37

Copyright © 2014 Pearson Education Chapter 11 Considering the Risk of Fraud

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | kelley-wilkinson |

| View: | 231 times |

| Download: | 23 times |

Copyright © 2014 Pearson Education

Chapter 11

Considering the Risk of Fraud

Chapter 11

Considering the Risk of Fraud

Copyright © 2014 Pearson Education11-2

Define fraud and distinguish between fraudulent financial reporting and misappropriation of assets.

Describe the fraud triangle and identify conditions for fraud.

Understand the auditor’s responsibility for assessing the risk of fraud and detecting material misstatements due to fraud.

Copyright © 2014 Pearson Education11-3

Identify corporate governance and other control environment factors that reduce fraud risks.

Develop responses to identified fraud risks.

Recognize specific fraud risk areas and develop procedures to detect fraud.

Understand interview techniques and other activities after fraud is suspected.

Copyright © 2014 Pearson Education

Define fraud and distinguishbetween fraudulent financial

reporting and misappropriation ofassets.

11-4

11

Copyright © 2014 Pearson Education11-5

Management Fraud

Fraudulent financial reporting

Misappropriation of assets

Copyright © 2014 Pearson Education

Describe the fraud triangle and identify conditions for fraud.

11-6

22

Copyright © 2014 Pearson Education11-7

Incentives/Pressures

Opportunities Attitudes/Rationalization

Copyright © 2014 Pearson Education11-8

Copyright © 2014 Pearson Education11-9

Incentives/Pressures:

Financial stability or profitability is threatened byeconomic, industry, or entity operating conditions

Excessive pressure exists for management tomeet debt requirements

Personal net worth is materially threatened

Copyright © 2014 Pearson Education11-10

Opportunities:

There are significant accounting estimates thatare difficult to verify

There is ineffective oversight over financialreporting

High turnover or ineffective accounting, internalaudit, or information technology staff exists

Copyright © 2014 Pearson Education11-11

Attitudes/Rationalization:

Inappropriate or inefficient communicationand support of the entity’s values is evident

A history of violations of laws is known

Management has a practice of makingoverly aggressive or unrealistic forecasts

Copyright © 2014 Pearson Education11-12

Incentives/Pressures:

Personal financial obligations create pressureto misappropriate assets

Adverse relationships between managementand employees motivate employees tomisappropriate assets

Copyright © 2014 Pearson Education11-13

Opportunities:

There is a presence of large amounts of cashon hand or inventory items

There is an inadequate internal control overassets

Copyright © 2014 Pearson Education11-14

Attitudes/Rationalization:

Disregard for the need to monitor or reducerisk of misappropriating assets exists

There is a disregard for internal controls

Copyright © 2014 Pearson Education

Understand the auditor’s responsibility for assessing the risk of fraud and detecting

material misstatements due to fraud.

11-15

33

Copyright © 2014 Pearson Education11-16

Auditing standards provide guidance to Auditors in assessing the risk of fraud.

Auditing standards state that, in exercising Professional skepticism, an auditor “neither assumes that management is dishonest nor assumes unquestioned honesty.”

Copyright © 2014 Pearson Education11-17

Copyright © 2014 Pearson Education11-18

Discussion among engagement team Procedures performed to assess risk Specific risks and audit response Reasons supporting conclusions Results of procedures performed Other conditions and analytical relationships Nature of communications

Copyright © 2014 Pearson Education

Identify corporate governance and other control environment factors

that reduce fraud risks.

11-19

44

Copyright © 2014 Pearson Education11-20

1. Culture of honesty and high ethics

2. Management's responsibilityto evaluate risks of fraud

3. Audit committee oversight

Copyright © 2014 Pearson Education11-21

Organizational code of conduct

General employee conduct

Conflicts of interest

Outside activities, employment, and directorships

Copyright © 2014 Pearson Education11-22

Relationships with clients and suppliers

Gifts, entertainment, and favors

Kickbacks and secret commissions

Organization funds and other assets

Copyright © 2014 Pearson Education11-23

Organization records and communications

Dealing with outside people and organizations

Prompt communications

Privacy and confidentiality

Copyright © 2014 Pearson Education11-24

Copyright © 2014 Pearson Education

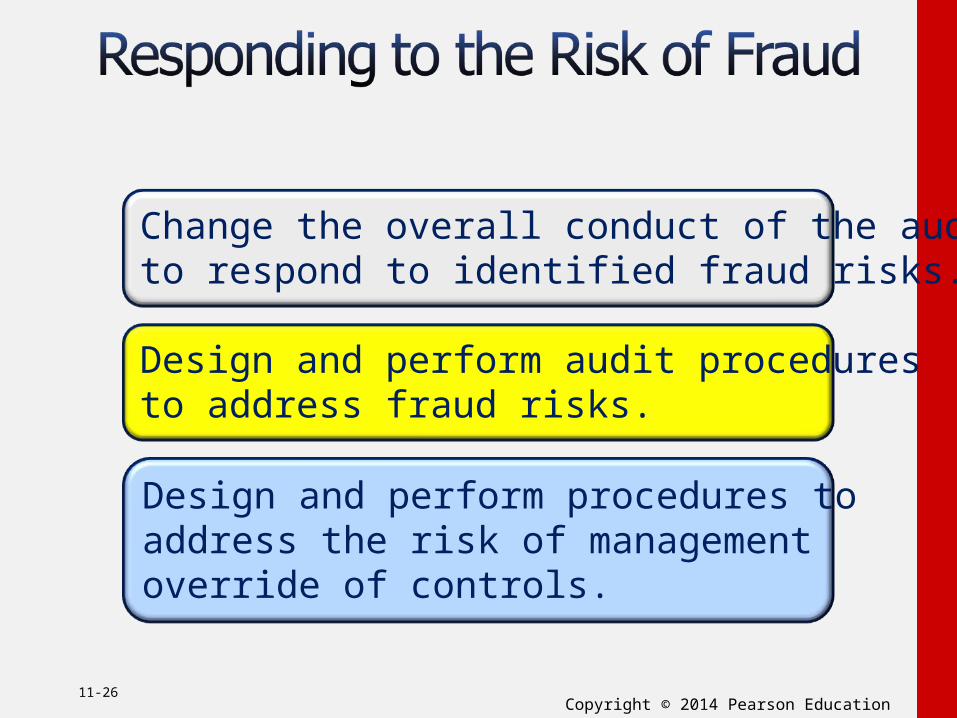

Develop responses to identified fraud risks.

11-25

55

Copyright © 2014 Pearson Education11-26

Change the overall conduct of the auditto respond to identified fraud risks.

Design and perform audit proceduresto address fraud risks.

Design and perform procedures toaddress the risk of managementoverride of controls.

Copyright © 2014 Pearson Education

Recognize specific fraud risk areas and develop procedures to detect fraud.

11-27

66

Copyright © 2014 Pearson Education11-28

Revenue and accounts receivable fraud risks

Inventory fraud risks

Purchases and accounts payable fraud risks

Other areas of fraud risk

Copyright © 2014 Pearson Education11-29

Copyright © 2014 Pearson Education11-30

Copyright © 2014 Pearson Education11-31

77

Copyright © 2014 Pearson Education11-32

Copyright © 2014 Pearson Education11-33

Informational

Assessment

Interrogative

Evaluating responses

Observing behavioral cues

Listening

Copyright © 2014 Pearson Education11-34

Copyright © 2014 Pearson Education11-35

Copyright © 2014 Pearson Education11-36

Copyright © 2014 Pearson Education11-37

Copyright

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Printed in the United States of America.