27

Corporate Corporate Finance Finance

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | donna-todd |

| View: | 248 times |

| Download: | 5 times |

Corporate Corporate FinanceFinance

Working Capital Working Capital ManagementManagement

Classification of working capitalClassification of working capital Current Assets Financing – Hedging Current Assets Financing – Hedging

approachapproach Short term Vs long term financingShort term Vs long term financing Risk of short & long term financingRisk of short & long term financing Trade off of short & long term Trade off of short & long term

financingfinancing

Classification of working Classification of working capitalcapital

Components: Components: Inventory,Inventory, cash, cash, securities, securities, receivablesreceivables

Time basis: it may be Time basis: it may be temporary or temporary or permanentpermanent

Temporary working Temporary working capitalcapital

Temporary working capital is the amount of investment Temporary working capital is the amount of investment in current assets that varies according to the seasonal in current assets that varies according to the seasonal requirements. requirements.

ExampleExample

consider an ice cream manufacturing firm. During the consider an ice cream manufacturing firm. During the months of Maymonths of May September the manufacturer has to September the manufacturer has to keep the maximum inventory to support high level keep the maximum inventory to support high level sales. During offseason like from November to January sales. During offseason like from November to January the sales are extremely low and lower investment in the sales are extremely low and lower investment in inventory is required. Now consider if a festival like Eid inventory is required. Now consider if a festival like Eid or Christmas is falling during December and this would or Christmas is falling during December and this would result in high sales, then a temporary increase in result in high sales, then a temporary increase in inventory would be required to support this sale level.inventory would be required to support this sale level.

Permanent working Permanent working capitalcapital

Permanent working capital is the minimum Permanent working capital is the minimum investment in current assets that is required investment in current assets that is required support long-term minimum need. Permanent support long-term minimum need. Permanent working capital resembles to fixed assets in two working capital resembles to fixed assets in two aspects. First the dollar investment is long term aspects. First the dollar investment is long term despite contradiction that assets being financed despite contradiction that assets being financed are called ‘current’. Second, for a growing firm, are called ‘current’. Second, for a growing firm, the need to increase the minimum permanent the need to increase the minimum permanent working capital is the same as of fixed assets. working capital is the same as of fixed assets. However, there is a case of difference between However, there is a case of difference between the permanent working capital and fixed asset.the permanent working capital and fixed asset.

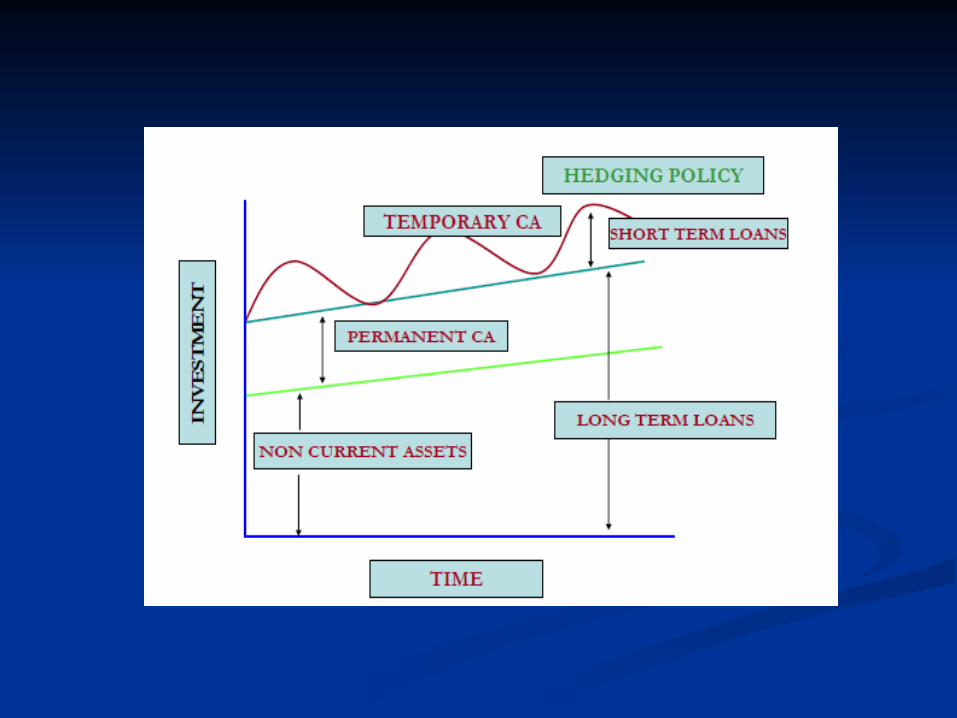

Current Assets Financing Current Assets Financing

Hedging approach:Hedging approach:Under this approach each asset would be offset Under this approach each asset would be offset with a financing instrument of the same with a financing instrument of the same maturity. Short term seasonal investment maturity. Short term seasonal investment requirements should be financed through short requirements should be financed through short term loans and permanent current asset and all term loans and permanent current asset and all fixed assets should be financed through long fixed assets should be financed through long term loan and equity. term loan and equity.

Short Term & Long Term Short Term & Long Term MixMix

Investment in current asset does involve a trade off Investment in current asset does involve a trade off between the risk and profitability. As a matter of fact the between the risk and profitability. As a matter of fact the current liabilities side of working capital does not consist current liabilities side of working capital does not consist of active decision variables in the sense; you cannot defer of active decision variables in the sense; you cannot defer payment to creditors beyond certain limits. Same is true payment to creditors beyond certain limits. Same is true for accrued expenses like electricity, payroll etc. There’s for accrued expenses like electricity, payroll etc. There’s no big room for playing with current liabilities which are no big room for playing with current liabilities which are also termed as spontaneous source of finance. As the also termed as spontaneous source of finance. As the underlying investment in current assets grows, accounts underlying investment in current assets grows, accounts payable and accruals also tend to grow, in part financing payable and accruals also tend to grow, in part financing the increase in assets. The issue here is how to handle the increase in assets. The issue here is how to handle assets not supported by spontaneous financing. This is assets not supported by spontaneous financing. This is termed as residual financing requirements – that is net termed as residual financing requirements – that is net investment after deducting spontaneous financing.investment after deducting spontaneous financing.

OvertradingOvertrading In contrast with over-capitalization, overtrading In contrast with over-capitalization, overtrading

occurs when a firm tries to do too much too quickly occurs when a firm tries to do too much too quickly with too little long term capital, so that it is trying with too little long term capital, so that it is trying to support too large trade volume with limited to support too large trade volume with limited capital resources.capital resources.

Signs leading to overtradingSigns leading to overtrading There is significant increase in turnover.There is significant increase in turnover. Increase in current assets is rapid.Increase in current assets is rapid. Stock turnover the debtors turnover might slow Stock turnover the debtors turnover might slow

down, in which case the rate of increase indown, in which case the rate of increase in stocks and debtors would be even greater than the stocks and debtors would be even greater than the

increase in sales.increase in sales.

Payment to creditors is pushed to Payment to creditors is pushed to increase length.increase length.

Short term loans are exceeding the limits Short term loans are exceeding the limits and firm tries to negotiate increased and firm tries to negotiate increased limits.limits.

The current and quick ratio fallsThe current and quick ratio falls The firm leads to liquid deficit situation The firm leads to liquid deficit situation

where current liabilities are greater than where current liabilities are greater than current assets.current assets.

Indications & RemediesIndications & Remedies

Set New Payment TermsSet New Payment Terms Offer Discounts for Prompt Offer Discounts for Prompt

PaymentPayment Use factoring or invoice Use factoring or invoice

discountingdiscounting Negotiate payment terms with Negotiate payment terms with

your suppliersyour suppliers

Cash ManagementCash Management

Motives for Cash holdingMotives for Cash holding Cash flow problems and remediesCash flow problems and remedies Investing surplus cashInvesting surplus cash Inventory approach to cash Inventory approach to cash

managementmanagement Demerits.Demerits.

Cash FlowCash FlowProblems and RemediesProblems and Remedies

Growth: a growing business needs to have Growth: a growing business needs to have more non current assets and these fixed more non current assets and these fixed assets must be financed.assets must be financed.

Seasonal business: like on Eid and Seasonal business: like on Eid and religious occasions, the business activity religious occasions, the business activity jumps manifolds and firms need more jumps manifolds and firms need more cash to procure inventory etc.cash to procure inventory etc.

Capital expense or one-off expenditure.Capital expense or one-off expenditure. Losses increase the cash flow problemsLosses increase the cash flow problems

How to improve cash How to improve cash flow:flow:

decreasing the receipt floatdecreasing the receipt float deferring capital expenditure (capex) and deferring capital expenditure (capex) and

developmental workdevelopmental work accelerating cash inflows which were set accelerating cash inflows which were set

for recovery at a later period.for recovery at a later period. liquidating investmentsliquidating investments deferring payments to creditorsdeferring payments to creditors rescheduling loan paymentsrescheduling loan payments planning is of immense importance planning is of immense importance

especially rolling cash budgets.especially rolling cash budgets.

Motives for Cash holdingMotives for Cash holding

Transactions Motive ensures that the firm Transactions Motive ensures that the firm has enough funds to transact its routine, has enough funds to transact its routine, day-to-day business affairs. Safety Motive day-to-day business affairs. Safety Motive protects the firm against being unable to protects the firm against being unable to meet unexpected demands for cash. meet unexpected demands for cash. Speculative Motive allows the firm to take Speculative Motive allows the firm to take advantage of unexpected opportunities advantage of unexpected opportunities that may arisethat may arise

Investing Surplus CashInvesting Surplus Cash Companies may have surplus cash or some Companies may have surplus cash or some

companies may be rich in cash and this leads us to companies may be rich in cash and this leads us to think “what to do with the surplus cash?” Obviously, think “what to do with the surplus cash?” Obviously, the “surplus” here means temporary and it should the “surplus” here means temporary and it should be invested in short term for earning return on it. be invested in short term for earning return on it. Before putting the surplus cash into any bank Before putting the surplus cash into any bank deposit, the firm will consider three factors:deposit, the firm will consider three factors:

Liquidity – company can withdraw the money out of Liquidity – company can withdraw the money out of deposit quickly and without the loss of value.deposit quickly and without the loss of value.

Profitability – the deposit must offer good return for Profitability – the deposit must offer good return for the risk being taken.the risk being taken.

Safety – there’s no chance of loss of deposit.Safety – there’s no chance of loss of deposit.

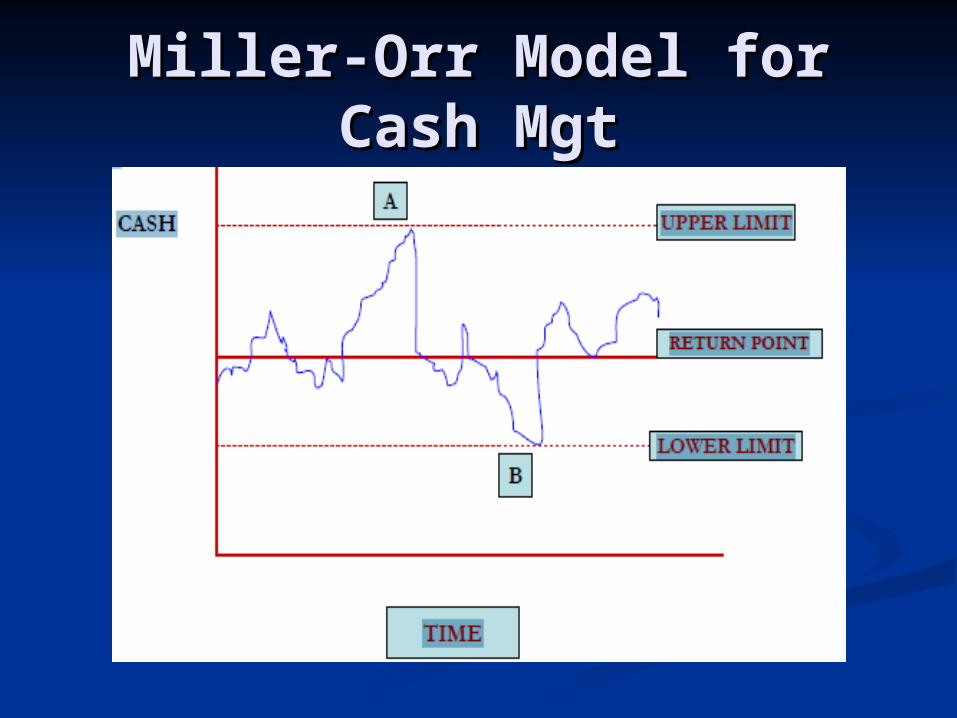

Miller-Orr Model for Miller-Orr Model for Cash MgtCash Mgt

ExplanationExplanation Most firms maintain a minimum amount of cash on Most firms maintain a minimum amount of cash on

hand to meet daily obligations or as a requirement hand to meet daily obligations or as a requirement from the firm's bank. A maximum amount may also be from the firm's bank. A maximum amount may also be specified to reflect the tradeoff between the specified to reflect the tradeoff between the transaction cost of investing in liquid assets (e.g. transaction cost of investing in liquid assets (e.g. Money Market Funds) and the cost of lost interest if Money Market Funds) and the cost of lost interest if the cash is not invested. The Miller-Orr model the cash is not invested. The Miller-Orr model computes the spread between the minimum and computes the spread between the minimum and maximum cash balance limits as maximum cash balance limits as Spread = 3(0.75 x Spread = 3(0.75 x transaction cost x variance of daily cash flows / transaction cost x variance of daily cash flows / daily interest rate) ^(1/3) daily interest rate) ^(1/3) (where a^b is used to (where a^b is used to denote "a to the power b"). The maximum cash balance denote "a to the power b"). The maximum cash balance is the spread plus the minimum cash balance, which is is the spread plus the minimum cash balance, which is assumed to be known.assumed to be known.

The "The "return point" is defined as the return point" is defined as the minimum cash balance plus spread/3.minimum cash balance plus spread/3.

Whenever the cash balance hits (or exceeds) the Whenever the cash balance hits (or exceeds) the maximum, the firm should invest the difference maximum, the firm should invest the difference between the amount available and the return between the amount available and the return point; if the minimum is reached, sufficient point; if the minimum is reached, sufficient securities should be sold to bring it up to the securities should be sold to bring it up to the return point.return point.

Inventory ManagementInventory Management

Inventory management is the active Inventory management is the active control program which allows the control program which allows the management of sales, purchases and management of sales, purchases and payments.payments.

The Inventory Management will control The Inventory Management will control operating costs and provide better operating costs and provide better understanding.understanding.

Inventory CostInventory Cost

Inventory costs depend on the amount of Inventory costs depend on the amount of space required, and how much that space space required, and how much that space costs. If the assumption is made that every costs. If the assumption is made that every part spends an equal amount of time located part spends an equal amount of time located in inventory, then the cost of inventory can in inventory, then the cost of inventory can be shared equally amongst all parts.be shared equally amongst all parts. Carrying cost:Carrying cost: Ordering cost:Ordering cost: Shortage Cost:Shortage Cost:

Economic order quantityEconomic order quantity EOQ The amount of orders that minimizes total EOQ The amount of orders that minimizes total

variable costs required to order and hold inventory. variable costs required to order and hold inventory. Re-order quantity is the quantity for which order is Re-order quantity is the quantity for which order is placed when the stock reached re-orders level. By fixing placed when the stock reached re-orders level. By fixing this quantity the purchaser has not to be to re-calculate this quantity the purchaser has not to be to re-calculate the quantity to be purchased each time he orders for the quantity to be purchased each time he orders for material.material.

Re-order quantity is known as economic order quantity Re-order quantity is known as economic order quantity because it is the quantity which is most economical to because it is the quantity which is most economical to order. In other words, economic order quantity is that order. In other words, economic order quantity is that size of quantity of the order which gives maximum size of quantity of the order which gives maximum economy in purchasing any material and ultimately economy in purchasing any material and ultimately contributes towards maintaining the material at the contributes towards maintaining the material at the optimum level and minimum cost.optimum level and minimum cost.

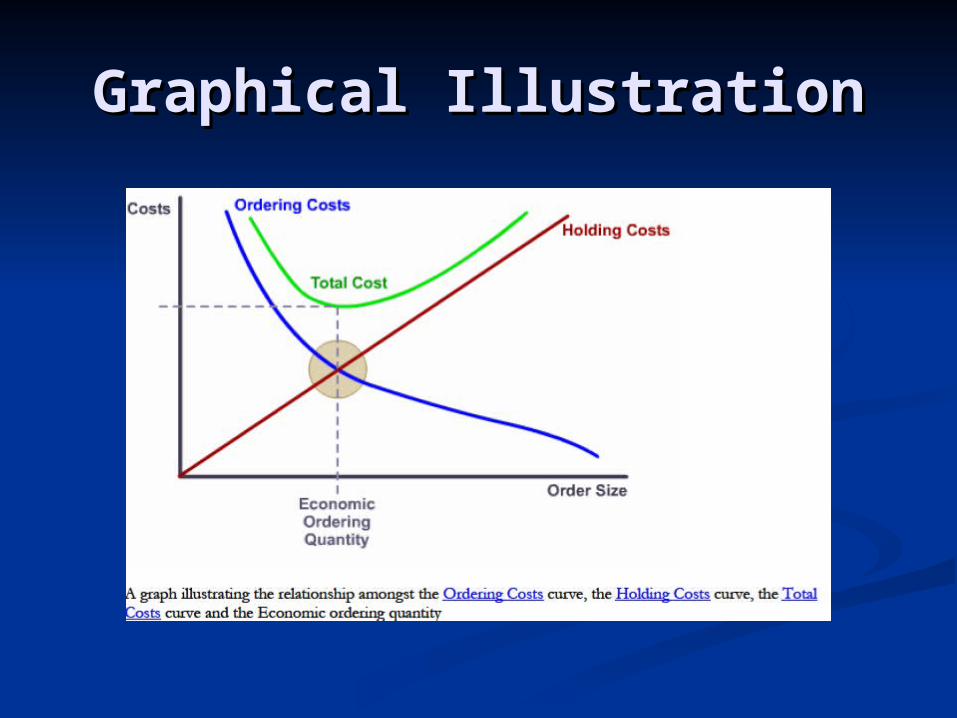

Graphical IllustrationGraphical Illustration

Reorder levelReorder level This is that level of material at which purchase requisition is This is that level of material at which purchase requisition is

initiated for fresh supplies. This is fixed some where initiated for fresh supplies. This is fixed some where between minimum level and maximum level. This is fixed in between minimum level and maximum level. This is fixed in such a way that by re-ordering when material falls to this such a way that by re-ordering when material falls to this level, then in the normal course of events, new supplies will level, then in the normal course of events, new supplies will be received just before the minimum level is reached. Its be received just before the minimum level is reached. Its formula is:formula is:

Re-order Level = Maximum consumption * Maximum re-Re-order Level = Maximum consumption * Maximum re-order periodorder period

The following factors are considered in fixing this level:The following factors are considered in fixing this level: Rate of consumption of the materialRate of consumption of the material Minimum levelMinimum level Delivery time; i.e., the time normally taken from the time of initiating Delivery time; i.e., the time normally taken from the time of initiating

a purchase requisition, to the receipts of materiala purchase requisition, to the receipts of material Variation in delivery time.Variation in delivery time.

Stock outsStock outs The situation when a firm runs out of stock which The situation when a firm runs out of stock which

results in shutdown of slow down of production / results in shutdown of slow down of production / sales. This approach is designed to minimize the sales. This approach is designed to minimize the risk of stock outs at all costs. Particularly in risk of stock outs at all costs. Particularly in manufacturing environment stocks-outs can have manufacturing environment stocks-outs can have a disastrous effect on the production process.a disastrous effect on the production process.

Maximum Stock LevelMaximum Stock Level Minimum Stock LevelMinimum Stock Level

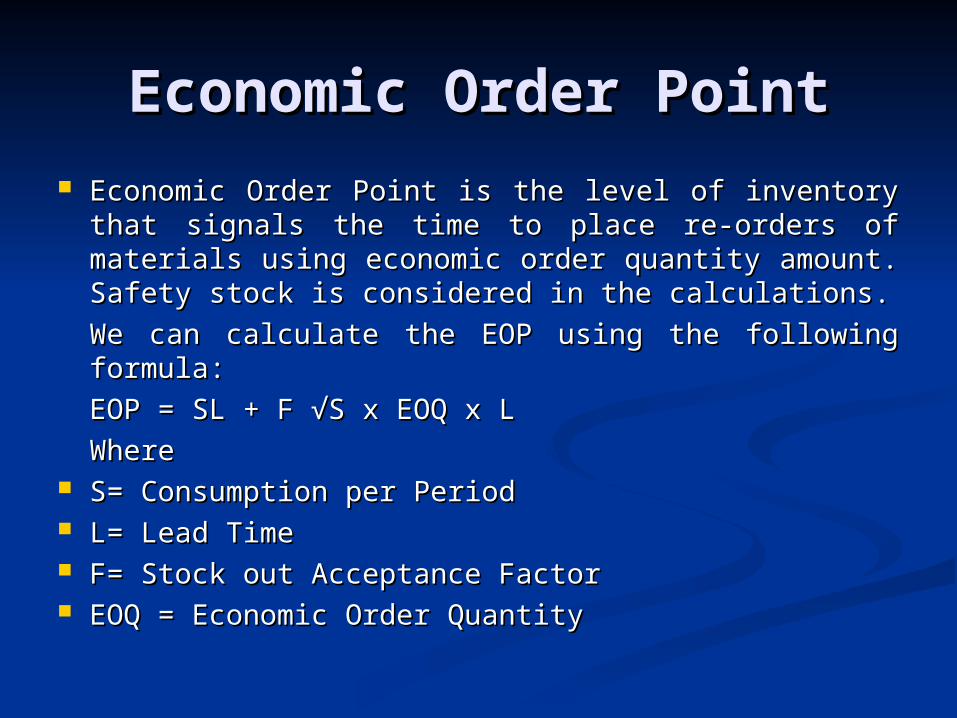

Economic Order PointEconomic Order Point Economic Order Point is the level of inventory that Economic Order Point is the level of inventory that

signals the time to place re-orders of materials using signals the time to place re-orders of materials using economic order quantity amount. Safety stock is economic order quantity amount. Safety stock is considered in the calculations.considered in the calculations.

We can calculate the EOP using the following We can calculate the EOP using the following formula:formula:

EOP = SL + F √S x EOQ x LEOP = SL + F √S x EOQ x L

WhereWhere S= Consumption per PeriodS= Consumption per Period L= Lead TimeL= Lead Time F= Stock out Acceptance FactorF= Stock out Acceptance Factor EOQ = Economic Order QuantityEOQ = Economic Order Quantity

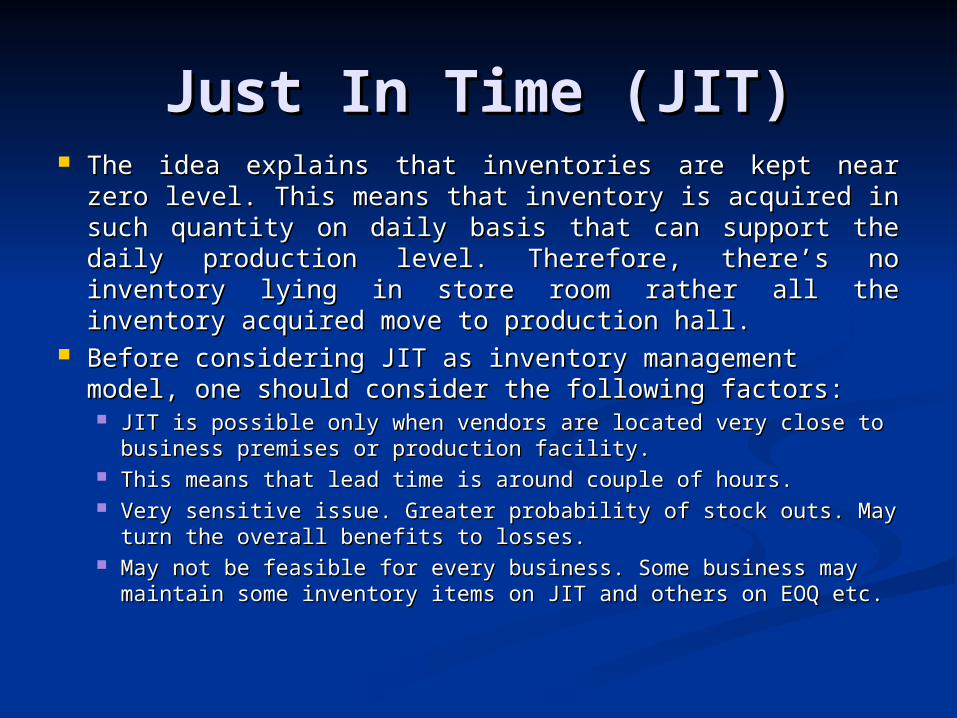

Just In Time (JIT)Just In Time (JIT) The idea explains that inventories are kept near zero The idea explains that inventories are kept near zero

level. This means that inventory is acquired in such level. This means that inventory is acquired in such quantity on daily basis that can support the daily quantity on daily basis that can support the daily production level. Therefore, there’s no inventory lying in production level. Therefore, there’s no inventory lying in store room rather all the inventory acquired move to store room rather all the inventory acquired move to production hall.production hall.

Before considering JIT as inventory management model, Before considering JIT as inventory management model, one should consider the following factors:one should consider the following factors: JIT is possible only when vendors are located very close to JIT is possible only when vendors are located very close to

business premises or production facility.business premises or production facility. This means that lead time is around couple of hours.This means that lead time is around couple of hours. Very sensitive issue. Greater probability of stock outs. May turn Very sensitive issue. Greater probability of stock outs. May turn

the overall benefits to losses.the overall benefits to losses. May not be feasible for every business. Some business may May not be feasible for every business. Some business may

maintain some inventory items on JIT and others on EOQ etc.maintain some inventory items on JIT and others on EOQ etc.