24

Corporate Tax Reform III – Dispatch of the Federal Council Webcast 9 June 2015

| Date post: | 26-Jul-2015 |

| Category: |

Economy & Finance |

| Upload: | kpmg-switzerland |

| View: | 643 times |

| Download: | 0 times |

Corporate Tax

Reform III –

Dispatch of the

Federal Council

Webcast

9 June 2015

1© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Welcome to our webcast!

Background of the Corporate Tax Reform III

Dispatch with legislative draft June 5, 2015

What has changed since September 22, 2014

Disclosure rules for hidden reserves and transitional measures (Step-up)

Innovation: Patent box and R&D input incentives

Other measures

Abolished measures

Outlook and our position

Your contacts

2© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

Background of Corporate Tax Reform III

Debate with EU on Swiss tax regimes since 2005

2007: ring fencing criticized, violation of Free Trade Agreement

EU Code of Conduct for Business Taxation

2012: Dialogue with EU started

2013: Reports on Corporate Tax Reform III

Willingness to discontinue 5 tax regimes

at Cantonal level: holding, domicile and mixed company regimes

at Federal level: principal company regime

Swiss finance branch regime

New measures in compliance with OECD principles

No retaliatory measures by EU member states

22 September 2014: Legislative draft of Corporate Tax Reform III

5 June 2015: Dispatch of Corporate Tax Reform III with draft legislation

3© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

June 2015: Dispatch of Corporate Tax Reform III (1/2)

Increasing international acceptance of Swiss

Corporate Tax legislation

Further development of the

competitiveness of Switzerland as an

attractive business location

Securing of adequate tax revenues

to finance public activities

Goals of the Reform

4© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

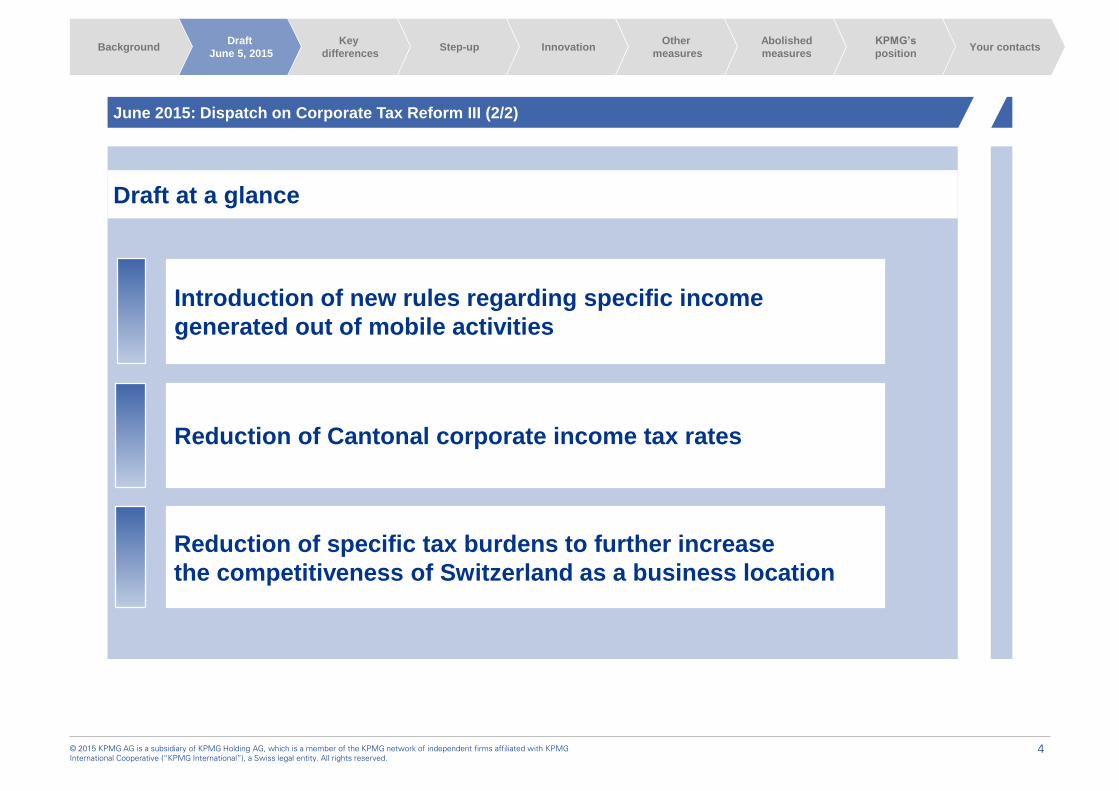

June 2015: Dispatch on Corporate Tax Reform III (2/2)

Draft at a glance

Introduction of new rules regarding specific income

generated out of mobile activities

Reduction of Cantonal corporate income tax rates

Reduction of specific tax burdens to further increase

the competitiveness of Switzerland as a business location

5© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

What has changed since 22 September, 2014

High level comparison

Legislative draft of 22 September 2014

License Box

Abolishment of Cantonal tax statuses, principal

company taxation practice and finance branch regime

Step-up Disclosure rules for hidden reserves

Patent Box

R&D input incentives

No NID

Reduced number of further measuresSeveral further measures

Notional Interest Deduction (NID)

Abolishment of Cantonal tax statuses, principal

company taxation practice and finance branch regime

Dispatch of 5 June 2015

Disclosure rules

for hidden

reserves and

transitional

measures

7© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

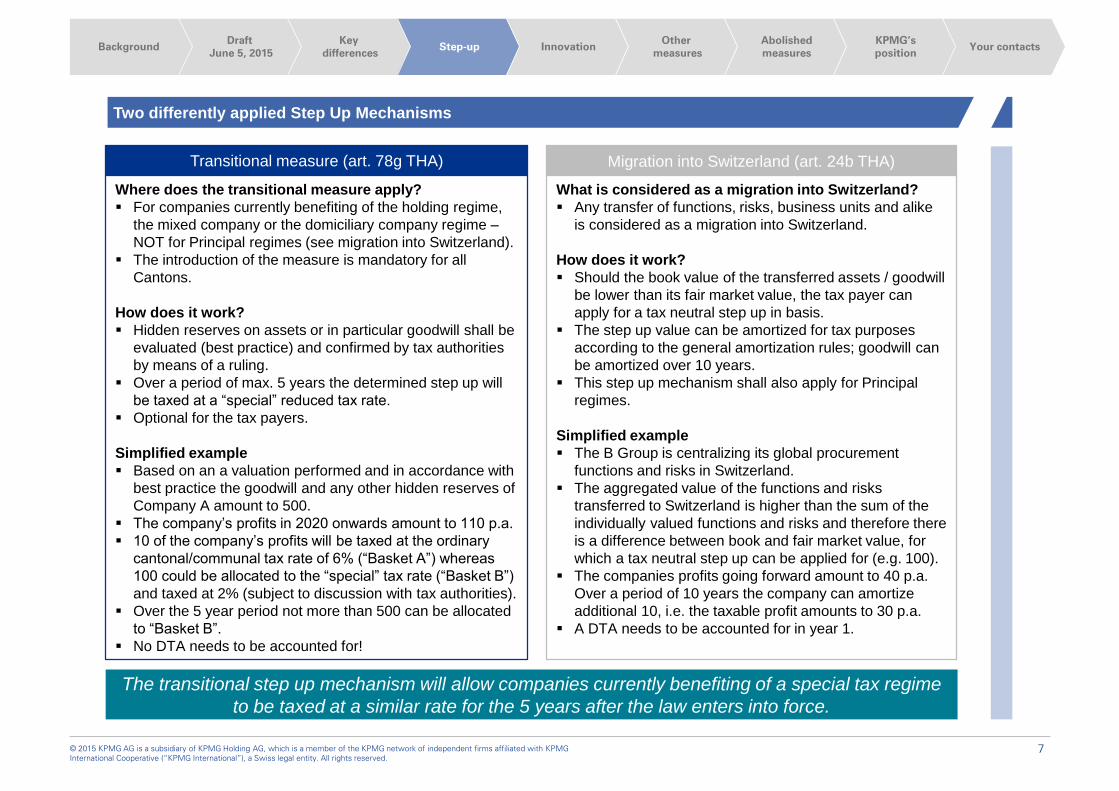

Transitional measure (art. 78g THA) Migration into Switzerland (art. 24b THA)

Where does the transitional measure apply?

For companies currently benefiting of the holding regime,

the mixed company or the domiciliary company regime –

NOT for Principal regimes (see migration into Switzerland).

The introduction of the measure is mandatory for all

Cantons.

How does it work?

Hidden reserves on assets or in particular goodwill shall be

evaluated (best practice) and confirmed by tax authorities

by means of a ruling.

Over a period of max. 5 years the determined step up will

be taxed at a “special” reduced tax rate.

Optional for the tax payers.

Simplified example

Based on an a valuation performed and in accordance with

best practice the goodwill and any other hidden reserves of

Company A amount to 500.

The company’s profits in 2020 onwards amount to 110 p.a.

10 of the company’s profits will be taxed at the ordinary

cantonal/communal tax rate of 6% (“Basket A”) whereas

100 could be allocated to the “special” tax rate (“Basket B”)

and taxed at 2% (subject to discussion with tax authorities).

Over the 5 year period not more than 500 can be allocated

to “Basket B”.

No DTA needs to be accounted for!

The transitional step up mechanism will allow companies currently benefiting of a special tax regime

to be taxed at a similar rate for the 5 years after the law enters into force.

Two differently applied Step Up Mechanisms

What is considered as a migration into Switzerland?

Any transfer of functions, risks, business units and alike

is considered as a migration into Switzerland.

How does it work?

Should the book value of the transferred assets / goodwill

be lower than its fair market value, the tax payer can

apply for a tax neutral step up in basis.

The step up value can be amortized for tax purposes

according to the general amortization rules; goodwill can

be amortized over 10 years.

This step up mechanism shall also apply for Principal

regimes.

Simplified example

The B Group is centralizing its global procurement

functions and risks in Switzerland.

The aggregated value of the functions and risks

transferred to Switzerland is higher than the sum of the

individually valued functions and risks and therefore there

is a difference between book and fair market value, for

which a tax neutral step up can be applied for (e.g. 100).

The companies profits going forward amount to 40 p.a.

Over a period of 10 years the company can amortize

additional 10, i.e. the taxable profit amounts to 30 p.a.

A DTA needs to be accounted for in year 1.

Innovation: Patent

box and R&D

input incentives

9© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

Corporate Tax Reform III: Facilitating innovation in an organization’s value chain, promoting Switzerland

ProcurementOperational

excellence

Logistics &

DistributionProduction R&D Marketing Sales

Primary activities

Innovation is key for developed economies

Centralization of business models and high value add

activities

Continuous trend of innovation friendly tax regimes

Maintain competitive advantage

OECD-BEPS (Action 5!)

What is driving the international tax landscape

Simplified overview value chain “innovation” driven organization

100%

Profitability

10© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

Matching the international tax standard for promoting innovation

Basic research

Proof of concept

development

release

enhancements

Potential input incentive

Potential output incentive

Input incentive: primarily linked to the cost structure of an organization.

Output incentive: focus on the commercial benefits from the exploitation of R&D.

The combination of input - and output incentives are common practice in competing jurisdictions and may further strengthen the

competitive position of the Cantons in the (inter)national tax landscape.

lifecycle

innovation

11© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

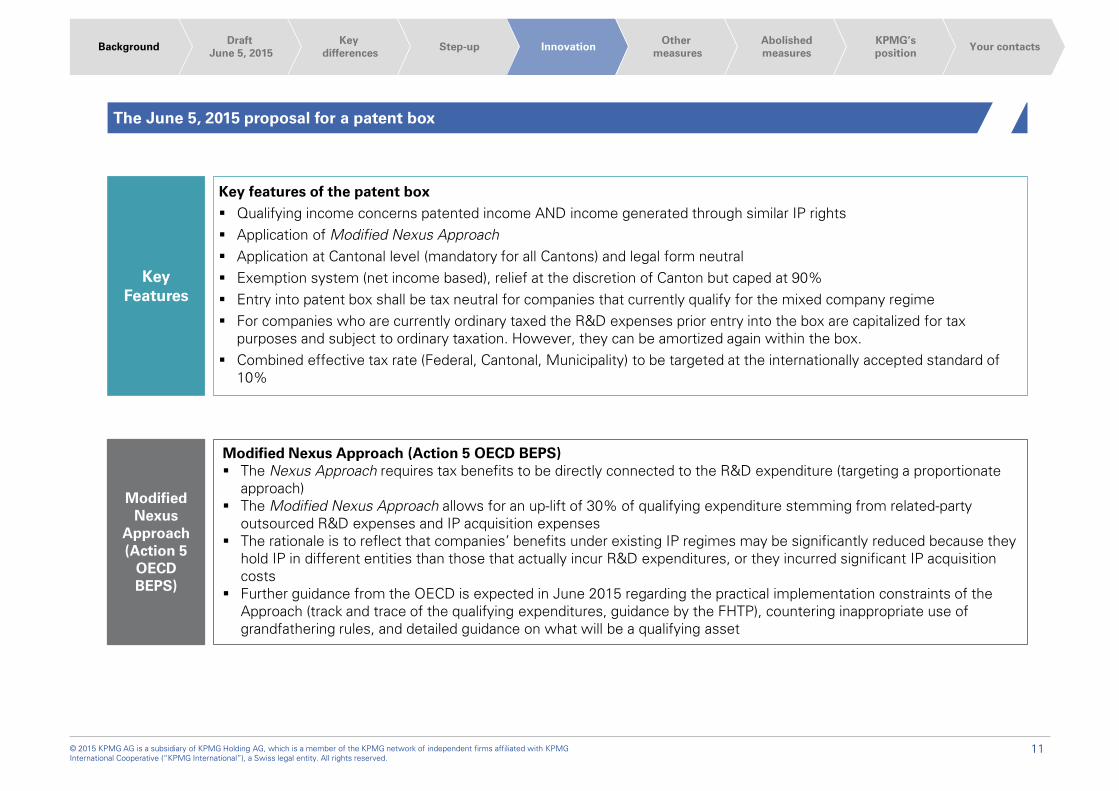

The June 5, 2015 proposal for a patent box

Key

Features

Key features of the patent box

Qualifying income concerns patented income AND income generated through similar IP rights

Application of Modified Nexus Approach

Application at Cantonal level (mandatory for all Cantons) and legal form neutral

Exemption system (net income based), relief at the discretion of Canton but caped at 90%

Entry into patent box shall be tax neutral for companies that currently qualify for the mixed company regime

For companies who are currently ordinary taxed the R&D expenses prior entry into the box are capitalized for tax

purposes and subject to ordinary taxation. However, they can be amortized again within the box.

Combined effective tax rate (Federal, Cantonal, Municipality) to be targeted at the internationally accepted standard of

10%

Modified Nexus Approach (Action 5 OECD BEPS)

The Nexus Approach requires tax benefits to be directly connected to the R&D expenditure (targeting a proportionate

approach)

The Modified Nexus Approach allows for an up-lift of 30% of qualifying expenditure stemming from related-party

outsourced R&D expenses and IP acquisition expenses

The rationale is to reflect that companies’ benefits under existing IP regimes may be significantly reduced because they

hold IP in different entities than those that actually incur R&D expenditures, or they incurred significant IP acquisition

costs

Further guidance from the OECD is expected in June 2015 regarding the practical implementation constraints of the

Approach (track and trace of the qualifying expenditures, guidance by the FHTP), countering inappropriate use of

grandfathering rules, and detailed guidance on what will be a qualifying asset

Modified

Nexus

Approach

(Action 5

OECD

BEPS)

12© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

The June 5, 2015 proposal for a patent box

Total profit

-/- non-box income

-/- routine activity related income

-/- commercial IP

Patent box qualifying income

30% (max.) uplift qualifying expenditure (related party outsourcing and acquisition costs)

Qualifying expenditure incurred to develop

IP asset

---------------------------------------------------

Overall expenditure incurred to develop IP

asset

X overall Income from IP

asset= eligible IP income for

the Patent box

Modified nexus

Residual income approach applying the modified nexus concept

Year -2 Year -1 Year 0 Year 1 Year 2 Year 3

R&D Cost 120 at entry Patent income pa 90 / total income pa 100

Total costs to develop IP

Total qualifying costs to develop Patent

Modified Nexus Impact max uplift (30%)

160

120

36

Total Profit Year 1*

-/- non-qualifying income

Patent box income (incl. amort.)*

100

-10

90

* incl. amortization of Patent which stays in the box based on

current understanding of the proposal.

Expensed qualified R&D expenditure

One-off taxation to benefit from patent box

Annual patent box income: 156/160 x 90 = 88

Exempt patent box income (90% exemption) =

Taxable patent box income (90 -/- 79)

Non-box income

Taxable income year 1:

Taxable income year 2:

120

120

88

79

11

10

141

21

13© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

Corporate Tax Reform III: Facilitating innovation through input incentives

Key

Features

Key features of the envisaged input incentive

Input incentives can be described as tax incentives that are primarily linked to the cost structure of an organization

Super deduction of qualifying R&D costs at Cantonal level at the discretion of the Cantons (no impact on the vertical

compensation)

Super deduction also applied on expenses related to Swiss contract R&D (tax incentive can only be claimed once – usually on the

level of the purchaser of the R&D services)

Not limited to patented IP (potentially broad scope), targeting rather R(esearch) than D(evelopment)

Aimed at the production of intangible assets, targeting the Swiss domestic Principal of R&D activities instead of the Contractor

System to be designed according to principle of (super)deductions (vs. tax credits)

Incentive capped by loss situation (no cash out)

Envisaged implementation in the THA

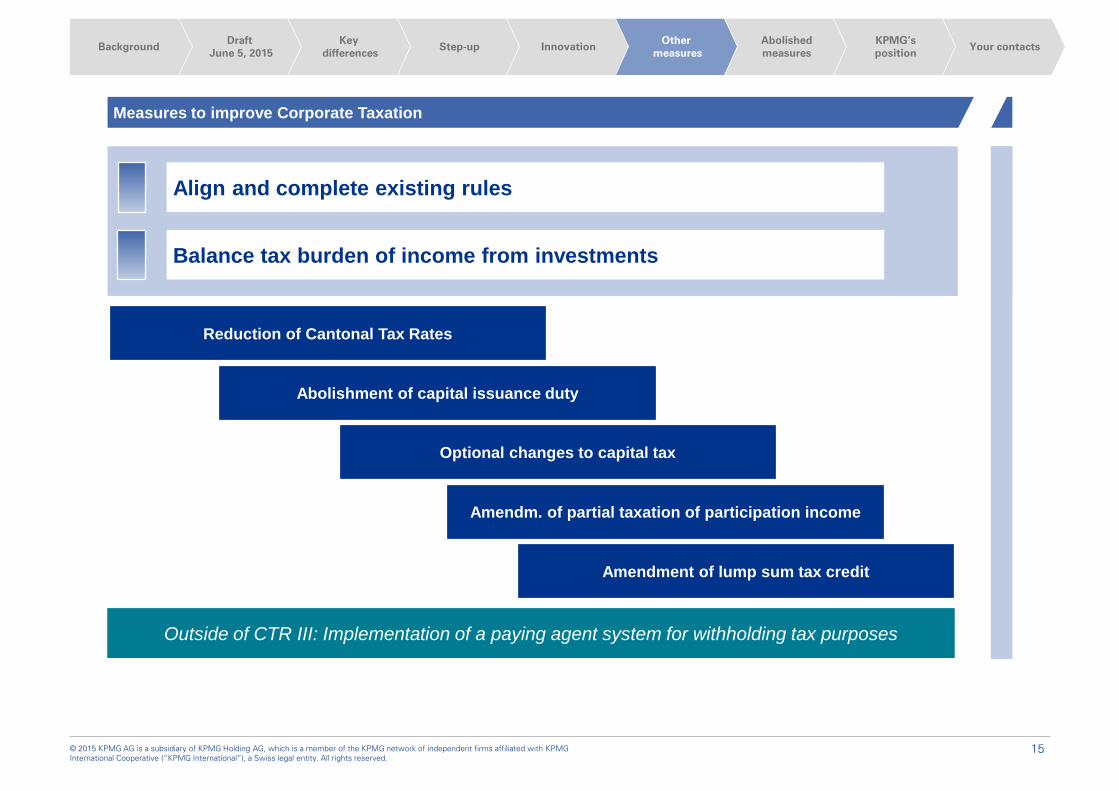

Other measures

15© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Align and complete existing rules

Balance tax burden of income from investments

Optional changes to capital tax

Abolishment of capital issuance duty

Amendment of lump sum tax credit

Reduction of Cantonal Tax Rates

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

Measures to improve Corporate Taxation

Amendm. of partial taxation of participation income

Outside of CTR III: Implementation of a paying agent system for withholding tax purposes

Abolished

measures

17© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

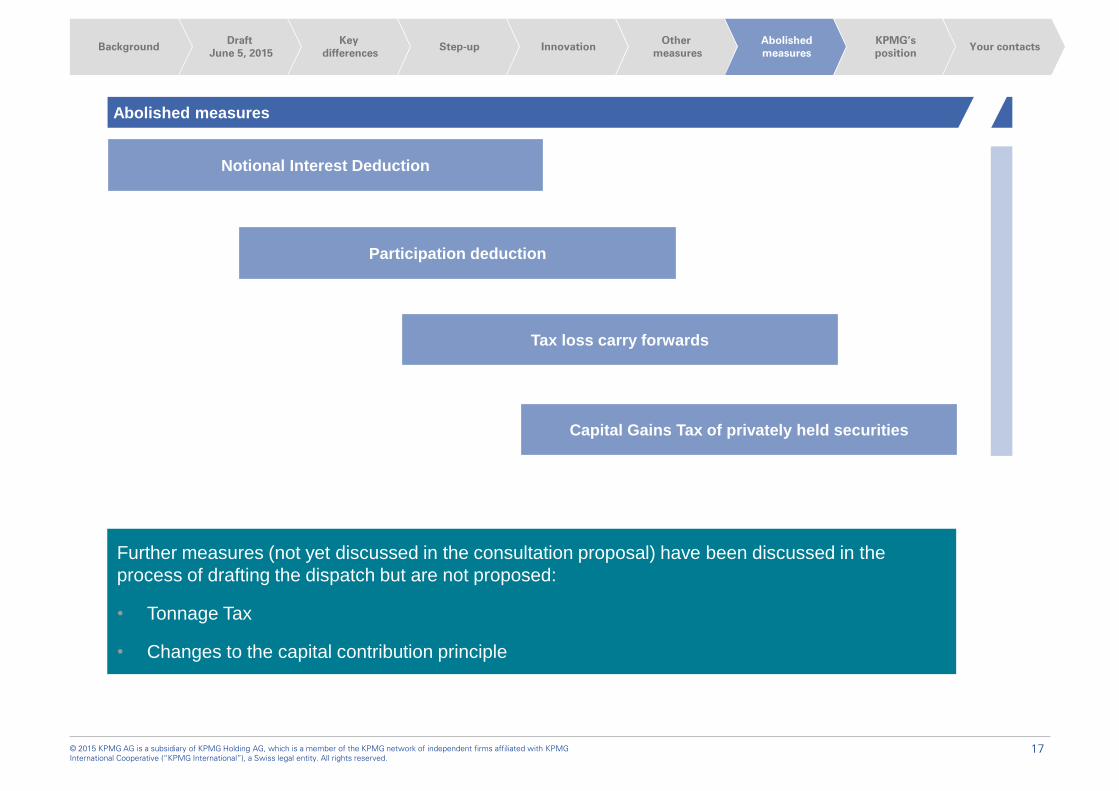

Abolished measures

Notional Interest Deduction

Tax loss carry forwards

Participation deduction

Capital Gains Tax of privately held securities

Further measures (not yet discussed in the consultation proposal) have been discussed in the

process of drafting the dispatch but are not proposed:

• Tonnage Tax

• Changes to the capital contribution principle

18© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Focus on NID (1/2)

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

NID on “higher-than-average” equity proposed in the

consultation

No NID on so-called „core capital“, i.e. equity that

exceeds the core capital qualifies as „higher-

than-average“ equity, subject to NID

Definition of core capital and applicable interest

rate:

Proposed calculation of core capital

according to fixed quotas per asset

category (e.g. cash 0% / 15%, third-party

receivables 40%, intangibles 55%,

investments 100%) to be published by

authorities in a Circular Letter

Proposed interest rate: safe harbor rate

published by authorities (e.g. long-term

rate on Federal bonds + 0.5%), in

minimum 2%; no higher rate according to

transfer pricing study accepted

Federal Council refrained from proposing any

NID in the dispatch:

NID was mainly refused by the Cantons in

the consultation (shortfall in tax revenues)

International acceptance was partially

questioned

However, NID is still discussed…

NID is still discussed and may be proposed

again within the parliamentary debate

However, NID will be amended in order to meet

the concerns addressed in the consultation

The following changes are discussed:

No NID on non-business related assets

No NID in connection with intra-group

loans based on group internal sales of

participations or on leveraged dividends

No minimum interest rate but flexibility to

apply a higher arm’s length interest rate

in case of loans to group companies (i.e.

group financing, taxation of an interest

margin)

Especially with respect to the flexibility in the

interest rate it should be possible to offer a

competitive income tax environment for group

financing activities after abolishment of the

Swiss finance branch practice

19© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

Assets Liabilities

100 cash 150 debt

100 third-party receivables

100 IP 250 equity

100 investments

Core equity quota Core equity

15% cash* 15

40% third-party receivables 40

55% IP 55

100% investments 100

210

Core equity (no NID) 210

Equity subject to NID 40

Total equity 250

Equity subject to NID 40

X (assumed) interest rate x 3%

NID 1.2 * Assumption: business related cash; otherwise 100%

Calculation example

Focus on NID (2/2)

Outlook and our

position

21© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

Expected timeline until implementation

c 2019 - …

Publication of

Legislative

Draft

22.09.2014

Decision

Federal Council

Preparation of

Dispatch

April 2015

Law enters

into force

(1.1.2017 if no

referendum)*

Start of

Consultation

Procedure

Implementation into

Cantonal Law*

Publication of

Dispatch

Start of

Parliamentary

Discussions in

Commissions and

Chambers

05.06.2015

Final Decision

Parliament

Start of

Referendum

Period

End of

Consultation

Procedure

31.01.2015

20172016 201820152014

*In case of a referendum and public vote, the entry into force will be delayed by one year.

22© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

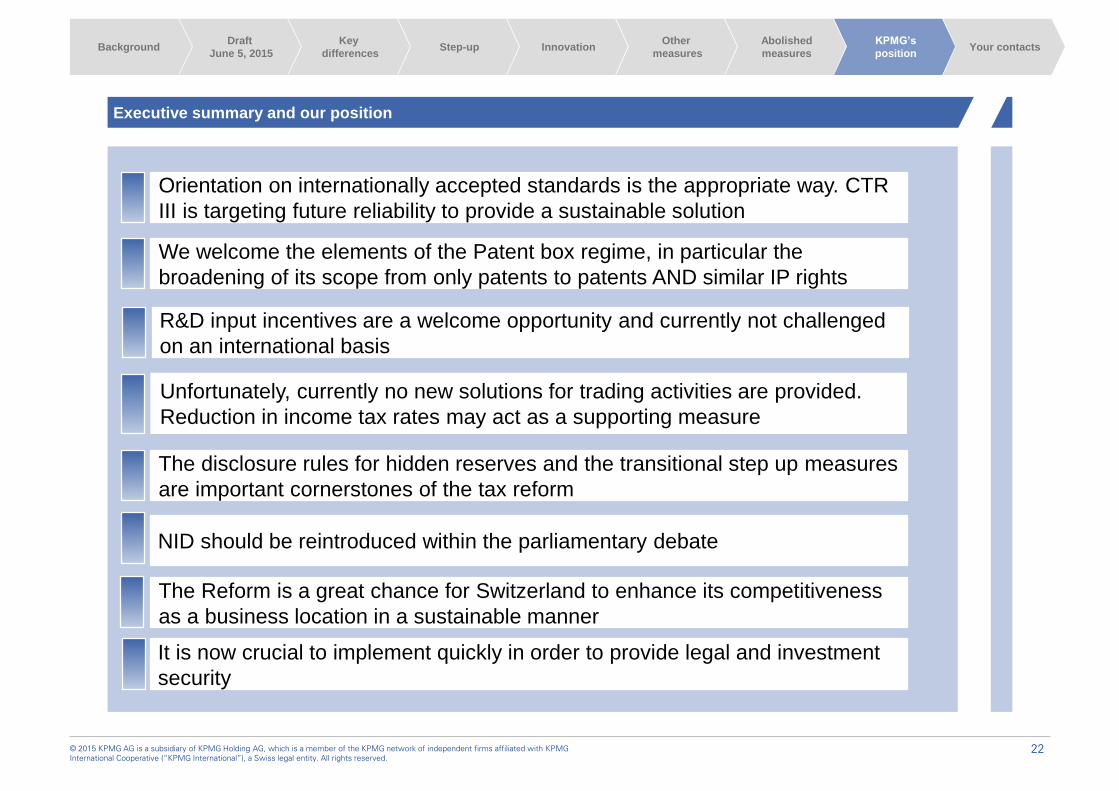

Executive summary and our position

Orientation on internationally accepted standards is the appropriate way. CTR

III is targeting future reliability to provide a sustainable solution

We welcome the elements of the Patent box regime, in particular the

broadening of its scope from only patents to patents AND similar IP rights

The disclosure rules for hidden reserves and the transitional step up measures

are important cornerstones of the tax reform

The Reform is a great chance for Switzerland to enhance its competitiveness

as a business location in a sustainable manner

It is now crucial to implement quickly in order to provide legal and investment

security

Unfortunately, currently no new solutions for trading activities are provided.

Reduction in income tax rates may act as a supporting measure

NID should be reintroduced within the parliamentary debate

R&D input incentives are a welcome opportunity and currently not challenged

on an international basis

23© 2015 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

BackgroundDraft

June 5, 2015

Key

differencesStep-up Innovation

Other

measures

Abolished

measures

KPMG’s

positionYour contacts

Your contacts

► Please direct any inquiries to [email protected]

Peter Uebelhart

Managing Partner

Tax

Tel: +41 58 249 42 24

Stefan Kuhn

Partner

Head of Corporate Tax

Tel: +41 58 249 54 14

Hans Mies

Director

Corporate Tax

Tel: +41 58 249 59 41

Olivier Eichenberger

Senior Manager

Corporate Tax

Tel: +41 58 249 41 67