39

Glomac Berhad 110532-M Menara Glomac, Glomac Damansara, Jalan Damansara, 60000 Kuala Lumpur, Malaysia. T +603.7723 9000 F +603.7729 9000 W www.glomac.com.my CORPORATE PRESENTATION June 2014

Glomac Berhad 110532-M Menara Glomac, Glomac Damansara, Jalan Damansara, 60000 Kuala Lumpur, Malaysia.

T +603.7723 9000 F +603.7729 9000 W www.glomac.com.my

CORPORATE PRESENTATION

June 2014

2

CONTENT

Executive Summary

Review of 9M FYE Apr 2014 Financial Results

Sales & Progress Billings

Update on Projects

Summary & Conclusion

3

Overview

Founded by Tan Sri Dato’ FD Mansor and Datuk Richard

Fong in 1988

• Listed on the Main Board of Bursa Malaysia in June 2000

Helmed by Datuk Seri FD Iskandar as Group Managing

Director / Chief Executive Officer

Over 2 decades of solid record in developing innovative

residential & commercial properties

Properties worth over RM4bn handed over to-date

• Klang Valley / Greater Kuala Lumpur focus

4

Financial Snapshot

0

20

40

60

80

100

120

Profit Attributable to Owners' of the Company RMmil

0

200

400

600

800

Revenue RMmil

FY ‘10 FY ‘09 FY ‘11 FY ‘12 FY ‘13 FY ‘14

(9-mth)

FY ‘09 FY ‘10 FY ‘11 FY ‘12 FY ‘13 FY ‘14

(9-mth)

345 317

597 652 681

502

32 41

63

85

102

86

5

Financial Snapshot

0

200

400

600

800

1,000

Unbilled Sales RMmil

0

2

4

6

8

Net Dividend Per Share (Sen)

FY ‘09 FY ‘12 FY ‘11 FY ‘10 FY ‘13 FY ‘14

(9-mth)

4.4 4.5

6.4 6.8

5.9

FY ‘09 FY ‘10 FY ‘11 FY ‘12 FY ‘13 FY ‘14

(9-mth)

364

588 550

731

888 792

Glomac Berhad 110532-M Menara Glomac, Glomac Damansara, Jalan Damansara, 60000 Kuala Lumpur, Malaysia.

T +603.7723 9000 F +603.7729 9000 W www.glomac.com.my

RESULTS REVIEW

9M FYE Apr 2014

7

9M FY14 Financial Results

1 attributable to equity holders of the company

^ Based on weighted average share base of 723.1m for 9M FY14 and 683.0m for 9M FY13

FYE Apr

(RM mil)

9M

FY14

9M

FY13 % chg

3Q

FY14

3Q

FY13 % chg

Revenue 501.8 445.3 +12.7 183.7 159.9 +14.9

Gross profit 144.0 134.0 +7.5 51.3 48.1 +6.7

Pre-tax profit 118.9 104.5 +13.8 35.5 37.0 -4.1

Net profit 1 86.0 70.3 +22.3 22.7 25.4 -10.6

Net EPS (sen)^ 11.9 10.3 +15.5 3.1 3.5 -11.4

Gross margin 28.7% 30.0% - 27.9% 30.1% -

Pre-tax margin 23.7% 23.5% - 19.3% 23.1% -

8

Financial Highlights

9M FY14 revenue +12.7% to RM501.8m sustained by

• Lakeside Residences and Saujana Rawang

• Tail-end of Glomac Damansara and Glomac Cyberjaya 2

• New projects Glomac Centro and Reflection Residences

are beginning to contribute

PBT rose 13.8% to RM118.9mil

• Construction progress at ongoing projects

• RM15m gain from sale of Australian investment at

associate level registered in 2Q FY14

9M FY14 PAT up 22.3% to RM86.0mil

• Net EPS of 11.9sen; Annualised net EPS of 15.9sen

• Corresponding P/E of 6.8x at RM1.08 share price

9

Financial Highlights

PBT margin maintained at 23.7% at 9M FY14 stage

• 3Q FY14 margin impacted by higher construction materials

and labour cost, and new land conversion premium rates in

Saujana Rawang

Net gearing is at a comfortable 24%

• Ample capacity to acquire additional landbank

• Recently bought 62.6 acres in Bandar Saujana Utama for

RM23mil (RM8.44 per sq ft) cash

Net assets per share of RM1.21

• RM1.08 share price represents 11% discount

Proposed interim dividend of 2.25 sen per share (single tier)

• Matching the 3 sen less tax at 25% previously

Glomac Berhad 110532-M Menara Glomac, Glomac Damansara, Jalan Damansara, 60000 Kuala Lumpur, Malaysia.

T +603.7723 9000 F +603.7729 9000 W www.glomac.com.my

SALES &

PROGRESS BILLINGS

11

9M FY14 New Sales At RM368mil

Sales Summary (RM mil) 3Q FY14 9M FY14 9M FY13

Lakeside Residences 9 18 63

Glomac Centro 12 88 62

Reflection Residences @

Mutiara Damansara 19 28 89

Bandar Saujana Utama 10 66 108

Saujana Rawang 33 117 127

Glomac Damansara

Residences 3 8 23

Glomac Cyberjaya 2 0 3 31

Others 19 40 16

105 368 519

Modest performance; impacted by recent measures

• RPGT re-introduced, withdrawal of DIBs, net income

calculation for mortgage, etc

12

Strategic Decision To Defer

Selected Launches

Fine-tuning pricing strategy and costing for some projects

• Including assessing GST impact

Anticipate improved visibility and outlook for property

demand once market adjusts to tightening measures

• Expect consolidation to last another 6 to 12 months

Revised launch dates

• Phases 6 & 7 of Lakeside Residences and Saujana KLIA

township in FY15

• Centro V in CY15/16

FY14 sales guidance revised to RM500mil

13

Unbilled Sales At RM792m

*Unbilled sales is net of minority interest in projects with < 100% equity interest

Summary Of Projects 31 Jan 2014 (RM mil)

Launched GDV

(RM mil)

Overall Take-Up Rate (%)

Unbilled Sales*

Lakeside Residences 264 97 125

Glomac Damansara 527 96 72

Glomac Cyberjaya 2 133 60 17

Glomac Centro 381 74 236

Reflection Residences @

Mutiara Damansara * 286 94 113

Bandar Saujana Utama 1,550 100 41

Saujana Rawang 604 92 148

Sri Saujana, Johor 491 96 40

Total 4,236 792

Glomac Berhad 110532-M Menara Glomac, Glomac Damansara, Jalan Damansara, 60000 Kuala Lumpur, Malaysia.

T +603.7723 9000 F +603.7729 9000 W www.glomac.com.my

PROJECTS UPDATE

15

Strong Greater

KL Presence

16

Projects Enjoy Excellent

Connectivity

17

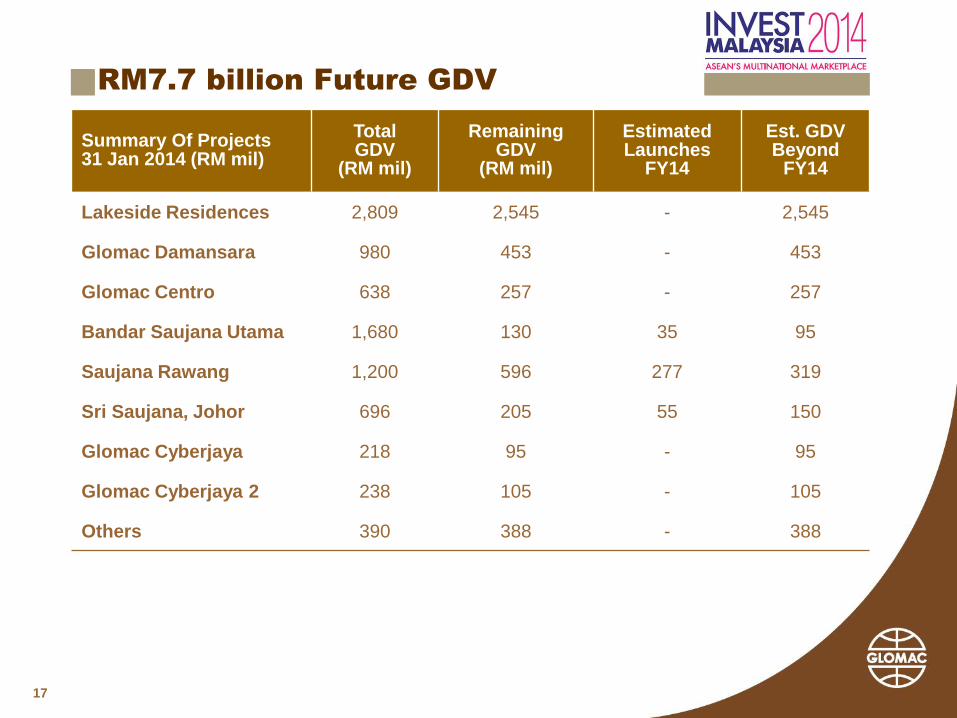

RM7.7 billion Future GDV

Summary Of Projects 31 Jan 2014 (RM mil)

Total GDV

(RM mil)

Remaining GDV

(RM mil)

Estimated Launches

FY14

Est. GDV Beyond

FY14

Lakeside Residences 2,809 2,545 - 2,545

Glomac Damansara 980 453 - 453

Glomac Centro 638 257 - 257

Bandar Saujana Utama 1,680 130 35 95

Saujana Rawang 1,200 596 277 319

Sri Saujana, Johor 696 205 55 150

Glomac Cyberjaya 218 95 - 95

Glomac Cyberjaya 2 238 105 - 105

Others 390 388 - 388

18

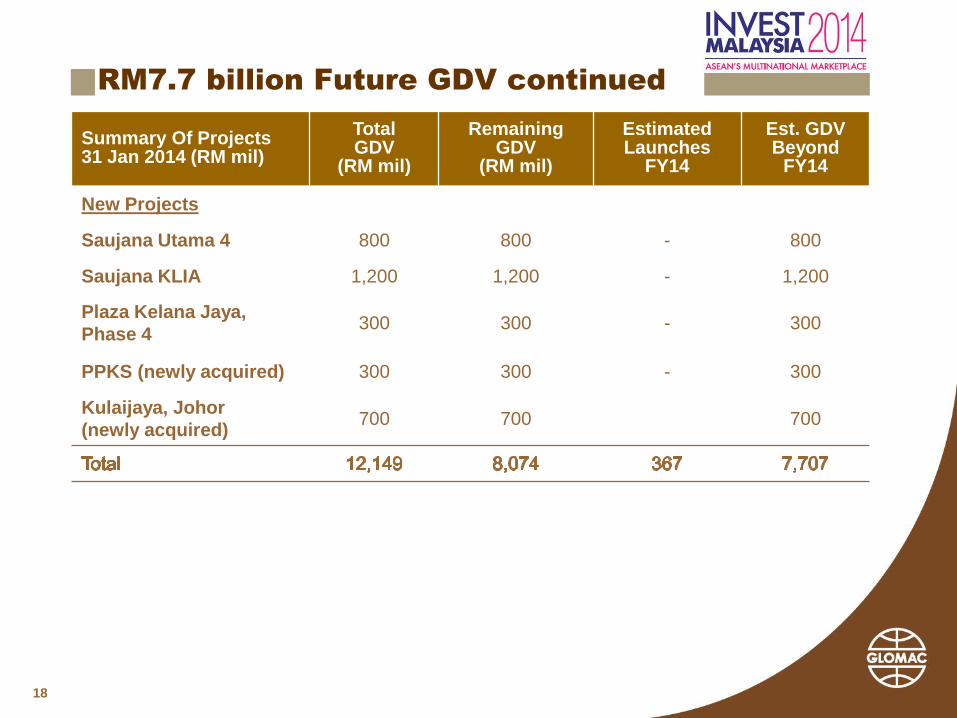

RM7.7 billion Future GDV continued

Summary Of Projects 31 Jan 2014 (RM mil)

Total GDV

(RM mil)

Remaining GDV

(RM mil)

Estimated Launches

FY14

Est. GDV Beyond

FY14

New Projects

Saujana Utama 4 800 800 - 800

Saujana KLIA 1,200 1,200 - 1,200

Plaza Kelana Jaya,

Phase 4 300 300 - 300

PPKS (newly acquired) 300 300 - 300

Kulaijaya, Johor

(newly acquired) 700 700 700

19

20

Overall Development Clubhouse

Phase 3, Symphony - Facade Symphony – Living room

21

Flagship project with sizeable GDV of at least RM2.5bn

• 200 acres leasehold land acquired for RM77m

Prime location in close proximity to Puchong’s thriving

commercial hub

Serviced by

KESAS and LDP

2 new LRT stations (Ampang extension line) targeted for

completion in 2014

22

RM229m worth of properties successfully launched in FY13

(Phases 2 to 4)

• Take-up at 97% with remaining unsold comprising a handful

of Bumi units

Targeted launch of 153 units of 2-storey link houses under

Phases 6 & 7 with GDV of RM120m in FY15

• Fine-tuning pricing and costing

• Ongoing improvements to surrounding infrastructure to

improve pricing power and saleability in future

23

24 Main Lobby

Facade

25-storey Office Tower

Glomac Damansara

25

356 units in two 26-storey tower blocks with estimated GDV of

RM285m

Overall take-up has improved further to 96%

• Delivery of vacant possession in April

Final phase of Glomac Damansara comprising boutique retail

mall with GDV of RM375m

• Earmarked for en-bloc sale on tenanted basis to capture better

value

• Actively engaging with potential tenants in anticipation of

completion in CY15

26

27

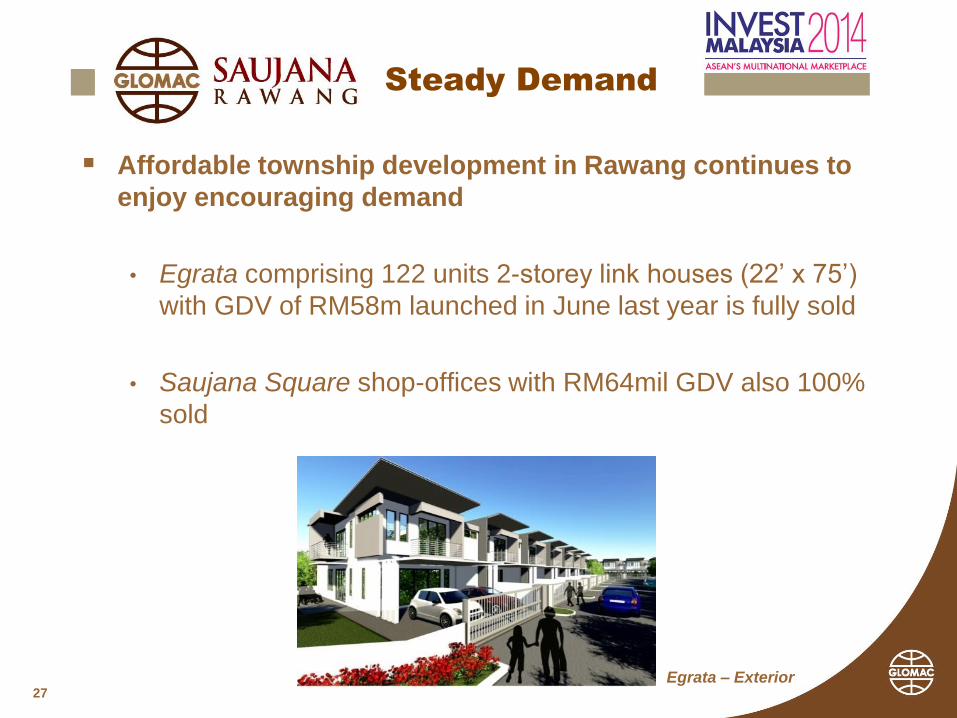

Steady Demand

Affordable township development in Rawang continues to

enjoy encouraging demand

• Egrata comprising 122 units 2-storey link houses (22’ x 75’)

with GDV of RM58m launched in June last year is fully sold

• Saujana Square shop-offices with RM64mil GDV also 100%

sold

Egrata – Exterior

28

New Phases

• Alcedo in November 2013

• 50 units of Semi-Ds with GDV of RM51m

• Ardea – 50 units of 2-storey link houses

under Phase 1 with GDV of RM26m

• 2nd Phase to comprise another 68 units

Aquila Phase slated for 1Q FY15

• 124 units of 2-storey link houses with

preliminary GDV estimate of RM63m

Alcedo – 2.5 storey Semi-D

Alcedo – 2 storey Semi-D

29

Prime PJ Location

30

Healthy Take-Up

For Phase 1

Take-up of Phase 1 with estimated GDV of RM381m at 75%

Centro V

Centro V (Phase 2) now

scheduled for FY15 launch

• 394 units serviced apartments

valued at RM214m

• Layout will focus on smaller

units with sizes ranging from

600 to 1,100 sq ft

• 18 units 2-storey shop office with

GDV of RM43m

31

32

299 units freehold serviced apartments

in a 39-storey block with estimated

GDV of RM286m

Take-up is at a solid 94%

Meaningful bottomline contribution

expected from FY15 onwards

• Building works are now in full swing

33

New Acquisition in

Kulaijaya, Johor Bahru

Project Location

Approx. 6km from

Lagenda Putra

34

New Acquisition in

Kulai Jaya, Johor Bahru

New acquisition by Glomac in Kulaijaya, Johor Bahru. Land size of about

174 acres with an indicative GDV of RM700mil.

Exciting new township which is within the Iskandar Region, development

will focus on the affordable segment.

This acquisition spreads Glomac’s presence in Johor Bahru on top of the

current Sri Saujana, Kota Tinggi project that has an indicative GDV of

RM700mil.

35

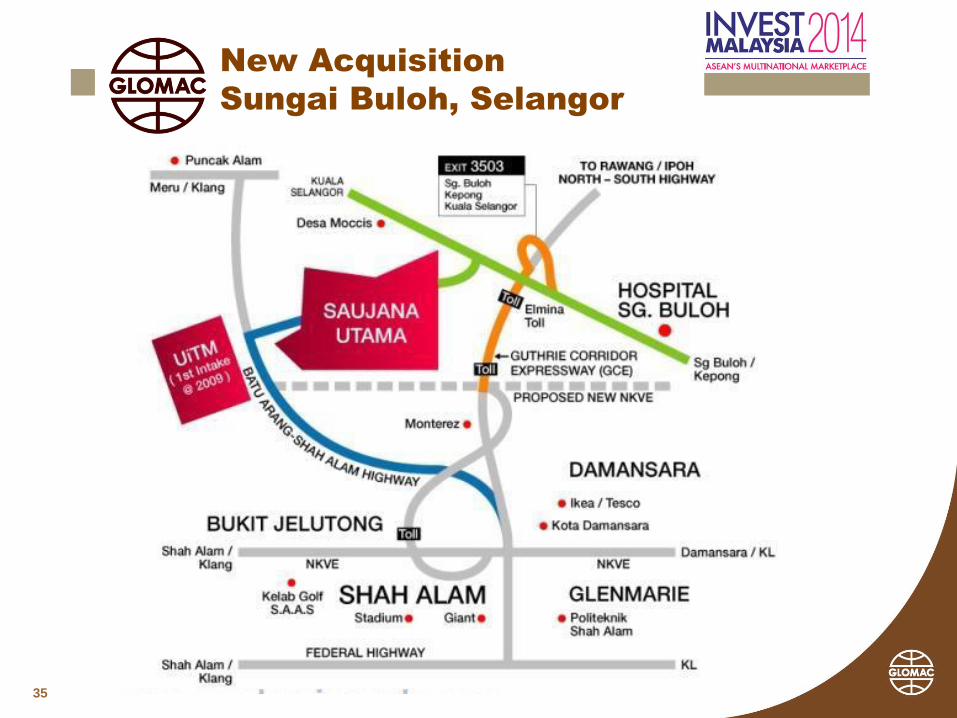

New Acquisition

Sungai Buloh, Selangor

36

New Acquisition in the

District of Kuala Selangor

Glomac bought 6 pieces of land for RM23mil in Sungai Buloh which totals

to about 62.6 acres with an indicative Gross Development Value of

RM300mil

The new acquisition is within Glomac’s thriving Bandar Saujana Utama

(BSU) township

The acquisition is Glomac’ overall strategy to extend the BSU township

which has matured over 15 years, and is now well established with a

hypermarket, shopping mall, shop offices and has more than 65,000

residents.

Glomac Berhad 110532-M Menara Glomac, Glomac Damansara, Jalan Damansara, 60000 Kuala Lumpur, Malaysia.

T +603.7723 9000 F +603.7729 9000 W www.glomac.com.my

SUMMARY & CONCLUSION

38

Continued Focus On

Landed Products In FY15

Earnings prospects for next 12 months anchored by high unbilled

sales of RM792m

• Confident of delivering improved net earnings in FY14

More modest FY14 sales target of RM0.5bn

• Short-term market consolidation due to cooling measures

• Strategic decision to push launches (Lakeside Residences, Saujana

KLIA, Centro V) into FY15

Key launches to resume in FY15 and we are continuously adding to

future GDV

• Recent acquisition of 62.6 acres in Bandar Saujana Utama will add

indicatively another RM300m to future GDV

• Another new acquisition in Kulaijaya, Johor. 174 acres with an

indicative GDV of RM700m

Target to match FY13’s net dividend of 4.9 sen/share

• Proposed interim dividend of 2.25 sen/share (single-tier)

Glomac Berhad 110532-M Menara Glomac, Glomac Damansara, Jalan Damansara, 60000 Kuala Lumpur, Malaysia.

T +603.7723 9000 F +603.7729 9000 W www.glomac.com.my

THANK YOU

Q & A Session

IMPORTANT DISCLAIMER

The information in this report has been prepared for general circulation based on internal sources available at

the time of issue of this report and opinions are subject to change without notice. This report may contain

forward looking statement and forecasts, which are based on the assumptions that are subject to

uncertainties. This report is prepared solely for information purposes only and not to be construed as a

solicitations for contracts. The Company accepts no liability whatsoever for any direct or consequential loss

arising from the use of this document.