29

Corporate Overview

Corporate Overview

Introduction to Cumberland Farms

Cumberland Farms Snapshot

Company Overview Family-owned fuel retailer and convenience store operator with 563

locations across Connecticut, Rhode Island, Massachusetts, Vermont, New Hampshire, Maine, New York and Florida

Market leading position in the Northeast

Own ~88% of the store locations

In early 2009, Cumberland Farms launched a long-term rebranding campaign under the Accelerate In-Store Mix (“AIM”) format featuring a food-centric concept, enhanced interior design and a new logo

Achieved significant Average Per Store Week (“APSW”) growth from this initiative as well as closing / selling non-core locations

The Company was founded in 1939 by the Haseotes family

New Store Design (AIM Format)

Targeting +80% AIM formatted stores in next 2 years (70% today)

58%

42% 31%

69%

Strong Financial Results (LTM 9/30/18)

Segment Breakdown (LTM 9/30/18)

Revenue Gross Profit

Merchandise

Fuel

Total Revenue: $4.0 billion

Merchandise Sales: $1.2 billion

Fuel Gallons: 1.0 billion

Adjusted EBITDA: $149.4 million

Merchandise

Fuel

Established Brand with a Long Operating History

Ari Haseotestakes over

responsibilities of retail division

20082017

AIM next generation

launch

Early 1980’sLaunched coffee

offering

1939Founded by Vasilios

and Aphrodite Haseotes in

Cumberland, RI

2009Began investing in

AIM concept stores to better serve

customers

Mid 1950’sBegan selling and

producing ice cream and dairy products

1986Acquired

Northeast and Mid-Atlantic

marketing assets of Gulf Oil

1976Private label

beverage and bakery commissary

Enhanced breakfast offering as a part of

the AIM initiative

Late 2000’s

~2012Introduced pizza

offering as a part of the AIM initiative

Late 1990’sExpanded hot and

cold beverage offering

Exercised its option to acquire all outstanding

shares ofGulf Oil LP

2005

Product introductions

1971Opened first

fuel station inPutnam, CT

2015Sold Gulf and

Assured Dealer businesses

to ArcLight Capital Partners

2014Opened the

Culinary Center at its

Distribution Facility in

Westborough, MA

Recap of Recent Strategic Activity

Sale of Gulf Oil and Assured Dealer Division Singularly Focused on Retail Business With Four Key Tenets

Full Adoption of Mission, Vision and

Values based Culture

Continued Capital Investment in Store

Base

Deployment of Food & Beverage

Offerings

Focused Effort to Enhance Guest and

Team Member Experience and

Increase Efficiency

1

2

3

4

Two divisions divested on December 29, 2015 to ArcLight Capital Partners

Gulf Oil division was reported as a separate entity

Assured Dealer division was historically reported with the Retail segment in Cumberland Farms’ financial statements

Cumberland entered into a fuel supply agreement with the purchaser through 2019

Divestitures have further streamlined Company operations and have resulted in a more focused C-store business

Our Mission: To deliver the friendliest, cleanest and most

convenient customer experience by firstbeing the best place to work.

AIM Investments

142 155 165 174 176 20228 67 104 134 172 182170

222 269 308 348 384

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

AIM Remodels Major Capital Projects

Grow Foodservice Sales

Net Promoter Score

7% 16%

27% 21% 24%

43% 27%

33% 37% 37% 35% 46%

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

All CFI Shoppers AIM Shoppers

Pizza Coffee Breakfast

Number of locations

FLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFL

CTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRI

MAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMA

NJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPA

NYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNY

NHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNH

VTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVT

MEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEME

Leading C-Store Retailer in the Northeast and Florida

Company-operated convenience store network

Revenue from motor fuel sales, food sales, convenience merchandise and service sales

As of December 31, 2018, operated 563 stores

Approximately 88% owned stores

Many new AIM stores anticipated to be over 5,000 sq. ft., although now studying a more compact model

Up to 20 fueling positions for new AIM stores

560,000 sq. ft. owned manufacturing and distribution facility in Westborough, MA services all Northeast stores

Northeast

Florida

Northeast Stores:

515

Florida Stores:

48

Total Stores: 563

Second highest brand equity according to the Nielsen’s 2017 Store Choice Driver Report

39%

18%

14%

11%

5%

4% 3% 3% 3%

In-Store Operations

Key Categories Merchandise Mix

Cigarettes Foodservice Other Packaged BeveragesBeer & WineOther Tobacco

CandySalty Snacks

Dairy

Cigarettes

Foodservice

Private Label

Lower margin item, but crucial traffic driver Pricing driven by taxes in respective states Despite challenging regulatory environment, industry-

wide volume declines are mitigated as convenience stores gain share due to decisions by some retail channels to exit the category

Cigarettes represent 34.5% of merchandise sales when adjusted for the national state average excise taxes

Key focus area is currently slightly below industry average and represents a high margin opportunity

Coffee offering is key traffic driver “Chill Zone” (frozen / fountain beverage) Sandwich cases and fresh food / fresh bakery offering Opened Culinary Center in 2014 in order to supply

stores with fresh sandwiches, pizza and other fresh packaged products

Represents 10% of in-store sales Strong heritage in dairy products create logical and

compelling brand extension possibilities Important enhancement to overall store

experience and brand strength Expected to be key future margin driver

Sales Split

Foodservice Offering Private Label Offering

Representative Products

9.9%

21.8% 24.3%

Legacy Stores AIM Stores NACS Top Quartile

Foodservice and Private Label Growth

Private Label Foodservice Cumberland Farms has been driving higher margin foodservice

sales (fountain drinks, coffee, frozen drinks and sandwiches)

Coffee, one of the more popular offerings, is 7.1% of total merchandise sales as of March 31, 2018

Foodservice and dispensed beverage sales in AIM stores represent 21.8% of total merchandise sales vs. 9.9% in legacy stores

Cumberland has significantly closed the gap with NACS Top Quartile over the past few years as AIM store count increases

In fiscal 2007, foodservice comprised only 6.5% of merchandise sales in legacy stores

Private label products represent 10% of in-store sales

Marketed under the Cumberland Farms, Farmhouse and Farmhouse Premium brands

Base private label offering includes dairy products and other “everyday essentials” such as bread, water, sandwiches, juice, soda and chips

Farmhouse brand has expanded to candy and salty and sweet snacks –also markets hot, iced and take-home coffee products

Private label products are a key driver of margins and enhance the overall in-store customer experience and brand strength

Above average penetration compared to national brands within competing product categories

Continued focus on developing more differentiated and unique premium quality and priced products

Foodservice and Dispensed Beverages as% of Total Merchandise Sales

Merchandise Distribution & Supply

Competitive Advantage of a Closed-Loop System vs. Outsourced Model

Distribution and Supply Overview

Controlled number of stock keeping units (“SKUs”) at warehouse increases inventory turns

Increases freshness of inventory at store level Stores receive multiple

deliveries per week

Vendor consolidation (ice cream, dairy, perishables, bakery, foodservice, private label) provides fewer deliveries to each individual store

Increases speed-to-market on new items or product changes

Provides clear line of sight to total delivered cost of goods

Self-distribute three-fourths of merchandise (excluding motor fuel) through Westborough, MA warehouse and distribution facility

560,000 sq. ft. facility on 4.1 million sq. ft. of land with commissary and freezer capabilities

Fleet of leased and owned trucks supplies 500+ convenience stores and provides improved inventory management

Distribution service agreement with wholesale distributor; primary distributor of food products and convenience merchandise to Florida stores

Distribution center in the Northeast supplies this wholesale distributor weekly with foodservice and private label products

Remaining one-fourth of the merchandise is delivered via direct store delivery (e.g. Coca-Cola, Pepsi / Frito Lay and beer)

AdvantageCost

SavingsOperating

Efficiencies

Fuel Operations

(1)

Fuel Sales Overview

Fuel represents 68% of revenues and 42% of gross profit

Cumberland Farms established its SmartPay program in 2013 to provide greater savings for customers and promote brand loyalty

Payment program allows customers to save $0.10 on every gallon of fuel purchased and receive rewards for every 50 gallons of fuel purchased

Fuel breakdown as a percentage of FY2017 gallons:

Unleaded: 85%

Unleaded Plus: 5%

Super Unleaded: 7%

Diesel: 3%

Cumberland Farms was rated the nation’s favorite fueling station in a study by Market Force in May 2018

Leading Position and Scale in Attractive Markets

____________________(1) Population from 2016 U.S. Census (as of July 1, 2017), Number of stores from NACS 2016 SOI Report.(2) NACS Report as of December 31, 2016.(3) Represents store count as of September 30, 2018.(4) Market efficiency defined as gas gallon market share divided by gas outlet share.

CFI convenience stores and fuel stations are generally situated on well-traveled thoroughfares or other easily accessible sites in the Northeast and Florida

Population density, employment and personal income data are very favorable in the Northeast as compared to other regions of the U.S. (1)

Northeast has second fewest number of convenience stores per capita in the U.S. (1)

Lack of developable land combined with the regulatory and permitting considerations for fuel stations limit the threat of competition from new entrants

CFI’s Leading Position in Northeast Markets

U.S. Average

U.S. Convenience Stores per Capita (1)

Market Share by Store Count

(3)

Stores per 10,000 People

(4)(2)Market CFI Market MarketState Sites Sites Share Efficiency

RI 509 46 9.0% 1.42

MA 3,392 207 6.1% 1.62

NH 900 47 5.2% 1.09

ME 1,028 43 4.2% 1.38

CT 1,695 71 4.2% 1.73

VT 592 19 3.2% 1.12

NY 8,570 82 1.0% 1.21

Northeast 16,686 515 3.1%

FL 9,930 48 0.5% 0.98

Total 26,616 563 2.1%

3.57

4.37 4.63

5.71

0.00

1.00

2.00

3.00

4.00

5.00

6.00

West Northeast Midwest South

32%39%

46%38% 39%

43%

2015 2016 2017

Unaided Aided

Significant Brand Awareness and Customer Loyalty

CF Total AIM Competitors (4)

Is easy to get to 61% 77% 46%

My family has always shopped there 32% 43% 18%

Is a place I would go out of my way to shop at 26% 35% 14%

Is a store I trust 58% 71% 39%

Is a newer store 52% 82% 24%

Has a good reputation 61% 73% 40%

Has food or snacks that I crave 52% 62% 38%

The area where I make my coffee / get my fountain beverage is always clean 50% 62% 31%

The employees know me 20% 26% 14%

Their food is fresh 41% 51% 25%

Has a loyalty program that allows me to save money on gas or merchandise 39% 53% 22%

Is fast to get my hot food 38% 49% 25%

Restrooms are always clean 36% 47% 24%

Cumberland Farms Customer Loyalty Consumer Perceptions of Top Store Attributes 2018 – Cumberland Farms vs. Competition

Cumberland Farms Brand Awareness

Cumberland Farms has strong loyalty among customers

Unaided and aided awareness is growing

82 83 82

54% 53% 55%

2015 2016 2017

69 70 70

38% 35% 37%

2015 2016 2017

Brand Awareness

Performance of both Legacy and AIM stores is strong versus competitors

Relative strength for CF (index >= 120)

Legacy Store Model Loyalty Trends

AIM Store Model Loyalty Trends

Total PromotersCustomer Loyalty Index

33% 37% 37% 38%

56% 57% 58% 54%

2014 2015 2016 2017

All Stores New Stores

0100200300400500600700800

0

20,000

40,000

60,000

80,000

100,000

Jan-13 Feb-14 Mar-15 Mar-16 Apr-17 Apr-18

Number of Transactions Number of Enrollments

26%

28%

33%

13%

SmartPay Introduction

Introduction of SmartPay Loyalty Program Fuel Volume Breakdown by Method of Payment SmartPay program launched in 2013 to provide greater savings for

customers and promote brand loyalty

Payment program allows customers to save $0.10 on every gallon of fuel purchased

Receive rewards for every 50 gallons of fuel purchased, plus free monthly product coupons on favorite items such as Farmhouse Blend coffee and Hyper-Freeze beverages

Pizza and breakfast sandwich loyalty clubs launched in FY ‘18

Enables customers to activate fuel pump from mobile device as well as pay for in-store merchandise

SmartPay gallons have grown to ~26% of total gallons sold as of March 31, 2018

Offers two mobile apps for personal and business uses

Awareness of SmartPay Continues to Grow

Cumulative Number of SmartPay Enrollments and Transactions

Num

ber o

f Tra

nsac

tions

(000

’s) N

umber of Enrollm

ents (000’s)

SmartPay Platform Drives Volume and Value

SmartPay Debit CashCredit

The number of customers who are aware of CFI’s SmartPay loyalty program is higher in new stores

But first, why SmartPay?

$116

$25

$51

$-

$20

$40

$60

$80

$100

$120

$140

Payroll Benefits Credit Card Fees

2013 Expenses in $ MM

Card Processing Fees growing at an unsustainable rate – prior to launch, CAGR was ~17%, and the second largest category of expense overall

Through SmartPay, we believed we could:

Solve what was/is known to be a major pain point for consumers (gasoline prices)

Remove friction from the transaction/create a novel way to transact with Cumberland Farms

Insulate Cumberland Farms from rising cost of processing

CF Total CF New Store All Others 7-Eleven Hess Mobil Stewarts Speed-way

2018 2017 2018 2017 2018 2017 2018 2017 2018 2017 2018 2017 2018 2017 2018 2017

Base: Total respondents (unweighted) 2004 2001 821 806 1981 1973 227 249 150 160 204 163 86 53 147 148Base: Total respondents (weighted) 2004 2001 915 924 1978 1972 258 248 147 147 222 175 73 39 141 159

Is easy to get to 61% 57% 77% 70% 46% 44% 50% 44% 37% 41% 51% 54% 58% 72% 49% 46%

My family has always shopped there 32% 30% 43% 42% 18% 18% 25% 17% 9% 23% 21% 18% 31% 45% 18% 22%

Is a newer store 52% 51% 82% 81% 24% 23% 21% 18% 12% 28% 30% 26% 37% 42% 31% 36%

Has a loyalty program that allows me to save money on gas or merchandise 39% 38% 53% 54% 22% 23% 14% 20% 22% 35% 29% 27% 26% 30% 35% 34%

Is a store I trust 58% 52% 71% 67% 39% 37% 37% 30% 35% 39% 48% 47% 65% 73% 45% 40%

Is a place I would go out of my way to shop at 26% 25% 35% 37% 14% 16% 13% 12% 10% 27% 16% 16% 27% 30% 13% 16%

Has a good reputation 61% 59% 73% 72% 40% 41% 41% 37% 33% 44% 41% 48% 60% 69% 38% 43%

Has foods or snacks that I crave 52% 50% 62% 61% 38% 40% 41% 41% 34% 48% 43% 44% 51% 53% 41% 39%

The area where I make my coffee or get my fountain beverage is always clean 50% 62% 31% 29% 27% 41% 43% 37%

The employees know me 20% 21% 26% 28% 14% 13% 11% 13% 8% 10% 23% 13% 24% 25% 17% 14%

Restrooms are always clean 36% 36% 47% 49% 24% 25% 22% 16% 17% 23% 30% 29% 35% 49% 28% 26%

Is fast to get my hot food 38% 49% 24% 18% 17% 25% 39% 26%

Their food is fresh 41% 41% 51% 51% 25% 26% 25% 24% 21% 30% 28% 29% 40% 56% 24% 30%

New CF Stores –vs.– CompetitionTop Tier – the things that are most

important*

Relative weakness for CF (index <=80) Relative strength for CF (index >= 120)

Index calculated by dividing Total CF score by competitive score and multiplying by 100

Competitive Comparison of Attribute Scores

Q13. Please rate how well each of the following statements describes the following convenience stores using a six point scale.

*Derived importance from Key Drivers Analysis

SmartPay Consumer Rating Metrics

SmartPay Consumer Rating Metrics

SmartPay Consumer Rating Metrics

SmartPay Financial Metrics

1.31%

1.25%

1.26%

1.30%

1.27%

1.21%

1.14%

1.16%

1.18%

1.20%

1.22%

1.24%

1.26%

1.28%

1.30%

1.32%

FY13 FY14 FY15 FY16 FY17 FY18

Adjusted CC Fees % of Total Revenue

SmartPay Financial Metrics

-0.1

-0.05

0

0.05

0.1

0.15

0.2

Historical DTC & DTLC

DTC DTLC Linear (DTC) Linear (DTLC)

SmartPay Roadmap

Mobile Strategy & EnhancementsGiven our strong performance to date with SmartPay, leveraging the current platform as the foundation for future innovations is critical to our mobile strategy

A 12-month roadmap was designed to enhance the mobile offering and meet changing customer needs

Consumer Needs &

Expectations

Cumberland Farms

Strategy

Technology / Digital Trends

SmartPay Roadmap

Mobile CheckoutWith increasing consumer interest in mobile scan & pay, functionality was added to our existing platform to deliver an accelerated experience for the coffee drinker

• Customer is able to select their desired item, add to their mobile cart, purchase, and leave the store without interacting with an associate or waiting in a queue

• During the first three weeks of the soft launch, the usage increased by 2.8x amongst the 68% of users who shopped the brand for 3+ years

• 83% of participants reported an “excellent experience” with the functionality, citing speed as the main driver of rating

SmartPay Roadmap

Additional Planned EnhancementsEnhancements for May 2019 launch are designed to accomplish three critical goals, positioning the mobile platform as a key strategic benefit and differentiator for the brand

Lower the Barrier to Entry

• Additional Payment Options: Expanding beyond ACH with credit, debit, Venmo, PayPal

• Integration with mobile banking to expedite the enrollment process for ACH accounts

Drive Transactions

• Exclusive pricing and offers

• Mobile checkout to drive peak daypart coffee purchases

• Sub-accounts: allow user to set up an account for another individual from the same funding source (children, spouse, etc.)

Enhance Speed

• Integrated barcode: applies selected coupons and payment method into a single register-scan

• Mobile checkout to drive peak daypart coffee purchases without register interaction

Future Considerations & Functionality: mobile order ahead, delivery, curbside / at pump pick up

Growth Strategy

Multi-Pronged Growth Strategy

Growth Strategy

Shifting merchandise mix towards higher-margin, differentiated items (e.g., private label and foodservice items such as coffee, frozen and fountain drinks, pizza, fresh sandwiches and bakery)

Focusing intensively upon brand development, consumer research and understanding and product innovation

Investing in technologies to drive efficiency and allow for more rapid, profitable and accurate decision making (i.e. fuel pricing software to optimize gross profit / volume dynamic and a supply chain management system)

Investing in technologies to drive customer loyalty and drive down credit card processing fees (i.e. SmartPay)

Utilizing AIM Concept stores to grow sales (APSW) and increase store productivity

Aggressively managing general & administrative expenses to enhance productivity and streamline business model

Investing in Team Members – recruiting, compensation / benefits, talent development and engagement

Enhance Sales and Profitability of Existing Stores

Remodeling Existing Locations & Building

New Locations in AIM Format

Manage Expenses & Improve Cost

Structure

5

42

58

30

1410 9

2

7

4

5

8

19

119

1912

2

5

68 7

1

3

15

20

1320 11

7

46

66

43

53

47

3941

37

2%

10%

21%

30%

41% 48%

55%

62%

69%

0

10

20

30

40

50

60

70

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

Cumberland Farms began investing in AIM stores in 2009 and has rapidly increased the AIM site count since then to 384 AIM stores

Multi-year initiative features an expanded focus on foodservice and an enhanced in-store experience through re-imaging and improved brand management

AIM stores are outperforming their legacy counterparts in all of the major merchandise categories and have also seen improved loyalty among customers

The investment in AIM stores has been financed with internal cash flow from operations, the proceeds from the sale of stores in non-strategic locations and minimal debt

Overview of AIM Concept

AIM Capital Project Count by YearAIM Conversion

New Stores Offset Raze & Rebuild AIM Conversion AIM % of TotalStore Count

(# of Stores)

Example of AIM Store TransformationBefore After

APSW Merchandise $21K APSW Gallons 13K

APSW Merchandise $48K APSW Gallons 42K

Overview of AIM Concept

Examples of AIM Store Transformation

AfterBefore

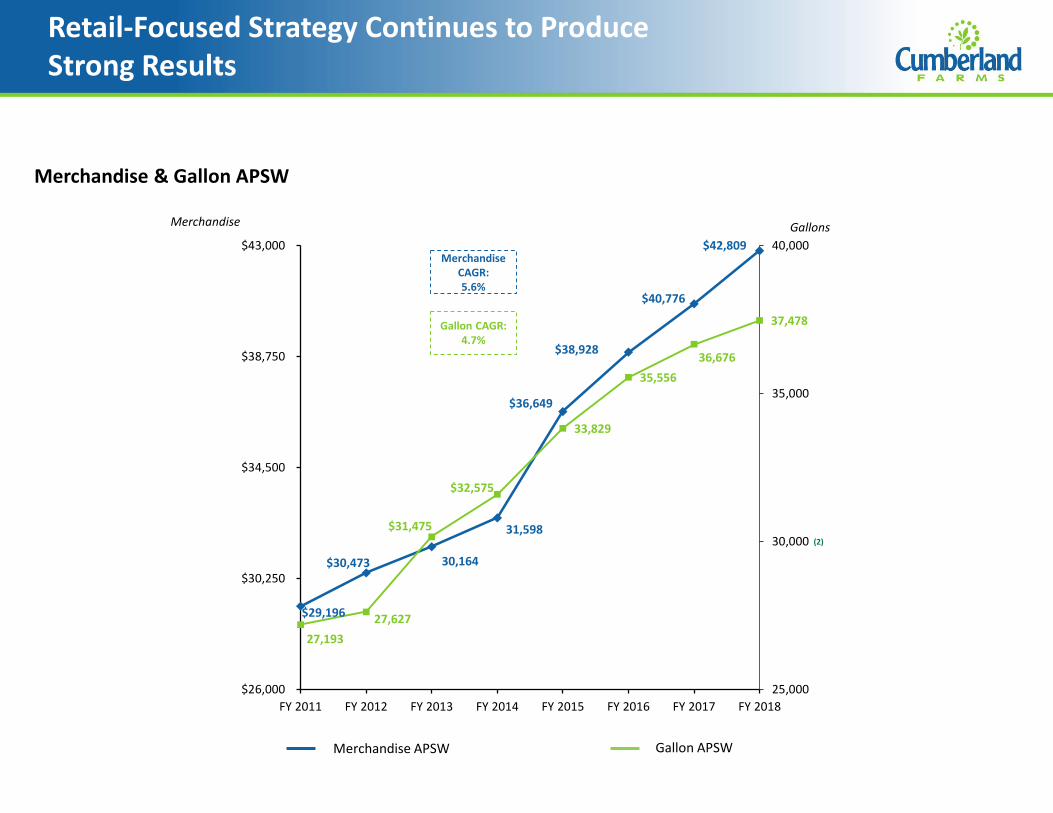

$29,196

$30,473

$31,475

$32,575

$36,649

$38,928

$40,776

$42,809

27,193 27,627

30,164

31,598

33,829

35,556 36,676

37,478

25,000

30,000

35,000

40,000

$26,000

$30,250

$34,500

$38,750

$43,000

FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

Merchandise APSW

Merchandise & Gallon APSW

Gallon APSW

GallonsMerchandise

Merchandise CAGR:5.6%

Gallon CAGR:4.7%

(2)

Retail-Focused Strategy Continues to Produce Strong Results

Operations Strategy

Overview of Operations Strategy

![[Translation for Reference and Convenience Purposes … · [Translation for Reference and Convenience Purposes Only] ITOCHU Corporation CORPORATE GOVERNANCE - 2 - President of the](https://static.documents.pub/doc/80x56/5b5e71387f8b9a8b4a8c5006/translation-for-reference-and-convenience-purposes-translation-for-reference.jpg)