1 CORPORATE GOVERNANCE AND BOARD PRACTICES IN THE NIGERIAN BANKING INDUSTRY Chris Ogbechie* Lagos Business School PAN AFRICAN UNIVERSITY Km 22, Lekki-Epe Expressway, Lagos NIGERIA Tel: 002341 2711617-20 Fax: 002341 4616173 E-mail: [email protected]and Dr. Dimitrios N. Koufopoulos, Brunel Business School BRUNEL UNIVERSITY, Uxbridge, Middlesex UB8 3PH, UK Tel: (01895) 265250, Fax: (01895) 269775, E-mail: [email protected]January 2010

Transcript

1

CORPORATE GOVERNANCE AND BOARD PRACTICES IN THE NIGERIAN BANKING INDUSTRY

Chris Ogbechie* Lagos Business School

PAN AFRICAN UNIVERSITY Km 22, Lekki-Epe Expressway, Lagos

Chris Ogbechie holds a First Class Honours Bachelor’s degree in Mechanical Engineering from Manchester University and a Master’s Degree in Business Administration (MBA) from Manchester Business School. He is currently a Doctoral student in the Brunel Business School. His main research interests are on upper echelons theory, board effectiveness and corporate governance.

Dr. Dimitrios N. Koufopoulos (B.Sc, MBA, PhD, MCMI, FIMC) is Senior Lecturer in the Brunel Business School. His work has appeared in the European Marketing Academy Conference, British Academy of Management and Strategic Management Society proceedings and in various journals like Long Range Planning Journal, Journal of Strategic Change and Journal of Financial Services Marketing, Corporate Ownership and Control and Corporate Board. His research interests are on strategic planning systems, top management teams, corporate governance and corporate strategies.

3

ABSTRACT

This study evaluates corporate governance issues in Banks operating in Nigeria that deals with board characteristics, composition, operations and processes, and as well as their degree of compliance with Central bank of Nigeria Code of Corporate Governance,

The empirical findings of the study reveal useful insights with respect to Corporate Governance Practices in Banks operating in Nigeria. The results show that Nigerian Banks have embraced the principles of good Corporate Governance and have achieved high degree of compliance with the Central Bank of Nigeria Code of Corporate Governance.

This paper draws a number of conclusions and recommendations and also highlights some limitations that can be improved upon in future studies.

The issues of corporate governance continue to attract considerable national and international

attention and have again appeared at the top of the agenda with the current global financial

meltdown. Corporate governance is about effective, transparent and accountable governance

of affairs of an organization by its management and board. It is about a decision-making

process that holds individuals accountable, encourages stakeholder participation and

facilitates the flow of information. The ongoing global financial crisis has further reinforced

the message that governance of firms, especially of financial institutions, should always aim

at protecting the interests of all stakeholders, which include shareholders, depositors,

creditors, regulators and the public.

The corporate governance of financial service sector and more specifically of banks in

developing economies has been almost ignored by researchers (Caprio and Levine, 2002).

Even in developed economies, the corporate governance of this sector has only recently been

discussed in the literature (Macay and O’Hara, 2001).

The corporate governance of banks in developing economies is important for several reasons.

First, banks have an overwhelmingly dominant position in the financial systems of

developing economies, and are extremely important engines of economic growth (King and

Levine 1993 a, b). Second, banks in these developing economies are typically one of the most

important sources of finance for the majority of firms. Third, banks in developing countries

are the main depository for the economy’s savings and provide the means for payment.

Given the importance of banks, their governance now assumes a central role in view of the

peculiar contractual form of banking, corporate governance mechanisms for banks should

encapsulate depositors and shareholders.

5

There is substantial evidence to show the positive link between finance sector development

(FSD), and economic growth and poverty reduction (King and Levine, 1993; Levine and

Zervos, 1998; and Rajan and Zingales, 1998). The Nigerian banking industry therefore has a

significant role to play in the development of the country’s economy. Banks have been the

main sources of financing in the Nigerian financial market and bank loans were the

predominant sources of debt financing in the economy (Central Bank of Nigeria Annual

Report 2006).

Corporate governance is particularly important in the Nigerian banking industry because a

number of recent financial failures, frauds and questionable business practices had adversely

affected investors’ confidence. In 1995 several CEOs and directors of banks in Nigeria where

arrested for non-performing loans that were given to themselves, relations and friends. Some

of the banks that could not meet the Central Bank of Nigeria (CBN) recapitalization

requirement in 2006, where found to be saddled with non-performing loans that were given to

directors and their friends. The financial health and performance of banks are important for

the economic growth of Nigeria. This is why the regulator of the industry in Nigeria, a result,

As a result,the Central Bank of Nigeria, had decided to reform the industry in order to

achieve global competitiveness.

The corporate governance landscape in Nigeria has been dynamic and has generated interest

from within and outside the country. In 2003, the Nigerian Securities and Exchange

Commission (SEC) adopted a Code of Best Practices on Corporate Governance for publicly

quoted companies in Nigeria and this code is currently being reviewed. At the end of the

consolidation exercise in the banking industry, the CBN, in March 2006, released the Code of

Corporate Governance for Banks in Nigeria, to complement and enhance the effectiveness of

the SEC code, which was implemented at the end of 2006. The three major governance issues

6

that attracted the attention of the regulators are directors’ dealings, conflict of interest and

creative accounting.

LITERATURE REVIEW

Boards and Corporate Governance

Effective corporate governance practices are essential to achieving and maintaining public trust and confidence in the banking system, which are critical to proper functioning of the banking sector and the economy of a country as a whole. Poor corporate governance may contribute to bank failures, which could in turn lead to a run on the bank, unemployment and negative impact on the economy (Basel Committee, 1999). In addition, problems or failures of banks are likely to rapidly expand and have a disproportional adverse impact on the smooth operation of the financial system of a country (Allen & Herring, 2001; Sbracia & Zaghini, 2003). The board of directors has a significant role to play in ensuring good corporate governance in the bank and at the heart of the corporate governance debate is the view that the board of directors is the guardian of shareholders’ interest (Dalton et.al., 1998). Boards are being criticized for failing to meet their governance responsibilities. Major institutional investors put pressure on (incompetent) directors and have long advocated changes in the board structure (Monks and Minow, 2001). Their call has been strengthened by many corporate governance reforms resulting from major corporate failures. These reforms put great emphasis on formal issues such as board independence, board leadership structure, board size and committees (Van den Berghe and De Ridder, 1999; Weil, Gotshal and Manges, 2002). These structural measures are assumed to be important means to enhance the power of the board, protect shareholders’ interest and hence increase shareholder wealth (Westphal, 1998; Becht et.al., 2002). Structural measures (board characteristics) are not sufficient to understand the workings of boards and Zahra and Pearce (1989) argued that there is “a growing awareness of the need to understand better how boards can improve their effectiveness as instruments of corporate governance”.Board Characteristics and Corporate Governance

Board characteristics refer to size, the division of labour between the board chair and the

CEO, and finally its composition and diversity.

Board Size refers to the total number of directors on the board of any corporate organization.

Determining the ideal board size for an organization is very important because the number

and quality of directors in a firm determines and influences the board functioning and hence

corporate performance. Proponents of large board size believe it provides an increased pool

7

of expertise because larger boards are likely to have more knowledge and skills at their

disposal. They are also capable of reducing the dominance of an overbearing CEO (Forbes

and Milliken, 1999) and hence put the necessary checks and balances. Board’s monitoring

and supervising capacity is increased as more and more directors join the board (Jensen,

1993). Besides, there are authors who believe that large board size adversely affects the

performance and well being of any firm. Larger boards are difficult to coordinate, and are

very prone to fictionalizations and coalitions that will delay strategic decision making

processes (Forbes and Milliken, 1999).

Board Leadership structure is another critical aspect of board structure. In the independent

structure two individuals serve in the roles of CEO and Board chairperson. A situation in

which these roles are held by one individual is called CEO duality (Dalton, 1993).

Shareholders activist groups are against CEOs serving simultaneously as chairperson of the

board and some researchers also posited the same (Dobrzynski, 1991; Levy, 1993b; Cadbury,

1992; Goodstein et al, 1994). Due to agency theory anxiety over management domination of

the board, there is predilection for the separate board leadership structure (Dalton et al, 1998).

According to agency theory, duality structure can lead to entrenchment by the CEO, thereby

reducing the monitoring effectiveness of the board (Finkelstein and D’Aveni, 1994) and

inability to enforce good governance practices.

Board Composition refers to the distinction between inside and outside directors, and this is

traditionally shown as the percentage of outside directors on the board (Goergen and

Renneboog, 2000). For Baysinger and Butler (1985), composition may be easily

differentiated into inside directors, affiliate directors and outside directors. Inside directors

are those directors that are also managers and/or current officers in the firm while outside

8

directors are non-manager directors. Among the outside directors there are directors who are

affiliate, and others that are independent. Affiliate directors are non-employee directors with

personal or business relationship with the company while independent directors are those that

have neither personal nor business relationships with the company. Although inside and

outside directors have their respective merits and demerits, many authors favour outside-

dominated boards (Pablo et al, 2005). Outside directors provide superior performance

benefits to the firm as a result of their independence from firm’s management (Baysinger and

Butler, 1985). They can increase the element of independence and objectivity in board’s

strategic decision-making, and also help in providing independent supervision of the

company’s management (Fama and Jensen, 1983), hence making the board’s oversight

function more effective.

Board Diversity is defined as a concept used to depicts the varied personal characteristics that

make the workforce heterogeneous (DeCenzo and Robbins, 2005). So board diversity can be

said to be those varied personal characteristics and physical differences in people who are

members of the board that make the board heterogeneous. For boards to be effective there is

need for diverse perspective in the board to confront the thinking of management.

The promotion of diverse perspectives in a board can generate a wider range of solutions and

decision criteria for strategic decisions (Eisenhardt and Bourgeois, 1988; Goodstein et al,

1994; Kosnik, 1990). In the same vein corporate governance scholars believe that board

diversity can directly or indirectly impact firms (Kosnik, 1990).

Board Processes and Corporate Governance

9

A growing number of research works is now moving away from the organisational outcomes of

board structure and characteristics to greater focus on board processes and functions. Indeed, a

growing number of studies suggest that the agency framework should be used in conjunction

with complementary theories (Daily et al. 2003; Pettigrew 1992), including behavioural

(Hambrick and Mason 1984; Sanders and Carpenter 2003) and socio-cognitive research

(Carpenter et al. 2003; Carpenter and Sanders, 2002) in examining governance-related issues.

Whilst board structure conditions board effectiveness, it is the behavioural dynamics of a board

and the web of interpersonal and group relationships between executive and independent

directors that determine board effectiveness (Roberts et al. 2005). Therefore, ‘good’ corporate

governance drivers may also be associated with factors that affect board dynamics and

interrelationships, such as the role of a Chairperson, information flows inside and outside the

firm, coalition formation, etc.

An unrestricted access to information is generally regarded as a source of directors’ power, as

well as directors’ in-depth knowledge of the business (Golden and Zajac 2002; Roberts et al.

2005; Useem 1993; Westphal 1999). This will ensure a more effective oversight function.

Other factors such as the board meeting agenda, the process and conduct of board meetings,

and process of open debate may increase board effectiveness (McNulty and Pettigrew 1999,

Pye 2002).

Boards require a high degree of specialized knowledge and skill to function effectively. The

knowledge and skills most relevant to boards are in two dimensions, functional area

knowledge and skills and firm-specific knowledge and skills. Functional area knowledge and

skills include accounting, finance, marketing, and law. Board members can either possess

10

these skills or have access to external networks that can provide them. Firm-specific

knowledge and skills refer to detailed information about the firm and an intimate

understanding of its operations and internal management issues. Boards often need this kind

of “tacit” knowledge (Nonaka, 1994) in order to deal effectively with strategic issues.

If boards are to perform their control tasks effectively, they must integrate their knowledge of

the firm with their expertise in the business areas. In addition, if boards are to perform their

service tasks effectively, they must be able to combine their knowledge of various functional

areas and apply that knowledge properly to firm-specific issues.

Board Culture and Corporate Governance

Board culture is a system of informal, unwritten, yet powerful norms derived from shared

values that influence behaviour (Nadler, 2004). Every board of directors creates a

governance culture which is referred as a pattern of belief, traditions and practices that

prevail when the board convenes to carry out their duties (Prybil, 2008).

Board must develop a culture of accountability and engagement (Reed 2003). Board leaders

should pay strict attention to how much board time is spent passively listening to reports and

how much time is spent discussing strategic issues and the duties of care and loyalty. Active

and vigorous board discussion, debate and questioning is not only a sign of a good board, it is

the sign of an engaged board. An open culture of cooperation and transparency is healthy and

will ensure good governance practices.

11

It is believed that effective governance requires a proactive culture of commitment and

engagement that drives both the board and the organization it governs toward high

performance. Engaged cultures are characterized by honesty and a willingness to challenge,

and they reflect the social and work dynamics of a high-performance team (Nadler, 2004).

The oversight role and responsibilities of boards require them to make many decisions that

shape the organization and its direction. The way in which a board move toward its decision

making processes is a basic part of its culture and has a major impact on the organization’s

performance (Useem, 2006).

Strategic Process Involvement and Corporate Governance

The board of directors performs the pivotal role in any system of corporate governance. It is

accountable to the stakeholders and directs and controls the management. It stewards the

company, sets its strategic aim and financial goals, and oversees their implementation, puts in

place adequate internal controls and periodically reports the activities and progress of the

company in a transparent manner to the stakeholders.

Tregoe and Zimmermann (1980) define strategy as the framework, which guides those

choices that determine the nature and direction of an organization. In line with Tregoe’s

(1980) definition, strategic decisions are those decisions that border on the long-term thrust

and direction of any organization. Creating a vision, mission and values; developing

corporate culture and climate; positioning in the dynamic market; setting corporate direction,

reviewing and deciding key corporate resources; deciding on implementation model and

processes etc are all part of the strategic activities or decisions that the board uses in driving

or directing the thrust of an organization’s future, particularly in the long-run (Garratt, 1996;

Pearce and Zahra, 1991). More specifically, Goodstein et al (1994) submitted that the

12

strategic role of the board is that of taking important decisions on strategic changes that help

the organization adapt to important environmental changes.

Board Relationships with CEO and Top Management and impact on Corporate Governance

At the heart of any CEO-Board relationship is the need to acquire, control, or coordinate the

flow of information. Some researchers have noted that the CEO may influence the board

through selective use of information, control over board’s agenda, and personal persuasion

through access to key board members (Zald, 1969; Mace, 1971) and this could have an

adverse effect on the board’s oversight function.

For good corporate governance, it is important that the CEO does not dictate the agenda for

the board and control the outcomes of board decisions. The CEO should not be a member of

key board committees, and not participate in the selection of new board members (Jeffrey et

al, 1993).

Analysts have shown that one of the most important CEO-Board relationships is independent

monitoring and control. Independent monitoring and control are better provided by the true

independent directors who, most times use control function to protect the interest of all the

firm’s stakeholders. The extent to which this control function is applied determines the type

of relationship that exists between the CEO and the board of directors (particularly the

independent directors). In some cases, it produces negative relationship characterized by lack

of mutual understanding and distrust.

Boards of directors, in performing their oversight role, are expected to supervise the actions

of management, provide advice, and veto poor management decisions (Fama, 1980; Jensen,

1986). In their control capacity, boards of directors are also responsible for removing

13

ineffective management. The propensity to engage in such actions however, is often a

function of influence relationship, cognition about performance, and/or political action than

of boards’ actual effectiveness as a rational management control system (Mace, 1971;

Baysinger and Hoskisson, 1990).

According to agency perspective, while top managers are responsible for on-going decision

management, the board of directors is responsible for decision control which involves

monitoring and evaluating management decision making and performance (Fama & Jensen,

1983). This in effect implies that the board is an efficient control device that can help align

management decision making with shareholders’ interests (Beatty and Zajac, 1994).

Board Evaluation and Corporate Governance

Tricker (1999a) argues that just as professionalism in management today calls for assessment,

performance reviews, and training and development, so too should directors be evaluated.

Although advocates of corporate governance plead for a formal board and director

evaluation, this is still a bridge too far for most boards of directors. Several studies indicate

that it is still relatively unusual for boards to undertake an evaluation of their performance

both as a board and as individual directors, and that few boards carry out independent,

external review (Blake, 1999; Davies, 1999). Steinberg (2000) notes that fewer than 20

percent of US boards evaluate themselves as a board or appraise the performance of

individual directors. Van der Walt and Ingley (2001), from their research among boards of

New Zealand companies found that 86 percent claimed to carry out some kind of review. Van

den Beghe & Levrau (2004), argue that only a small number of companies evaluate the

performance of the entire board and that individual evaluation is also exceptional and occurs

mainly if a director stands for re-election.

14

Board appraisals could be rationalized on the basis that they assist in identifying weaknesses

and thereby helping boards and their members to enhance their performance. These will also

help to develop a board or director development programme for capabilities and so close

identified gaps in performance. Evaluations provide the opportunity to define the current and

future role of the board and an opportunity to determine if the associated skills of the board

and its members were appropriate (Van der Walt & Ingley, 2001).

Evaluations can help directors assess their performance over time as needs of a board shift,

and provide a basis for deciding whether a director should be reappointed. These evaluations

demonstrate to investors that the board is holding individual directors accountable for their

performance (Conger and Lawlor III, 2002).

It is apparent that developing meaningful evaluations as a tool for enhancing board, director

and organizational performance presents a significant challenge in terms of overcoming

resistance and gaining credibility and acceptance for the process.

Dilenschneider (1996), argues that the challenge in coming up with effective substantive

measures of directors’ performance requires a more sophisticated approach, including less

objective interpersonal factors such as teamwork, director selection and value contributed by

board members. Along with function and process, therefore, competence and interpersonal

dynamics should be included in the appraisal model. While such behavioural factors are more

difficult aspects to quantify, they are frequently vital in determining board effectiveness

(Staff, 2000).

15

How often board evaluation should be conducted is another crucial matter for consideration.

While some authors favour annual review or evaluation (because it is usually consistent with

the planning cycle adopted by most boards), others recommend that board evaluation should

be done every six months (biannual). There are also authors who believe that board

evaluation should be an on-going process, and not just an annual event (Carver, 1997a).

This paper evaluates the state of corporate governance in Nigerian Banking sector in terms of

compliance with the Central Bank of Nigeria (CBN) corporate governance guidelines and

global best practices. It also looks at the practices of the board in achieving good corporate

governance in their banks.

RESEARCH METHODOLOGY

Research Objectives

The main objectives of the research are to:

• Evaluate the level of compliance of the CBN corporate governance guidelines amongst

Nigerian banks.

• Understand the following corporate governance issues in the Nigerian banking industry:

o The composition and procedures followed by the board of directors.

o Issues upon which the board of directors is/should be appraised.

o The involvement of the board of directors with the bank’s strategy development.

o Board relationship with the top management team and the CEO.

o Directors views regarding the future development of corporate governance.

Significance of the Research

16

Nigeria cannot afford to have an under-performing banking industry, which is seen as the

heartbeat of the economy. Since the banking industry in Nigeria has undergone many recent

changes, understanding the governance of Nigerian banks is arguably more important than

ever before. The practice of good corporate governance makes a bank to conduct its business

in an ethical way. This builds a good reputation for the bank and makes investors always

willing to invest in it. This is important as about 22 of the 24 banks in Nigeria are now

publicly quoted in the Nigerian Stock Exchange. In addition, if Nigerian banks are perceived

to have imbibed international best practices in corporate governance, they will be in good

positions to attract more foreign capital and at the same time be strongly positioned to operate

in foreign markets.

A sound banking industry will be in a strong position to drive the economic reforms of the

Federal Government of Nigeria and provide the support to grow the private sector.

Most of the 22 Nigerian banks now publicly quoted transformed from private banks to public

banks. It is important to find out how this transformation is being handled on the governance

side.

The Nigerian Banking Industry

In 2005, there were 89 deposit banks operating in a highly concentrated market with the top

ten banks accounting for over 80 per cent of the total assets/liabilities. The statutory

capitalization requirement was N2 billion and the small size of these banks had an adverse

effect on their cost structure thus making the cost of intermediation high. The total

capitalization of all Nigerian banks then stood at N293 billion, which was just the size of the

fourth largest bank in South Africa. As a result Nigerian banks were unable to finance major

17

transactions in the growing oil and gas, and telecom sectors, which constitute the fastest

growing sectors in the Nigerian economy.

Prior to 2005, the Nigerian banking system could not deliver on its defined roles and was

characterized by:

- Low aggregate banking credit to the domestic economy (18.4% as percentage of

GDP)

- Systemic crisis – banks were frequently out of clearing

- Inadequate capital base

- Oligopolistic structure – 10 out of 89 banks accounted for over 80% of total banking

system assets

- Gross insider abuses that resulted in huge non-performing insider related activities

- Over dependency on public sector deposits

- Poor corporate governance

- Low banking/population density – 1: 30,432

- Payment system that encouraged cash-based transactions.

These factors led the Central Bank of Nigeria (CBN), in 2004, to undertake a massive

transformation of the banking industry to achieve the following objectives (CBN Report

2006):

• Establish a banking system that will rapidly drive Nigeria’s economic growth and

development.

• Integrate the Nigerian banking system into the global financial system.

• Target at least one Nigerian bank in the top 100 banks in the world within 10 years.

• In the long term make Nigeria Africa’s financial hub.

18

As a first step in actualizing these goals, the CBN on July 6, 2004 announced that all banks

operating in Nigeria should have a minimum capitalization of N25 billion on or before

December 31, 2005. This recapitalization could be achieved by either injection of new funds

or mergers and acquisitions.

The outcomes of the transformation have been impressive. At the end of the consolidation

exercise, the number of banks reduced from 89 to 25 as at January 2006. By the end of

February 2008, there were 11 banks with over $1 billion in tier 1 capital; several Nigerian

banks are operating in 16 African countries and in 7 other countries outside Africa. As at

2007, the total branch network was about 3,900 as against 2,600 in 2005. These banks are

universal banks offering all banking services and product range to corporate and individual

customers. Twenty two of these banks are publicly owned and listed on the Nigerian Stock

Exchange (NSE).

The banking business is based on trust and public confidence and as such it is important to

enthrone good corporate governance practices in the industry. In Nigeria the banking industry

is very critical to the country’s economic growth because of its role in the mobilization of

funds, the allocation of credits to the various sectors of the economy, the payment and

settlement system, and the implementation of monetary policy. Effective corporate

governance practices are therefore essential in achieving and maintaining public trust and

confidence in the banking sector.

Research Methodology

The research study was undertaken, between September 2007 and June 2008, to understand

and assess corporate governance practices in the Nigerian Banking Industry.

19

The methodology used in this research included a combination of questionnaires and

interviews:

It also included interviews with two officials of the Central Bank of Nigeria, the regulatory

body of the banks.

Structured questionnaires were mailed to the chairpersons and directors of all banks in

Nigeria in October 2007, accompanied by a personalized letter. Follow up phone calls and

additional reminder mail wave were carried out between January and March 2008. About 250

questionnaires were sent out and a total of 110 responses were received. Only 2 of the

responses were discarded for not being properly completed. 108 responses were valid and this

represents 43.2 percent response rate.

Measurements

Independent variables: Board size was measured by the absolute number of directors

(Dedman, 2000). Board composition was operationalised as the percentage of outside

directors on the board (Udueni, 1999). Board leadership structure is a binary variable coded

as “0” for those firms employing the separate board structure and “1” for those employing the

joint structure. The diversity of the board was captured by counting number of directors that

have similar background.

Dependent variables: A 7-point Likert scale from “strongly disagree” to “strongly agree” was

employed to measure the various constructs and variables. Eight items captured the strategic

processes (Dulewicz and Herbert, 1999); six items captured the relationship among the board

of directors and top management team (Dulewicz and Herbert, 1999). Six items captured the

board’s culture and fourteen items captured the board’s appraisal.

20

RESEARCH FINDINGS

The survey results capture the current corporate governance practices in the Nigerian

Banking industry as regards Board of Directors’ characteristics, board processes, board

involvement in the strategic process, board relationship with the CEO and the top

management team.

Board Characteristics

Board Size

Results from the research show that the average size of the boards of Nigerian banks is 14

directors, with the smallest having 8 directors and the largest 20 directors. A board size of 16

directors is the most popular. The Central bank of Nigeria (CBN) corporate governance code

for banks operating in Nigeria recommend a maximum board size of 20 directors. All the

banks are compliant. However, United Bank for Africa Plc has applied to the CBN for

approval to increase their board size to 24 but the Central Bank is yet to grant its approval.

The banks have gone for medium to large board sizes because most of them (22 of the 24

banks) are now publicly owned and as such more interest groups are now being represented.

In addition, each board should have enough number of directors to serve on the board

committees that they are expected to have.

Board Leadership (Duality)

The research results show that the boards of all the banks have separate chairman and chief

executive officer. This implies that all the banks comply with the Central Bank of Nigeria

21

corporate governance guideline, which stipulates that the chairman and CEO must be

separate.

Board Independence

Board independence is dependent on the composition of the board in terms of the distinction

between inside and outside directors, which is traditionally shown as the percentage of

outside directors on the board.

About 64% of directors on the boards of Nigerian banks are non-executive directors. This

means that the boards of banks in Nigeria can be said to be independent, which is in line with

the CBN guideline that the number of non-executive directors should be more than that of

executive directors. The number of executive (inside) directors on the boards of banks range

from 3 to 8 with the average being 5, while the number for non-executive (outside) directors

range from 4 to 13 with an average of 9. Among the non-executive directors, about 6 are

truly independent while about 2 are affiliates. Again this is in line with the CBN guideline

that states that at least two non-executive directors should be independent. The total number

of affiliates and executive directors is slightly more than that of truly independent directors

on the boards of banks in Nigeria. This will affect the true independence of the boards in

practice.

Board Diversity

Results of our survey show that directors of Nigerian banks believe that their boards are quite

diversified (with a score of 5.9 on a 7-point scale) in terms of having a mix of people with

different personality, educational, occupational and functional background.

22

Only 16 banks have female directors on their boards 12 of them have one female director

each, two have two female directors each, one has three female directors and one has four

female directors.

However, the four most dominant occupational background of members of the board of

directors are banking and financial services, accounting and finance, law, and general

management/business administration.

In spite of the diversity the directors see the skills of the board members are quite

complementary with a rating of 5.9 on a 7-point scale. They also see their members as being

very knowledgeable and experienced in business and financial matters in general and in the

banking business in particular, with a score of 6.1 on a 7-point scale.

BOARD OPERATION AND PROCESSES

Board Meetings

The modal average frequency of holding board meetings among the survey sample is every

three months or quarterly. This is the minimum standard prescribed in the CBN code and as

such the banks could be said to be in substantial compliance with the code.

According to the respondents, board meetings are conducted with openness and transparency.

Board Culture

In this case culture means the set of informal unwritten rules which regulates board and the

directors’ behaviour. The results of the survey (see figure 1) show the following cultural

characteristics of boards of Nigerian banks:

23

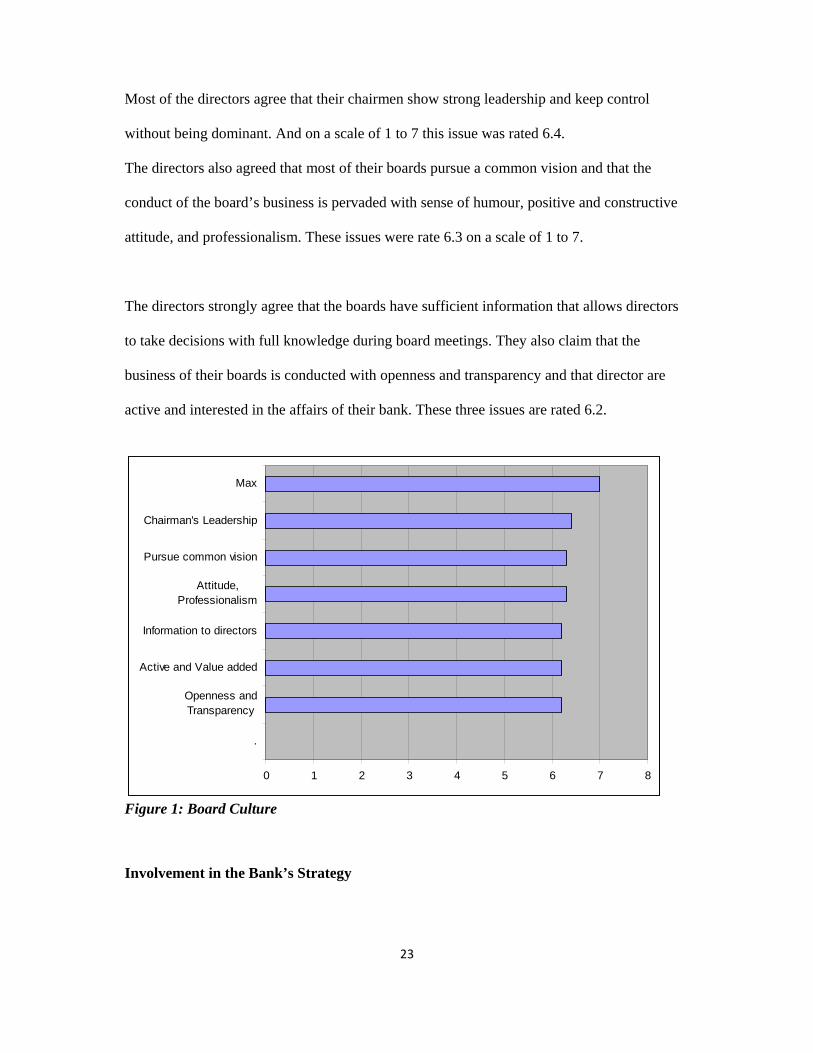

Most of the directors agree that their chairmen show strong leadership and keep control

without being dominant. And on a scale of 1 to 7 this issue was rated 6.4.

The directors also agreed that most of their boards pursue a common vision and that the

conduct of the board’s business is pervaded with sense of humour, positive and constructive

attitude, and professionalism. These issues were rate 6.3 on a scale of 1 to 7.

The directors strongly agree that the boards have sufficient information that allows directors

to take decisions with full knowledge during board meetings. They also claim that the

business of their boards is conducted with openness and transparency and that director are

active and interested in the affairs of their bank. These three issues are rated 6.2.

0 1 2 3 4 5 6 7 8

.

Openness andTransparency

Active and Value added

Information to directors

Attitude,Professionalism

Pursue common vision

Chairman's Leadership

Max

Figure 1: Board Culture

Involvement in the Bank’s Strategy

24

The results show that boards are moderately involved in their banks strategy development as

the average ratings for the eight factors used in determining involvement are between 4.7 and

5.8 on a 7-point scale (see figure 2). The most important factor, with a rating of 5.8, is the

determination of the bank’s vision and mission to guide and set the pace for its operations and

future development. This shows the degree of importance director’s place in shaping the

future of their bank. This will even become more important in the future because the Central

Bank of Nigeria will hold the directors of banks in Nigeria responsible for the performance

and state of affairs of their bank. The least important factor, with a rating of 4.7, is the

determination of the business units’ strategies and implementation. This is because the

directors expect their management to be more involved in the activities of business units.

Directors expect to be involved in determining and enforcing company policies for effective

running of the bank. In addition their involvement in the bank’s strategy process should

include the determination and review of the bank’s objectives to match its mission and

values; the review and evaluation of opportunities, threats and risks in the external

environment, and strengths, weaknesses and risks of their bank. Directors also see their

involvement in ensuring that their bank’s organization structure and capabilities are

appropriate for implementing its chosen strategies.

25

0 1 2 3 4 5 6 7 8

Determines thebusiness unit strategies

and plans

Adapts performancemeasures to monitor the

implementation

Selects strategicoptions and provides

resources

Ensures company'sobjectives match vision

and mission

Undertakes SWOTanalysis

Ensures appropriatecapabilities for strategy

implementation

Determine thecompany's vision and

mission

Determine and enforcescompany policies

Maximum Point

Figure 2: Involvement in Bank’s Strategy

Board Dynamics

Our results show that good relationship among the board, top management team and the CEO

is important to the directors. This is being achieved by delegating authority to management

and monitoring its implementation of policies, strategies and business plans. This is rated as

26

the most important factor (6.1 on a 7-point scale) in ensuring good relationship between the

board and management. The second most important factor, with a score of 5.7, is ensuring

that internal control procedures provide valid and reliable information for monitoring the

operations and performance of the bank. Other factors that enhance good relationship

between the board and top management are: communicating performance of management to

them and aligning rewards and sanctions with performance; well defined evaluation process

for the CEO and appropriate reward that is linked to performance; good management

development programme; and succession planning.

0 1 2 3 4 5 6 7 8

Involved in managementdevelopment and

succession

Rewards and evaluates theCEO

Ensures appropriatereward and development of

management

Ensures effective internalcontrol procedures

Delegates authority tomanagement

Maximum point

Figure 3: Relationship between the Board and Top Management

27

Appraisal of Board of Directors

Boards of banks in Nigeria have to do more to ensure the effectiveness of their over-sight

function. They must therefore be concerned with more than organizational and management

performance; they also need to review their own performance. Behavioural psychologists

and organizational learning experts agree that people and organizations cannot learn without

feedback and so, no matter how good a board is, it’s bound to get better if it’s reviewed

intelligently. Board evaluation and directors’ appraisals are now being regarded as tools that

can enhance board effectiveness.

Board evaluation can therefore provide a process for boards to identify sources of governance

failures. They will allow boards to take a closer look at areas of concern before they reach

crisis point. However, board evaluations are not a universal panacea for all board ills, but

when used correctly and regularly, they may play a major role in averting governance

failures.

76 percent of respondents claim that their boards are appraised, 65 percent claim that

individual directors are appraised, while 59 percent claim that the chairman is appraised. The

most common appraisal frequency is yearly with 73 percent of the respondents and the

appraisal is conducted by mainly external consultants (73 percent).

Respondents were asked to rate 14 issues on which the board of directors is appraised on a

scale of 1 to 7, where one is strongly disagree and 7 strongly agree. The three most important

issues upon which board of directors are being appraised that have ratings of over 5 are:

28

overall governing of the bank, shaping the long-term strategy of the bank, and managing the

bank during crisis. The long-term future and the survival of the bank are therefore seen as the

most important responsibilities of the board.

Other important issues on which the boards are evaluated include: monitoring strategy

implementation, effectively inquiring into major performance deficiencies, proposing

changes in the bank’s direction, bolstering the bank’s image, enhancing good government and

regulator relations, and balancing the interest of different stakeholders.

The directors are also of the view that boards should be appraised on how well they deal with

unforeseen corporate problems and possible threats to the bank’s survival, and how well they

handle CEO and top management succession.

Board appraisal is an annually event for most of the banks and for about 73 percent of the

respondents it is conducted by external consultants. However, for a small minority, (about 6.6

percent) of the respondents, appraisal is conducted by the CEO.

29

0 1 2 3 4 5 6 7 8

Building Networks with strategic partners

Involvement in CEO succession

Planning for top management

Anticipating possible threats to company survival

Dealing with unseen corporate problems

Balacing interest of different stakeholders

Bolstering the company's image in the community

Monitoring strategy implementation

Enhancing government relations

Proposing changes in company direction

Effectively inquiring into major performancedeficiencies

Managing during crisis

Governing Overall

Shaping long term strategy

.

Figure 4: Factors on which directors are appraised

Future Development of Corporate Governance

The views of directors of banks in Nigeria were sought as regards to the future direction of

corporate governance in Nigeria. The most important areas for improvement are: establishing

formal training programme for newly appointed directors and continuous training for

30

directors; monitoring the legal and ethical conduct of the bank; and regularly evaluating the

performance of Audit Committee.

Other issues that should be addressed in order to enhance corporate governance include

report to shareholders on state of corporate governance in the bank at annual general

meetings, establishment of remuneration and nomination committees, and establishment of

professional qualifications for board members as a means of ensuring high level of

professionalism and competence.

CONCLUSIONS

The empirical findings of this study have revealed a number of critical issues as regards

corporate governance practices in the Nigerian Banking industry. Most of the banks are now

publicly quoted and so obliged to make their financial performance public. It also means that

accountability and transparency will be of interest to the management of these banks.

Some of the Nigerian banks already have foreign investors and as the Nigerian banking

industry opens up to international investors, the banks that do try to improve their corporate

governance rating will have much to gain. The banks that adopt best practices will get the

most interest from international investors. The more Nigerian banks reach out to global

investors, the greater the pressure will be to adopt corporate governance best practices.

The Central Bank of Nigeria issued its code of corporate governance for banks operating in

Nigeria as a means of enhancing the stability and soundness of the Nigerian banking sector

through improved corporate performance. Our findings show that all Nigerian banks have

embarked on one or more corporate governance initiatives in response to this mandatory

CBN Code.

31

Most of the boards of Nigerian banks include members with relevant professional experience

and educational profile with banking and finance being the most popular background.

These boards are of relatively large size, ranging between eight to twenty board members,

with fourteen being the average. Ogbechie and Koufopoulos (2007) found that the average

size of boards in publicly quoted companies in Nigeria is about 8 and so banks in Nigeria can

be said to have large sizes. This large board size affords the banks to opportunity to have

directors with diverse experience and expertise that could add value to the bank.

These boards also exhibit a balanced board leadership structure with all of them having

different persons as CEO and board chairperson. This in turn indicates that theoretically the

boards are not under the influence of the CEO. However, in practice many of the banks have

chairpersons whose appointments were influenced by the CEOs and as such under

considerable influence of these CEOs.

The independence of boards of Nigerian banks is supported by the number of outside

directors on the board, who account for about 64% of the board. Nigerian banks seem to

favour the opinion that outside directors can bring their experience and social capital to add

value to the banks. It has been argued that firms with a higher proportion of external

directors and with CEOs being separate from the Chairpersons are more likely to have

superior performance as a result of their independence from firm’s management (Baysinger

and Butler, 1985). They can bring to the board a wealth of knowledge and experience, which

the company’s own management may not possess. This seems to be confirmed in the case of

Nigerian banks. Based on the findings that for the majority of the banks, board leadership is

32

independent, CEO and Chairperson Seats are held by different persons, and Nigerian banks

have large boards.

Empirical findings indicate that boards of Nigerian banks significantly contribute to all stages

of the strategic process from analysis to formulation and finally implementation. The boards’

frequency of meetings is also an indication of their involvement in the emergent strategy

development process that characterizes banks. This high level involvement for boards with

relatively high proportion of outside directors goes against the findings of Demb and

Neubauer (1992) that there is less chance for non-executive directors to intervene or to

submit their opinion in a firm’s strategy process.

The boards of directors in Nigerian banks are actively involved in the determination of their

banks’ vision and mission and also the determination and enforcement of the banks’ policies.

These factors are critical for the long-term success of firms. However, boards of Nigerian

banks seem to be reluctant in evaluating their CEO and in management development and

succession. This could imply that CEOs have a strong hold on their boards.

The intense competition in post-consolidation era and the close monitoring/supervision of the

regulatory agency, CBN, mean that Nigerian banks have to adjust their governance

structures. Adoption of good corporate governance practices will entail several advantages to

the banks, the most important being the access to capital for investment and the enhancement

of their corporate image. The empirical findings of this study show that the banks have

embraced the basic corporate governance principles and have to internalize them.

Most of the banks have a formal board evaluation process in place which is done by external

consultants. Planning for succession is rarely formalized. Risk management capabilities in

33

most of the banks are yet to go beyond credit risk management to include the full spectrum of

risks facing a bank

One of the factors that have so far hampered the rapid development of corporate governance

in the Nigerian banking industry is the lack of a strong institutional investor base that can

lobby banks to change their behaviour. The time is ripe for a transparent corporate

governance rating in Nigeria.

Further research on corporate governance in the banking industry is needed particularly on

the effectiveness of boards and the impact on bank performance. Corporate governance is not

just about playing “watchdog” over management, it is more about enhancing corporate

strategic choices, acknowledging and responding to the interests and concerns of

stakeholders, developing and bolstering managerial competencies and skills and ultimately

protecting and maximizing shareholder wealth.

The study of the Nigerian banks shed some light and contributes to the ongoing, emerging

and extremely important research stream that relates to financial services especially at this

time that there is more focus on the degree of regulation in this sector.

This research highlights some important elements of corporate governance in a dynamic

sector that has a strong influence on national economy, particularly in emerging markets.

34

REFERENCES

Allen, F. And Herring, R. (2001), “Banking regulations versus securities market regulations”, Wharton Financial Institutions Center, No. 29

Basel Committee on Banking Supervision 1999, “Enhancing corporate governance for banking organizations”.

Baysinger, B.D. & Bulter, H.N. 1985, “Corporate governance and the board of directors: performance effects of change in board composition”, Journal of Law, Economics and Organization, vol. 1, pp. 101-124.

Baysinger, B. and Hoskisson, R.E. (1990). “The Composition of Boards of Directors and Strategic Control: Effects on Corporate Strategy”. The Academy of Management Review, Vol. 15(1), pp. 72-87.

Beatty, R. E. and E. J. Zajac (1994), “Managerial incentives, monitoring, and risk bearing: A study of executive compensation, ownership, and board structure in initial public offerings”. Administrative Science Quarterly, Vol. 39, pp. 313-335.

Becht, M., Bolton, P. And Roel, A. (2002), “Corporate Governance and Control.” Working paper 9371, National Bureau of Economic Research.

Blake, A (1999), “Dynamic Directors: Aligning Board Structure for Business Success”, Basingstoke: Macmillan. Cadbury A. (1992), “The Financial Aspects of corporate governance – A report of the committee on corporate governance”, Gee and Co., London.

Caprio, G. and Levine, R. (2002), “Corporate Governance of Banks: Concepts and International Observations”, paper presented at the Global Corporate Governance Forum Network Research Meeting. Carpenter, MA, Pollock, TG & Leary, M.M. (2003), “Testing a model of reasoned risk-taking: governance, the experience or principals and agents, and global strategy in high-technology IPO firms”, Strategic Management Journal, Vol. 24, pp. 803-820. Carpenter, MA & Sanders, WG 2002, “Top management team compensation: the missing link between CEO pay and firm performance”, Strategic Management Journal, Vol. 23, pp. 367-375. Carver, J. (1997), “Board Self-assessment (Carver Guide 8)”. San Francisco: Jossey-Bass Publishers.

35

Central Bank of Nigeria 2006, “Code of Corporate Governance for Banks in Nigeria Post Consolidation”. Central Bank of Nigeria (2006), “Annual Report”..

Conger, JA & Lawlor III, E. (2002) “Evaluating the directors: The next step in boardroom effectiveness”, Ivey Business Journal, September/October 2002.

Daily, C., Dalton, D., and Rajagopalan, N. (2003). “Governance through ownership: centuries of practice, decades of research”, Academy of Management Journal, Vol. 46: pp. 115-158.

Dalton, D.R. (1993). “Board of Directors leadership and structures: Control and performance implications”, Entrepreneurship: Theory and practice.Vol. ……………………..

Dalton, D.R., Daily, C.M., Ellstrand, A.E., and Johnson, J.L.(1998). “Meta-Analytic Reviews of Board Composition, Leadership Structure and Financial Performance”. Strategy Management Journal, Vol. 19 (3), pp. 269-290.

Davies, A (1999), “A Strategic Approach to Corporate Governance”, Aldershot: Gower Vol. 59, pp. 34-37.

Decenzo, D.A. & Robbins, S.P. (2005), “Fundamentals of Human Resource Management”, 8th ed., New York: John Wiley & Sons

Demb, A. and Neubauer, F. (1992). “The corporate board”. New York: Oxford University Press.

Dilenschneider, R.L. (1996) “The Board as a Think Tank’, Directors & Boards, Vol. 21, no. 1, pp. 30-38.

Dobrzynski, J. (18 November 1991). “Chairman and CEO: One hat too many”, Business Week, Vol. 12(3), pp. 263-280.

Eisebhardt, K. M. and L. J. Bourgeois (1988). “Politics of strategic decision making in high-velocity environments: Towards a midrange theory”. Academy of Management Journal, Vol. 31, pp. 737-770.

Fama, E.F. (1980), “Agency Problems and The Theory of the Firm”. Journal of Political Economy, Vol. 88, pp. 288-307.

Fama. E. and Jensen, M. (1983). “Separation of ownership and control”. Journal of Law and Economics, 26, pp. 301-326.

36

Finkelstein, S. and R. A. D’Aveni (1994). “CEO duality as a double-edged sword: How boards of directors balance entrenchment avoidance and unity of command”. Academy of Management Journal, Vol. 37, pp. 1079-1108.

Forbes, D.P. and Milliken, F. (1999). “Cognition and corporate governance: Understanding board of directors as strategic decision making group”. Academy of Management Review, Vol. 3, pp. 489-505.

Garrett, B. (1996), “The Fish Rots from the Head – the crisis in our Boardrooms: Developing the crucial skills of the Competent Director”, London: Harper Collins.

Goergen, M. and Renneboog, L. (2000), “Insider Control by Large Investor Groups and Managerial Disciplining in listed Belgian Companies”. Managerial Finance, Vol. 26, pp. 22-41.

Golden, B.R. & Zajac, E.J. 2001, “When will board influence strategy? Inclination x power = strategic change”, Strategic Management Journal, Vol. 15, No. 3, pp. 241-250. Hambrick, DC & Mason, PA 1984, “Upper echelons: the organizations as a reflection of its top managers”, Academy of Management Review, Vol. 16, pp. 193-206. Jeffrey, A.A., Fennell, M.L., and Halpern, M.T. (1993), “Leadership Instability in Hospitals: The influence of Board – CEO Relations and Organisation Growth and Decline”. Administrative Science Quarterly, Vol. 38.

Jensen, M.C. (1986), “Agency Cost of Free Cash Flow, Corporate Finance and Takeovers”. American Economic Review, Vol. 76, pp. 323-329.

Jensen, M.C. (1993), “The Modern Industry Revolution, Exit and the Failure of Internal Control Systems”. The Jourmal of Finance. Vol. 48, No. 30, pp. 831-880.

King, R.G. and Levine, R. (1993a), “Finance and Growth: Schumpeter Might be Right”. Quartery Journal of Economics, Vol. 108, pp. 717-737.

King, R.G. and Levine, R. (1993b), “Finance, Entrepreneurship and Growth: Theory and Evidence”. Journal of Monetary Economics, Vol. 32, pp. 513-542.

Kosnik, R.D. (1990), “Effects of board demography and directors incentives on corporate greenmail decisions”. Academy of Management Journal, Vol. 33, pp. 129-151.

Levine, R. and Zervos, S. (1998), “Stock Markets, Banks, and Economic Growth”. The American Economic Review, Vol. 88.

Macay, J. and M. O’Hara, (2003), “The Corporate Governance of Banks”, Federal Reserve Bank of New York Economic Policy Review, April 5, pp. 91 – 107 Mace, M. (1971), “Directors: Myth and reality”. Boston: Harvard Business School Press.

37

McNulty, T. & Pettigrew, A. (1999), “Strategists on the board”, Organization Studies, Vol. 20, pp. 47-74. Monks, R.A. & Minow, N. (2001), “Corporate Governance”, 2nd Edition, Oxford: Blackwell Publishers Inc. Nadler, D.A. (2004), “Building Better Boards”, Harvard Business Review, May 2004. pp. xx Nonaka, I. (1994), “A dynamic theory of organizational knowledge creation”, Organization Science, Vol. 5, pp. 14-37. OECD Basel Committee on Banking Supervision (2006), “Enhancing Corporate Governance for Banking Organisaations”. BIS: Basel.

Pablo, de Andres, Valentine, Azofra and Felix Lopez (2005), “Corporate Boards in OECD Countries: Size, Composition, Functioning and Effectiveness”, Corporate Governance, Vol. 13, No.2, pp. 197-210 Pearce, J. and S. Zahra (1991). “The relative power of CEOs and boards of directors: Associations with corporate performance”. Strategic Management Journal, 12, pp. 135-153.

Pettigrew, A.M. (1992), “ On studying managerial elites”, Strategic Management Journal, Vol. 13, no. 8, pp. 163-182. Prybil, L. (2008), “What’s your Board’s Culture?”, Trustee Magazine, June issue. Pye, A. (2002), “Corporate directing: governing, strategizing and leading action”, Corporate Governance: An International Review, Vol. 10, no. 3, pp. 153-162. Rajan, R. and Zingales, L. (1998), “Financial Dependence and Growth”, American Economic Review, Vol. 88, pp. 559-586. Reed, J.S. (2003), “Ethics and the Not-for-Profit board”, Boardroom Press, December 2003, pp7. Roberts, J.T., McNulty, P. & Stiles, P. (2005), “Beyond agency conceptions of the work of the non-executive directors: creating accountability in the boardroom”, British Journal of Management, Vol. 16, pp. S5-S6. Sanders, W.G. & Carpenter, M.A. (2003), “Strategic satisfying? A behavorial agency perspective on stock repurchase program announcements”, Academy of Management Journal, Vol. 46, pp. 160-179. Sbracia, M. and Zaghini, A. (2003), “The role of the banking system in the international transmission of shocks”, The World Economy, vol. 26, pp. 727 – 754 Security and Exchange Commission (SEC) of Nigeria (2003), “Report of the Committee on Corporate Governance of Public Companies in Nigeria”.

38

Staff (2000), “e-Business and Board Independence Key to Performance, Activists Say”, Investor Relations Business, Vol. 1, pp. 16 Steinberg, R. (2000), “Effective Boards: Making the Dynamics Work”, Directorship, Vol.26, No.11, pp. 7-9. Tregoe, B. B. & Zimmermann, J. W. (1980). “Top Management Strategy”. Simmon Schuster. pp17.

Tricker, R.I. (1999), “Fat Cats and Englishmen”, Director, Vol. 52, No. 12, pp. 34. Useem, M. (1993), “Executive defense: shareholder power and corporate reorganization”, Cambridge, MA: Harvard University Press. Useem, W. (2006), “How well-run Boards make Decisions”, Harvard Business Review, pp. 130-138.

Van den Berghe, L. & De Ridder, L. (1999), “International standardization of good corporate governance”, Kluwwer Academic Publishers.

Van den Berghe, L.A. & Levrau, A. (2004), “Evaluating Boards of Directors: What constitutes a good corporate board?”, Corporate Governance, An International Review, Vol. 12, No.4, pp. 461-478. Van der Walt, N.T. & Ingley, C.B. (2001), “Evaluating board effectiveness: the changing context of strategic governance”, Journal of Change Management, Vol. 1, No.4, pp.313-31.

Wade, J., O’Reilly, C. A. and Chandratat, I. (1990), “Golden parachutes: CEOs and the exercise of social influence”. Administrative Science Quarterly, Vol. 35, pp. 587-603.

Westphal, J.D. (1998), “Board games: how CEOs adapt to increases in structural board independence from management”, Administrative Science Quarterly, Vol. 43, No. 3, pp. 511-537. Westphal, J.D. (1999), “Collaboration in the boardroom: the consequences of social ties in the CEO/board relationship”, Academy of Management Journal, Vol. 42, pp. 7-24. Zahra, S.A. & Pearce, J.A. (1989), “Boards of directors and corporate financial performance: a review and integrative model”, Journal of Management, Vol. 15, No. 2, pp. 291-334. Zald, M.N. (1969), “The Power and Function of Boards of Directors: A Theoretical Synthesis”. American Journal of Sociology, Vol. 75, pp. 97-111.