Page 1 of 21 Analytical tools to Study Corporate Governance in Financial Sector of Iran 1 Afshin Ashofteh 2 Abstract Recent academic work and policy analysis give insight into the governance problems exposed by the financial crisis and suggest possible solutions. We begin this research by designing some appropriate research tools which could be used to explain the current situation, target situation, weaknesses and strengths of governance of banks and other sectors of finance in IRAN. Actually, we consider the differences of the governance in the Central Bank of Iran, banks and other players of financial atmosphere in this research, and then look at ten areas of governance and market discipline. We discuss promising solutions and areas where further research is needed. Keywords: Corporate Governance, Central Banking, Governance, Supervision, Structure of Board of Directors, Transparency, Interdependence, Accountability, Responsibility, Fairness, Social Awareness, Organisational Success, Internal Control of Processing. JEL Classification: E58, G35. Introduction Firstly I would like to appreciate my colleagues for their kind assistance in this important topic of banking and financial sector crisis and adequate corporate governance structure as a tool to prevent crisis from arising. The high profile financial failures like “Enron” and “WorldCom”, to name one but two, have undermined trust in the corporate sector in general, and in the financial sector, in particular. In fact, the financial world, especially the banking world, thrives on trust. According to the Organization for Economic Cooperation and Development (OECD) (1999), corporate governance original definition is: "Corporate governance specifies the distribution of rights and responsibilities among different participants in the corporation, such as the board, managers, shareholders, and other stakeholders; and spells out the rules and procedures for making decisions on corporate affairs. By doing this, it also provides the structure through which the company objectives are set, and accordingly the means of attaining those objectives and monitoring performance." According to the Economist and Noble Laureate Milton Friedman, 1 This report has been accomplished as a part of the project entitled in “Vision for the Financial Services Industry of IRAN” in the Central Bank of IRAN and Monetary & Banking Research Institute, under the supervision of Prof. Pierre A. Bultez. I sincerely acknowledge his valuable ideas and contribution to the improvement of this part of project. 2 Senior officer – Central Bank of Iran - [email protected], [email protected]

Transcript

Page 1 of 21

Analytical tools to Study Corporate Governance in Financial

Sector of Iran1

Afshin Ashofteh2

Abstract

Recent academic work and policy analysis give insight into the governance problems exposed by

the financial crisis and suggest possible solutions. We begin this research by designing some

appropriate research tools which could be used to explain the current situation, target situation,

weaknesses and strengths of governance of banks and other sectors of finance in IRAN.

Actually, we consider the differences of the governance in the Central Bank of Iran, banks and

other players of financial atmosphere in this research, and then look at ten areas of governance

and market discipline. We discuss promising solutions and areas where further research is

needed.

Keywords: Corporate Governance, Central Banking, Governance, Supervision, Structure of Board of

Directors, Transparency, Interdependence, Accountability, Responsibility, Fairness, Social

Awareness, Organisational Success, Internal Control of Processing.

JEL Classification: E58, G35.

Introduction

Firstly I would like to appreciate my colleagues for their kind assistance in this important topic

of banking and financial sector crisis and adequate corporate governance structure as a tool to

prevent crisis from arising.

The high profile financial failures like “Enron” and “WorldCom”, to name one but two, have

undermined trust in the corporate sector in general, and in the financial sector, in particular. In

fact, the financial world, especially the banking world, thrives on trust.

According to the Organization for Economic Cooperation and Development (OECD) (1999),

corporate governance original definition is: "Corporate governance specifies the distribution of

rights and responsibilities among different participants in the corporation, such as the board,

managers, shareholders, and other stakeholders; and spells out the rules and procedures for

making decisions on corporate affairs. By doing this, it also provides the structure through which

the company objectives are set, and accordingly the means of attaining those objectives and

monitoring performance." According to the Economist and Noble Laureate Milton Friedman,

1 This report has been accomplished as a part of the project entitled in “Vision for the Financial Services Industry of IRAN” in

the Central Bank of IRAN and Monetary & Banking Research Institute, under the supervision of Prof. Pierre A. Bultez. I sincerely acknowledge his valuable ideas and contribution to the improvement of this part of project. 2 Senior officer – Central Bank of Iran - [email protected], [email protected]

Page 2 of 21

"Corporate Governance is to conduct the business in accordance with owners or shareholders'

desires, while conforming to the basic rules of the society embodied in law and local customs"3.

Corporate governance has another dimension which serves and guides to secure the dedication of

stakeholders with the objective to functionalize their skills, knowledge and experience to avail

the full benefits. To avail the maximum organizational benefits, corporate governance sets legal

terms and conditions for the allotment of property rights among stakeholders, organizing their

associations, and manipulating their incentives for achieving their eager to work together. For

further addition to corporate governance, it is vital due to the delegation of responsibility for

production, process improvement, and innovation4.

"Corporate governance is the system by which companies are directed and controlled. Boards of

directors are responsible for the governance of their companies. The shareholders' role in

governance is to appoint the directors and the auditors and to satisfy themselves that an

appropriate governance structure is in place. The responsibilities of the directors include setting

the company's strategic aims, providing the leadership to put them into effect, supervising the

management of the business, and reporting to shareholders on their stewardship. The Board's

actions are subject to laws, regulations, and the shareholders in general meeting"5. In his most

comprehensive sense, corporate governance comprises all the forces that have effects on firm’s

decision making process. It would protect not only the stockholder’s rights, but also the

bounding agreement and collapsing power of debtors. Corporate governance also gains the

commitment of the employees, customers, and suppliers. Additionally, it is the Power to diffuse

the risks by combining all the forces.

According to Attiya Y. Javid, Robina Iqbal (2010), the performance has a link with good

corporate governance for the sustainable organizational success. It is also denoted that good

corporate governance serves for a number of public policy objectives in new markets.

1. Corporate Governance in Financial Sectors

From a financial industry perspective, corporate governance involves the manner in which the

business affairs of individual institutions are governed by their Boards and management. It also

includes the effective management of compliance with applicable laws, regulations, and

guidelines. The focus on corporate governance in IRAN should be particularly acute in financial

services and, most of all, in the banking sector owing to powerful affluent banking system.

In particular, Governance in Iranian banks is a considerably more complex issue than in other

sectors. Banks will attempt to comply with the same codes of board governance as other

companies but, in addition, factors like risk management, capital adequacy and funding, internal

3 Economic Times, 2001

4 Suzanne, C. Neil et al. 2006 5 Cadbury commission (1992)

Page 3 of 21

control, and compliance all have an impact on their matrix of governance. The complexity will

go further when we want to talk about this subject in the Central Bank of IRAN as one of the

specific organizations with very specific characteristics like sanction, autonomy, etc. Therefore,

before we go into the corporate governance in financial sectors of IRAN, let us highlight the

elements of corporate governance in the banking system of IRAN very briefly.

Builds/restores a bank’s reputation

Build trust between CBI, banks and their stakeholders, including governors,

shareholder, investors, regulator, depositors, employees – key in weak external

environment

Less and better managed risk

Fewer defaults, fewer financial crises brings economic and financial stability

Increases access to finance

Investment, growth, and employment opportunities

Lowers cost of capital and improves valuation

Investment & growth opportunities

Improves operational performance

Better allocation of resources & better decision-making create wealth

Governance is also a curiously two-sided issue for banks, since their funding and often

ownership of other companies make them a significant stakeholder in their own right.

The Board of Directors stands at the heart of many systems and structures encompassing the

totality of corporate governance. From a banking industry perspective, corporate governance

involves the manner in which the business and affairs of individual institutions are governed by

their boards of directors and senior management, affecting how banks do the following:

Set corporate objectives (including generating economic returns to owners);

Run the day-to-day operations of the business;

Consider the interests of recognized stakeholders;

Align corporate activities and behavior with the expectation that banks will operate in a

safe and sound manner, and in compliance with applicable laws and regulations; and

Protect the interests of depositors.

In the financial system, corporate governance is not only vital at the individual company level,

but it also is a critical element in maintaining a sound financial system and a robust economy.

2. The Methodology

2.1. Goals of the research:

Our aim is to measure how much the literature of Miles, L. (2010) which indicates that the

Page 4 of 21

independence of director has effect on organizational success and to measure if the independence

has insignificant effects on organizational success in our environment.

We would like to measure if discipline and social awareness have strong impacts on the

perceived organizational success. Similar indications can be found in the study of Mungule, O

(2005) in support that discipline is one of the major contributors in organizational success.

Findings of this study in accordance with the importance of accounting standards being part of

the discipline in organizations should show us what variables are the most important ones for

Iranian banking and financial sector organizations to be successful.

In order to achieve the aim, we suggest using the method proposed by Credit Lyonnais Securities

Asia (further referred as CLSA) to measure corporate governance. In a recent review, CLSA

calculated an index with corporate governance rankings for 495 firms across 25 emerging

markets and 18 sectors. The descriptive statistics presented in the CLSA report show that

companies ranked high on the governance index have better operating performance and higher

stock returns. We propose to customize the governance rankings produced by CSLA for further

investigations, the relationship between firm level governance, other firm level characteristics,

and the country level legal environment according to the situation of IRAN.

In fact, we all know the importance of corporate governance and somehow the current situation

in IRAN, however, in this study, we intend to demonstrate what the key elements are and that are

focused on while proposing an implementation’s solutions; all concepts are important and our

findings will help us to prioritize the tasks.

Hence, we can summarize the goals of the study in these three items:

1. Measuring the social awareness about Corporate Governance in financial sectors of

IRAN.

2. Knowing the key elements in Corporate Governance, which we would need to focus on

while proposing an implementation’s solutions for vision of financial sector.

3. Prioritise the required tasks to move from the current situation to the target situation.

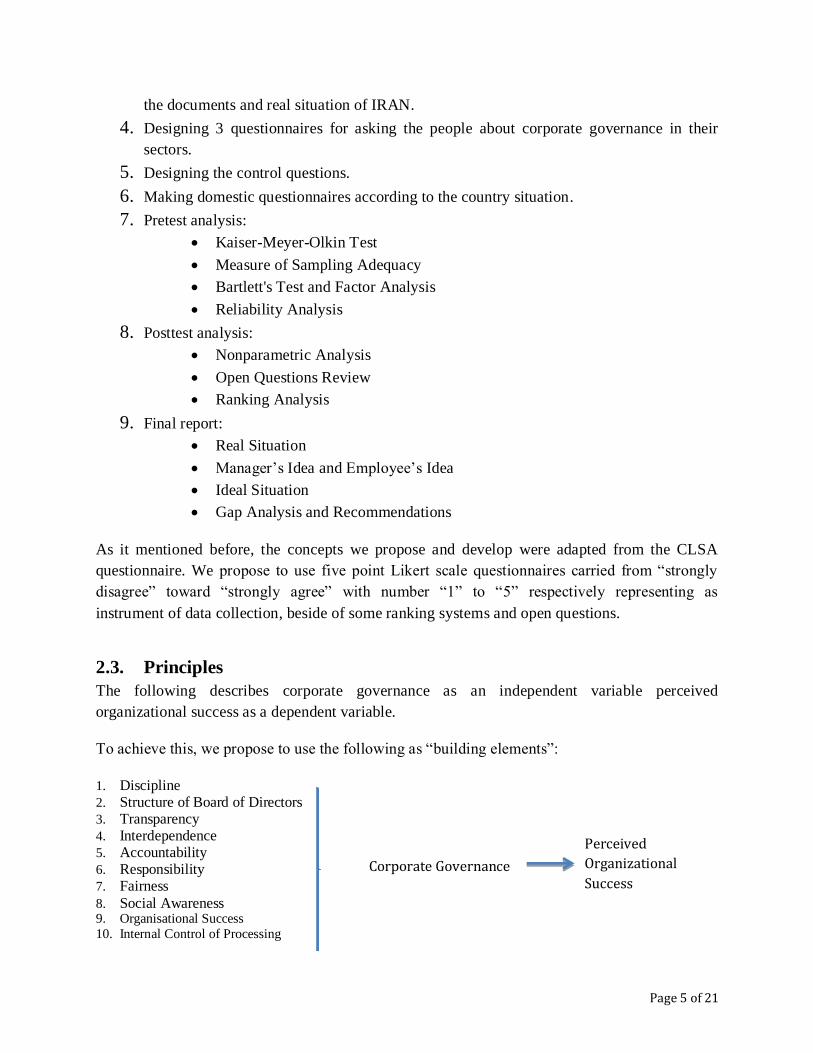

2.2. The steps of the research:

The following steps outline the strategy of this study that we followed briefly:

1. Literature review on Corporate Governance in financial sector of IRAN.

2. Increasing the main principle of CG research from 8 to 10 according to specific situation

in IRAN.

3. Designing 3 forms for evaluating corporate governance in different sectors according to

Page 5 of 21

the documents and real situation of IRAN.

4. Designing 3 questionnaires for asking the people about corporate governance in their

sectors.

5. Designing the control questions.

6. Making domestic questionnaires according to the country situation.

7. Pretest analysis:

Kaiser-Meyer-Olkin Test

Measure of Sampling Adequacy

Bartlett's Test and Factor Analysis

Reliability Analysis

8. Posttest analysis:

Nonparametric Analysis

Open Questions Review

Ranking Analysis

9. Final report:

Real Situation

Manager’s Idea and Employee’s Idea

Ideal Situation

Gap Analysis and Recommendations

As it mentioned before, the concepts we propose and develop were adapted from the CLSA

questionnaire. We propose to use five point Likert scale questionnaires carried from “strongly

disagree” toward “strongly agree” with number “1” to “5” respectively representing as

instrument of data collection, beside of some ranking systems and open questions.

2.3. Principles

The following describes corporate governance as an independent variable perceived

organizational success as a dependent variable.

To achieve this, we propose to use the following as “building elements”:

1. Discipline 2. Structure of Board of Directors 3. Transparency 4. Interdependence 5. Accountability 6. Responsibility 7. Fairness

8. Social Awareness 9. Organisational Success

10. Internal Control of Processing

Corporate Governance

Perceived

Organizational

Success

Page 6 of 21

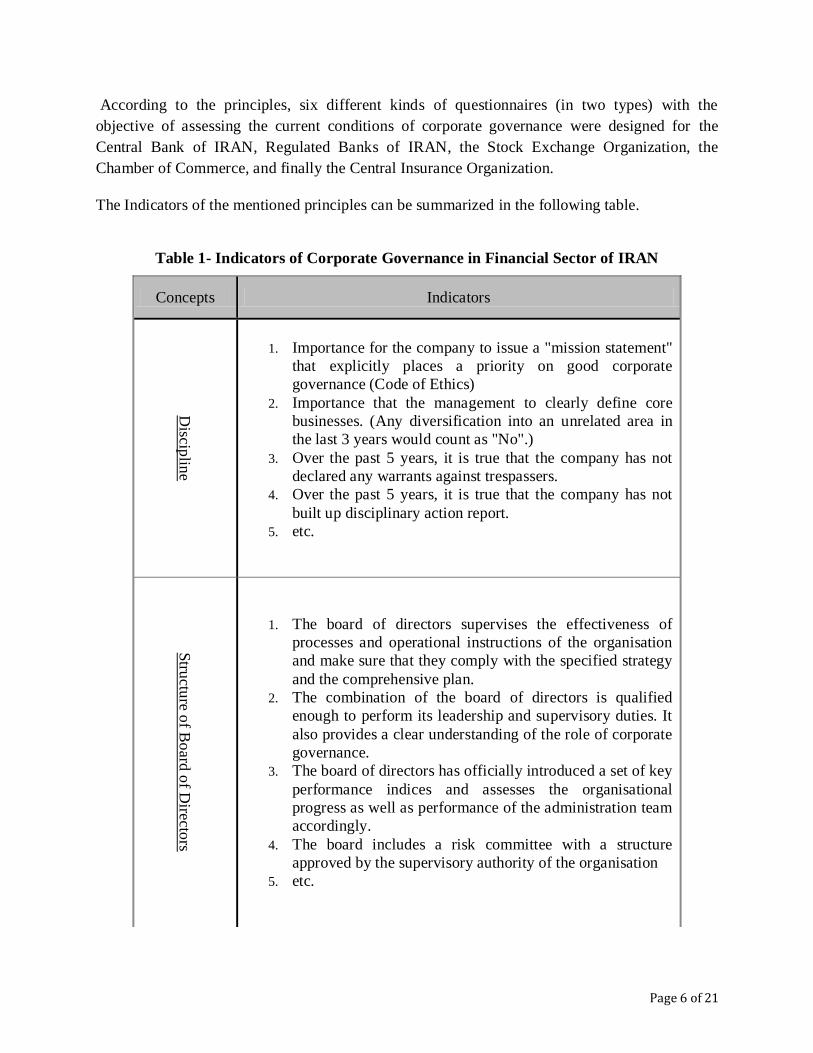

According to the principles, six different kinds of questionnaires (in two types) with the

objective of assessing the current conditions of corporate governance were designed for the

Central Bank of IRAN, Regulated Banks of IRAN, the Stock Exchange Organization, the

Chamber of Commerce, and finally the Central Insurance Organization.

The Indicators of the mentioned principles can be summarized in the following table.

Table 1- Indicators of Corporate Governance in Financial Sector of IRAN

Concepts Indicators

Discip

line

1. Importance for the company to issue a "mission statement"

that explicitly places a priority on good corporate

governance (Code of Ethics)

2. Importance that the management to clearly define core

businesses. (Any diversification into an unrelated area in

the last 3 years would count as "No".)

3. Over the past 5 years, it is true that the company has not

declared any warrants against trespassers.

4. Over the past 5 years, it is true that the company has not

built up disciplinary action report.

5. etc.

Stru

cture o

f Bo

ard o

f Directo

rs

1. The board of directors supervises the effectiveness of

processes and operational instructions of the organisation

and make sure that they comply with the specified strategy

and the comprehensive plan.

2. The combination of the board of directors is qualified

enough to perform its leadership and supervisory duties. It

also provides a clear understanding of the role of corporate

governance.

3. The board of directors has officially introduced a set of key

performance indices and assesses the organisational

progress as well as performance of the administration team

accordingly.

4. The board includes a risk committee with a structure

approved by the supervisory authority of the organisation

5. etc.

Page 7 of 21

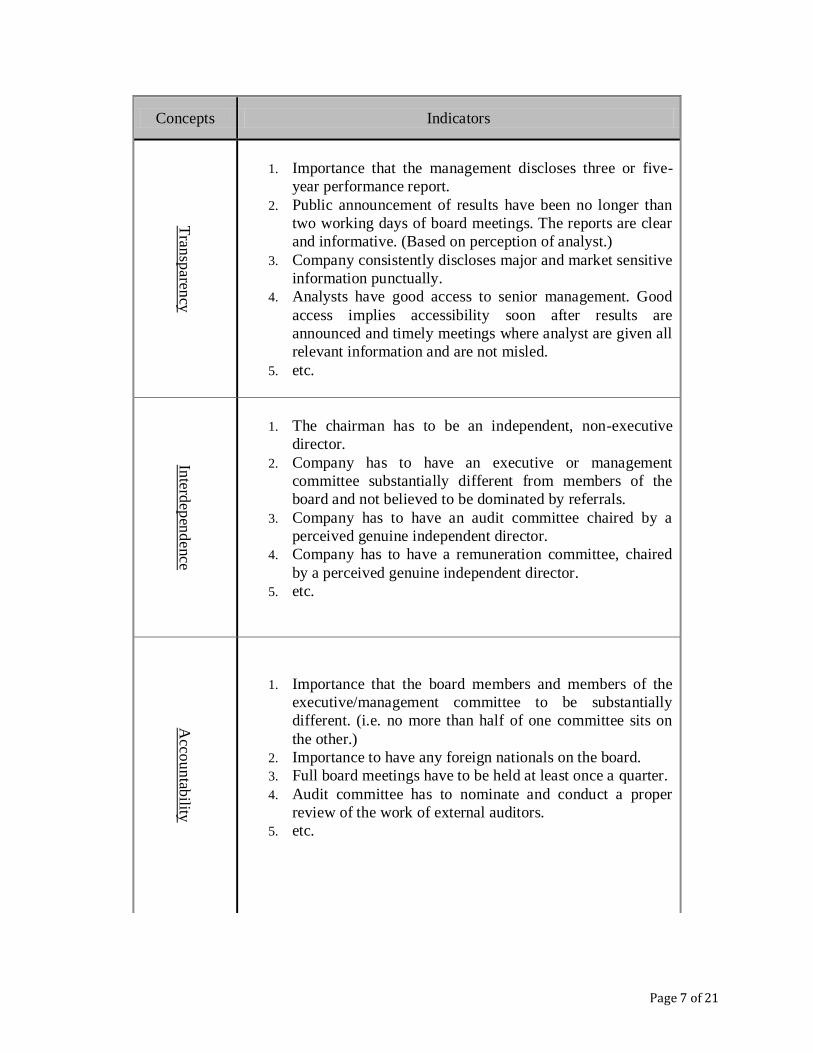

Concepts Indicators

Tran

sparen

cy

1. Importance that the management discloses three or five-

year performance report.

2. Public announcement of results have been no longer than

two working days of board meetings. The reports are clear

and informative. (Based on perception of analyst.)

3. Company consistently discloses major and market sensitive

information punctually.

4. Analysts have good access to senior management. Good

access implies accessibility soon after results are

announced and timely meetings where analyst are given all

relevant information and are not misled.

5. etc.

Interd

epen

den

ce

1. The chairman has to be an independent, non-executive

director.

2. Company has to have an executive or management

committee substantially different from members of the

board and not believed to be dominated by referrals.

3. Company has to have an audit committee chaired by a

perceived genuine independent director.

4. Company has to have a remuneration committee, chaired

by a perceived genuine independent director.

5. etc.

A

ccou

ntab

ility

1. Importance that the board members and members of the

executive/management committee to be substantially

different. (i.e. no more than half of one committee sits on

the other.)

2. Importance to have any foreign nationals on the board.

3. Full board meetings have to be held at least once a quarter.

4. Audit committee has to nominate and conduct a proper

review of the work of external auditors.

5. etc.

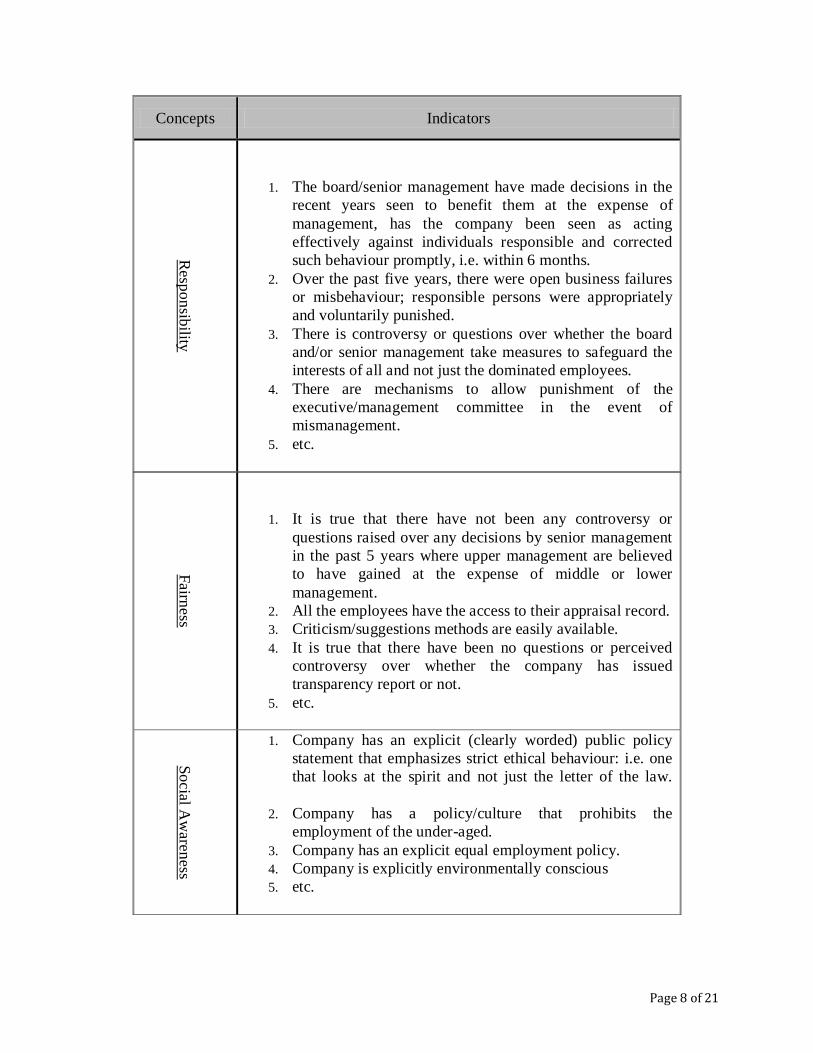

Page 8 of 21

Fairn

ess

1. It is true that there have not been any controversy or

questions raised over any decisions by senior management

in the past 5 years where upper management are believed

to have gained at the expense of middle or lower

management.

2. All the employees have the access to their appraisal record.

3. Criticism/suggestions methods are easily available.

4. It is true that there have been no questions or perceived

controversy over whether the company has issued

transparency report or not.

5. etc.

So

cial Aw

areness

1. Company has an explicit (clearly worded) public policy

statement that emphasizes strict ethical behaviour: i.e. one

that looks at the spirit and not just the letter of the law.

2. Company has a policy/culture that prohibits the

employment of the under-aged.

3. Company has an explicit equal employment policy.

4. Company is explicitly environmentally conscious

5. etc.

Concepts Indicators

Resp

on

sibility

1. The board/senior management have made decisions in the

recent years seen to benefit them at the expense of

management, has the company been seen as acting

effectively against individuals responsible and corrected

such behaviour promptly, i.e. within 6 months.

2. Over the past five years, there were open business failures

or misbehaviour; responsible persons were appropriately

and voluntarily punished.

3. There is controversy or questions over whether the board

and/or senior management take measures to safeguard the

interests of all and not just the dominated employees.

4. There are mechanisms to allow punishment of the

executive/management committee in the event of

mismanagement.

5. etc.

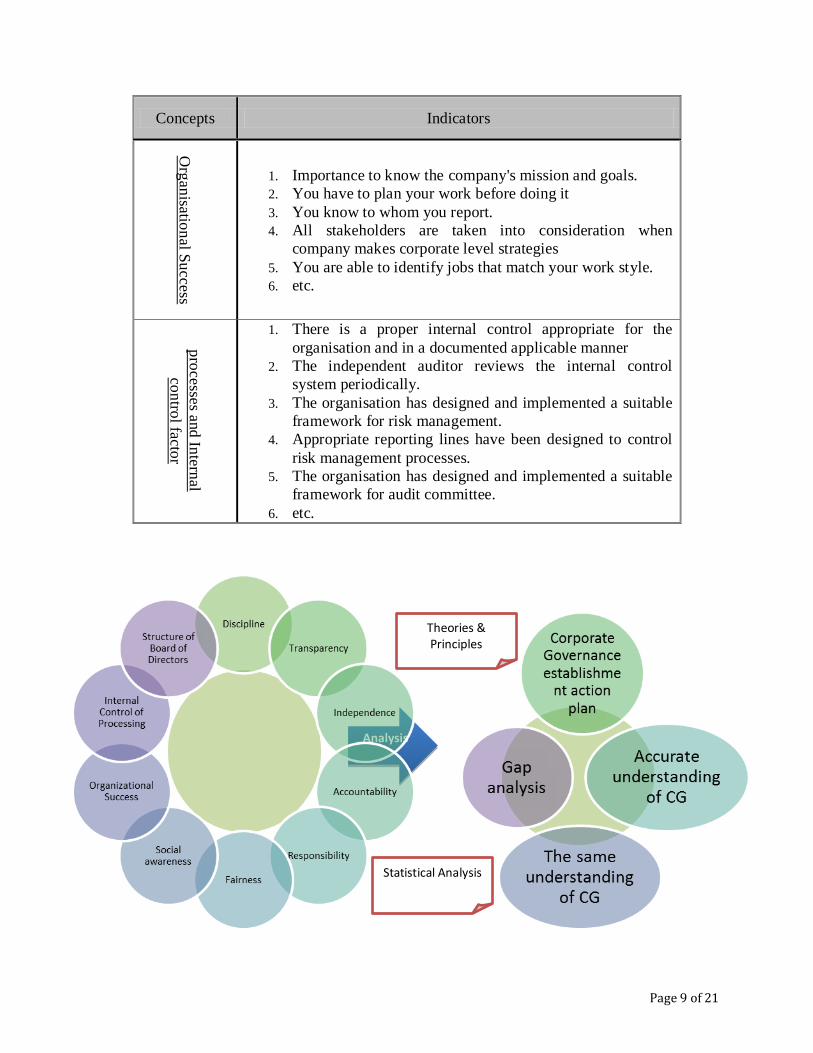

Page 9 of 21

Analysis

Org

anisatio

nal S

uccess

1. Importance to know the company's mission and goals.

2. You have to plan your work before doing it

3. You know to whom you report.

4. All stakeholders are taken into consideration when

company makes corporate level strategies

5. You are able to identify jobs that match your work style.

6. etc.

pro

cesses and

Intern

al

con

trol facto

r

1. There is a proper internal control appropriate for the

organisation and in a documented applicable manner

2. The independent auditor reviews the internal control

system periodically.

3. The organisation has designed and implemented a suitable

framework for risk management.

4. Appropriate reporting lines have been designed to control

risk management processes.

5. The organisation has designed and implemented a suitable

framework for audit committee.

6. etc.

Concepts Indicators

Theories & Principles

Statistical Analysis

Page 10 of 21

3. Statistical and Conceptual Analysis of Questionnaire Pretest of

Corporate Governance

In this part, we worked on the reliability of the questionnaires by working on stability and

validity of each part and time estimation which is needed to answer the entire each questionnaire

by averaging the time consuming by responders.

In this case, first of all we calculated the internal consistency reliability of the questionnaire by

calculating the Cronbach's Alpha which is widely used nowadays. We had some missing data in

only one question that shows the accuracy of our discussion to repliers. We imputed this missing

value with missing values imputation method discussed by me in 2002.6 The Cronbach's Alpha

of the whole scale was 0.931 for 38 items, showing the high level of internal consistency and

suggesting that items are homogenous, however, a few number of items asking the same question

in slightly different ways. Hence, we calculated Cronbach's Alpha for each principle separately

without considering the Control Questions which could cause some kinds of bias. Secondly, we

identified the questions with no response or less response and investigated the main results. It

was done by calculating the correlation between the two questions in one principle and finds out

the questions with high correlation and merging these questions after confirming the sameness of

their concepts. Finally, we estimated the total time of response to the questionnaires by using

confidence interval concepts of statistics applied on the recorded time.

Although Cronbach's Alpha is widely used nowadays, we were aware of some certain problems

related to it. The first problem was that alpha was dependent not only on the magnitude of the

correlations among items, but also on the number of items in the scale. As we know, a scale can

be made to look more 'homogenous' simply by doubling the number of items, even though the

average correlation remains the same. This leads directly to the second problem. If we have two

scales which each measures a distinct aspect and combines them to form one long scale, alpha

would probably be high, although the merged scale is obviously tapping two different attributes.

Third, for too high alpha, we got concerned about a high level of item redundancy; that is, a

number of items asking the same question in slightly different ways. Consequently, in this

research, we tried to find the adequate number of items with a comprehensive look at the all

aspects, and as we had collected a significant number of responses, we also estimated the

measurement errors directly using Confirmatory Factor Analysis for the final data set. Item

reliability was calculated as estimated error, while a cut-off point of 0.8 works for us and

construct reliability was also calculated.

In addition to the mentioned items above, we propose to look at the one of my last articles for

some other measures and procedures to work with validity, reliability, and consistency of

measurement instruments7. Most appropriate in our situation was the use of categorical principal

6 Ashofteh,A.(2002) 7 Ashofteh,A.(2003)

Page 11 of 21

component analysis. This provided us with detailed information about the measurement of the

response categories of each item in relation to the other items and the items as a whole given all

the scores of the respondents.

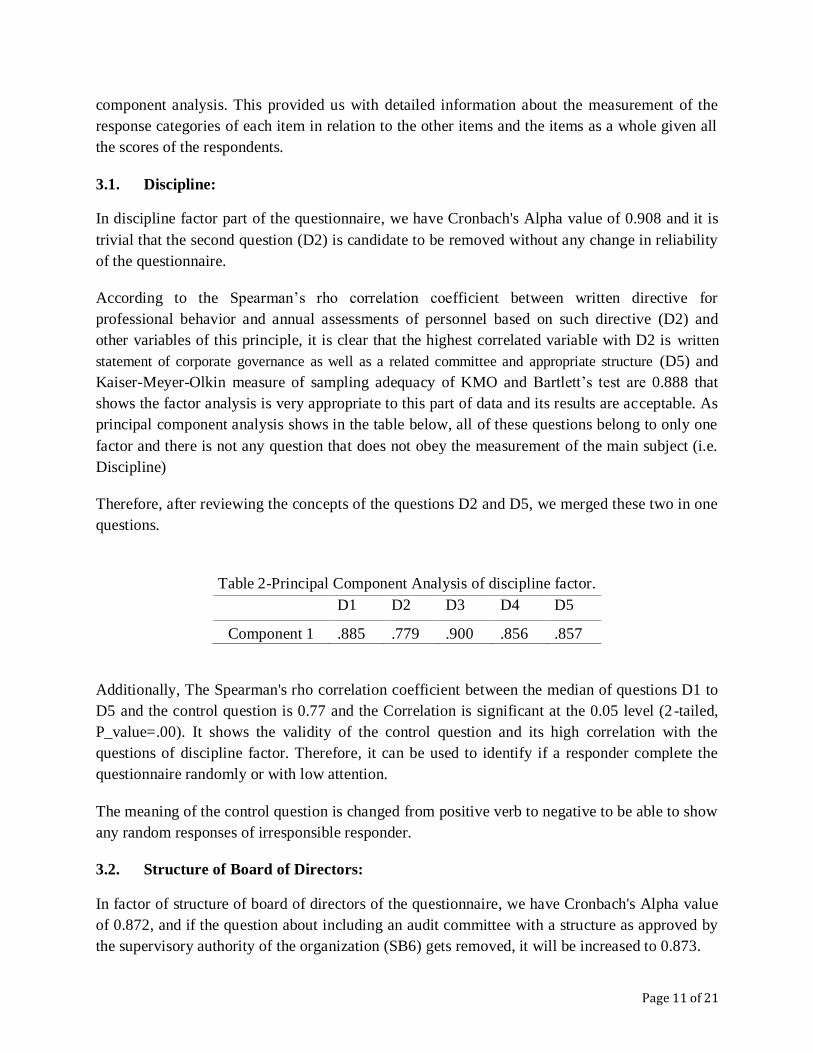

3.1. Discipline:

In discipline factor part of the questionnaire, we have Cronbach's Alpha value of 0.908 and it is

trivial that the second question (D2) is candidate to be removed without any change in reliability

of the questionnaire.

According to the Spearman’s rho correlation coefficient between written directive for

professional behavior and annual assessments of personnel based on such directive (D2) and

other variables of this principle, it is clear that the highest correlated variable with D2 is written

statement of corporate governance as well as a related committee and appropriate structure (D5) and

Kaiser-Meyer-Olkin measure of sampling adequacy of KMO and Bartlett’s test are 0.888 that

shows the factor analysis is very appropriate to this part of data and its results are acceptable. As

principal component analysis shows in the table below, all of these questions belong to only one

factor and there is not any question that does not obey the measurement of the main subject (i.e.

Discipline)

Therefore, after reviewing the concepts of the questions D2 and D5, we merged these two in one

questions.

Table 2-Principal Component Analysis of discipline factor.

D1 D2 D3 D4 D5

Component 1 .885 .779 .900 .856 .857

Additionally, The Spearman's rho correlation coefficient between the median of questions D1 to

D5 and the control question is 0.77 and the Correlation is significant at the 0.05 level (2 -tailed,

P_value=.00). It shows the validity of the control question and its high correlation with the

questions of discipline factor. Therefore, it can be used to identify if a responder complete the

questionnaire randomly or with low attention.

The meaning of the control question is changed from positive verb to negative to be able to show

any random responses of irresponsible responder.

3.2. Structure of Board of Directors:

In factor of structure of board of directors of the questionnaire, we have Cronbach's Alpha value

of 0.872, and if the question about including an audit committee with a structure as approved by

the supervisory authority of the organization (SB6) gets removed, it will be increased to 0.873.

Page 12 of 21

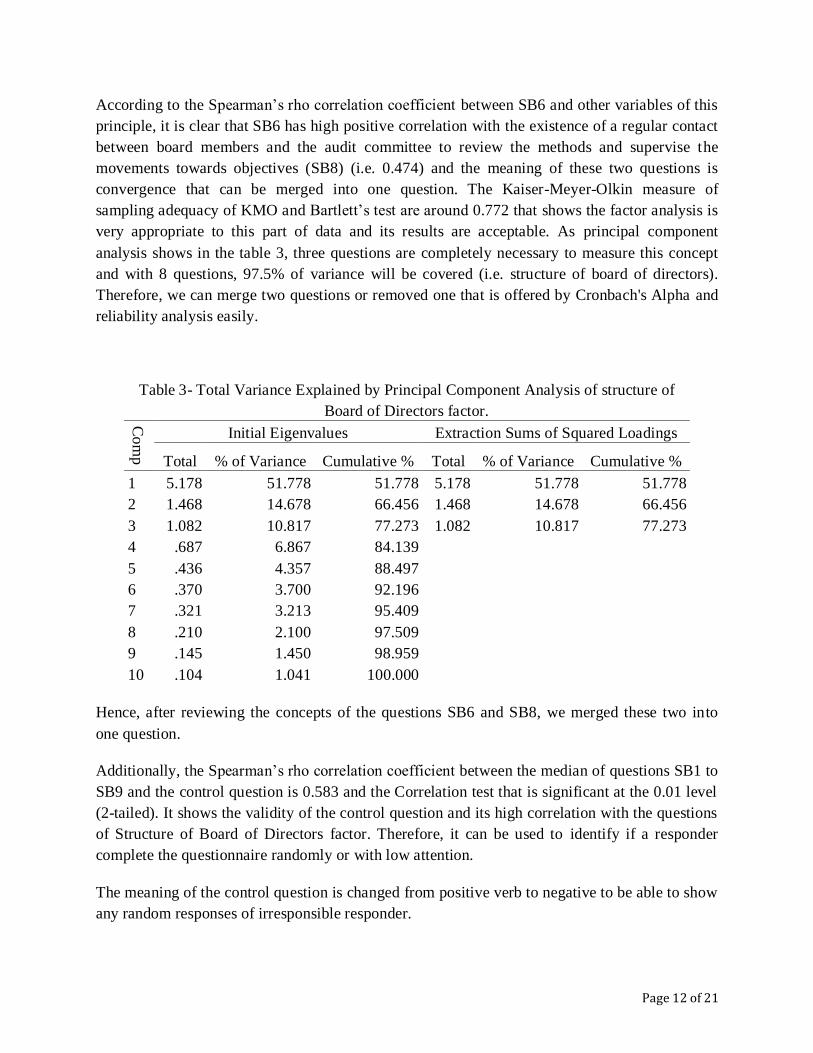

According to the Spearman’s rho correlation coefficient between SB6 and other variables of this

principle, it is clear that SB6 has high positive correlation with the existence of a regular contact

between board members and the audit committee to review the methods and supervise the

movements towards objectives (SB8) (i.e. 0.474) and the meaning of these two questions is

convergence that can be merged into one question. The Kaiser-Meyer-Olkin measure of

sampling adequacy of KMO and Bartlett’s test are around 0.772 that shows the factor analysis is

very appropriate to this part of data and its results are acceptable. As principal component

analysis shows in the table 3, three questions are completely necessary to measure this concept

and with 8 questions, 97.5% of variance will be covered (i.e. structure of board of directors).

Therefore, we can merge two questions or removed one that is offered by Cronbach's Alpha and

reliability analysis easily.

Table 3- Total Variance Explained by Principal Component Analysis of structure of

Board of Directors factor.

Co

mp

Initial Eigenvalues Extraction Sums of Squared Loadings

Total % of Variance Cumulative % Total % of Variance Cumulative %

1 5.178 51.778 51.778 5.178 51.778 51.778

2 1.468 14.678 66.456 1.468 14.678 66.456

3 1.082 10.817 77.273 1.082 10.817 77.273

4 .687 6.867 84.139

5 .436 4.357 88.497

6 .370 3.700 92.196

7 .321 3.213 95.409

8 .210 2.100 97.509

9 .145 1.450 98.959

10 .104 1.041 100.000

Hence, after reviewing the concepts of the questions SB6 and SB8, we merged these two into

one question.

Additionally, the Spearman’s rho correlation coefficient between the median of questions SB1 to

SB9 and the control question is 0.583 and the Correlation test that is significant at the 0.01 level

(2-tailed). It shows the validity of the control question and its high correlation with the questions

of Structure of Board of Directors factor. Therefore, it can be used to identify if a responder

complete the questionnaire randomly or with low attention.

The meaning of the control question is changed from positive verb to negative to be able to show

any random responses of irresponsible responder.

Page 13 of 21

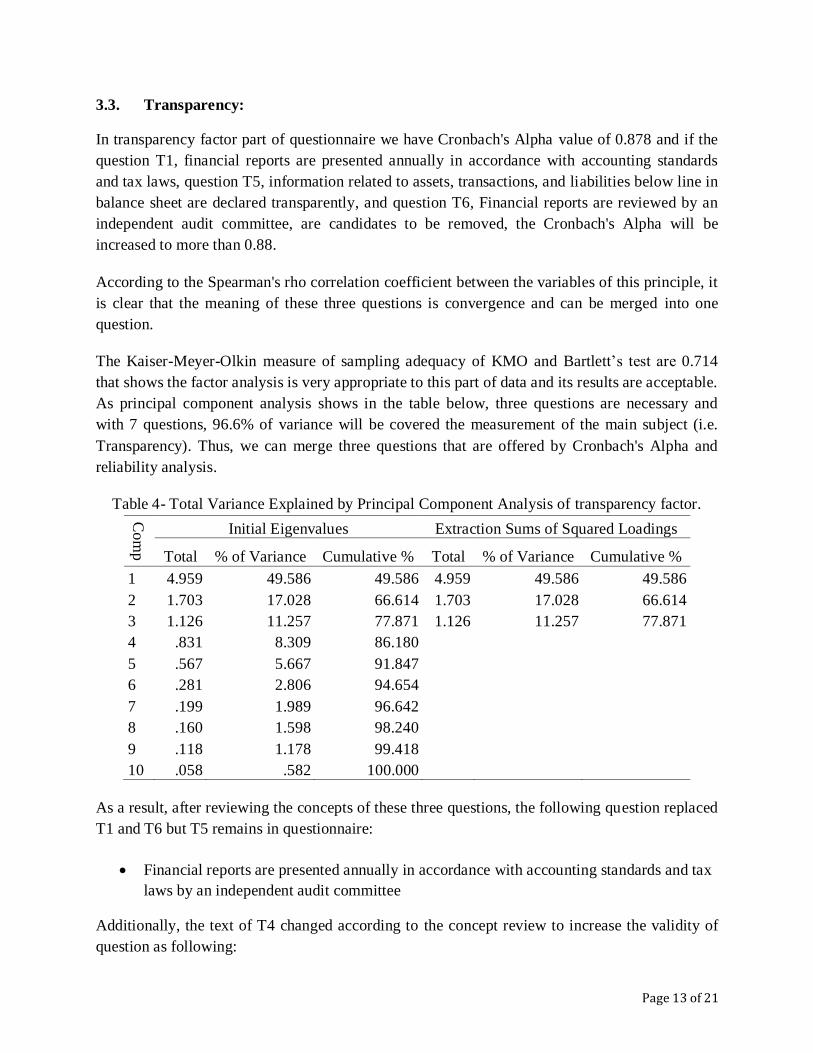

3.3. Transparency:

In transparency factor part of questionnaire we have Cronbach's Alpha value of 0.878 and if the

question T1, financial reports are presented annually in accordance with accounting standards

and tax laws, question T5, information related to assets, transactions, and liabilities below line in

balance sheet are declared transparently, and question T6, Financial reports are reviewed by an

independent audit committee, are candidates to be removed, the Cronbach's Alpha will be

increased to more than 0.88.

According to the Spearman's rho correlation coefficient between the variables of this principle, it

is clear that the meaning of these three questions is convergence and can be merged into one

question.

The Kaiser-Meyer-Olkin measure of sampling adequacy of KMO and Bartlett’s test are 0.714

that shows the factor analysis is very appropriate to this part of data and its results are acceptable.

As principal component analysis shows in the table below, three questions are necessary and

with 7 questions, 96.6% of variance will be covered the measurement of the main subject (i.e.

Transparency). Thus, we can merge three questions that are offered by Cronbach's Alpha and

reliability analysis.

Table 4- Total Variance Explained by Principal Component Analysis of transparency factor.

Co

mp

Initial Eigenvalues Extraction Sums of Squared Loadings

Total % of Variance Cumulative % Total % of Variance Cumulative %

1 4.959 49.586 49.586 4.959 49.586 49.586

2 1.703 17.028 66.614 1.703 17.028 66.614

3 1.126 11.257 77.871 1.126 11.257 77.871

4 .831 8.309 86.180

5 .567 5.667 91.847

6 .281 2.806 94.654

7 .199 1.989 96.642

8 .160 1.598 98.240

9 .118 1.178 99.418

10 .058 .582 100.000

As a result, after reviewing the concepts of these three questions, the following question replaced

T1 and T6 but T5 remains in questionnaire:

Financial reports are presented annually in accordance with accounting standards and tax

laws by an independent audit committee

Additionally, the text of T4 changed according to the concept review to increase the validity of

question as following:

Page 14 of 21

In addition to the usual financial reports, the organizational annual reports include risks

and other useful reports which could be used by reader to better interpretation of financial

statements.

Furthermore, The Spearman's rho correlation coefficient between the median of questions and

the control question is 0.17 and the Correlation is not significant at the 0.05 level (2 -tailed,

P_value=0.47). It shows the validity of the control question of this part because in this factor the

meaning of the control question is opposite of other regular questions. Therefore, its low

correlation with the questions of transparency factor shows its high validity and it can be used to

identify if a responder complete the questionnaire randomly or with low attention.

3.4. Interdependence:

In independence factor part of questionnaire we have Cronbach's Alpha value of 0.861 and no

question is candidate to be removed.

Hotelling's T-Squared test shows that the answers to these questions are not different

meaningfully and it shows the possibility of merging some questions into this principle. Anyway,

owing to the important parts of independency which are asked in each question, no question is

candidate to be removed.

Table 5- Hotelling's T-Squared of independence factor.

Hotelling's T-Squared F df1 df2 Sig

11.719 2.467 4 16 .087

Finally, three questions were added to strengthen the measurement of independency from the

third parties.

3.5. Accountability:

In accountability factor part of questionnaire we have Cronbach's Alpha value of 0.116 and if the

A1, board members are different from administration team, is candidate to be removed, that the

Cronbach's Alpha will be increased to more than 0.68.

According to the Spearman's rho correlation coefficient between the variables of this principle, it

is clear that the A1 not only do not relate to the other questions, but also is completely opposite.

Accordingly, after reviewing the concept of A1, this question got removed from the

questionnaire completely.

Page 15 of 21

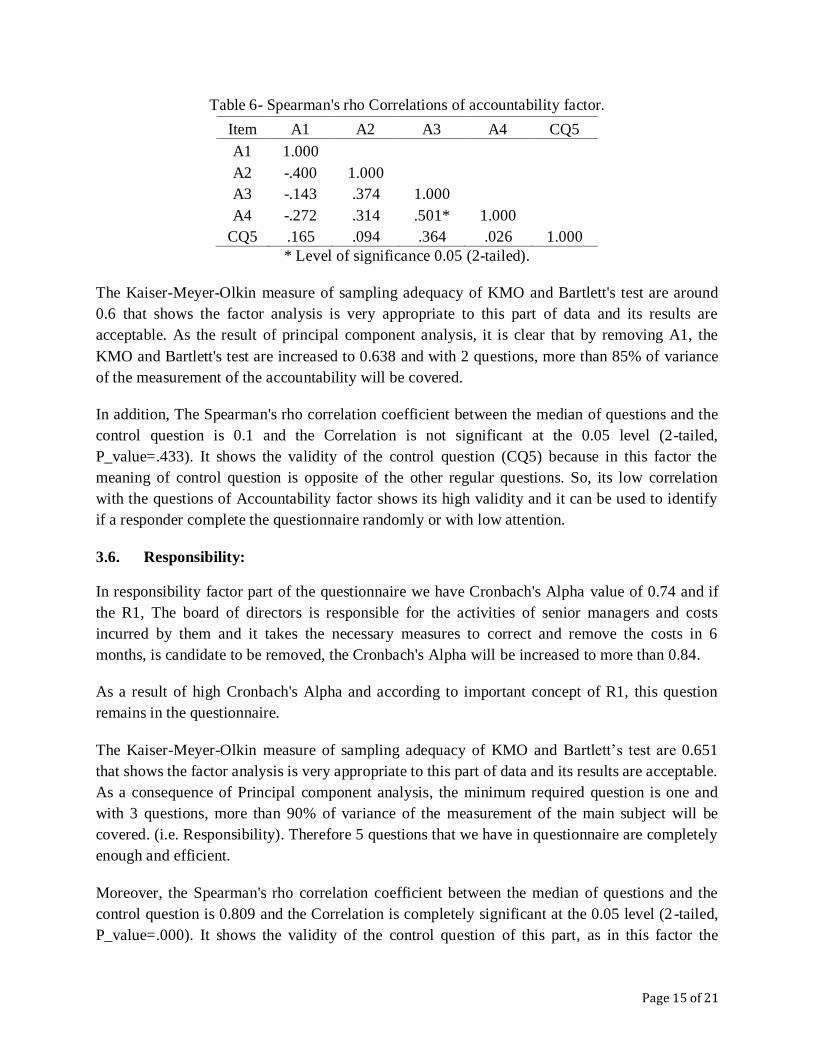

Table 6- Spearman's rho Correlations of accountability factor.

Item A1 A2 A3 A4 CQ5

A1 1.000

A2 -.400 1.000

A3 -.143 .374 1.000

A4 -.272 .314 .501* 1.000

CQ5 .165 .094 .364 .026 1.000

* Level of significance 0.05 (2-tailed).

The Kaiser-Meyer-Olkin measure of sampling adequacy of KMO and Bartlett's test are around

0.6 that shows the factor analysis is very appropriate to this part of data and its results are

acceptable. As the result of principal component analysis, it is clear that by removing A1, the

KMO and Bartlett's test are increased to 0.638 and with 2 questions, more than 85% of variance

of the measurement of the accountability will be covered.

In addition, The Spearman's rho correlation coefficient between the median of questions and the

control question is 0.1 and the Correlation is not significant at the 0.05 level (2-tailed,

P_value=.433). It shows the validity of the control question (CQ5) because in this factor the

meaning of control question is opposite of the other regular questions. So, its low correlation

with the questions of Accountability factor shows its high validity and it can be used to identify

if a responder complete the questionnaire randomly or with low attention.

3.6. Responsibility:

In responsibility factor part of the questionnaire we have Cronbach's Alpha value of 0.74 and if

the R1, The board of directors is responsible for the activities of senior managers and costs

incurred by them and it takes the necessary measures to correct and remove the costs in 6

months, is candidate to be removed, the Cronbach's Alpha will be increased to more than 0.84.

As a result of high Cronbach's Alpha and according to important concept of R1, this question

remains in the questionnaire.

The Kaiser-Meyer-Olkin measure of sampling adequacy of KMO and Bartlett’s test are 0.651

that shows the factor analysis is very appropriate to this part of data and its results are acceptable.

As a consequence of Principal component analysis, the minimum required question is one and

with 3 questions, more than 90% of variance of the measurement of the main subject will be

covered. (i.e. Responsibility). Therefore 5 questions that we have in questionnaire are completely

enough and efficient.

Moreover, the Spearman's rho correlation coefficient between the median of questions and the

control question is 0.809 and the Correlation is completely significant at the 0.05 level (2 -tailed,

P_value=.000). It shows the validity of the control question of this part, as in this factor the

Page 16 of 21

meaning of control question is similar to the other regular questions. Thus, its high correlation

with the questions of responsibility factor shows its high validity and it can be used to identify if

a responder complete the questionnaire randomly or with low attention.

The meaning of the control question is changed from positive verb to negative to be able to show

any random responses of irresponsible responder.

3.7. Fairness:

In fairness factor part of questionnaire we have Cronbach's Alpha value of 0.55 and if the F2, all

members of staff have access to records of their assessment and are given the right to offer

criticisms as well as suggestions easily, is candidate to be removed, that the Cronbach's Alpha

will be increased to more than 0.76.

As a result of high Cronbach's Alpha and according to important concept of F2, this question

remains in the questionnaire.

The Kaiser-Meyer-Olkin measure of sampling adequacy of KMO and Bartlett's test are around

0.7 that show the factor analysis is very appropriate to this part of data and its results are

acceptable. As the result of principal component analysis, the minimum required question is at

least two questions, and with 4 questions, more than 90% of variance of the measurement of the

fairness factor will be covered. Therefore, 6 questions that we have in questionnaire are

completely efficient and sufficient.

Additionally, the Spearman’s rho correlation coefficient between the median of questions and the

control question is -0.108 and the Correlation is not significant at the 0.05 level (2-tailed,

P_value=0.651). It shows the no validity of the control question of fairness (CQ7), since in this

factor the meaning of control question is similar to the other regular questions.

Consequently, its low correlation with the questions of fairness factor shows its poor validity and

it recommends probable changes in the questions and more attention.

After reviewing the meaning of the questions, it was approved that the meaning of the questions

is not appropriate as a control question and it was changed as follows:

Old CQ7: The rights of deposit holders and shareholders are clearly defined and protected in the

organizational policies as well as its corporate governance directive.

New CQ7: Totally, the rights of all stockholders are not clearly defined or protected.

As it is clear, the meaning of the control question is also changed from positive verb to negative

to be able to show any random responses of irresponsible responder.

3.8. Social awareness:

Page 17 of 21

In social awareness factor part of questionnaire we have Cronbach's Alpha value of 0.44 and no

question is candidate to be removed. Therefore, this analysis suggests that some questions will be

added to the measurement of this principal.

Furthermore, the Kaiser-Meyer-Olkin measure of sampling adequacy of KMO and Bartlett’s test

are around 0.35 that shows the factor analysis is not appropriate to this part of data and the result

of principal component analysis confirmed that the questions of this principal shall be reviewed

completely for better measurement.

Study on the concepts of this part shows that the guidance of the statistical analysis is completely

right and this part of the questionnaire changed completely by removing and adding some

questions.

Additionally, the Spearman’s rho correlation coefficient between the median of questions and the

control question is 0.41 and the Correlation is not significant at the 0.05 level (2 -tailed,

P_value=0.07). It shows that no validity of the control question of this part, as in this factor the

meaning of control question is similar to the other regular questions. Thus, its low correlation

with the questions of Social awareness factor shows its poor validity and it recommends some

changes in the question and more attention.

The meaning of the control question is also changed from positive verb to negative to be able to

show any random responses of irresponsible responder.

3.9. Organizational Success:

In organizational success factor part of questionnaire we have Cronbach's Alpha value of 0.93

and if the questions OS4, employees current jobs match the work procedures, and OS6, there is a

rewarding policy in the organization and all staff are aware of it, are candidate to be removed,

that the Cronbach's Alpha will be increased to more than 0.93.

Due to high Cronbach's Alpha and according to important concept of F2, this question remains in

the questionnaire.

The Kaiser-Meyer-Olkin measure of sampling adequacy of KMO and Bartlett’s test are 0.825

that shows the factor analysis is very appropriate to this part of data and its results are acceptable.

As the result of principal component analysis, the minimum required question is at least two

questions, and with 5 questions, more than 90% of variance of the measurement of the main

subject will be covered. (i.e. Organizational Success). Therefore, 9 questions that we have in the

questionnaire are more than the requirement. It strongly recommends us to remove some

specified questions.

After reviewing the questions, it became clear that the concepts of the questions OS6, OS7, there

is a suitable assessment system to reward the employees and they have accepted and approved

Page 18 of 21

the system, and OS8, employees proposals are taken into consideration while reviewing the

assessment system, are very similar and they can be merged.

Moreover, the Spearman’s rho correlation coefficient between the median of questions and the

control question is 0.637 and the Correlation is not significant at the 0.05 level (2-tailed,

P_value=.003). It shows the validity of the control question, since in this factor the meaning of

the control question is similar to the other regular questions. So, its high correlation with the

questions of Organizational Success factor shows its good validity.

As it is clear, the meaning of the control question is also changed from positive verb to negative

to be able to show any random responses of irresponsible responder.

3.10. The Internal Control of Processing:

In the internal control of processing factor part of questionnaire we have Cronbach's Alpha value

of 0.856 and if the IC1, there is a proper internal control appropriate for the organization and in a

documented applicable manner, and IC7, organization management supports the internal audit

unit and its reports in order to maintain and promote the effectiveness of the internal control

system, are candidates to be removed, that the Cronbach's Alpha will be increased to more than

0.88.

Hotelling's T-Squared test shows that the answers to these questions are not different

meaningfully and it shows the possibility of merging some questions into this principle.

Table 7- Hotelling's T-Squared test of Internal Control of Processing factor.

Hotelling's T-Squared F df1 df2 Sig

24.005 1.895 8 12 .153

In addition, the Kaiser-Meyer-Olkin measure of sampling adequacy of KMO and Bartlett’s test

are around 0.717 that shows the factor analysis is very appropriate to this part of data and its

results are acceptable. As the result of Principal component analysis, the minimum required

question is at least three questions, and with 5 questions, more than 90% of variance of the

measurement of the main subject will be covered. (i.e. The Internal Control of Processing).

Therefore, 9 questions that we have in questionnaire are more than the requirement of this

measurement.

According to the mentioned analysis above, we investigate the meaning of the questions and the

possibility of merging some of them.

The meaning of these two questions could be merged into one question easily:

Page 19 of 21

IC1: There is a proper internal control appropriate for the organization and in a documented

applicable manner.

IC2: The independent auditor reviews the internal control system periodically.

And also the following questions are the same:

IC6: Audit and risk committees are authorized to ask all managers and organization departments

for reports and data.

IC7: Organization management supports the internal audit unit and its reports so as to maintain

and promote the effectiveness of the internal control system.

The Spearman’s rho correlation coefficient between the median of questions and the control

question is 0.584 and the Correlation is significant at the 0.05 level (2-tailed, P_value=.007). It

shows no validity of the control question (CQ10), as in this factor the meaning of control

question is against the other regular questions. Accordingly, its high correlation with the

questions of the internal control of processing factor shows its poor validity and it recommends

probable changes in the question and more attention.

After reviewing the meaning of the question, it was approved that the meaning of the question is

not appropriate as a control question and it was changed as follows:

Old CQ10: Internal control cannot assist the organization in the achievement of its business

objectives.

New CQ10: According to the experience, several internal controls of system were not very

helpful in organization goal achievement.

As it is clear, the meaning of the control question is also changed from positive verb to negative

to be able to show any random responses of irresponsible responder.

4. Concluding Remarks

In this research, we have illustrated the principles of corporate governance and we have designed

and tested a standard method and tools to measure the current situation in different areas of

financial system of IRAN. They could be used to show that how the lack of good corporate

(bank) governance can lead the Iranian financial system to a crisis and ultimately to an economic

recession. Obviously, the failure of the financial system of country is triggered by a number of

factors. However, the unsound and unsafe banking practices of bank management exacerbate the

situation and are possible in the lack of adequate corporate governance as a main risk factor.

Page 20 of 21

5. Suggestions:

The message of the importance of good corporate governance, particularly in the financial sector

of IRAN, is promoting general stability and successful functioning of the overall financial

system. Hence, we have to be very active at promoting sound corporate governance in the

financial sector of IRAN, especially in banks, by using these standard domestic questionnaires

which are obtained in this research.

References

Ashofteh,A. (2002): Estimating Systematic Missing Values by Simulation. Proceeding of Tarbiat

Modares University, 2: 304-311.

Ashofteh,A. (2003): Survey on Evaluating Missing Values. Journal of Andishe_ye_Amari (Expository

Journal of IRANIAN STATISTCAL SOCIETY), 8(2): 40-47.

Ashofteh,A. (2003):Robust Estimators of Location and Scale. Journal of Andishe_ye_Amari (Expository

Journal of IRANIAN STATISTCAL SOCIETY), 8(1): 28-35.

Attiya,Y., and Robina Iqbal, (2010). Corporate Governance in Pakistan: Corporate Valuation, Ownership

and Financing, PIDE-Working Papers 2010:57, Pakistan Institute of Development Economics.

Bultez Pierre,A. (2005): Corporate Governance Procedures and Check-list. National Bank of Slovakia.

Cadbury Commission (1992):Report of the Committee on the Financial Aspects of Corporate

Governance. Gee: London.

Giovanni, F. (2003):Corporate Governance in Banking and Economic Performance - Future Options for

People’s Republic of China. Asian Development Bank Institute.

Ghorbani, S., and, Seyed Tabaie,Z. (2013):Does corporate governance matter in Iran? International

Journal of Banking and Finance,9(3), Article 3.

Ilyas,M., and Raffiq,M. (2012), Impact of Corporate Governance on Perceived Organisational Success.

Journal of Business and Social Science.

Lum Chee Soon and Nam Sang-Woo (2006):Corporate Governance of Banks in Asia. Volume 1.

Mungule, O. (2005):Economic and Corporate Governance and Accountability in Southern Africa.

Economic Commission for Africa.

Miles, L. (2010):Transplanting the Anglo American CG model into Asian countries: prospects and

practicality. Middle Se University.

Sang-woo,N. (2006):A Study of Indonesia, Republic of Korea, Malaysia, and Thailand. Corporate

governance of banks in Asia; Volume 1, ISBN: 4899740115.

Nathan,S., Viincent,R. (2007):From knowledge to wisdom: the case of corporate governance in Islamic

Banking. Journal of Information and Knowledge Management Systems, 37(4):471-483.

Suzanne, C. and Neil et. al. (2006):Corporate Governance and Human Resource Management. British