30

Copyright 2014 by Diane S. Docking 1 Interest Rate Risk Management: ISGAP

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | parker-longstaff |

| View: | 214 times |

| Download: | 0 times |

Copyright 2014 by Diane S. Docking 1

Interest Rate Risk Management:ISGAP

Learning Objectives

Define the repricing gap measure of interest rate risk.

Understand the process of ISGAP management

Copyright 2014 by Diane S. Docking 2

Copyright 2014 by Diane S. Docking 3

Managing Interest Rate Risk

Changes in interest rates: cause variability in net interest income (NII)

and net interest margin (NIM) impact value of financial assets, liabilities,

and reinvestment returns cause repricing of loans, securities, and

deposits impacting NII

Copyright 2014 by Diane S. Docking 4

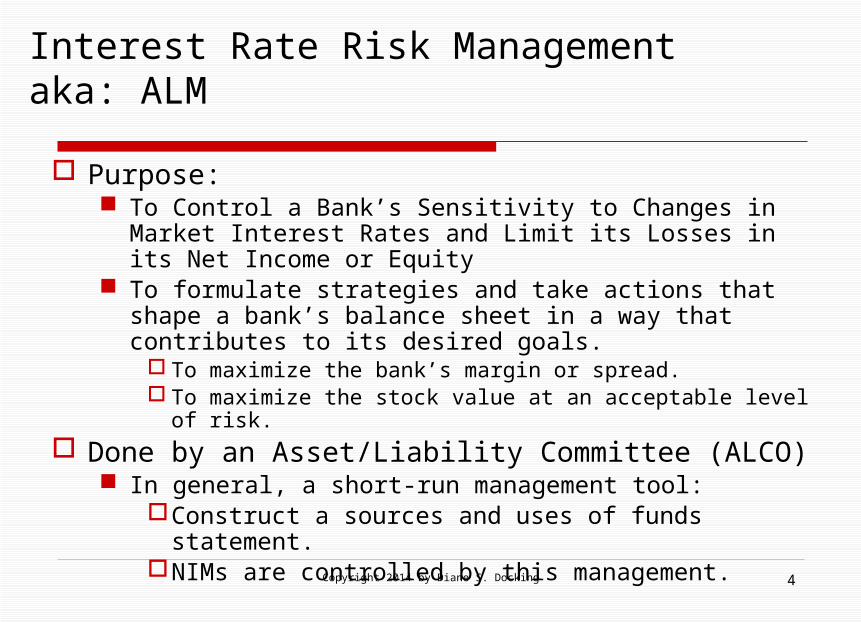

Interest Rate Risk Managementaka: ALM

Purpose: To Control a Bank’s Sensitivity to Changes in Market

Interest Rates and Limit its Losses in its Net Income or Equity

To formulate strategies and take actions that shape a bank’s balance sheet in a way that contributes to its desired goals.

To maximize the bank’s margin or spread. To maximize the stock value at an acceptable level of risk.

Done by an Asset/Liability Committee (ALCO) In general, a short-run management tool:

Construct a sources and uses of funds statement.NIMs are controlled by this management.

Copyright 2014 by Diane S. Docking 5

Assets Earning Total NIM

NII

Defn: Net Interest Margin & Net Interest Income

or

where:

* Or Total Average Assets

expenseinterestincomeinterestNII

*Assets Total NIM

NII

Copyright 2014 by Diane S. Docking 6

Defn: Interest-Sensitive Assets (ISA or RSA*)

Interest rate is subject to change/repricing within a year: Short-Term Securities and Loans Variable-Rate Securities and Loans Current portion of Fixed-Rate Securities

and Loans to be received

*Interest or Rate sensitive

Copyright 2014 by Diane S. Docking 7

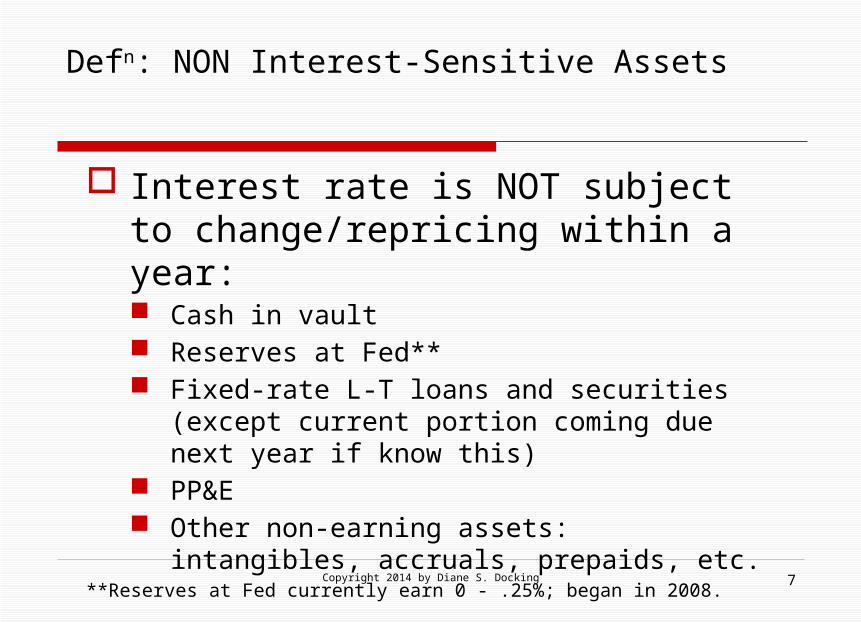

Defn: NON Interest-Sensitive Assets

Interest rate is NOT subject to change/repricing within a year: Cash in vault Reserves at Fed** Fixed-rate L-T loans and securities (except

current portion coming due next year if know this)

PP&E Other non-earning assets: intangibles,

accruals, prepaids, etc.**Reserves at Fed currently earn 0 - .25%; began in 2008.

Copyright 2014 by Diane S. Docking 8

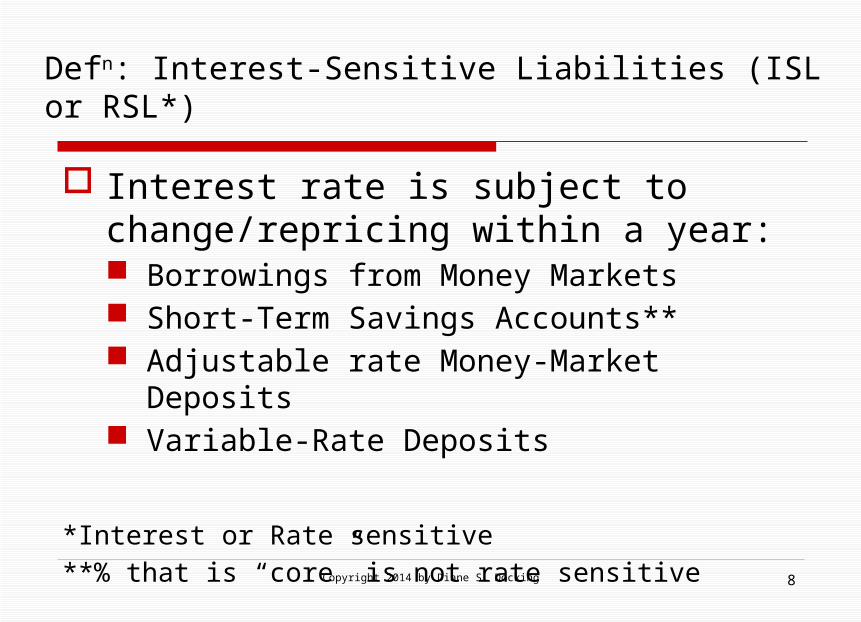

Defn: Interest-Sensitive Liabilities (ISL or RSL*)

Interest rate is subject to change/repricing within a year: Borrowings from Money Markets Short-Term Savings Accounts** Adjustable rate Money-Market Deposits Variable-Rate Deposits

*Interest or Rate sensitive**% that is “core” is not rate sensitive

Copyright 2014 by Diane S. Docking 9

Defn: NON Interest-Sensitive Liabilities

Interest rate is NOT subject to change/repricing within a year: DDA paying no interest Deposits where interest rates cannot be

adjusted within a year Fixed-rate Long-term savings, CD’s IRAs Fixed-rate Long-term debt

Copyright 2014 by Diane S. Docking 10

ISGAP

GAP = ISA - ISL Positive GAP where ISA > ISL Negative GAP where ISL > ISA

Portfolio Maturity Mismatch

11Copyright 2014 by Diane S. Docking

Copyright 2014 by Diane S. Docking 12

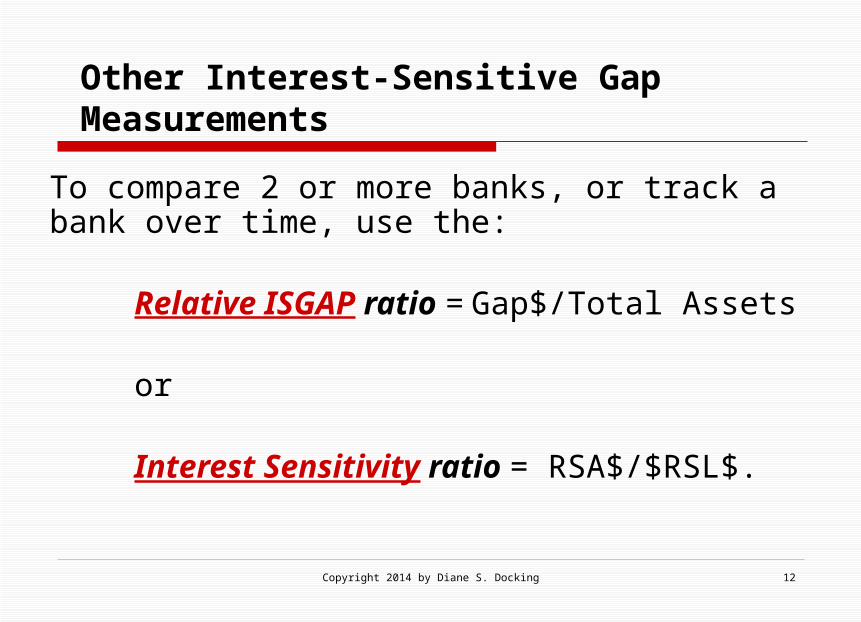

To compare 2 or more banks, or track a bank over time, use the:

Relative ISGAP ratio = Gap$/Total Assets

or

Interest Sensitivity ratio = RSA$/$RSL$.

Other Interest-Sensitive Gap Measurements

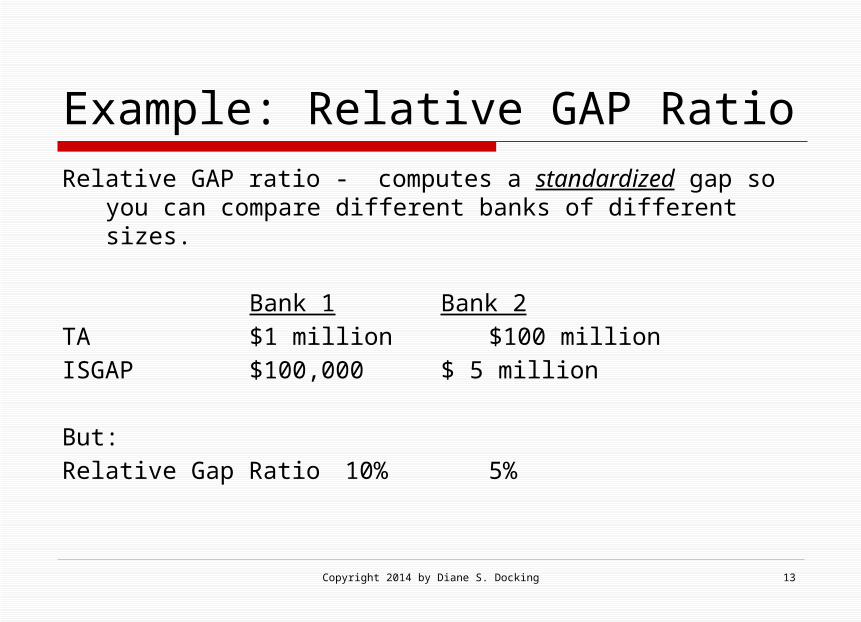

Example: Relative GAP RatioRelative GAP ratio - computes a standardized gap so you

can compare different banks of different sizes.

Bank 1 Bank 2TA $1 million $100

millionISGAP $100,000 $ 5

million

But:Relative Gap Ratio 10% 5%

Copyright 2014 by Diane S. Docking 13

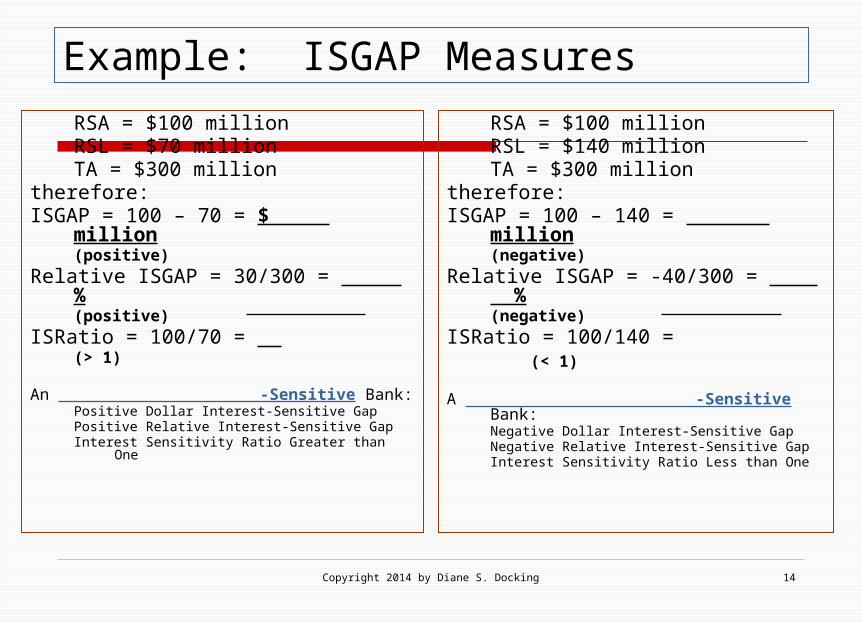

Example: ISGAP Measures

RSA = $100 millionRSL = $70 millionTA = $300 million

therefore:ISGAP = 100 – 70 = $ million

(positive)Relative ISGAP = 30/300 = %

(positive)ISRatio = 100/70 =

(> 1)

An -Sensitive Bank:Positive Dollar Interest-Sensitive GapPositive Relative Interest-Sensitive GapInterest Sensitivity Ratio Greater than One

RSA = $100 millionRSL = $140 millionTA = $300 million

therefore:ISGAP = 100 – 140 = million

(negative)Relative ISGAP = -40/300 = %

(negative)ISRatio = 100/140 = (< 1)

A -Sensitive Bank:Negative Dollar Interest-Sensitive GapNegative Relative Interest-Sensitive GapInterest Sensitivity Ratio Less than One

14Copyright 2014 by Diane S. Docking

Copyright 2014 by Diane S. Docking 15

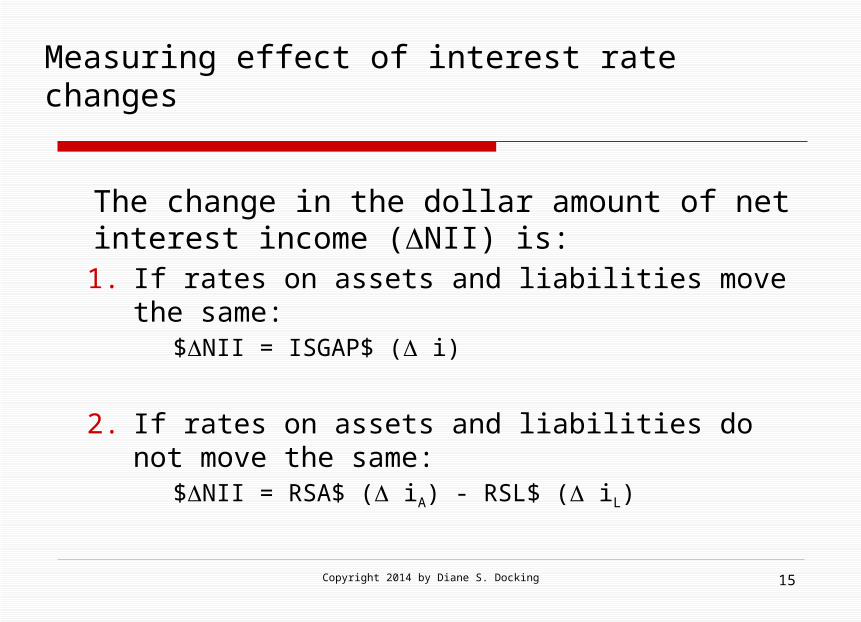

Measuring effect of interest rate changes

The change in the dollar amount of net interest income (NII) is:1. If rates on assets and liabilities move the same:

$NII = ISGAP$ ( i)

2. If rates on assets and liabilities do not move the same:

$NII = RSA$ ( iA) - RSL$ ( iL)

Copyright 2014 by Diane S. Docking 16

Relationship Between ISGAP and Changes in NII

ISGAP D i D NII

+ +

+ -

- +

- -

0 +

0 -

17Copyright 2014 by Diane S. Docking

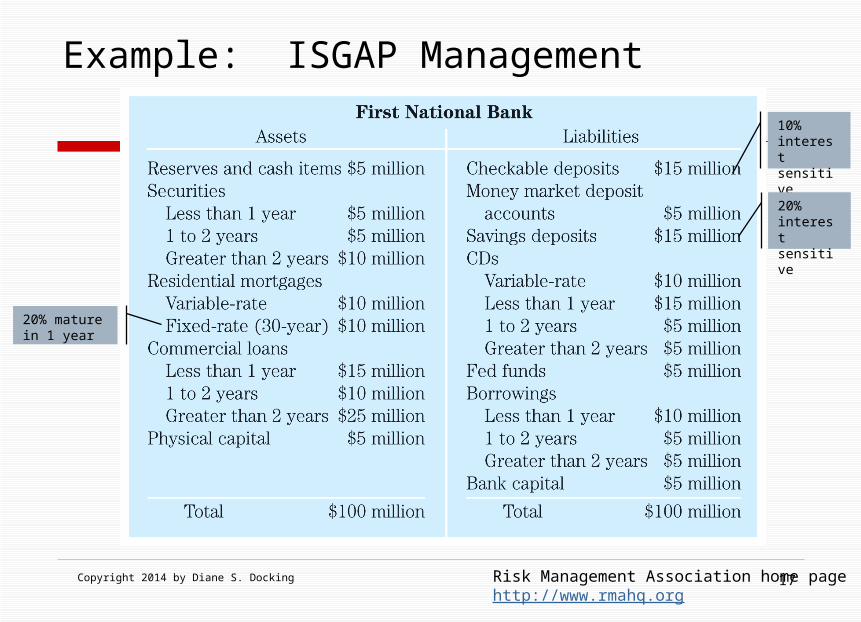

Example: ISGAP Management

Risk Management Association home pagehttp://www.rmahq.org

20% mature in 1 year

10% interest sensitive

20% interest sensitive

18Copyright 2014 by Diane S. Docking

Solution to Example: ISGAP Management

Rate-Sensitive Assets =

RSA = ___________

Rate-Sensitive Liabs =

RSL = __________

GAP = RSA RSL =

19Copyright 2014 by Diane S. Docking

Solution to Example: ISGAP Management

if i 5% Asset Income = +5% $32.0m = +$ 1.6mLiability Costs = +5% $49.5m = +$ 2.5m

∆ NII = $1.6m $ 2.5 = $0.9mOR

Since RSL > RSA, i results in: NIM , NII

∆ NII = GAP ∆i= $17.5m 5% = $0.9m

Copyright 2014 by Diane S. Docking20

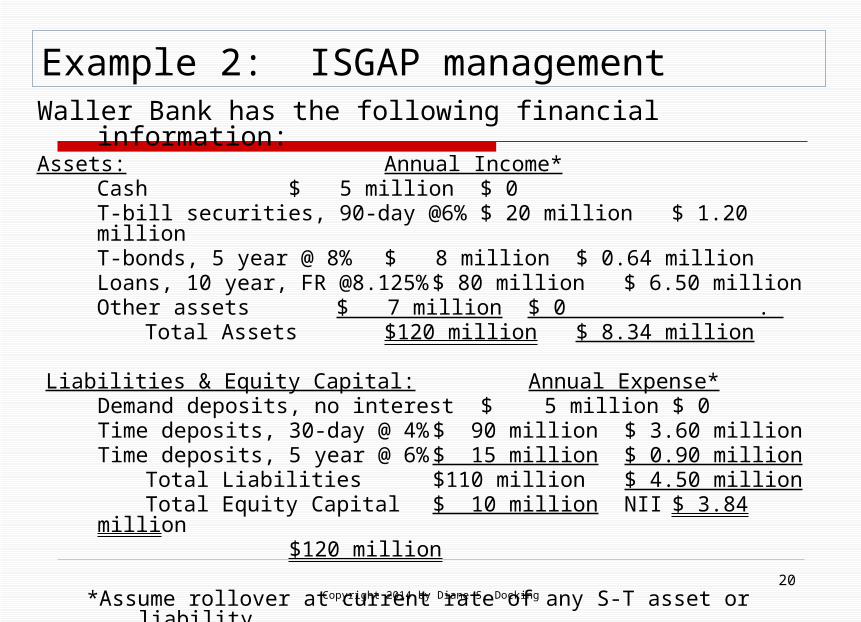

Example 2: ISGAP managementWaller Bank has the following financial information:Assets: Annual

Income*Cash $ 5 million $ 0T-bill securities, 90-day @6% $ 20 million $ 1.20 millionT-bonds, 5 year @ 8% $ 8 million $ 0.64 millionLoans, 10 year, FR @8.125% $ 80 million $ 6.50 millionOther assets $ 7 million $ 0 .

Total Assets $120 million $ 8.34 million

Liabilities & Equity Capital: Annual Expense*Demand deposits, no interest $ 5 million $ 0Time deposits, 30-day @ 4% $ 90 million $ 3.60 millionTime deposits, 5 year @ 6% $ 15 million $ 0.90 million

Total Liabilities $110 million $ 4.50 million

Total Equity Capital $ 10 million NII $ 3.84 million

$120 million

*Assume rollover at current rate of any S-T asset or liability.

Copyright 2014 by Diane S. Docking 21

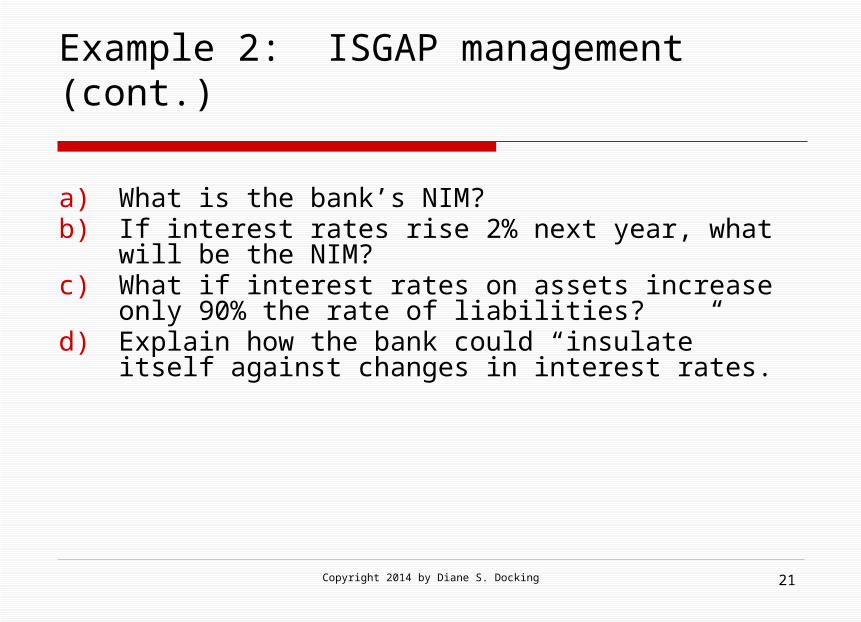

Example 2: ISGAP management (cont.)

a) What is the bank’s NIM?b) If interest rates rise 2% next year, what will be the

NIM?c) What if interest rates on assets increase only 90%

the rate of liabilities?d) Explain how the bank could “insulate” itself against

changes in interest rates.

Solution for Example 2: ISGAP management

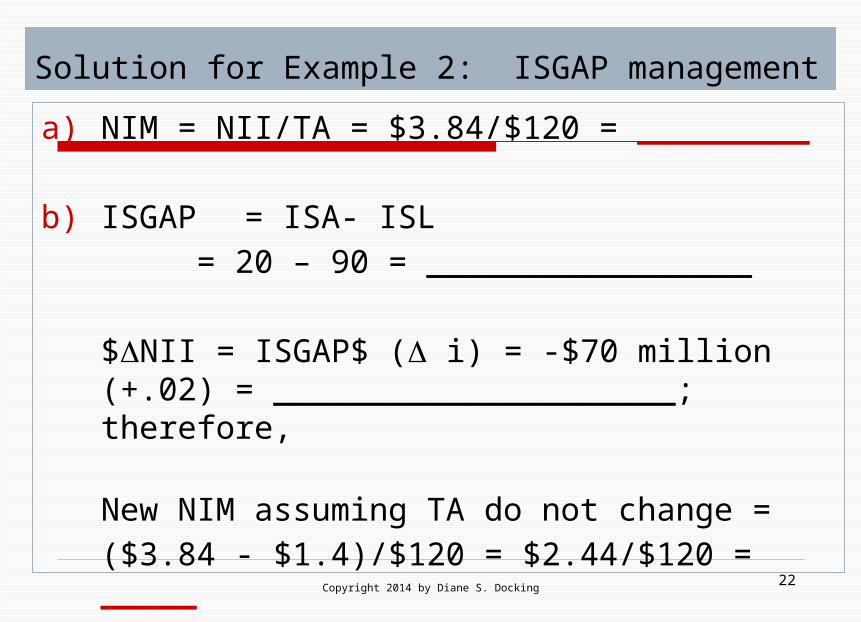

a) NIM = NII/TA = $3.84/$120 = _________

b) ISGAP= ISA- ISL= 20 – 90 = _________________

$NII = ISGAP$ ( i) = -$70 million (+.02) = _____________________; therefore,

New NIM assuming TA do not change = ($3.84 - $1.4)/$120 = $2.44/$120 = _____

22Copyright 2014 by Diane S. Docking

Solution for Example 2: ISGAP management (cont.)

c) If interest rates on assets increase only 1.8% then:$NII = RSA$ ( iA) - RSL$ ( iL)

= [$20 (.018)] – [$90 (+.02)] =.36 – 1.8 = _________________

New NIM assuming TA do not change = ($3.84 - $1.44)/$120 = $2.40/$120 = _____

23Copyright 2014 by Diane S. Docking

Solution for Example 2: ISGAP management (cont.)

d) Needs to increase ______and/or decrease ______ to bring ISGAP = 0.

HOW?

24Copyright 2014 by Diane S. Docking

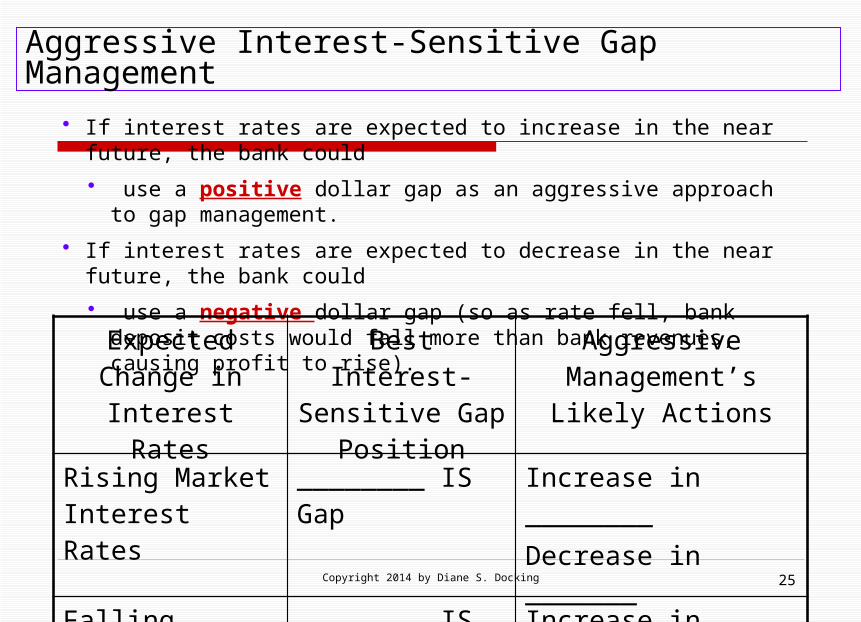

Aggressive Interest-Sensitive Gap Management

• If interest rates are expected to increase in the near future, the bank could

• use a positive dollar gap as an aggressive approach to gap management.

• If interest rates are expected to decrease in the near future, the bank could

• use a negative dollar gap (so as rate fell, bank deposit costs would fall more than bank revenues, causing profit to rise).Expected Change

in Interest RatesBest Interest-Sensitive Gap

Position

Aggressive Management’s Likely

Actions

Rising Market Interest Rates

________ IS Gap Increase in ________Decrease in _______

Falling Market Interest Rates

________ IS Gap Increase in ________Decrease in _______

25Copyright 2014 by Diane S. Docking

Copyright 2014 by Diane S. Docking 26

Measuring interest rate sensitivity and the dollar gap

Incremental gaps Measure the gaps for different maturity

buckets (e.g., 0-30 days, 30-90 days, 90-180 days, and 180-365 days).

Cumulative gaps Add up the incremental gaps from maturity

bucket to bucket. The total difference in dollars between those

bank assets and liabilities which can be repriced over a designated time period.

Computer-Based Techniques and Maturity Buckets

7-27

27Copyright 2014 by Diane S. Docking

Copyright 2014 by Diane S. Docking 28

Measuring interest rate sensitivity and the dollar gap

Defensive versus aggressive asset/liability management: Defensively guard against changes in NII

(e.g., near zero gap). Aggressively seek to increase NII in

conjunction with interest rate forecasts (e.g., positive or negative gaps).

Many times some gaps are driven by market demands (e.g., borrowers want long-term loans and depositors want short-term maturities.

Copyright 2014 by Diane S. Docking 29

Problems with Interest-Sensitive Gap Management

1. Time horizon problems related to when assets and liabilities are repriced. Dollar gap assumes they are all repriced on the same day, which is not true. For example, a bank could have a zero 30-day gap, but with

daily liabilities and 30-day assets NII would react to changes in interest rates over time.

A solution is to divide the assets and liabilities into maturity buckets (i.e., incremental gap).

Interest Rates Paid on Liabilities Tend to Move Faster than Interest Rates Earned on Assets

Interest Rate Attached to Bank Assets and Liabilities Do Not Move at the Same Speed as Market Interest Rates

Point at Which Some Assets and Liabilities Are Repriced is Not Easy to Identify

Copyright 2014 by Diane S. Docking 30

Problems with Interest-Sensitive Gap Management

2. Focus on net interest income rather than shareholder wealth.

Dollar gap may be set to increase NIM if interest rates increase, but equity values may decrease if the value of assets fall more than liabilities fall (i.e., the duration of assets is greater than the duration of liabilities).

Interest-Sensitive Gap Does Not Consider Impact of Changing Interest Rates on Equity Position

3. Financial derivatives could be used to hedge dollar gap effects on equity values.