31

| Date post: | 12-Apr-2018 |

| Category: |

Documents |

| Upload: | truonghanh |

| View: | 215 times |

| Download: | 1 times |

1H12 consolidated net income up 23% year-on-year; with core net income up 35%

Growth driven by key business units:

ALI: Earnings trajectory sustained with robust growth across all business segments

BPI: Solid growth of core banking business boosted by trading gains realized in 1Q12

MWC: Strong billed volume growth coupled with tariff increase and positive contribution from new businesses

Continued improvement in electronics and BPO businesses

2

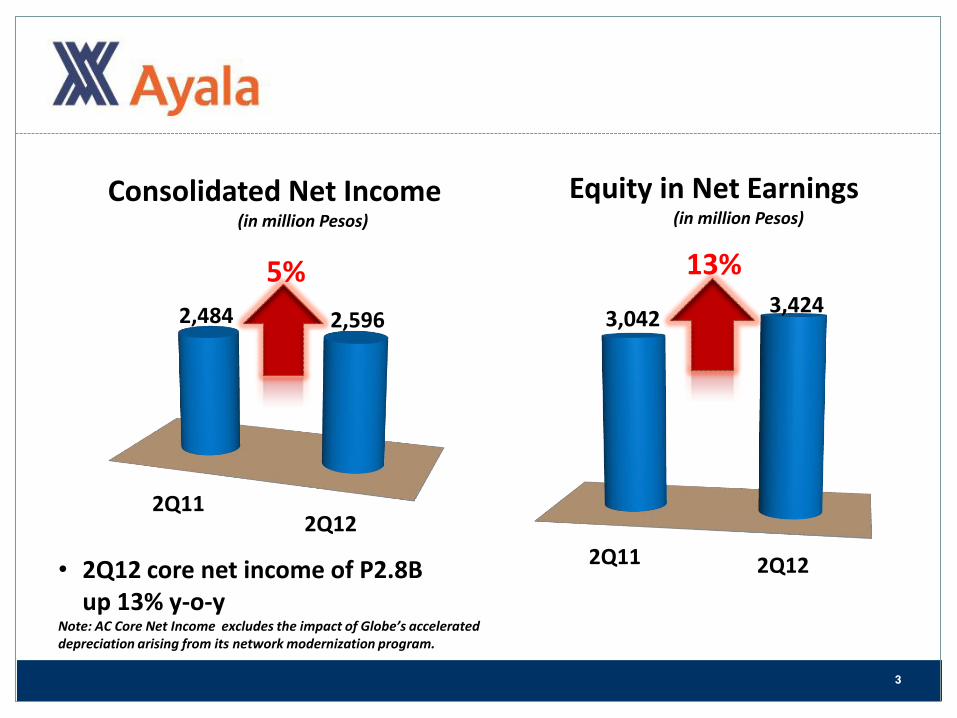

2Q11 2Q12

3,042 3,424

2Q11 2Q12

2,484 2,596

Consolidated Net Income (in million Pesos)

Equity in Net Earnings (in million Pesos)

13%

• 2Q12 core net income of P2.8B up 13% y-o-y Note: AC Core Net Income excludes the impact of Globe’s accelerated depreciation arising from its network modernization program.

5%

3

1H11 1H12

6,173 7,665

1H11 1H12

4,935 6,079

23%

Consolidated Net Income (in million Pesos)

Equity in Net Earnings (in million Pesos)

24%

• 1H12 core net income of P6.3B up 35% Note: 1H12 core net income excludes the impact of Globe’s accelerated depreciation arising from its network modernization program and excludes AG Holdings revaluation gains recognized in 1H11.

4

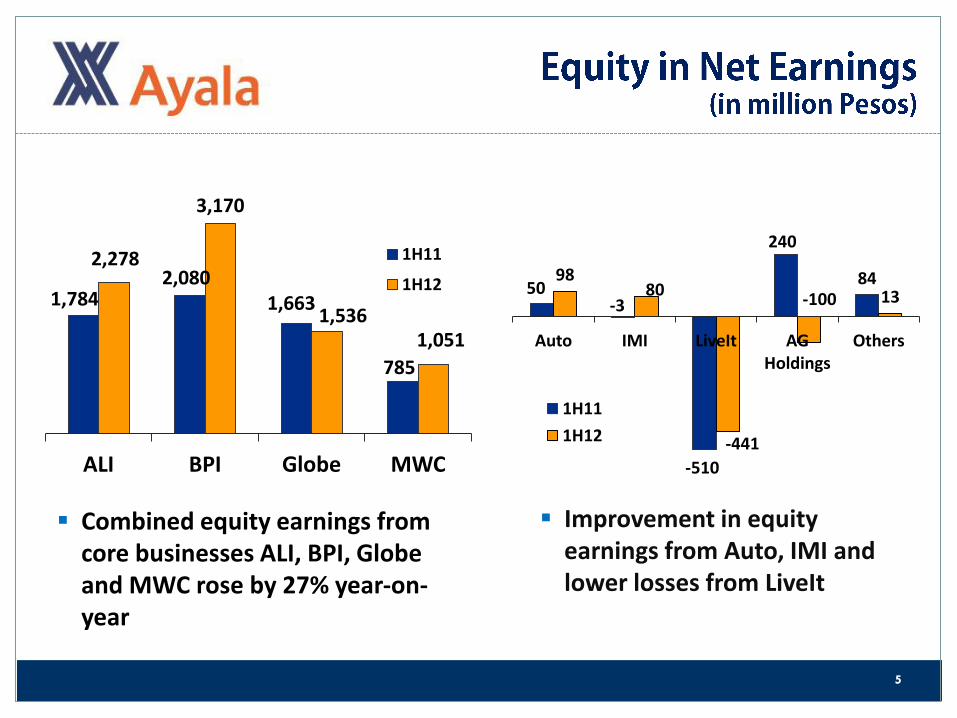

Combined equity earnings from core businesses ALI, BPI, Globe and MWC rose by 27% year-on-year

Improvement in equity earnings from Auto, IMI and lower losses from LiveIt

1,784 2,080

1,663

785

2,278

3,170

1,536 1,051

ALI BPI Globe MWC

1H11

1H12 50 -3

-510

240

84 98 80

-441

-100 13

Auto IMI LiveIt AG Holdings

Others

1H11

1H12

5

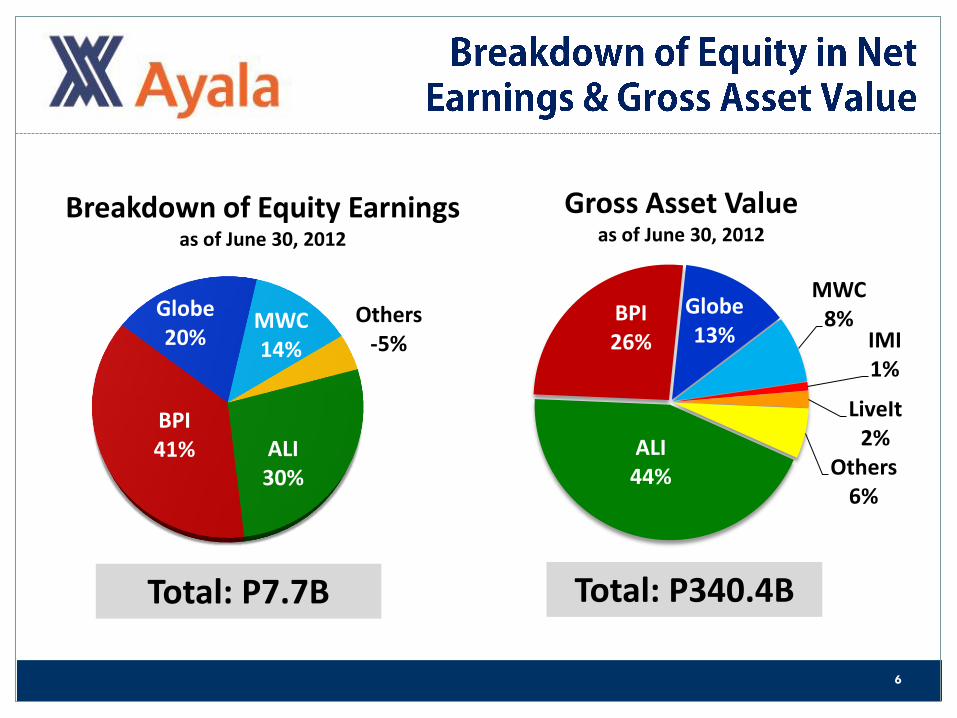

ALI 30%

BPI 41%

Globe 20%

MWC 14%

Others -5%

Breakdown of Equity Earnings as of June 30, 2012

Total: P7.7B

ALI 44%

BPI 26%

Globe 13%

MWC 8%

IMI 1%

LiveIt 2%

Others 6%

Gross Asset Value as of June 30, 2012

Total: P340.4B

6

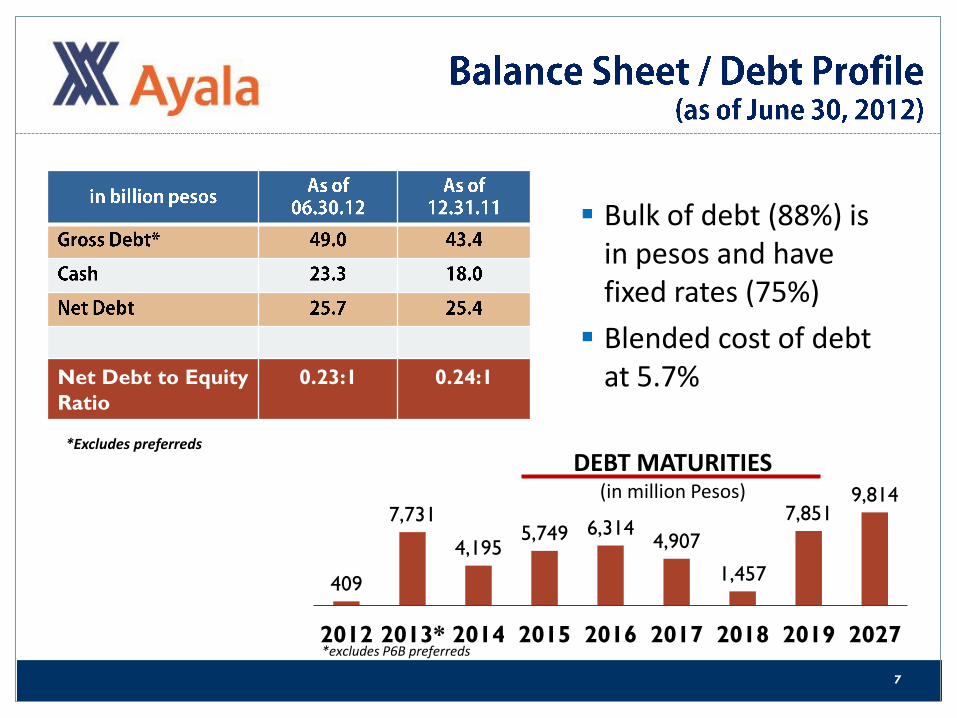

Net Debt to Equity

Ratio

0.23:1 0.24:1

*Excludes preferreds

409

7,731

4,195 5,749 6,314

4,907

1,457

7,851 9,814

2012 2013* 2014 2015 2016 2017 2018 2019 2027

DEBT MATURITIES (in million Pesos)

Bulk of debt (88%) is in pesos and have fixed rates (75%)

Blended cost of debt at 5.7%

*excludes P6B preferreds

7

AC Treasury Share Placement

Placement of 15 million common shares held in Treasury

Shares sold at P430 per share

Raised cash proceeds of P6.45B

Proceeds for working capital and funding of potential investments

5.18 million shares left in Treasury

8

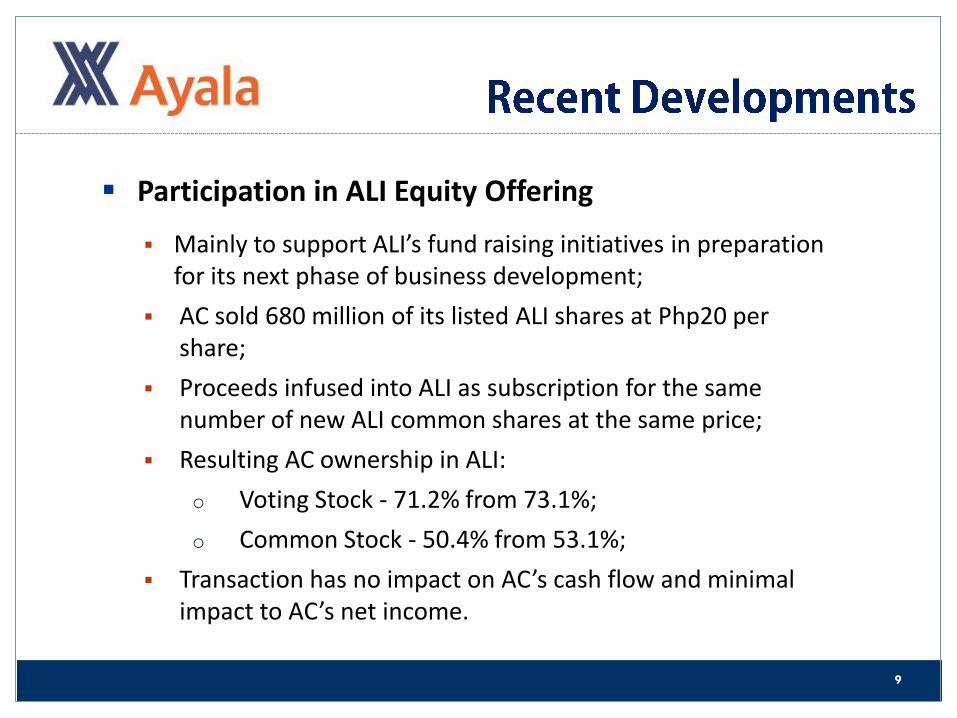

Mainly to support ALI’s fund raising initiatives in preparation for its next phase of business development;

AC sold 680 million of its listed ALI shares at Php20 per share;

Proceeds infused into ALI as subscription for the same number of new ALI common shares at the same price;

Resulting AC ownership in ALI:

o Voting Stock - 71.2% from 73.1%;

o Common Stock - 50.4% from 53.1%;

Transaction has no impact on AC’s cash flow and minimal impact to AC’s net income.

Participation in ALI Equity Offering

9

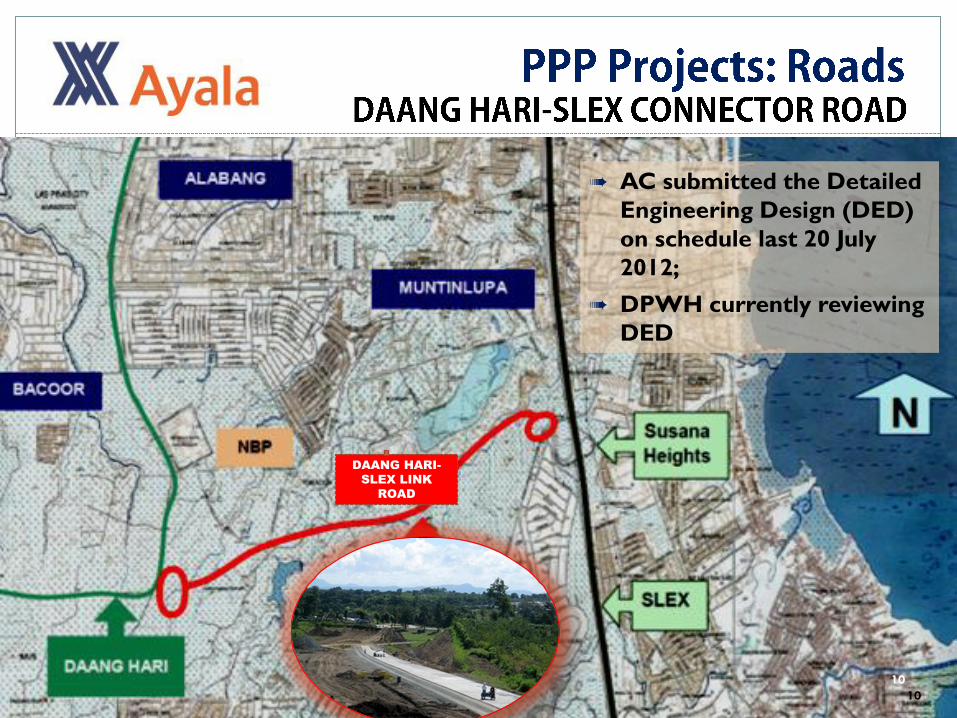

à AC submitted the Detailed

Engineering Design (DED)

on schedule last 20 July

2012;

à DPWH currently reviewing

DED

DAANG HARI-

SLEX LINK

ROAD

10

10

11

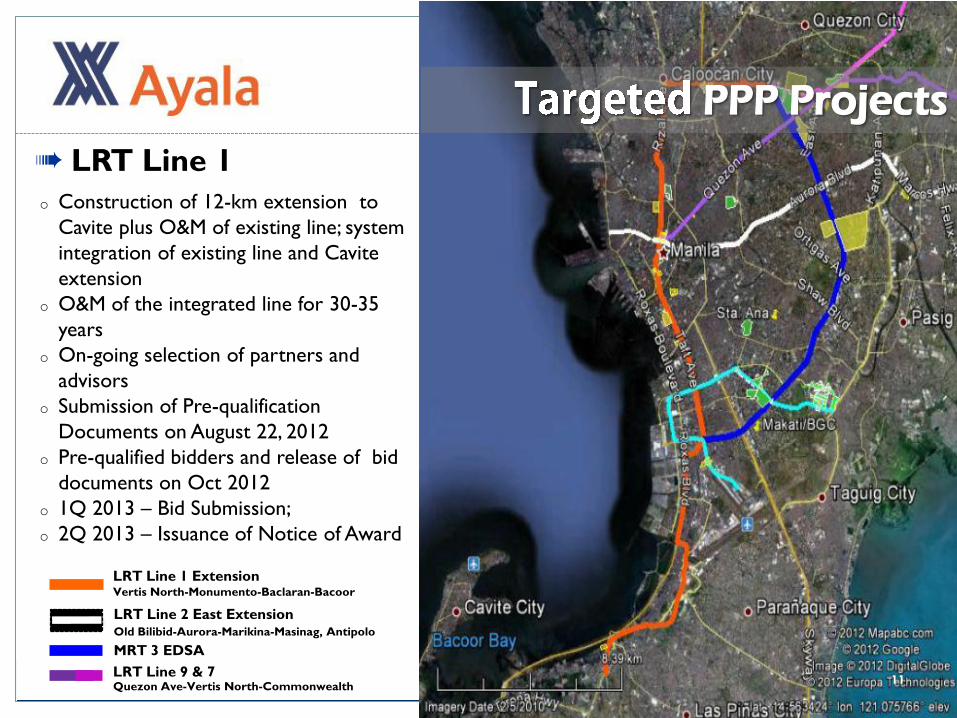

o Construction of 12-km extension to

Cavite plus O&M of existing line; system

integration of existing line and Cavite

extension

o O&M of the integrated line for 30-35

years

o On-going selection of partners and

advisors

o Submission of Pre-qualification

Documents on August 22, 2012

o Pre-qualified bidders and release of bid

documents on Oct 2012

o 1Q 2013 – Bid Submission;

o 2Q 2013 – Issuance of Notice of Award

à LRT Line 1

PPP Projects

LRT Line 1 Extension Vertis North-Monumento-Baclaran-Bacoor

LRT Line 2 East Extension Old Bilibid-Aurora-Marikina-Masinag, Antipolo

MRT 3 EDSA

LRT Line 9 & 7 Quezon Ave-Vertis North-Commonwealth

Design, Build, Operate & Maintain a 7-km 4-lane viaduct from Skyway to Roxas Boulevard and Macapagal Ave.

Estimated Construction Cost: P11B

30-year concession period

Pre-qualification submission: Sept 18, 2012

Bid Submission: December 2012

12

à NAIA EXPRESSWAY

12

o Divided into:

Cavite Section – 27.5 km, 6-lane tolled expressway from Kawit to Silang/ Aguinaldo (via PPP)

Laguna Section - 15.0 km, 6-lane tolled expressway from Silang to SLEX (via ODA)

o NEDA-ICC approved; invitation to pre-qualify expected to come out in the next few months

à Cavite-Laguna (CALA) Expressway

13

14

• Country’s 2nd primary gateway • Terminal expansion being

planned and feasibility study for new international terminal underway

• Development of new airport in Northern Mindanao

• Operation and maintenance of Laguindingan and Palawan airports to support ALI

Mactan Cebu International Airport

Laguindingan Airport

14

15

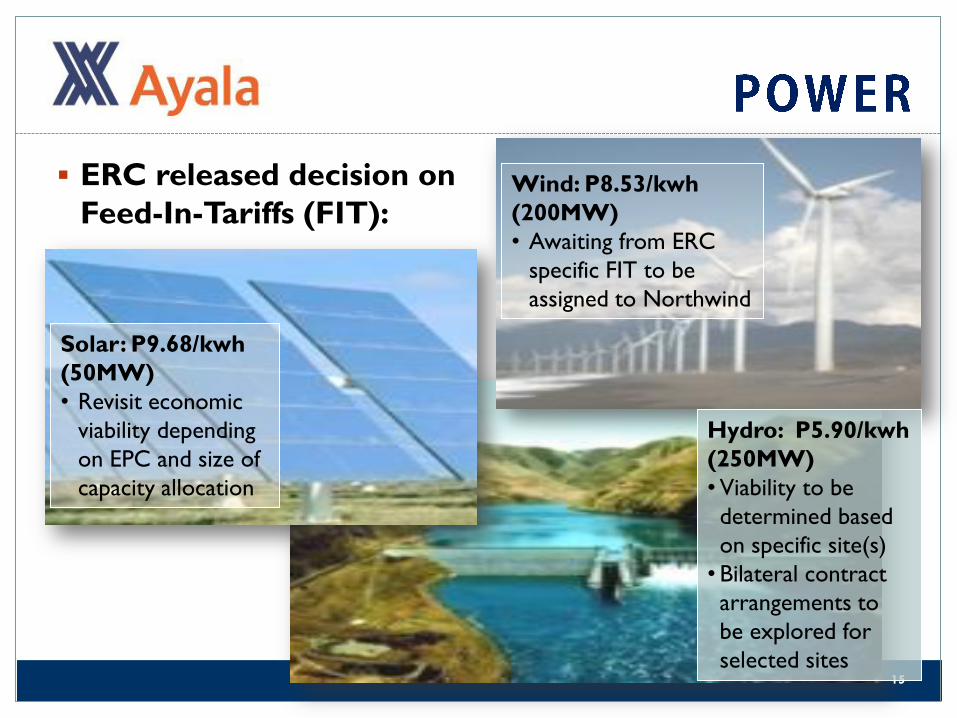

ERC released decision on

Feed-In-Tariffs (FIT):

Solar: P9.68/kwh

(50MW)

• Revisit economic

viability depending

on EPC and size of

capacity allocation

Wind: P8.53/kwh

(200MW)

• Awaiting from ERC

specific FIT to be

assigned to Northwind

Hydro: P5.90/kwh

(250MW)

•Viability to be

determined based

on specific site(s)

• Bilateral contract

arrangements to

be explored for

selected sites

16

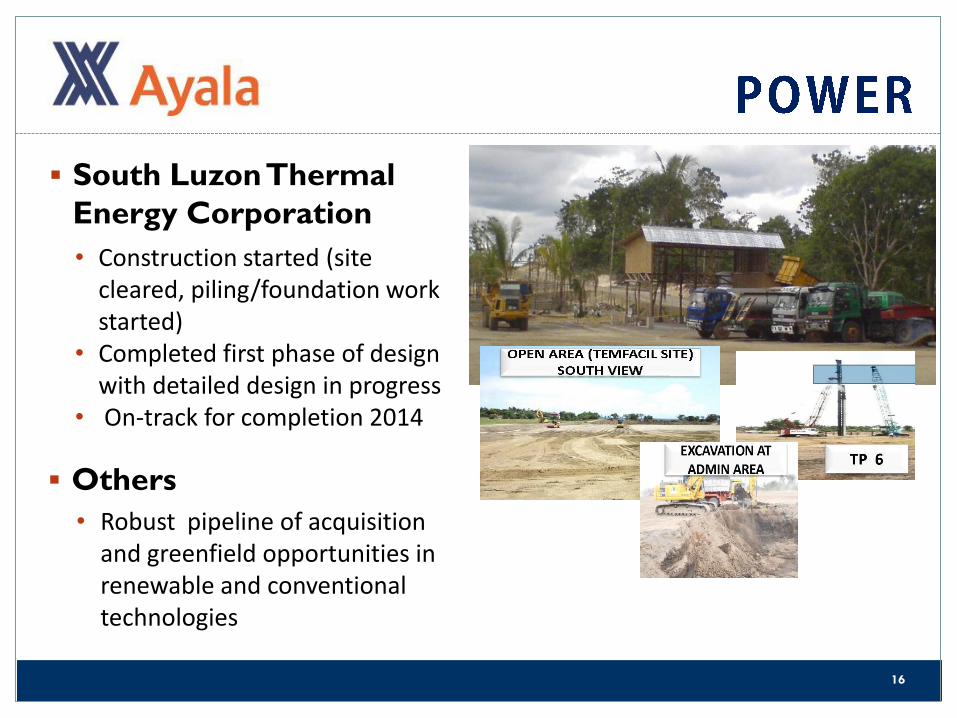

South Luzon Thermal

Energy Corporation

• Construction started (site cleared, piling/foundation work started)

• Completed first phase of design with detailed design in progress

• On-track for completion 2014

• Robust pipeline of acquisition and greenfield opportunities in renewable and conventional technologies

Others

BUSINESS UNIT REVIEW

17

1,759 2,194

3,381

4,326

2Q11 2Q12 1H11 1H12

Net Income (in million Pesos)

+25%

+28%

• Revenues up 18% in 1H12 due to: o 24% growth in Residential Segment o 21% increase in Commercial Leasing o 47% increase in Services o 15% growth in Hotels & Resorts

• 200 basis point improvement in NIAT margin

4Q11 1Q12 2Q12

12.8

19.3 19.8 Amaia

Avida

Alveo

ALP

Residential Sales Take-Up (in billion Pesos)

• Record sales continue: o Ave. monthly take-up of P6.5B in

1H12, up 64% vs P4.0B in 1H11 o Ave. monthly bookings of P3.5B up

57% vs. P2.2B in 1H11

• Strong demand across all brands

18

3Q11 4Q11 1Q12 2Q12

1,000 1,048 1,042 1,081

Occupied Mall GLA (‘000 sqms)

Harbor Point (Subic)

3Q11 4Q11 1Q12 2Q12

298 301 338 338

Two Evotech NUVALI

Occupied BPO Office GLA (‘000 sqms)

• New malls boost mall performance

• Occupied GLA up 8% y-o-y

• Ave. lease rate up 6% • Occupancy rate of

94%

• Occupied BPO GLA up 19% y-o-y

• Ave. lease rate up 4% • Occupancy rate of

83%

19

3,344 3,615

6,198

9,449

2Q11 2Q12 1H11 1H12

NET INCOME (in million Pesos)

• Revenues up 24% due to: o 9% growth in net interest

income o 51% increase in non-interest

income

• NIMs improved by 14 basis points

• Loan growth from all segments sustained

o Middle Market & SME +19%

o Corporate + 15%

o Consumer + 17%

• Improvement in cost efficiency

• ROE of 21%

In Billion Php June 30, 2012 YoY Growth

Total Resources 899 5%

Deposits 733 6%

AUM 730 +15%

Net Loans 480 + 17%

Selected Ratios June 2012 Dec 2011

30-day NPL 1.4% 1.9%

Cost-to-Income 49.5% 56.2%

Basel II CAR 14.5%

+8% +52%

20

3,344 3,615

6,198

9,449

2Q11 2Q12 1H11 1H12

NET INCOME (in million Pesos)

• Revenues up 24% due to: o 9% growth in net interest

income o 51% increase in non-interest

income

• NIMs improved by 14 basis points

• Loan growth from all segments sustained

o Middle Market & SME +19%

o Corporate + 15%

o Consumer + 17%

• Improvement in cost efficiency

• ROE of 21%

In Billion Php June 30, 2012 YoY Growth

Total Resources 899 5%

Deposits 733 6%

AUM 730 +15%

Net Loans 480 + 17%

Selected Ratios June 2012 Dec 2011

30-day NPL 1.4% 1.9%

Cost-to-Income 49.5% 56.2%

Basel II CAR 14.5%

+8% +52%

21

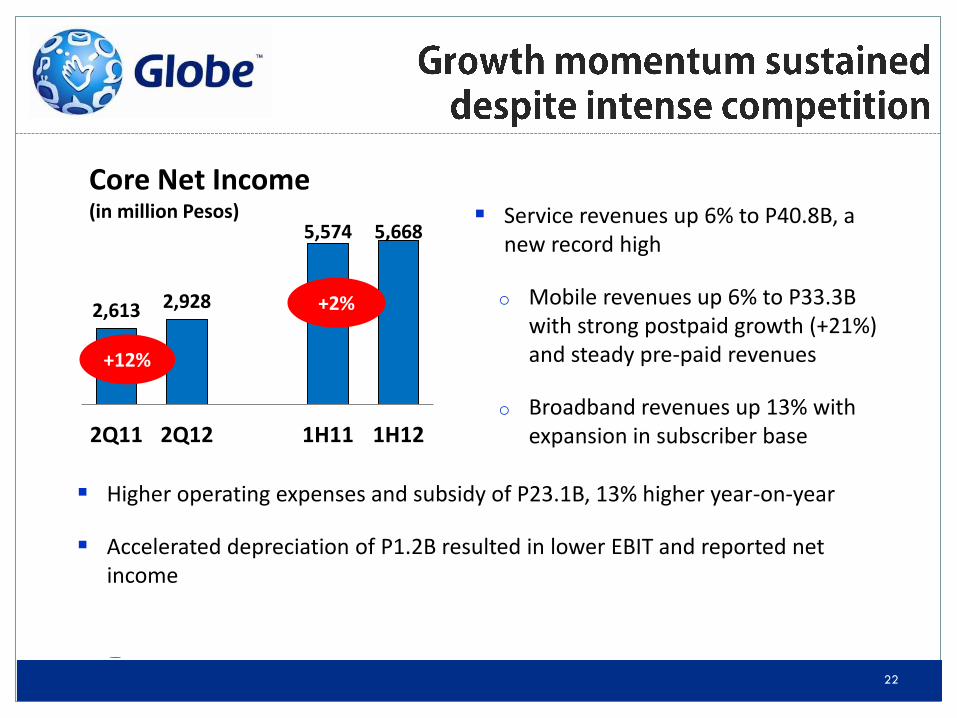

Manila Water

Service revenues up 6% to P40.8B, a new record high

o Mobile revenues up 6% to P33.3B with strong postpaid growth (+21%) and steady pre-paid revenues

o Broadband revenues up 13% with expansion in subscriber base

2,613 2,928

5,574 5,668

2Q11 2Q12 1H11 1H12

Core Net Income (in million Pesos)

+12%

+2%

Higher operating expenses and subsidy of P23.1B, 13% higher year-on-year

Accelerated depreciation of P1.2B resulted in lower EBIT and reported net income

22

Manila Water

Mobile subscribers increased by 12% year-on-year with strong growth across all brands

272 317

1,021 1,267

1H 2011 1H 2012

Wireless

DSL

1,293

1,584

Broadband Subscribers (in ‘000)

+22%

Subscribers by Brand (in Thousand SIMs)

1H12 YoY

Globe Postpaid 1,600 28%

Globe Prepaid 16,110 9%

TM 14,017 12%

Totals 31,726 12%

Broadband subscribers grew by 22% with quarterly gross additions at new all-time high

Continued launch of products and services that

provide differentiated customer experience

23

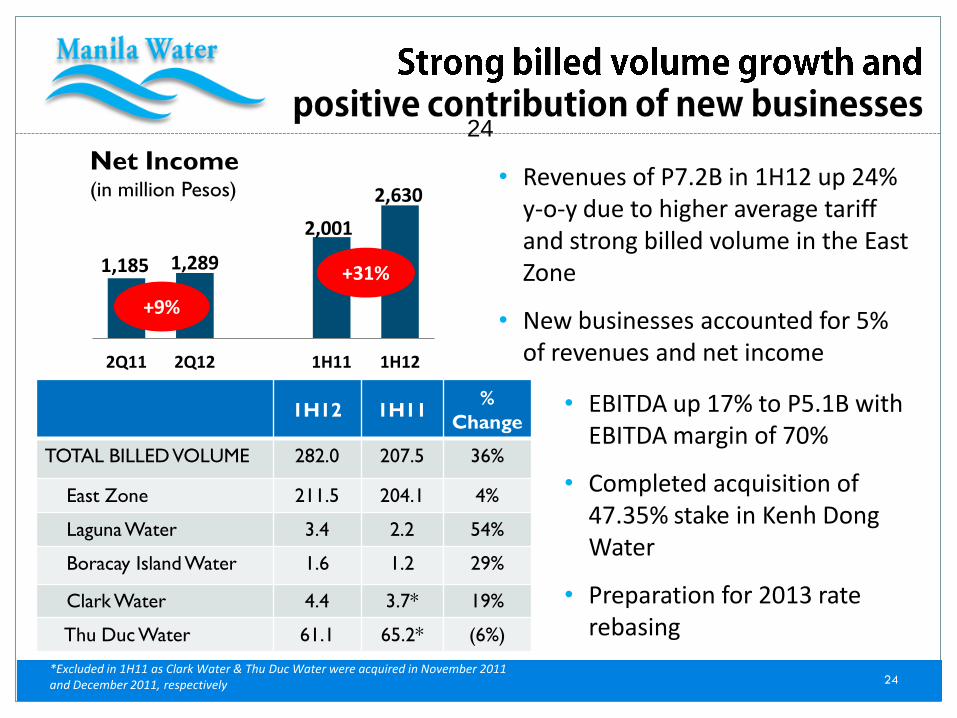

1H12 1H11 %

Change

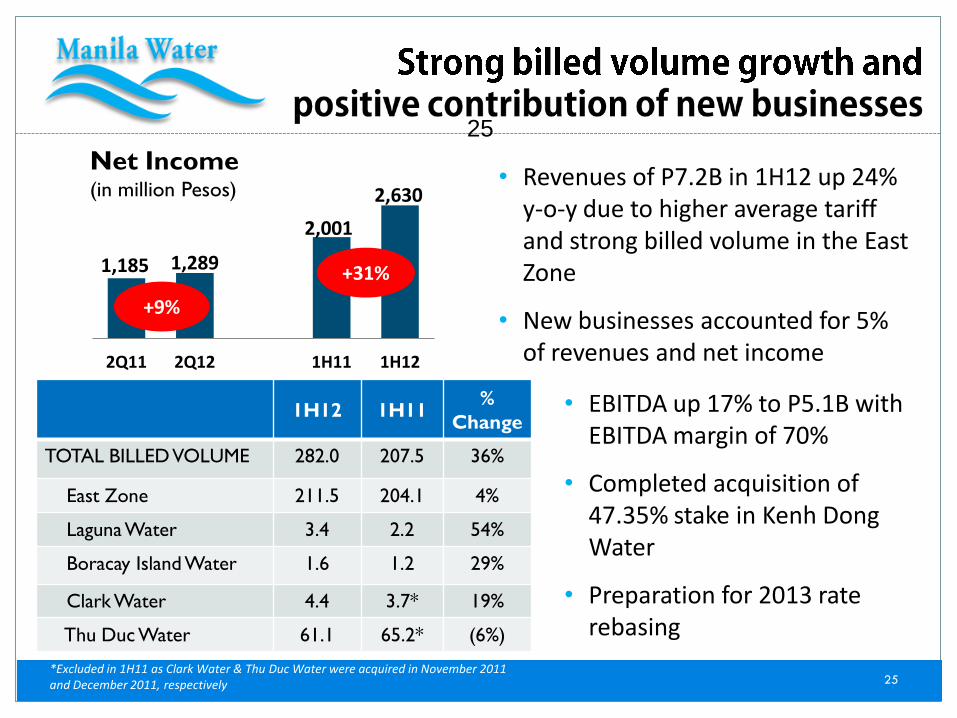

TOTAL BILLED VOLUME 282.0 207.5 36%

East Zone 211.5 204.1 4%

Laguna Water 3.4 2.2 54%

Boracay Island Water 1.6 1.2 29%

Clark Water 4.4 3.7* 19%

Thu Duc Water 61.1 65.2* (6%)

Net Income (in million Pesos)

1,185 1,289

2,001

2,630

2Q11 2Q12 1H11 1H12

+9%

+31%

• EBITDA up 17% to P5.1B with EBITDA margin of 70%

• Completed acquisition of 47.35% stake in Kenh Dong Water

• Preparation for 2013 rate rebasing

• Revenues of P7.2B in 1H12 up 24% y-o-y due to higher average tariff and strong billed volume in the East Zone

• New businesses accounted for 5% of revenues and net income

*Excluded in 1H11 as Clark Water & Thu Duc Water were acquired in November 2011 and December 2011, respectively

24

24

1H12 1H11 %

Change

TOTAL BILLED VOLUME 282.0 207.5 36%

East Zone 211.5 204.1 4%

Laguna Water 3.4 2.2 54%

Boracay Island Water 1.6 1.2 29%

Clark Water 4.4 3.7* 19%

Thu Duc Water 61.1 65.2* (6%)

Net Income (in million Pesos)

1,185 1,289

2,001

2,630

2Q11 2Q12 1H11 1H12

+9%

+31%

• EBITDA up 17% to P5.1B with EBITDA margin of 70%

• Completed acquisition of 47.35% stake in Kenh Dong Water

• Preparation for 2013 rate rebasing

• Revenues of P7.2B in 1H12 up 24% y-o-y due to higher average tariff and strong billed volume in the East Zone

• New businesses accounted for 5% of revenues and net income

*Excluded in 1H11 as Clark Water & Thu Duc Water were acquired in November 2011 and December 2011, respectively

25

25

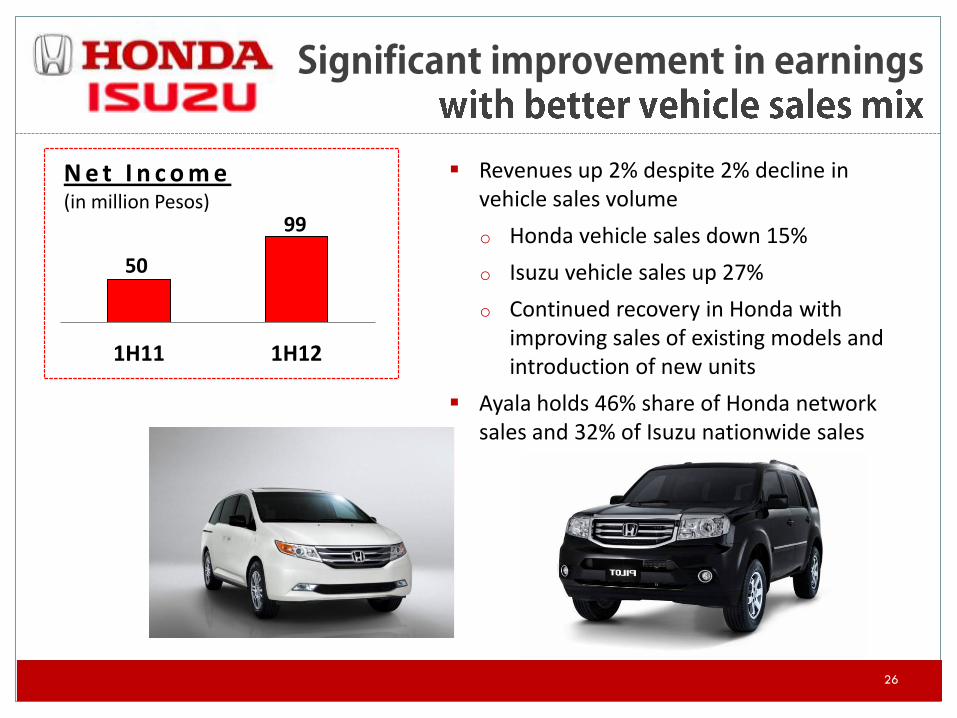

50

99

1H11 1H12

N e t I n c o m e (in million Pesos)

Revenues up 2% despite 2% decline in vehicle sales volume

o Honda vehicle sales down 15%

o Isuzu vehicle sales up 27%

o Continued recovery in Honda with improving sales of existing models and introduction of new units

Ayala holds 46% share of Honda network sales and 32% of Isuzu nationwide sales

26

1.1

3.1

1H11 1H12

Net Income (in million US$) 1H12 revenues grew by 24% to

US$326M due to full-year impact of EPIQ acquisition

EBITDA improved by 22% y-o-y to US$16M with reduced operating expenses

Net income growth brought about by lower selling & admin expenses

Sales mix is 83% turnkey and 17% consignment

77

143

0

42

80

135

86

25

Phils China Europe PSi

1H11

1H12

Revenues (in million US$)

+ 173%

27

$152.3 $166.2

1H 2011 1H 2012

9% YoY growth

Share of Revenues (In USD Millions)

$10.4 $13.1

1H 2011 1H 2012

26% YoY growth

Share of EBITDA (In USD Millions)

• Share of Revenues of $166.2, up 9% year-on-year

• Share of EBITDA of US$13M up 26% due primarily to improved profitability at Stream and Affinity Express.

28

28

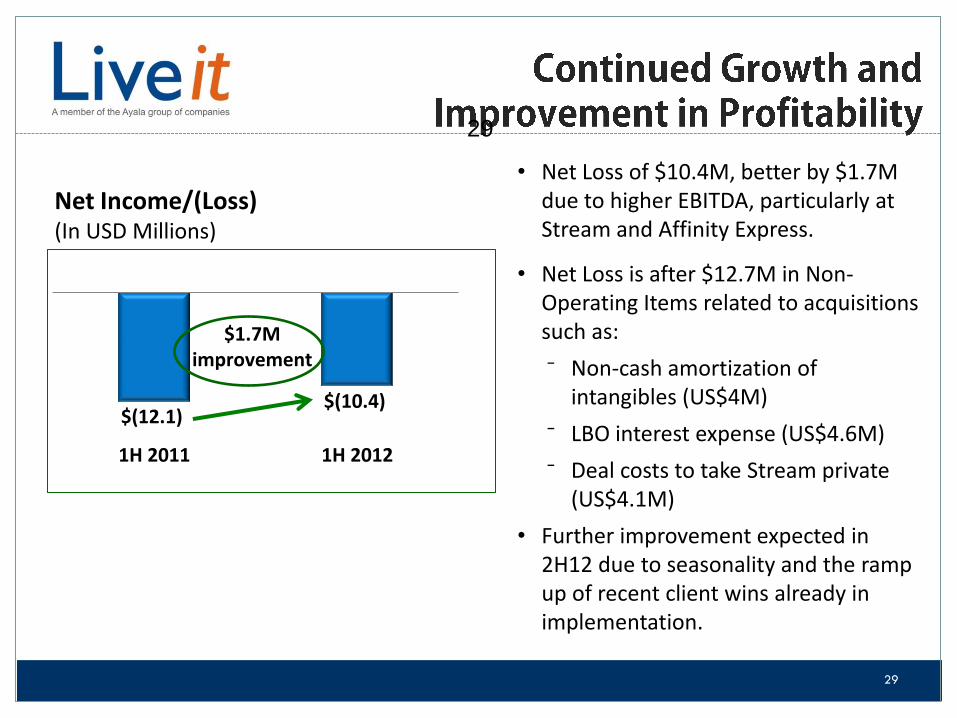

$(12.1) $(10.4)

1H 2011 1H 2012

$1.7M improvement

Net Income/(Loss) (In USD Millions)

• Net Loss of $10.4M, better by $1.7M due to higher EBITDA, particularly at Stream and Affinity Express.

• Net Loss is after $12.7M in Non- Operating Items related to acquisitions such as:

⁻ Non-cash amortization of intangibles (US$4M)

⁻ LBO interest expense (US$4.6M)

⁻ Deal costs to take Stream private (US$4.1M)

• Further improvement expected in 2H12 due to seasonality and the ramp up of recent client wins already in implementation.

29

29

30

Sustained growth momentum of core businesses

International businesses continue to improve

Expanding and executing on new businesses

Strong funding capacity with flexibility to scale up investments