37

| Date post: | 23-Jan-2017 |

| Category: |

Documents |

| Upload: | mines-and-money |

| View: | 986 times |

| Download: | 0 times |

Li Yusheng Senior Analyst

Beijing Antaike Information Development

Yusheng Li

Beijing Antaike Information Development Co., Ltd.

5th December, 2012 London UK

Copper market analysis and investment climate:

Where we are in the cycle

Mines And Money London 2012

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

4 4

Disclaimer

This document has been prepared with care. However, Beijing Antaike Information Development Co., Ltd. (hereinafter Antaike) makes no warranty of any kind in regard to the contents and shall not be liable for incidental or consequential damages, financial or otherwise, arising out of the use of this document.

Copyright

The contents of this presentation are copyright Antaike

© 2012 Antaike

Disclaimer & Copyright

4

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

5 5

Outline of the presentation

1. Copper price and its driving forces

2. China’s copper supply and demand

3. Prospects for China’s copper supply/demand

4. Copper price outlook in 2013

5

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

1. Copper price and its driving forces

a. Copper price review

6

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

Copper price review

7 Data source: LME , SHFE

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

8 8

Sharp fluctuations in copper price over the past

decade

Copper price started to climb up from Q4, 2003 and soared

in 2006. It rose to the record high of US$8,685 per tonne on

LME and RMB85,500yuan/t on SHFE in the year. Then it

continued to surge and refreshed the highest several times.

But the upward trend came to an end in Q4, 2008, with price

falling to the low of US$2,825 per tonne on LME and

RMB22,320 yuan/t on SHFE. In Feb. 2011, the price once

again went up and reached US$10,190 per tonne on LME

and 75,660 yuan/t on SHFE.

Copper price review

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

1. Copper price and its driving forces

b. Factors affecting copper price

9

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

US dollar index

Inventory

Unpredictable events

Fundamentals: supply-demand

Factors affecting copper price

10

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

Copper inventory vs price

11 Data source: LME, SHFE

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

US dollar index vs copper price

12 Data source: LME, NYMEX

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

Factors affecting copper price

Events

SRB? 2006, 2009

Lehman Brothers 2008

QE1, QE2, and QE3?

Demand/supply

kt 2002 2011 CAGR

Mine copper output 13581.8 16035.5 1.86%

Refined copper output 15269.3 19650.0 2.84%

Refined copper consumption 15155.6 19888.1 3.07%

Data source: ICSG

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

14 14

2. China’s copper supply and demand

“China factor”

14

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

15

China became the biggest copper consumer in the world in

2002. From 2002 to 2011, it witnessed a CAGR of 11.8% in

copper consumption, from 2.68 million tonnes to to 7.33 million

tonnes.

During the same period, China’s copper production increased

quickly, getting to 5.20 million tonnes in 2011, with a CAGR of

13.7%, but shortage of raw materials continued to widen.

Big difference appeared between apparent and actual

consumption of refined copper from 2009, while copper scrap

supply declined.

15

“China factor”

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

China’s copper demand

16

Data source: China Customs, CNIA, Antaike

0

1000

2000

3000

4000

5000

6000

7000

8000

kt

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

China's refined copper consumption

Actual Apparent

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

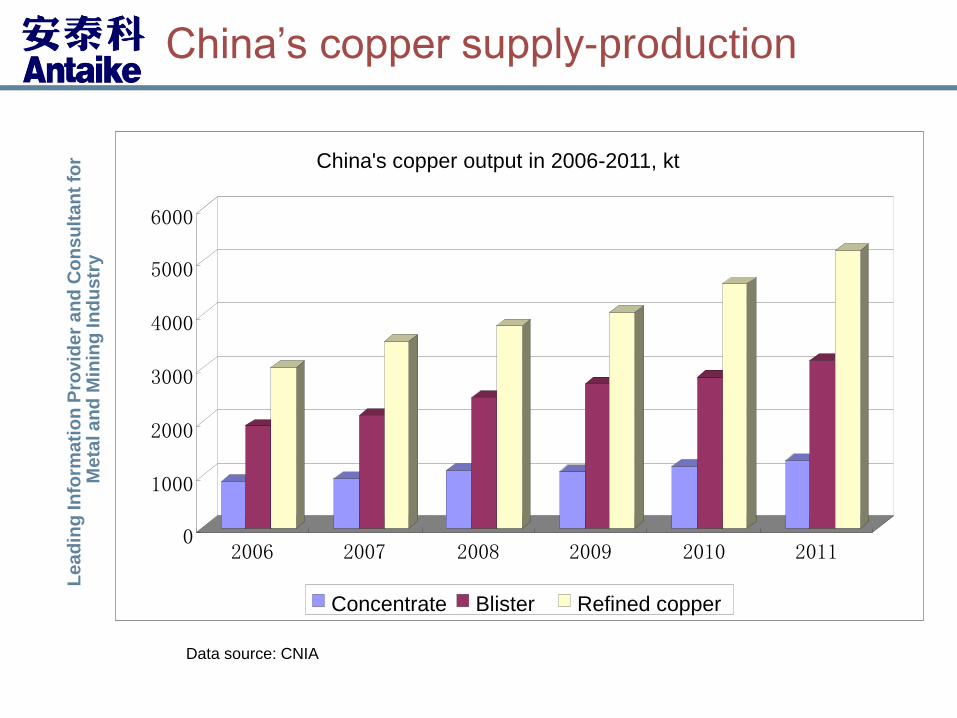

China’s copper supply-production

17

kt 2006 2007 2008 2009 2010 2011

Cu Concentrate 872.9 928.0 1076.1 1044.5 1155.8 1267.2

Copper Blister 1917.5 2111.5 2453.3 2693.9 2825.6 3136.1

Refined Copper 3003.2 3499.4 3794.6 4051.3 4573.5 5196.9

Copper semis 5324.4 6302.1 8367.1 8736.4 9851.3 10281.5

China’s copper production

Data source: CNIA

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

China’s copper supply-production

Data source: CNIA

0

1000

2000

3000

4000

5000

6000

2006 2007 2008 2009 2010 2011

China's copper output in 2006-2011, kt

Concentrate Blister Refined copper

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

China’s copper supply-import

kt 2007 2008 2009 2010 2011

Cu Concentrate 4516.2 5192.1 6130.9 6468.1 6375.5

Copper Scrap 5584.7 5576.9 3998.1 4364.3 4687.3

Copper Blister 172.8 197.6 228.1 399.0 416.3

Refined Cu (imp) 1493.7 1456.4 3185.2 2922.1 2835.4

Refined Cu (exp) 125.9 96.1 72.9 38.7 156.3

Refined Cu (net import) 1367.8 1360.3 3112.3 2883.4 2679.1

Data source: China Customs

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

China’s copper supply-import

Data source: China Customs

0

1000

2000

3000

4000

5000

6000

7000

2006 2007 2008 2009 2010 2011

China's copper imports in 2006-2011, kt

Concentrate Cu scrap Refined Cu Cu Blister

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

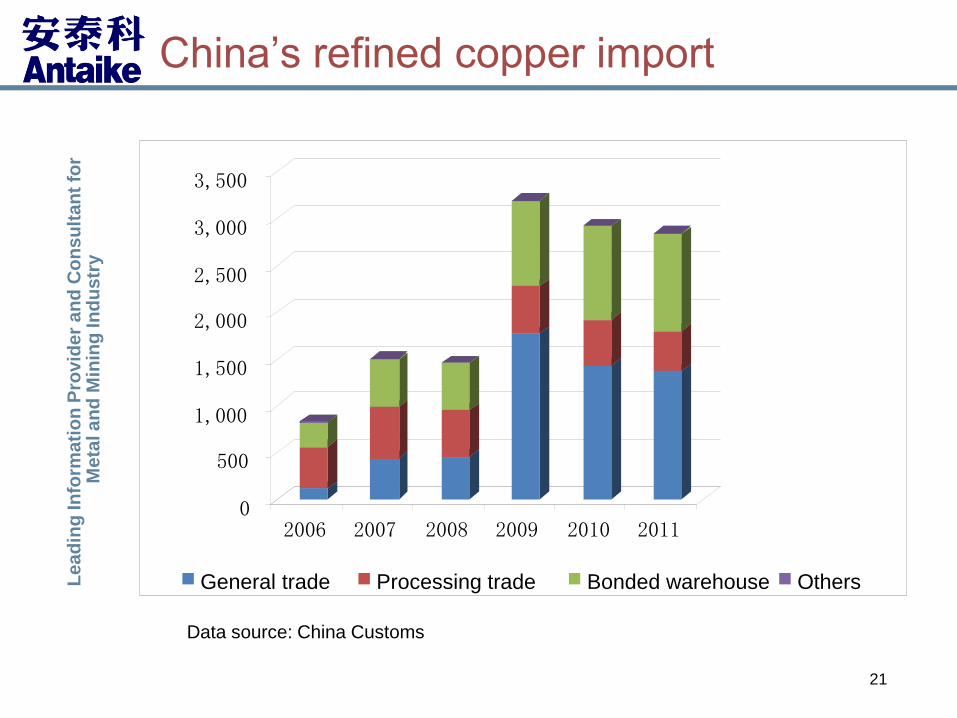

China’s refined copper import

21

kt

Data source: China Customs

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2006 2007 2008 2009 2010 2011

General trade Processing trade Bonded warehouse Others

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

22

Copper scrap import declined significantly in 2009

SRB restocked

Copper financing-collateral for loan

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

23 23

3. Prospects for China’s copper supply/demand

23

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

24

Production, kt Jan-Sep, 2011 Jan-Sep, 2012 Y-o-Y

Cu Concentrate 919.2 1155.0 13.8%

Refined Copper 3932.6 4205.6 7.3%

Copper Semis 7572.9 8389.1 9.4%

Import & Export, kt Jan-Sep, 2011 Jan-Sep, 2012 Y-o-Y

Cu Concentrate 4633.6 5347.0 15.4%

Copper Blister 307.6 384.5 25.0%

Copper Scrap 3429.5 3551.5 3.6%

Refined Copper (imp) 1789.2 2681.9 49.9%

Refined Copper (exp) 153.6 214.8 39.8%

Net Import 1635.6 2467.1 50.8%

China copper market review

24 Data source: CNIA, China Customs

China’s Copper supply in January-September, 2012

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

25

Supply:

From January to September, 2012, China’s refined copper

output was 4.21 million tonnes with an increase of 7.3% y-o-y,

and net import of refined copper increased by 50.8% y-o-y to

2.47 million tonnes, and refined copper supply rose to 6.67

million tonnes with an increase of 19.8% y-o-y.

Demand:

From January to September, 2012, China’s refined copper

consumption was 5.71 million tonnes, the rate of demand

growth slowed down to 4.6 % y-o-y.

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

26

Major industrial product output

Data source: NBS

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

27

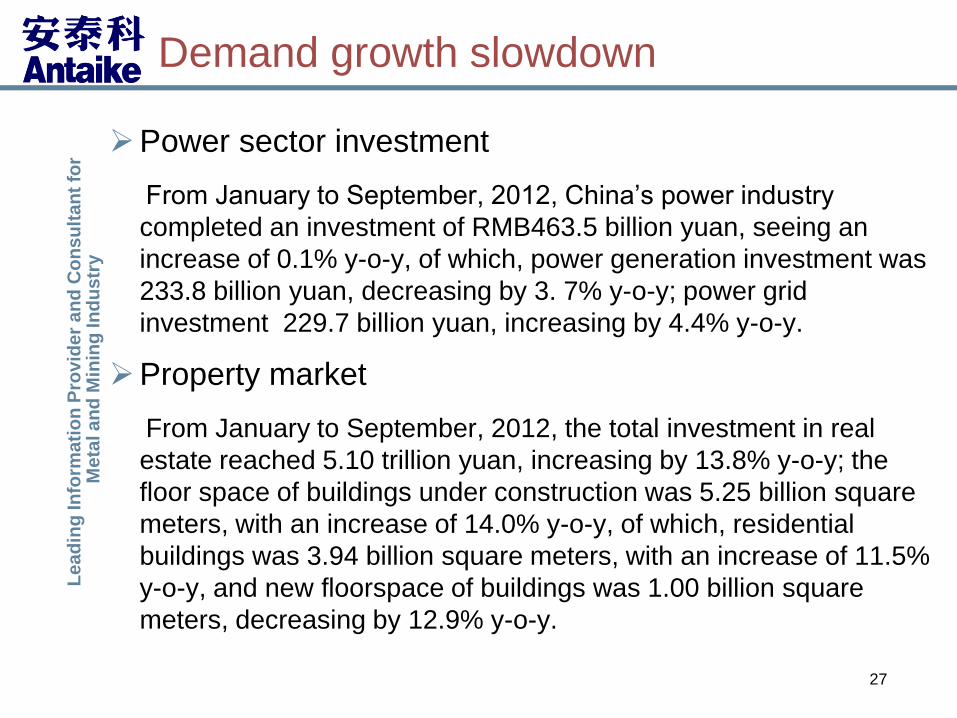

Demand growth slowdown

Power sector investment

From January to September, 2012, China’s power industry

completed an investment of RMB463.5 billion yuan, seeing an

increase of 0.1% y-o-y, of which, power generation investment was

233.8 billion yuan, decreasing by 3. 7% y-o-y; power grid

investment 229.7 billion yuan, increasing by 4.4% y-o-y.

Property market

From January to September, 2012, the total investment in real

estate reached 5.10 trillion yuan, increasing by 13.8% y-o-y; the

floor space of buildings under construction was 5.25 billion square

meters, with an increase of 14.0% y-o-y, of which, residential

buildings was 3.94 billion square meters, with an increase of 11.5%

y-o-y, and new floorspace of buildings was 1.00 billion square

meters, decreasing by 12.9% y-o-y.

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

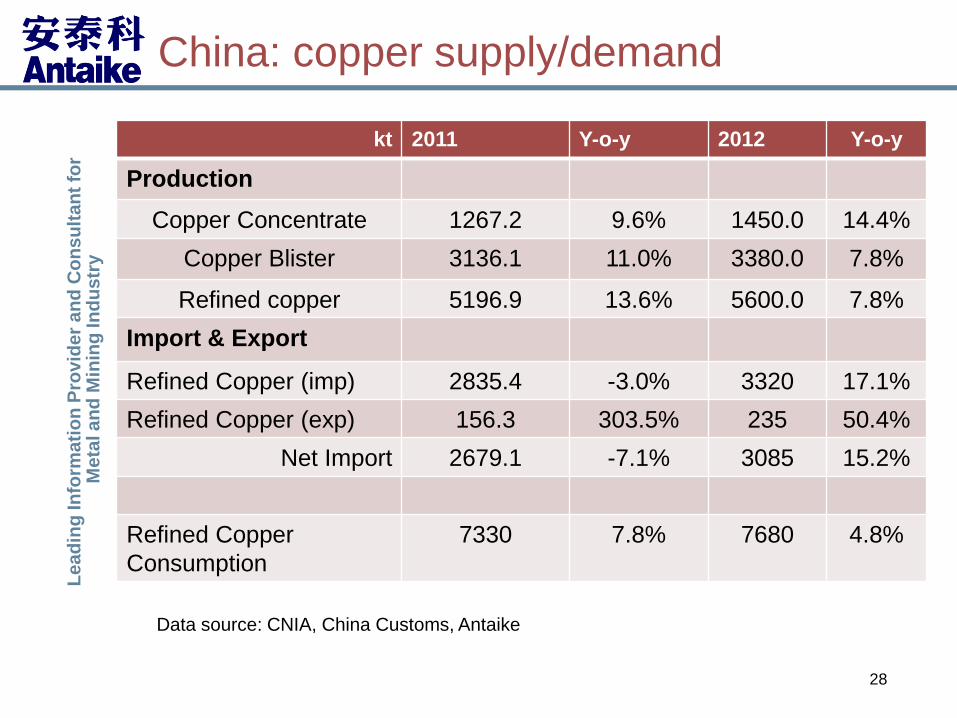

28

China: copper supply/demand

kt 2011 Y-o-y 2012 Y-o-y

Production

Copper Concentrate 1267.2 9.6% 1450.0 14.4%

Copper Blister 3136.1 11.0% 3380.0 7.8%

Refined copper 5196.9 13.6% 5600.0 7.8%

Import & Export

Refined Copper (imp) 2835.4 -3.0% 3320 17.1%

Refined Copper (exp) 156.3 303.5% 235 50.4%

Net Import 2679.1 -7.1% 3085 15.2%

Refined Copper

Consumption

7330 7.8% 7680 4.8%

Data source: CNIA, China Customs, Antaike

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

China copper supply/demand by 2015

29

mlt 2013 2014 2015

Production

Concentrates 1.55 1.64 1.74

Refined copper 6.10 6.60 7.00

Consumption

Refined copper 8.10 8.53 8.90

Balance -2.00 -1.93 -1.90

Data source: Antaike

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

30 30

4. Copper price outlook in 2013

30

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

Copper price outlook in 2013

Production: the year of 2013 will be the last year for a number of

copper smelting projects to come on-stream. It is forecasted

China’s copper smelting and refining capacity would be 5.59 Mt

and 9.76 Mt in 2013, respectively, up by 920kt and 1.4 Mt

compared to 2012. The refined copper output will be 6.1 Mt in 2013,

up by 8.9% y-o-y.

Consumption: soft demand leads to slowdown in growth of copper

consumption in China in 2012 and Chinese government released a

package of stimulus policies to encourage the real economy. The

economic environment is expected to get better in 2013 and copper

demand may rebound slightly. It is forecasted the Chinese refined

copper consumption would be 8.1 Mt in 2013, up by 5.5% y-o-y.

Balance: Chinese refined copper production would be a bit more

than that of consumption in 2013. The gap between the output and

consumption would shrink to about 2 Mt.

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

Copper price outlook in 2013

It is expected that global economy will recover a

little bit in 2013, but might see “uneven” between

different regions or countries. Generally speaking,

the economy is difficult to get warm quickly. In

addition, growth in demand from China will remain

moderately low, so copper price will continue to

move in a even wider range than that in 2012,

staying at about US$7,900 per tonne on average on

international market and RMB 57,500-58,000 yuan/t

in China.

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

Copper industry is facing the challenges from the

slowing demand conditions.

China will remain as the largest copper consuming

country and continue to be a key support to world

copper market, although the growth rate will be

slow down in next five years.

Raw material supply shortage will increase to

Chinese copper companies with their involvement

in copper mining projects overseas.

Summary

33

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

34 34

Thank you!

34

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

35 35

About Antaike

○ Regular research reports ○ Consultancy ○Metal Events

The Most Essential and Authoritative Source for Chinese Metals Market

The Leading Information Provider and Consultancy for the Global Metals and Mining

Industry

Since being established in 1992, Antaike has built a reputation for its authoritative, strategic, and in-depth analysis

of the Chinese metals industries and markets. It also provides news, trade and production data, prices and

forecast.

Working under China Nonferrous Metals Industry Association (CNIA) and directly overseen by the Information

Center of China National Nonferrous Metals Industry, Antaike has become a key center for information collection

and delivery within the country and across the world.

Antaike has a team of nearly 100 highly skilled employees, including more than 30 senior metals analysts, who

have all been involved in the metals and mining industry for over a decade. It offers customized consulting

assignments to deliver high quality and specialized advice and business intelligence.

Antaike has built up good relationship with thousands of Chinese miners, smelters, refineries, fabricators, metals

consumers and traders, as well as Chinese government departments. At the same time, it has been working with

a large number of international metals and mining corporations, associated organizations and research institutes.

It has more than 10,000 clients, both in China and abroad.

Antaike’s metal events have been attracting more and more attendees in recent years. They have become the

biggest and most informative gatherings in China and even the world, with their focus on specific metals such as

copper, aluminum, lead and zinc, nickel and cobalt, gold and silver, indium, and others.

Antaike’s motto is to supply the best services to our clients and to use our information to create business value.

35

Le

ad

ing

In

form

ati

on

Pro

vid

er

an

d C

on

su

lta

nt

for

Me

tal a

nd

Min

ing

In

du

str

y

36 36

Contact:

Yusheng Li

Beijing Antaike Information Co., Ltd.

2nd Floor, 12B Fuxing Road, Beijing 100814, CHINA

Tel:+86 10 6396 5357

Fax: +86 10 6397 1647

Email:[email protected]

website:www.antaike.com