56

CORPORATE FINANCIAL THEORY Lecture 3

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | joshua-millwood |

| View: | 216 times |

| Download: | 2 times |

CORPORATE FINANCIALTHEORY

Lecture 3

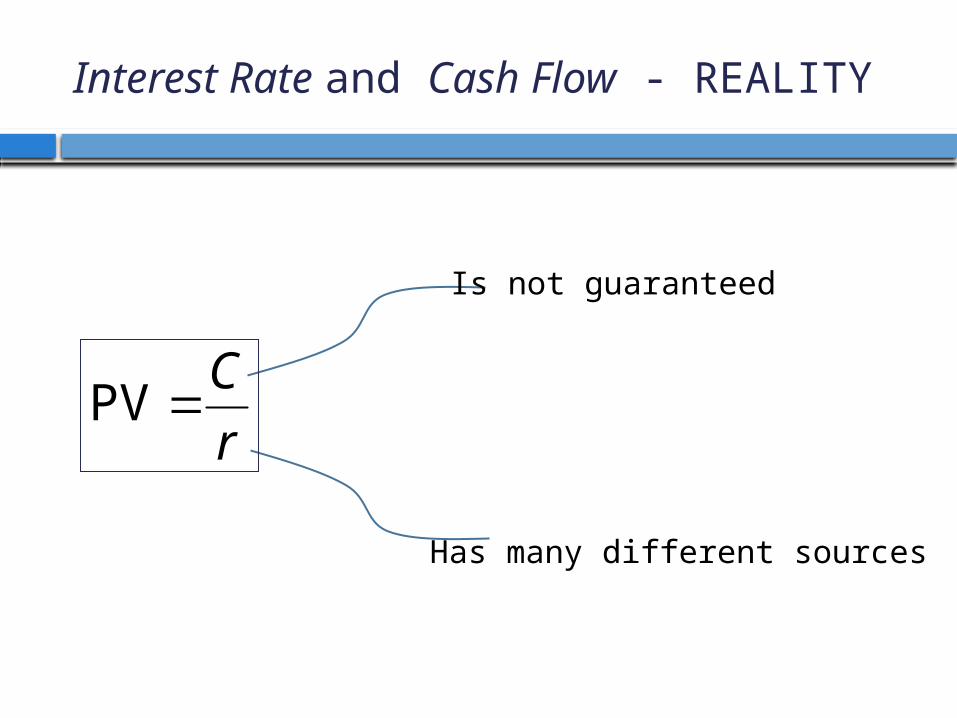

Interest Rate and Cash Flow - REALITY

r

CPV

Is not guaranteed

Has many different sources

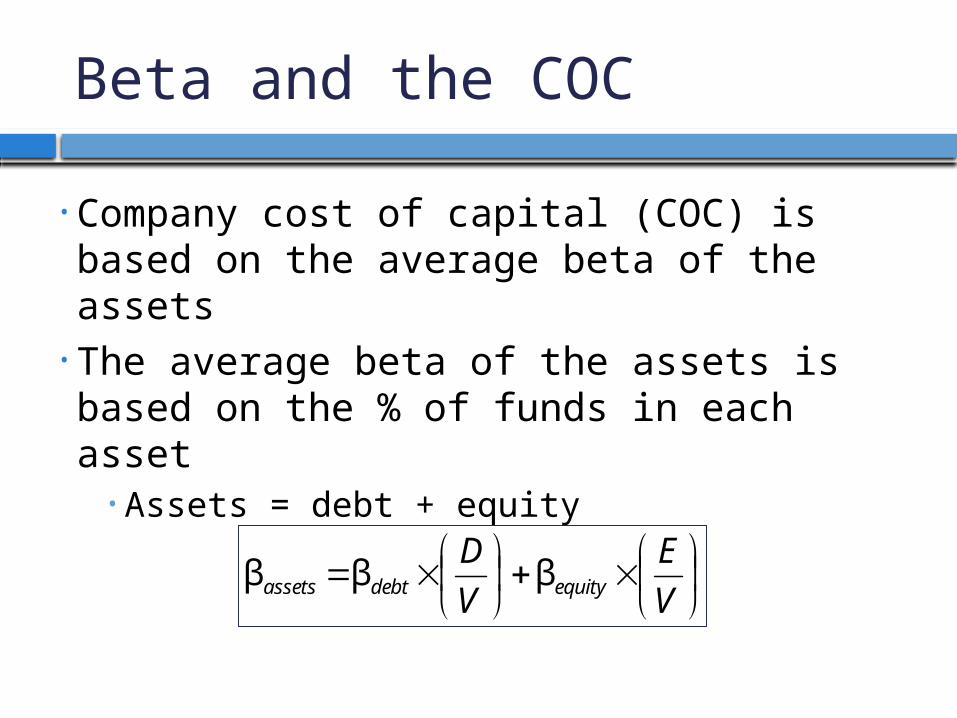

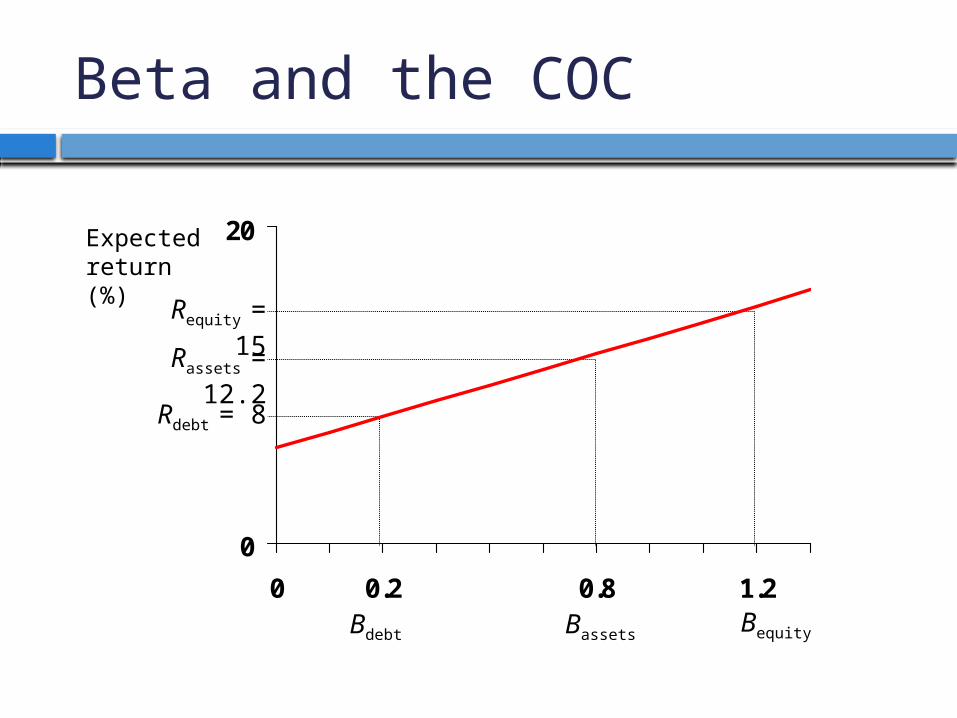

Beta and the COC

• Company cost of capital (COC) is based on the average beta of the assets

• The average beta of the assets is based on the % of funds in each asset• Assets = debt + equity

V

E

V

Dequitydebtassets βββ

0

20

0 0.2 0.8 1.2

Expected return (%)

Bdebt Bassets Bequity

Rdebt = 8

Rassets = 12.2

Requity = 15

Beta and the COC

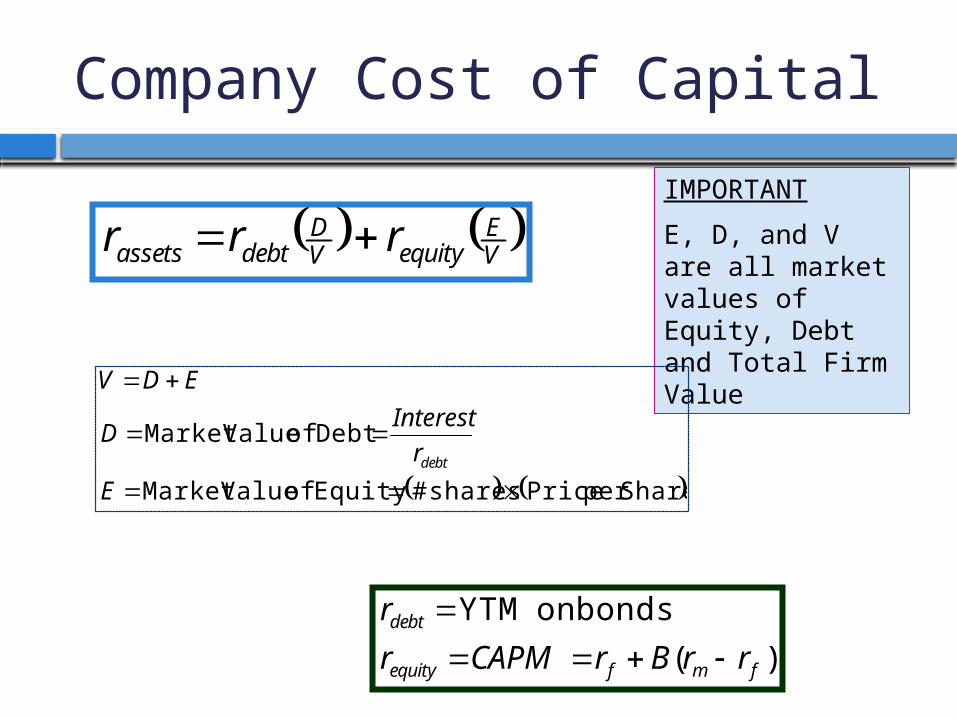

Company Cost of Capitalsimple approach

Company Cost of Capital (COC) is based on the average beta of the assets

The average Beta of the assets is based on the % of funds in each asset

Assets = Debt + Equity

equityequityDebtDebtassets rrr %%

COCCapital ofCost assetsr

IMPORTANT

E, D, and V are all market values of Equity, Debt and Total Firm Value

Company Cost of Capital

Shareper Price shares # Equity of ValueMarket

Debt of ValueMarket

E

r

InterestD

EDV

debt

VE

equityVD

debtassets rrr

)(

bondson YTM

fmfequity

debt

rrBrCAPMr

r

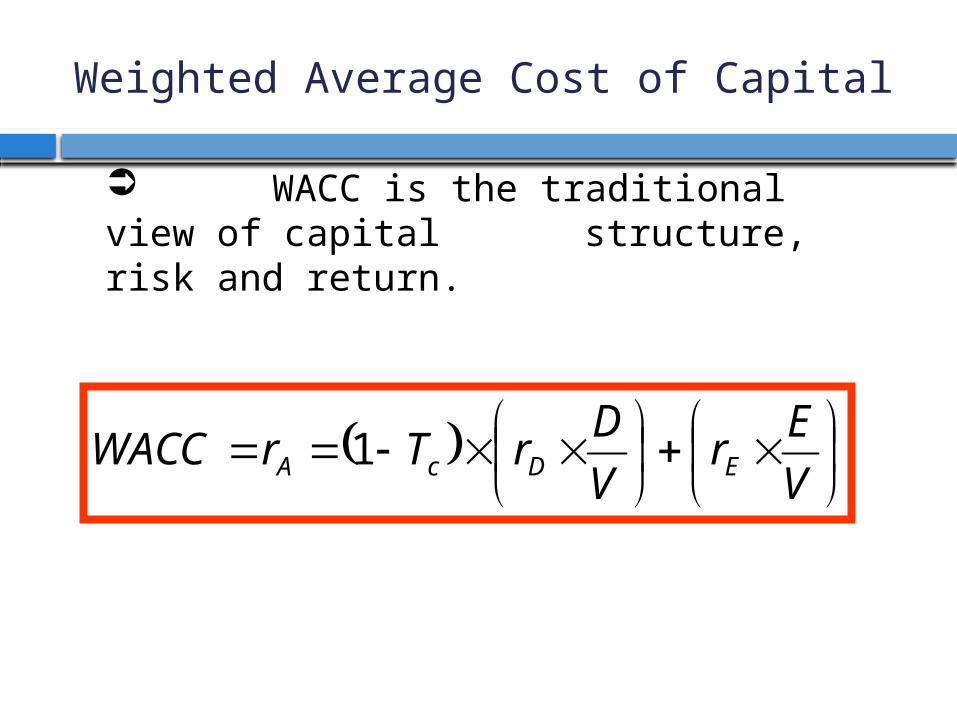

Weighted Average Cost of Capital

V

Er

V

DrTrWACC EDcA 1

WACC is the traditional view of capital structure, risk and return.

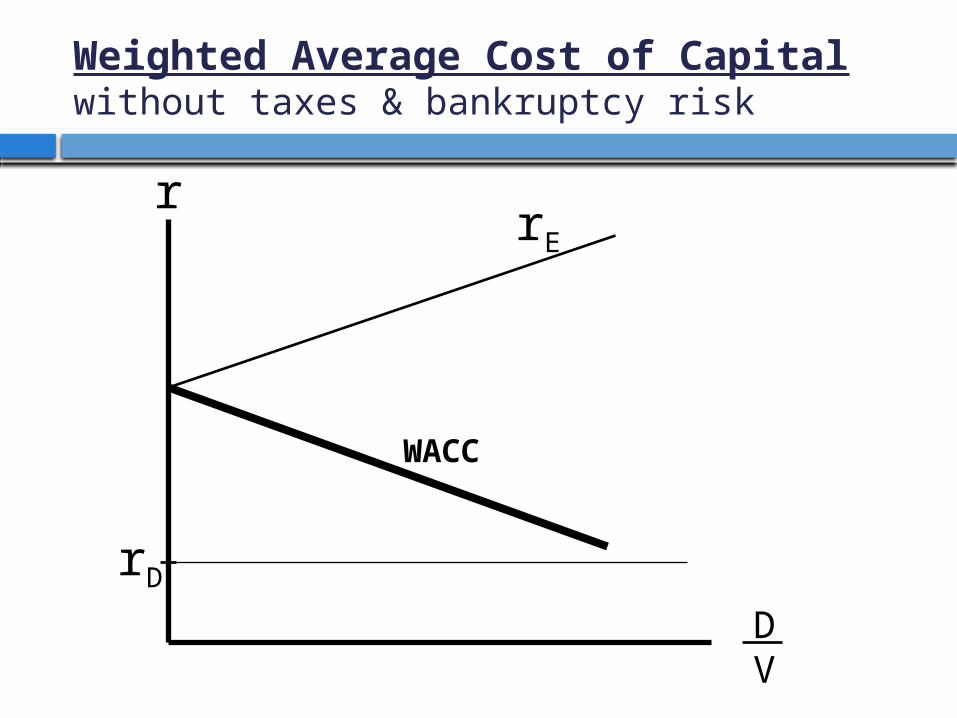

Weighted Average Cost of Capitalwithout taxes & bankruptcy risk

r

DV

rD

rE

r

DV

rD

rE

WACC

Weighted Average Cost of Capitalwithout taxes & bankruptcy risk

DV

rD

rE

Includes Bankruptcy Risk

Weighted Average Cost of Capitalwithout taxes & bankruptcy risk

r

r

DV

rD

rE

Weighted Average Cost of Capitalwithout taxes & bankruptcy risk

Includes Bankruptcy Risk

r

DV

rD

rE

WACC

Weighted Average Cost of Capitalwithout taxes & bankruptcy risk

Includes Bankruptcy Risk

r

DV

WACCr*

D*

Weighted Average Cost of Capitalwithout taxes & bankruptcy risk

Includes Bankruptcy Risk

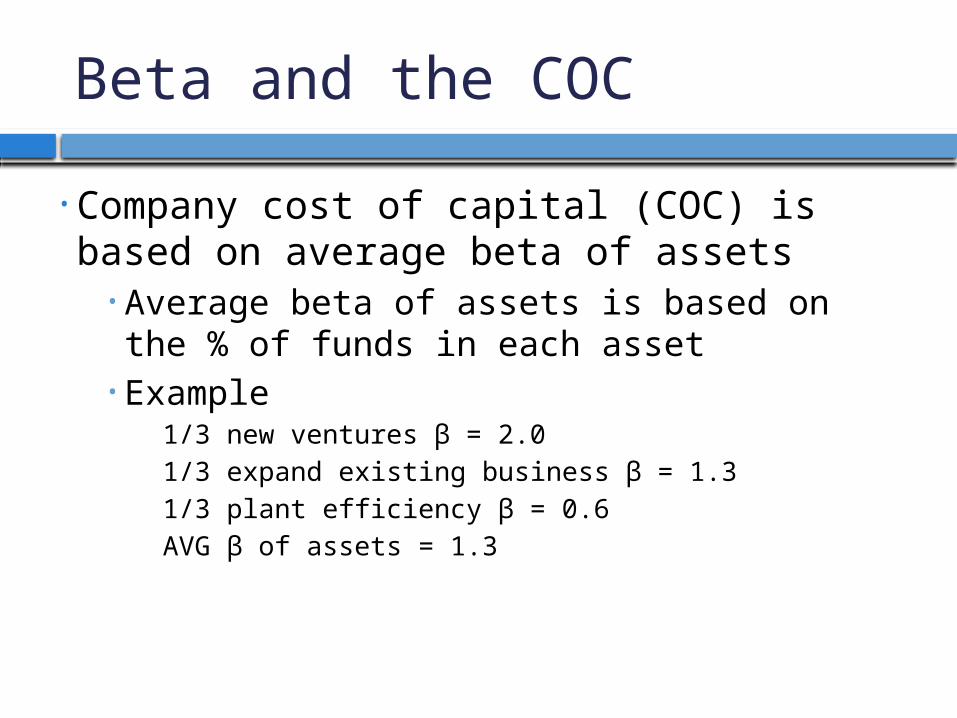

• Company cost of capital (COC) is based on average beta of assets• Average beta of assets is based on the % of funds in each asset

• Example1/3 new ventures β = 2.01/3 expand existing business β = 1.31/3 plant efficiency β = 0.6AVG β of assets = 1.3

Beta and the COC

• Company Cost of Capital

Beta and the COC

10%nologyknown tech t,improvemenCost

COC)(Company 15%business existing ofExpansion

20%products New

30% ventureseSpeculativ

RateDiscount Category

Project risk

Allowing for Possible Bad OutcomesExampleProject Z will produce one cash flow, forecasted at $1 million at year 1. It is regarded as average risk, suitable for discounting at 10% company COC:

100,909$1.1

000,000,1

1PV 1

r

C

Project risk

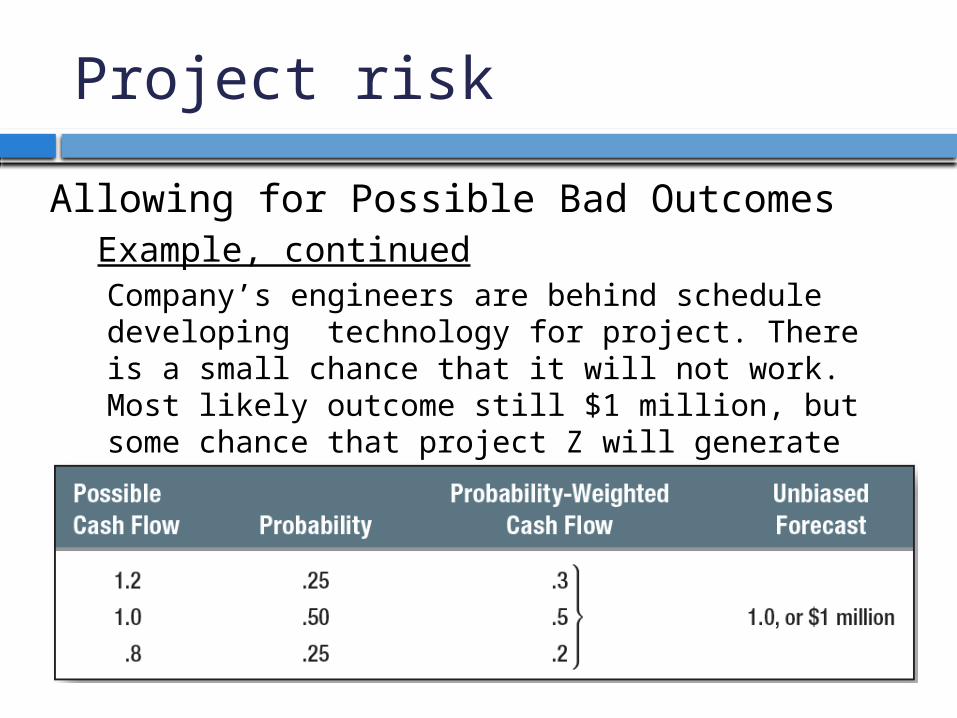

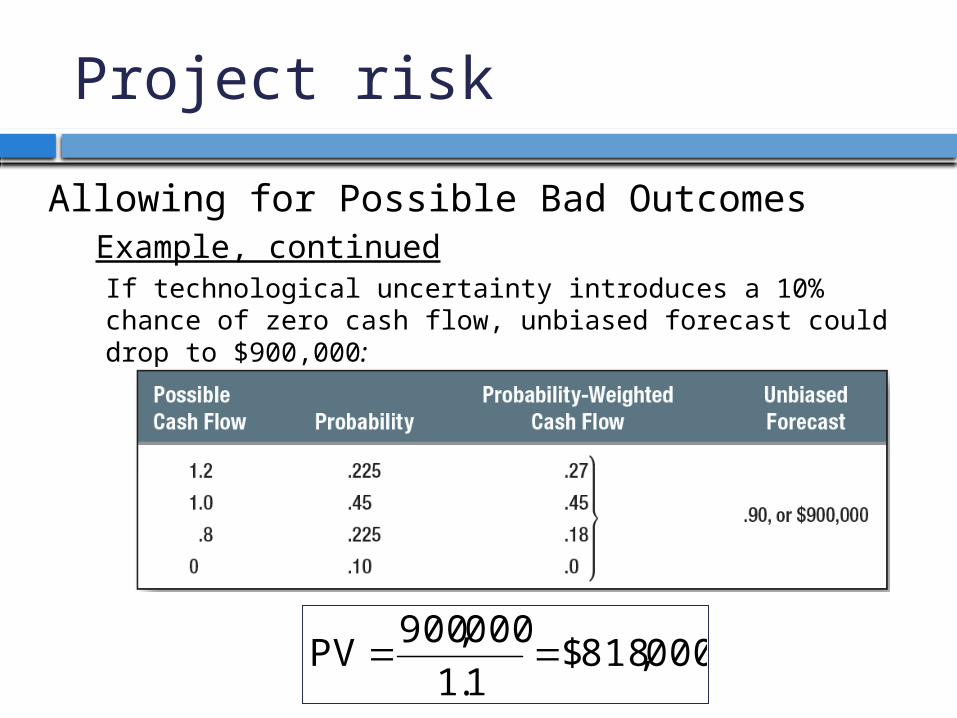

Allowing for Possible Bad OutcomesExample, continuedCompany’s engineers are behind schedule developing technology for project. There is a small chance that it will not work. Most likely outcome still $1 million, but some chance that project Z will generate zero cash flow next year:

Project risk

Allowing for Possible Bad OutcomesExample, continuedIf technological uncertainty introduces a 10% chance of zero cash flow, unbiased forecast could drop to $900,000:

000,818$1.1

000,900PV

Risk, DCF and CEQ

Risk, Discounted Cash Flow (DCF), and Certainty Equivalents (CEQ)

tf

tt

t

rr

C

)1(

CEQ

)1(PV

Risk,DCF and CEQ

ExampleProject A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project?

Risk,DCF and CEQ

Example

Project A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project?

%12

)8(75.6

)(

fmf rrBrr

Risk,DCF and CEQ

Example

Project A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project?

%12

)8(75.6

)(

fmf rrBrr

240.2 PVTotal

71.21003

79.71002

89.31001

12% @ PV FlowCashYear

AProject

Risk,DCF and CEQ

Example

Project A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project?

%12

)8(75.6

)(

fmf rrBrr

240.2 PVTotal

71.21003

79.71002

89.31001

12% @ PV FlowCashYear

AProject

Now assume that the cash flows change, but are RISK FREE. What is the new PV?

Risk,DCF and CEQ

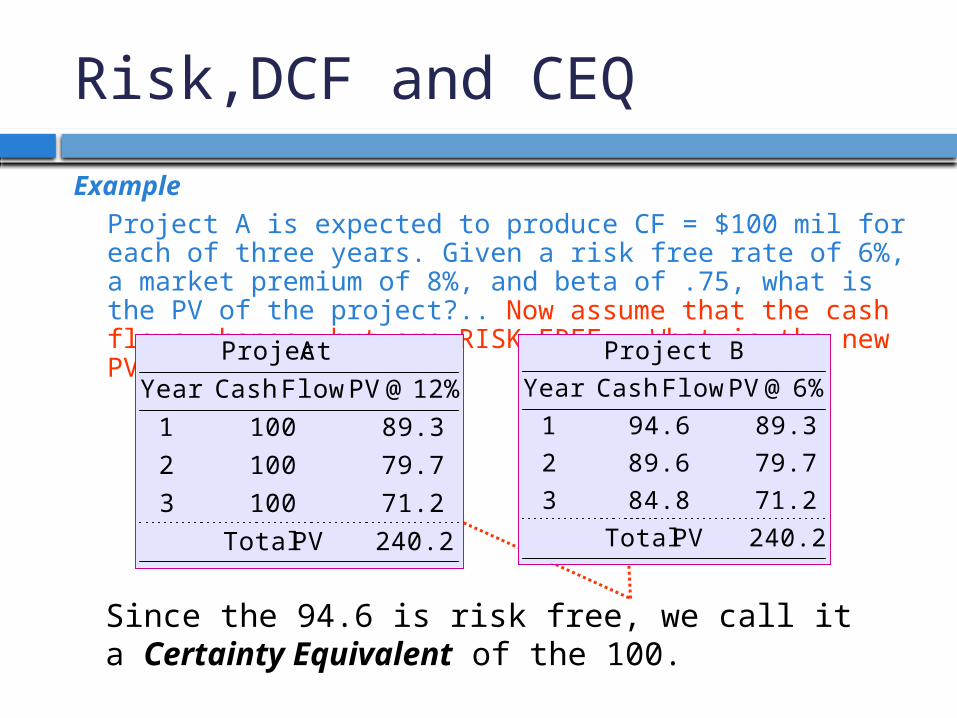

ExampleProject A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project?.. Now assume that the cash flows change, but are RISK FREE. What is the new PV?

240.2 PVTotal

71.284.83

79.789.62

89.394.61

6% @ PV FlowCashYear

Project B

240.2 PVTotal

71.21003

79.71002

89.31001

12% @ PV FlowCashYear

AProject

Risk,DCF and CEQ

ExampleProject A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project?.. Now assume that the cash flows change, but are RISK FREE. What is the new PV?

240.2 PVTotal

71.284.83

79.789.62

89.394.61

6% @ PV FlowCashYear

Project B

240.2 PVTotal

71.21003

79.71002

89.31001

12% @ PV FlowCashYear

AProject

Since the 94.6 is risk free, we call it a Certainty Equivalent of the 100.

Risk,DCF and CEQ

Example

Project A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project? DEDUCTION FOR RISK

15.284.81003

10.489.61002

5.494.61001riskfor

DeductionCEQFlowCash Year

Risk,DCF and CEQ

ExampleProject A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project?.. Now assume that the cash flows change, but are RISK FREE. What is the new PV?

The difference between the 100 and the certainty equivalent (94.6) is 5.4%…this % can be considered the annual premium on a risky cash flow

flow cash equivalentcertainty 054.1

flow cashRisky

Risk,DCF and CEQ

ExampleProject A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project?.. Now assume that the cash flows change, but are RISK FREE. What is the new PV?

8.84054.1

100 3Year

6.89054.1

100 2Year

6.94054.1

100 1Year

3

2

Capital Budgeting & Risk

Invest in highest NPV project

Need Discount rate to get NPV

Use CAPM to get discount rate

Modify CAPM (account for proper risk)

Modify Cash Flows

Capital Budgeting & Risk

Sensitivity Analysis - Analysis of the effects of changes in sales, costs, etc. on a project.

Scenario Analysis - Project analysis given a particular combination of assumptions.

Simulation Analysis (Monte Carlo) - Estimation of the probabilities of different possible outcomes.

Break Even Analysis - Analysis of the level of sales (or other variable) at which the company breaks even.

Decision Trees – Binomial model in which outcomes are path dependent.

Real Options – The value of flexibility.

Sensitivity Analysis

ExampleGiven the expected cash flow forecasts for Otobai Company’s Motor Scooter project, listed on the next slide, determine the NPV of the project given changes in the cash flow components using a 10% cost of capital. Assume that all variables remain constant, except the one you are changing.

Sensitivity Analysis

Example - continuedPossible Outcomes

bil 2bil 3bil 4Cost Fixed

275,000300,000360,000CostVar Unit

380,000375,000350,000priceUnit

.16.1.04ShareMarket

mil 1.1mil 1.0mil .9SizeMarket

OptimisticExpectedcPessimistiVariable

Range

Sensitivity Analysis

Example - continuedNPV Possibilities (Billions Yen)

6.53.40.4Cost Fixed

11.13.415.0-CostVar Unit

5.03.44.2-priceUnit

17.33.410.4-ShareMarket

5.73.41.1SizeMarket

OptimisticExpectedcPessimistiVariable

Range

Sensitivity Analysis

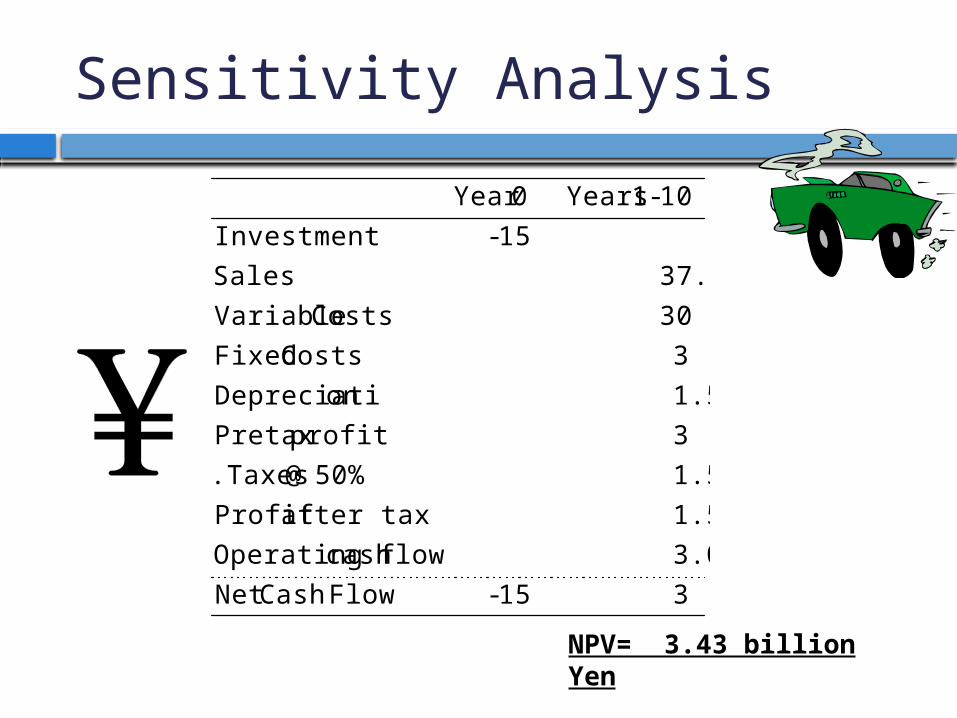

315- FlowCashNet

3.0flow cash Operating

1.5after taxProfit

1.550% @ .Taxes

3profitPretax

1.5onDepreciati

3Costs Fixed

30Costs Variable

37.5Sales

15-Investment

10-1 Years0Year

NPV= 3.43 billion Yen

Sensitivity Analysis

Example - continuedPossible Outcomes

bil 2bil 3bil 4Cost Fixed

275,000300,000360,000CostVar Unit

380,000375,000350,000priceUnit

.16.1.04ShareMarket

mil 1.1mil 1.0mil .9SizeMarket

OptimisticExpectedcPessimistiVariable

Range

Sensitivity Analysis

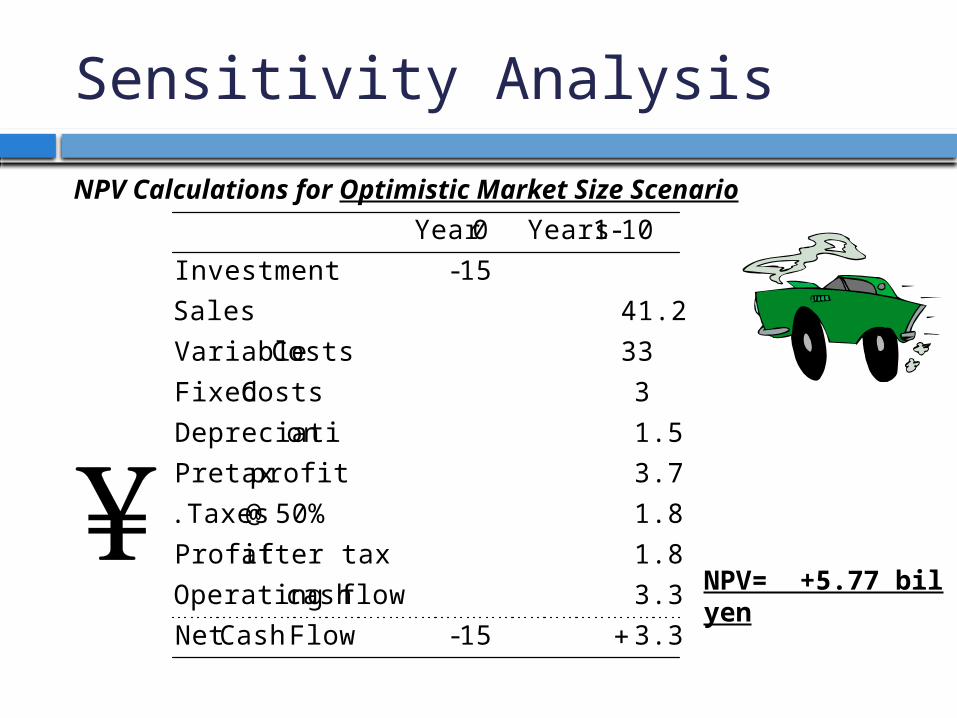

NPV Calculations for Optimistic Market Size Scenario

NPV= +5.77 bil yen

3.3815- FlowCashNet

3.38flow cash Operating

1.88after taxProfit

1.8850% @ .Taxes

3.75profitPretax

1.5onDepreciati

3Costs Fixed

33Costs Variable

41.25Sales

15-Investment

10-1 Years0Year

Sensitivity Analysis

Example - continuedNPV Possibilities (Billions Yen)

6.53.40.4Cost Fixed

11.13.415.0-CostVar Unit

5.03.44.2-priceUnit

17.33.410.4-ShareMarket

5.73.41.1SizeMarket

OptimisticExpectedcPessimistiVariable

Range

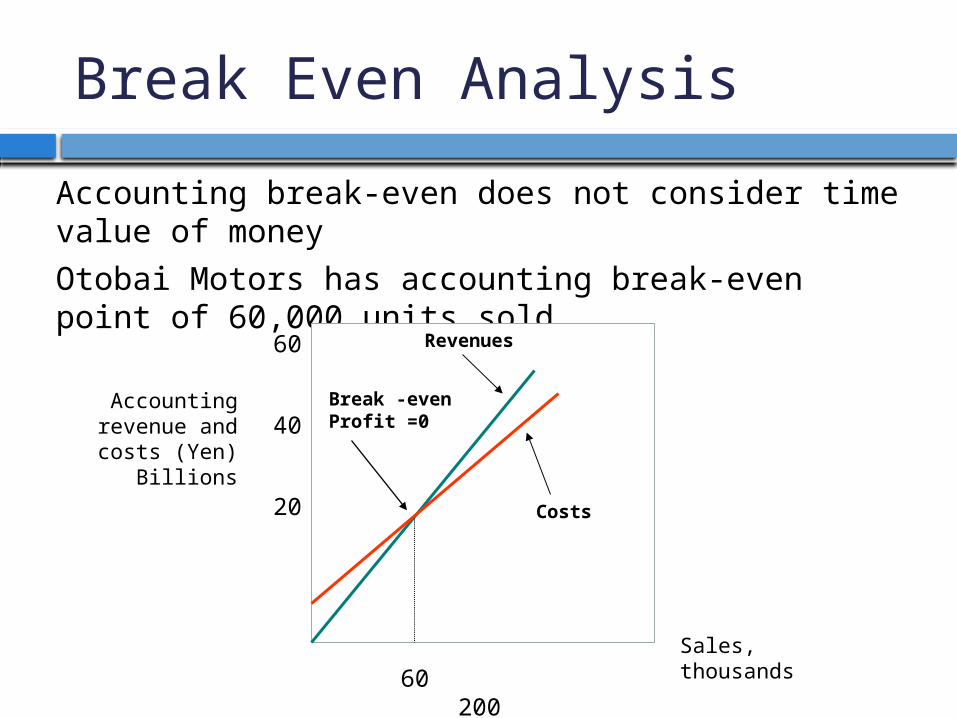

Break Even Analysis

Accounting break-even does not consider time value of money

Otobai Motors has accounting break-even point of 60,000 units sold

60 200

Sales, thousands

Accounting revenue and

costs (Yen)Billions

60

40

20

Break -evenProfit =0

Revenues

Costs

Break Even Analysis

Point at which NPV=0 is break-even point

Otobai Motors has a break-even point of 85,000 units sold

Sales, thousands

PV (Yen)Billions

400

200

19.6

85 200

Break-evenNPV = 0

PV inflows

PV Outflows

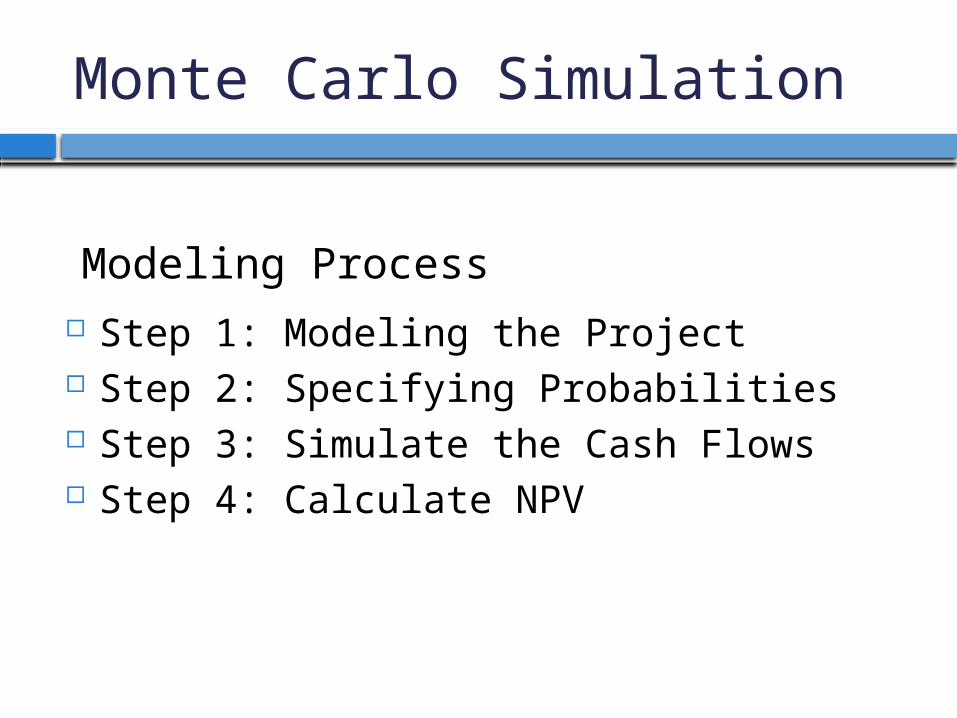

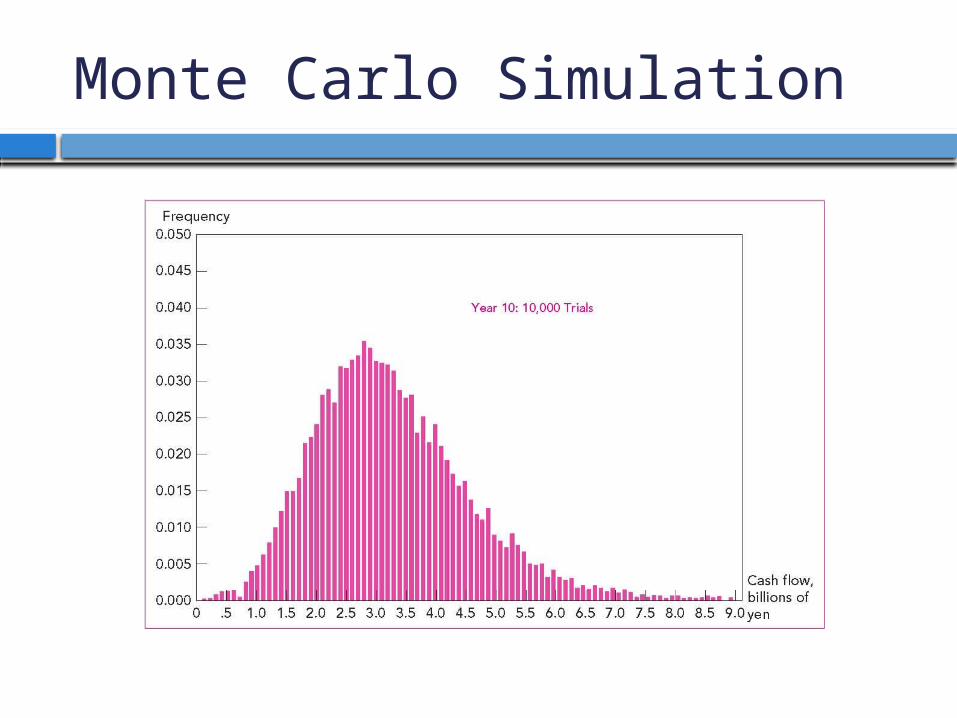

Monte Carlo Simulation

Step 1: Modeling the Project Step 2: Specifying Probabilities Step 3: Simulate the Cash Flows Step 4: Calculate NPV

Modeling Process

Monte Carlo Simulation

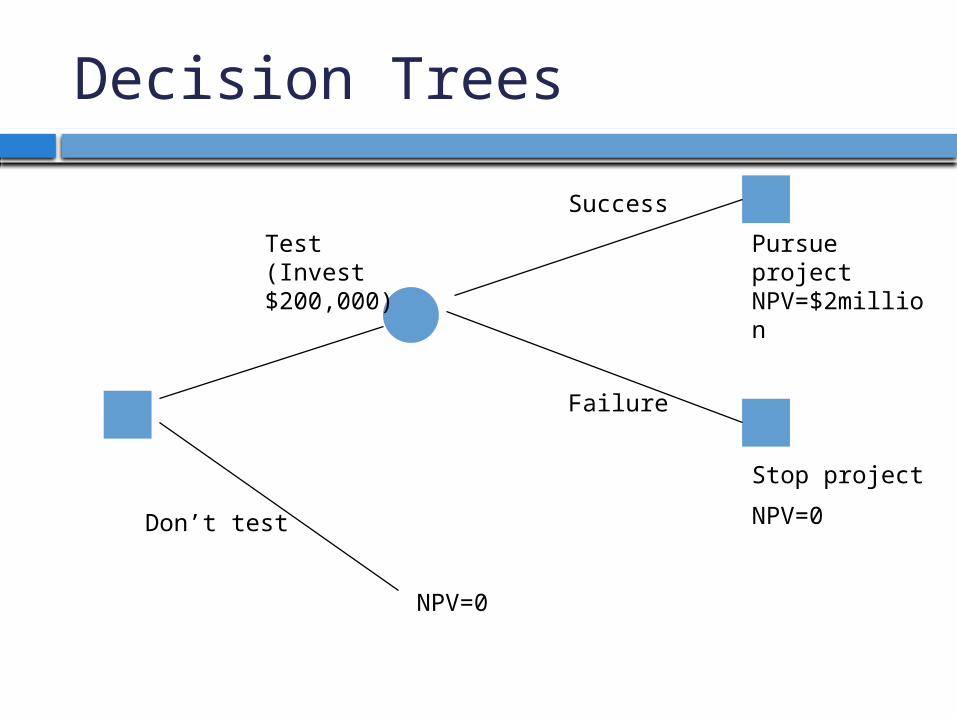

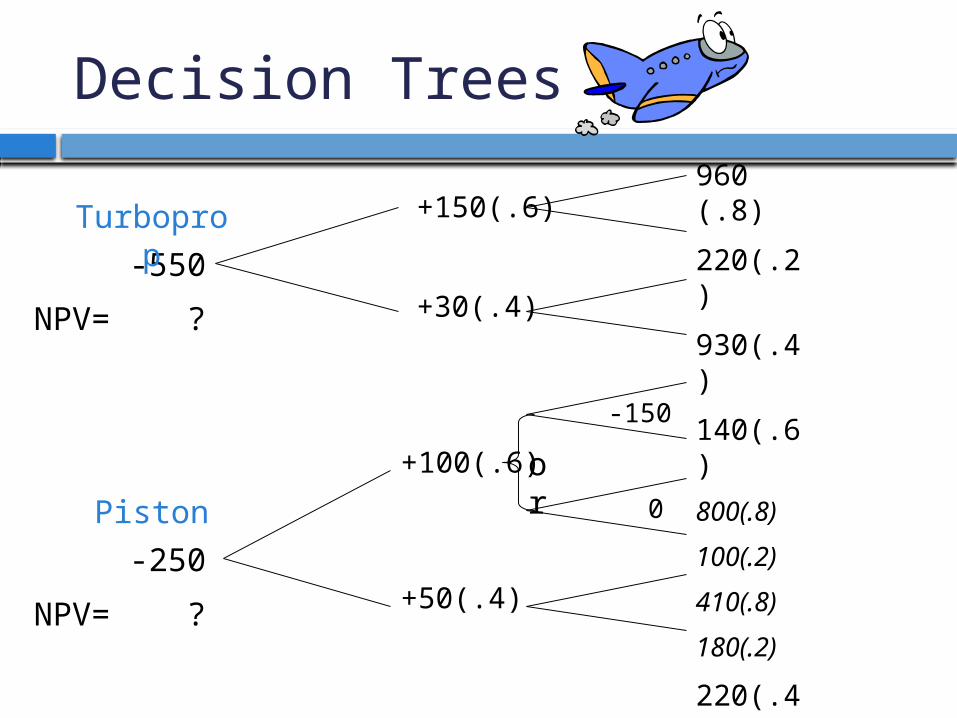

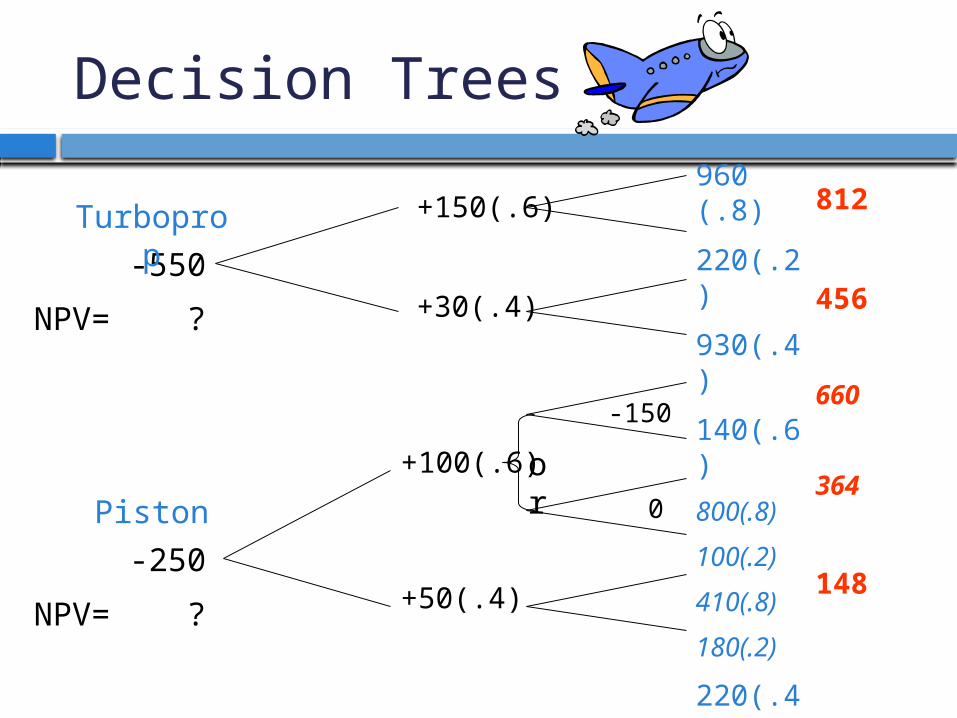

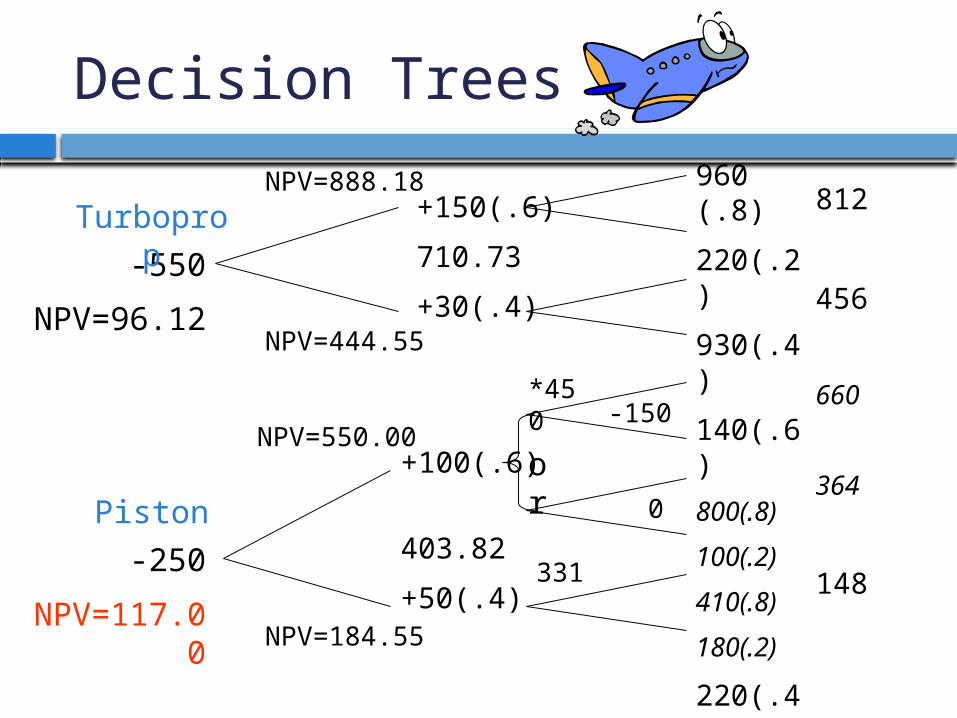

Decision Trees

NPV=0

Don’t test

Test (Invest $200,000)

Success

Failure

Pursue project NPV=$2million

Stop project

NPV=0

Decision Trees

960 (.8)

220(.2)

930(.4)

140(.6)

800(.8)

100(.2)

410(.8)

180(.2)

220(.4)

100(.6)

+150(.6)

+30(.4)

+100(.6)

+50(.4)

-550

NPV= ?

-250

NPV= ?

-150

0

or

Turboprop

Piston

Decision Trees

960 (.8)

220(.2)

930(.4)

140(.6)

800(.8)

100(.2)

410(.8)

180(.2)

220(.4)

100(.6)

+150(.6)

+30(.4)

+100(.6)

+50(.4)

-550

NPV= ?

-250

NPV= ?

-150

0

or

812

456

660

364

148

Turboprop

Piston

Decision Trees

960 (.8)

220(.2)

930(.4)

140(.6)

800(.8)

100(.2)

410(.8)

180(.2)

220(.4)

100(.6)

+150(.6)

+30(.4)

+100(.6)

+50(.4)

-550

NPV= ?

-250

NPV= ?

-150

0

or

812

456

660

364

148 81220.22080.960

Turboprop

Piston

Decision Trees

960 (.8)

220(.2)

930(.4)

140(.6)

800(.8)

100(.2)

410(.8)

180(.2)

220(.4)

100(.6)

-550

NPV= ?

-250

NPV= ?

-150

0

or

812

456

660

364

148

+150(.6)

+30(.4)

+100(.6)

+50(.4)

NPV=444.55

NPV=888.18

NPV=550.00

NPV=184.55

*450

331

18.88815010.1

812

Turboprop

Piston

Decision Trees

960 (.8)

220(.2)

930(.4)

140(.6)

800(.8)

100(.2)

410(.8)

180(.2)

220(.4)

100(.6)

812

456

660

364

148

+150(.6)

710.73

+30(.4)

+100(.6)

403.82

+50(.4)

-150

0

*450

331

or

NPV=444.55

NPV=888.18

NPV=550.00

NPV=184.55

-550

NPV= ?

-250

NPV= ?

40.55.44460.18.888

Turboprop

Piston

Decision Trees

960 (.8)

220(.2)

930(.4)

140(.6)

800(.8)

100(.2)

410(.8)

180(.2)

220(.4)

100(.6)

812

456

660

364

148

+150(.6)

710.73

+30(.4)

+100(.6)

403.82

+50(.4)

-550

NPV=96.12

-250

NPV=117.00

-150

0

*450

331

or

NPV=444.55

NPV=888.18

NPV=550.00

NPV=184.55

12.9655010.1

73.710

Turboprop

Piston

Decision Trees

960 (.8)

220(.2)

930(.4)

140(.6)

800(.8)

100(.2)

410(.8)

180(.2)

220(.4)

100(.6)

-550

NPV= ?

-250

NPV= ?

-150

0

or

812

456

660

364

148

+150(.6)

+30(.4)

+100(.6)

+50(.4)

*450

331

45015010.1

660Turboprop

Piston

Decision Trees

960 (.8)

220(.2)

930(.4)

140(.6)

800(.8)

100(.2)

410(.8)

180(.2)

220(.4)

100(.6)

812

456

660

364

148

+150(.6)

710.73

+30(.4)

+100(.6)

403.82

+50(.4)

-550

NPV=96.12

-250

NPV=117.00

-150

0

*450

331

or

NPV=444.55

NPV=888.18

NPV=550.00

NPV=184.55

Turboprop

Piston

Flexibility & Real Options

Decision Trees - Diagram of sequential decisions and possible outcomes.

Decision trees help companies determine their Options by showing the various choices and outcomes.

The Option to avoid a loss or produce extra profit has value.

The ability to create an Option thus has value that can be bought or sold.

Corporate Real Options

1. Option to expand (make follow up investment)

2. Option to abandon3. Timing option (wait and invest later)

4. Flexible production facilities

Value = NPV with option - NPV w/o option

Value = Black Scholes approach

Corporate Real Options

Example - AbandonMrs. Mulla gives you a non-retractable offer to buy your company for

$150 mil at anytime within the next year. Given the following decision tree of possible outcomes, what is the value of the offer (i.e. the put option) and what is the most Mrs. Mulla could charge for the option?

Use a discount rate of 10%

Corporate Real Options

Example - AbandonMrs. Mulla gives you a non-retractable offer to buy your company for

$150 mil at anytime within the next year. Given the following decision tree of possible outcomes, what is the value of the offer (i.e. the put option) and what is the most Mrs. Mulla could charge for the option?

Year 0 Year 1 Year 2

120 (.6) 100 (.6) 90 (.4)NPV = 145 70 (.6) 50 (.4)

40 (.4)

Corporate Real Options

Example - AbandonMrs. Mulla gives you a non-retractable offer to buy your company for

$150 mil at anytime within the next year. Given the following decision tree of possible outcomes, what is the value of the offer (i.e. the put option) and what is the most Mrs. Mulla could charge for the option?

Year 0 Year 1 Year 2

120 (.6) 100 (.6) 90 (.4)NPV = 162 150 (.4) Option Value =

162 - 145 =$17 mil

Corporate Real Options

Reality

• Decision trees for valuing “real options” in a corporate setting can not be practically done by hand.

• We must introduce binomial theory & B-S models