Corporate Social Responsibility and Internal Control Effectiveness * Young Sang Kim ** Northern Kentucky University Yura Kim University of Seoul Hyun-Dong Kim Korea Advanced Institute of Science and Technology (KAIST) Keywords: corporate social responsibility; internal control effectiveness; material weakness; financial reporting quality JEL: G34; M14 * This work was supported by the 2015 Research Fund of the University of Seoul. ** Corresponding author: Young Sang Kim, Professor of Finance, Department of Economics and Finance, Haile/US Bank College of Business, Northern Kentucky University, Highland Heights, KY 41099, Email: [email protected], Tel: 1-859-572-5160, Fax: 1-859-572-6177.

Transcript

Corporate Social Responsibility and Internal Control Effectiveness*

Young Sang Kim**

Northern Kentucky University

Yura Kim University of Seoul

Hyun-Dong Kim

Korea Advanced Institute of Science and Technology (KAIST)

Keywords: corporate social responsibility; internal control effectiveness; material

weakness; financial reporting quality

JEL: G34; M14

* This work was supported by the 2015 Research Fund of the University of Seoul.

** Corresponding author: Young Sang Kim, Professor of Finance, Department of Economics

and Finance, Haile/US Bank College of Business, Northern Kentucky University, Highland

Heights, KY 41099, Email: [email protected], Tel: 1-859-572-5160, Fax: 1-859-572-6177.

Corporate Social Responsibility and Internal Control Effectiveness

Abstract

This study empirically examines whether corporate social responsible firms exhibit more

effective internal control over financial reporting. Specifically, we investigate whether ethical

and socially responsible firms apply business practices to ensure financial transparency and

accountability for their stakeholders. Using various measures of corporate social responsibility

(CSR) and a battery of robust regression analysis over the period from 2004 to 2012, we find

that CSR firms are more likely to have effective internal control and less likely to have material

weakness under Section 404 of the Sarbanes-Oxley Act (SOX). Our results are robust to the

propensity matching of firm characteristics, considering various measures of CSR, and

adjusting for several endogenous problems.

Keywords: corporate social responsibility; internal control effectiveness; material

weakness; financial reporting quality

JEL: G34; M14

1

1. Introduction

Corporate social responsibility (CSR) has become a new area of concern for the

wellbeing of society. Various stakeholders beyond shareholders and investors are increasingly

demanding that firms be responsible and accountable for their impact on society and the

environment as a whole. Investors consider the ethical conducts of the firms when they make

investment decisions2, while customers consider environmental and corporate social impacts

in their purchasing decisions. As stakeholders are becoming increasingly aware of CSR as

members of civil society, corporations are not only promoting the business accountability of

the entity itself, but are also ensuring that their business partners in the supply chain are

operating business in a socially responsible manner. In response to this increasing demand in

the society, corporate social responsibility or corporate sustainability are becoming very

important parts of the business agenda and are considered prominent features of business and

society.3

From an organizational perspective, CSR refers to business stewardship that benefits

the environment, society, and economy. To be socially responsible and sustainable, firms are

under increased pressure to maintain a high level of ethical standards and transparency in every

business practice (Jones, 1995; Mackey, Mackey, and Barney, 2007; Jo and Harjoto, 2011; Kim,

Park, and Wier, 2012). The key objective of CSR from a financial reporting point of view is to

2 In the 2015 Good Must Grow survey, 65% of consumers said that they would consider purchasing from socially

conscious firms, up from 60% in 2013. 3 For instance, according to “2012 Corporate/ESG/Sustainability/Responsibility Reporting: Does It Matter?,” an

analysis released by the Governance and Accountability Institute, 57% of S&P 500 index companies issued

corporate sustainability or responsibility reports, up from 20% the previous year. The percentage of S&P 500

index companies that report on sustainability or responsibility also increased, going from 72% to 75% and then

to 81% in 2013, 2014, and 2015 respectively (www.ga-institute.com).

2

ensure that the firm’s control environment is compliant, effective, efficient, and sustainable,

and that its financial information is accurate and transparent.

As firms face increased pressure to act in socially responsible ways, they are also under

great public scrutiny to provide accurate and timely financial reporting. Sarbanes Oxley Act

(SOX, hereafter), signed into law on July 30, 2002, was designed to enhance financial reporting

quality so that potential stakeholders can stay fully apprised of the firm’s financial situation.

Under Section 404 of the SOX, companies are mandated to publish any “material” information

concerning the scope and adequacy of the structure and procedures of their internal control

over financial reporting. The Exchange Act, Rules 13a-15(f) and 15d-15(f) define internal

control over financial reporting as a “process designed by, or under the supervision of, the

issuer’s principal executive and principal financial officers, or persons performing similar

functions, and effected by the issuer’s board of directors, management and other personnel, to

provide reasonable assurance regarding the reliability of financial reporting and the preparation

of financial statements for external purposes in accordance with generally accepted accounting

principles and includes those policies and procedures.”

In this paper, we study whether CSR firms apply business practices to ensure financial

transparency and accountability in order to satisfy their stakeholders. Specifically, we examine

whether CSR firms exhibit effective internal control over financial reporting as measured by

material weakness disclosure over financial reporting under SOX Section 404.4 The evidence

4 Material weakness is defined as a deficiency, or combination of deficiencies, in internal control over financial

reporting, such that there is a reasonable possibility that a material misstatement of the company’s annual or

interim financial statements will not be prevented or detected in a timely way (Public Company Accounting

Oversight Board (PCAOB) Auditing Standard No. 2, 2004). The PCAOB Auditing Standard No. 5 replaces the

term “more than remote likelihood” with “reasonable possible” when defining internal control material weakness.

3

concerning CSR motivation and impacts on firm performance and/or policy implications is far

from clear conclusion and the link between CSR and internal control over financial reporting

has not yet been examined extensively in the literature. Prior research reports on the ethical

aspect of CSR activities. For example, Kim et al. (2012) claim that socially responsible firms

constrain both accruals and real earnings management and thus deliver more transparent and

reliable financial information to their stakeholders. Their research is based on a theoretical

foundation posting that moral firms operate based on trust and cooperation with their

stakeholders, which prevents opportunism (Jones, 1995). Stakeholder theory suggests that

entities should be accountable to all of their stakeholders who can affect, or be affected by the

achievement of the objectives of the entities (Freeman, 1984). Using a sample of Spanish firms,

Gras-Gil, Manzano, and Fernandez (2016) report that more socially committed firms engage

in less earnings management, improving financial reporting quality. Overall, socially

responsible firms are not inclined to pursue short-term gain, but set the right corporate culture

and develop long term corporate-stakeholder relationships.

The contrary evidence finds that firms may be motivated to engage in CSR for

opportunistic reasons. The firm may use CSR as a medium with which to signal the market that

it is a good corporation (Mahoney, 2012). Entrenched managers may conduct in CSR practices

to burnish their reputation, in turn causing agency conflicts between the managers and

shareholders (Jensen and Meckling, 1976; Barnea and Rubin, 2005). Some firms engage in

CSR activities irresponsibly, and thus bring negative consequences to the stakeholders

including shareholders, employees, customers, and suppliers. For example, firms that engage

in excessive CSR spending are more likely to avoid taxes measured in terms of the likelihood

of engaging in tax sheltering and the extent of book-tax differences (Hoi, Wu, and Hao, 2013).

4

To examine the impact of CSR on internal control over financial reporting effectiveness,

we utilize a firm’s corporate social ratings provided by MSCI ESG STATS (previously known

as “KLD”) to measure firms’ CSR activities and extract internal control effectiveness measures

from the Audit Analytics database. Our measure of internal control effectiveness over financial

reporting is material weakness disclosure under Section 404 of the SOX. As external auditors

influence the likelihood of internal control deficiencies (e.g., Zhang, Zhou, and Zhou, 2007),

we include external auditor-related variables. Using a large sample of U.S. firms over the period

of 2004-2012, we find that CSR firms are more likely to have effective internal control over

financial reporting. Specifically, CSR firms are less likely to have material weaknesses under

Section 404 of the SOX. Additionally, the likelihood of a multiple material weakness decreases

as firms are more active in their CSR.

The contributions of this article are twofold. First, to our knowledge, we are among the

first to document a robust negative relation between CSR and internal control weakness over

financial reporting. Our results show that higher CSR firms are less likely to report material

weakness, and exhibit more effective internal control over financial reporting. We employ

several measures of CSR and provide several robust tests including propensity matching and

two-stage regression with instrumental variables. Second, we shed light on how CSR extends

to corporate behavior and effective financial reporting. Although some studies explore the

association between CSR and earnings quality, their empirical results are inconsistent and do

not advance our understandings of internal control over financial reporting. In this paper, we

try to fill this gap between CSR and internal control effectiveness using a large sample of U.S.

firms and a battery of robust empirical tests.

5

The rest of the paper is organized as follows. Section two reviews the relevant literature

and builds the hypothesis. Section three describes the data collection and research model, and

the empirical findings of the study are then provided in section four. Finally, section five

concludes the paper.

2. Literature Review and Hypothesis Development

2.1. Literature review

Research on various aspects of CSR has received considerable attention in the literature

and the media over the decades. One strand of CSR research shows that a firm actively engages

in CSR activities by being ethical and transparent and therefore, brings a positive outcome to

the organization and stakeholders. Others argue that a firm’s engagement in CSR activities may

be for self-benefit purposes and CSR is a marketing strategy of “hypocritical window dressing”

(Forbes, 2011).

Proponents of CSR believe that it is a form of corporate culture related to ethical

conduct and “doing business right” and that firms engage in CSR activities to benefit society

at large. Kreps (1990) claims that corporate culture is a shared belief or principles among

members of the organization and that “designing and maintenance of the culture is crucial to

efficient organization.” A good design and maintenance of corporate culture foster beneficial

transactions in the future. Additional evidence show that socially responsible firms have been

shown to be less likely to engage in myopic earnings management (Kim et al., 2012; Gras-Gil

et al., 2016) and tax avoiding activities (Lanis and Richardson, 2015). Some prior works

examine the relation between CSR activities and future firm performance. Based on social

responsibility ratings provided by Fortune magazine’s annual survey of corporate reputations,

6

McGuire, Sundgren, and Schneeweis (1988) document that firms with high scores perform

better on stock-market based measures such as risk-adjusted return, alpha, and total return and

on accounting-based measures such as ROA, sales growth, asset growth, and operating income

growth. Likewise, Luo and Bhattacharya (2006) report that CSR activities increase market

value although the mediating effect of customer satisfaction. For a sample of Indian firms,

Mishra and Suar (2010) develop CSR score based on various CSR databases including KLD

database, GRI guidelines (Global Reporting Initiatives), and the SAI (Social Accountability

International). They find that CSR firms improve both their financial and non-financial

performance such as workplace relations and personnel development. Harjoto and Jo (2011)

find that firms with effective corporate governance engage in CSR activities to resolve conflicts

between managers and investing and non-investing stakeholders supporting their conflict-

resolution hypothesis of CSR engagement. Ultimately, a firm’s CSR engagement enhances

operational performance and increases firm value. Examining the relation between CSR and

insider trading, Gao, Lisic, and Zhang (2014) find empirical evidence that managers of “CSR-

conscious” firms are significantly less likely to be involved in insider trades than are those of

“non-CSR-conscious” firms. However, the finding that the managers of socially responsible

firms refrain from informed trading is stronger if the interests of the managers and of the firm

are more closely aligned.

Others argue that firms’ CSR is done for opportunistic reasons and that insiders such

as managers and large blockholders intend to build personal reputations as good corporate

citizens concerned for employees, society, and the environment, at the expense of other

stakeholders (Barnea and Rubin, 2005). They propose that the overinvestment problem can

occur and thus, that CSR initiatives hamper firm value and can be a source of conflicts among

7

different stakeholders. Supporting the view that excessive CSR spending can bring negative

consequences for a firm and its stakeholders, Hoi, et al. (2013) find that excessive and

irresponsible engagement of CSR activities can lead firms to be involved in unethical business

practices to avoid taxes. The empirical finding by Preuss (2010) that even firms headquartered

in tax havens or Offshore Finance Centres (OFCs) claim that they are social responsible firms

seem to suggest that some firms are strategic with CSR activities and that their commitment is

for window dressing. In addition, CSR activities impact the cost of equity financing. Firms

with high CSR ratings pay lower cost of equity financing (El Ghoul, Guedhami, Kwok, and

Mishra, 2011) and also pay significantly less for bank loans (Gross and Roberts, 2011). In a

theoretical paper, Mackey et al. (2007) prove that firms decide to make an investment in

socially responsible activities in order to maximize their market value. They argue that firms

are willing to move back and forth from socially responsible to traditional profit maximizing

firms in order to maximize profits. Thus, the firm’s choice to remain socially responsible or not

is dependent on the value maximization theory. Supporting this view, a number of studies find

that incumbent managers may strategically use CSR as an entrenchment mechanism while

colluding with social and environmental activist (Cespa and Cestone, 2007) or non-

shareholding stakeholders (Surroca and Tribo, 2008).

Another strand of the literature on internal control effectiveness is growing and has

become of much interest in social studies. As a result of corporate financial scandals such as

Enron and WorldCom, SOX was implemented on July 30, 2002 to ensure the quality of

financial reporting and safeguard stakeholders. In particular, SOX 404 became effective on

November 15, 2004. Under the Section 404 of the SOX, managers need to assess the

effectiveness of the internal control over financial reporting followed by external auditors’

8

attestation of that effectiveness. If any material weakness exists, auditors must issue an adverse

opinion on the effectiveness of internal control over financial reporting. (PCAOB Standard

No.2; Standard No. 5). In fact, Section 302 of the SOX became effective on August 29, 2002,

before SOX 404. Under Section 302, firms started to disclose information about their internal

controls on a quarterly basis. We focus on SOX 404 rather than SOX 302. While Section 302

as somewhat vague disclosure requirements concerning material weaknesses, Section 404

states clear rules for disclosure (Doyle, Ge, and McVay, 2007a). Moreover, Section requires

additional reports including the examination of independent auditors, making the examination

of a firm’s material weaknesses more careful and accurate (Rice and Weber, 2012).

Internal control research has examined what factors drive the effectiveness of internal

control. Various determinants of internal control effectiveness have been identified by a

growing body of recent literature. The earlier research confirms that internal control

effectiveness is closely related to various firm characteristics. Weak internal control firms are

smaller, have more operating segments, are more likely to have foreign currency transactions

and are less profitable (Bryan and Lilien, 2005; Ge and McVay, 2005; Doyle et al., 2007a).

Several studies also agree that firms with more effective corporate controls are less likely to

report internal control weaknesses. For example, independent audit committees, audit

committee with financial expertise, and a larger audit committees report fewer internal control

deficiencies (Ashbaugh-Skaife, Collins, and Kinney, 2007; Hoitash, Hoitash, and Bedard,

2009). Firms with more independent boards of directors are also less likely to disclose internal

control weakness (Li, Lim, and Wang, 2007). Furthermore, Rice and Weber (2012) investigate

various determinants of internal control reporting including both firm characteristics and

governance factors. They find that the possibility of disclosing existing material weaknesses is

9

negatively related to external capital needs, non-audit fees, and the size of the audit firm,

whereas it is positively related to financial distress, prior material weaknesses, auditor change,

and management replacement. Our paper complements this line of research by adding CSR as

a new determinant of a firm’s internal control effectiveness.

Corporate governance is very closely related to the effectiveness of internal control.

Li, Sun, and Ettredge (2010) argue that CFOs’ professional qualifications affects internal

control strength and that firms with CFOs possessing financial expertise and experience are

less likely to have material weaknesses. Similarly, Krishnan and Visvanathan (2007) show that

a smaller proportion of audit committee members with financial expertise is related to more

internal control deficiencies. Lin, Wang, Chiou, and Huang (2014) create a CEO entrenchment

measure based on the principal component analysis of several CEO characteristics such as CEO

compensation structure, and CEO duality and find that more entrenched CEOs are related to a

lower quality of internal control.

Ample research explores how internal control strength affects a firm’s conduct of

business. Material weaknesses are related to lower quality estimated accruals (Doyle, Ge, and

McVay, 2007b). Ineffective internal control has a negative impact on the accuracy of

management forecast reports since managers provide guidance based on erroneous internal

reports (Feng, Li, and McVay 2009). Furthermore, Donelson, Ege, and McInnis (2016)

document that those material weaknesses are positively associated with the future revelation of

fraud. Their research is related to our paper in that it provides evidence linking internal controls

and corporate ethical behavior. Prior studies also investigate how internal control effectiveness

affects audit-related factors. For example, firms with a material weakness are significantly

10

related to a higher audit fees (Raghunandan and Rama, 2006), and firms that pay high audit

fees tend to more frequently dismiss their auditors (Ettredge, Li, and Scholz, 2007).

2.2. Hypothesis development

Stakeholder theory argues that good firms maintain a positive relationship with their

stakeholders and involve in business practices to maximize long-term value (Donaldson and

Preston, 1995; Donaldson, 1999). The CSR process is related to the ethical and moral

dimensions of firm operations and is closely related to corporate culture of conducting business.

The concept of CSR extends beyond the traditional view posited by a Nobel prize-winning

economist, Milton Friedman that a firm uses its resources and engages in activities to increase

profits and also includes benefiting society. Based on stakeholder theory, socially responsible

firms aim to increase long-term profits, build stakeholder trust, and take responsibility for

society through transparent and ethical behaviors. Also managers engage in CSR in order to

resolve conflicts among stakeholders, with the ultimate aim of maximizing shareholders’

wealth (Jensen, 2001). Therefore, this view argues that CSR is adopted in order to promote

shareholders’ welfare. Both Kim et al. (2012) and Gras-Gil et al. (2016) report that more

socially committed firms constrain earnings management ensuring that their financial reporting

is accurate and transparent. In addition, Dhaliwal et al. (2012) find that CSR firms are

associated lower analyst forecast errors providing more value relevant information to investors.

Active engagement in CSR activities reduces financial risks to the firm (Ortizky and Benjamin,

2001) and creates shareholder value in acquisitions (Deng et al., 2013). If CSR firms operate

business at sustainable levels and seek to improve operating efficiency and the effectiveness of

11

their internal control structure, then the firms expect to report fewer material weaknesses in

internal control. Overall, the strand of literature suggests that CSR firms that are moral and

their corporate culture and governance play a role in setting the right course of action for the

business. We therefore propose the following hypothesis:

Stakeholder Hypothesis: A firm actively engaged in corporate social responsibility

(CSR) is positively associated with the effectiveness of internal control over financial

reporting pursuant to Section 404 of the SOX.

Alternatively, according to signaling theory, firms voluntarily disclose information to

the capital market to attract investors and gain a favorable reputation (Verrecchia, 1983).

Corporations may choose to engage in and disclose CSR activities to send a signal to the market

that they are better than others (Mahoney, 2012) and obtain support from and inhibit the

consumption by ethically responsible consumers and investors (Shea, 2010). Firms may use a

“halo effect” to improve brand strength and financial performance (The Economist, June 27,

2015). Individuals such as top managers and firms may choose to engage in CSR activities

opportunistically in the pursuit of self-interested profits. For examples, the top managers

involve in CSR activities to build personal reputations as good corporate citizens at the expense

of other stakeholders (Barnea and Rubin, 2005). Overall, firms’ CSR actions may be a strategic

choice and the costs of engagement can exceed benefits. If firms’ CSR activities are mere

“window-dressing” exercises for managing their presented image in the market at the cost of

some stakeholders of the firm, then CSR activities may have no or a negative relation to the

internal control structure. We thus propose the following hypothesis:

12

Signaling Hypothesis: A firm actively engaged in corporate social responsibility (CSR)

is negatively or insignificantly associated with the effectiveness of internal control over

financial reporting pursuant to Section 404 of the SOX.

3. Data and Research Design

3.1 Sample construction

Initially, we obtain our sample from Audit Analytics, which includes external auditor

information and internal control reports. We adopt SOX Section 404 Material Weakness to

measure the effectiveness of the internal control system. Section 404 has required accelerated

filers to report their material weakness since 2004. Non-accelerated filers have had to conform

to SOX Section 404 since 2008. A registrant must comply with all of the requirements to report

on internal control over financial reporting if it satisfies the definition of a “large accelerated

filer” or an “accelerated filer,” as defined in Exchange Act Rule 12b-2.

We utilize a firm’s corporate social ratings provided by MSCI ESG STATS (previously

known as KLD) to measure the firm’s CSR activities. Many practitioners and academics use

KLD data as a reliable measure of a firm’s CSR, and they are referenced in a number of articles

and papers. Sharfman (1996) provides a comprehensive review of the validity of KLD

measures. They evaluate firms’ CSR activities on seven dimensions - corporate governance,

community, diversity, employee relations, environment, human rights, product, and other

exclusionary screen categories (e.g., alcohol, gambling, tobacco and military) using financial

statements, media coverage, government documents, and peer-reviewed articles. For each firm,

the KLD evaluates strengths (positive indicators) and concerns (negative indicators) in seven

non-exclusionary dimensions and records only the concerns in exclusionary dimensions. For

each strength activities, KLD assigns a score if a firm acts socially responsibly. The firm

13

receives one point if it is involved in an activity of social concern. The composite KLD score

is measured by calculating the differences between the strengths and the concerns in each

dimension. However, raw CSR scores may create problems since the number and composition

of CSR strengths and concerns vary over time. To address this problem, we compute an

adjusted CSR score which divides the strengths and concerns of each dimension by its relative

number of strength and concern indications (Deng, Kang, and Low, 2013). In this paper, we

use both raw and adjusted KLD scores as the main independent variables in the analyses.

We obtain financial accounting data from the Compustat database and consider only

firm-year observations with available financial variables in Compustat, audit information from

Audit Analytics, and CSR measures from MSCI ESG STATS (KLD) database. Due to the

different regulations and reporting standards involved, we exclude financial institutions (SIC

code from 6000 to 6999) and regulated firms (SIC code from 4900 to 4949) from our sample.

The sample selection procedure yields a final sample of 15,961 firm-year observations from

3,070 unique firms covering 2004 to 2012.

3.2 Research model

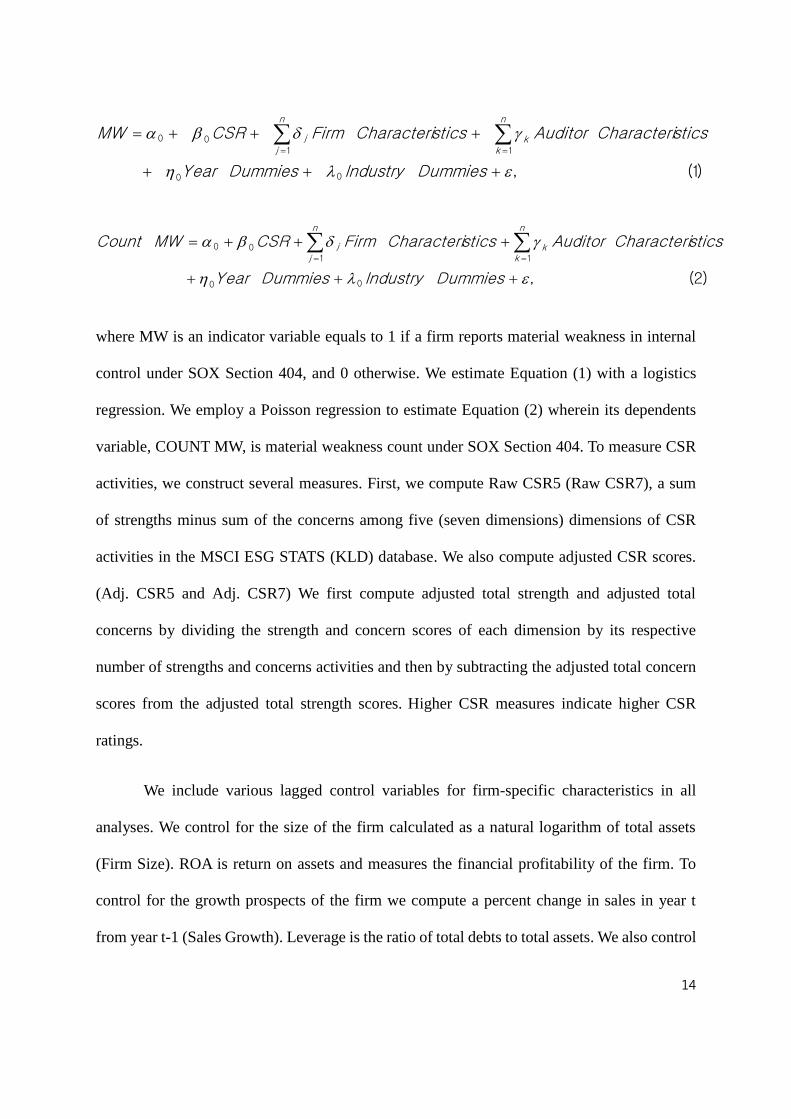

To examine the relation between CSR and thes effectiveness of a firm’s internal control

over financial reporting pursuant to Section 404 of SOX, we regress the effectiveness of

internal control measured by a dummy variable of material weakness disclosure (MW) as well

as the number of material weakness count (Count MW) on several CSR proxies along with

firm characteristics and external auditor characteristics as follows:

This table reports the Pearson correlation coefficients among variables for the sample. All variable definitions are defined in Appendix A. *, **, *** indicate statistical

significance at the 10%, 5%, and 1% levels, respectively.