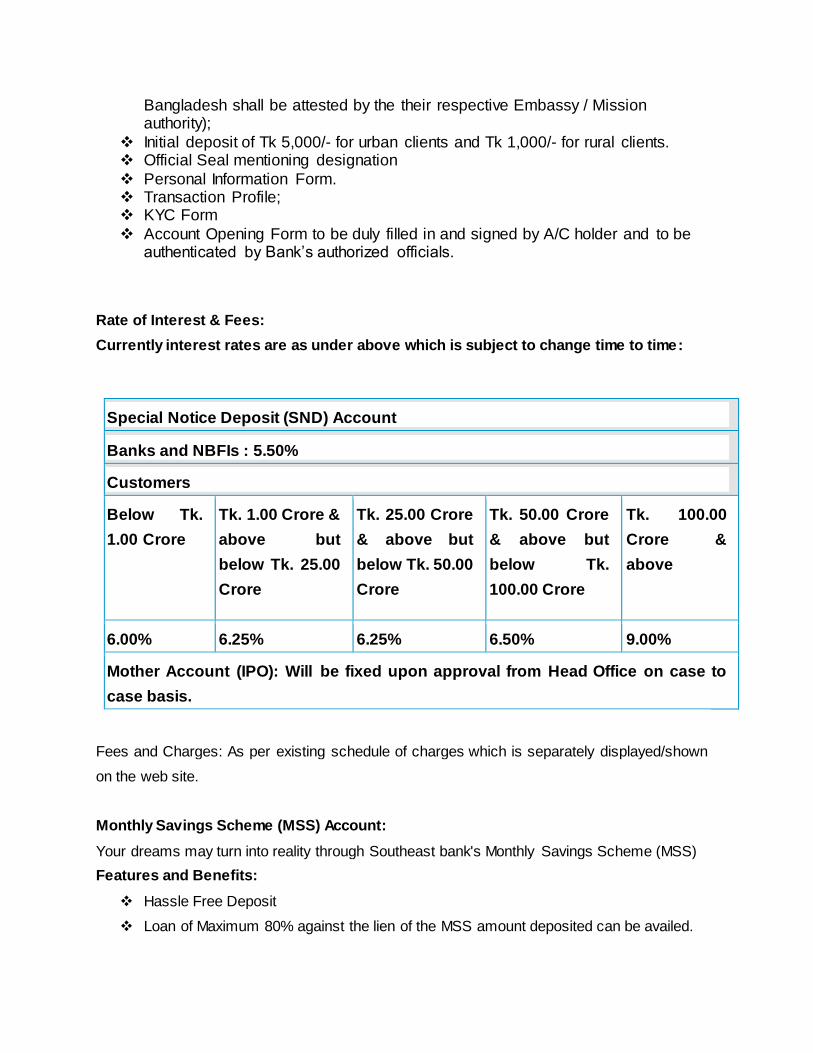

Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients.

Official Seal mentioning designation

Personal Information Form.

Transaction Profile;

KYC Form

Account Opening Form to be duly filled in and signed by A/C holder and to be

authenticated by Bank’s authorized officials.

Rate of Interest & Fees:

No Interest is paid on CD Account.

Fees and Charges: As per existing schedule of charges which is separately

displayed/shown on the web site.

FIXED DEPOSIT ACCOUNT (FDR)

Fixed Deposit Receipt (FDR) Account offers the customers the opportunity to invest a fixed

amount for a fixed period at a fixed rate of interest. The customers have the option to re - invest

their funds both principal amount and interest amount on maturity or principal amount and the

interest amount being paid into their SB or CD accounts.

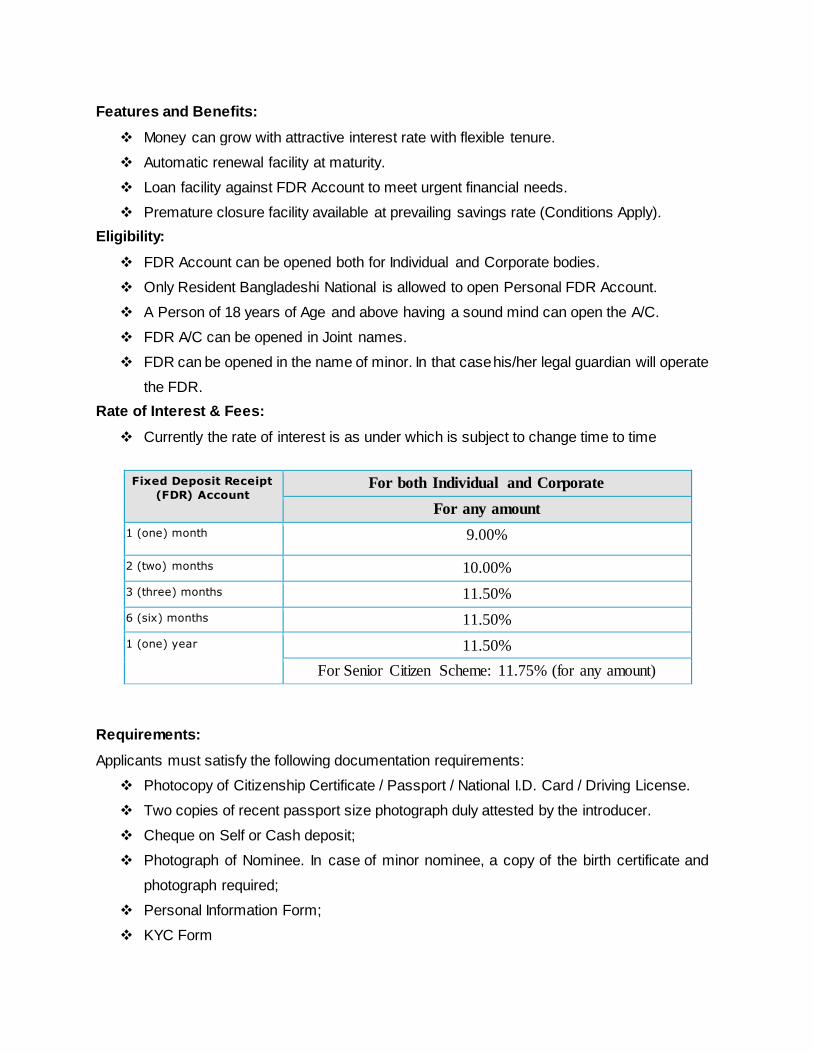

Features and Benefits:

Money can grow with attractive interest rate with flexible tenure.

Automatic renewal facility at maturity.

Loan facility against FDR Account to meet urgent financial needs.

Premature closure facility available at prevailing savings rate (Conditions Apply).

Eligibility:

FDR Account can be opened both for Individual and Corporate bodies.

Only Resident Bangladeshi National is allowed to open Personal FDR Account.

A Person of 18 years of Age and above having a sound mind can open the A/C.

FDR A/C can be opened in Joint names.

FDR can be opened in the name of minor. In that case his/her legal guardian will operate

the FDR.

Rate of Interest & Fees:

Currently the rate of interest is as under which is subject to change time to time

Fixed Deposit Receipt

(FDR) Account For both Individual and Corporate

For any amount

1 (one) month 9.00%

2 (two) months 10.00%

3 (three) months 11.50%

6 (six) months 11.50%

1 (one) year 11.50%

For Senior Citizen Scheme: 11.75% (for any amount)

Requirements:

Applicants must satisfy the following documentation requirements:

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License.

Two copies of recent passport size photograph duly attested by the introducer.

Cheque on Self or Cash deposit;

Photograph of Nominee. In case of minor nominee, a copy of the birth certificate and

photograph required;

Personal Information Form;

KYC Form

TIN Certificate.

Single/Joint A/C can be open.

Double Benefit Scheme (DBS) Account:

Double Benefit Scheme (DBS) Account is a time specified deposit scheme for clients where the

deposited money will be doubled on maturity.

Features and Benefits

Amount to be deposited TK 10,000 or its multiple;

Deposited amount will be doubled in 6 years;

Account can be opened at any working day of the month;

Allowed to open more than one DBS Account at any branch of the Bank;

Loan facility against lien of DBS Account;

The Scheme is covered by Insurance and Insurance Premium is borne by the bank;

Premature closure facility.

Eligibility:

DBS Account can be opened both for Individual and Corporate bodies.

Only Resident Bangladeshi National is allowed to open Personal DBS Account.

Age bar for opening of Personal DBS Account: 18 years or above.

Single/Joint account can be opened.

Minor account can be opened under the supervision of his / her / their guardian.

Requirements:

Applicants must satisfy the following documentation requirements:

Photocopy of Citizenship Certificate / Passport/ National I.D. Card / Driving License.

Two copies of recent passport size photograph duly attested by the introducer.

Certified document(s) for source of income.

TIN Certificate.

Cheque on Self or Cash deposit;

Single/Joint A/C can be opened

Fees and Charges: As per existing schedule of charges which is separately

displayed/shown in web site.

Special Notice Deposit (SND) Account:

Special Notice Deposit (SND) Account is an interest bearing deposit where advance notice of 7

to 30 days required for amount withdrawal. SND A/C is usually opened by Firms, Corporate

Financial Institution.

Features and Benefits:

Bank pays attractive interest.

Personalized MICR Cheque Book is available.

Nominal service charge.

Any branch banking facility (Cash withdrawal and deposit from any branch)

Bank accepts and supports Standing Instructions.

Nomination facility is available to nominate beneficiary for account proceeds.

Interest is payable on half yearly basis.

Charge free statement of A/C, Balance Confirmation Certificate twice in a year on half

yearly / yearly basis.

Option is available to collect e - Statement on monthly basis.

Eligibility:

SND Account can be opened by both Individual/Firms/Corporate bodies.

Age bar for Personal SND Account: 18 years or above.

Joint account can be opened.

Account can be opened in the name of Trust / Club / Association / Societies / Non -

Trading Concerns.

Requirements:

Applicants must satisfy the following documentation requirements:

Personal Banking:

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License.

Two copies of recent passport size photograph duly attested by the introducer. Certified document(s) for source of income. Tin Certificate.

Proof of communication address: Photocopy of an Electricity Bill / Gas Bill / Wasa Bill / Telephone Bill.

The account requires an introduction by an existing and satisfactory account holder of Southeast Bank Limited.

Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients.

Nominee form and photograph of nominee(s) (signature attested by the account holder). In case of minor nominee, a copy of the birth certificate and photograph

required; Personal Information Form. Transaction Profile.

KYC Form.

Account Opening Form to be duly filled in and signed by A/C holder and to be authenticated by Bank’s authorized officials.

Corporate Banking:

Sole Proprietorship Concern:

Copy of valid Trade License; Permission of Board of Investment required for FC (Foreign Currency) Account; Declaration for opening foreign currency account duly filled in and signed;

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License.

Two copies of recent passport size photograph duly attested by the introducer. Certified document(s) for source of income. Tin Certificate.

Proof of communication address: Photocopy of an Electricity Bill / Gas Bill / Wasa Bill / Telephone Bill.

The account requires an introduction by an existing and satisfactory account holder of Southeast Bank Limited.

Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients.

Nominee form and photograph of nominee(s) (signature attested by the account holder). In case of minor nominee, a copy of the birth certificate and photograph

required; Personal Information Form. Transaction Profile.

KYC Form. Account Opening Form to be duly filled in and signed by A/C holder and to be

authenticated by Bank’s authorized officials.

Partnership Concern:

Copy of Partnership Deed of the Firm (Registered / At least notarized); Firm Registration Certificate (if registered);

List of Partners with their addresses; Copy of valid Trade License; Permission of Board of Investment required for FC (Foreign Currency) Account;

Recent passport size photograph(s) of signatory / signatories attested by the introducer. (Photograph(s) of the signatory / signatories of non - residents of

Bangladesh shall be attested by their respective Embassy / Mission authority); Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving

License. (Photocopy of valid Passport of the signatory of non - residents of

Bangladesh shall be attested by the their respective Embassy / Mission authority);

Resolution of the partners of the firm for opening the account and authorization for its operation duly certified by managing partner of the firm;

Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients. Official Seal; Tin Certificate (If Any);

Personal Information Form. Transaction Profile;

KYC Form Account Opening Form to be dully filled in and signed by A/C holder and to be

authenticated by Bank’s authorized officials.

Private Limited Company:

Certified true copy of Certificate of incorporation; Certified true copy of the Memorandum & Articles of Association of the Company

duly attached;

Certified true copy of Form XII of the company; Permission of Board of Investment required for FC (Foreign Currency) Account;

Extract of the Resolution of the Board Meeting of the Company for opening the account and authorization of its operation duly certified by the Chairman / Managing Director of the Company;

Recent passport size photograph(s) of signatory / signatories attested by the introducer. (Photograph(s) of the signatory / signatories of non - residents of Bangladesh shall be attested by the their respective Embassy / Mission

authority); Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving

License. (Photocopy of valid Passport of the signatory of non-residents of Bangladesh shall be attested by the their respective Embassy / Mission authority);

List of Directors with addresses; Copy of valid Trade License;

Official Seal with designation; Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients. Tin Certificate;

Personal Information Form. Account Opening Form to be dully filled in and signed by A/C holder and to be

authenticated by Bank’s authorized officials.

Public Limited Company:

Certified true copy of Certificate of incorporation; Certified true copy of certificate of commencement;

Certified true copy of the Memorandum & Articles of Association of the Company duly attached;

Certified true copy of Form XII of the company; Permission of Board of Investment required for FC (Foreign Currency) Account;

Extract of the Resolution of the Board Meeting of the Company for opening the account and authorization of its operation duly certified by the Chairman /

Managing Director of the Company; Recent passport size photograph(s) of signatory / signatories attested by the

introducer. (Photograph(s) of the signatory / signatories of non - residents of

Bangladesh shall be attested by the their respective Embassy / Mission authority);

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License. (Photocopy of valid Passport of the signatory of non - residents of Bangladesh shall be attested by the their respective Embassy / Mission

authority); List of Directors with addresses;

Copy of valid Trade License; Official Seal with designation; Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients.

Tin Certificate;

Personal Information Form. Account Opening Form to be dully filled in and signed by A/C holder and to be

authenticated by Bank’s authorized officials.

Trusts / Clubs / Associations / Societies / Co - operatives / NGO / Non - trading Concerns:

Certified true copy of the constitution / By - Laws / Trust Deed / Memorandum

and Articles of Association; Certificate of Registration of the Association / Club / Charity / Trust / Society / Co-

operative / NGO / Non - trading concern for inspection and return (along with a

duly certified photocopy for Bank’s records); List of members of the Governing Body / Executive Committee of the Association

/ Club / Charity / Trust / Society / Co-operative / NGO / Non - trading concern with their addresses;

Extract of Resolution of the Association / Club / Charity / Trust / Society / Co -

operative / NGO / Non-trading concern for opening the account and authorization of its operation duly certified by the Chairman / Secretary of the Association /

Club / Charity / Trust / Society / Co - operative / NGO / Non - trading concern etc. Recent passport size photograph(s) of signatory / signatories attested by the

introducer. (Photograph(s) of the signatory / signatories of non - residents of

Bangladesh shall be attested by the their respective Embassy / Mission authority);

Photocopy of Citizenship Certificate / Passport / National I.D. Card / Driving License. (Photocopy of valid Passport of the signatory of non - residents of

Bangladesh shall be attested by the their respective Embassy / Mission authority);

Initial deposit of Tk 5,000/- for urban clients and Tk 1,000/- for rural clients. Official Seal mentioning designation

Personal Information Form. Transaction Profile; KYC Form

Account Opening Form to be duly filled in and signed by A/C holder and to be authenticated by Bank’s authorized officials.

Rate of Interest & Fees:

Currently interest rates are as under above which is subject to change time to time:

Special Notice Deposit (SND) Account

Banks and NBFIs : 5.50%

Customers

Below Tk.

1.00 Crore

Tk. 1.00 Crore &

above but

below Tk. 25.00

Crore

Tk. 25.00 Crore

& above but

below Tk. 50.00

Crore

Tk. 50.00 Crore

& above but

below Tk.

100.00 Crore

Tk. 100.00

Crore &

above

6.00% 6.25% 6.25% 6.50% 9.00%

Mother Account (IPO): Will be fixed upon approval from Head Office on case to

case basis.

Fees and Charges: As per existing schedule of charges which is separately displayed/shown

on the web site.

Monthly Savings Scheme (MSS) Account:

Your dreams may turn into reality through Southeast bank's Monthly Savings Scheme (MSS)

Features and Benefits:

Hassle Free Deposit

Loan of Maximum 80% against the lien of the MSS amount deposited can be availed.

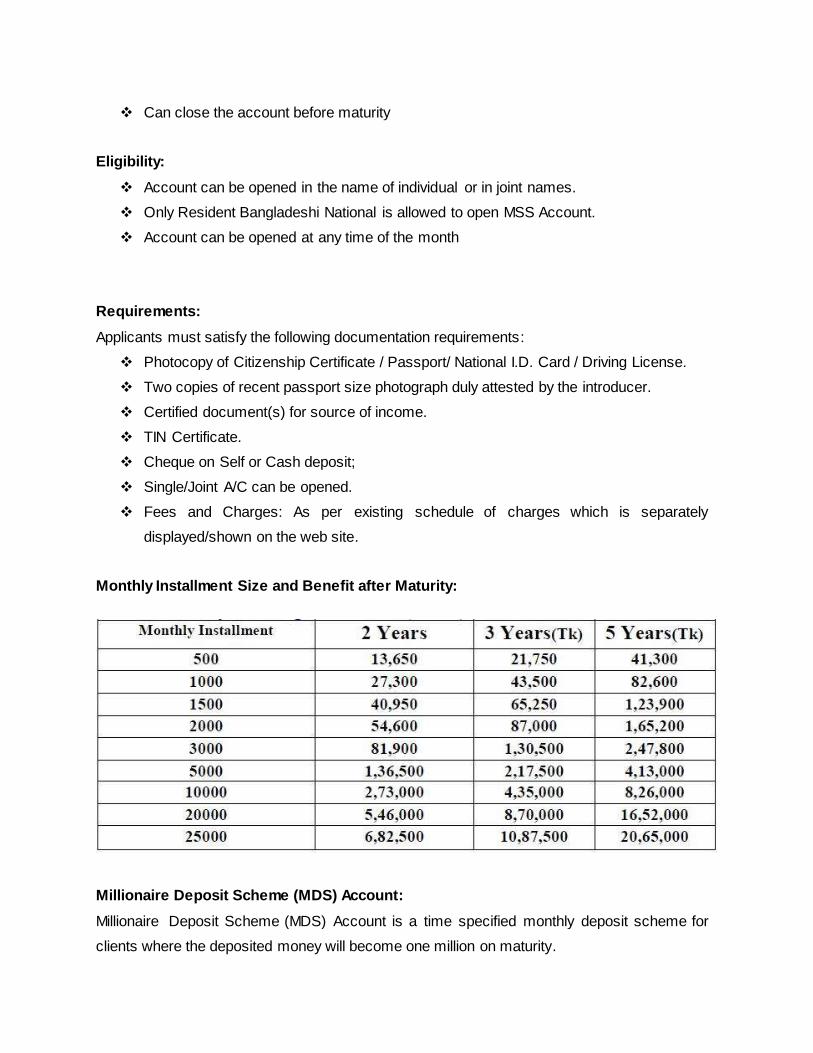

Can close the account before maturity

Eligibility:

Account can be opened in the name of individual or in joint names.

Only Resident Bangladeshi National is allowed to open MSS Account.

Account can be opened at any time of the month

Requirements:

Applicants must satisfy the following documentation requirements:

Photocopy of Citizenship Certificate / Passport/ National I.D. Card / Driving License.

Two copies of recent passport size photograph duly attested by the introducer.

Certified document(s) for source of income.

TIN Certificate.

Cheque on Self or Cash deposit;

Single/Joint A/C can be opened.

Fees and Charges: As per existing schedule of charges which is separately

displayed/shown on the web site.

Monthly Installment Size and Benefit after Maturity:

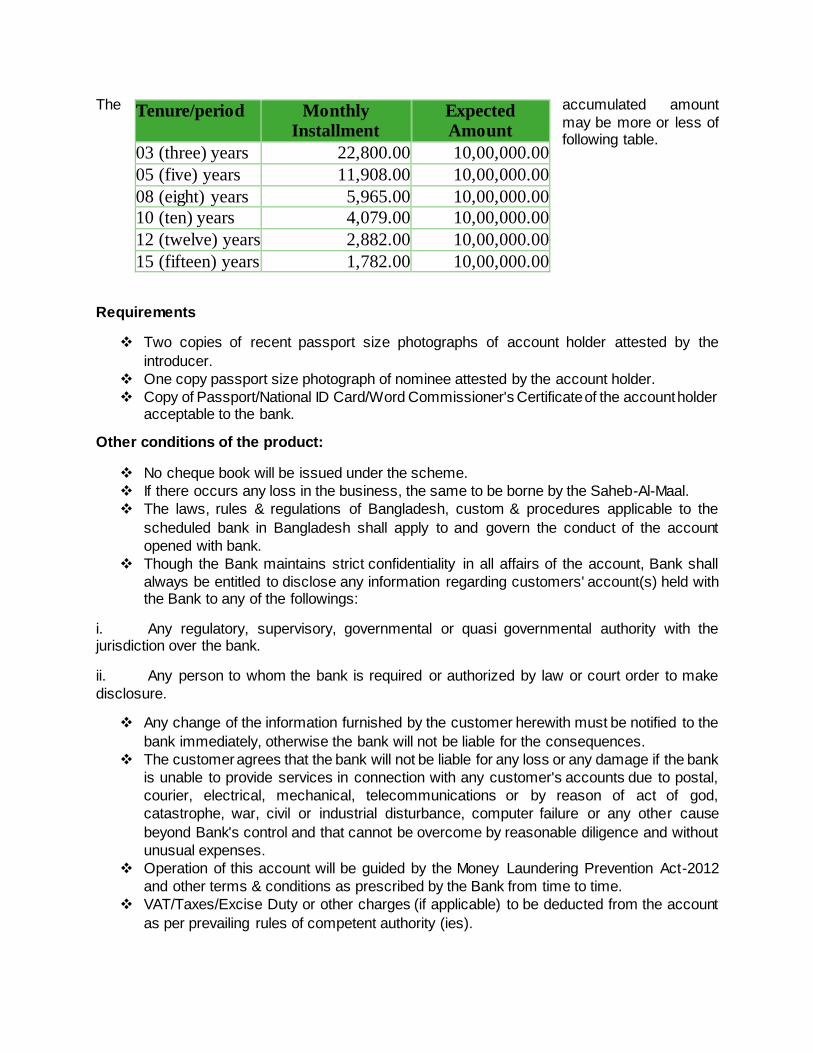

Millionaire Deposit Scheme (MDS) Account:

Millionaire Deposit Scheme (MDS) Account is a time specified monthly deposit scheme for

clients where the deposited money will become one million on maturity.

Features and Benefits:

Tenor: 4,5,6,7,8,9 and 10 years term;

Deposit on monthly installment basis;

Attractive rate of interest;

Account can be opened at any working day of the month;

Monthly installment can be deposited through a standing debit instruction from the

designated CD/SB Account;

Monthly installment can be deposited in advance;

An account can be transferred from one branch to another branch of the bank;

Credit facility for maximum of 2 years can be availed at any time during the period of the

scheme;

Allowed to open more than one MDS Account for different amount at any branch of the

Bank;

Eligibility:

MDS Account can be opened both for Individual and Corporate bodies.

Only Resident Bangladeshi National is allowed to open MDS Account.

Age bar for opening of Personal MDS Account: 18 years or above.

Single/Joint account can be opened.

Account can be opened in the name of minor. In that case his/her legal guardian will

operate the account.

Requirements:

Applicants must satisfy the following documentation requirements:

Photocopy of Citizenship Certificate / Passport/ National I.D. Card / Driving License.

Two copies of recent passport size photograph duly attested by the introducer.

Certified document(s) for source of income.

TIN Certificate.

Cheque on Self or Cash deposit;

Single/Joint A/C can be opened.

Fees and Charges: As per existing schedule of charges which is separately

displayed/shown in web site.

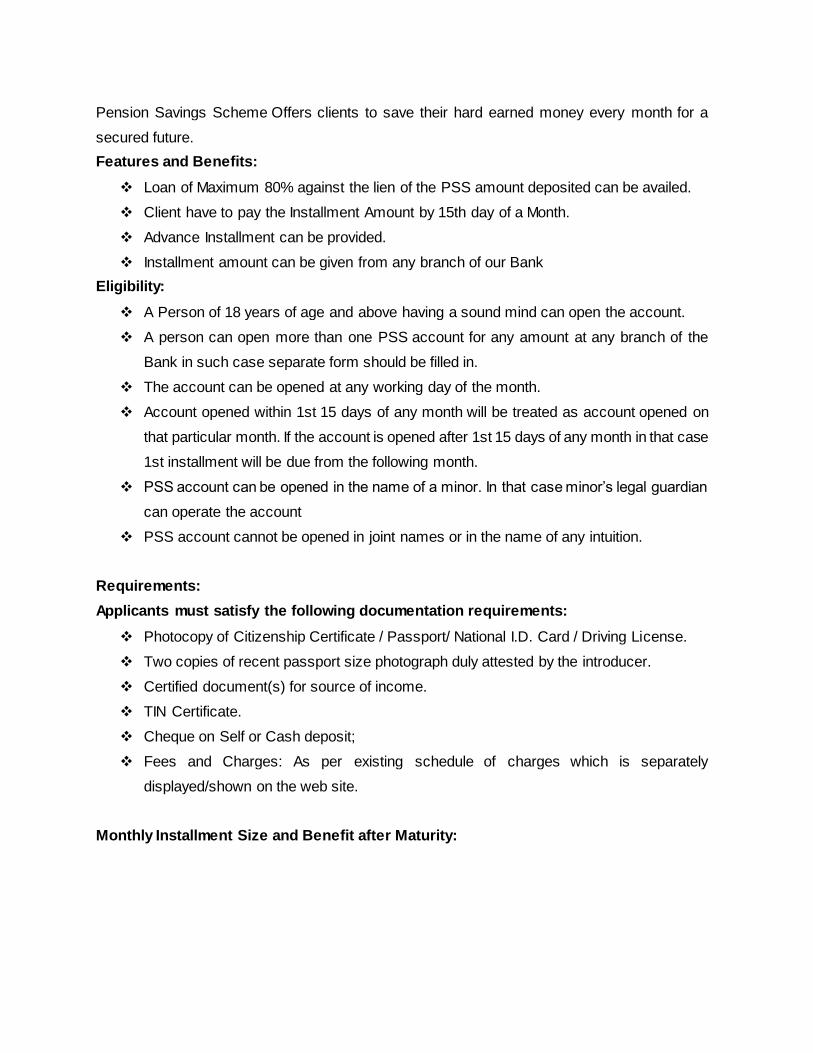

Pension Savings Scheme:

Pension Savings Scheme Offers clients to save their hard earned money every month for a

secured future.

Features and Benefits:

Loan of Maximum 80% against the lien of the PSS amount deposited can be availed.

Client have to pay the Installment Amount by 15th day of a Month.

Advance Installment can be provided.

Installment amount can be given from any branch of our Bank

Eligibility:

A Person of 18 years of age and above having a sound mind can open the account.

A person can open more than one PSS account for any amount at any branch of the

Bank in such case separate form should be filled in.

The account can be opened at any working day of the month.

Account opened within 1st 15 days of any month will be treated as account opened on

that particular month. If the account is opened after 1st 15 days of any month in that case

1st installment will be due from the following month.

PSS account can be opened in the name of a minor. In that case minor’s legal guardian

can operate the account

PSS account cannot be opened in joint names or in the name of any intuition.

Requirements:

Applicants must satisfy the following documentation requirements:

Photocopy of Citizenship Certificate / Passport/ National I.D. Card / Driving License.

Two copies of recent passport size photograph duly attested by the introducer.

Certified document(s) for source of income.

TIN Certificate.

Cheque on Self or Cash deposit;

Fees and Charges: As per existing schedule of charges which is separately

displayed/shown on the web site.

Monthly Installment Size and Benefit after Maturity:

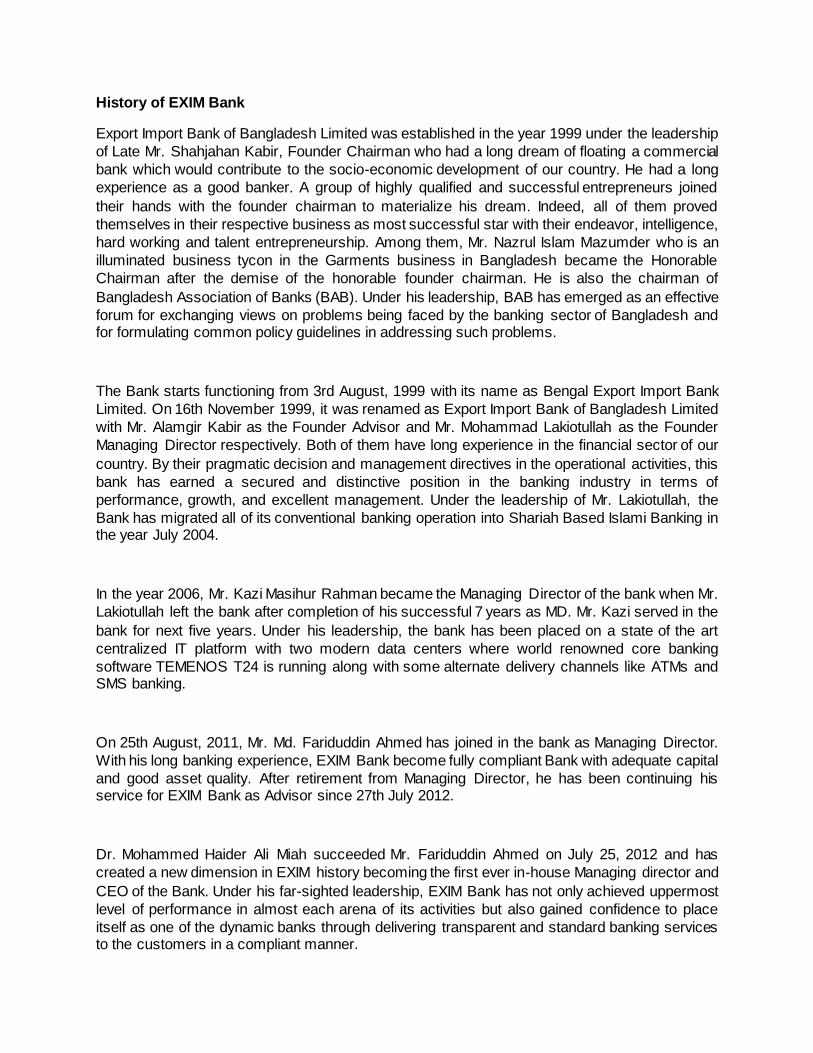

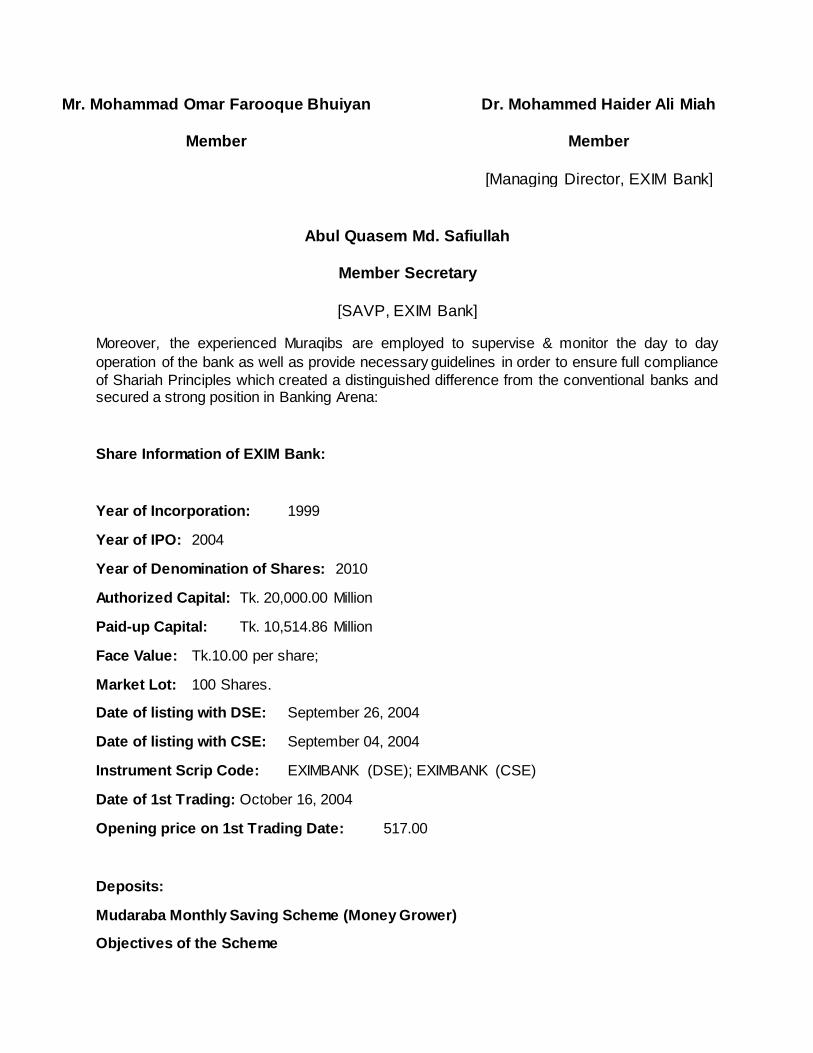

History of EXIM Bank

Export Import Bank of Bangladesh Limited was established in the year 1999 under the leadership

of Late Mr. Shahjahan Kabir, Founder Chairman who had a long dream of floating a commercial

bank which would contribute to the socio-economic development of our country. He had a long

experience as a good banker. A group of highly qualified and successful entrepreneurs joined

their hands with the founder chairman to materialize his dream. Indeed, all of them proved

themselves in their respective business as most successful star with their endeavor, intelligence,

hard working and talent entrepreneurship. Among them, Mr. Nazrul Islam Mazumder who is an

illuminated business tycon in the Garments business in Bangladesh became the Honorable

Chairman after the demise of the honorable founder chairman. He is also the chairman of

Bangladesh Association of Banks (BAB). Under his leadership, BAB has emerged as an effective

forum for exchanging views on problems being faced by the banking sector of Bangladesh and for formulating common policy guidelines in addressing such problems.

The Bank starts functioning from 3rd August, 1999 with its name as Bengal Export Import Bank

Limited. On 16th November 1999, it was renamed as Export Import Bank of Bangladesh Limited

with Mr. Alamgir Kabir as the Founder Advisor and Mr. Mohammad Lakiotullah as the Founder

Managing Director respectively. Both of them have long experience in the financial sector of our

country. By their pragmatic decision and management directives in the operational activities, this

bank has earned a secured and distinctive position in the banking industry in terms of

performance, growth, and excellent management. Under the leadership of Mr. Lakiotullah, the

Bank has migrated all of its conventional banking operation into Shariah Based Islami Banking in the year July 2004.

In the year 2006, Mr. Kazi Masihur Rahman became the Managing Director of the bank when Mr.

Lakiotullah left the bank after completion of his successful 7 years as MD. Mr. Kazi served in the

bank for next five years. Under his leadership, the bank has been placed on a state of the art

centralized IT platform with two modern data centers where world renowned core banking

software TEMENOS T24 is running along with some alternate delivery channels like ATMs and SMS banking.

On 25th August, 2011, Mr. Md. Fariduddin Ahmed has joined in the bank as Managing Director.

With his long banking experience, EXIM Bank become fully compliant Bank with adequate capital

and good asset quality. After retirement from Managing Director, he has been continuing his service for EXIM Bank as Advisor since 27th July 2012.

Dr. Mohammed Haider Ali Miah succeeded Mr. Fariduddin Ahmed on July 25, 2012 and has

created a new dimension in EXIM history becoming the first ever in-house Managing director and

CEO of the Bank. Under his far-sighted leadership, EXIM Bank has not only achieved uppermost

level of performance in almost each arena of its activities but also gained confidence to place

itself as one of the dynamic banks through delivering transparent and standard banking services to the customers in a compliant manner.

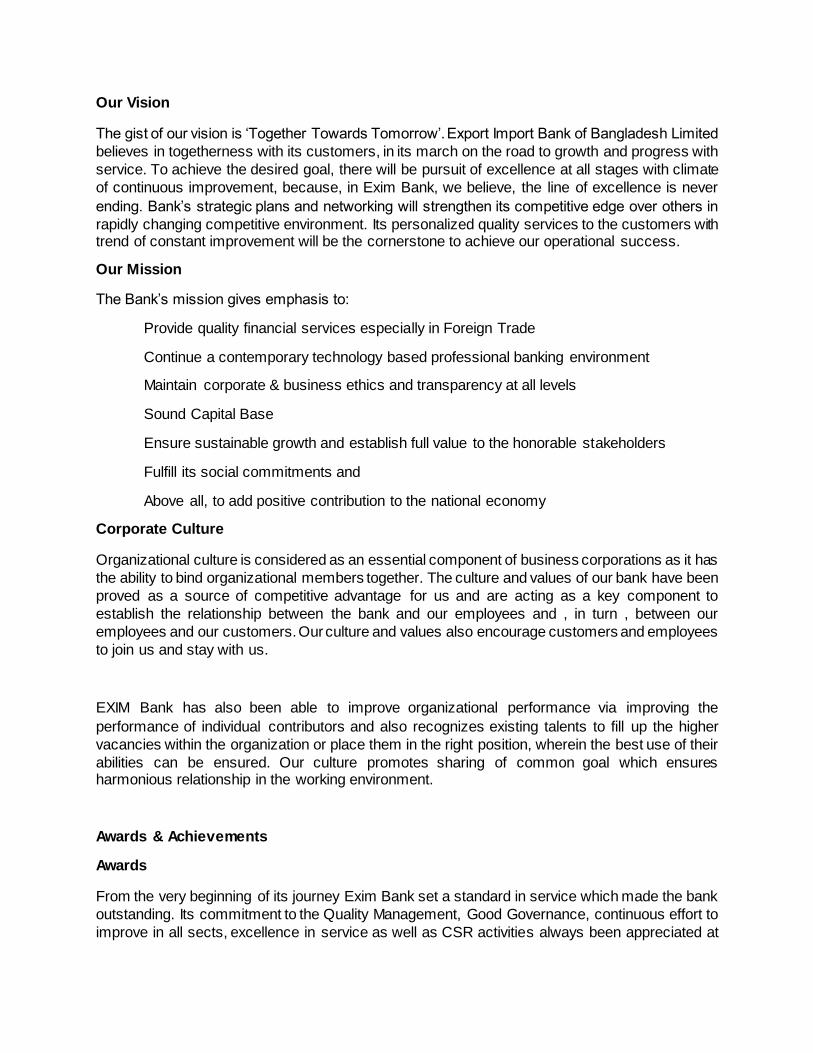

Our Vision

The gist of our vision is ‘Together Towards Tomorrow’. Export Import Bank of Bangladesh Limited

believes in togetherness with its customers, in its march on the road to growth and progress with

service. To achieve the desired goal, there will be pursuit of excellence at all stages with climate

of continuous improvement, because, in Exim Bank, we believe, the line of excellence is never

ending. Bank’s strategic plans and networking will strengthen its competitive edge over others in

rapidly changing competitive environment. Its personalized quality services to the customers with trend of constant improvement will be the cornerstone to achieve our operational success.

Our Mission

The Bank’s mission gives emphasis to:

Provide quality financial services especially in Foreign Trade

Continue a contemporary technology based professional banking environment

Maintain corporate & business ethics and transparency at all levels

Sound Capital Base

Ensure sustainable growth and establish full value to the honorable stakeholders

Fulfill its social commitments and

Above all, to add positive contribution to the national economy

Corporate Culture

Organizational culture is considered as an essential component of business corporations as it has

the ability to bind organizational members together. The culture and values of our bank have been

proved as a source of competitive advantage for us and are acting as a key component to

establish the relationship between the bank and our employees and , in turn , between our

employees and our customers. Our culture and values also encourage customers and employees

to join us and stay with us.

EXIM Bank has also been able to improve organizational performance via improving the

performance of individual contributors and also recognizes existing talents to fill up the higher

vacancies within the organization or place them in the right position, wherein the best use of their

abilities can be ensured. Our culture promotes sharing of common goal which ensures harmonious relationship in the working environment.

Awards & Achievements

Awards

From the very beginning of its journey Exim Bank set a standard in service which made the bank

outstanding. Its commitment to the Quality Management, Good Governance, continuous effort to

improve in all sects, excellence in service as well as CSR activities always been appreciated at

home and abroad. In consequence, Exim Bank achieved several national and international awards.

"International Diamond Prize for Excellence in Quality" award

"World Finance" award

Achievements

First private sector bank to open exchange house in UK

Implementation of the world renowned Core Banking Software (TEMENOS T24)

Conversion from Conventional Banking to Shariah Based Islami Banking.

Prime Operational Area of the Bank

As a full-fledged Islamic bank in Bangladesh, EXIM Bank extended all Islamic banking services

including wide range of saving and investment products, foreign exchange and ancillary services

with the support of sophisticated IT and professional management. The investment portfolio of

the bank comprises of diversified areas of business and industry sectors. The sectors include

textiles, edible oil, ready-made garments, chemicals, cement, telecom, steel, real estate and other

service industry including general trade finance. The bank has given utmost importance to acquire

quality assets and is committed to retain good customers through customer relationship

management and financial counseling. At the same time efforts have been made to explore/induct

new clients having good potentiality to diversify and create a well-established structured investment portfolio and to minimize overall portfolio risk.

Investment: Bank's investment port-folio are segmented under the following heads:

Retail/Consumers investment.

Micro enterprise investment.

Small and Medium Enterprise investment.

Large and Corporate investment.

Syndicate investment.

Modes of investments:

Murabaha (MTR, MPI, MIB).

Bai Muazzal.

Izara Bil Baia.

Wazirat Bil Wakala .

Bai-Salam.

Quard.

Musharaka Documentary Bills (MDB)/LDBP.

Bai-As-Sarf/FDBP.

EXIM Bank is very much responsive and interested to involve themselves both directly and

indirectly with the development process of the banking industry and national economy. As we

believe the development of small and medium-size enterprises plays a pivotal role in the growth

and prosperity of a nation. Although large-scale corporations, particularly industrial concerns

contribute sizably/ largely in Gross Domestic Products (GDP) and other economic variables of

prosperity but the significance of SMEs is widely recognized around the globe. SMEs make a

substantial contribution towards GDP, revenue collection in the form of taxes, fostering

entrepreneurship culture, employment opportunities, income generation, skills development of

human resources, poverty alleviation, and improving the standard of living and quality of life.

Above all the prime economic benefits of SMEs development include encouraging perfect

competition and fair distribution of wealth. If there are only large-scale corporations either, then

there will be a monopoly in an industry, with a single suppliers, or oligopoly with only few suppliers,

or monopolistic competition with only some suppliers, then the major portion of national income

and wealth will move within the hands of big capitalists. SME sector, however, begets fair competition and equitable distribution of wealth.

SME Defined:

Generally, SME means small and medium size enterprises, the definition published by Ministry of Industries and endorsed by Bangladesh Bank are as follows:

Micro Industry/Enterprise:

Micro Industry/ Enterprise Total Fixed Assets (Excluding land & factory building)

Total no. of Employees

Service concern Up to Tk.5.00 lac Up to 10 persons

Trading concern Up to Tk.5.00 lac Up to 10 persons

Manufacturing concern Up to Tk.50.00 lac Up to 24 persons

***If a concern goes to Micro industry/enterprise based on any one above standard (asset or

employee) but it goes to Small industry/enterprise based on other above standard (asset or employee) then it may be considered as ‘Small Industry/Enterprise’

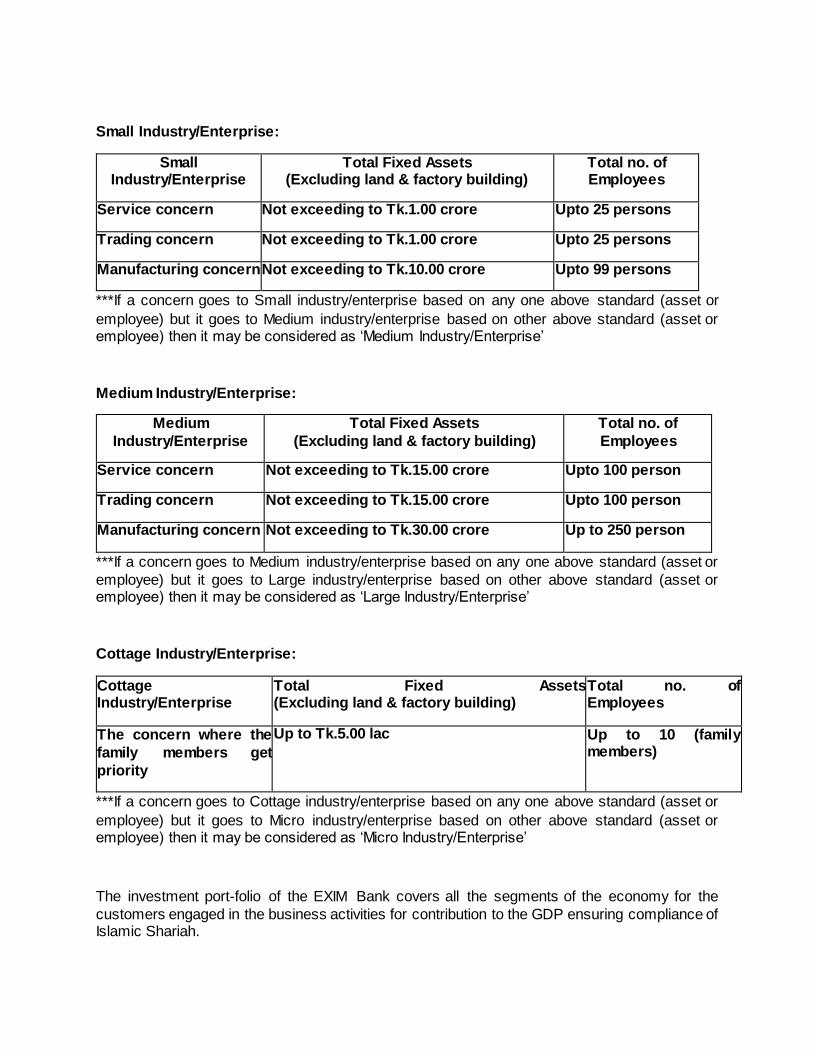

Small Industry/Enterprise:

Small Industry/Enterprise

Total Fixed Assets (Excluding land & factory building)

Total no. of Employees

Service concern Not exceeding to Tk.1.00 crore Upto 25 persons

Trading concern Not exceeding to Tk.1.00 crore Upto 25 persons

Manufacturing concern Not exceeding to Tk.10.00 crore Upto 99 persons

***If a concern goes to Small industry/enterprise based on any one above standard (asset or

employee) but it goes to Medium industry/enterprise based on other above standard (asset or employee) then it may be considered as ‘Medium Industry/Enterprise’

Medium Industry/Enterprise:

Medium

Industry/Enterprise

Total Fixed Assets

(Excluding land & factory building)

Total no. of

Employees

Service concern Not exceeding to Tk.15.00 crore Upto 100 person

Trading concern Not exceeding to Tk.15.00 crore Upto 100 person

Manufacturing concern Not exceeding to Tk.30.00 crore Up to 250 person

***If a concern goes to Medium industry/enterprise based on any one above standard (asset or

employee) but it goes to Large industry/enterprise based on other above standard (asset or employee) then it may be considered as ‘Large Industry/Enterprise’

Cottage Industry/Enterprise:

Cottage Industry/Enterprise

Total Fixed Assets (Excluding land & factory building)

Total no. of Employees

The concern where the

family members get

priority

Up to Tk.5.00 lac Up to 10 (family members)

***If a concern goes to Cottage industry/enterprise based on any one above standard (asset or

employee) but it goes to Micro industry/enterprise based on other above standard (asset or employee) then it may be considered as ‘Micro Industry/Enterprise’

The investment port-folio of the EXIM Bank covers all the segments of the economy for the

customers engaged in the business activities for contribution to the GDP ensuring compliance of Islamic Shariah.

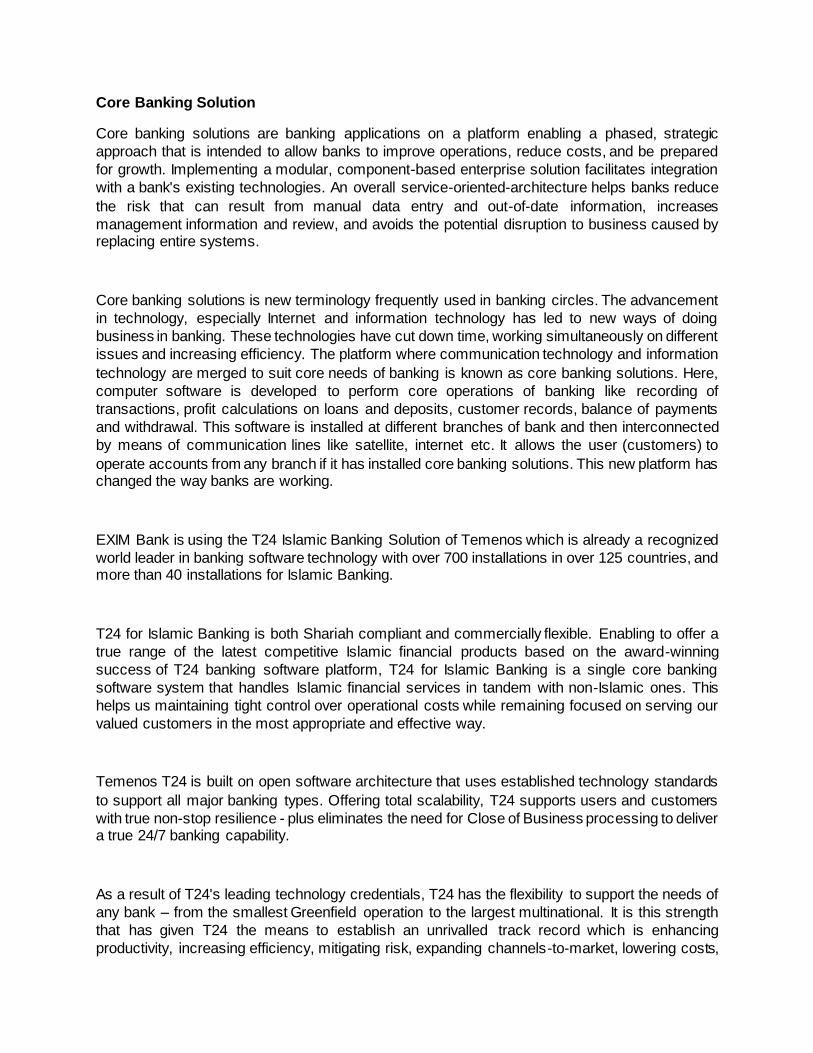

Core Banking Solution

Core banking solutions are banking applications on a platform enabling a phased, strategic

approach that is intended to allow banks to improve operations, reduce costs, and be prepared

for growth. Implementing a modular, component-based enterprise solution facilitates integration

with a bank's existing technologies. An overall service-oriented-architecture helps banks reduce

the risk that can result from manual data entry and out-of-date information, increases

management information and review, and avoids the potential disruption to business caused by replacing entire systems.

Core banking solutions is new terminology frequently used in banking circles. The advancement

in technology, especially Internet and information technology has led to new ways of doing

business in banking. These technologies have cut down time, working simultaneously on different

issues and increasing efficiency. The platform where communication technology and information

technology are merged to suit core needs of banking is known as core banking solutions. Here,

computer software is developed to perform core operations of banking like recording of

transactions, profit calculations on loans and deposits, customer records, balance of payments

and withdrawal. This software is installed at different branches of bank and then interconnected

by means of communication lines like satellite, internet etc. It allows the user (customers) to

operate accounts from any branch if it has installed core banking solutions. This new platform has changed the way banks are working.

EXIM Bank is using the T24 Islamic Banking Solution of Temenos which is already a recognized

world leader in banking software technology with over 700 installations in over 125 countries, and more than 40 installations for Islamic Banking.

T24 for Islamic Banking is both Shariah compliant and commercially flexible. Enabling to offer a

true range of the latest competitive Islamic financial products based on the award-winning

success of T24 banking software platform, T24 for Islamic Banking is a single core banking

software system that handles Islamic financial services in tandem with non-Islamic ones. This

helps us maintaining tight control over operational costs while remaining focused on serving our

valued customers in the most appropriate and effective way.

Temenos T24 is built on open software architecture that uses established technology standards

to support all major banking types. Offering total scalability, T24 supports users and customers

with true non-stop resilience - plus eliminates the need for Close of Business processing to deliver a true 24/7 banking capability.

As a result of T24's leading technology credentials, T24 has the flexibility to support the needs of

any bank – from the smallest Greenfield operation to the largest multinational. It is this strength

that has given T24 the means to establish an unrivalled track record which is enhancing

Carrying high volumes based on multiple, secure and scalable servers, T24 does not limit the

number of transactions, users or customers. Having more than 55 offices worldwide, Temenos is

providing over 1,500 customer deployments in more than 125 countries across the world. This ensures T24 is able to support any size of financial institution and all levels of traffic.

Board of Directors

CHAIRMAN

Mr. Md. Nazrul Islam Mazumder

DIRECTORS

I. Mr. Md. Nazrul Islam Swapan

II. Mr. Mohammad Abdullah

III. Mrs. Nasreen Islam

IV. Mr. Mohammed Shahidullah

V. Al-haj Md. Nurul Amin

VI. Mr. Mohammad Omar Farooque Bhuiyan

VII. Mr. Anjan Kumar Saha

VIII. Mr. Md. Habib Ullah Dawn

IX. Major Khandaker Nurul Afser (Retd.)

X. Lt. Col. (Retd) Serajul Islam BP (BAR)

XI. Mr. Ranjan Chowdhury

XII. Khandakar Mohammed Saiful Alam XIII. Mr. Muhammad Sekandar Khan

MANAGING DIRECTOR & CEO

Dr. Mohammed Haider Ali Miah

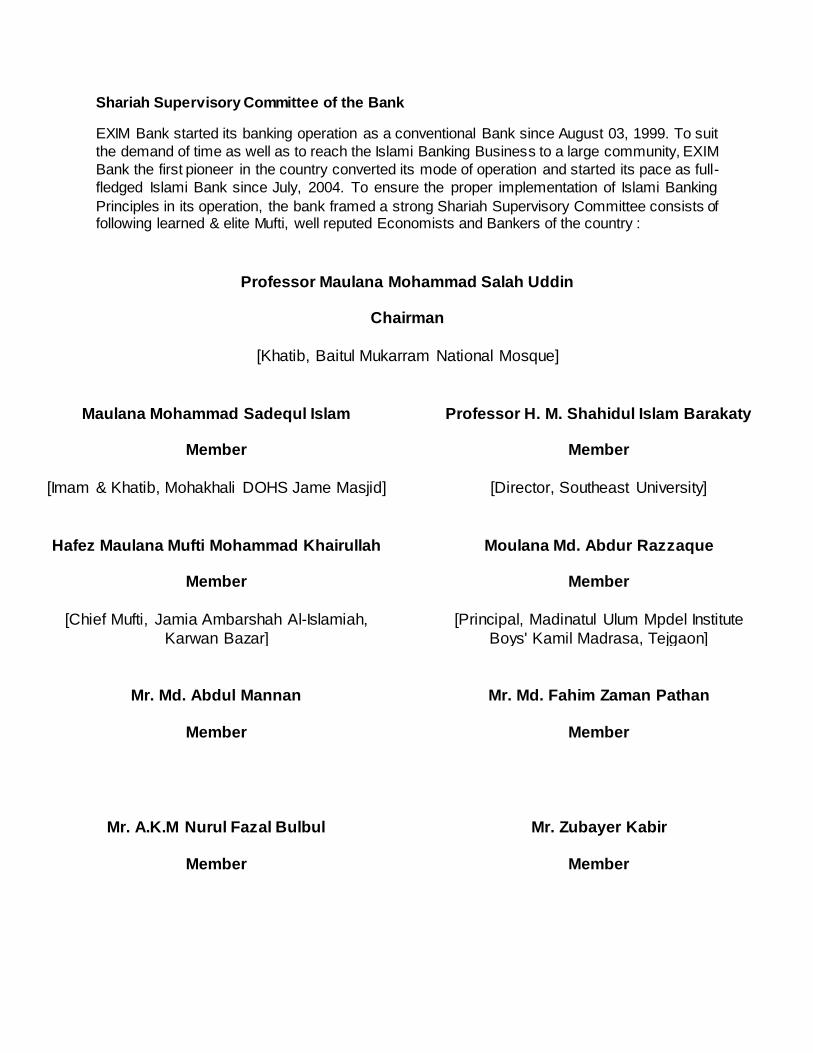

Shariah Supervisory Committee of the Bank

EXIM Bank started its banking operation as a conventional Bank since August 03, 1999. To suit

the demand of time as well as to reach the Islami Banking Business to a large community, EXIM

Bank the first pioneer in the country converted its mode of operation and started its pace as full-

fledged Islami Bank since July, 2004. To ensure the proper implementation of Islami Banking

Principles in its operation, the bank framed a strong Shariah Supervisory Committee consists of following learned & elite Mufti, well reputed Economists and Bankers of the country :

Professor Maulana Mohammad Salah Uddin

Chairman

[Khatib, Baitul Mukarram National Mosque]

Maulana Mohammad Sadequl Islam

Member

[Imam & Khatib, Mohakhali DOHS Jame Masjid]

Professor H. M. Shahidul Islam Barakaty

Member

[Director, Southeast University]

Hafez Maulana Mufti Mohammad Khairullah

Member

[Chief Mufti, Jamia Ambarshah Al-Islamiah,

Karwan Bazar]

Moulana Md. Abdur Razzaque

Member

[Principal, Madinatul Ulum Mpdel Institute

Boys' Kamil Madrasa, Tejgaon]

Mr. Md. Abdul Mannan

Member

Mr. Md. Fahim Zaman Pathan

Member

Mr. A.K.M Nurul Fazal Bulbul

Member

Mr. Zubayer Kabir

Member

Mr. Mohammad Omar Farooque Bhuiyan

Member

Dr. Mohammed Haider Ali Miah

Member

[Managing Director, EXIM Bank]

Abul Quasem Md. Safiullah

Member Secretary

[SAVP, EXIM Bank]

Moreover, the experienced Muraqibs are employed to supervise & monitor the day to day

operation of the bank as well as provide necessary guidelines in order to ensure full compliance

of Shariah Principles which created a distinguished difference from the conventional banks and secured a strong position in Banking Arena:

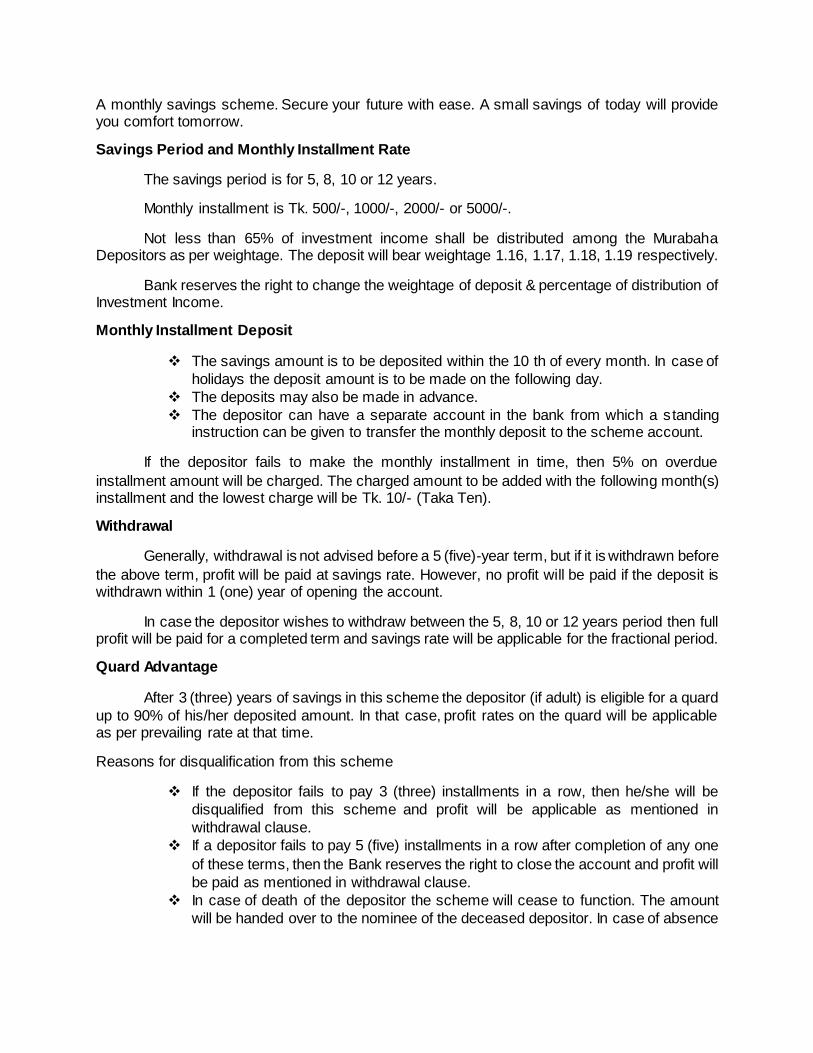

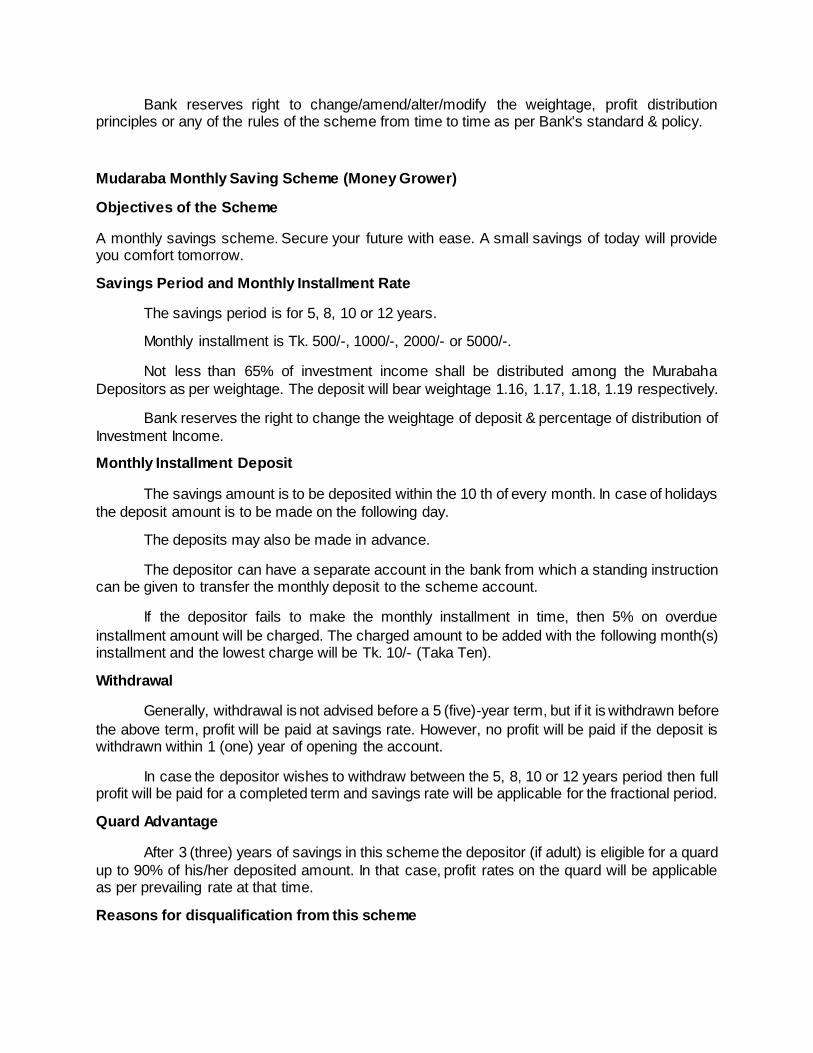

A monthly savings scheme. Secure your future with ease. A small savings of today will provide you comfort tomorrow.

Savings Period and Monthly Installment Rate

The savings period is for 5, 8, 10 or 12 years.

Monthly installment is Tk. 500/-, 1000/-, 2000/- or 5000/-.

Not less than 65% of investment income shall be distributed among the Murabaha Depositors as per weightage. The deposit will bear weightage 1.16, 1.17, 1.18, 1.19 respectively.

Bank reserves the right to change the weightage of deposit & percentage of distribution of Investment Income.

Monthly Installment Deposit

The savings amount is to be deposited within the 10 th of every month. In case of

holidays the deposit amount is to be made on the following day.

The deposits may also be made in advance.

The depositor can have a separate account in the bank from which a standing instruction can be given to transfer the monthly deposit to the scheme account.

If the depositor fails to make the monthly installment in time, then 5% on overdue

installment amount will be charged. The charged amount to be added with the following month(s) installment and the lowest charge will be Tk. 10/- (Taka Ten).

Withdrawal

Generally, withdrawal is not advised before a 5 (five)-year term, but if it is withdrawn before

the above term, profit will be paid at savings rate. However, no profit will be paid if the deposit is withdrawn within 1 (one) year of opening the account.

In case the depositor wishes to withdraw between the 5, 8, 10 or 12 years period then full profit will be paid for a completed term and savings rate will be applicable for the fractional period.

Quard Advantage

After 3 (three) years of savings in this scheme the depositor (if adult) is eligible for a quard

up to 90% of his/her deposited amount. In that case, profit rates on the quard will be applicable as per prevailing rate at that time.

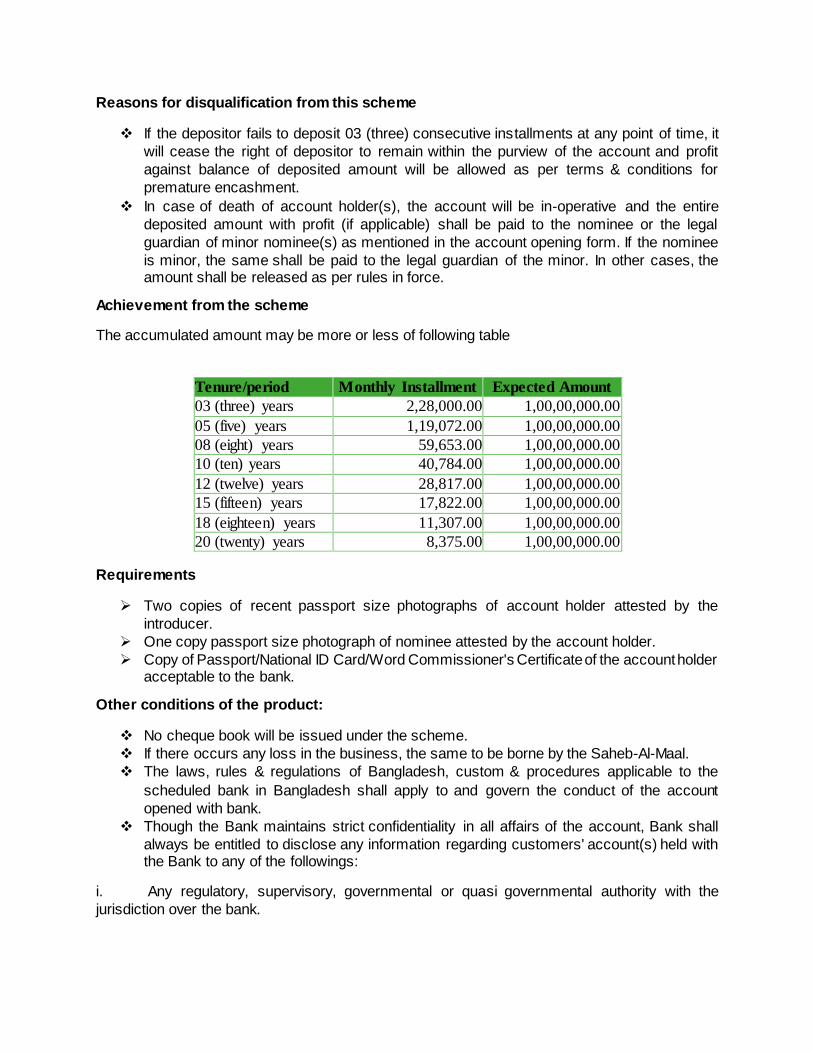

Reasons for disqualification from this scheme

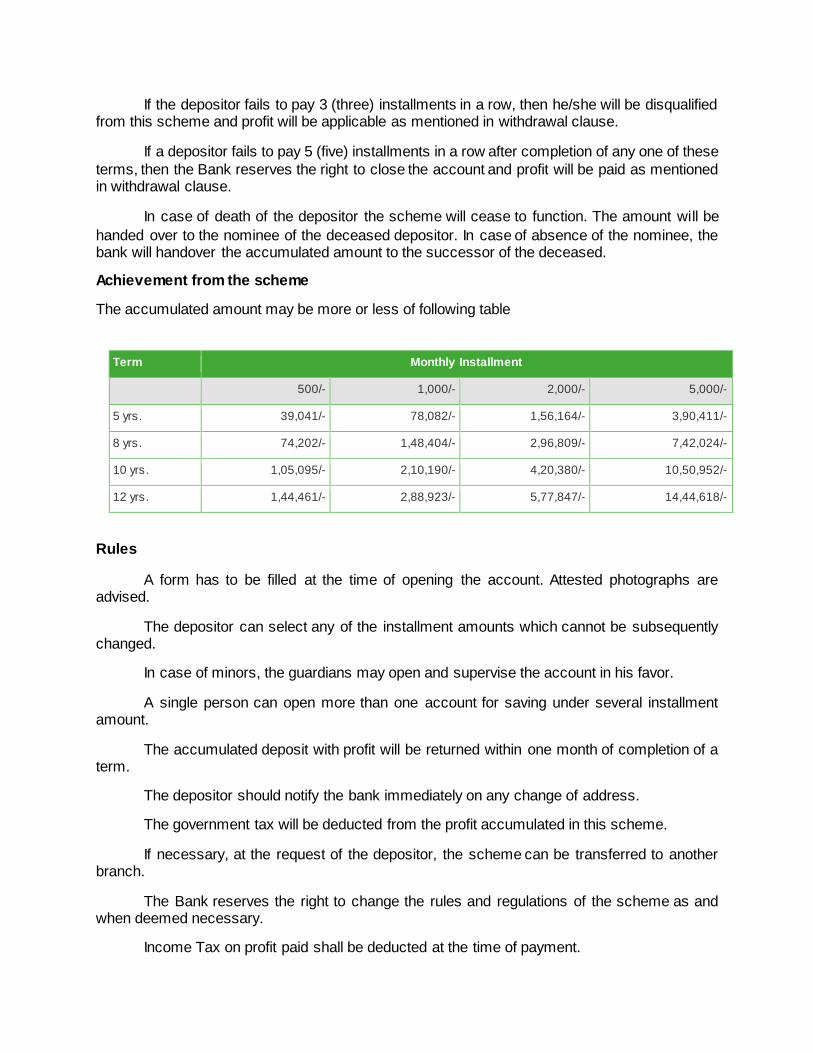

If the depositor fails to pay 3 (three) installments in a row, then he/she will be

disqualified from this scheme and profit will be applicable as mentioned in

withdrawal clause.

If a depositor fails to pay 5 (five) installments in a row after completion of any one

of these terms, then the Bank reserves the right to close the account and profit will

be paid as mentioned in withdrawal clause.

In case of death of the depositor the scheme will cease to function. The amount

will be handed over to the nominee of the deceased depositor. In case of absence

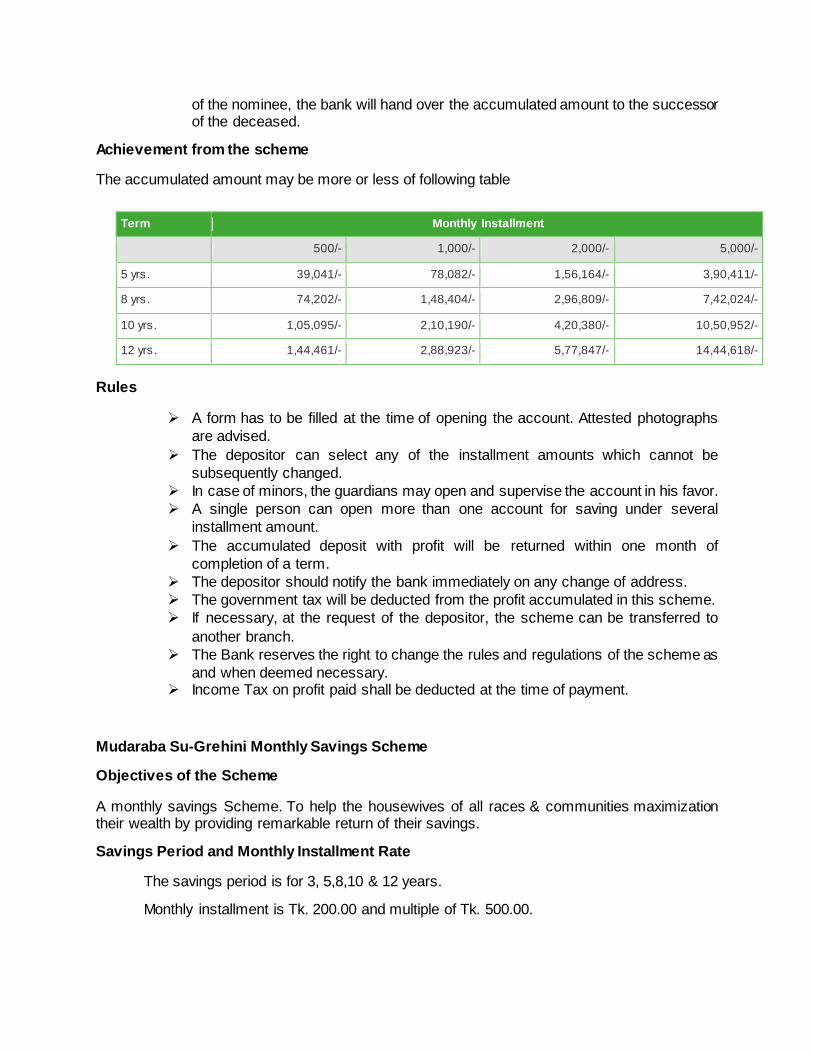

of the nominee, the bank will hand over the accumulated amount to the successor of the deceased.

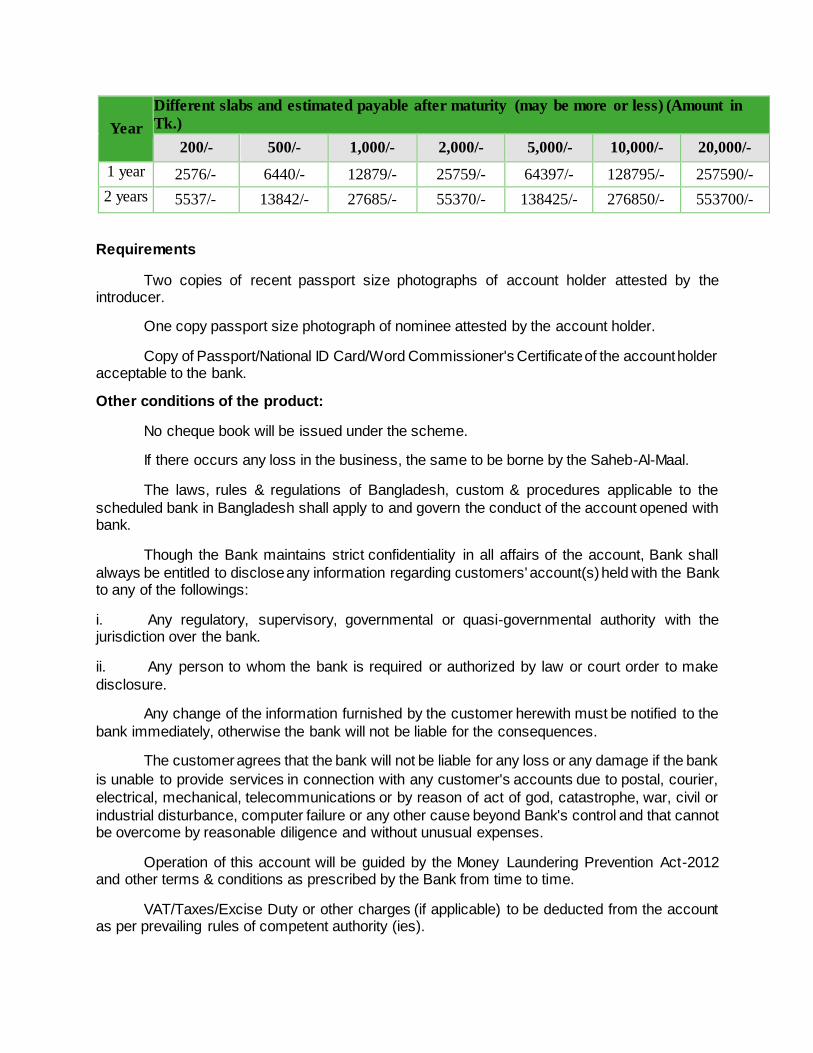

Achievement from the scheme

The accumulated amount may be more or less of following table

A form has to be filled at the time of opening the account. Attested photographs

are advised.

The depositor can select any of the installment amounts which cannot be

subsequently changed.

In case of minors, the guardians may open and supervise the account in his favor.

A single person can open more than one account for saving under several

installment amount.

The accumulated deposit with profit will be returned within one month of

completion of a term.

The depositor should notify the bank immediately on any change of address.

The government tax will be deducted from the profit accumulated in this scheme.

If necessary, at the request of the depositor, the scheme can be transferred to

another branch.

The Bank reserves the right to change the rules and regulations of the scheme as

and when deemed necessary. Income Tax on profit paid shall be deducted at the time of payment.

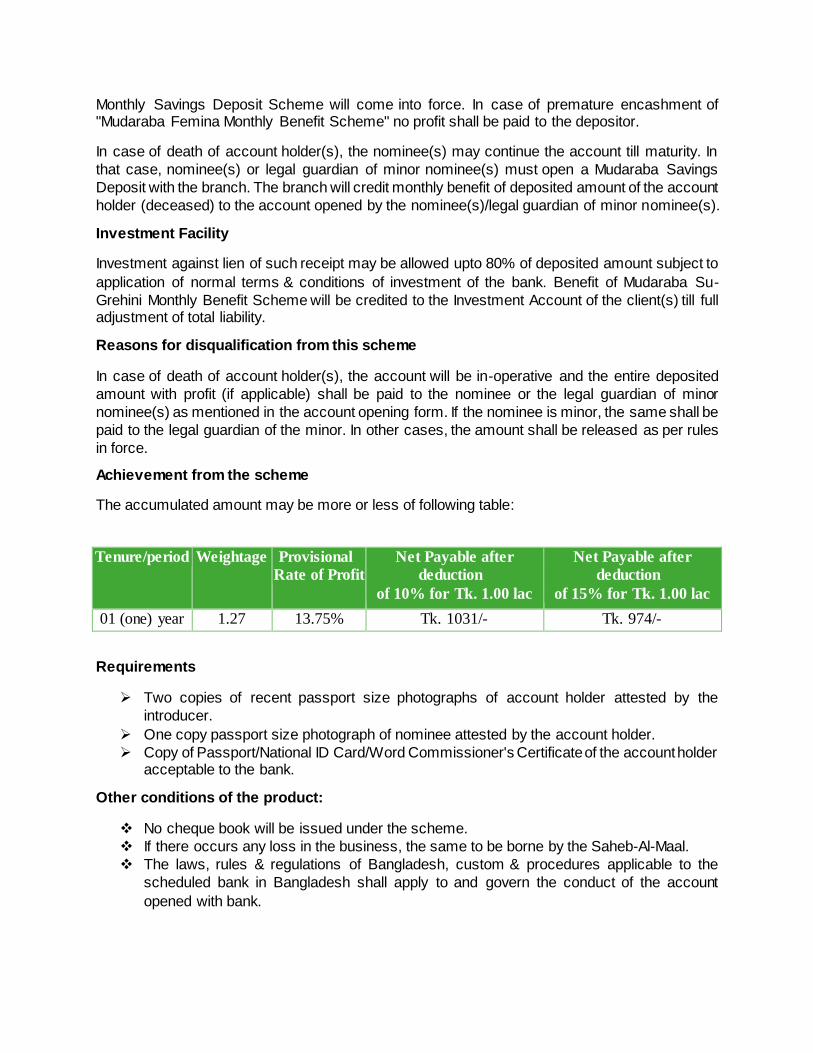

Mudaraba Su-Grehini Monthly Savings Scheme

Objectives of the Scheme

A monthly savings Scheme. To help the housewives of all races & communities maximization their wealth by providing remarkable return of their savings.

Savings Period and Monthly Installment Rate

The savings period is for 3, 5,8,10 & 12 years.

Monthly installment is Tk. 200.00 and multiple of Tk. 500.00.

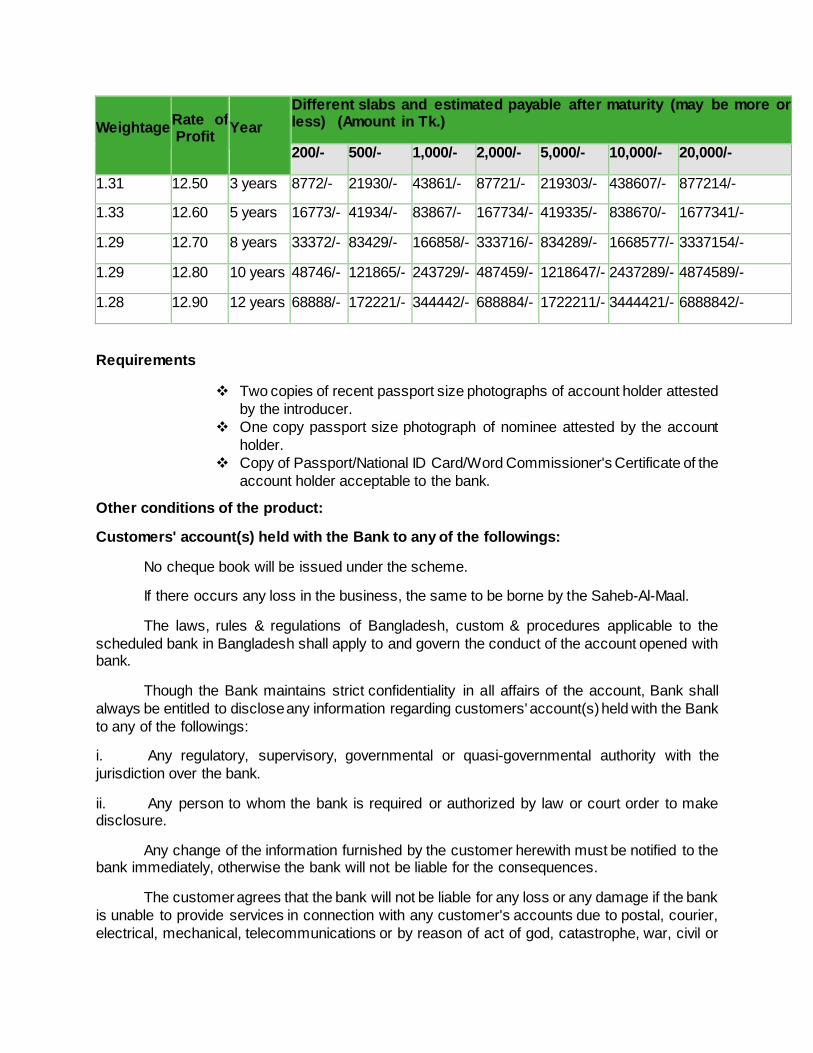

At least 65% of investment income shall be distributed among the Mudaraba Depositors as per weightage. The Deposit will bear weightage 1.31, 1.33, 1.29, 1.29 and 1.28 respectively.

Bank reserves the right to change the weightage of deposit and percentage of distribution of Investment Income.

Monthly Installment Deposit

The savings amount is to be deposited within the 10th of every month. In case of holidays the deposit amount is to be made on the following day.

The deposits may also be made in advance.

The depositor can have a separate account in the bank from which a standing instruction can be given to transfer the monthly deposit to the scheme account.

If the depositor fails to make the monthly installment in time, then 5% on overdue

installment amount will be charged. The charged amount to be added with the following month(s) installment and the lowest charge will be Tk. 10/- (Taka Ten).

Withdrawal

Generally, withdrawal is not advised before a 3(three)-year term, but if it is withdrawn

before the above term, profit will be paid at Savings rate. However, no profit will be paid if the

deposit is withdrawn within 1 (one) year of opening the account.

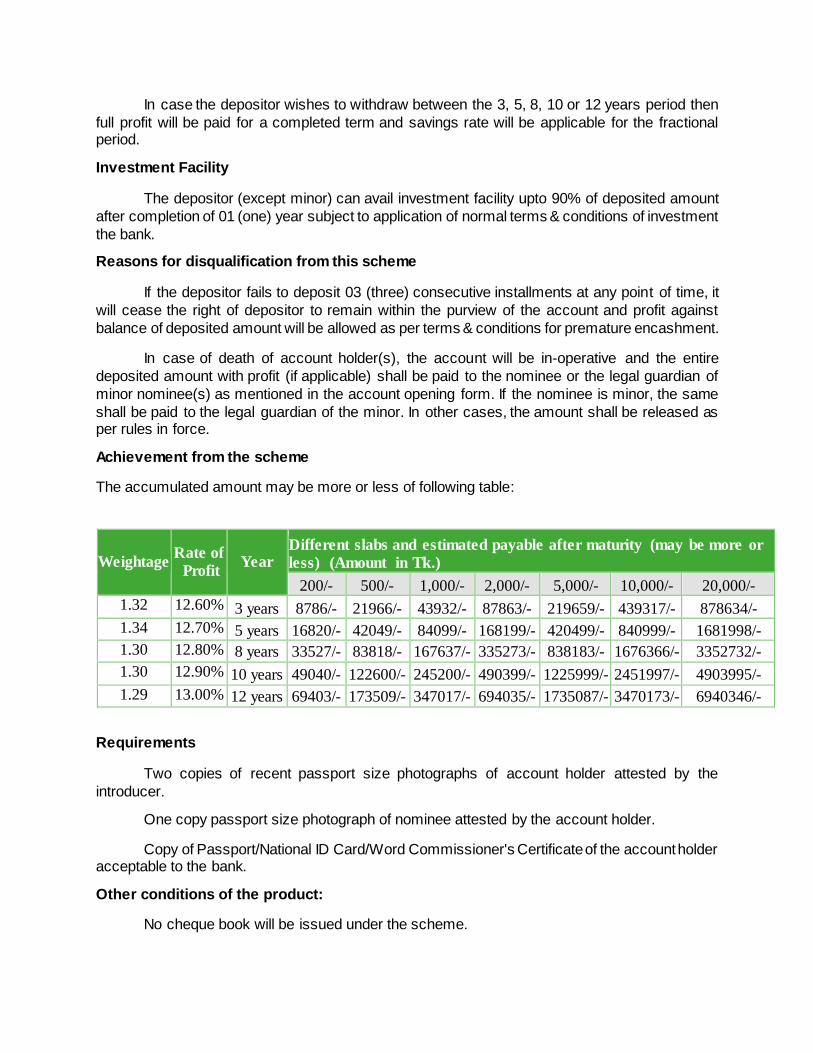

In case the depositor wishes to withdraw between the 3, 5, 8, 10 or 12 years period then

full profit will be paid for a completed term and savings rate will be applicable for the fractional period.

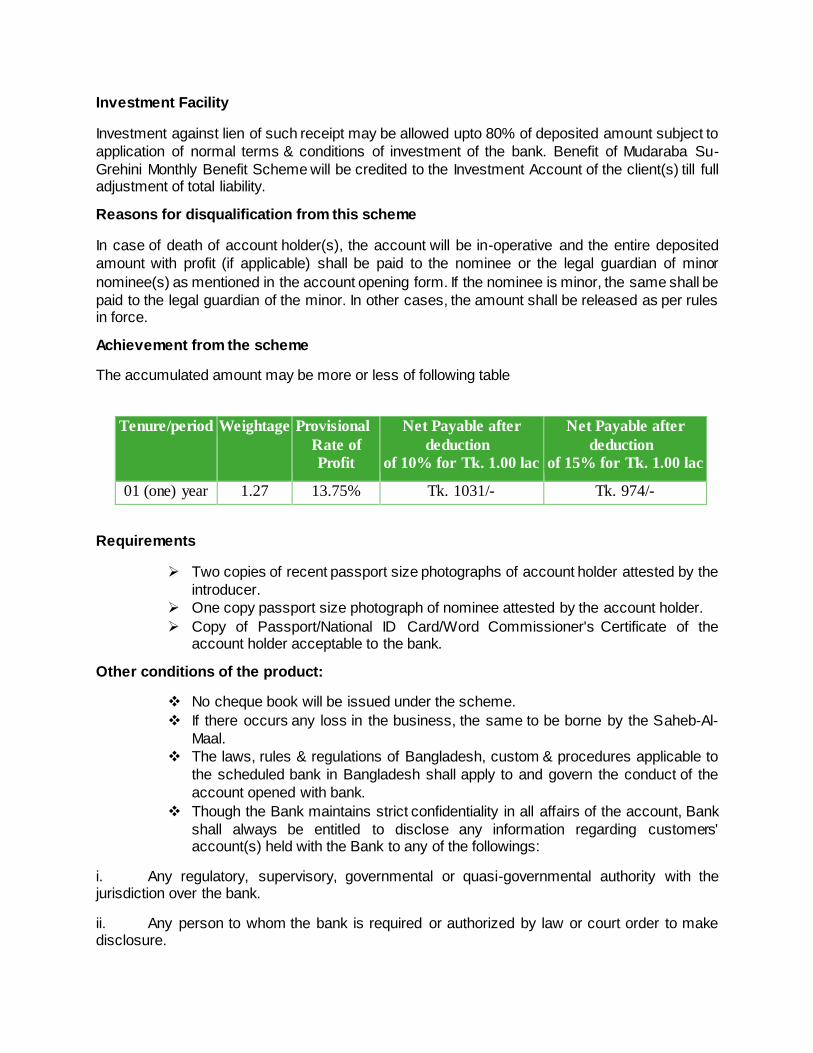

Investment Facility

The depositor (except minor) can avail investment facility upto 90% of deposited amount

after completion of 01 (one) year subject to application of normal terms & conditions of investment the bank.

Reasons for disqualification from this scheme

If the depositor fails to deposit 03 (three) consecutive installments at any point of time, it

will cease the right of depositor to remain within the purview of the account and profit against balance of deposited amount will be allowed as per terms & conditions for premature encashment.

In case of death of account holder(s), the account will be in-operative and the entire

deposited amount with profit (if applicable) shall be paid to the nominee or the legal guardian of

minor nominee(s) as mentioned in the account opening form. If the nominee is minor, the same

shall be paid to the legal guardian of the minor. In other cases, the amount shall be released as per rules in force.

Achievement from the scheme

The accumulated amount may be more or less of following table

Weightage Rate of Profit

Year

Different slabs and estimated payable after maturity (may be more or less) (Amount in Tk.)

Two copies of recent passport size photographs of account holder attested

by the introducer.

One copy passport size photograph of nominee attested by the account

holder.

Copy of Passport/National ID Card/Word Commissioner's Certificate of the

account holder acceptable to the bank.

Other conditions of the product:

Customers' account(s) held with the Bank to any of the followings:

No cheque book will be issued under the scheme.

If there occurs any loss in the business, the same to be borne by the Saheb-Al-Maal.

The laws, rules & regulations of Bangladesh, custom & procedures applicable to the

scheduled bank in Bangladesh shall apply to and govern the conduct of the account opened with bank.

Though the Bank maintains strict confidentiality in all affairs of the account, Bank shall

always be entitled to disclose any information regarding customers' account(s) held with the Bank

to any of the followings:

i. Any regulatory, supervisory, governmental or quasi-governmental authority with the

jurisdiction over the bank.

ii. Any person to whom the bank is required or authorized by law or court order to make disclosure.

Any change of the information furnished by the customer herewith must be notified to the bank immediately, otherwise the bank will not be liable for the consequences.

The customer agrees that the bank will not be liable for any loss or any damage if the bank

is unable to provide services in connection with any customer's accounts due to postal, courier,

electrical, mechanical, telecommunications or by reason of act of god, catastrophe, war, civil or

industrial disturbance, computer failure or any other cause beyond Bank's control and that cannot be overcome by reasonable diligence and without unusual expenses.

Operation of this account will be guided by the Money Laundering Prevention Act-2012 and other terms & conditions as prescribed by the Bank from time to time.

VAT/Taxes/Excise Duty or other charges (if applicable) to be deducted from the account as per prevailing rules of competent authority (ies).

Bank reserves right to change/amend/alter/modify the weightage, profit distribution principles or any of the rules of the scheme from time to time as per Bank's standard & policy.

Mudaraba Femina Monthly Savings Scheme

Objectives of the Scheme

A monthly savings Scheme. To help the female employees of all races & communities maximization their wealth by providing remarkable return of their savings.

Savings Period and Monthly Installment Rate

The savings period is for 3, 5,8,10 & 12 years.

Monthly installment is Tk. 200.00 and multiple of Tk. 500.00.

At least 65% of investment income shall be distributed among the Mudaraba Depositors as per weightage. The Deposit will bear weightage 1.32, 1.34, 1.30, 1.30 and 1.29 respectively.

Bank reserves the right to change the weightage of deposit and percentage of distribution of Investment Income.

Monthly Installment Deposit

The savings amount is to be deposited within the 10th of every month. In case of holidays the deposit amount is to be made on the following day.

The deposits may also be made in advance.

The depositor can have a separate account in the bank from which a standing instruction

can be given to transfer the monthly deposit to the scheme account.

If the depositor fails to make the monthly installment in time, then 5% on overdue

installment amount will be charged. The charged amount to be added with the following month(s) installment and the lowest charge will be Tk. 10/- (Taka Ten).

Withdrawal