25

Copyright © 2009 Pearson Prentice Hall. All rights reserved. Chapter 1 Currency Exchange Rates

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | bryan-sullivan |

| View: | 219 times |

| Download: | 0 times |

Copyright © 2009 Pearson Prentice Hall. All rights reserved.

Chapter 1

Currency Exchange Rates

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 2

Currency Abbreviations

Abbreviations are used to refer to the various currencies. These abbreviations could be commonly used symbols or “official” three-letter codes.

Financial newspapers such as the Financial Times generally use symbols, while traders use three-letter codes. Symbols include $ (U.S. dollar), ¥ ( Japanese yen), € (euro), £ (British pound), A$ (Australian dollar), and Sfr (Swiss franc).

Three-letter codes for the same currencies are USD, JPY, EUR, GBP, AUD, and CHF.

We will alternatively use in this book (as done in the real world) the various currency abbreviations that are commonly encountered. For example, the Japanese yen can be referred to as ¥, JPY, or yen.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 3

Currency Exchange Rate Quotations

A currency exchange rate is the rate used to exchange two currencies. An exchange rate states the price of one currency in terms of units of another currency.

Examples: $:€, €:$, ¥:$ Note: the notation in this new edition of the

text has changed relative to previous editions.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 4

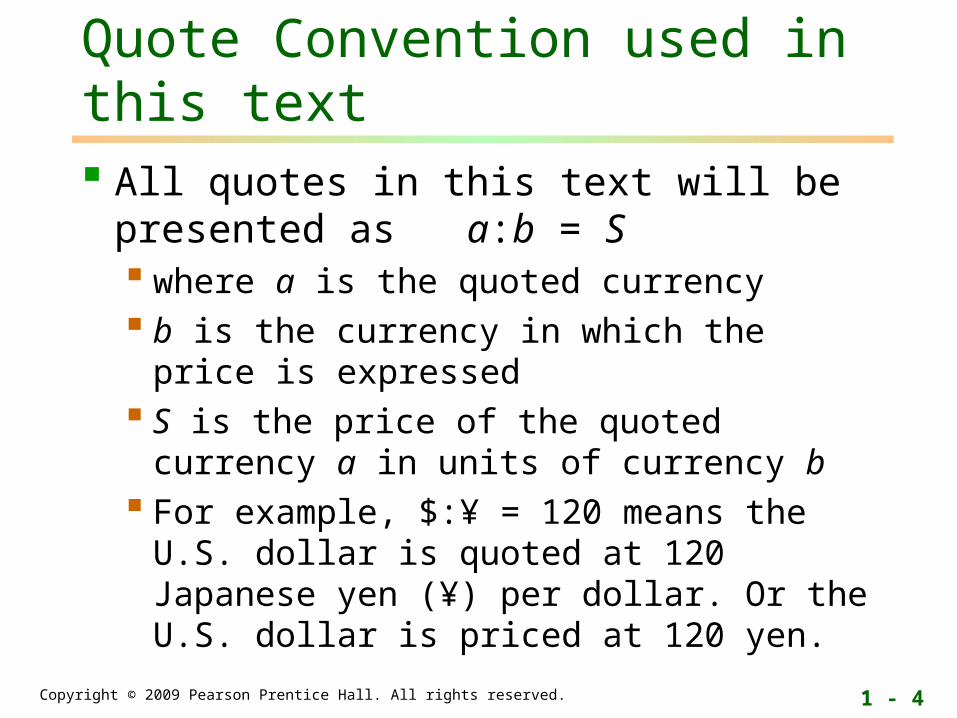

Quote Convention used in this text

All quotes in this text will be presented as a:b = S

where a is the quoted currency b is the currency in which the price is expressed S is the price of the quoted currency a in units

of currency b For example, $:¥ = 120 means the U.S. dollar is

quoted at 120 Japanese yen (¥) per dollar. Or the U.S. dollar is priced at 120 yen.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 5

Direct Exchange Quotes

A direct exchange rate is the domestic price of foreign currency.

For example, an American investor seeing a direct quote €:$ = 1.25 knows she will pay $1.25 for one euro.

To a European investor, the direct quote is $:€ = 0.8 which says that 1 dollar (foreign currency) is worth 0.8 euro.

An appreciation of the foreign currency causes an increase in the direct quote.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 6

Indirect Foreign Exchange Quotations

An indirect exchange rate is the amount of foreign currency that one unit of domestic currency will purchase.

For an American investor, the indirect quote $:€ = 0.8 says that 1 dollar will purchase 0.8 euro.

Direct quotes and indirect quotes are reciprocals of each other.

An appreciation of the foreign currency causes a decrease in the indirect quote.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 7

Example: Direct and Indirect Exchange Rates

On July 1, the British pound (£) is quoted as £:$ = 1.80. Is this a direct or indirect quote from the

viewpoint of an American and a British investor?

A month later, the exchange rate moved to £:$ = 1.90. Which currencies appreciated or depreciated?

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 8

Example: Direct and Indirect Exchange Rates - Continued

Answer: The pound is quoted in terms of dollars. This quote is a direct quote from the American viewpoint and an indirect quote from the British viewpoint.

The pound is the quoted currency. Over a month, the pound’s price increased from $1.80 to $1.90, so the pound appreciated and the dollar depreciated.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 9

Currency Movements and Exchange Rate Quotations

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 10

Cross Rate Calculations

A cross rate is the exchange rate between two countries inferred from each country’s exchange rate with a third country.

For example, bank A gives the following quotations: €:$ = 1.25 $:¥ = 120

Calculate the euro in yen (€:¥) rate: (€:$) ($:¥) = 1.25 120 = 150 The resulting quotation is: €:¥ = 150. One euro

is worth 150 yen.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 11

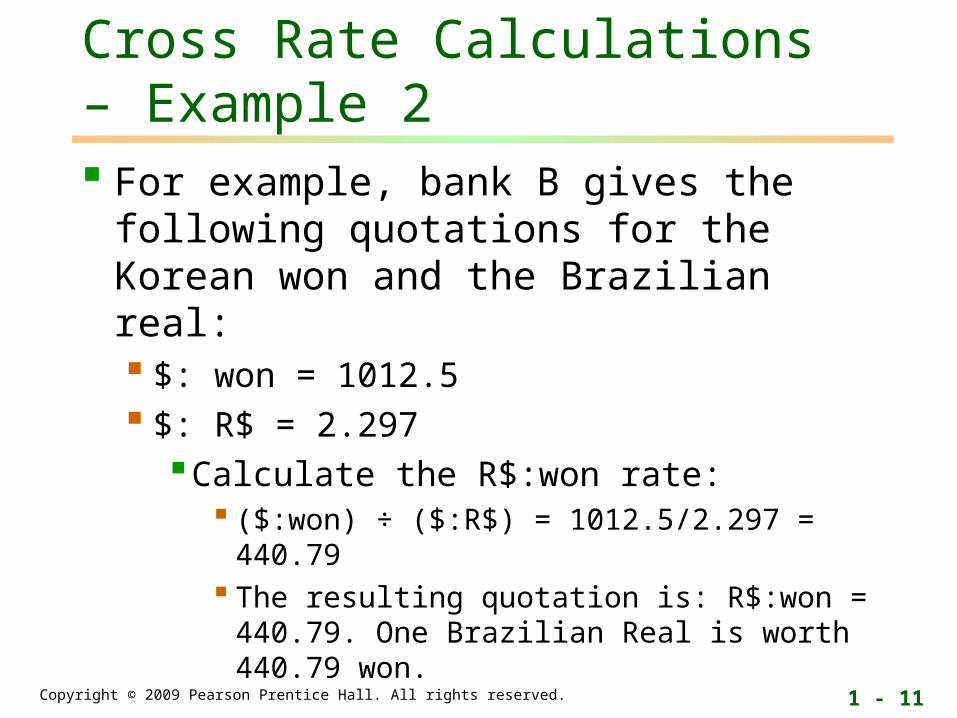

Cross Rate Calculations – Example 2

For example, bank B gives the following quotations for the Korean won and the Brazilian real: $: won = 1012.5 $: R$ = 2.297

Calculate the R$:won rate: ($:won) ÷ ($:R$) = 1012.5/2.297 = 440.79 The resulting quotation is: R$:won = 440.79.

One Brazilian Real is worth 440.79 won.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 12

Foreign Exchange Market

The international currency market has two main components:

A worldwide Forex market between major banks and specialized currency dealers. This is a wholesale interbank market for large transactions. It is an OTC market, by telephone and electronic trading platforms, where trading takes place 24 hours a day, 5 days a week. It is the largest and most liquid financial market in the world.

A retail market where investors and corporations deal with local banks.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 13

Forex Market Conventions

In the Forex market, quotations on trading screens are generally given with five significant digits and three-letter codes. For example, the USD:JPY quote could appear as 120.10 and the EUR:USD as 1.2515.

Market makers quote both a bid and an ask price, and there is no additional fee or commission.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 14

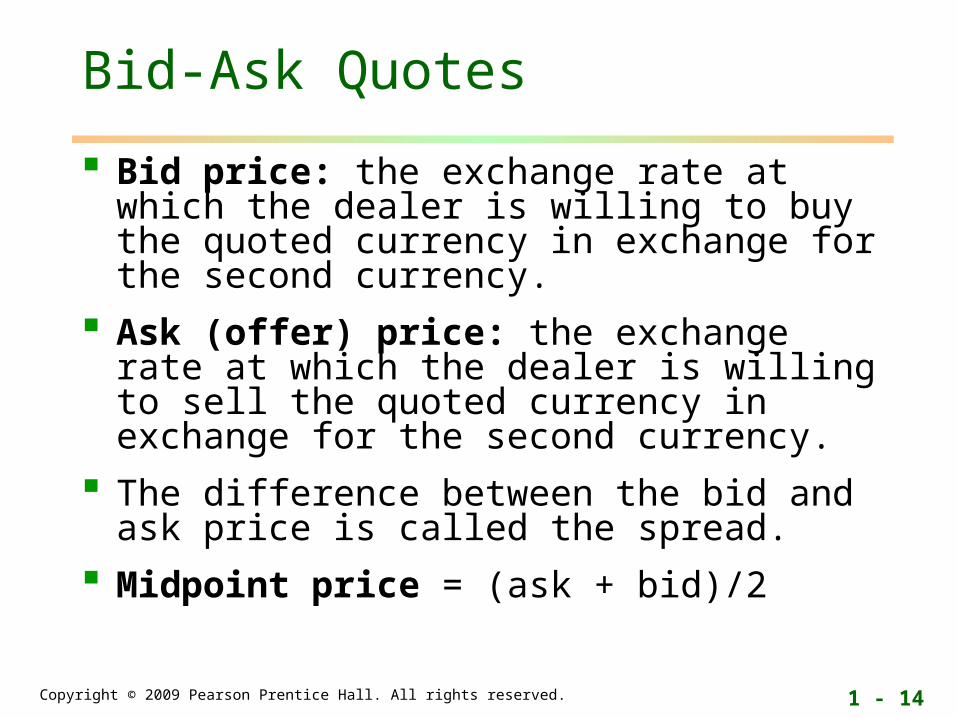

Bid-Ask Quotes

Bid price: the exchange rate at which the dealer is willing to buy the quoted currency in exchange for the second currency.

Ask (offer) price: the exchange rate at which the dealer is willing to sell the quoted currency in exchange for the second currency.

The difference between the bid and ask price is called the spread.

Midpoint price = (ask + bid)/2

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 15

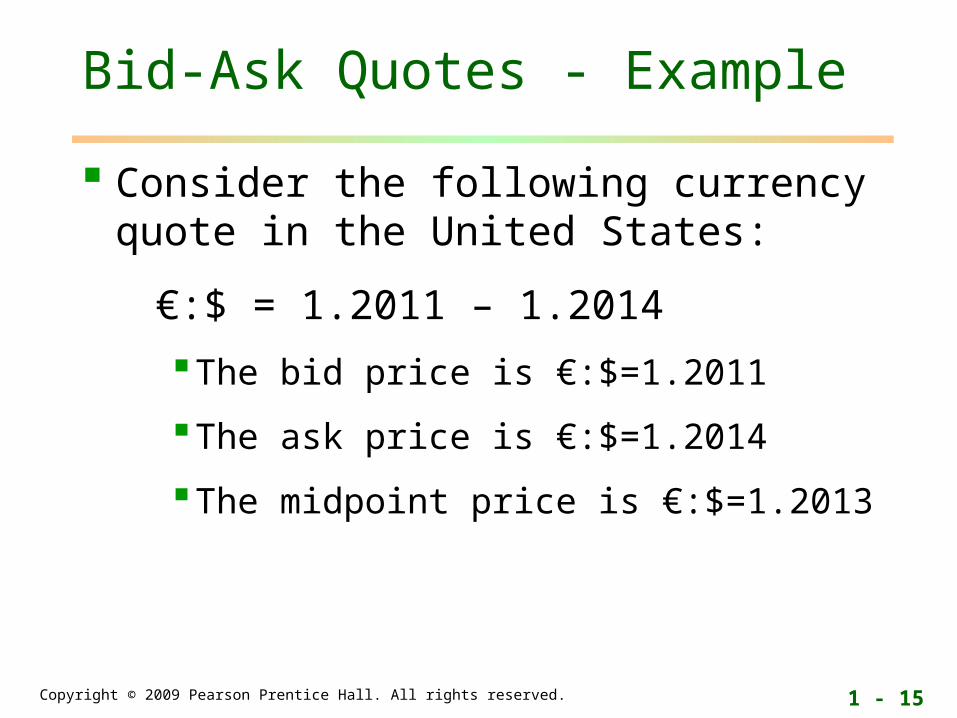

Bid-Ask Quotes - Example

Consider the following currency quote in the United States:

€:$ = 1.2011 – 1.2014

The bid price is €:$=1.2011

The ask price is €:$=1.2014

The midpoint price is €:$=1.2013

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 16

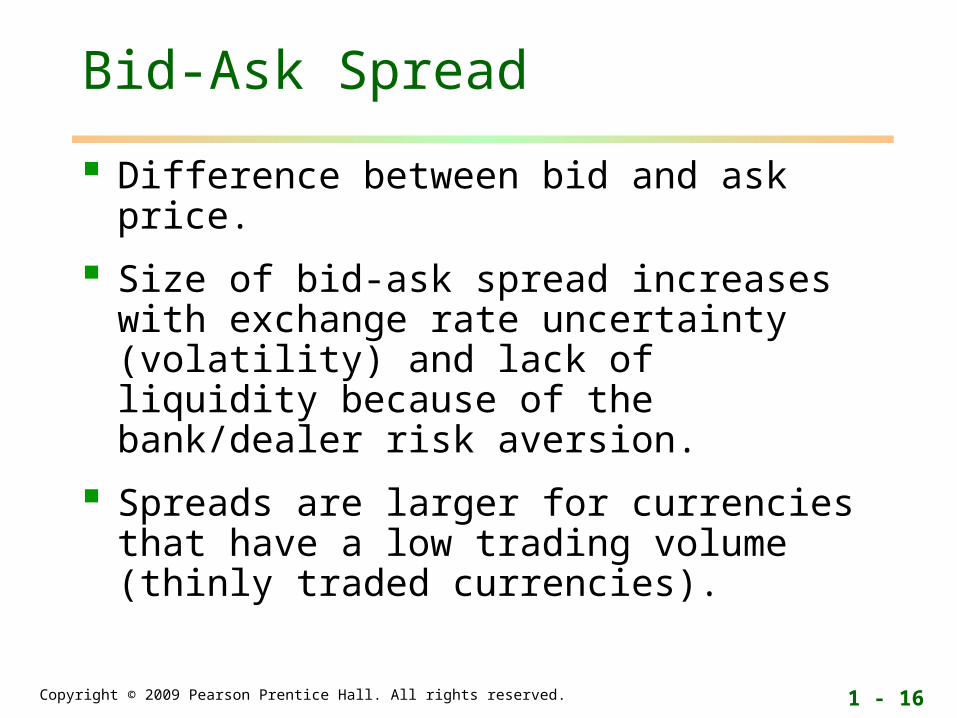

Bid-Ask Spread

Difference between bid and ask price.

Size of bid-ask spread increases with exchange rate uncertainty (volatility) and lack of liquidity because of the bank/dealer risk aversion.

Spreads are larger for currencies that have a low trading volume (thinly traded currencies).

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 17

Two Principles for bid and ask rates

The a:b ask exchange rate is the reciprocal of the b:a bid exchange rate.

The a:b bid exchange rate is the reciprocal of the b:a ask exchange rate.

Example:

the €:$ quote of €:$ = 1.2011 – 1.2014 is equivalent to a $:€ quote of:

$:€ = 0.83236 – 0.83257

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 18

Arbitrage

Arbitrage involves the simultaneous purchase of an undervalued asset or portfolio and sale of an overvalued but equivalent asset or portfolio, in order to obtain a risk free profit on the price differential.

An arbitrage could be created if it were profitable to buy from one bank and sell to another bank.

When describing arbitrage, we are usually discussing a riskless transaction that does not require any invested capital.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 19

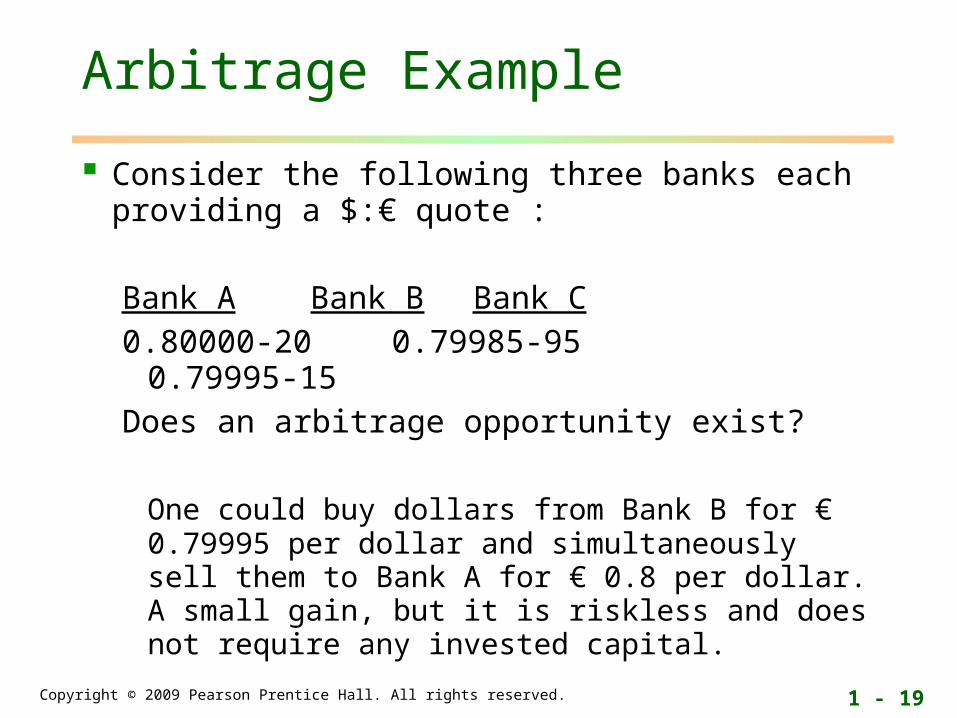

Arbitrage Example

Consider the following three banks each providing a $:€ quote :

Bank A Bank B Bank C

0.80000-20 0.79985-95 0.79995-15

Does an arbitrage opportunity exist?

One could buy dollars from Bank B for € 0.79995 per dollar and simultaneously sell them to Bank A for € 0.8 per dollar. A small gain, but it is riskless and does not require any invested capital.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 20

Triangular Arbitrage

Example 1.4

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 21

Forward Rates

Spot rates are quoted for immediate currency transactions (although in practice delivery takes place 48 hours later).

Forward exchange rates are contracted today but with delivery and settlement in the future.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 22

Forward Premiums/Discounts

Forward exchange rates are often quoted as a premium, or discount, to the spot exchange rate.

Given an exchange rate of a:b, the annualized forward premium on the quoted currency a equals:

%100.

12

forwardmonthsNorateSpot

rateSpotrateForward

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 23

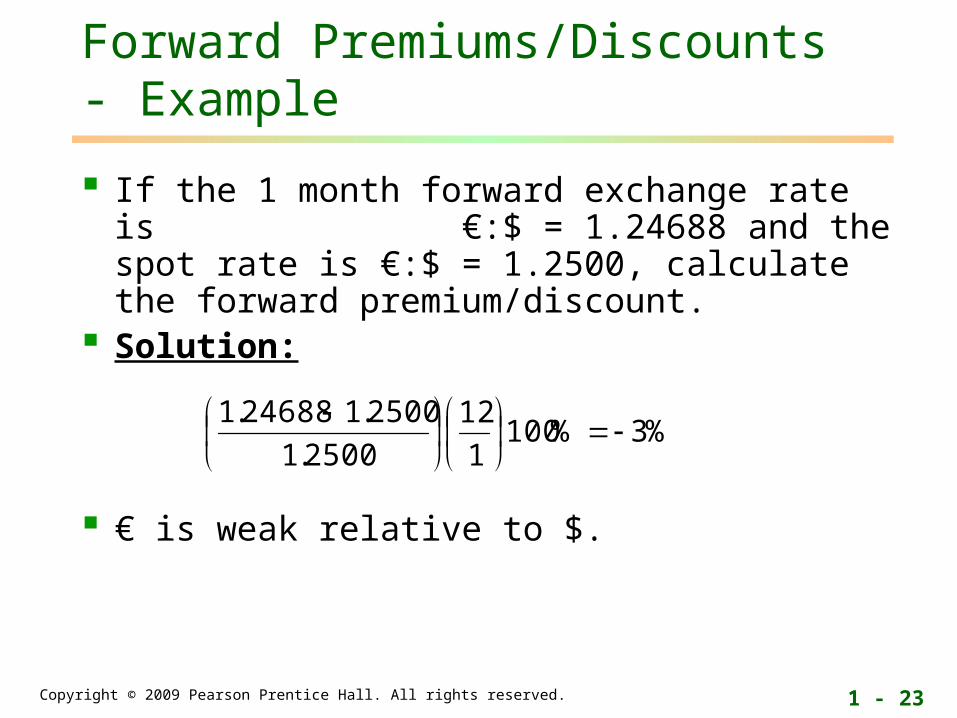

Forward Premiums/Discounts - Example

If the 1 month forward exchange rate is €:$ = 1.24688 and the spot rate is €:$ = 1.2500, calculate the forward premium/discount.

Solution:

€ is weak relative to $.

%3%1001

12

2500.1

2500.124688.1

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 24

Interest Rate Parity

For two currencies, A and B, with the exchange rate quoted as the number of units of B for one unit of A,

A

BA

r

rr

rateSpot

rateSpotrateForward

1

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1 - 25

Interest Rate Parity Example

Example p16~p17 Example 1.5 Example 1.6