49

Strictly Private & Confidential FINANCIAL YEAR 2014-15 D E C E M B E R 2 0 1 4

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | rohit-shroff |

| View: | 30 times |

| Download: | 0 times |

Strictly Private & Confidential

FINANCIAL YEAR 2014-15

D E C E M B E R 2 0 1 4

Strictly Private & Confidential2

87.6%

12.4%

Indian Retail – Huge Opportunity

2

Source: ICRIER Report and BMI Retail Report

• Even a 1% market share of the Indian Retail pie , provides a $ 6.75 Billion turnover in 2016.

• The opportunity to set up various retail models (from niche to big box) exists in the next few years .

• Department stores opportunities will increase due to lack of anchors in new malls and entry of international brandsin the country.

2012

Indian Retail: USD 500 bn

Organised Retail: USD 35 bn (7%)

2016

Indian Retail: USD 675 bn

Organised Retail: USD 84 bn (12.4%)

93.0%

7.0%

Strictly Private & Confidential3

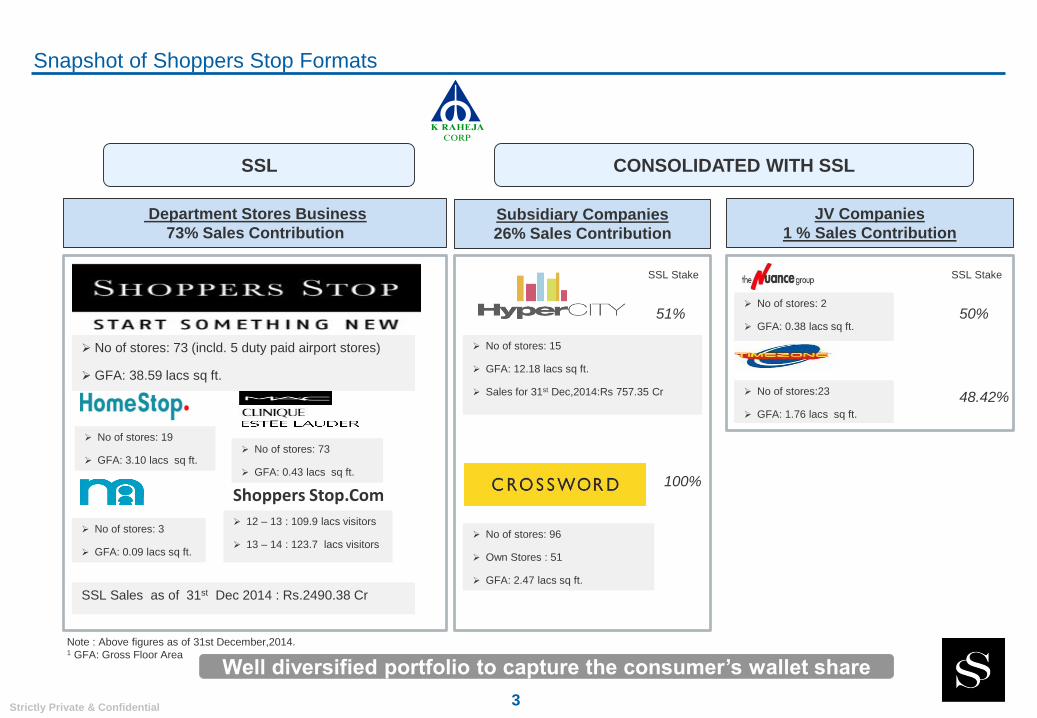

Snapshot of Shoppers Stop Formats

SSL

No of stores: 73 (incld. 5 duty paid airport stores)

GFA: 38.59 lacs sq ft.

No of stores: 3

GFA: 0.09 lacs sq ft.

No of stores: 73

GFA: 0.43 lacs sq ft.

No of stores: 19

GFA: 3.10 lacs sq ft.

Department Stores Business

73% Sales Contribution

12 – 13 : 109.9 lacs visitors

13 – 14 : 123.7 lacs visitors

Shoppers Stop.Com

No of stores: 15

GFA: 12.18 lacs sq ft.

Sales for 31st Dec,2014:Rs 757.35 Cr

No of stores: 2

GFA: 0.38 lacs sq ft.

No of stores:23

GFA: 1.76 lacs sq ft.

No of stores: 96

Own Stores : 51

GFA: 2.47 lacs sq ft.

Subsidiary Companies

26% Sales Contribution

50%

48.42%

Well diversified portfolio to capture the consumer’s wallet share

Note : Above figures as of 31st December,2014.1 GFA: Gross Floor Area

JV Companies

1 % Sales Contribution

SSL Stake

51%

100%

SSL Stake

CONSOLIDATED WITH SSL

SSL Sales as of 31st Dec 2014 : Rs.2490.38 Cr

Strictly Private & Confidential4

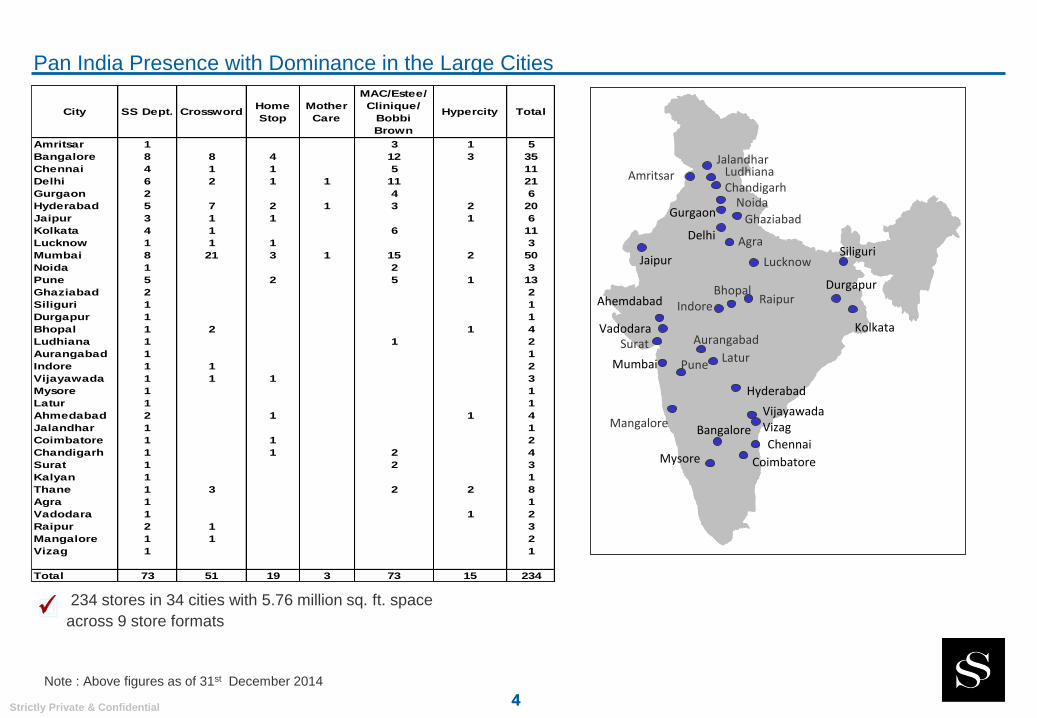

Pan India Presence with Dominance in the Large Cities

4

Note : Above figures as of 31st December 2014

234 stores in 34 cities with 5.76 million sq. ft. space

across 9 store formats

City SS Dept. CrosswordHome

Stop

Mother

Care

MAC/Estee/

Clinique/

Bobbi

Brown

Hypercity Total

Amritsar 1 3 1 5

Bangalore 8 8 4 12 3 35

Chennai 4 1 1 5 11

Delhi 6 2 1 1 11 21

Gurgaon 2 4 6

Hyderabad 5 7 2 1 3 2 20

Jaipur 3 1 1 1 6

Kolkata 4 1 6 11

Lucknow 1 1 1 3

Mumbai 8 21 3 1 15 2 50

Noida 1 2 3

Pune 5 2 5 1 13

Ghaziabad 2 2

Siliguri 1 1

Durgapur 1 1

Bhopal 1 2 1 4

Ludhiana 1 1 2

Aurangabad 1 1

Indore 1 1 2

Vijayawada 1 1 1 3

Mysore 1 1

Latur 1 1

Ahmedabad 2 1 1 4

Jalandhar 1 1

Coimbatore 1 1 2

Chandigarh 1 1 2 4

Surat 1 2 3

Kalyan 1 1

Thane 1 3 2 2 8

Agra 1 1

Vadodara 1 1 2

Raipur 2 1 3

Mangalore 1 1 2

Vizag 1 1

Total 73 51 19 3 73 15 234

Kolkata

Delhi

Jaipur

Mumbai

Hyderabad

BangaloreChennai

GurgaonGhaziabad

Pune

Noida

Amritsar

Bhopal

Aurangabad

Siliguri

Durgapur

Lucknow

LudhianaChandigarh

Indore

VijayawadaVizag

Ahemdabad

Mysore

Latur

Jalandhar

Coimbatore

SuratVadodara

Agra

Raipur

Mangalore

Strictly Private & Confidential

Store Additions since 1991

11 1

22 2

3

2 2

3

1

5

34

6

13

4

12

6

1 1 1 1 2 2 2 35

79

12

1416

1920

25

28

32

38

51

55

67

73

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

Additions 1 1 1 2 2 2 3 2 2 3 1 5 3 4 6 13 4 12 6

Total 1 1 1 1 2 2 2 3 5 7 9 12 14 16 19 20 25 28 32 38 51 55 67 73

91-92 92-93 93-94 94-95 95-96 96-97 97-98 98-99 99-00 00-01 01-02 02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12 12-13 13-14 14-15

5

Store Status Since Inception – SS Department Format

2000-01 Sales -

Rs.214 Crore

2011-12 Sales -

Rs.2000 Crore

Strictly Private & Confidential6

Transitioned the Shoppers Stop Brand from Premium to Bridge-to-Luxury

6

Successfully introduced a number of international brands, the new Indian aspires to own

Jack & Jones, French Connection, CK Jeans, GAS, Tommy Hilfiger & Mustang in apparel segment.

Loccitane, Lancome, MAC, Clinique & Estee Lauder in cosmetics

CK, Armani & Gucci in sun glasses

Burberry, Nina Ricci, Diesel & Boss in watches

Luxury

Bridge to Luxury

Contemporary

Popular

Mass

Premium

2009

SSL

2005

Our Transition

Consistent Improvement of Product Mix and Brands Profile to Attract ‘Aspirational’ Customers

Strictly Private & Confidential7

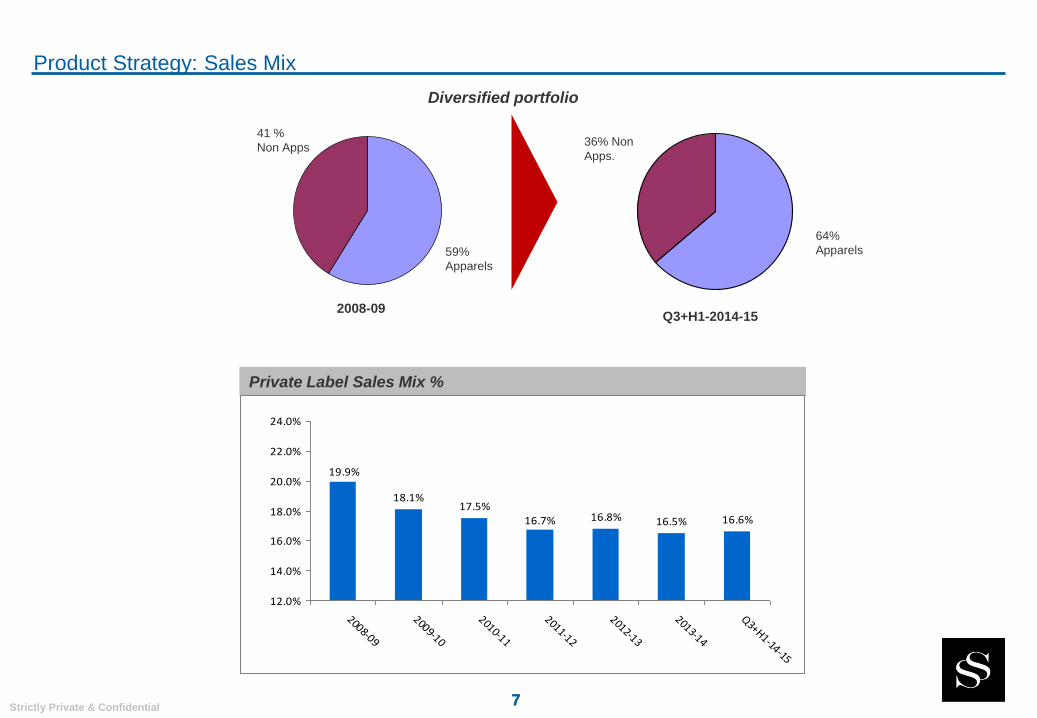

Product Strategy: Sales Mix

7

Q3+H1-2014-152008-09

41 %

Non Apps36% Non

Apps.

64%

Apparels59%

Apparels

Diversified portfolio

Private Label Sales Mix %

18.1%17.5%

16.8% 16.5% 16.6%

19.9%

16.7%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

24.0%

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

Q3+H1-14-15

Strictly Private & Confidential8

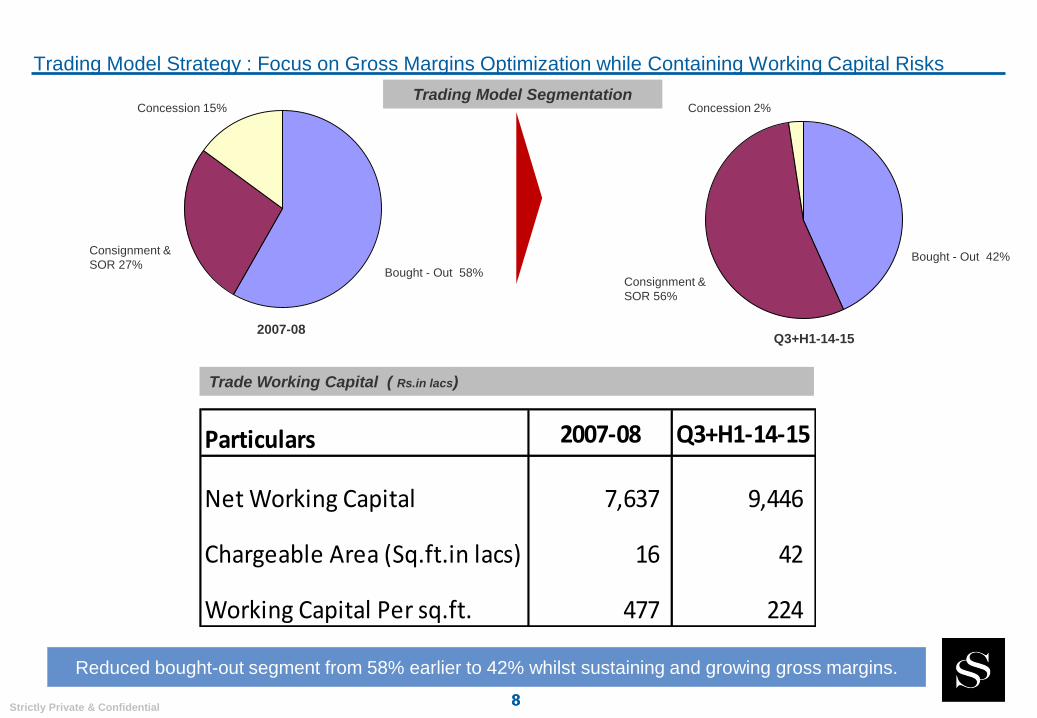

Trading Model Strategy : Focus on Gross Margins Optimization while Containing Working Capital Risks

8

Trading Model SegmentationConcession 15%

Consignment &

SOR 27%Bought - Out 58%

Concession 2%

Consignment &

SOR 56%

Bought - Out 42%

2007-08Q3+H1-14-15

Reduced bought-out segment from 58% earlier to 42% whilst sustaining and growing gross margins.

Trade Working Capital ( Rs.in lacs)

Particulars 2007-08 Q3+H1-14-15

Net Working Capital 7,637 9,446

Chargeable Area (Sq.ft.in lacs) 16 42

Working Capital Per sq.ft. 477 224

Strictly Private & Confidential9

Sustainable Improvements in Costs

Rent per sq.ft & % to Sales ( SS Dept. Business )

Service tax & GST

• Service tax on rent & other expenses having impact of 1.6% of sales•GST is expected to provide set-off of Service Tax against VAT.

Inventory Control

•Stock unsold for two seasons written off – Conservative inventory policy•PICS (Perpetual Inventory Control System ) in place – shrinkage below 0.5% of sales•Inventory under control at all times coupled with stock de-risking through change of trading model.

Shrinkage ( SS Dept. Business )

63

69

68

64

66 66 67

69

10.8%10.5%

9.8% 10.1% 10.6% 10.4% 10.5% 10.6%

56

58

60

62

64

66

68

70

72

74

2008-092009-10

2010-112011-12

2012-132013-14

Q3+H1-13-14

Q3+H1-14-15

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0.52%

0.40%0.36%

0.30%0.35%

0.40%

0.31%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

FY09FY10

FY11FY12

FY13FY14

Q3+H1-14-15

Strictly Private & Confidential10

Performance Analysis

Oracle Financials

E-Retail

BIJDA Allocation

Mobile App

HRMSDCMS

WH Mgmt.

Oracle POS

POS System

Arthur Planning B2B

JDA MMS

CRM & Loyalty

Technology Architecture

Dhristi- Netezza Data Warehouse

Planned and Focused Investment in Technology

Hyperion

Strictly Private & Confidential11

Better customer connect reflected in the growth of First Citizen members and their contribution

11

First Citizen Members (in ‘000)

First Citizen Contribution to Total Sales (%)

11

1,6112,017

2,8883,296

3,631

1,277

2,503

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY09FY10

FY11FY12

FY13FY14

Q3+H1-14-15

72%72% 75% 73%72% 69% 72%

-5%

5%

15%

25%

35%45%

55%

65%

75%

85%

FY09FY10

FY11FY12

FY13FY14

Q3+H1-14-15

Strictly Private & Confidential

9,704 9,3738,408

9,404 9,385 9,2278,668

6,315

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

Q3+H1-14-15

1,383 1,5471,873

2,1892,563

3,053

2,2132490

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

Q3+H1-13-14

Q3+H1-14-15

12

Resulting Increase in Revenue

Sales (Rs. in Cr. )

LTL Growth % ( Quarter wise )

LTL Sales Growth for SS Dept.Store for Q3-14-15Stores > 5 Years - (2.7)%Stores < 5 Years - 7.9%

Sales per sq.ft. LTL Store (in Rs. )**

**Year wise Sales per sq. ft. is not comparable due to YOY increase in LTL Sq ft area

-6.3%

0.80%

11%

2.3%

2.1%

16.0%

21.0%

13.0%

22.0%

14.0%

7.0%

11.2%

-1.3%

10.0%

1.0%

4.8%

12.5%

10.0%

12.0%

15.5%

5.5%

8.40%

3.70%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Q1-09-10

Q2-09-10

Q3-09-10

Q4-09-10

Q1-10-11

Q2-10-11

Q3-10-11

Q4-10-11

Q1-11-12

Q2-11-12

Q3-11-12

Q4-11-12

Q1-12-13

Q2-12-13

Q3-12-13

Q4-12-13

Q1-13-14

Q2-13-14

Q3-13-14

Q4-13-14

Q1-14-15

Q2-14-15

Q3-14-15

Strictly Private & Confidential

1,104 1,133

821 856 913 9751,031 1,087

-200400600800

1,0001,200

FY09FY10

FY11FY12

FY13FY14

Q3+H1-13-14

Q3+H1-14-15

2,669 2,640 2,736

1,8432,029

2,209 2,313 2,481

-

500

1,000

1,500

2,000

2,500

3,000

FY09FY10

FY11FY12

FY13FY14

Q3+H1-13-14

Q3+H1-14-15

28% 27%

24%23%

21% 21%23%23%

10%12%14%16%18%20%22%24%26%28%30%

FY09FY10

FY11FY12

FY13FY14

Q3+H1-13-14

Q3+H1-14-15

233

310349

223

365402

468

351

-

50

100

150

200

250

300

350

400

450

500

FY09FY10

FY11FY12

FY13FY14

Q3+H1-13-14

Q3+H1-14-15

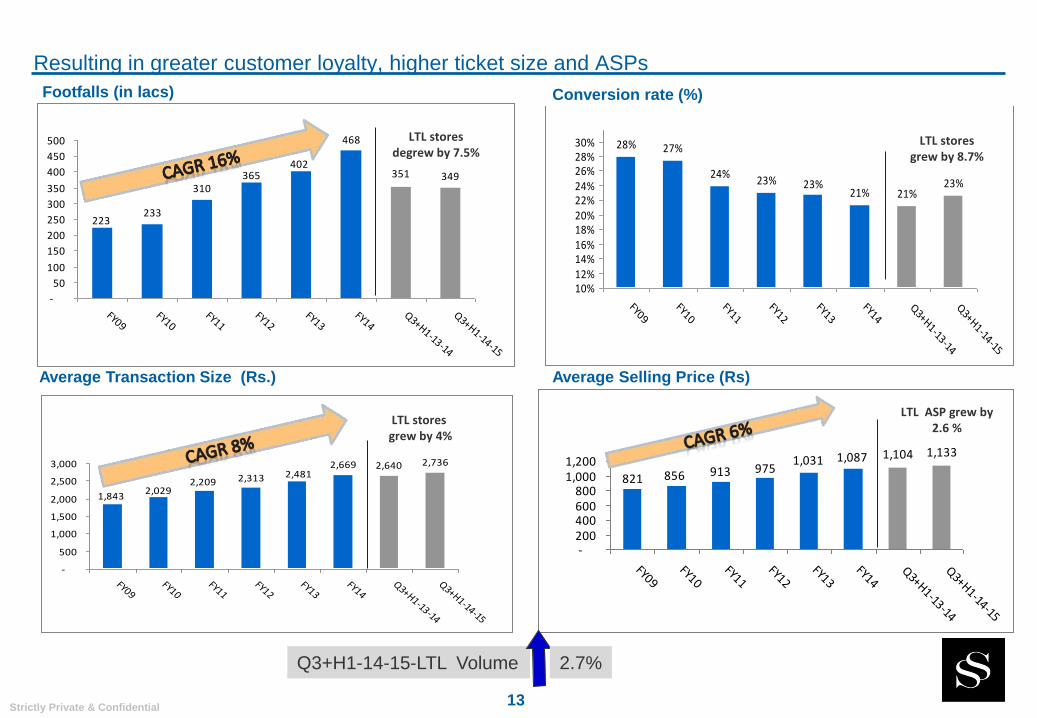

13

Resulting in greater customer loyalty, higher ticket size and ASPs

Footfalls (in lacs) Conversion rate (%)

Average Selling Price (Rs)Average Transaction Size (Rs.)

Q3+H1-14-15-LTL Volume 2.7%

LTL storesdegrew by 7.5%

LTL storesgrew by 8.7%

LTL storesgrew by 4%

LTL ASP grew by 2.6 %

Strictly Private & Confidential14

….. and Better Returns

Asset turnover ratio ( Total Assets without Group Investment)

Operating Cash Flows ( Rs. in Cr.)

ROCE % (Capital Employed without Group Investment)

Consistent bottom-line coupled with superior resource management has resulted in steady returns

4.1

4.85.2

4.75.1

4.3

-

1.0

2.0

3.0

4.0

5.0

6.0

FY09FY10

FY11FY12

FY13FY14

14.10%

-4.1%

25.3%

33.4%

22.90%

14.00%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

FY09FY10

FY11FY12

FY13FY14

81.1

110.0101.0

82.2

139.2140.9

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

FY09FY10

FY11FY12

FY13FY14

Strictly Private & Confidential15

Brand Campaign - 2013

15

Strictly Private & Confidential16

Brand Campaign - 2013

16

Strictly Private & Confidential17

Exclusive Label Campaign - 2013

Strictly Private & Confidential18

Exclusive Label Campaign - 2013

Strictly Private & Confidential19

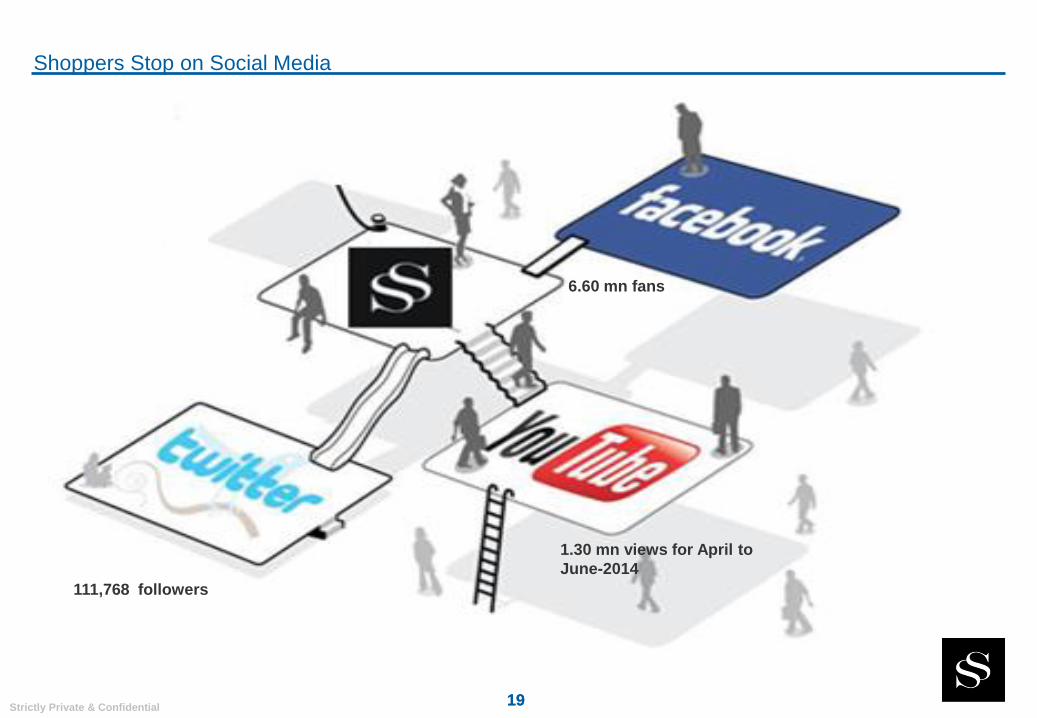

Shoppers Stop on Social Media

19

6.60 mn fans

1.30 mn views for April to

June-2014

111,768 followers

Strictly Private & Confidential20

Luckiest Boy Happiest Boy Most Special Boy

Smartest Boyfriend Most Painful Questions

http://www.youtube.com/watch?v=RtmWLHCUR0Ihttp://www.youtube.com/watch?v=ziV1EsUSsXI

http://www.youtube.com/watch?v=uqp9G-LwBQc http://www.youtube.com/watch?v=4QnIkWEmmCs http://www.youtube.com/watch?v=2s2Rsx1RQXw

Our Viral Ads

Strictly Private & Confidential2121

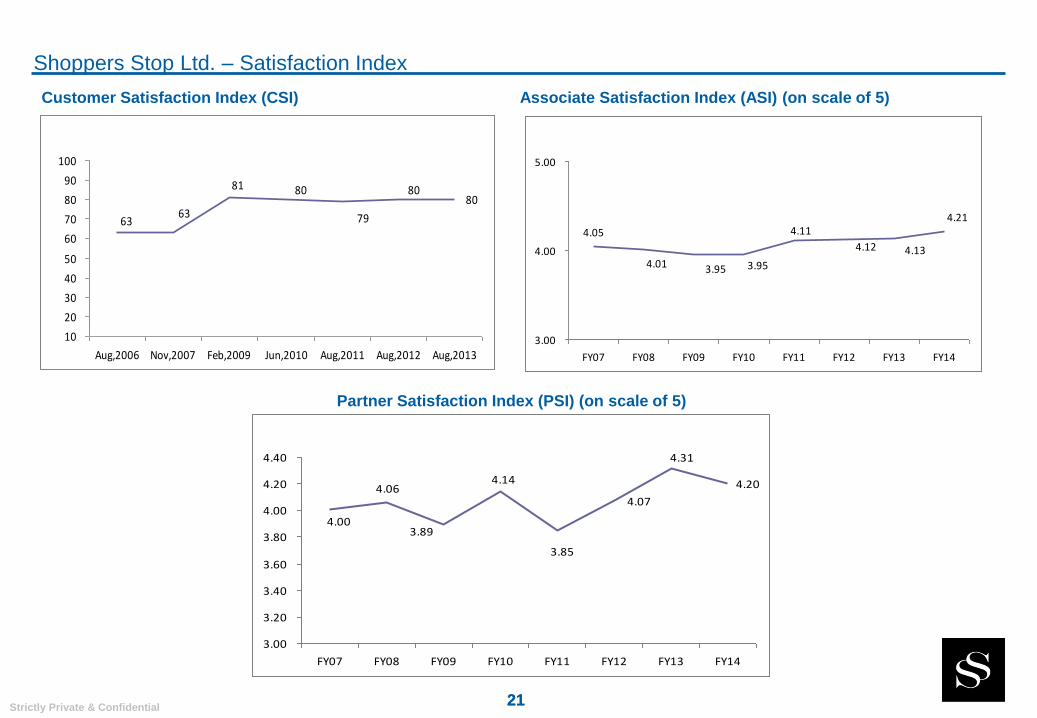

Customer Satisfaction Index (CSI) Associate Satisfaction Index (ASI) (on scale of 5)

Partner Satisfaction Index (PSI) (on scale of 5)

Shoppers Stop Ltd. – Satisfaction Index

80

6363

81 80

79

80

10

20

30

40

50

60

70

80

90

100

Aug,2006 Nov,2007 Feb,2009 Jun,2010 Aug,2011 Aug,2012 Aug,2013

4.21

4.13

4.05

4.01 3.95 3.95

4.11

4.12

3.00

4.00

5.00

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

4.07

4.20

4.31

4.00

4.06

3.89

4.14

3.85

3.00

3.20

3.40

3.60

3.80

4.00

4.20

4.40

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Strictly Private & Confidential22

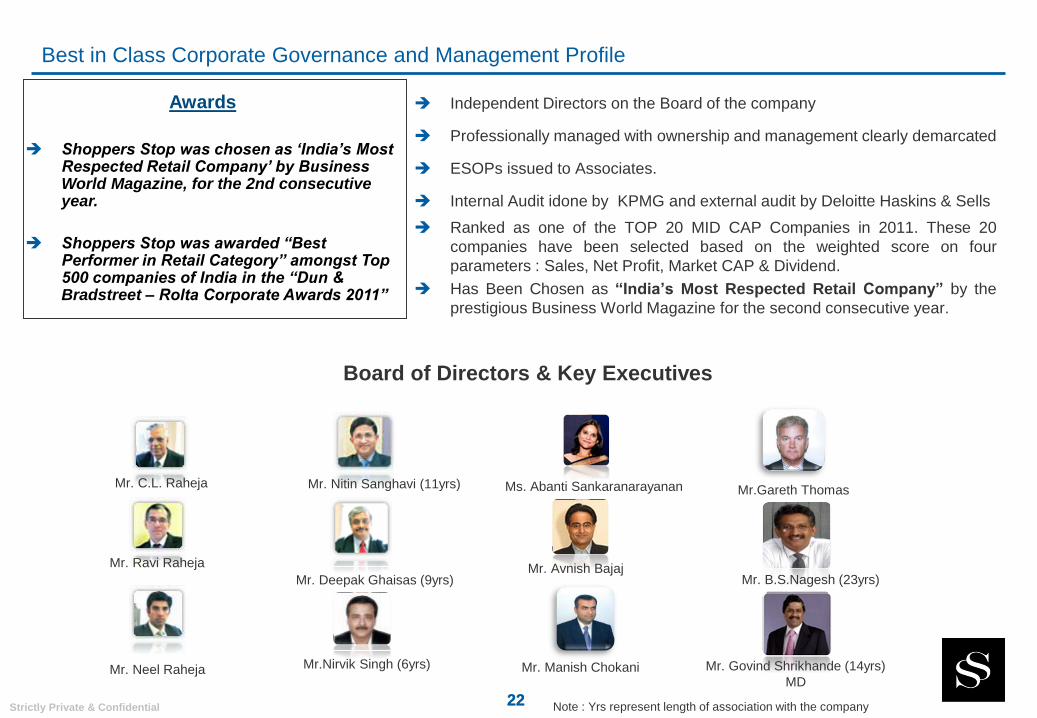

Best in Class Corporate Governance and Management Profile

22

Independent Directors on the Board of the company

Professionally managed with ownership and management clearly demarcated

ESOPs issued to Associates.

Internal Audit idone by KPMG and external audit by Deloitte Haskins & Sells

Ranked as one of the TOP 20 MID CAP Companies in 2011. These 20

companies have been selected based on the weighted score on four

parameters : Sales, Net Profit, Market CAP & Dividend.

Has Been Chosen as “India’s Most Respected Retail Company” by the

prestigious Business World Magazine for the second consecutive year.

Board of Directors & Key Executives

Mr. Deepak Ghaisas (9yrs)

Mr. Nitin Sanghavi (11yrs)

Mr.Nirvik Singh (6yrs)

Mr. C.L. Raheja

Mr. Neel Raheja

Mr. Ravi Raheja

Mr. B.S.Nagesh (23yrs)

Mr. Govind Shrikhande (14yrs)

MD

Note : Yrs represent length of association with the company

Mr. Avnish Bajaj

Awards

Shoppers Stop was chosen as ‘India’s Most Respected Retail Company’ by Business World Magazine, for the 2nd consecutive year.

Shoppers Stop was awarded “Best Performer in Retail Category” amongst Top 500 companies of India in the “Dun & Bradstreet – Rolta Corporate Awards 2011”

Ms. Abanti Sankaranarayanan

Mr. Manish Chokani

Mr.Gareth Thomas

Strictly Private & Confidential23

Corporate Social Responsibility

23

Giving Back to Society

‘Shoppers Stop’ , over the years , has contributed in its own way to make the Planet a

better place .

In our continuing endeavor to contribute to society , one of the novel practices that we have

adapted across all stores, is to celebrate the ‘ Store Birthday ‘ with the ‘Underprivileged ‘

within the store catchment .

Birthday celebrations earlier was all about fun time at the stores . Now the celebration has

moved outside the store : at Old Age homes, at Homes for the abandoned Girl Child, Home

for Destitute’ s & so on .

The Store team does its own bit by spending the day with this cross-section: touching

their lives, celebrating with them & being a part of their life .

This engagement continues & is not a one day affair : the team is in continuous touch with

these institutes & keep contributing in its own way.

A glimpse into some of the initiatives .

Strictly Private & Confidential24

Corporate Social Responsibility

24

ANDHERI STORE

Collective Drive To Save A Life

KOLKATA STORES

Visit to Old Age Home At the local Orphanage

DELHI STORE

Spending time with underprivileged children

MULUND STORE LUCKNOW STORE

A day at the Orphanage

Strictly Private & Confidential25

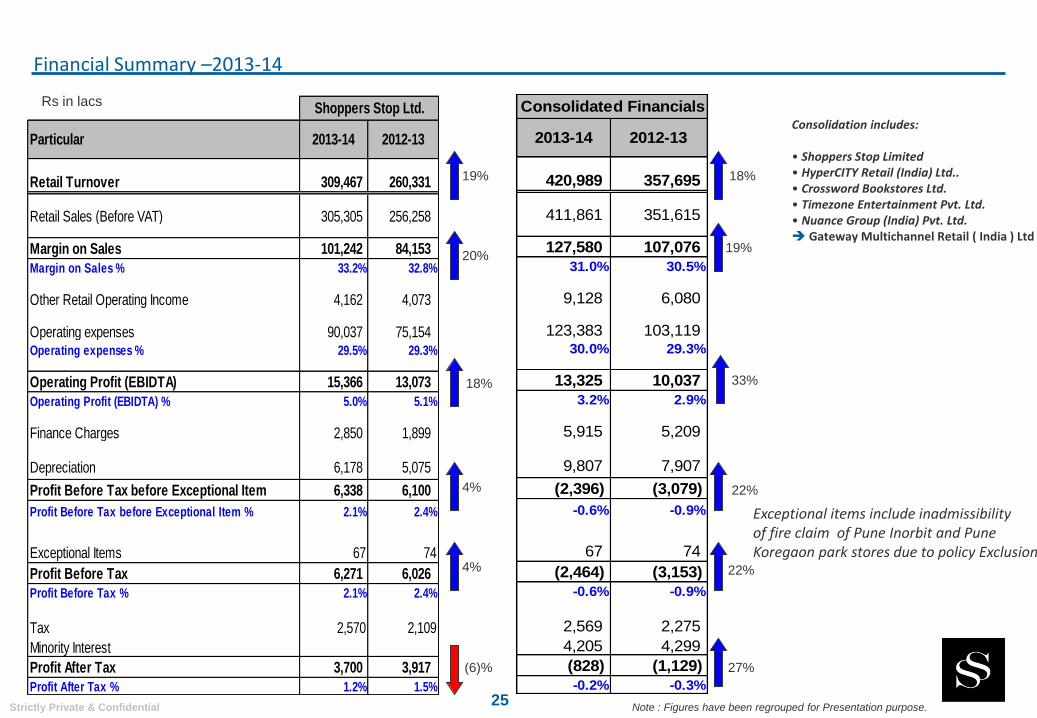

Financial Summary –2013-14

19%

Rs in lacs

Consolidation includes:

• Shoppers Stop Limited• HyperCITY Retail (India) Ltd..• Crossword Bookstores Ltd.• Timezone Entertainment Pvt. Ltd.• Nuance Group (India) Pvt. Ltd. Gateway Multichannel Retail ( India ) Ltd

Note : Figures have been regrouped for Presentation purpose.

20%

18%

4%

4%

(6)%

18%

19%

33%

22%

22%

27%

Particular 2013-14 2012-13

Retail Turnover 309,467 260,331

Retail Sales (Before VAT) 305,305 256,258

Margin on Sales 101,242 84,153

Margin on Sales % 33.2% 32.8%

Other Retail Operating Income 4,162 4,073

Operating expenses 90,037 75,154 Operating expenses % 29.5% 29.3%

Operating Profit (EBIDTA) 15,366 13,073

Operating Profit (EBIDTA) % 5.0% 5.1%

Finance Charges 2,850 1,899

Depreciation 6,178 5,075

Profit Before Tax before Exceptional Item 6,338 6,100

Profit Before Tax before Exceptional Item % 2.1% 2.4%

Exceptional Items 67 74

Profit Before Tax 6,271 6,026

Profit Before Tax % 2.1% 2.4%

Tax 2,570 2,109

Minority Interest

Profit After Tax 3,700 3,917

Profit After Tax % 1.2% 1.5%

Shoppers Stop Ltd.

2013-14 2012-13

420,989 357,695

411,861 351,615

127,580 107,076

31.0% 30.5%

9,128 6,080

123,383 103,119 30.0% 29.3%

13,325 10,037

3.2% 2.9%

5,915 5,209

9,807 7,907

(2,396) (3,079)

-0.6% -0.9%

67 74

(2,464) (3,153)

-0.6% -0.9%

2,569 2,275

4,205 4,299

(828) (1,129)

-0.2% -0.3%

Consolidated Financials

Exceptional items include inadmissibility of fire claim of Pune Inorbit and PuneKoregaon park stores due to policy Exclusion

Strictly Private & Confidential26

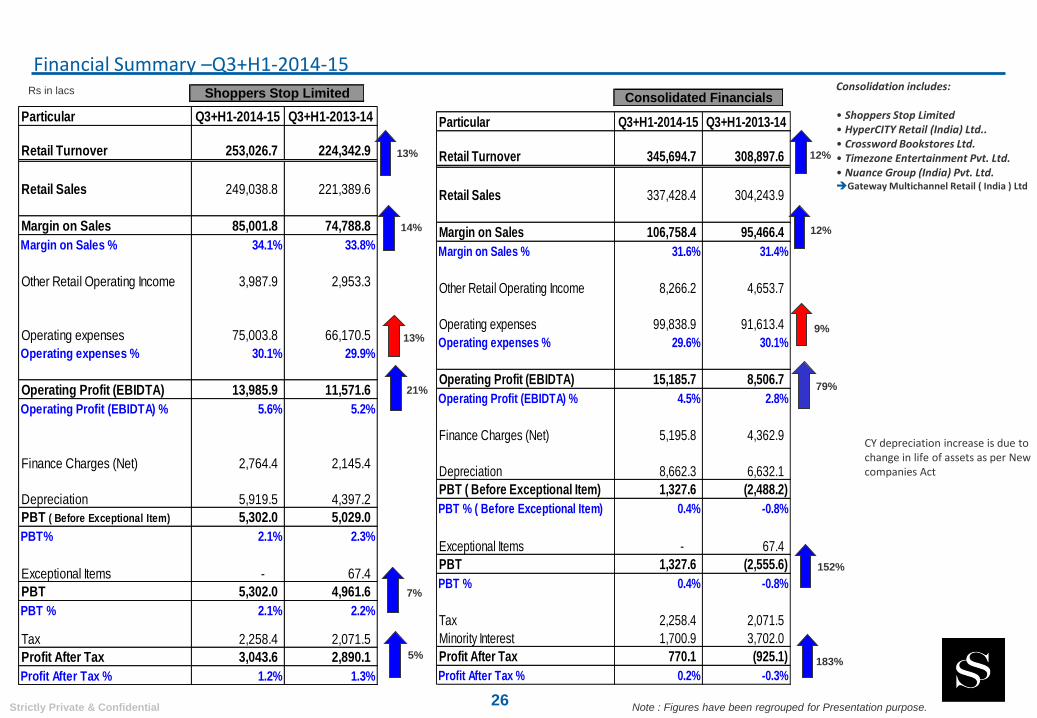

Financial Summary –Q3+H1-2014-15Rs in lacs Consolidation includes:

• Shoppers Stop Limited• HyperCITY Retail (India) Ltd..• Crossword Bookstores Ltd.• Timezone Entertainment Pvt. Ltd.• Nuance Group (India) Pvt. Ltd.Gateway Multichannel Retail ( India ) Ltd

Note : Figures have been regrouped for Presentation purpose.

CY depreciation increase is due to change in life of assets as per New companies Act

Shoppers Stop Limited Consolidated Financials

Particular Q3+H1-2014-15 Q3+H1-2013-14

Retail Turnover 253,026.7 224,342.9

Retail Sales 249,038.8 221,389.6

Margin on Sales 85,001.8 74,788.8

Margin on Sales % 34.1% 33.8%

Other Retail Operating Income 3,987.9 2,953.3

Operating expenses 75,003.8 66,170.5

Operating expenses % 30.1% 29.9%

Operating Profit (EBIDTA) 13,985.9 11,571.6

Operating Profit (EBIDTA) % 5.6% 5.2%

Finance Charges (Net) 2,764.4 2,145.4

Depreciation 5,919.5 4,397.2

PBT ( Before Exceptional Item) 5,302.0 5,029.0

PBT% 2.1% 2.3%

Exceptional Items - 67.4

PBT 5,302.0 4,961.6

PBT % 2.1% 2.2%

Tax 2,258.4 2,071.5

Profit After Tax 3,043.6 2,890.1

Profit After Tax % 1.2% 1.3%

13%

14%

7%

5%

13%

21%

Particular Q3+H1-2014-15 Q3+H1-2013-14

Retail Turnover 345,694.7 308,897.6

Retail Sales 337,428.4 304,243.9

Margin on Sales 106,758.4 95,466.4

Margin on Sales % 31.6% 31.4%

Other Retail Operating Income 8,266.2 4,653.7

Operating expenses 99,838.9 91,613.4

Operating expenses % 29.6% 30.1%

Operating Profit (EBIDTA) 15,185.7 8,506.7

Operating Profit (EBIDTA) % 4.5% 2.8%

Finance Charges (Net) 5,195.8 4,362.9

Depreciation 8,662.3 6,632.1

PBT ( Before Exceptional Item) 1,327.6 (2,488.2)

PBT % ( Before Exceptional Item) 0.4% -0.8%

Exceptional Items - 67.4

PBT 1,327.6 (2,555.6)

PBT % 0.4% -0.8%

Tax 2,258.4 2,071.5

Minority Interest 1,700.9 3,702.0

Profit After Tax 770.1 (925.1)

Profit After Tax % 0.2% -0.3%

12%

79%

12%

9%

183%

152%

Strictly Private & Confidential27

Shoppers Stop Ltd – Balance Sheet

27

Rs.in lacs

Note : Figures have been regrouped for Presentation purpose.

Unaudited Audited

Dec'14 March'14

EQUITY AND LIABILITIES

SHAREHOLDERS' FUNDS

Share capital 4,166.8 4,160.8

Reserves and surplus 72,002.8 68,706.5

Net Worth 76,169.6 72,867.3

NON CURRENT LIABILITIES

Long-term borrowings 23,964.3 19,983.3

Long-term provisions 893.4 996.2

Total Non Current Liabilites 24,857.7 20,979.5

CURRENT LIABILITIES

Short-term borrowings 15,831.2 17,480.7

Trade payables 40,159.9 30,969.5

Other current liabilities 21,118.9 22,521.3

Short-term provisions 417.7 1,066.2

Total Current Liabilites 77,527.7 72,037.8

Total 178,555.0 165,884.5

ASSETS

NON CURRENT ASSETS

Total Fixed assets 62,298.7 58,090.0

Non current investments 40,649.5 38,759.9

Long term loans and advances 28,510.3 30,119.4

Total Non Current Assets 131,458.4 126,969.2

CURRENT ASSETS

Inventories 33,885.9 29,553.6

Trade Receivables 4,210.5 2,600.3

Cash and cash equivalents 1,311.5 873.4

Short term Loans and advances 5,574.7 4,397.5

Other current assets 2,114.0 1,490.5

Total Current Assets 47,096.7 38,915.3

Total 178,555.1 165,884.5

PARTICULARS Particulars Q3+H1-14-15 Q3+H1-13-14

Debt Equity 0.58 0.53

Asset Turnover Ratio (Without Invt. In Group Co.) 3.56 3.54

Current Ratio 0.88 0.85

SSL Debt : 448 CrHypercity Debt : 225 Cr

Strictly Private & Confidential

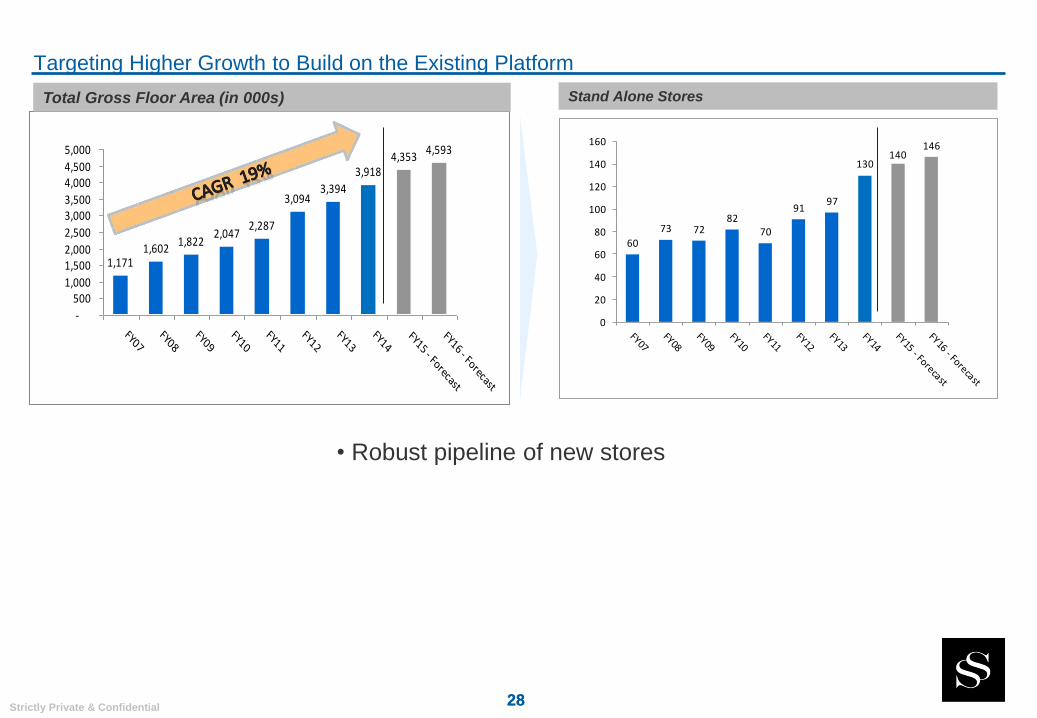

60

73 7282

70

9197

130140

146

0

20

40

60

80

100

120

140

160

1,1711,602

1,8222,047

2,287

3,0943,394

3,9184,353

4,593

-

5001,000

1,5002,000

2,500

3,0003,500

4,0004,500

5,000

FY07FY08

FY09FY10

FY11FY12

FY13FY14

FY15 - Forecast

FY16 - Forecast

28

Targeting Higher Growth to Build on the Existing Platform

28

Total Gross Floor Area (in 000s) Stand Alone Stores

• Robust pipeline of new stores

Strictly Private & Confidential29

Strictly Private & Confidential

Proof of Concept Established, Business Model Refined & Roll Out Planned for Expansion

Focused store rollout strategy

• Total Retail space 1.2 Mn sqft. with 15 stores operation in 9 cities.

1 1 37 9 12 12 15 16

20

0

10

20

30

2007 2008 2009 2010 2011 2012 2013 2014 2015E 2016E

No of stores

Proof of concept

established

Two Consecutive Quarters Company EBIDTA Breakeven Achieved in FY15

Business Model &

Strategy refined

• Cluster based growth strategy, with Core, Mid sized and Compact stores

– Existing stores after right sizing to be of 75-100 K sq ft.

– New stores of 50-60 K sq ft to drive assortment, differentiation and profitability.

– New compact size format of 25-30 K sq ft for penetration & leveraging resources.

30

Strictly Private & Confidential

Pan India Presence with Dominance in the Large Cities

• 15 stores in 9 cities with 1.2 million sq ft of space.

• Plans to expand retail outlets based on cluster

approach.

• Average footfalls per month: 1.7 Mn, indicating

strong customer pull.

Jaipur

Mumbai (4)

Hyderabad (2)

Bangalore (3)

Pune

Ahmedabad

Amritsar

Hypercity

Bhopal

DC Location

Note : Above figures as of 31st Dec 2014

City HYP Stores

Mumbai 4

Pune 1

Ahmedabad 1

Bangalore 3

Hyderabad 2

Amritsar 1

Jaipur 1

Bhopal 1

Baroda 1

Total 15

Baroda

31

Strictly Private & Confidential

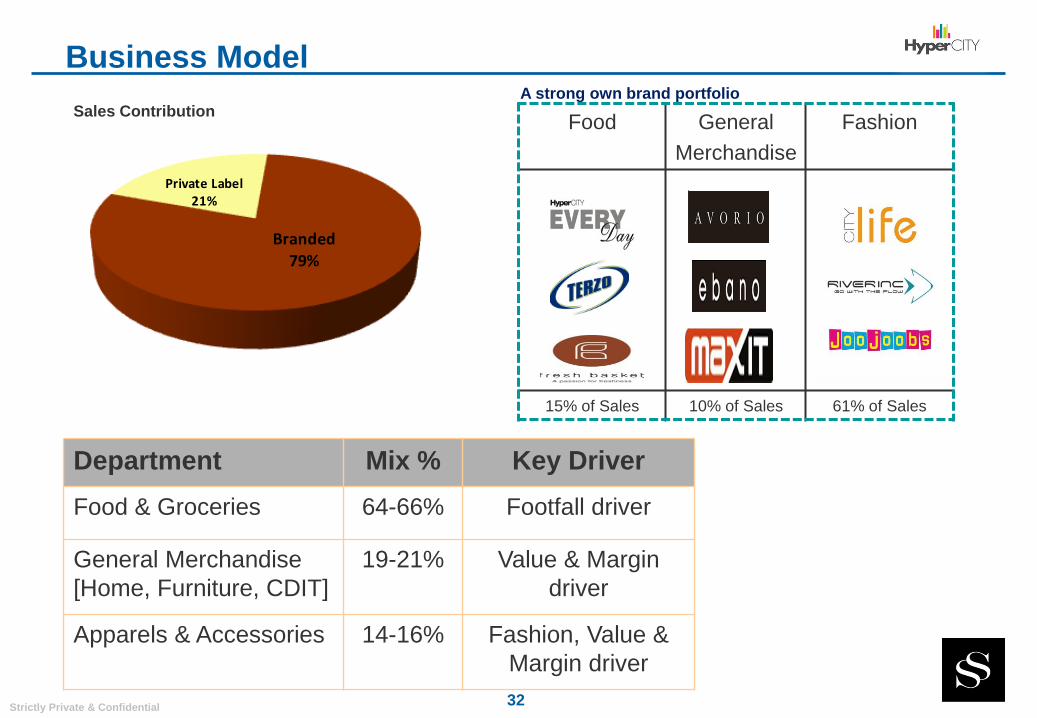

Branded 79%

Private Label 21%

Business Model

Department Mix % Key Driver

Food & Groceries 64-66% Footfall driver

General Merchandise

[Home, Furniture, CDIT]

19-21% Value & Margin

driver

Apparels & Accessories 14-16% Fashion, Value &

Margin driver

A strong own brand portfolio

Food General

Merchandise

Fashion

15% of Sales 10% of Sales 61% of Sales

Sales Contribution

32

Strictly Private & Confidential

Positioning & Product Strategy

Target customers: 21-45 years with

Income - 20,000+

► Discerning, Urban, Upscale with

High Disposable Income

Other In-store attractions – Café,

Laundry, Wine, Saloon, SPA

Widest product range on offer in a

hypermarket in India, 50K SKUs

Awarded the “100 Must Visit Retail

Destinations for year 2007-08

around the world”

International Award for “ Corporate

Achievement to Recognize Quality

& Excellence”– April 2010.

“India’s Most Admired

Hypermarket” at Images Retail

Awards 2012.

Positioning

Product Offering

FOOD

Grocery

Readyfood

InstantFood

Non -FOOD

Homecare

Personal

Perishable

Fruits & Vegetables

Just-in Non-

Veg Section

Milk Products

Freshly

Baked

Integrated CDIT

SmallApplicances

Personalcare

Home

Home Ware

Home Decor

Home Needs

Furniture

Dining

Bedroom

Living Room

Kitchens

Sports

Health & Fitness

Inddor Games

Outdoor Games

Cycles

Toys

Infants

Soft Toys

Action

Figures

Learning

Electronics

Ride Ons

Fashion

Clothing

Footwear

Accesories

Jewellery

33

Strictly Private & Confidential

Back End Operations

Majority of product written

off on completion of 12

months

Quarterly count cycle ,

enabling reliable inventory

and Shrinkage monitoring

Supply Chain and

Systems

Back end operations and

IT

Best Practices and

Policy

Operates multi channel

supply chain for various

product categories

Imports account for 8% of

General Merchandise

All DC operations on Scanner

based picking

Furniture and CDIT products

are home delivered

Reliable Inventory –

Merchandize Management

System

Dynamic Auto-replenishment

system, enabling consistent

high availability of stocks

E-Payment for 99%

transactions

34

Strictly Private & Confidential

Footfalls, ASP , Conversion and Average Ticket size

Footfalls (In Lacs)

Average Selling Price (Rs)Average Transaction size (Rs)

Conversion rate (%)

Hypercity Sales Growth YTD-2014-15:-Sales Growth - 7% LTL Sales Growth - (1%) (Ex- CDIT : 3%)LTL Sales Per Sq.ft. growth - 13%

Hypercity Sales P. Sq.ft. on Chargeable Area YTD-2014-15:Sales per sq.ft. in Rs. 5,770LTL Sales per Sq. ft. in Rs* 6,223

• * LTL sales psf is after excluding major concessionaire/ sub-lease area of 71k sq ft (LY: 4k sq ft).

154.81 152.58

70.00

85.00

100.00

115.00

130.00

145.00

YTD FY14 YTD FY15

82 87

10

30

50

70

90

YTD FY14 YTD FY15

42.3%44.9%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

YTD FY14 YTD FY15

1,085 1,106

700

800

900

1,000

1,100

YTD FY14 YTD FY15

35

Strictly Private & Confidential

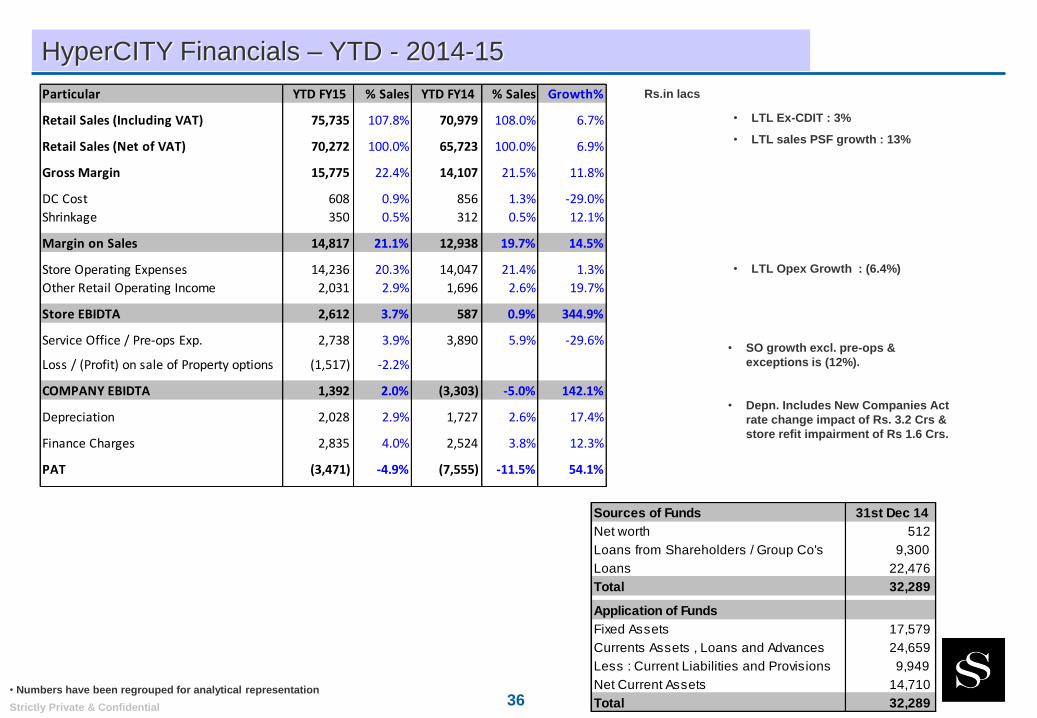

HyperCITY Financials – YTD - 2014-15

Rs.in lacs

• Numbers have been regrouped for analytical representation

Particular YTD FY15 % Sales YTD FY14 % Sales Growth%

Retail Sales (Including VAT) 75,735 107.8% 70,979 108.0% 6.7%

Retail Sales (Net of VAT) 70,272 100.0% 65,723 100.0% 6.9%

Gross Margin 15,775 22.4% 14,107 21.5% 11.8%

DC Cost 608 0.9% 856 1.3% -29.0%

Shrinkage 350 0.5% 312 0.5% 12.1%

Margin on Sales 14,817 21.1% 12,938 19.7% 14.5%

Store Operating Expenses 14,236 20.3% 14,047 21.4% 1.3%

Other Retail Operating Income 2,031 2.9% 1,696 2.6% 19.7%

Store EBIDTA 2,612 3.7% 587 0.9% 344.9%

Service Office / Pre-ops Exp. 2,738 3.9% 3,890 5.9% -29.6%

Loss / (Profit) on sale of Property options (1,517) -2.2%

COMPANY EBIDTA 1,392 2.0% (3,303) -5.0% 142.1%

Depreciation 2,028 2.9% 1,727 2.6% 17.4%

Finance Charges 2,835 4.0% 2,524 3.8% 12.3%

PAT (3,471) -4.9% (7,555) -11.5% 54.1%

Sources of Funds 31st Dec 14

Net worth 512

Loans from Shareholders / Group Co's 9,300

Loans 22,476

Total 32,289

Application of Funds

Fixed Assets 17,579

Currents Assets , Loans and Advances 24,659

Less : Current Liabilities and Provisions 9,949

Net Current Assets 14,710

Total 32,289

• LTL Ex-CDIT : 3%

• LTL sales PSF growth : 13%

• LTL Opex Growth : (6.4%)

• SO growth excl. pre-ops &

exceptions is (12%).

• Depn. Includes New Companies Act

rate change impact of Rs. 3.2 Crs &

store refit impairment of Rs 1.6 Crs.

36

Strictly Private & Confidential37

Our Stores

3737

Strictly Private & Confidential38

SS Department Stores

38

Strictly Private & Confidential39

SS Department Stores

Strictly Private & Confidential40

Home Stop

Strictly Private & Confidential41

Crossword Book Stores

41

Strictly Private & Confidential42

Mother Care

Strictly Private & Confidential43

MAC

43

Strictly Private & Confidential44

ESTEE LAUDER

Strictly Private & Confidential45

CLINIQUE

45

Strictly Private & Confidential46

HyperCITY Stores

46

Strictly Private & Confidential47

New HyperCITY Compact Store – at Whitefield Bengaluru

47

Strictly Private & Confidential48

New HyperCITY Compact Store – at Whitefield Bengaluru

48

Strictly Private & Confidential

T H A N K Y O U

DISCLAIMER : Certain statements in this release concerning our future growth prospects are forward-looking statements within the meaning of

applicable securities laws and regulations , and which involve a number of risks and uncertainties, beyond the control of the Company, that could

cause actual results to differ materially from those in such forward-looking statements. The risks and uncertainties relating to these statements

include, but are not limited to, risks and uncertainties regarding fluctuations in earnings, our ability to manage growth, intense competition including

those factors which may affect our cost advantage, wage increases, our ability to attract and retain highly skilled professionals, political instability,

legal restrictions on raising capital or acquiring companies outside India, and unauthorized use of our intellectual property and general economic

conditions affecting our industry. Shopper’s Stop Ltd. may, from time to time, make additional written and oral forward looking statements, including

our reports to shareholders. The Company does not undertake to update any forward-looking statement that may be made from time to time by or on

behalf of the company. The Company also expects the media to have access to all or parts of this release and the management’s commentaries and

opinions thereon, based on which the media may wish to comment and/or report on the same. Such comments and/or reporting maybe made only

after taking due clearance and approval from the Company’s authorized personnel. The Company does not take any responsibility for any

interpretations/ views/commentaries/reports which may be published or expressed by any media agency, without the prior authorization of the

Company’s authorized personnel.

49