38

CaixaBank Fixed Income Presentation November 2013

CaixaBank Fixed Income Presentation November 2013

Disclaimer

The purpose of this presentation is purely informative and the information contained herein is subject to, and must be read in conjunction with, all other publicly available information. In particular, regarding the data provided by third parties, neither CaixaBank, S.A. (“CaixaBank”), nor any of its administrators, directors or employees, is obliged, either explicitly or implicitly, to vouch that these contents are exact, accurate, comprehensive or complete, nor to keep them updated, nor to correct them in the case that any deficiency, error or omission were to be detected. Moreover, in reproducing these contents in any medium, CaixaBank may introduce any changes it deems suitable, may omit partially or completely any of the elements of this document, and in case of any deviation between such a version and this one, assumes no liability for any discrepancy. This document has at no time been submitted to the Comisión Nacional del Mercado de Valores (CNMV – the Spanish Stock Markets regulatory body) for approval or scrutiny. In all cases its contents are regulated by the Spanish law applicable at time of writing, and it is not addressed to any person or legal entity located in any other jurisdiction. For this reason it may not necessarily comply with the prevailing norms or legal requisites as required in other jurisdictions. CaixaBank cautions that this presentation might contain forward-looking statements. While these statements represent our judgment and future expectations concerning the development of our business, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from our expectations. Statements as to historical performance, historical share price or financial accretion are not intended to mean that future performance, future share price or future earnings for any period will necessarily match or exceed those of any prior year. Nothing in this presentation should be construed as a profit forecast. This presentation on no account should be construed as a service of financial analysis or advice, nor does it aim to offer any kind of financial product or service. In particular, it is expressly remarked here that no information herein contained should be taken as a guarantee of future performance or results. In making this presentation available, CaixaBank gives no advice and makes no recommendation to buy, sell or otherwise deal in CaixaBank shares, or any other securities or investment whatsoever. Any person at any time acquiring securities must do so only on the basis of such person’s own judgment as to the merits or the suitability of the securities for its purpose and only on such information as is contained in such public information having taken all such professional or other advice as it considers necessary or appropriate in the circumstances and not in reliance on the information contained in this presentation. Without prejudice to legal requirements, or to any limitations imposed by CaixaBank that may be applicable, permission is hereby expressly refused for any type of use or exploitation of the contents of this presentation, and for any use of the signs, trademarks and logotypes which it contains. This prohibition extends to any kind of reproduction, distribution, transmission to third parties, public communication or conversion into any other medium, for commercial purposes, without the previous express permission of CaixaBank and/or other respective proprietary title holders. Any failure to observe this restriction may constitute a legal offence which may be sanctioned by the prevailing laws in such cases. In so far as it relates to results from investments, this financial information from the CaixaBank Group for 9M 2013 has been prepared mainly on the basis of estimates.

2

Highlights

Largest customer base in Spain with circa 20% market share in key retail products

Recent acquisitions (BCIV and BdV) strengthen regional footprint and market share leadership, generating significant cost savings

Caixabank is the sole purely domestic Spanish bank with an investment grade rating by all 3 agencies

NII +1% qoq due to improved funding costs: price of new time deposits falls to 137 bps

Sound capital position: Core Capital BIS 2.5 of 12.5%

Early delivery of BIS 3 targets: Core Capital FL already at 8.3% (pre-DTA reform)

CaixaBank stands out for the quality of its capital and for its low leverage

Leading retail franchise in Spain

Q3 results: NII turns ahead of expectations

Robust capital position

3

The stock of NPLs was reduced by €173 million in Q3

80% of NPLs backed by real collateral, 23% not past due

Coverage ratio still high at 65% even after reclassifying refinanced loans in Q2

€16.6 billion in credit provisions, €4.4 of which are generic provisions

€1.5 billion of real estate assets sold or rented year-to-date

Asset Quality stabilization

Delivering on synergies and rightsizing actions

Restructuring process continues as planned: 212 branches closed and 1,070 net departures in Q13

Synergy targets confirmed: €265 M of the €243 M expected for 2013 already booked

Share of client income flows grows on the back of strong distribution network

Capture of key income flows from customers reinforces loyalty and facilitates cross-selling

386,300 payrolls captured from January to September 2013 (+135% vs 2012)

Significant market share gain (+126 bps YTD)

4

Commercial activity

2013: latest available figures Peers: Santander, BBVA, Bankia, Sabadell and Popular Source: Social Security and FRS Inmark

14.4 14.8 15.1 15.7 15.9

20.0 21.3

12.0 12.9

6.0

11.2

1.1

6.3

8.6

8.9

2.6

2.7

2007 2008 2009 2010 2011 2012 2013

Peer 1

Peer 2

Peer 4

Undisputed leadership in payrolls Payrolls market share, %

Peer 3

Peer 5

Control of client incomes enhances share of wallet and increases cross-selling opportunities

5

2013: Latest data available Peers: Santander, BBVA, Bankia, Sabadell and Popular Source: Bank of Spain, INVERCO, ICEA and FRS Inmark

High market shares in key retail products

Market share, %

Retail strength results in the highest customer penetration among peers

Customer penetration, %

20.4 21.0 21.6 21.0 21.0

26.1 27.4

16.0 15.5

9.8

14.1

1.8

8.6

11.0 13.5

4.0 4.7

2007 2008 2009 2010 2011 2012 2013

Peer 2

Peer 1

Peer 4

(1) Loans + deposits (2) Other Resident Sectors according to Bank of Spain (3) Includes PPIs + PPAs

Peer 3

Peer 5

“Non-traditional” products also show high market share growth

2007 market share growth

17.8%

17.6%

14.1%

11.2%

5.6%

9.1%

9.8%

11.5%

9.4% Business volume(1)

Demand deposits

Deposits(2)

Loans(2)

Mutual funds

Pension plans(3)

Saving insurance

POS terminal turnover

14.7%

15.3%

14.2%

15.2%

14.2%

17.9%

19.8%

23.6%

+5.3%

+3.8%

+4.4%

+6.1%

+8.6%

+6.7%

+5.7%

+5.8%

Credit cards turnover +2.8% 20.4%

Commercial activity

Continued reduction of the funding gap as macro deleveraging trend persists

Business volume: Loan book and customer funds In Billion Euros

(1) Deducting BdV figures as of 31/12/12 – includes changes under CABK management (2) Retail funds defined as: deposits, CP, retail debt securities (including sub. debt), mutual funds, pension plans and other retail off-balance sheet products. (3) Excluding the impact of the conversion of certain bank financing into bonds

Loan-book deleveraging continues as expected

Positive evolution of retail funds reflects commercial strength

Funding gap maintains a strong reduction: LTD ratio now at 118% (-10 pp YTD)

Pricing discipline in deposits leads to migration to long-term fee-generating products

Slight increase in retail funds and continued deleveraging lead to a significant reduction in LTD ratio to 118%

Dec-12 Sep-13

514.0 514.6

6

YTD

-2.1% -7.6%

+3.8% +0.7%

Total Organic1

Retail funds2

Loans3

Business volume

+0.1% YTD

+4.5%

-4.4%

Inorganic

Organic1

Commercial activity

(1.9%)

4.1%

(0.8%)

(1.7%)

0.7%

(8.7%)

(1) Deducting BdV data at 31/12/12- includes changes under CABK management (2) Balances are reduced as CP converts into deposits and BCIV MCB converts into shares (3) Primarily includes regional govt. securities, and Caja de Ahorros y Pensiones de Barcelona sub debt. Balance is reduced due to the maturity of Repsol preferred shares

Volumes of retail funds stable despite strict pricing policy on deposits

7

Successful management of retail fund volumes despite strict pricing: +0.7% qoq

Fall in demand deposits impacted by Q2 seasonality

Insurance, pension plans and mutual funds continue to benefit from client migration

Wholesale funding being gradually reduced

Total customer funds breakdown In Billion Euros

I. Customer funds on balance sheet

Demand deposits

Time deposits

Debt securities2

Subordinated liabilities2

Institutional issuance

Insurance

Other funds

II. Off-balance sheet funds

Mutual funds

Pension plans

Other managed resources3

Total customer funds

Retail funds

Wholesale funds

243.8

74.0

82.5

3.0

3.6

47.6

30.0

3.1

55.6

26.5

16.3

12.8

299.3

251.7

47.6

2.4%

6.9%

7.8%

(66.3%)

(17.0%)

(1.6%)

7.5%

8.6%

5.1%

15.9%

3.8%

(10.7%)

2.9%

3.8%

(1.6%)

YTD 30th Sep. Organic1 YTD (%)

+3.7%

-0.8%

Inorganic

Organic1 Total customer funds

+€8.4bn (+2.9%)

Commercial activity

Significant deleveraging continues as clients reduce debt levels

(1) Deducting BdV data at 31/12/12- includes changes under CABK management (2) Excluding the impact of the conversion of bank financing into bonds

Reduction of the loan book continues as country deleverages:

Real Estate developer loan book continues its strong decline

Business loans impacted by low credit demand for capex:

o Large corporates continue to benefit from wholesale funding markets

o Improved macro environment should lead to credit demand normalization

8

Loan-book breakdown In Billion Euros, gross

I. Loan to individuals

Residential mortgages – home purchases

Other

II. Loan to businesses

Non -RE businesses

Real Estate developers

RE subsidiaries

Loans to individuals & businesses

III. Public sector

Total loans

119.9

88.8

31.1

84.9

59.6

23.7

1.6

204.9

10.4

215.3

0.6%

1.3%

(1.3%)

(6.3%)

(3.8%)

(12.3%)

(2.0%)

(2.4%)

(20.6%)

(3.5%)

YTD 30th Sep.

(4.6%)

(13.1%)

(9.2%)

(23.2%)

Organic1 YTD (%)

+5.5%

-7.6%

Inorganic

Organic1 Loan book2

(-2.1%)

NOTE: Excluding the impact of the conversion of certain bank financing into bonds

(2.1%) (7.6%)

Commercial activity

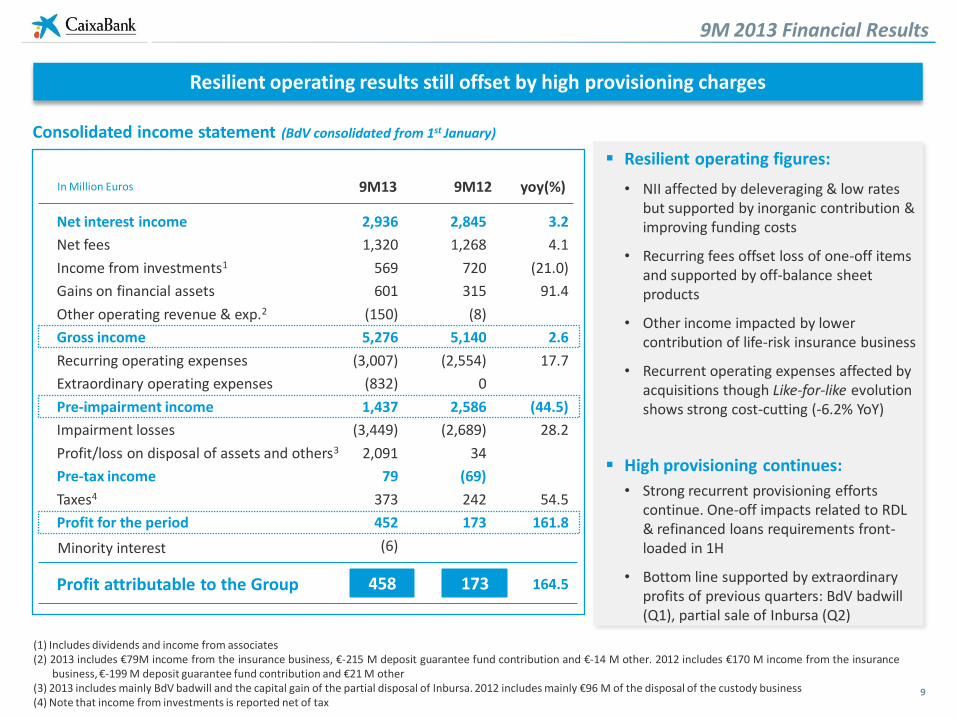

9M 2013 Financial Results

Consolidated income statement (BdV consolidated from 1st January)

9

Resilient operating results still offset by high provisioning charges

(1) Includes dividends and income from associates (2) 2013 includes €79M income from the insurance business, €-215 M deposit guarantee fund contribution and €-14 M other. 2012 includes €170 M income from the insurance

business, €-199 M deposit guarantee fund contribution and €21 M other (3) 2013 includes mainly BdV badwill and the capital gain of the partial disposal of Inbursa. 2012 includes mainly €96 M of the disposal of the custody business (4) Note that income from investments is reported net of tax

9M12

Net interest income

Net fees

Income from investments1

Gains on financial assets

Other operating revenue & exp.2

Gross income

Recurring operating expenses

Extraordinary operating expenses

Pre-impairment income

Impairment losses

Profit/loss on disposal of assets and others3

Pre-tax income

Taxes4

Profit for the period

Profit attributable to the Group

2,845

1,268

720

315

(8)

5,140

(2,554)

0

2,586

(2,689)

34

(69)

242

173

yoy(%)

3.2

4.1

(21.0)

91.4

2.6

17.7

(44.5)

28.2

54.5

161.8

164.5

9M13

2,936

1,320

569

601

(150)

5,276

(3,007)

(832)

1,437

(3,449)

2,091

79

373

452

(6)

458 173

In Million Euros

Minority interest

Resilient operating figures:

• NII affected by deleveraging & low rates but supported by inorganic contribution & improving funding costs

• Recurring fees offset loss of one-off items and supported by off-balance sheet products

• Other income impacted by lower contribution of life-risk insurance business

• Recurrent operating expenses affected by acquisitions though Like-for-like evolution shows strong cost-cutting (-6.2% YoY)

High provisioning continues:

• Strong recurrent provisioning efforts continue. One-off impacts related to RDL & refinanced loans requirements front-loaded in 1H

• Bottom line supported by extraordinary profits of previous quarters: BdV badwill (Q1), partial sale of Inbursa (Q2)

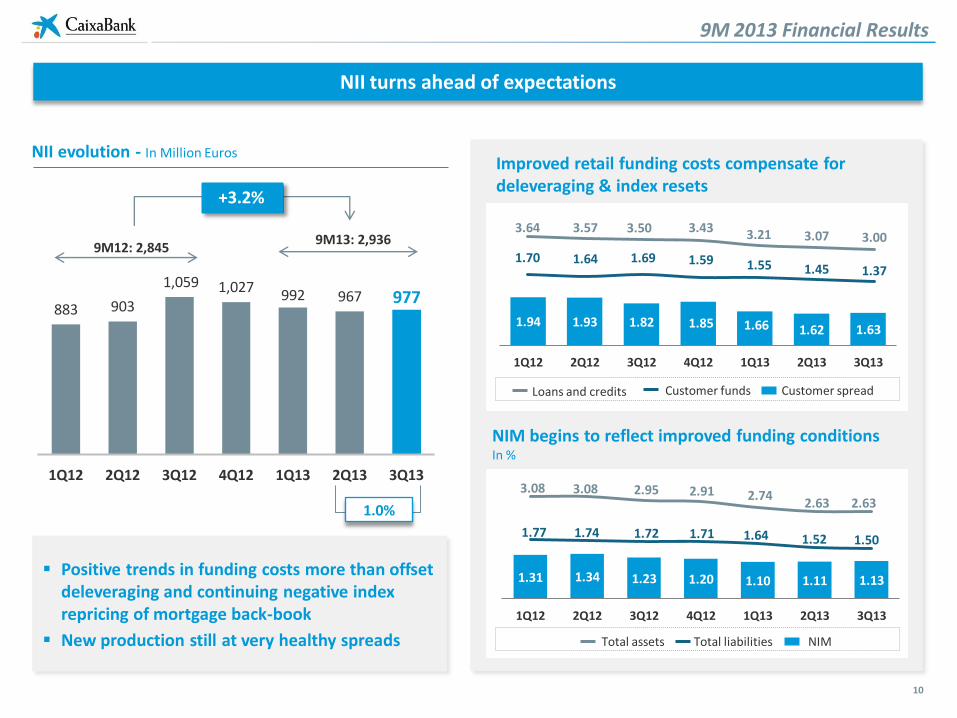

NII turns ahead of expectations

10

NII evolution - In Million Euros

883 903

1,059 1,027 992 967 977

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

+3.2%

9M12: 2,845 9M13: 2,936

1.0%

Positive trends in funding costs more than offset deleveraging and continuing negative index repricing of mortgage back-book

New production still at very healthy spreads

NIM begins to reflect improved funding conditions In %

Improved retail funding costs compensate for deleveraging & index resets

3.64 3.57 3.50 3.43 3.21 3.07 3.00

1.70 1.64 1.69 1.59 1.55 1.45 1.37

Customer funds Loans and credits Customer spread

1.94 1.93 1.82 1.85 1.66 1.62 1.63

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

1.31 1.34 1.23 1.20 1.10 1.11 1.13

3.08 3.08 2.95 2.91 2.74 2.63 2.63

1.77 1.74 1.72 1.71 1.64 1.52 1.50

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Total liabilities NIM Total assets

9M 2013 Financial Results

Successful management of time deposits spreads has been critical to offset low rate impacts

11

Strict pricing discipline leads to a significant reduction in new time deposit costs

New asset production continues at high spreads, with limited impact due to the lack of credit demand

Time deposits and retail CP - Back vs. front book (bps)

Loan book yields - Back vs. front book (bps)

254 258 244 235

224

180 173

137

4Q12 1Q13 2Q13 3Q13

343 321 307 300

430 424 465 472

4Q12 1Q13 2Q13 3Q13

Front book Back book Front book Back book

-30 bps

-71 bps

+158 bps +172 bps

-98 bps

Favourable trends on deposit costs though maturity profiles delay impact

Back book still affected by negative Euribor 12M index resets

-78 bps +103 bps +87 bps

9M 2013 Financial Results

12

High provisioning charges continue while weak economic conditions persist

(1) Includes provisions for contingencies and losses on financial investments (2) €1bn related to BCIV and €1.5 bn to BdV loan book (gross) after accounting for APS

Recurrent charges consistent with previous quarters Recurrent credit impairments, In Million Euros

952 1,018

1,387

633

1H12 2H12 1H13 3Q13

High provisioning efforts to continue in upcoming quarters:

o Economy stabilising but still with significant headwinds

o Generic provisions cannot be reallocated to other loan books

9M13 Total Impairments In Million Euros

Pending RDL 18/2012

Provisions for refinanced loans

Less: transfer from RE generic

Other credit provisions

Other provisions1

Impairment losses

Fair Value Adjustments2

902

540

(165)

2,020

152

3,449

2,507

TOTAL impairments: €5,956 M

9M 2013 Financial Results

Asset quality

Organic trends confirm gradual reduction in pace of NPL formation

13

Stabilisation trends in new NPL formation

NPL ratio increases partly due to denominator effect (deleveraging)

NPLs (in Billion Euros)

11.8 20.5 22.6

8.5 2.0

3.3

3Q12 4Q12 1Q13 2Q13 3Q13

BCIV BdV

25.7 25.9 22.5 20.2 20.3

Refinanced loans

NPL coverage remains high at 65% after front-loading required provisions on refinanced loans in 1H13

63% 63%

77%

66% 65%

3Q12 4Q12 1Q13 2Q13 3Q13

65%

€25.7 bn Total NPLs

~80% Backed by real collateral

€6.6 bn Are not past due (25% of total)

11.40% NPL ratio

6.69% Ex RE developers

€16.6 bn Total Credit provisions

Including: €4.4 bn Generic Provisions

NPL ratios affected by reclassification of refinanced loans and denominator effect

14 (1) Includes contingent liabilities

5.72%

4.54%

9.11%

21.59%

10.29%

51.53%

1.39%

11.40%

NPL1 ratio by segments

Loans to individuals

Residential mortgages - home purchase

Other

Loans to businesses

Corporate and SMEs

Real Estate developers

Public sector

Total loans

Ex- Real Estate developers

NPL 30th Jun

5.67%

4.70%

8.37%

20.98%

9.41%

50.59%

1.54%

11.17%

6.41%

NPL 30th Sep

6.69%

NPL 31st Dec

3.57%

2.80%

5.72%

17.24%

5.96%

44.22%

0.74%

8.63%

3.98%

Ratio affected by extraordinary items

Residential mortgages continue to show resilience while pressure remains on SMEs as economic weakness persists

RE Developer ratio deteriorates at lower pace and transfer to foreclosed assets continues

Key drivers of YTD NPL ratio evolution:

YTD change: +277bps

• Banco de Valencia

• Refinanced loans

• Deleveraging (lower denominator)

• NPL formation

+23bps

+134bps

+101bps

+19bps

Asset quality

119.9

88.8

31.1

84.9

59.6

25.3

10.4

Loan Book € Bn

215.3

584 763 897

-198

380 64

-173

528

566 462

1,190

831

566

329

Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13

Total NPLs Foreclosed RE

15

Falling net inflows of problematic assets consistent with improving macro

Organic evolution confirms progressive reduction of new net NPL formation

High foreclosure levels gradually offset by commercial activity

(1) Evolution of total gross NPLs (excluding provisions) and total gross foreclosed assets (quarterly variation of the loan-equivalent amounts), excluding the impact of BCIV and BdV acquisitions and the impact of the reclassification of €3.3bn of refinanced loans to NPLs materialized in 2Q13

Expect this gradual trend to continue:

Stabilisation of the economy

Increased activity in Real Estate market

Continued positive evolution of 0-90 days past due bucket

NPLs & Foreclosed assets1 – Organic QoQ variation €M

1,112 1,329 1,359

992 1,211

156

Positive Evolution of 0-90 Days Past Due Bucket Rebased to 100

630

100 92

67 70 66 57 50 39

Jul-12 Sep-12 Nov-12 Jan-13 Mar-13 May-13 Jul-13 Sep-13

BdV

Asset quality

Clean-up of real estate loan exposure an ongoing process

16

RE developer loans breakdown evolution In Billion Euros

Provisions (in Billion Euros)

Coverage

NPL 6.1 49.6%

Substandard 0.7 29.8%

Performing 1.9 21.4%

Provisions for RE developer loans

8.7 36.9%

Better mix than peers:

o Exposure to land of 19.5%, o/w €4 bn out of €4.6 bn already classified as problematic with 55% specific provisions

o 58.7% is finished housing

Coverage of problematic loans at 59%1

Coverage of total developer loans at 36.9% - close to OW adverse scenario of 37.6% EL

(1) Includes €1.9 bn of generic RE provision but excludes collateral value

14.0 12.0 11.2 9.8 8.9

3.7 3.1 2.8

2.6 2.6

12.2 11.9 12.5

12.6 12.2

9M12 4Q12 1Q13 1H13 9M13

29.9

Performing

Substandard

NPL

23.7 27.0 26.5 25.0

+€0.9 bn

-€4.2 bn

Non-organic

Organic RE developer loans

YTD -€3.3 bn

Asset quality

High coverage of foreclosed assets enables a quick pace of disposals

17

Building Center1 repossessed real estate assets for sale breakdown

Sales continue to accelerate, although seasonality has affected the activity of the quarter

Rentals represent 49% of total 9M13 commercial activity

Total rental portfolio of €1.5 bn NBV, with 87% occupancy ratio and gross yield of 4.8% of net book value

(1) The real estate holding company of CaixaBank, S.A. (2) Total disposals of €3.6bn and 21,705 units, at loan-equivalent amounts & including developer disposals

RE assets from loans to construction and RE development

Finished building

Buildings under construction

Land

RE assets from mortgage loans to households

Other repossessed assets

Total (net)

Rental portfolio (net)

4,761

2,753

315

1,693

1,190

376

6,327

1,531

50%

40%

53%

60%

46%

50%

49%

Net amount Coverage

As of September 2013. In Million Euros

Increased commercial activity Building Center commercial activity

In Million Euros

1,544 790

754

Sales

Rental Assets

9M13 unit disposal2: 12,988

143

641

995

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

J F M A M J Jl A S O N D

2011 2012 2013

Asset quality

Access to wholesale markets at attractive prices a reflection of liquidity position

(1) Includes cash, interbank deposits, accounts at central banks and unencumbered sovereign debt (2) €6.8bn from CABK + €5.8bn from BdV (3) Defined as: gross loans (€215,312M) net of loan provisions (€16,133 M) (total loan provisions excluding those corresponding to contingent guarantees) and excluding pass-

through funding from multilateral agencies (€7,364 M) / retail funds (deposits, retail issuances) (€163,040 M)

Total available liquidity

In Billion Euros

LTRO facility: €21.5 bn (€12.6 bn2 prepaid in 1H13)

Existing liquidity > pending LTRO

Wholesale maturities and LTRO repayment can be comfortably managed:

Proven access to market at attractive prices: €4.75bn issued in 2013, €1.75bn in Q3 2013:

Oct’13: issuance of €1bn of 3.5yr senior unsecured at MS+170

Oct’13: issuance of €0.75bn of 10NC5 subordinated debt at MS+395

Strong deleveraging has gradually reduced funding gap

LTD ratio evolution3

128% 125% 118%

Dec'12 Mar'13 Jun'13 Sep'13

117%

18

€3.5bn

2013

€8.6 bn

2014

€7.0 bn

2015

35.6 44.5

17.5

21.8

Dec'12 Sep'13

Unused ECB discount facility

Balance sheet liquidity1

53.1

66.3

As a % of total assets

15.2% 19.3%

Wholesale maturities as of September 30th

Liquidity and funding

Access to wholesale markets at attractive prices a reflection of liquidity position

19

Liquidity and funding

Stats:

Book/Orders 5000/320

Non Spanish Allocation 82%

Real Money Accounts 81%

Issuer RatingDeal

SizeMaturity Spread Coupon Stats

M/S&P/F Book / orders

Banco Popular Ba1/BB/BB+ €750 2.5 MS+362 4.00% 1300/176

CaixaBank Baa3/BBB-/BBB €1,000 3 MS+285 3.25% 5000/320

BBVA Baa3/BBB-/BBB+ €1,500 3 MS+273 3.25% 3600/340

BBVA Baa3/BBB-/BBB+ €1,500 5 MS+295 3.75% 5400/381

Santander Baa2/BBB/BBB+ €1,000 7 MS+275 4.00% 1200/200

Issuer RatingDeal

SizeMaturity Spread Coupon Stats

M/S&P/F

Book / orders

Bankinter A3/-/A- €500 3.5 MS+220 2.75% 3000

Kutxa Aa3/-/AA- €750 4 MS+220 3.00% 3750/200

Santander Aa3/-/- €2,000 5 MS+195 2.875% 2600/186

Bankinter A3/-/A- €500 5 MS+220 3.125% 700

Sabadell A3/-/- €1,000 5 MS+250 3.375% 3300

CaixaBank A3/AA-/- €1,000 5 MS+210 3.00% 2700/180

Popular Aa3/-/- €500 6 MS+270 3.75% 1100/100

BBVA Aa3/-/- €1,000 10 MS+215 3.875% 3000/160

Spanish Senior Unsecured issues in 2013

Spanish Covered Bond issues in 2013

Stats:

Issuer RatingDeal

SizeMaturity Spread Coupon Stats

M/S&P/F Book / orders

Banco Popular Ba1/BB/BB+ €750 2.5 MS+362 4.00% 1300/176

CaixaBank Baa3/BBB-/BBB €1,000 3 MS+285 3.25% 5000/320

BBVA Baa3/BBB-/BBB+ €1,500 3 MS+273 3.25% 3600/340

BBVA Baa3/BBB-/BBB+ €1,500 5 MS+295 3.75% 5400/381

Santander Baa2/BBB/BBB+ €1,000 7 MS+275 4.00% 1200/200

Issuer RatingDeal

SizeMaturity Spread Coupon Stats

M/S&P/F

Book / orders

Bankinter A3/-/A- €500 3.5 MS+220 2.75% 3000

Kutxa Aa3/-/AA- €750 4 MS+220 3.00% 3750/200

Santander Aa3/-/- €2,000 5 MS+195 2.875% 2600/186

Bankinter A3/-/A- €500 5 MS+220 3.125% 700

Sabadell A3/-/- €1,000 5 MS+250 3.375% 3300

CaixaBank A3/AA-/- €1,000 5 MS+210 3.00% 2700/180

Popular Aa3/-/- €500 6 MS+270 3.75% 1100/100

BBVA Aa3/-/- €1,000 10 MS+215 3.875% 3000/160

Spanish Senior Unsecured issues in 2013

Spanish Covered Bond issues in 2013

Book / orders 2500/161

Non Spanish Allocation 71%

Real Money Accounts 78%

Issuer RatingDeal

Size

Issuance

dateMaturity Spread Coupon Stats

M/S&P/F

Book / orders

Cajamar Baa2/-/BBB €500 07/05/2013 3 MS+290 3.375% 900 / 108

Bankinter A3/-/A- €500 10/01/2013 3.5 MS+220 3000

Bankinter (tap) A3/-/A- €500 29/04/2013 3.3 MS+172 1000 / 75

Popular A3 €400 13/05/2013 4 MS+205 4.125% 525 / 45

Kutxa Aa3/-/AA- €750 18/01/2013 4 MS+220 3.00% 3750/200

Popular Baa2 €750 02/09/2013 4 MS+240 3.50% 800 / 100

Santander Aa3/-/- €2,000 21/01/2013 5 MS+195 2.875% 2600/186

Bankinter A3/-/A- €500 24/01/2013 5 MS+220 3.125% 700

Sabadell A3/-/- €1,000 11/01/2013 5 MS+250 3.375% 3300

CaixaBank A3/AA-/- €1,000 12/03/2013 5 MS+210 3.000% 2700/180

Popular A3 €500 14/01/2013 6 MS+270 1100/100

Popular (tap) A3 €100 30/04/2013 6 MS+235

BBVA Aa3/-/- €1,000 17/01/2013 10 MS+215 3.875% 3000/160

2.75%

3.75%

Book / orders 2800 / 150

Non Spanish Allocation 65%

Real Money Accounts 83%

Book / Orders 2700/180

Non Spanish Allocation 79%

Real Money Accounts 71%

Spanish Subordinated Debt Issues in 2013 Stats:

Issuer Rating

Deal

Size

Issuance

dateMaturity Spread Coupon

M/S&P/F

CaixaBank -/BB+/BBB- €750 29/10/2013 10NC5 MS+395 5.000%

Book / orders 3300 / 300

Non Spanish Allocation 87%

Real Money Accounts 74%

Issuer RatingDeal

Size

Issuance

dateMaturity Spread Coupon

M/S&P/F

Banco Popular Ba1/BB/BB+ €750 08/01/2013 2.5 MS+362 4.00%

Banco Popular Ba3/BB-/BB+ €750 06/11/2013 2.5 MS+232 2.875%

CaixaBank Baa3/BBB-/BBB €1,000 09/01/2013 3 MS+285 3.25%

BBVA Baa3/BBB-/BBB+ €1,500 05/03/2013 3 MS+273 3.25%

CaixaBank Baa3/BBB-/BBB €1,000 07/10/2013 3.5 MS+170 2.500%

BBVA Baa3/BBB-/BBB+ €1,500 03/01/2013 5 MS+295 3.75%

CaixaBank Baa3/BBB-/BBB €1,000 30/04/2013 5 MS+245 3.125%

Santander Baa2/BBB/BBB+ €1,000 16/01/2013 7 MS+275 4.00%

2

0

Assets Encumbrance

Liquidity and funding

UNENCUMBERED

LOANS PORTFOLIO TOTAL

RMBS/ABSTOTAL

ENCUMBERED

TOTAL

UNENCUMBEREDLEGALLY

REQUIRED

COLLATERAL

REMAINING

COLLATERAL

MORTGAGES PORTFOLIO (ex - sec) 139,932 93,538 46,393 --- 139,932 ---

PUBLIC SECTOR PORTFOLIO (ex - sec) 12,049 10,000 2,049 --- 12,049 ---

OTHER LOANS PORTFOLIO (ex - sec) 28,232 --- --- --- --- 28,232

SECURITISATIONS (**) 9,632 --- --- 9,632 9,632 ---

LOANS TO CUSTOMERS 189,845 103,538 48,442 9,632 161,612 28,232

REPOS / ENCUMBERED ASSETS 10,488 --- --- --- 10,488 ---

INSURANCE COMPANIES ASSETS (ENCUMBERED) 32,897 --- --- --- 32,897 ---

REST OF ASSETS (UNENCUMBERED) 109,445 --- --- --- --- 109,445

TOTAL ASSETS 342,675 103,538 48,442 9,632 204,997 137,678

ENCUMBERED

(*) Legally required OC ratio is 125% for Mortgage CB and 142,9% for Public Sector CB. Nevertheless, CB are backed by the whole portfolio, which thus it's fully encumbered.

(**) It includes all type of securitized loans

(***) Related to collateral agreements (CSA/GMRA/other)

COVERED BONDS*

c c

PUBLIC ISSUANCE

RETAINED/ECB

COLLATERAL TOTAL ISSUED

MORTGAGE COVERED BONDS 40,541 34,289 74,831

PUBLIC SECTOR COVERED BONDS 350 6,650 7,000

RMBS/ABS (***) 2,118 7,513 9,632

SENIOR DEBT (except GGB) 7,621 154 7,775

GOVERNMENT GUARANTEED BONDS 1,485 320 1,805

TOTAL ISSUED 52,116 48,927 101,042

30/09/2013

3,615

9,010

7,262 7,175

4,022

5,648

2,484

379

2,874

1,394

250

2,364

610 450 189 90 20 44 20 163

-

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2025 2027 2031 2037 2038 2046 2047 2048 Perp.

Senior Debt (includes GGB) Covered Bonds Subordinated debt/Preferred Stock Other

21

(1) Data in Million €, excluding retained issues, and including GGBs Bancaja. Bonds issued in October 2013 are not included yet. (Issued in October -> € 1 bn senior unsecured bond (maturity 2017) , and € 0.75 bn sub debt 10NC5)

Source: CaixaBank

Institutional Caixabank&BdV’s Issues: Maturity Profile as of September 2013 1

INSTITUTIONAL DEBT OUTSTANDING1: 48.064 € Mn

Liquidity and funding

12.5% 11.6% 11.4% 11.4% 10.3% 10.3%

0%

5%

10%

15%

Peer 1 Peer 2 Peer 3 Peer 4 Peer 5

Dec'12 Sep'13

Solvency

Sound capital position

BIS-2.5 Core Capital evolution

In %

Core Capital

RWAs

17.7 bn

161.2 bn

17.7 bn

141.4 bn

22

(1) Mainly includes the impact of restructuring costs, the charges related to refinanced loan book, the booking of €700M of net FV adjustments attributable to the BCIV acquisition and other non-recurrent adjustments

(2) DTAs as of Sept 30th include €2.8 bn of temporary differences related to credit provisions and foreclosed assets (3) Peers include: Bankia, BBVA, Popular, Sabadell and Santander. Last reported figures

11.0%

+169bps 12.5%

Organic

-31bps

+64bps

Inbursa

Other non-recurrent

items1

+62bps

BdV

-66bps RDL

18/2012

-43bps

FROB Prepayment

Core Capital BIS-3 FL (Sep’13)

8.3%

BIS-2.5 Core Capital peer comparison3

In %

Reinforcement of Core Capital continues: 150 bps of core capital generated in 9 months despite €1bn of BCIV FROB prepayment

Early delivery of year-end BIS-3 FL targets. Core Capital BIS-3 FL stands at 8.3%.

Main impact under BIS-3 FL regime related to DTA deductions: significant capital uplift from the outcome of the negotiation on DTAs expected by year end2

23

26.1%

CaixaBank has grown its Core Capital base by more than 30% since Dec 2010… without resorting to public aid, rights issues or selling core assets, and while absorbing significant provisions

Core Capital evolution

Strong capital generation

13.4

16.6 17.2 17.1

18.1

17.7

8.9%

11.3%

12.5% 13.0%

11.6%

12.5%

100

110

120

130

140

150

160

170

180

190

200

d-10 m-11 j-11 s-11 d-11 m-12 j-12 s-12 d-12 m-13 j-13 s-13

Core Capital % Core Capital

-7%

-4%

-2%

3%

6%

14%

14%

20%

22%

25%

27%

30%

30%

39%

58%

-7% -2% 3% 8% 13% 18% 23% 28% 33% 38% 43% 48% 53% 58%

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Peer 8

Peer 9

Peer 10

Peer 11

Peer 12

CaixaBank

Peer 14

Peer 15

Core Capital Base growth since Dec 2010

Peers Include ABN, Barclays, Commerzbank, CS, DB, ING, Lloyds, Nordea, Rabobank, RBS, SEB, SHB, SG and UBS. Last reported accounts

Average ex-CaixaBank: 17%

(bn€)

+3.2%

10.6%

+ €4.3 bn

Solvency

Access to wholesale markets: The First benchmark Tier 2 out of Spain since 2007

Basel 2.5 Leverage Ratio (%)

24

Solvency

Instrument: Subordinated Non-Deferrable Securities

Tier 2 issue – Terms

Issue Ratings: BB+/BBB- (S&P/Fitch) Issue Date: 29/10/2013

Maturity Date: 14/11/2013 (10NC5)

Optional Redemption: One time issuer call after 5 years (14/11/2018) Coupon: 5%

Interest: 5% payable annually till 14/11/2018. Then, MS 5y prevailing at the issuer call date + 395 bps

Tier 2 issue – Main objectives

Reinforce total capital position and loss-absorption capacity

Diversify capital and funding bases

Distribution by Geography Distribution by Investor Type

459 INVERSORES DEUDA SENIOR More than 450 investors participated in our 3 senior unsecured

issuances

c. 30% out of them also took part in our recent Tier 2 transaction

Around 300 investors in the Tier 2 deal: 172 were new

AROUND 630 INVESTORS

Investors participation in

CaixaBank Senior & Sub Debt (2013)

Size: €750 mm

RWAs / Assets (%)

Peers Include ABN, Bankia, Barclays, BBVA, Commerzbank, CS, DB, ING, Lloyds, Nordea, Popular, Rabobank, RBS, Sabadell, Santander, SEB, SHB, SG and UBS. Last reported accounts Leverage ratio is defined as CET1 B2.5 over Total Assets

CaixaBank stands out for the quality of its capital and for its low leverage

55.2% 53.6%

46.2% 42.1% 41.3%

36.3% 35.8% 33.5% 32.9% 32.3% 31.6% 30.1% 28.7%

25.6% 25.3% 25.0% 22.3% 21.5%

18.6% 16.5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

Peer 1 Peer 2 Peer 3 Peer 4 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 Peer 12 Peer 13 Peer 14 Peer 15 Peer 16 Peer 17 Peer 18 Peer 19 Peer 20

6.1% 5.8%

5.3% 5.2% 4.9% 4.9% 4.5%

4.1% 4.0% 4.0% 3.9% 3.9% 3.8% 3.8% 3.7% 3.6% 3.5%

2.8% 2.8% 2.2%

0%

5%

Peer 1 Peer 2 Peer 3 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 Peer 12 Peer 13 Peer 14 Peer 15 Peer 16 Peer 17 Peer 18 Peer 19 Peer 20

Basel 2.5 Leverage Ratio (%)

25

Solvency

26

Covered Bond Label Compliant since 1st January 2013

Moody’s Investors Service A3

AA-

Best rated Covered Bonds in Spain

High quality collateral & strong overcollateralization

Low risk profile: mortgage portfolio prudently managed

Always aiming to the best market standards Transparency: complete quarterly information available in our

web page: http://www.caixabank.com/inversoresinstitucionales/inversoresrentafija_en.html

Solid OC levels Total OC: 187% -> and flexibility to optimize our collateral:

Legal OC: 130%

34 bn of retained /unused Covered Bonds

….Despite following eligibility criteria stricter than legal

Almost 70% of residential loans, out of which:

90% with LTV < 80%

89% First home loans

Comfortably above the legally required ratio (125%)….

Remaining Issuing Capacity: 4,4€ Bn (mortgage & public sector CB)

CaixaBank Covered Bonds Programme - Highlights

Covered Bonds

Mortgage Covered Bond Programme

CaixaBank Covered Bonds Programmes - Main figures Sept ‘13

27

Spanish Public Sector Covered Bond Programme

Issuing capacity & Collateral type

Remaining Issuing Capacity 4,436 € Bn Collateral by Type

65%27%

8%

Residential Commercial Public Sector

RATINGS 30/09/2013

Moody's A3

S&P AA-

RATINGS 30/09/2013

Moody's A3

Mortgages CB; 3,002

Public Sector CB; 1,434

MORTGAGE COVER BONDS 30/09/2013

Outstanding nominal (mill €) 74,831

OC (total) 187%

OC (legal - eligible portfolio) 130%

Issuing Capacity 3,002

Average Maturity (years) 6.11

PUBLIC SECTOR COVER POOL

Cover Pool Size (mill €) 12,049

Number of loans 6,857

Average loan Balance (€) 1,757,161

WA Seasoning (years) 3.5 yrs

WA Remaining Term (years) 6.5 yrs

30/09/2013 PUBLIC SECTOR COVER BONDS 30/09/2013

Outstanding nominal (mill €) 7,000

OC 172%

Issuing Capacity 1,434

Average Maturity (years) 2.6

MORTGAGE COVER POOL 30/09/2013

Cover Pool Size (mill €) 139,932

Residential Assets 71%

Comercial Assets 29%

Elegible Pool (mill €) 97,291

Number of loans 1,482,926

Average loan Balance (€) 94,362

WA Seasoning (years) 6.5

WA Remaining Term (years) 19.5

WA LTV 57.4%

WA LTV Elegible Pool 52.9%

Covered Bonds

2,692

7,407

5,708

6,029

4,041

3,999

2,144

379

2,874

1,354

250

0

0

0450

189 90

20

952

459

1,325

303

2,031

3,247

3,010

3,500976

2,0631,300

3,500

2,464

4,250

1,900

0

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2031

2037

2038

2048

Public Issues Retained Issues

Total Collateral Eligible vs non-eligible Max. CB Issuance Outstanding CBs vs Remaining Issuing

Capacity

139.9

97.3

77.8 74.8

42.6

3.0

28

CaixaBank Mortgage Covered Bond Programme Sept ‘13

Remaining Issuing Capacity

x 80%

ELIGIBLE

REMAINING ISSUING CAPACITY: 3 Bn €

Maturity Profile

Total Covered Bonds -> 74,831 € Bn Public -> 40,541 € Bn Retained -> 34,289 € Bn

Issued

In Billion €

Mortgages Public Sector

Total Collateral for Covered Bonds 145,758 11,659 Elligible Portfolio 101,130 11,659

Cédulas

Hipotecarias

Cédulas

Territoriales

Used Collateral 99,199 9,571 Covered Bond Issued Amount 79,359 6,700

Over Collaterization (**) 184% 174%

Available Collateral 1,932 2,087

REMAINING ISSUING CAPACITY (*) 1,545 1,461 Mn €

(*) Issuing Capacity= 80% of Collateral Available for C. Hipotecarias and 70% for C. Territoriales

(**) Due to the early amortisation of € 3 Bn of retained cedulas on April 15th, OC ratio is currently higher

Data in Million €

3,006 Available Issuing Capacity

86,1€ bn

89,1 € bn

113 bn

157 € bn

≈ 3 € bn Remaining

Issuing Capacity

44 € bn

Outstanding CBs

Max. CB Issuance

Elegible vs non-elegible

Total Collateral (Mortgages+Public

Sector)

(**) Data in million €

Mortgages

Total Collateral for Covered Bonds 139,932 Elligible Portfolio 97,291

Cédulas

Hipotecarias

Used Collateral 93,538 Covered Bond Issued Amount 74,831

Over Collaterization 187%

Available Collateral 3,752

REMAINING ISSUING CAPACITY (*) 3,002

Covered Bonds

29

CaixaBank Mortgage Covered Bond Programme Sept ‘13

OC Evolution

OC Legal

130%

Decision of generating additional collateral for the ECB credit facility to anticipate any potential deterioration in markets

Banca Cívica integration

Solid levels of total and legal OC OC could reach 345% in case Retained Covered Bonds were amortized

Covered Bonds

20%

14%

18%

22%

16%

4% 3%2%

1% 0% 1%0%

5%

10%

15%

20%

25%

90% of the loans with LTV < 80%

30

CaixaBank Mortgage Covered Bond Programme Sept ‘13

RESIDENTIAL ASSETS

Portfolio Breakdown

Seasoning

Cover Pool Description – Main figures

90% of the pool with LTV <80%

Total Mortgage Loans (ex securitization) (€ k) 99,646,116

Number of loans 1,272,938

Average Loan balance (€) 78,280

Number of Borrowers 1,085,514

Number of properties 1,348,548

WA Seasoning in months 81.3 6.8 yrs

WA Remaining term in months 261.0 21.8 yrs

Expected WA life of the portfolio in years 12.0 yrs

WA LTV (%) 57.2%

First Rank 94%

Floating Rate loan Interest Rate type: 99.4%

WA Interest Rate (Floating Rate loans) 2.22%

WA Interest Rate (Fixed Rate loans) 5.00%

Unindexed LTV

Ranges Distributions

Total Loan Balance

(ex sec) €k%

0-≤40% 19,784,799 20%

>40%-≤50% 13,517,855 14%

>50%-≤60% 17,882,966 18%

>60%-≤70% 22,176,919 22%

>70%-≤80% 16,327,370 16%

>80%-≤85% 3,547,371 4%

>85%-≤90% 2,950,224 3%

>90%-≤95% 1,833,125 2%

>95%-≤100% 731,828 1%

>100%-≤105% 273,131 0%

>105% 620,528 1%

99,646,116

Seasoning (months) € k %

< 12 2,907,330 3%

≥12-<24 4,046,305 4%

≥24-<36 6,975,247 7%

≥36-<60 13,180,140 13%

≥60 72,537,094 73%

Total: 99,646,116 3%

4%

7%

13%

73%

< 12

≥12-<24

≥24-<36

≥36-<60

≥60

Covered Bonds

* The minor difference between cover pool size reported in previous slides (139.932 MM €) and the sum of residential and commercial portfolio showed in the cover pool description and breakdown detail (99.646 MM€ + 40.751 MM€ = 140.397 MM €), is due to the use of different criteria. Both figures will converge in coming reports.

89%

8%1% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

First Home Second Home Not Owner occupied Other

31

CaixaBank Mortgage Covered Bond Programme Sept ‘13

RESIDENTIAL ASSETS

First home loans represent 89% of the residential pool

Property type € k %

First Home 89,153,176 89%

Second Home 8,235,246 8%

Not Owner occupied 1,222,357 1%

Other 1,035,337 1%

Total: 99,646,116

Loan Purpose € k %

Adquisition 63,102,584 63%

Re-mortgage 18,691,668 19%

Equity release 4,528,272 5%

Rehabilitation 6,179,178 6%

New construction 4,485,070 5%

Other 2,659,344 3%

Total: 99,646,116

63%

19%

5% 6% 5% 3%

0%

10%

20%

30%

40%

50%

60%

70%

Adquisition Re-mortgage Equity release Rehabilitation New construction

Other

Regional Distribution € k %

Catalonia 28,201,166 28%

Andalusia 17,447,791 18%

Madrid 12,866,049 13%

Valencia 7,725,958 8%

Canary Islands 6,461,078 6%

Balearic Islands 3,828,151 4%

Castile León 3,759,017 4%

Navarra 3,192,647 3%

Castile La Mancha 3,187,693 3%

Basque Country 2,694,843 3%

Murcia 2,602,180 3%

Galicia 2,060,959 2%

Aragon 1,667,514 2%

Cantabria 889,964 1%

Extremadura 859,784 1%

Others/ No info 807,935 1%

Asturias 789,226 1%

La Rioja 511,834 1%

Ceuta 74,347 0%

Melilla 17,979 0%

Total: 99,646,116

Acquisitions have led to a more diversified regional distribution of the assets

Covered Bonds

32

CaixaBank Mortgage Covered Bond Programme Sept ‘13

COMMERCIAL ASSETS

Portfolio Breakdown

Cover Pool Description – Main figures

Total Mortgage Loans (ex securitization) (€ k) 40,751,158 WA LTV (%) 57.9%

Number of loans 209,988 Floating Rate loan Interest Rate type: 96.5%

Average Loan balance (€) 194,064 WA Interest Rate (Floating Rate loans) 2.9%

Number of Borrowers 95,916 WA Interest Rate (Fixed Rate loans) 5.1%

Number of properties 259,326

WA Seasoning in months 69.2 5.8 yrs

WA Remaining term in months 166.0 13.8 yrs

Total Mortgage Loans (ex securitization) (€ k) 40,751,158 WA LTV (%) 57.9%

Number of loans 209,988 Floating Rate loan Interest Rate type: 96.5%

Average Loan balance (€) 194,064 WA Interest Rate (Floating Rate loans) 2.9%

Number of Borrowers 95,916 WA Interest Rate (Fixed Rate loans) 5.1%

Number of properties 259,326

WA Seasoning in months 69.2 5.8 yrs

WA Remaining term in months 166.0 13.8 yrs

Unindexed LTV

Ranges

Distributions

Total Loan

Balance

(ex sec) €k

%

0-≤40% 9,870,586 24%

>40%-≤50% 5,822,730 14%

>50%-≤60% 6,973,482 17%

>60%-≤70% 7,295,198 18%

>70%-≤80% 4,348,329 11%

>80%-≤85% 1,238,881 3%

>85%-≤90% 1,129,575 3%

>90%-≤95% 856,852 2%

>95%-≤100% 1,289,563 3%

>100%-≤105% 643,796 2%

>105% 1,282,165 3%

Total: 40,751,158

24%

14%

17% 18%

11%

3% 3% 2%3%

2%3%

0%

5%

10%

15%

20%

25%

30%

Property Type € k %

Offices 1,437,907 4%

Commercial stores 5,630,116 14%

Industrial 3,583,489 9%

Hotel 1,774,734 4%

RED: Flats & Houses 11,920,525 29%

Land 6,394,870 16%

Others 10,009,516 25%

Total: 40,751,158

4%

14%

9%

4%

29%

16%

25%

0%

5%

10%

15%

20%

25%

30%

35%

Offices Commercial stores Industrial Hotel RED: Flats & Houses Land Others

Covered Bonds

33

CaixaBank Mortgage Covered Bond Programme Sept ‘13

COMMERCIAL ASSETS

Portfolio Breakdown

Loan Maturity (yrs) € k %

≤ 5 8,052,745 20%

>5 - ≤10 8,251,565 20%

>10 - ≤15 7,742,942 19%

>15 - ≤25 8,966,965 22%

>25 - ≤50 7,736,790 19%

>50 151 0%

Total: 40,751,158

Regional Distribution € k %

Andalusia 8,295,096 20%

Catalonia 8,268,150 20%

Madrid 6,587,932 16%

Canary Islands 4,000,692 10%

Valencia 2,721,578 7%

Castile León 1,540,065 4%

Castile La Mancha 1,473,479 4%

Balearic Islands 1,369,037 3%

Basque Country 1,225,358 3%

Navarra 1,126,996 3%

Others/ No info 976,467 2%

Murcia 817,853 2%

Galicia 678,470 2%

Aragon 614,693 2%

Extremadura 334,383 1%

Cantabria 274,288 1%

La Rioja 228,925 1%

Asturias 192,738 0%

Ceuta 17,621 0%

Melilla 7,337 0%

Total: 40,751,158 100%

20%

20%

19%

22%

19%

0%

≤ 5

>5 - ≤10

>10 - ≤15

>15 - ≤25

>25 - ≤50

>50

Covered Bonds

-

-

-

-

350 -

1,500

2,700

250

250

1,450

500

-

500

1,000

1,500

2,000

2,500

3,000

20

14

20

15

20

16

20

17

20

18

20

19

Public Issues Retained Issues

Total Collateral Max. CB Issuance Outstanding CBs vs Remaining Issuing Capacity

12.0

8.4

7.0

0.0

1.4

34

CaixaBank Public Sector Covered Bond Programme Sept ‘13

Remaining Issuing Capacity

x 70%

REMAINING ISSUING CAPACITY: 1,4 Bn €

Maturity Profile

Total Covered Bonds -> 7,000 € Bn Public -> 350 € Bn Retained -> 6,650 € Bn

Issued

In Billion €

Mortgages Public Sector

Total Collateral for Covered Bonds 145,758 11,659 Elligible Portfolio 101,130 11,659

Cédulas

Hipotecarias

Cédulas

Territoriales

Used Collateral 99,199 9,571 Covered Bond Issued Amount 79,359 6,700

Over Collaterization (**) 184% 174%

Available Collateral 1,932 2,087

REMAINING ISSUING CAPACITY (*) 1,545 1,461 Mn €

(*) Issuing Capacity= 80% of Collateral Available for C. Hipotecarias and 70% for C. Territoriales

(**) Due to the early amortisation of € 3 Bn of retained cedulas on April 15th, OC ratio is currently higher

Data in Million €

3,006 Available Issuing Capacity

86,1€ bn

89,1 € bn

113 bn

157 € bn

≈ 3 € bn Remaining

Issuing Capacity

44 € bn

Outstanding CBs

Max. CB Issuance

Elegible vs non-elegible

Total Collateral (Mortgages+Public

Sector)

(**) Data in million €

Public Sector

Total Collateral for Covered Bonds 12,049 Elligible Portfolio 12,049

Cédulas

Territoriales

Used Collateral 10,000 Covered Bond Issued Amount 7,000

Over Collaterization 172%

Available Collateral 2,049

REMAINING ISSUING CAPACITY (*) 1,434

Covered Bonds

35

CaixaBank Public Sector Covered Bond Programme Sept ‘13

Portfolio Breakdown

Loan Maturity

Cover Pool Description – Main figures

Total Mortgage Loans (ex securitization) (€ k) 12,048,852 Floating Rate loan Interest Rate type: 92.1%

Number of loans 6,857 WA Interest Rate (Floating Rate loans) 3.01%

Average Loan balance (€) 1,757,161 WA Interest Rate (Fixed Rate loans) 4.44%

Number of Borrowers 1,866

Average exposure to borrowers (€ ) 6,457,048

WA Remaining term in months 116 9.7 yrs

WA Seasoning in months (1)

42 3.5 yrs

< 12 2,999,031 25%

≥12-<24 583,507 5%

≥24-<36 960,442 8%

≥36-<60 1,969,560 16%

≥60 5,536,312 46%

Total: 12,048,852

Loan Maturity € k %

<2m 0.02%

≥ 2m - <6m 0.88%

≥ 6m - <12m 0.28%

≥12m 1.02%

Loans in Arrears %

25%

5%

8%

16%

46%

< 12

≥12-<24

≥24-<36

≥36-<60

≥60

Covered Bonds

36

Listed Portfolio 30th September 2013

-

Appendices

37

Moody’s Investors Service Baa3

BBB-

BBB

P-3

A-3

F2

negative

negative

Long term

Short term

Outlook

A3

AA -

-

Credit Ratings

Mortgage Covered Bonds

Ratings

negative

(1) Negative Outlook (2) Short term with stable outlook

(1)

A (low) - R-1 (low) (2)

negative

Appendices

+34 93 411 75 03

Institutional Investors & Analysts Contact

We are at your entire disposal for any questions or suggestions you may wish to make. To contact us, please call or write to us at the following email address and telephone number: