51

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning GLOBAL GLOBAL TALENT TALENT RALLY RALLY Sally Khallash, [email protected] International workforce migration

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | barbara-booth |

| View: | 215 times |

| Download: | 0 times |

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

GLOBAL GLOBAL TALENTTALENT RALLYRALLY

Sally Khallash, [email protected]

International workforce migration

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

AgendaAgenda

• International Workforce Migration– Facts on Migration– Driving Forces– Origin and Destination countries– Migration Profiles & Life cycles– Pull factors– Strategies for Recruitment: Attract and Retain

• Workshop

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

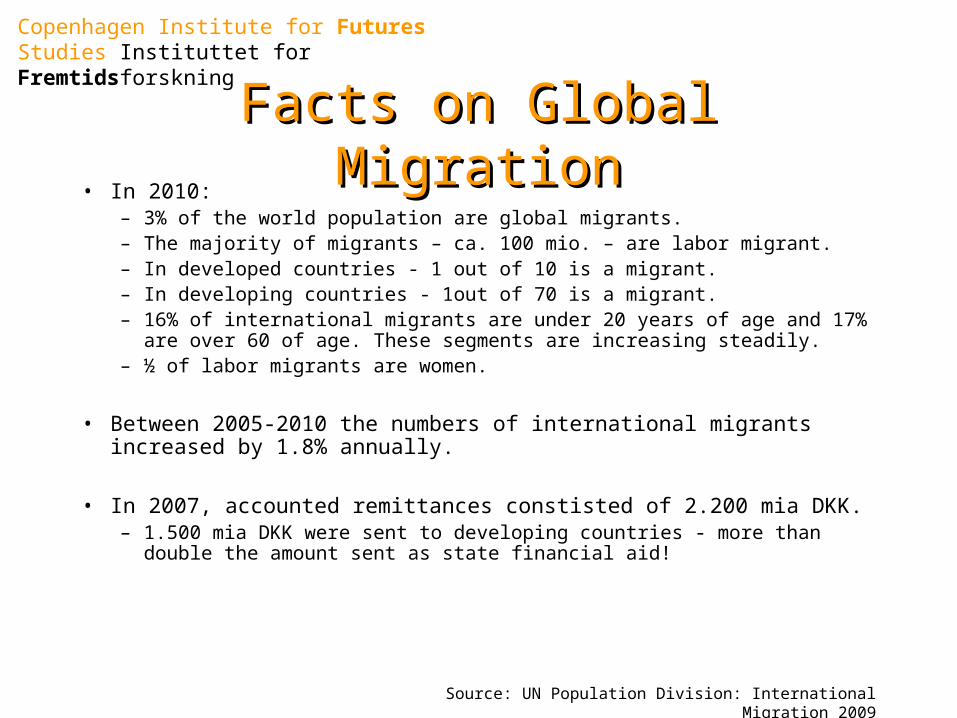

Facts on Global MigrationFacts on Global Migration• In 2010:

– 3% of the world population are global migrants.– The majority of migrants – ca. 100 mio. – are labor migrant.– In developed countries - 1 out of 10 is a migrant.– In developing countries - 1out of 70 is a migrant.– 16% of international migrants are under 20 years of age and 17% are

over 60 of age. These segments are increasing steadily.– ½ of labor migrants are women.

• Between 2005-2010 the numbers of international migrants increased by 1.8% annually.

• In 2007, accounted remittances constisted of 2.200 mia DKK.– 1.500 mia DKK were sent to developing countries - more than double

the amount sent as state financial aid!

Source: UN Population Division: International Migration 2009

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

New Tendencies in global man New Tendencies in global man power mobilitypower mobility

• Growing in number– More than trippled in 10 years.– 700 million internal migrants a years (urbanization).

• New destinations– 10 most popular destinations receive a smaller pct. compared to 2000. – Traditional South to North patter is changing.– Chinese and Indian migrants soon to compromise 40% of global

workforce.

• More unpredictable– BRIC and Next-11 countries as both origin and destination of

migration?

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Various types of MigrationVarious types of Migration

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Continuing types New & Future Types

Brain drain Brain Gain (Social & money remittances)

Temporary labor Education

Settlement/permanent Lifestyles choices

Reunification Pension

Forced Partner

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

WHAT WHAT DRIVESDRIVES

MIGRATIONMIGRATION??

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Drivers for developmentDrivers for development

Migration Cause

Factors affecting the decision to migrate

Supply-Push Demand-pull Driving Forces

Economic UnemploymentHigh taxesLow wagesFew develop. opp.

Labor demand Higher wagesCareer & personal development

Economic growthKnowledge centersDemographic Change GlobalisationIndividualisationPolarisationClimate ChangeHealthImmaterialisation/ Experiences

Non-Economic War and CrisisLack of securityDiscriminationUnhappy partner/family

Family Re-unificationEducationFreedom Adventure

Source: Phillip Martin m.fl.: International Migration. Facing the challenge i Population Bulletin, vol. 57, nr. 1, marts 2002

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Drivers for developmentDrivers for development

Source: Phillip Martin m.fl.: International Migration. Facing the challenge i Population Bulletin, vol. 57, nr. 1, marts 2002

Migration Cause

Factors affecting the decision to migrate

Supply-Push Demand-pull Driving Forces

Economic UnemploymentHigh taxesLow wagesFew development Opportunities

Labor demand Higher wagesCareer & personal development

Economic growthKnowledge centersDemographic Change GlobalisationIndividualisationPolarisationClimate ChangeHealthImmaterialisation/ Experiences

Non-Economic War and CrisisLack of securityDiscriminationUnhappy partner/family

Family Re-unificationEducationFreedom Adventure

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Economic DevelopemtEconomic DevelopemtGDP Growth 2000-2010GDP Growth 2000-2010

19%

33%

15%

61%

96%

28%

Source: www.imf.org - IMF World Economic Outlook (WEO)

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Economic DevelopemtEconomic DevelopemtGDP Growth 2010-2020GDP Growth 2010-2020

11%

32%

9%

61%

61%

15%

Source: www.imf.org - IMF World Economic Outlook (WEO) + CIFS estimate

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Economic developmentEconomic developmentMega-regionsMega-regions

’The more things are global, the more decisive location becomes’ Michael Porter Harvard Business School on the Location Paradox

Mega-regions

Population in Millions

Population global share

Economic activity, global share

Most frequent quoted scholars, global share

10 Biggest 416 6,5% 43% 53%

20 Biggest 540 10% 57% 76%

40 Biggest 1.150 18% 66% 83%

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Knowledge Accumulation:Knowledge Accumulation:New Knowledge HotspotsNew Knowledge Hotspots

Source: UNESCO 2009

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Knowledge Accumulation:Knowledge Accumulation:New Knowledge HotspotsNew Knowledge Hotspots

Source: UNESCO 2009

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Demographic Change:Demographic Change:An aging worldAn aging world

Source: UN Population Perspectives, 2008

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Demographic Change:Demographic Change:Europe and AfricaEurope and Africa

Source: UN Population Perspectives, 2008

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Globalisation:Globalisation:Number of migrants on a global scale Number of migrants on a global scale

81,3 86,399,3 111

154,9 165,1176,7

190,6214

0

50

100

150

200

250

1970

1975

1980

1985

1990

1995

2000

2005

2010

Year

Num

ber

in m

illi

on

UN Population Division: International migration, 2009.

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

DESTINATIDESTINATIONON

COUNTRIESCOUNTRIES

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Migration destinationsMigration destinations

23,4%50 mio.

3%7 mio.

32,7%70 mio.

8,3%18 mio.

28,5%61 mio.

3,4%8 mio.

Source: UN Population Division: International Migration 2009

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Top Destination CountriesTop Destination Countries

Source: UN Population Division: International Migration 2009

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

International Migrant stock International Migrant stock (in thousands)(in thousands)

Source: UN Population Division: International Migration 2009

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

International migrantsInternational migrants(percentage of total population)(percentage of total population)

Source: UN Population Division: International Migration 2009

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

WHERE DO WHERE DO MIGRANTS MIGRANTS

COME COME FROM?FROM?

.. AND HOW DO WE RECRUIT THEM?

10 approaches

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

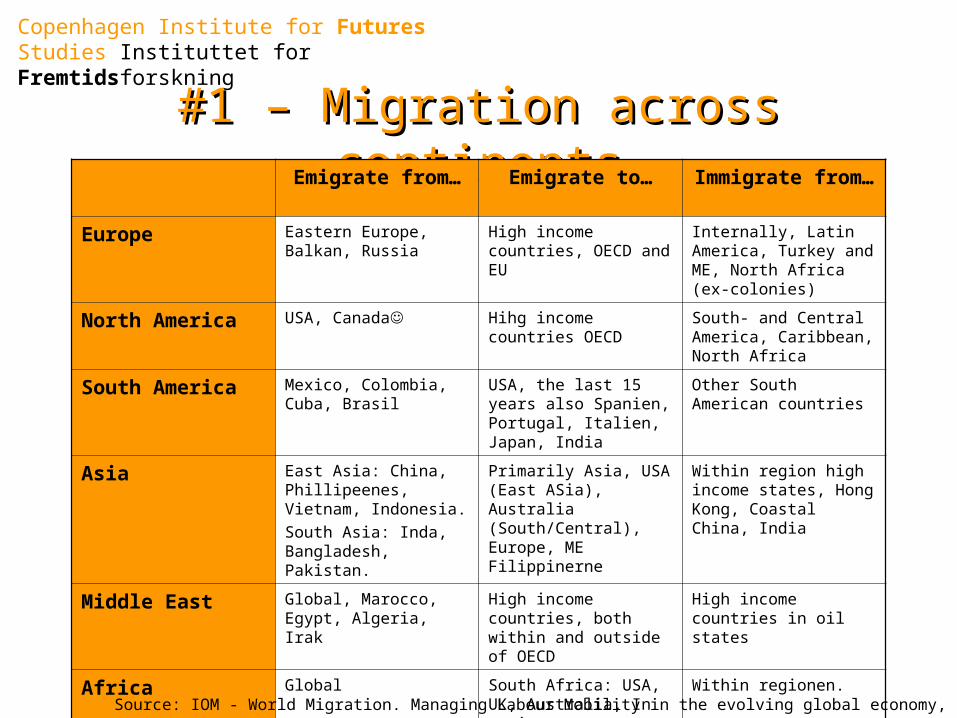

#1 – Migration across continents#1 – Migration across continentsEmigrate from… Emigrate to… Immigrate

from…

Europe Eastern Europe, Balkan, Russia

High income countries, OECD and EU

Internally, Latin America, Turkey and ME, North Africa (ex-colonies)

North America USA, Canada Hihg income countries OECD

South- and Central America, Caribbean, North Africa

South America Mexico, Colombia, Cuba, Brasil

USA, the last 15 years also Spanien, Portugal, Italien, Japan, India

Other South American countries

Asia East Asia: China, Phillipeenes, Vietnam, Indonesia.South Asia: Inda, Bangladesh, Pakistan.

Primarily Asia, USA (East ASia), Australia (South/Central), Europe, ME Filippinerne

Within region high income states, Hong Kong, Coastal China, India

Middle East Global, Marocco, Egypt, Algeria, Irak

High income countries, both within and outside of OECD

High income countries in oil states

Africa Global South Africa: USA, UK, Australia, In regionen.North and Eastt: Europe, North America.

Within regionen.

Source: IOM - World Migration. Managing Labour Mobility in the evolving global economy, 2008

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

#2 Top 25 Emigration-states,1995 og #2 Top 25 Emigration-states,1995 og 20052005

0

50

100

150

200

250

300

350

400

450

Land

Ne

t e

mig

rati

on

(tu

sin

de

r)

Source: IFFs analyse på baggrund af data fra UN Population Division: International Migration Global Assessment 2006

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

#3 – Skilled immigrants out of net #3 – Skilled immigrants out of net emigrationemigration

Source: IFFs analyse på baggrund af data fra UN Population Division: International Migration Global Assessment 2006

0

10

20

30

40

50

60

70

Country

Nu

mb

er o

f Q

ual

ifie

d e

mig

ran

ts (

in t

ho

usa

nd

s)

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning#4- Skilled immigrants out of net #4- Skilled immigrants out of net

emigration emigration per countryper country

Source: IFFs analyse på baggrund af data fra UN Population Division: International Migration Global Assessment 2006

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Land

Pct

.

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Source: IFFs analyse på baggrund af data fra UN Population Division: International Migration Global Assessment 2006

#5 - Remittances in top 25 receiving #5 - Remittances in top 25 receiving countries, 1995 and 2005countries, 1995 and 2005

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

WHOWHO MIGRATES?MIGRATES?

Migrant Profiles

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

#6- Mobility and Age#6- Mobility and Age

Source: Intelligence Group: Get ready for the international recruitment rally, 2009

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

#7 - Mobility and life stages#7 - Mobility and life stages

Life-stage

Apprx. Age

Number 2020 Challenges

Free 1 20-35 years

Slightly more Millenials

Nomads, searching for idendity, self-realization, big cities

Parent 35-55 years

Fewer Gen. X

Pressed for time and money, balance between work and family

Free 2 55+ years More Baby Boomers

New opportunities, consumption options, health, self-realization

Source: CIFS MR#3, 2010 ’Global Talent Rally’

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

#8 - New segments#8 - New segments

• Females – ½ of migrant population are females.– 60% of students in Europe & US and nearly 70% in developing

countries are females.– 40% more skilled females than males among migrants.

• Singles– Mobility does not fall according to life cycle.– Strong need for low skilled labor.

• Low skilled labor force– Migration myth we only need highly skilled labor.– In US: 2 pct. of labor force but 22 pct. of domestic help.

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

#9 #9 –– Immigrantprofiler Immigrantprofiler

Low-Skilled/ ufaglært

Medium-Skilled / faglært

Highly-Skilled/ Specialised

Permanent Rural MigrationAsyllum seeking

Political/Environmental Refugee

Forced MigrationElder/Retired

Political refugeesHealth Care

Political Refugee

Temporary Au-pairService sector- hospitality

YouthConstruction Sector

Health CareElder

YouthHealth Care

IT-SectorStudents

Circular Au-pairService sector- hospitality

Seasonal Labor

YouthConstruction Sector

Health Care

ResearchersGlobale talentsGeneration Y

Creative ClassResourcesful Elder

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

#10 - Hotspots#10 - Hotspots

• Close:– Iceland– Ireland

• Rest of Europe:– Turkey– Ukraine

•World:–Botswana–Venezuela–Malaysia–Mexico–Thailand–California

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

ConclusionConclusionNeed to actively recruit and retainNeed to actively recruit and retain

• A number of megatrends drive & change migration• New tendencies in migration (destinations, number of migrants,

unpredictabilities)

• From push to pull - demand driven labor migration:• Demand driven migration – hotspots and knowledge centres• Demographic change & the needs of the labor market• Talent attraction will be a highly competitive market• Migration is therefore becoming more circular in nature

• New types of migration, new drivers• Life-cycle, and migrant-profile oriented strategies• Migration becoming increasingly circular

• There is a need to actively attract and retain new talent.

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

ENJOY ENJOY YOURYOUR BREAKBREAK

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

ARE WE ARE WE ABLE TO ABLE TO

ATTRACT?ATTRACT?

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Global migration barometerGlobal migration barometer

Denmark Norway SwedenNeed for migrants

33 20 16

Attractive for migrants

12 4 7

Accessible for migrants

47 20 9

Source: Global Migration Barometer, Verdensbanken 2008

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Comparison of Nordic Comparison of Nordic CountriesCountries

Indication: Denmark

Norway Sweden

Qualified labor from 3rd party state

Labor from EU/EEC

Source: Nordisk Råd - Rekruttering af kompetencearbejdskraft fra tredjelande til Norden, 2010

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

The competent and The competent and unemployedunemployed

Source: Bernand Salt, ’Global Skills Convergense’, KPMG 2008

Copenhagen Institute for Futures Studies Instituttet for FremtidsforskningForeign Talents &

Researchers• 95 of 96 applications for a PhD at the University of Stavanger’s Institute of Petroleum

Technology have come from foreigners.The Foreigner, Norwegian News In English Tuesday, 30th November

• 1:4 of doctoral fellows & 1:6 of other academic staff at Norwegian universities and university college sectors are foreigners. Research Council of Norway, 2009.

• ”Why stay in Norway? Outdoor activities, family friendly culture, well-established research community - both temporary and long-term jobs, space for professional development.”

Professor Nadim, a qualified civil engineer from Iran.

• US: 1 foreign engineer creates 5 new jobs. DK: 1 foreign engineer creates 2 new jobs – indirectly many more.T. Rogers, Semiconductor & Danish Ministry of Economics and Business Affairs.

• DK: In 3 years foreign talents increase productivity with 5-15%.Jan Rose Skaksen, professor at ECON, CBS.

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

NEW NEW DEMANDSDEMANDS

AND AND NEEDSNEEDS

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

IImmportant Pull Factorsportant Pull Factors

Source: Intelligence Group, ’Get ready for the international recruitment rally’, 2009

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Incentives for the global Incentives for the global workerworker

Pull Factors Companies (in order of priority)

Pull Factors Countries(in order of priority)

Interesting work Personal security

Language classes Opportunities for professional development

Help finding housing Existance of interesting job and career opportunities

Career opportunities Career improvement options

Repatriation schemes Quality of health care system

Help finding child care & schools

The environment (green and clean)

Paid visit before beginning of work

Open hospitable population

Source: Oxford Research Expat study 2006

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Next generation: DisloyalNext generation: Disloyal

01020304050607080

Chang

e job

with

in2 ye

ars

Not in

expe

cted j

ob

Satisfi

ed w

ith cu

rrent

job

Lking f

r new

job

Pct.

Source: Experience 2008

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Generation Y / Millennials:Generation Y / Millennials:

Source: PWC, ’Talent Mobility 2020’

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

Talent-profiles in 2020:Talent-profiles in 2020:Difference in strategiesDifference in strategies

Generation X (’70 and start 80’erne):-Top of salary hierarchy.-’People are not flat’ – experienced and high competences- less mobile-Selective in tasks-selection- career focused-Seniority packages. Safety, commute-Long-term tasks

Generation Y / Millennials (’90-’00):-New on the labor market-Organizations and world without boundaries.-Most varied/international assignments-Customized & target oriented career styles.-Flexible in length and types of tasks-Emphasis on interests and opportunities

Baby Boomers (60’ies):-Reached height of career-Once again mobile-Location & Opportunities-Long-term tasks

Source: PWC, ’Talent Mobility 2020’

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

ConclusionConclusion Norway is attractive but not very accessible

Need to recruit from third countries

Foreigners contribute significantly to the economy.

New demands and needs Good standard of living (cheap!). From ‘cradle to grave’.

Incorporate different strategies according to life stages, profiles and needs.

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

SHORT SHORT WORKSHOPWORKSHOP

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

In pairs: Interview each other using following guide lines

• Migrant profile?– What is your marital status and gender? What is your income level (high, medium,

low)? Skills and qualification level (low, average, high, expert?) Which age group do you belong to (life phase)?

• Mobility and needs?Incentives to move to a specific country, megacity or company?– Pull: Personal incentives (Career, selfdevelopment, adventure, etc.) or family

incentives (education, spouses career, etc.)?– Push: Poorer opportunities in country of origin?

• Barriers to mobility?– Lack of knowledge? Lack of incentives?

• Based on the above information, discuss:– What strategy or strategies should I use to attract and retain you?

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

THANKS THANKS FOR YOUR FOR YOUR ATTENTIONATTENTION

!!Sally Khallash, [email protected]

Copenhagen Institute for Futures Studies Instituttet for Fremtidsforskning

DiscussionWith starting point in your companies, discuss strategies to recruit and retain the global talents you need. For instance:

• Expertise– What expertise is needed? Which fields?

• Profile– Age, mobility, experience, language skills, marital status, etc.?

• Attract– Where and how can we attract them? Through what media?

• Incentives– Career opportunities, living standards, travel, adventure, job opportunities,

education, etc.? • Retain

– Personal and academic development, customized career in varied fields, family packages, etc.?