ROYAL BANK of CANADA corporate structure personal & commercial banking ➤ personal financial services ➤ card services ➤ business banking ➤ insurance 10 million customers functions committees geographies businesses * wealth management ➤ royal trust ➤ royal mutual funds ➤ rbc ds – private client division ➤ royal bank action direct discount brokerage corporate & investment banking ➤ corporate banking ➤ financial institutions & trade ➤ rbc ds – institutional division atlantic quebec metro toronto ontario manitoba saskatchewan alberta & nwt b.c. & yukon u.s.a. bahamas & cayman barbados & caribbean latin america europe asia corporate affairs corporate secretary corporate treasury finance human resources internal audit law ombudsman operations & service delivery real estate risk management strategic development strategic investments systems & technology group risk wealth management business services technology policy corporate & investment banking asia advisory strategic investments personal & commercial markets organized climb group council ➤ comprises group office members and the heads of each of the businesses and major geographic and functional units. ➤ meets to review the group’s performance versus plan,to communicate group-wide issues and to deal with cross-functional matters. ➤ seven-member team led by the chief executive officer and including five vice-chairmen and the chief financial officer. ➤ responsible for the group’s overall strategic direction,competitive position,market performance, human resource planning, external relations and risk profile. ➤ provides strategic direction to operating units. ➤ meets weekly. * Each business segment (e.g. personal & commercial banking) is supported by an operating committee, with a representative from each business, charged with taking a broad view of the entire customer market and developing integrated customer strategies, marketing, sales and operations. Each business unit (e.g. personal financial services) is responsible and accountable for competitive performance and operational excellence in the market it serves. group office 58,000 employees for the committed to delivering value to shareholders and customers

Transcript

R O Y A L B A N K o f C A N A D A

corporate structure

personal & commercial banking

➤ personal financial services

➤ card services➤ business

banking➤ insurance

10 million customers

functions committeesgeographiesbusinesses*

wealthmanagement

➤ royal trust➤ royal mutual funds➤ rbc ds – private

business servicestechnology policycorporate &investment banking

asia advisorystrategic investments

personal &commercialmarkets

organized

climb

group council➤ comprises group office members and the heads of each of the businesses and major geographic and functional units.➤ meets to review the group’s performance versus plan, to communicate group-wide issues and to deal with

cross-functional matters.

➤ seven-member team led by the chief executive officer and including five vice-chairmenand the chief financial officer.

➤ responsible for the group’s overall strategic direction, competitive position, marketperformance, human resource planning, external relations and risk profile.

➤ provides strategic direction to operating units.➤ meets weekly.

* Each business segment (e.g. personal & commercial banking) is supported by an operating committee, with a representative from each business, charged withtaking a broad view of the entire customer market and developing integrated customer strategies, marketing, sales and operations. Each business unit (e.g. personalfinancial services) is responsible and accountable for competitive performance and operational excellence in the market it serves.

group office

58,000 employees

for the

committed to deliveringvalue to shareholders and customers

R O Y A L B A N K o f C A N A D A

our businesses

results by business segment

We present below the results for 1997 for our major

business segments. Page 20 shows the businesses

that fall under each of these segments.

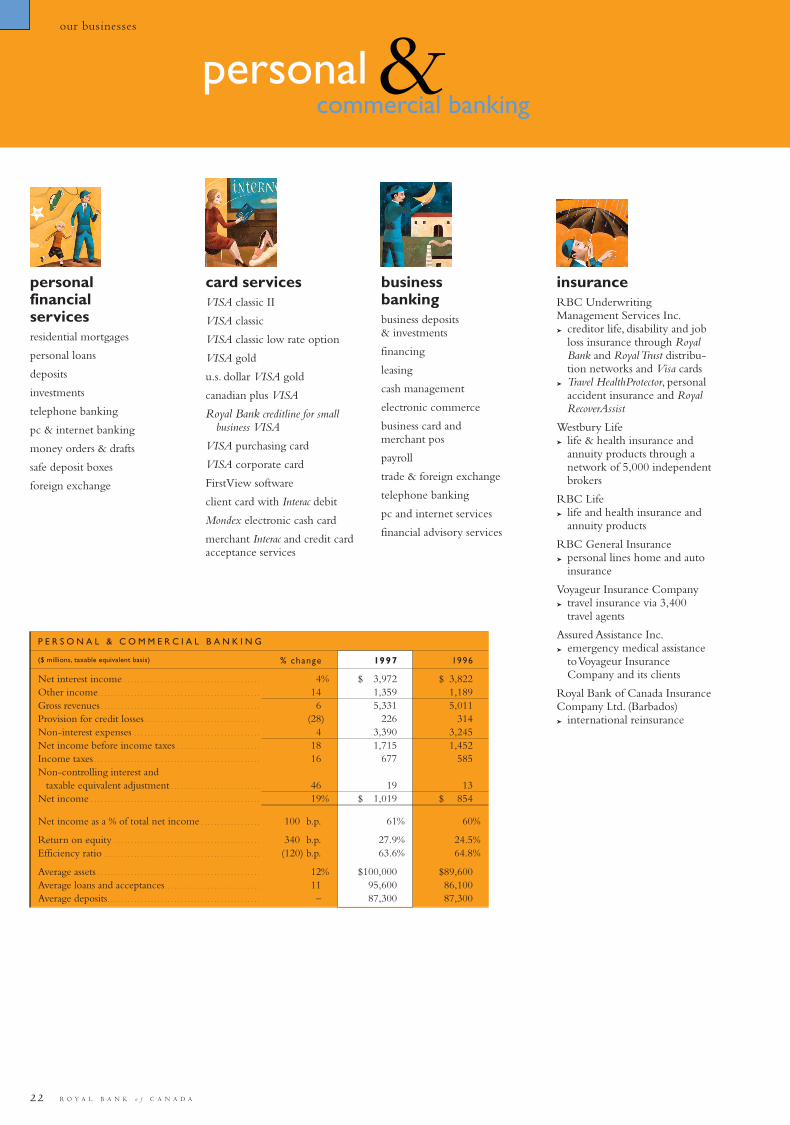

personal and commercial banking had a return onequity of 27.9% and accounted for 61% of Royal Bank’s netincome in 1997. A quarter of the revenues were derived fromother income.The efficiency ratio of 63.6% was better than theconsolidated ratio for the group.The segment’s objective is tofurther improve this ratio by growing revenues faster thanexpenses.

corporate and investment banking accounted for20% of total net income and had a return on equity of 18.7%.Sixty percent of total revenues stemmed from other income.The efficiency ratio was 57.2%. Improving return on equity andoverall efficiency continue to be a focus of this segment.

wealth management accounted for 14% of the bank’s net income. It recordeda 49.7% return on equity, reflecting the strong returns of the businesses in this segmentand the relatively low capital underpinning required for these largely off-balance sheetbusinesses. Over 80% of revenues were derived from fee income.The efficiency ratioof 77.9% reflected the types of businesses in this segment.

otherThis segment consists largely of thediscontinued LDC business, real estateoperations, corporate treasury (whichmanages the bank’s market risk position)and the systems and operations groups.The segment accounted for 5% of totalearnings, reflecting largely the returns ofthe LDC portfolio and the corporatetreasury group.

R E S U L T S B Y B U S I N E S S S E G M E N T

F O R T H E Y E A R E N D E D O C T O B E R 3 1 , 1 9 9 7 P E R S O N A L C O R P O R A T E &( $ M I L L I O N S , T A X A B L E E Q U I V A L E N T B A S I S ) & C O M M E R C I A L W E A L T H I N V E S T M E N T

B A N K I N G M A N A G E M E N T B A N K I N G O T H E R ( 1 ) T O T A L

(1) The Other segment is comprised mainly of LDC assets, real estate operations, corporate treasury, systems & technology and operatio ns & service delivery.

personal financial servicesresidential mortgages

personal loans

deposits

investments

telephone banking

pc & internet banking

money orders & drafts

safe deposit boxes

foreign exchange

card servicesVISA classic II

VISA classic

VISA classic low rate option

VISA gold

u.s. dollar VISA gold

canadian plus VISA

Royal Bank creditline for small business VISA

VISA purchasing card

VISA corporate card

FirstView software

client card with Interac debit

Mondex electronic cash card

merchant Interac and credit cardacceptance services

business bankingbusiness deposits & investments

financing

leasing

cash management

electronic commerce

business card and merchant pos

payroll

trade & foreign exchange

telephone banking

pc and internet services

financial advisory services

insuranceRBC UnderwritingManagement Services Inc.➤ creditor life, disability and job

loss insurance through RoyalBank and Royal Trust distribu-tion networks and Visa cards

➤ Travel HealthProtector, personalaccident insurance and RoyalRecoverAssist

Westbury Life➤ life & health insurance and

annuity products through anetwork of 5,000 independentbrokers

RBC Life➤ life and health insurance and

annuity products

RBC General Insurance➤ personal lines home and auto

insurance

Voyageur Insurance Company➤ travel insurance via 3,400

travel agents

Assured Assistance Inc.➤ emergency medical assistance

to Voyageur InsuranceCompany and its clients

Royal Bank of Canada InsuranceCompany Ltd. (Barbados)➤ international reinsurance

R O Y A L B A N K o f C A N A D A

our businesses

P E R S O N A L & C O M M E R C I A L B A N K I N G

Innovation means presenting future ideas now. This year we introduced North America’s first, and Canada’s only, Interactive VoiceResponse Loan System, allowing more than 34,500 client and non-client applicants across the country to apply for credit by phone,all in the time it might take to order pizza. Raising sights almost always means raising standards.

1997 PerformancePersonal and commercial banking’s netincome was up 19% from last year andaccounted for 61% of the bank’s total netincome. Earnings reflected a $70 million(pre-tax) gain from the sale of the payrollbusiness and a $50 million addition tothe general provision, compared to a$100 million addition to the generalprovision in 1996.The segment’s ROEwas up 340 basis points from 1996 to27.9%.

Revenues were up 5% excluding thepayroll gain, reflecting increases in all thebusinesses, with particularly good growthin insurance and card revenues.

Specific provisions for credit losseswere $176 million, down 18% from lastyear.The general provision for creditlosses, as mentioned, was $50 millionversus $100 million in 1996.

As expected, the efficiency ratioimproved – by 120 basis points in total,and 40 basis points excluding thepayroll gain.

R O Y A L B A N K o f C A N A D A

personal and commercial banking

Objectives The segment’s objective is to strengthen RoyalBank’s leadership position in the Canadian personal andbusiness market, while selectively pursuing niche globalopportunities. We aim to do so by focusing on customersatisfaction, employee satisfaction, business performance(revenue growth, efficiency enhancement and portfolioquality) and corporate reputation and image, utilizing a balanced scorecard approach.

The segment intends to maximize synergies between thebusinesses to strengthen brand positioning, revenue growthand cost management.

Strategies To significantly increase revenues and marketshare position in the Canadian market, the segment will focuson sales effectiveness, by leveraging strengthened client seg-mentation and information management and by capitalizingon relationship marketing capabilities. It intends to alignchannels, products, services, and the sales force to differen-tiated customer segment needs. The segment also plans toenhance risk management processes through technology.

The strategy is to selectively pursue global market oppor-tunities, implementing a targeted niche segment strategy, withpriority on the U.S.A. and Caribbean markets. The segmentexpects to expand and diversify the distribution of insuranceproducts through acquisitions, strategic alliances, and third-party products to develop new revenue streams.

R O Y A L B A N K o f C A N A D A

our businesses

➤ The largest providerof residential mort-gages, personal loansand deposits to9 million Canadians.

➤ Financial servicesprovider in theCaribbean with over60 units.

➤ Canada’s largestprovider of VISAand debit cards (bynumber of cards),processing services,and merchantterminals deployed.

➤ Serves 5.6 millioncredit card and6 million debit cardcustomers.

➤ Provides merchantswith electronic pro-cessing of credit anddebit transactions.

➤ Founding member of Mondex interna-tional and world-wide leader in smartpayment cards.

➤ VISA Classic II, one of Canada’s fastestgrowing new cards, continued to expandwith over 7,000 retail locations providingcardholder discounts, and with cardholdersatisfaction rating of 97%.

➤ Royal Bank CreditLine for small businessTM

VISA, an industry first in providing a“hassle-free” scorecard-driven applicationprocess, met with exceptional marketacceptance.

➤ Debit cards led the market in Interacvolume and active cardholders; and recentmarket-leading enhancements of purchasesecurity and extended warranty furtherstrengthens our position.

➤ Proprietary Windows-based expensemanagement software, FirstView, continuedto lead in the North American market,which is reflected in strong market sharegains in corporate (travel & entertainment)and purchasing cards.

➤ Syndicated Angus Reid industry researchindicated market leadership in the cross-selling of the card base.

➤ Leveraged expanded database capabilitiesvia direct marketing and alternativedelivery channels/segments to aggressivelycapture new business.

➤ The adoption of Mondex by the 10 largestdeposit taking institutions in Canadareaffirmed Royal Bank’s 1995 decision tobring this technology to Canada.

➤ Successfully launched Mondex in Guelph,Ontario, with the support of consumersand 90% of the target merchant commu-nity. Plans are in place to introduce Mondex to two additional Canadiancommunities in 1998.

➤ Continued the leadership role in smartcarddevelopment by working with national andinternational firms to develop smartcardproducts for use worldwide.

➤ Continued advances in e-commercewith interactive Internet web sites, on-lineapplications, and Canada’s first SecureElectronic Transaction (SET).

➤ Received “Best New Solutions Award”at the Retail Strategies and SolutionsConference recognizing the “Debit at thepump” solution with Chevron Canada.

➤ A “First to Market” POS terminal wasdeveloped and launched for the OntarioMedical Association (OMA), combiningdebit and credit payments along withHealth Card validation.

where we stand operational reviewbusinesses

personal financial services

cardservices

➤ Improved customer and employee satisfac-tion levels by 2% and 10% respectively,partially through introduction of problemresolution program.

➤ Introduced advanced segmentation andpredictive modelling techniques to gainadditional insight into customer needs.

➤ Enhanced position in the residential mort-gage business by introducing financialadvice to segments such as first-time homebuyers, renovators and home sellers.

➤ Offered seven new, targeted GICs andreduced investment processing time by 60%.

➤ Launched innovative programs for stu-dents, recognizing the lifetime potential ofthis market.

➤ Launched third-party alliance products,reverse mortgages and life annuities, pro-viding choice to clients and incrementalrevenue streams to the bank.

➤ Freed-up staff time to provide financialadvice and solutions.

➤ Upgraded financial planning accreditationsto one-third of staff, while Royal LearningNetwork courses provided more cost-efficienttraining to employees at 500+ branches viamulti-media hardware and software.

➤ Introduced Royal Direct PC and Internetbanking featuring award-winning ManagingYour Money software. Royal Direct PC,Internet and telephone banking is theworld’s largest alternative delivery channelprovider.

➤ Grew the mobile sales force, which servesclients when and where they choose, to over 500.

➤ Provided market-first enhancements toselected banking machines such as cash-back deposits for lower service fees, U.S.$travellers cheques, statement updates andaudio banking for clients with disabilities.

➤ Provided clients in 44 shared locationbranches with integrated access toRoyal Bank, Royal Trust and RBCDominion Securities.

➤ Professionals’ Program in the Bahamascontinued to increase market-dominantposition with professional and studentsectors.

➤ Was the only international bank remainingto serve residents of volcano-devastatedMontserrat.

commercial bankingpersonal&

R O Y A L B A N K o f C A N A D A

personal and commercial banking

financial performance objectives and strategies

➤ Revenues were up 4%, with good growth inboth net interest income and other income.

➤ Residential mortgage and personal loanvolumes increased by 15% and 6%respectively.

➤ Market shares for residential mortgages andpersonal loans were up 90 basis points and130 basis points, respectively, while portfolioquality remained sound.

➤ Lower personal deposit volumes and marketshare reflected a shift to investment productsin the low interest rate environment.

➤ New personal loan pricing strategy resultedin incremental net interest income of$16 million.

➤ More than 77,000 clients were referredamong the companies of Royal Bank,resulting in $5.6 billion of business, includ-ing $2.3 billion from outside the bank and$2.7 billion in retained business.

➤ New sales processes and employee trainingat 250 priority market locations contributedto 15% revenue growth in these locations.

➤ Caribbean revenues increased 16%.

Objectives1. Grow revenues by 5% annually.2. Grow earnings by 10% annually.3. Improve efficiency.4. Maintain leading market shares.

Strategies➤ Focus on proactively providing customer

solutions one customer at a time. Build one-on-one relationships with our cus-tomers, leveraging the information ourcustomers have entrusted us with.

➤ Customize information, products and ser-vices to meet individual client needs withconsistent treatment at all points of contact.

➤ Reduce administration duties in branches bycentralizing functions to enable staff toprovide clients with more financial advice.

➤ Enhance sales automation in all branches by1999 to streamline processes and enablefinancial advice/solutions-based conversa-tions with our clients.

➤ Leverage the distribution network to deliver third-party products for new revenuestreams.

➤ Increase shared locations in Canada to 78 in1998, and continue to expand this inte-grated concept in the Caribbean.

➤ Selectively capitalize on global opportunities.➤ Broaden and deepen leadership talent base,

reflecting the diversity of our employeepopulation and our communities.

➤ New accounts increased 30%, indicatingfuture growth in spending and outstandingbalances.

➤ VISA cardholder spending volumes increased12% and VISA merchant spending volumeswent up 9%.

Objectives1. Grow revenues by 10% annually.2. Increase market share in credit cards by

1% annually to the year 2000.

Strategies➤ Leverage database and direct marketing

capabilities to aggressively capture new segments.

➤ Explore synergies with merchant andalliance partners to provide cost efficienciesand value-added information-based prod-ucts, potentially combining card functions ofdebit, e-cash and credit on a relationshipcard platform.

➤ Invest in technology to meet customers’evolving needs for customization, informa-tion, and the convenience of alternatedelivery channels.

(1) As a % of all financial institutions in Canada at August 31. Market shares exclude Royal Trust,Action Direct andRBC Dominion Securities – Private Client Division for personal deposits and exclude Royal Trust for residential mortgages.Market shares for the entire group at August 31, 1997 and August 31, 1996 were 16.4% and 15.1% respectively forpersonal loans, 16.6% and 17.1% respectively for personal deposits and 14.4% and 13.9% respectively for residentialmortgages.

➤ Incorporated RBC Life to focus on directsales of life annuities, term insurance andother niche products.

➤ Implemented a direct marketing programfor life annuities for group customers.

➤ Incorporated RBC General Insurance todistribute personal lines home and autoinsurance.

➤ Reached an agreement with HB GroupInsurance Management Ltd., a subsidiaryof The Co-operators Group, to purchasethe technology, systems and expertisenecessary to develop a direct responseproperty and casualty insurance operation,commencing in 1998.

➤ Successfully launched Hospital Cash insur-ance product across the country.

➤ Broadened travel insurance operations byentering the convention and third partygroup administration markets.

➤ Expanded the operations of the InsuranceService Centre to include central review ofbranch creditor insurance applications.

➤ Developed a strategy for expansion ofinternational reinsurance operations withparticular emphasis on the retrocessionmarket.

➤ Consistent with strategy to expand existinginsurance operations, led a bid to acquireLondon Insurance Group. Since LondonInsurance Group was ultimately acquiredby another insurer, a $70 million breakupfee was paid to the bank and, net ofexpenses, $65 million was included in therevenues of the Other segment.

➤ Canada’s largestprovider of financialand electronic busi-ness banking servicesto small and mediumenterprises and com-mercial accounts,serving approxi-mately 380,000customers.

➤ Specialized teamsof market expertsfocused on targetedgrowth segments,which include:

➤ knowledge-basedindustries

➤ agriculture & agri-business

➤ public sector ➤ franchising ➤ professionals ➤ women entrepreneurs➤ aboriginals➤ youth markets.

➤ Established Royal Bank Canada GrowthCo. to help fill the ‘commercialization/company creation gap’ in knowledge-basedindustries and growth sectors.

➤ Launched new client-friendly equipmentleases for small business, offering leases upto $50,000 or Royal Business LeaseLineleasing services by phone, fax, mail or in-branch.This complemented the card-basedRoyal Bank CreditLine for small businessTM

launched in 1996.➤ Introduced Royal Brick & Mortar loans to

offer commercial mortgages at levels suit-able for small business, with title insurance,prepayment, and 60-day rate commitmentoptions.

➤ Launched business banking client (debit)card, which gives small businesses accessto business deposits, payments, transfersand cash at any of Royal Bank’s automatedbanking machines, and is linked to Interacdirect payment system.

➤ Created National Councils with smallbusiness, women and other entrepreneurscomplementing advisory councils on ag-biotech and agri-business.

➤ Published the first annual guides to“Exporting for Small Business in Canada”and “Guide to Small Business Financing inCanada”.

➤ Introduced Internet electronic bankingservices, including access to accountbalances, transaction history and transferof funds between accounts.

➤ New financial EDI payments enabled busi-ness customers to move information andpayments electronically, with automaticupdating of accounts payable and receiv-able capabilities.

➤ The sale of the Payroll and HumanResource Information Business toAutomatic Data Processing Inc. (ADP),combined with a simultaneous strategicalliance with ADP, resulted in a wider arrayof payroll and human resource productsand services to business customers.

➤ Extended ViaTech to 14 sites acrossCanada.ViaTech is a national network ofRoyal Bank and external professionals infinance, taxation, accounting, legal, man-agement, marketing and technical mattersfocused on the needs of knowledge-basedindustries. A similar national network,ViaSource, is being created to focus onsmall business.

where we stand operational reviewbusinesses

insurance

businessbanking

R O Y A L B A N K o f C A N A D A

our businesses

➤ Canada’s largest dis-tributor of creditorinsurance productsby premiums. Servesapproximately 1.8 million cus-tomers and generates$232 million of lifeand disability insur-ance premiums.

➤ Voyageur InsuranceCompany is Canada’slargest provider oftravel insuranceproducts in Canada,with $116 million inpremiums, distrib-uted through anetwork of 3,400travel agents.

➤ Westbury Life ranks7th in Canada interms of number ofnew individual lifeinsurance policiesissued.

commercial bankingpersonal&

financial performance objectives and strategies

R O Y A L B A N K o f C A N A D A

personal and commercial banking

➤ Although creditor life and disability premi-ums increased by 13%, market sharedeclined. This resulted from competitorsbecoming more active in this market inwhich the group already has a high cus-tomer penetration rate.

➤ Total premiums rose by 11%.➤ New life insurance premium market share

remained steady at 2%.

Objectives1. Fulfill customers’ personal insurance

requirements using different convenientdistribution channels.

2.Achieve strong revenue growth in domesticoperations.

3.Expand in key select international markets.4.Achieve annual gross premiums of $1 billion

by the year 2000.

Strategies➤ Expand existing insurance operations

through a combination of startup initiatives,joint ventures and acquisitions.

➤ Focus on technology and matching appropriate products to delivery channels to achieve a low-cost manufacturing anddistribution environment.

➤ Further expand the Insurance ServiceCentre to provide exceptional customerservice to creditor insurance clients and the branch network.

➤ Pursue new sources of international reinsur-ance business with a particular focus on thelife retrocession, property and casualty andfinancial reinsurance markets.

➤ Develop the Global Private Insuranceinitiative to sell insurance through the bank’sGlobal Private Banking units worldwide.

➤ Revenues grew by 8%.➤ Loans to SMEs (small and medium enter-

prises), including agriculture accounts,increased by 9% to $13.2 billion

➤ Efficiency ratio (excluding gain from sale ofpayroll business) was 48.0%, down 210 basispoints from 1996.

➤ Market share in business financing increased80 basis points to 14.2%, and 60 basis pointsin bank business financing to 20.4%.

➤ Market share of business deposits increasedby 380 basis points to 21.8%.

Objectives1.Accelerate revenue growth.2. Increase volumes faster than market.3. Further improve efficiency through

aggressive use of technology.4.Maintain portfolio quality.5.Differentiate the business from other

financial institutions in customer satisfaction.6.Broaden and deepen leadership base.

Strategies➤ Make significant gains in sales effectiveness

and management of customer information.➤ Continue strengthening risk management

processes, leveraging technology to strategi-cally manage portfolio and capital.

➤ Strengthen alignment of business bankers,key functional support, and human resourcepractices to strategic objectives.

➤ Dominate the SME market, lead in targetedgrowth segments, explore global nicheopportunities and expand ‘share of wallet’position.

➤ Profitably align channels, products, services,and sales force to customer segment needs.

(1) Of total financial institutions as at August 31, 1997.(2) Of total banks as at August 31, 1997.(3) As at April/May 1997.

royal trustprovides:

➤ personal wealth management services

➤ investment management

➤ global private banking

➤ global securities services

through a network of 152 offices across Canadaand in 21 other countriesaround the world.

royal mutual fundsoffers 27 mutual funds toCanadians and provides salesand client service throughthe group’s branch networkin Canada and by telephonethrough the Invest by phoneTM

service of Royal Direct.

rbc dominionsecurities – private client division offers full-service securities brokerage,investment advisory andother investment servicesthrough a network of over 1,600 investment advisors in 275 branches in Canada and 6 officesaround the world.

royal bank action directis an investment dealer for discount brokerageservices to Canadian clientswho do their own research,make their own decisionsand enjoy the convenienceof investing by speakingwith an investment repre-sentative or by usingautomated telephone orelectronic channels such as personal computers.

Without the team, there is no ascent. Last year, Royal Bank member companies referred more than 77,000 clients to each otherand generated $5.6 billion in business. Nearly half of this was from the competition and we are raising our sights to attract more new business.

1997 Performance In 1997, the wealth managementsegment of the group enhanced its repu-tation as a leading provider of wealthmanagement services through acquisi-tions and market share growth.

Net income increased by 20% from1996 and reflected strong growth in theearnings of Royal Trust and RoyalMutual Funds.The segment accountedfor 16% of Royal Bank’s total net income(excluding the impact of a $26 millionafter-tax restructuring charge for theacquisition of Richardson Greenshields),up from 14% last year.Wealth manage-ment’s return on equity was 49.7%(55.2% excluding the restructuringcharge), compared to 50.4% last year.Revenues were up 40% with fee income61% higher.

Assets under management were up29%, with more than half of the increaseresulting from new business. Assets underadministration increased by 50% due inpart to RBC Dominion Securities’acquisition of Richardson Greenshieldsand Royal Trust’s acquisition of MontrealTrust’s and Scotiabank’s institutionalcustody business.

Excluding restructuring costs of$51 million from these acquisitions,expenses increased 42% and the efficien-cy ratio was 75.4%.These reflected strongrevenues and, correspondingly, higherexpenses at RBC Dominion Securities.

With the integration of RichardsonGreenshields, RBC Dominion Securitiesestablished itself as the largest Canadiandealer in terms of the number of invest-ment advisors, total client assets, grossrevenue, market share and investmentresearch.

Royal Mutual Funds had net sales of$5.5 billion and the highest sales of anyfund company during the 1996-1997RRSP season.Two new funds - RoyalMonthly Income Fund and Royal PremiumMoney Market Fund – contributed to theoverall growth.

Royal Trust’s fee income grew 30%,due to strong growth in investment man-agement, Global Securities Services andglobal private banking. Royal Trustincreased its emphasis on financial coun-selling and now has over 150 accreditedfinancial planners.

Royal Bank Action Direct, the group’sdiscount brokerage arm, experiencedrecord growth in 1997 with assets underadministration up 50% to $5.4 billionand client accounts up 42% to 231,000.

R O Y A L B A N K o f C A N A D A

wealth management

Objectives The segment’s goal is to further establish itsposition as Canada’s leading provider of wealth managementservices in Canada and internationally, to increase fee revenueby at least 10% per year and to grow earnings.Strategies The primary focus is to leverage the capabilitiesof the various Wealth Management business units to improvethe quality of service offered to individual clients. The group’sreferral program has already generated substantial referralsamong group companies. The segment plans to extend fullfinancial service offices to other locations within thenetwork, as these have proven to be an extremely effective

means of meeting clients’ broad financial service needs.The segment aims to continue to develop its ability to providefinancial advice. A significant number of employees areexpected to achieve personal financial planning designationsin 1998. Bundled service offerings are being developed toprovide clients with a range of choices to support thisfinancial advice.

Internationally, the segment plans to continue to expandby developing alliances in under-represented markets.International investment capability will also be expanded in selected markets.

➤ Canada’s largestinvestment managerby assets under man-agement and largestcustodian by assetsunder administration.

➤ Largest global privatebanking network ofany Canadian finan-cial institution bynumber of branches.

➤ Over 150 employees earned personalfinancial planning accreditation.

➤ Formed distribution alliances for globalprivate banking services with two leadingAmerican banks, Norwest andNationsBank.

➤ Acquired Montreal Trust’s and Scotiabank’sinstitutional and pension custody business.

➤ Top ranked provider of Canadian custody(Global Custodian, Fall 1997) and 2nd inthe world for global custody (GlobalInvestor, May 1997).

➤ Personal Trust assets exceeded $20 billionfor the first time.

➤ Transition of TD Bank’s pension and institutional clients to Royal Trust wascompleted ahead of schedule.

➤ Increased institutional investmentmanagement assets by 36%.

➤ Canada’s thirdlargest mutual fundcompany asmeasured by assetsunder management.

➤ Largest among no-load mutual fundproviders.

➤ Balances exceeded $20 billion for thefirst time.

➤ New Royal Monthly Income Fund offeredinvestors steady monthly pay-outs whichcan be a combination of interest, dividendsand capital gains. Now exceeds$250 million.

➤ Launched Royal Premium Money MarketFund as a liquid, flexible, convenient choicefor large short-term investments whichnow has over $800 million in assets.

➤ Completed merger of similar Royal TrustMutual Funds and Royal Bank Royfunds.

➤ Introduced Personal Investment Planner,a tool which provides a framework foroffering client-driven financial advice andinvestment recommendations.

➤ Received top ranking for telephone clientservice in the independent L. S. Dalbarindustry survey.

➤ Canada’s largestinvestment advisor in RSP/RIFs, non-registered investmentassets, mutual funds,equities and wealthmanagement.

➤ Over $78 billion of investment assets.➤ Assets in the Sovereign Investment Program

increased to $1.7 billion, up 148% fromlast year.

➤ New fee-based, non-discretionary AdvisorAccount exceeded $1 billion in assets.

➤ Introduced Compass Financial Plan to helpclients develop a comprehensive financialplan.

➤ Introduced WealthBuilder RSP, Family ESP,and Royal Choices Group RSP.

➤ Completed the integration of RichardsonGreenshields.

where we stand operational reviewbusinesses

➤ Canada’s secondlargest discount broker.

➤ Among the top 10 discount broker-age firms in NorthAmerica in terms ofnumber of accounts.

➤ Welcomed over 75,000 new clientaccounts.

➤ Introduced Value RSP to appeal to mutualfund investors and a premium package,Select Service.

➤ Completed national roll-out of PCAction,PC-based investment system.

➤ Made touchtone telephone trading andquote system, TelAction, available 24 hoursa day, 7 days a week.

➤ Opened second Investor Centre inToronto.

➤ Expanded investment information availablefor clients through Research Source, theAction Direct Investor newsletter and theweb site.

➤ Mutual Fund Marketplace now exceeds 700 funds from over 50 fund families.

➤ At year end, 22% of all transactionswere completed electronically.

royal trust

royal mutualfunds

rbc dominion securities –private client division

royal bank action direct R O Y A L B A N K o f C A N A D A

corporate bankinga complete range of credit and operating services delivered through an international network of relationship managers

➤ loan trading

➤ loan syndications

➤ project and structured finance

➤ tax structured finance

➤ asset securitization

➤ global cash management

managing risk through:

➤ advanced portfolio management

➤ sophisticated credit mitiga-tion techniques

financial institutions &tradecorrespondent banking services provided to 3,500 of the world’s largest financial institutions:

➤ credit services

➤ deposit services

➤ collection services

➤ clearing services

➤ payment services

non-bank financial institution services provided to insurance companies,finance companies, and investment dealers around the world:

➤ credit products

➤ operating products

➤ treasury products

global trade & commodityfinance services:

➤ letters of credit

➤ guarantees

➤ receivables financing

rbc dominion securities –institutional divisionrbc ds global markets:

➤ foreign exchange includingcurrency risk management 24 hours a day, through an extensive global sales andtrading network

➤ fixed income and capitalmarket services including:origination and distributionof new products, secondarymarket sales and trading ofgovernment, provincial,municipal, and corporatedebt instruments, interestrate derivatives, swaps, riskmanagement

➤ money markets: overnightfunding, commercial paper,all major currency funding,Canadian dollar securitiesfunding

investment banking:

➤ advisory services for mergers,acquisitions, divestitures andreorganizations

➤ equity & debt underwriting

➤ advisory services for newissues, mergers, acquisitions

Look up! The outstanding success of our Loan Syndication and Project Finance strategies in Latin America have quickly made us the 7thlargest co-arranger in the world. It’s the kind of entry that some can only dream about.We call it a good start and plan on even better results.

1997 Performance Corporate and investment bankingaccounted for 20% of the bank’s netincome in 1997 compared to 10% in1996 when a $300 million addition tothe general provision reduced earnings.Return on equity improved to 18.7%.

Revenues increased by 21%,with net interest income up 18% andother income 23% higher due largely to improved performance at RBCDominion Securities’ (RBC DS)institutional division.

Non-interest expenses were similarlyhigher due to greater variable compen-sation costs at RBC DS.

Specific provisions for credit losseswere $142 million versus $124 millionlast year, as recoveries were lowerin 1997.

The efficiency ratio deteriorated to57.2%, reflecting the greater contributionof RBC DS, which has a much higherefficiency ratio than the other businessesin this segment due to its variable incen-tive compensation.

R O Y A L B A N K o f C A N A D A

corporate and investment banking

Objectives The major objective of this segment is to becomemore responsive in providing integrated corporate and invest-ment banking solutions to meet the financing and balance sheetneeds of our corporate and government clients. In addition, thesegment continues to broaden the range of products available toour customers in the United States including leveraged lending,securitization, trade and receivables financing, equity derivativesand other similar initiatives.

Strategies To achieve our objectives, we plan to meld thethree businesses serving corporate and government customersmore closely, and provide seamless delivery of a full range ofcorporate and investment banking products and services inCanada, and more selectively in other markets.To improveprofitability, the segment plans to focus on individual accountprofitability and on demarketing accounts with unacceptablereturns. Increased liquidity of the loan portfolio will be achievedthrough securitization, loan trading and other means.

➤ Serves more than1,000 corporate andinstitutional clientsin Canada, the USA,Europe, LatinAmerica and Asia.

➤ Delivers all the capa-bilities of the groupto clients around theworld.

➤ Leads in market posi-tion and importancedomestically accord-ing to independentbenchmarking.

➤ Exclusive agent forjust under 50% ofthe world’s largestbanks in settlingtheir Canadian dollarinterbank payments.

➤ Leading bank toCanadian insuranceindustry.

➤ Maintains trade linesin over 130countries.

➤ Leading provider ofcomprehensivecapital market prod-ucts, debt and equityunderwritings forCanadian corpora-tions, innovativefinancing instru-ments, income trusts,real estate finance,corporate brokerage,advice on mergers,acquisitions anddivestitures.

➤ Top-ranked dealer inresearch, sales andtrading of Canadianequities.

➤ Canada’s largestcommercial paperagent and provider ofsecurities and securi-ties financing.

➤ Canada’s mostprofitable foreignexchange bank.

➤ Active market makerin US$-based cur-rency, pairs, EMScrosses, and curren-cies of Asia, EasternEurope, and LatinAmerica.

where we stand operational reviewbusinesses

corporatebanking

financial institutions & trade

rbc dominionsecurities –institutionaldivision

R O Y A L B A N K o f C A N A D A

our businesses

➤ Lead-managed 73 debt and equity financ-ings, and co-managed a further 147transactions, to raise an aggregate $35.7billion for clients, a result which surpassesall other Canadian competitors.

➤ Led the structuring and distribution of 16 royalty and income trusts for anaggregate value of $3.5 billion.

➤ Advised on 9 of the top 15 M&A transac-tions in Canada in 1997.

➤ Advised Loram Corporation in an assess-ment of private sale and public marketalternatives for its three main businesses,resulting in Loram realizing proceeds inexcess of $2 billion.

➤ Played a key role in developing theCanadian high-yield debt market, leadmanaging three transactions for proceedsof $560 million.

➤ Merged fixed income, money market andforeign exchange operations, includingtheir derivatives, of Royal Bank, RBC DS,and Richardson Greenshields to formGlobal Markets trading group.

➤ Increased volumes of domestic securitieslent and/or financed by 25%.

➤ Significantly expanded the research team toprovide broader and more specialized cov-erage of Canadian industry.

➤ Expanded global mining research, salesand trading specialists and increasedinvestment in South African securitiesdealers, SMK Securities (PTY) Limited,to 25%.

➤ Introduced Index Linked StructuredNotes and GICs.

➤ Developed equity monetization productsfor corporate and high net worth clients.

➤ Expanded equity derivatives businessin Europe.

➤ Enhanced global syndications capabilitythrough units in Toronto, New York,London and Singapore.

➤ Established a loan trading unit in New York.➤ Formed a global project & structured

finance group.➤ Expanded in tax-structured financing.➤ Accelerated North American securitization

activity.➤ Launched a leveraged lending unit in the

U.S.A.➤ Followed a portfolio management

approach, using credit derivatives and other such tools to manage risk.

➤ Continued focus on relationship manage-ment with professional staff supported bysophisticated information and deliverysystems.

➤ Expanded and refined focus on selectedindustries including forest products, miningand metals, media/telecommunications,public sector, specialized manufacturing(including automotive and aircraftfinancing) and energy.

➤ Ranked among top 10 banks in the worldin the energy sector by the UK-based publication, Petroleum Economist.

➤ Launched Tradeview, a new suite ofelectronic products giving electronicbanking access to Canadian importers andexporters.

➤ Provided Internet access to correspondentbanking clients seeking account balancesand transactions.

➤ Invested in Northstar Trade Finance Inc.,a company which provides medium-termloans to support Canadian exporters.

➤ Opened offices in Los Angeles, Houstonand Boston through RBC Trade Finance(USA) Inc.

investment bankingcorporate&

financial performance objectives and strategies

R O Y A L B A N K o f C A N A D A

corporate and investment banking

➤ Despite an increase in loans and acceptances,revenues declined slightly due to narrowerspreads, particularly outside Canada.

➤ Efficiency ratio rose slightly and is now competitively positioned in the mid-40s.

➤ Specific provisions for credit losses declinedthis year.

Objectives1. Achieve top quartile risk-adjusted returns.

Strategies➤ Maintain position as a low-cost producer.➤ Ensure a sound and diversified portfolio.➤ Focus on financial partnerships with core

clients.➤ Expand internationally by providing solu-

tions to clients in selected industries.➤ Enhance fee-based businesses such as securi-

tization, syndication and secondary loanfunding.

➤ Revenues increased 19%.➤ Average assets were 56% higher with the

increase well dispersed geographically andlargely in short-term credits to banks andcorporations.

➤ Average letters of credit balances wereup 33%.

Objectives1.Grow revenues by at least 10% annually.2. Become a top 20 global trade bank by the

year 2001.

Strategies➤ Use technology to develop new products

and delivery channels, and to reduce costs.➤ Grow and internationally diversify revenues

from products provided to insurance com-panies.

➤ Revenues grew by 35% with strongperformance in all areas.

➤ Revenues from Global Markets grew by28% to $556 million.

➤ Revenues from Institutional Equityincreased 44% to $258 million.

Objectives1.Maintain position as market leader in debt

and equity financing and merger andacquisition advice.

2.Build upon top presence in equity and fixedincome sales, trading and research with newproduct capabilities which provideinnovative solutions.

3.Become one of the world’s top ten foreignexchange banks.

4. Focus on maximizing long-term profitability.

Strategies➤ Focus on industry specialization and coordi-

nation of the group’s corporate lendingfunction with targeted efforts of RBC DSdivision.

➤ Remain the leading investment dealerserving Canadian institutional clients.

➤ Foster still greater interdepartmental coop-eration on innovative solutions in the debtand equity capital markets, building uponrecent high yield debt and equity derivativesuccess.

➤ Invest in technology to better monitorcross-market flows.

➤ Control costs by centralizing operations,rationalizing systems and investing inelectronic platforms.

➤ Expand selectively internationally toaugment product expertise for preferredindustry sectors.