40

1 Copyright K. Cuthbertson, D.Nitzsche Lecture The FOREX Market 11/9/2001

| Date post: | 21-Dec-2015 |

| Category: |

Documents |

| View: | 214 times |

| Download: | 1 times |

1Copyright K. Cuthbertson, D.Nitzsche

Lecture The FOREX Market

11/9/2001

2Copyright K. Cuthbertson, D.Nitzsche

Investments:Spot and Derivative Markets,

K.Cuthbertson and D.Nitzsche

CHAPTER 15:CHAPTER 15:

- excluding p. 454-457, p461-477, Section 15.7 and - excluding p. 454-457, p461-477, Section 15.7 and Appendix 15.1Appendix 15.1

CHAPTER 16:CHAPTER 16:

Sections 16.1 and 16.2 and Box 16.2 and 16.3 onlySections 16.1 and 16.2 and Box 16.2 and 16.3 only

Reading

3Copyright K. Cuthbertson, D.Nitzsche

Basics: Spot, Forward and Balance of Payments

PPP -Price Competitiveness

Fixed Exchange Rate Policy

Floating Exchange Rates

Uncovered Interest Parity/ Exchange Rate Overshooting

Currency Union -EMU: Policy Issues

Topics

4Copyright K. Cuthbertson, D.Nitzsche

Basics

5Copyright K. Cuthbertson, D.Nitzsche

Spot Rates: Terminolgy and SWIFT codes

‘SWIFT’ Codes ‘TELEPHONE’

Sterling - $ GBP/USD Cable

French Franc-$ FRF/USD Paris

Deutsche Mark-$ DEM/USD Dollar-mark

Swiss Franc-$ CHF/USD Swissy

Yen-$ JPY/USD Bill and Ben

Note: e.g. Dollar - Sterling

If sterling appreciates then the USD must have depreciated

e.g. Appreciation of sterling from 2.0 $ per £ to 2.1 $ per £

6Copyright K. Cuthbertson, D.Nitzsche

Spot FX-market

Banks in London

- (“screens” \ telephone \ back office )

- Spot settled in 2 business days

300 participants (50 large banks-”own book”)

Also 10-12 FOREX brokers

Dealing spreads, commission, trading profits

International Commodities Clearing House (ICCH) - transfer of funds

7Copyright K. Cuthbertson, D.Nitzsche

Forward Market

Contract made today for delivery in the future

Forward rate is “price” agreed, today

eg. One -year Forward rate = 1.5 $ / £

Agree to purchase £100 ‘s forward

In 1-year, receive £100

and pay-out $150

8Copyright K. Cuthbertson, D.Nitzsche

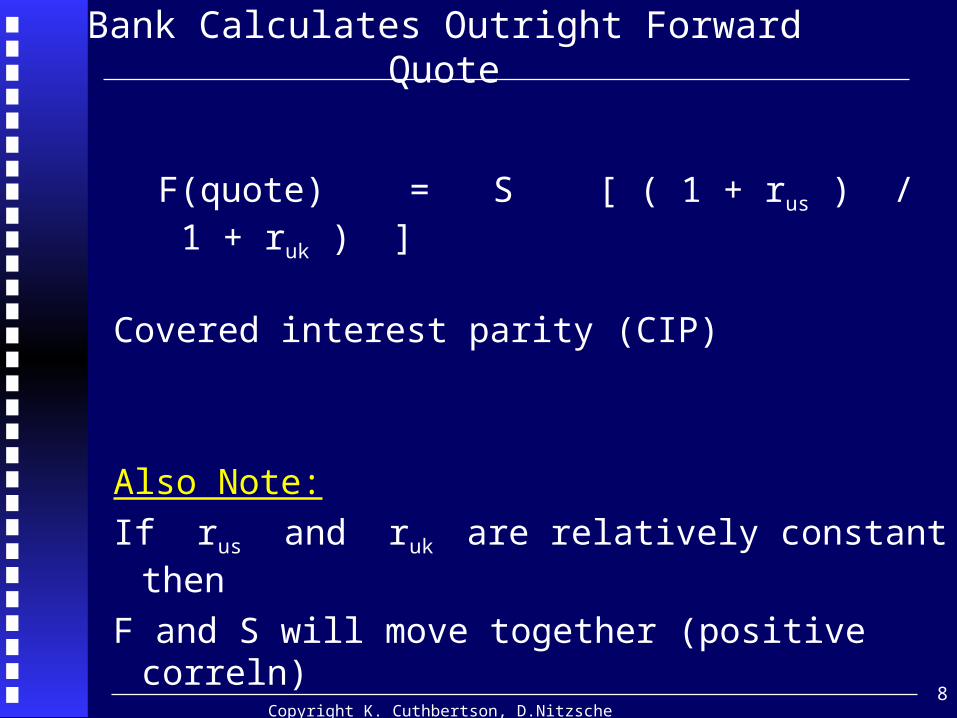

Bank Calculates Outright Forward Quote

F(quote) = S [ ( 1 + rus ) / ( 1 + ruk ) ]

Covered interest parity (CIP)

Also Note:

If rus and ruk are relatively constant then

F and S will move together (positive correln)

9Copyright K. Cuthbertson, D.Nitzsche

Exchange Rate Regimes

Fixed Exchange Rates (Crawling Peg)

-in practice, these are ‘narrow bands’

Pure Float (eg. USD-Yen, USD-Euro)

- sometimes Central Bank intervention

Common Currency (EMU), Mexico-USA?

Currency Board-

- form of fixed exchange rate where domestic currency is altered one-for-one with FX-reserves - ie. net FX receipts (Hong-Kong, Latvia, Agentina)

10Copyright K. Cuthbertson, D.Nitzsche

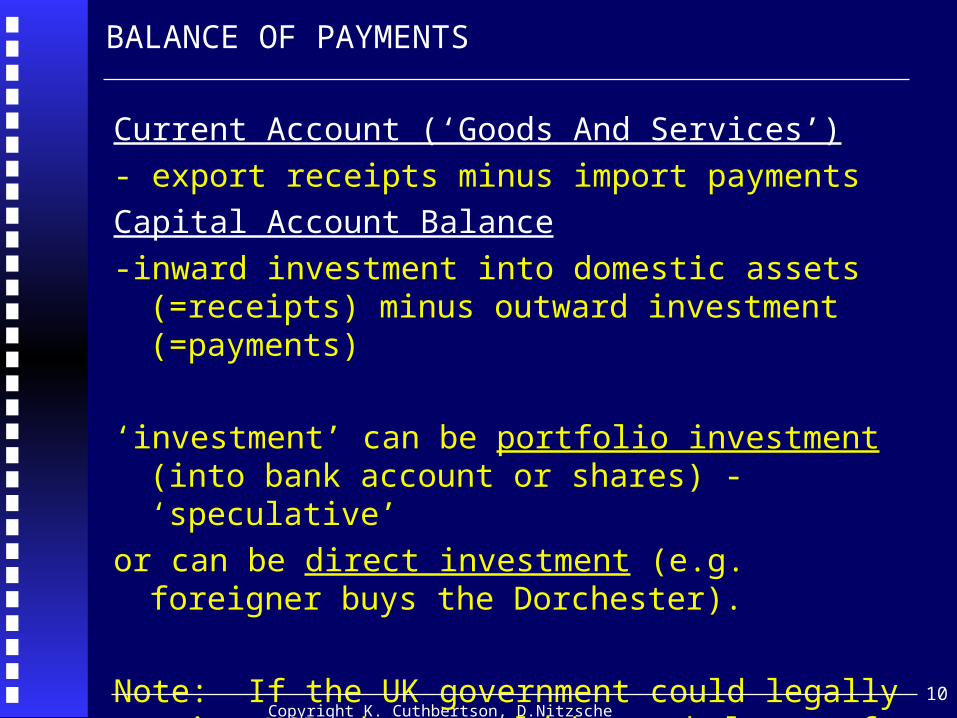

BALANCE OF PAYMENTS

Current Account (‘Goods And Services’)

- export receipts minus import payments

Capital Account Balance

-inward investment into domestic assets (=receipts) minus outward investment (=payments)

‘investment’ can be portfolio investment (into bank account or shares) - ‘speculative’

or can be direct investment (e.g. foreigner buys the Dorchester).

Note: If the UK government could legally print USD there would be no balance of payments problem

11Copyright K. Cuthbertson, D.Nitzsche

Purchasing Power Parity PPP

and

Price Competitiveness

12Copyright K. Cuthbertson, D.Nitzsche

PPP: “Law of One Price”

Let: HH= Harrod’s Hamper

SH= Sak’s Hamper

Suppose:

$P(SH) = $200 £P(HH) = £100 S = 2 $ per £

Then to a UK resident the price of SH in sterling is same as HH

UK is ‘price competitive’ and there is no incentive to switch purchases of goods between countries

This ‘special situation’ is know as purchasing power parity PPP

13Copyright K. Cuthbertson, D.Nitzsche

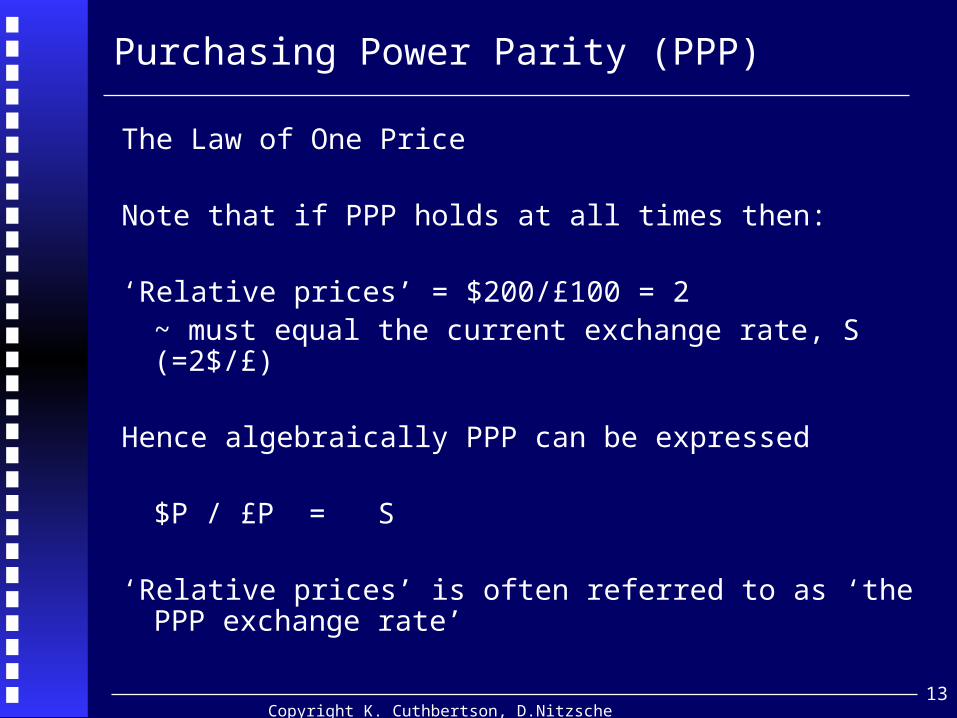

Purchasing Power Parity (PPP)

The Law of One Price

Note that if PPP holds at all times then:

‘Relative prices’ = $200/£100 = 2 ~ must equal the current exchange rate, S (=2$/£)

Hence algebraically PPP can be expressed

$P / £P = S ‘Relative prices’ is often referred to as ‘the PPP

exchange rate’

14Copyright K. Cuthbertson, D.Nitzsche

Actual S ($/£)= ______ and Relative Prices(Relative prices = ‘PPP-Exchange Rate’= ----- )

* Exchange Rates (Dollars per Pound)

100

150

200

250

300

Years

15Copyright K. Cuthbertson, D.Nitzsche

Figure 16.3: German Mark - Pound Sterling

(Actual and PPP Exchange Rate)

1.8

2

2.2

2.4

2.6

2.8

3

3.2

S (

DM

s p

er

Po

un

d S

terl

ing

)

actual exch. ratePPP exch. rate

16Copyright K. Cuthbertson, D.Nitzsche

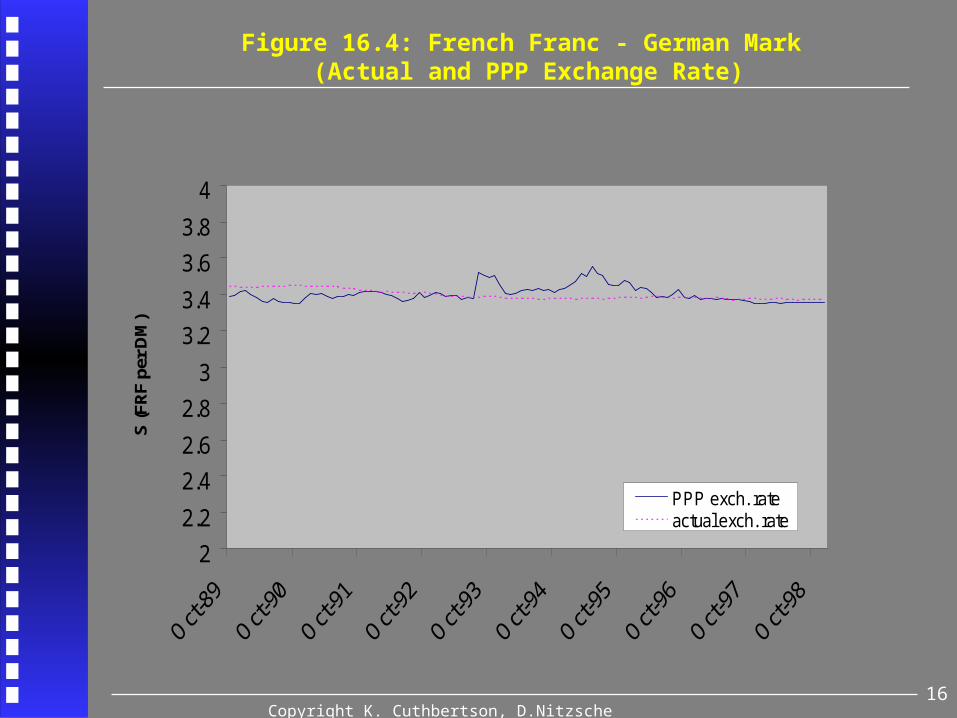

Figure 16.4: French Franc - German Mark (Actual and PPP Exchange Rate)

2

2.2

2.4

2.6

2.8

3

3.2

3.4

3.6

3.8

4

S (F

RF

per

DM

)

PPP exch. rateactual exch. rate

17Copyright K. Cuthbertson, D.Nitzsche

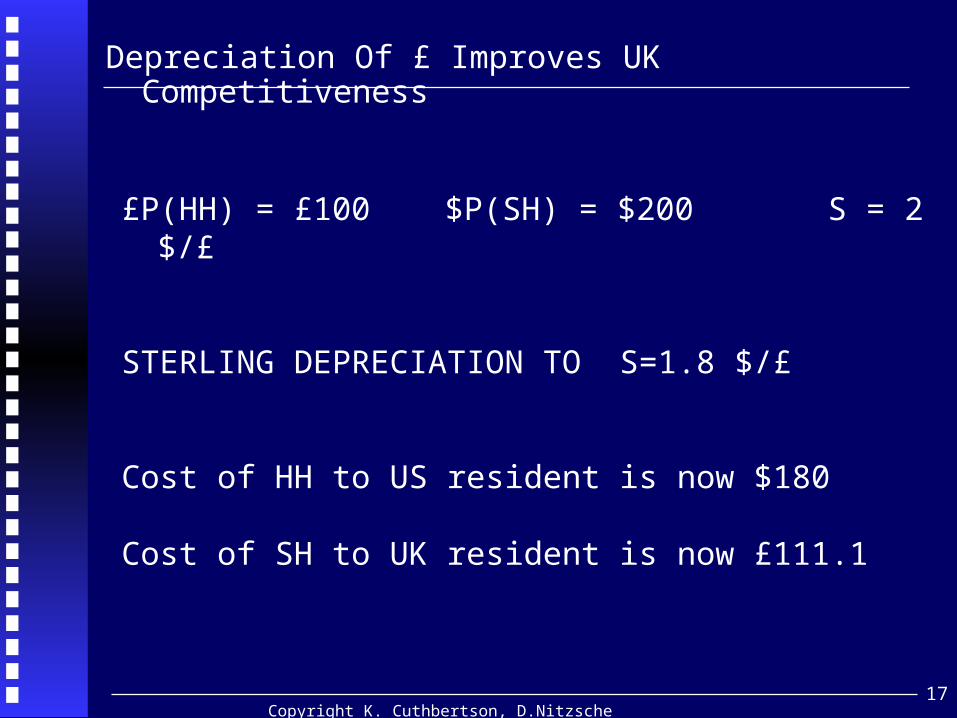

Depreciation Of £ Improves UK Competitiveness

£P(HH) = £100 $P(SH) = $200 S = 2 $/£

STERLING DEPRECIATION TO S=1.8 $/£

Cost of HH to US resident is now $180

Cost of SH to UK resident is now £111.1

18Copyright K. Cuthbertson, D.Nitzsche

Fixed Exchange Rates

19Copyright K. Cuthbertson, D.Nitzsche

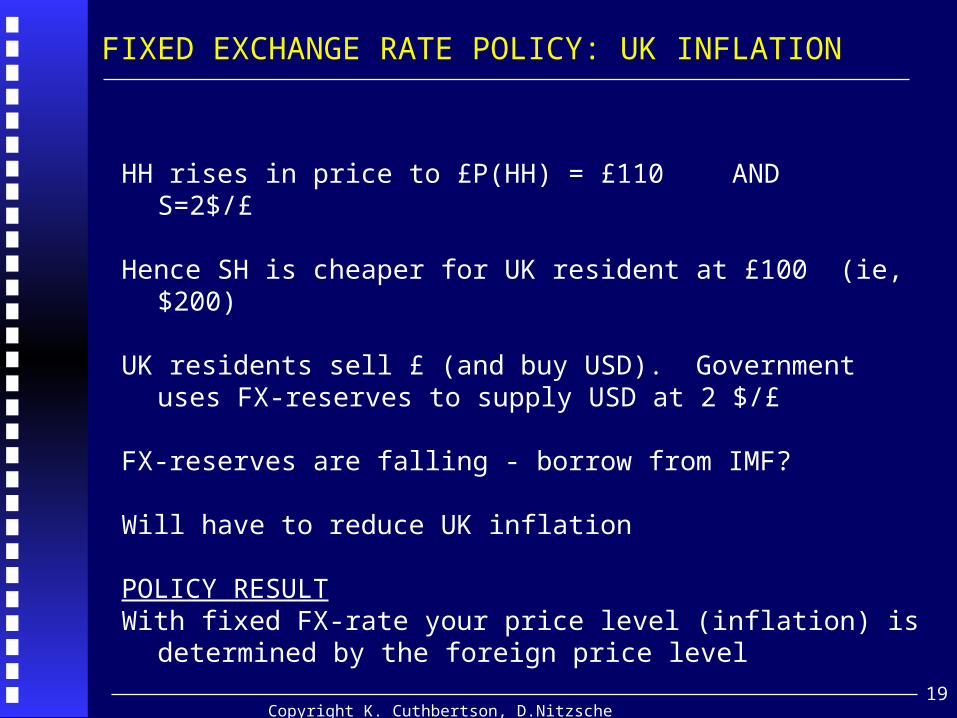

FIXED EXCHANGE RATE POLICY: UK INFLATION

HH rises in price to £P(HH) = £110 AND S=2$/£

Hence SH is cheaper for UK resident at £100 (ie, $200)

UK residents sell £ (and buy USD). Government uses FX-reserves to supply USD at 2 $/£

FX-reserves are falling - borrow from IMF?

Will have to reduce UK inflation

POLICY RESULTWith fixed FX-rate your price level (inflation) is determined by the

foreign price level

20Copyright K. Cuthbertson, D.Nitzsche

FIXED EXCHANGE RATE POLICY: UK INFLATION

CONTROLS ON CAPITAL ACCOUNT

To reduce UK inflation you can raise interest rates (tight monetary policy)

‘FREE’ CAPITAL FLOWS

If you raise UK interest rates, have massive capital inflow (if fixed rate is credible policy) which will put upward pressure on sterling.

Hence cannot have an independent interest rate policy - reducing inflation will need fiscal policy.

21Copyright K. Cuthbertson, D.Nitzsche

FIXED EXCHANGE RATE POLICY

Bretton Woods 1945-1973

USD as “anchor currency”

IMF - payments imbalances/devaluations

Gold at $35 per oz. (Fort Knox).

USD = world’s trading currency(Seigniorage)

Oil Crisis 1973 and 1979Inflation rates differ = “strain”

22Copyright K. Cuthbertson, D.Nitzsche

FIXED EXCHANGE RATES : SUMMARY

Reduces price uncertainty for exporters/importers

You have to accept the inflation rate of the ‘larger’ country. Cannot have an independently chosen inflation rate.

If you have higher ‘core’ inflation than larger country you will have to have contractionary fiscal policy (and unemployment)

With ‘free’ capital flows your interest rate must equal that of the large country

May need to borrow foreign exchange - if you then devalue this is costly !

23Copyright K. Cuthbertson, D.Nitzsche

Floating Exchange Rates

24Copyright K. Cuthbertson, D.Nitzsche

FLOATING EXCHANGE RATES : UK INFLATION

£P= £110 and S currently at $2 per £

SH is cheaper than HH and demand for USD increases and USD appreciates (and sterling depreciates)

Depreciation of £ implies an improvement in UK competitiveness to offset the higher £-price of HH

Policy Result (ignoring capital account)High inflation countries have a depreciating exchange

rate (which offsets some or all of loss of competitiveness due to high inflation)`

25Copyright K. Cuthbertson, D.Nitzsche

FLOATING EXCHANGE RATES : UK INFLATION

If S falls to exactly 1.818181 $/£ the SH would also cost £110 for a UK resident and price competitiveness is restored

BUT NOTETo exactly restore price competitiveness requires the specific

exchange rate of 1.8181 and decisions by ‘rational’ FX-speculators might not result in this exact rate - see overshooting below

ALSO NOTE

You can raise your interest rate to try and reduce inflation. Any capital inflow will tend to raise sterling FX rate which will put downward pressure on UK inflation (as export sector becomes less competitive)

26Copyright K. Cuthbertson, D.Nitzsche

FLOATING EXCHANGE RATES :SUMMARY

FX-rate is free to move (under market forces) and (ignoring capital flows) will tend to restore price competitiveness

You can have an independent interest rate policy and hence influence your own inflation rate over the longer term (3-5 years) and your unemployment rate over the short term (1-3 years)

Your interest rate policy has implications for the exchange rate - although difficult to predict

Danger is that FX-speculators will cause ‘wild’ movements in FX-rate and adversely alter price competitivenesss

‘Price uncertainty’ removed by using the forward market

27Copyright K. Cuthbertson, D.Nitzsche

Uncovered Interest Parity and

Exchange Rate Overshooting

.

28Copyright K. Cuthbertson, D.Nitzsche

Uncovered Interest Arbitrage (Parity) (UIP)(‘Smart’ , ‘rational’ Speculators)

UIP is a specific (equilibrium) relationship between domestic and foreign interest rates and the expected depreciation of a currency whereby speculators have no incentive to switch their funds between different countries

We assume that speculators (as a whole) are only concerned about the expected return on their investments (ie. They are “risk neutral”). They know their ‘bets’ are risky but this does not influence their decision.

Note: Expected (or forecast of the )spot rate in 1 years time = “ESt+1”

29Copyright K. Cuthbertson, D.Nitzsche

Uncovered Interest Arbitrage (Parity) (UIP)

WHAT GIVES BEST EXPECTED PAYOUT (IN USD) FOR US RESIDENT

1) r(UK) = r(US) = 2%, and Current St = 1 $/£

‘Forecast, ESt+1 = 0.5 $ per £ (ie. expected depreciation of sterling)

US speculator: $100 of funds from US to UK or vice-versa?

2) r(UK) = 3%, r(US) = 2%, (ie. interest differential of 1%)

Current S = 1 $/£, Forecast, ESt+1 = 0.99029 $/£

I.e Expected depreciation of sterling of about 1%

30Copyright K. Cuthbertson, D.Nitzsche

Uncovered Interest Arbitrage (Parity) (UIP)Smart Speculators

UIP =. ‘no switching of funds by speculators’

This will occur when:

Expected (%) depreciation of sterling

= Interest differential in favour of the UK= (rUK-rUS)

If r(UK) = 3% p.a. r(US) = 2%, (ie. interest differential of 1%) then ‘no switching of funds’ when speculators think that sterling will depreciate by 1% over the coming year.

31Copyright K. Cuthbertson, D.Nitzsche

Uncovered Interest Arbitrage (Parity) (UIP)Smart Speculators

Assume UIP is correct then

If the UK already has ‘high’ interest rates this implies that speculators expect sterling to depreciate over the coming year

Note that the above says nothing about the current level of the exchange rate St. The current level of the exchange rate may (or may not) be ‘high’ , but all CIP implies is that whatever the value of St is now, speculators believe it will fall in the future.

32Copyright K. Cuthbertson, D.Nitzsche

POLICY IMPLICATIONS OF UIP:EXCHANGE RATE OVERSHOOTING

Start: UIP holds:

rUK = rUS = 10% Expected depn £ = 0% (ie you expect spot rate to remain constant over coming year)

What are the implications for the current spot rate of an unexpected rise in UK interest rates by 2% by the MPC?

If speculators initially believe that sterling will remain constant then US investors will want to buy UK bonds and hence they buy spot £ , pushing up the sterling Ex-Rate today.

33Copyright K. Cuthbertson, D.Nitzsche

POLICY IMPLICATIONS OF UIPEXCHANGE RATE OVERSHOOTING

How high will todays spot rate rise ?

Sterling will appreciate today until it gets so high that US investors think it will fall by 2% over the coming year.

Now UIP is restored and capital inflows into the UK will cease.

34Copyright K. Cuthbertson, D.Nitzsche

Using UIP: Exchange rate Overshooting Increase in UK interest rates = ‘Tight’ Monetary Policy

1.03

1.00

B

A

Expected depreciation of 2%

today Time

1.01C

Exchange Rate

Appreciation

of Sterling, $ per £

C = Final ‘long run’ level for Exchange Rate

+1 year

35Copyright K. Cuthbertson, D.Nitzsche

Overshooting: UIP+’STICKY’ PRICES

The appreciation of sterling and overshooting of the exchange rate leads to an immediate loss of UK competitiveness. Exports fall (and imports increase), which further exacerbates the recession initially caused by the rise in interest rates.

The recession may last for 2-5 years -severe problem.

It can also be exacerbated if “the herd” (e.g. chartists) follow the “rational speculators” and buy spot sterling when it begins to rise, thus pushing sterling up even further.

In the longer term the economy may return to its ‘normal’ growth path and interest rates in the two countries may be again be equalised (this is a “big”, involved and complex story)

36Copyright K. Cuthbertson, D.Nitzsche

Currency Unions - EMU

Policy Issues

.

37Copyright K. Cuthbertson, D.Nitzsche

CURRENCY UNION:“Single currency”:EMU

Like an irrevocable fixed exchange rate regime

No independent interest rate policy (ECB, Frankfurt)

Must accept the inflation rate of other member states (OR UNEMPLOYMENT IF HIGH INFLATION)

Prices are ‘transparent’ and ‘uncertainty’ removed - within Euroland only

Unelected MPC in Threadneedle St or in Frankfurt ?

38Copyright K. Cuthbertson, D.Nitzsche

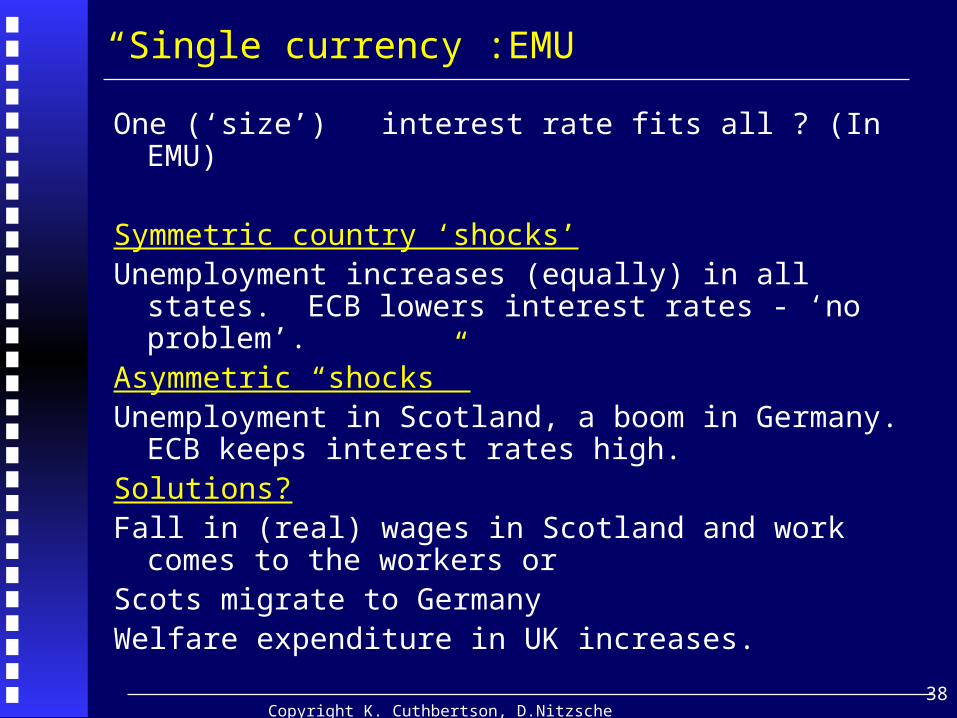

“Single currency”:EMU

One (‘size’) interest rate fits all ? (In EMU)

Symmetric country ‘shocks’Unemployment increases (equally) in all states. ECB

lowers interest rates - ‘no problem’.Asymmetric “shocks” Unemployment in Scotland, a boom in Germany. ECB

keeps interest rates high.Solutions?Fall in (real) wages in Scotland and work comes to the

workers orScots migrate to GermanyWelfare expenditure in UK increases.

39Copyright K. Cuthbertson, D.Nitzsche

“Single currency”:EMU

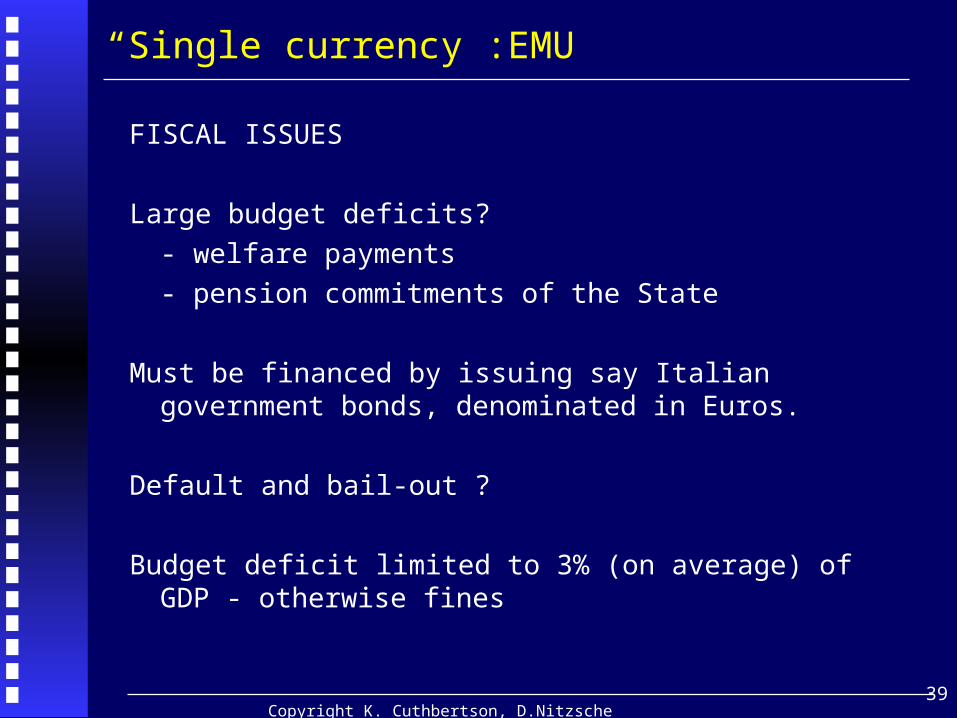

FISCAL ISSUES

Large budget deficits?

- welfare payments

- pension commitments of the State

Must be financed by issuing say Italian government bonds, denominated in Euros.

Default and bail-out ?

Budget deficit limited to 3% (on average) of GDP - otherwise fines

40Copyright K. Cuthbertson, D.Nitzsche

END OF LECTURE / SLIDES

.