25

Corporate Finance Introduction to risk Prof. André Farber SOLVAY BUSINESS SCHOOL UNIVERSITÉ LIBRE DE BRUXELLES

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| View: | 229 times |

| Download: | 6 times |

Corporate Finance

Introduction to riskProf. André FarberSOLVAY BUSINESS SCHOOLUNIVERSITÉ LIBRE DE BRUXELLES

A.Farber Vietnam 2004 |2

Introduction to risk

• Objectives for this session :– 1. Review the problem of the opportunity cost of capital

– 2. Analyze return statistics

– 3. Introduce the variance or standard deviation as a measure of risk for a portfolio

– 4. See how to calculate the discount rate for a project with risk equal to that of the market

– 5. Give a preview of the implications of diversification

A.Farber Vietnam 2004 |3

Setting the discount rate for a risky project

• Stockholders have a choice:– either they invest in real investment projects of companies

– or they invest in financial assets (securities) traded on the capital market

• The cost of capital is the opportunity cost of investing in real assets

• It is defined as the forgone expected return on the capital market with the same risk as the investment in a real asset

A.Farber Vietnam 2004 |4

Three key ideas

• 1. Returns are normally distributed random variables Markowitz 1952: portfolio theory, diversification

• 2. Efficient market hypothesis Movements of stock prices are random Kendall 1953

• 3. Capital Asset Pricing Model Sharpe 1964 Lintner 1965 Expected returns are function of systematic risk

A.Farber Vietnam 2004 |5

Preview of what follow

• First, we will analyze past markets returns.

• We will:– compare average returns on common stocks and Treasury bills

– define the variance (or standard deviation) as a measure of the risk of a portfolio of common stocks

– obtain an estimate of the historical risk premium (the excess return earned by investing in a risky asset as opposed to a risk-free asset)

• The discount rate to be used for a project with risk equal to that of the market will then be calculated as the expected return on the market:

Expected return on the market

Current risk-free rate

Historical risk premium

= +

A.Farber Vietnam 2004 |6

Implications of diversification

• The next step will be to understand the implications of diversification.

• We will show that:– diversification enables an investor to eliminate part of the risk of a stock held

individually (the unsystematic - or idiosyncratic risk).

– only the remaining risk (the systematic risk) has to be compensated by a higher expected return

– the systematic risk of a security is measured by its beta (), a measure of the sensitivity of the actual return of a stock or a portfolio to the unanticipated return in the market portfolio

– the expected return on a security should be positively related to the security's beta

A.Farber Vietnam 2004 |7

Capital Asset Pricing Model (CAPM)

• Risk – expected return relationship:

jFMFj RRRR )(Expected

returnRisk-free interest

rate

Market risk

premium

Risk

A.Farber Vietnam 2004 |8

Returns

• The primitive objects that we will manipulate are percentage returns over a period of time:

• The rate of return is a return per dollar (or £, DEM,...) invested in the asset, composed of– a dividend yield

– a capital gain

• The period could be of any length: one day, one month, one quarter, one year.

• In what follow, we will consider yearly returns

1

1

1

t

tt

t

tt P

PP

P

divR

A.Farber Vietnam 2004 |9

Ex post and ex ante returns

• Ex post returns are calculated using realized prices and dividends

• Ex ante, returns are random variables– several values are possible

– each having a given probability of occurence

• The frequency distribution of past returns gives some indications on the probability distribution of future returns

A.Farber Vietnam 2004 |10

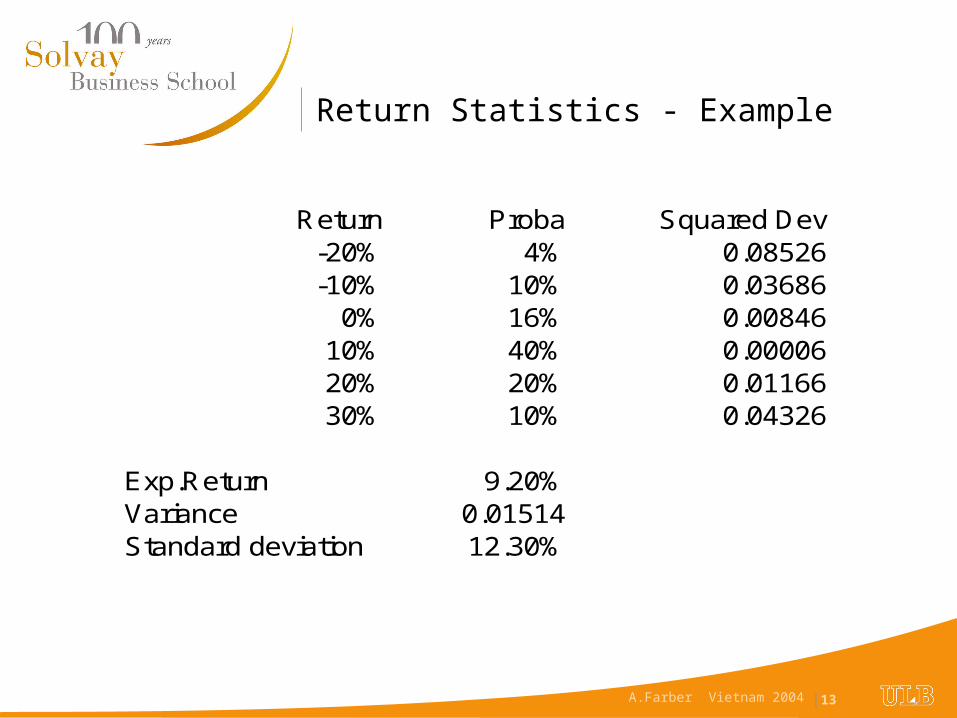

Frequency distribution

• Suppose that we observe the following frequency distribution for past annual returns over 50 years. Assuming a stable probability distribution, past relative frequencies are estimates of probabilities of future possible returns .

Realized Return Absolutefrequency

Relativefrequency

-20% 2 4%

-10% 5 10%

0% 8 16%

+10% 20 40%

+20% 10 20%

+30% 5 10%

50 100%

A.Farber Vietnam 2004 |11

Mean/expected return

• Arithmetic Average (mean)– The average of the holding period returns for the individual years

• Expected return on asset A:– A weighted average return : each possible return is multiplied or weighted by the

probability of its occurence. Then, these products are summed to get the expected return.

N

RRRRMean N

...21

1...

return ofy probabilit with

...)(

21

2211

n

ii

nn

ppp

Rp

RpRpRpRE

A.Farber Vietnam 2004 |12

Variance -Standard deviation

• Measures of variability (dispersion)

• Variance

• Ex post: average of the squared deviations from the mean

• Ex ante: the variance is calculated by multiplying each squared deviation from the expected return by the probability of occurrence and summing the products

• Unit of measurement : squared deviation units. Clumsy..

• Standard deviation : The square root of the variance

• Unit :return

VarR R R R R R

TT

2 12

22 2

1( ) ( ) ... ( )

Var R Expected RA A A( ) ) 2 2 val ue of (RA

Var R p R R p R R p R RA A A A A A N A N A( ) ( ) ( ) ... ( ), , , 21 1

22 2

2 2

SD R Var RA A A( ) ( )

A.Farber Vietnam 2004 |13

Return Statistics - Example

Return Proba Squared Dev-20% 4% 0.08526-10% 10% 0.03686

0% 16% 0.0084610% 40% 0.0000620% 20% 0.0116630% 10% 0.04326

Exp.Return 9.20%Variance 0.01514Standard deviation 12.30%

A.Farber Vietnam 2004 |14

Normal distribution

• Realized returns can take many, many different values (in fact, any real number > -100%)

• Specifying the probability distribution by listing:– all possible values– with associated probabilities

• as we did before wouldn't be simple.

• We will, instead, rely on a theoretical distribution function (the Normal distribution) that is widely used in many applications.

• The frequency distribution for a normal distribution is a bellshaped curve.

• It is a symetric distribution entirely defined by two parameters

• – the expected value (mean)

• – the standard deviation

A.Farber Vietnam 2004 |15

Belgium - Monthly returns 1951 - 1999Bourse de Bruxelles 1951-1999

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

-20.

00

-18.

00

-16.

00

-14.

00

-12.

00

-10.

00

-8.0

0

-6.0

0

-4.0

0

-2.0

0 0.

00

2.00

4.

00

6.00

8.

00

10.0

0

12.0

0

14.0

0

16.0

0

18.0

0

20.0

0

22.0

0

24.0

0

26.0

0

28.0

0

30.0

0

Rentabilité mensuelle

Fré

qu

en

ce

A.Farber Vietnam 2004 |16

Normal distribution illustrated

Normal distribution

0.0000

0.0050

0.0100

0.0150

0.0200

0.0250

68.26%

95.44%

Standard deviation from mean

A.Farber Vietnam 2004 |17

Risk premium on a risky asset

• The excess return earned by investing in a risky asset as opposed to a risk-free asset

•

• U.S.Treasury bills, which are a short-term, default-free asset, will be used a the proxy for a risk-free asset.

• The ex post (after the fact) or realized risk premium is calculated by substracting the average risk-free return from the average risk return.

• Risk-free return = return on 1-year Treasury bills

• Risk premium = Average excess return on a risky asset

A.Farber Vietnam 2004 |18

Total returns US 1926-1999

Arithmetic Mean

Standard Deviation

Risk Premium

Common Stocks 13.3% 20.1% 9.5%

Small Company Stocks 17.6 33.6 13.8

Long-term Corporate Bonds

5.9 8.7 2.1

Long-term government bonds

5.5 9.3 1.7

Intermediate-term government bond

5.4 5.8 1.6

U.S. Treasury bills 3.8 3.2

Inflation 3.2 4.5

Source: Ross, Westerfield, Jaffee (2002) Table 9.2

A.Farber Vietnam 2004 |19

Market Risk Premium: The Very Long Run

1802-1970 1871-1925

1926-1999

1802-1999

Common Stock 6.8 8.5 13.3 9.7

Treasury Bills 5.4 4.1 3.8 4.4

Risk premium 1.4 4.4 9.5 5.3

Source: Ross, Westerfield, Jaffee (2002) Table 9A.1

The equity premium puzzle:

Was the 20th century an anomaly?

A.Farber Vietnam 2004 |20

Notions of Market Efficiency

• An Efficient market is one in which:– Arbitrage is disallowed: rules out free lunches

– Purchase or sale of a security at the prevailing market price is never a positive NPV transaction.

– Prices reveal information

• Three forms of Market Efficiency

• (a) Weak Form Efficiency Prices reflect all information in the past record of stock prices

• (b) Semi-strong Form Efficiency Prices reflect all publicly available information

• (c) Strong-form Efficiency Price reflect all information

A.Farber Vietnam 2004 |21

Efficient markets: intuition

Expectation

Time

Price

Realization

Price change is unexpected

A.Farber Vietnam 2004 |22

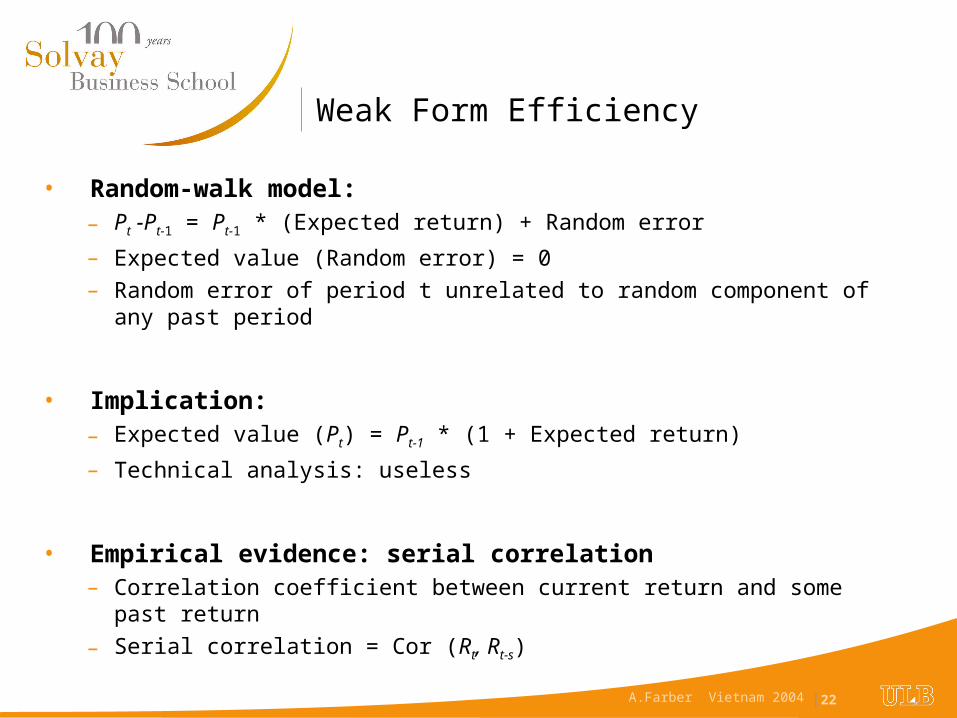

Weak Form Efficiency

• Random-walk model:– Pt -Pt-1 = Pt-1 * (Expected return) + Random error

– Expected value (Random error) = 0

– Random error of period t unrelated to random component of any past period

• Implication:– Expected value (Pt) = Pt-1 * (1 + Expected return)

– Technical analysis: useless

• Empirical evidence: serial correlation– Correlation coefficient between current return and some past return

– Serial correlation = Cor (Rt, Rt-s)

A.Farber Vietnam 2004 |23

Random walk - illustration

Bourse de Bruxelles 1980-1999

-30.00

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

-30.00 -25.00 -20.00 -15.00 -10.00 -5.00 0.00 5.00 10.00 15.00 20.00 25.00

Rentabilité mois t

Re

nta

bili

té m

ois

t+

1

A.Farber Vietnam 2004 |24

Semi-strong Form Efficiency

• Prices reflect all publicly available information

• Empirical evidence: Event studies

• Test whether the release of information influences returns and when this influence takes place.

• Abnormal return AR : ARt = Rt - Rmt

• Cumulative abnormal return:

• CARt = ARt0 + ARt0+1 + ARt0+2 +... + ARt0+1

A.Farber Vietnam 2004 |25

Strong-form Efficiency

• How do professional portfolio managers perform?

• Jensen 1969: Mutual funds do not generate abnormal returns

• Rfund - Rf = + (RM - Rf)

• Insider trading

• Insiders do seem to generate abnormal returns

• (should cover their information acquisition activities)