42

[Type text] Corporates in growth mode despite global headwinds Global Market Perspective | Q1 2016

[Type text]

Corporates in growth mode

despite global headwinds

Global Market Perspective | Q1 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 2

Global Market Perspective, First Quarter 2016

Global Market Perspective

Contents

Corporates in Growth Mode Despite Global Headwinds ............................................................................................... 3

Global Economy ................................................................................................................................................................ 6

Real Estate Capital Markets ............................................................................................................................................. 8

Investment Volumes ............................................................................................................................................................ 8

Capital Values and Yields ................................................................................................................................................. 13

Corporate Occupiers ...................................................................................................................................................... 14

Global Real Estate Health Monitor ................................................................................................................................. 16

Office Markets ................................................................................................................................................................. 17

Office Demand Dynamics ................................................................................................................................................. 17

Office Supply Trends ......................................................................................................................................................... 20

Office Rental Trends ......................................................................................................................................................... 24

Retail Markets .................................................................................................................................................................. 27

Industrial Warehousing Markets .................................................................................................................................... 29

Hotel Markets ................................................................................................................................................................... 30

Residential Markets ........................................................................................................................................................ 34

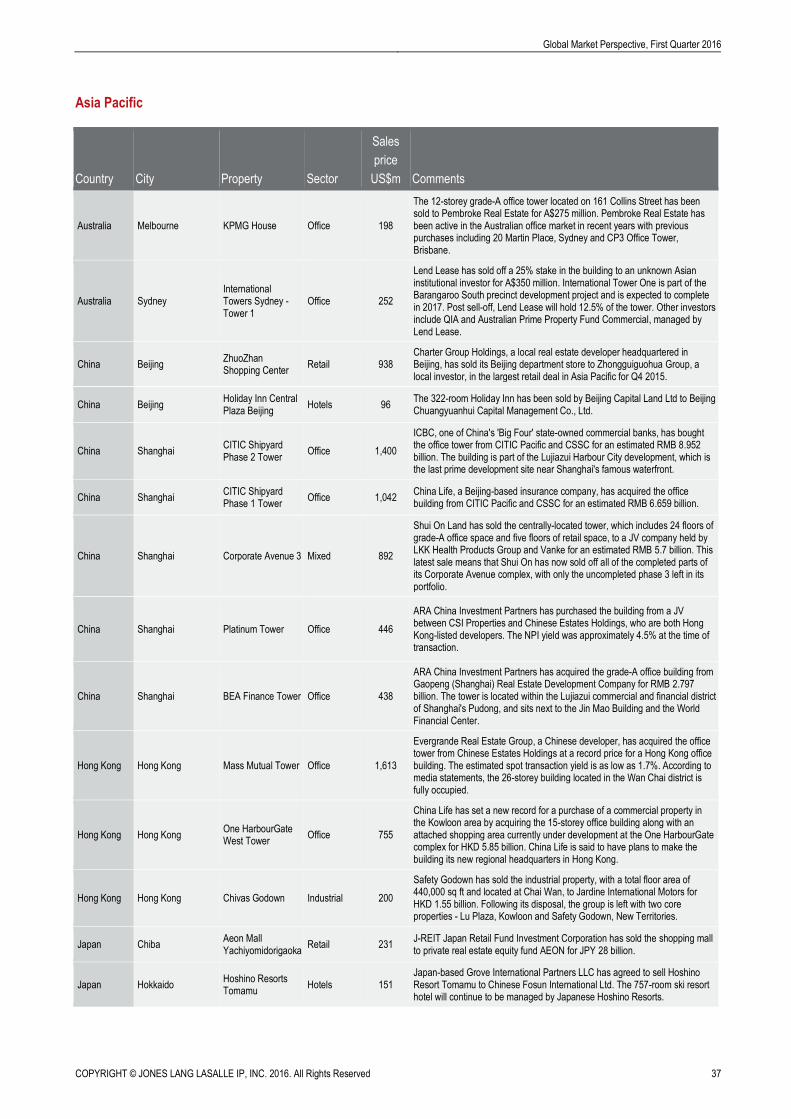

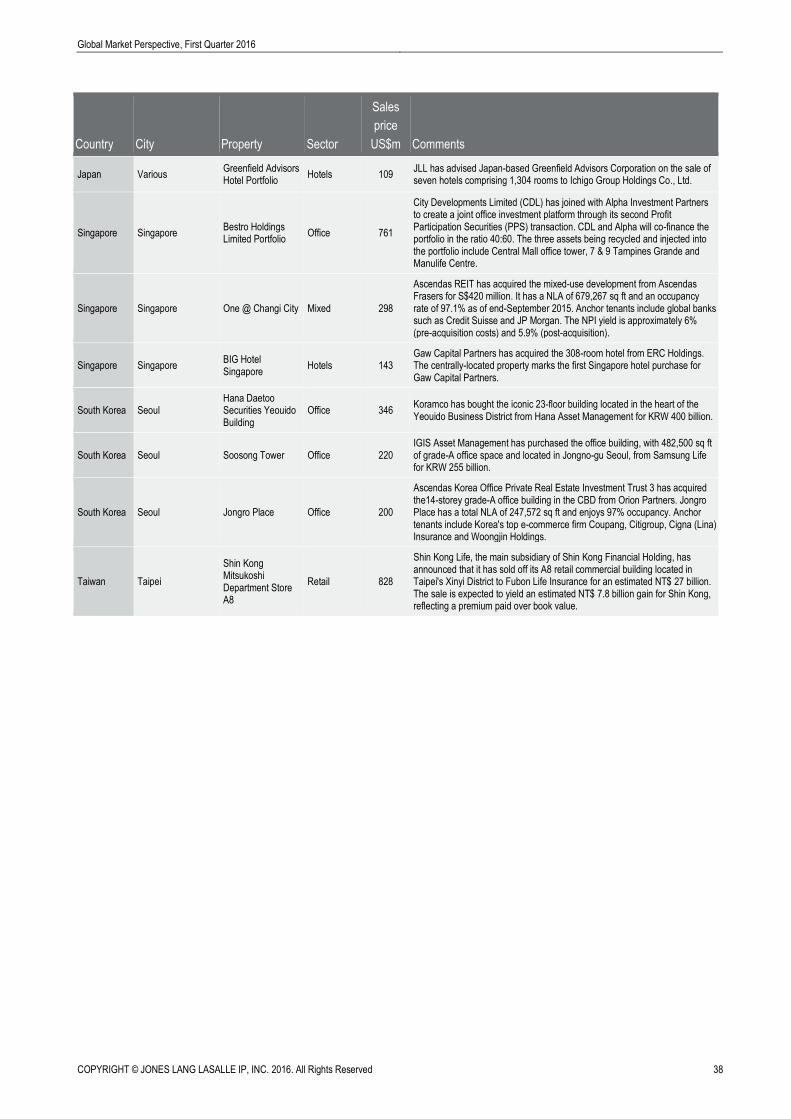

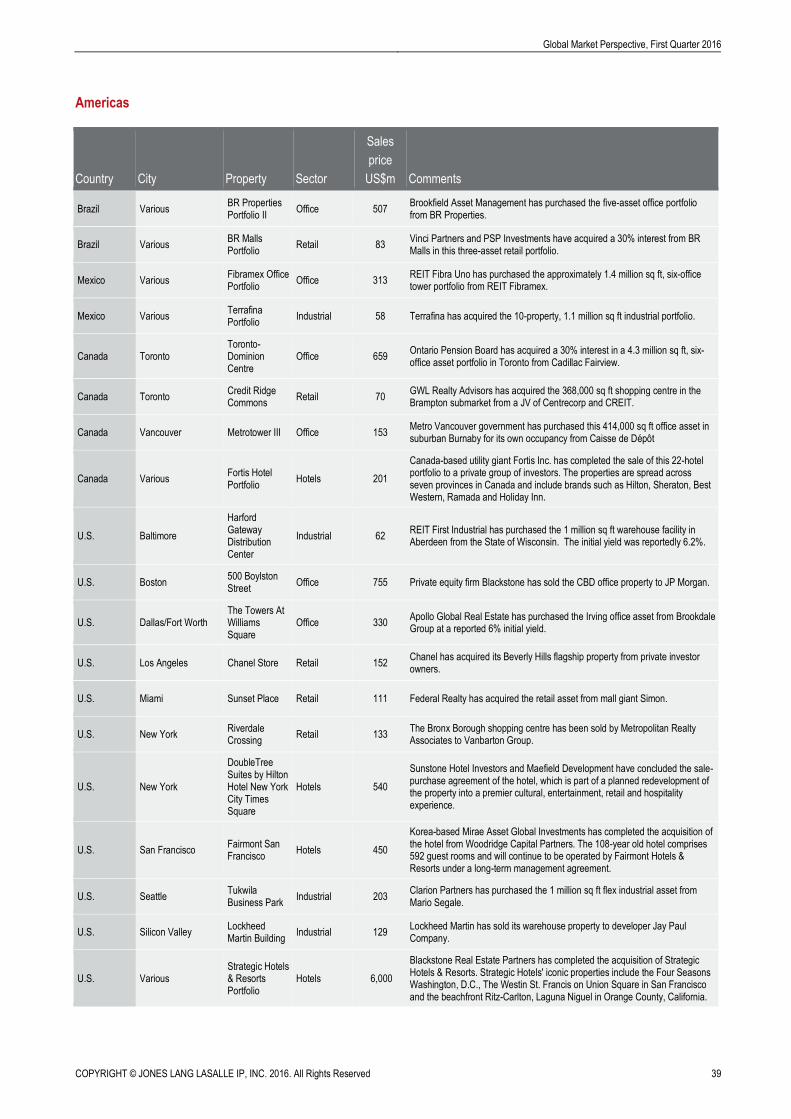

Key Investment Transactions in Q4 2015 ..................................................................................................................... 36

Illustrative Office Occupational Transactions in Q4 2015 ........................................................................................... 40

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 3

Corporates in Growth Mode Despite Global Headwinds

The occupational markets take the driving seat

JLL’s Global Market Perspective has chronicled the journey of the world’s dominant real estate markets since the

depths of the Great Recession in 2008, a journey that has been led throughout by strengthening investment markets as

a huge weight of money targets real estate assets. But, as we move into 2016, the dynamics have started to shift, with

the occupational markets now registering greater momentum. Market fundamentals are improving across all major

global regions and property sectors, and recent leasing activity has surprised on the upside. Geopolitical and economic

headwinds will weigh on business activity over the coming months, but for now, corporate occupiers remain in growth

mode which, combined with tightening supply, will support rental value growth during 2016 in most major markets.

Global Investment and Leasing Markets

Year-on-year change. Leasing volumes relate to offices

Source: JLL, February 2016

Investor activity slows in final quarter of 2015 as headwinds stiffen

Meanwhile, the pace of investment into commercial properties globally slowed slightly in the final quarter of 2015,

alongside other asset classes. Full-year 2015 transaction volumes, at US$704 billion, were just shy of 2014 levels, but

the strength of the U.S. dollar has underplayed the true level of market activity. At fixed exchange rates, full-year

volumes would be US$765 billion, 8% ahead of 2014 and a new record, surpassing the previous peak of US$758 billion

in 2007.

As we move into 2016, investor sentiment seems to be more cautious, with a combination of global economic and

political uncertainty, six years of consistent transactional growth, a turning credit cycle and record-high pricing in many

core markets making decisions more challenging. However, there is certainly no sign of investors pulling back in any

drastic way and yields continue to compress to new lows; rather we should expect growth from these levels to be more

measured. It should be remembered that globally we are at near peak levels and it is only currency fluctuations holding

the market back. With this backdrop we forecast 2016 volumes to be broadly in line with 2015 at between US$720-730

billion, with any potential upside (0%-5%) coming from the deployment of the significant capital from numerous sources

still to be allocated to the sector.

Investment Leasing

2015

2016

2014

0-5% +5%

-1% +8%

+21% +1%

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 4

Global Market Perspective, First Quarter 2016

Direct Commercial Real Estate Investment, 2006-2015

Source: JLL, February 2016

Office leasing volumes exceed expectations

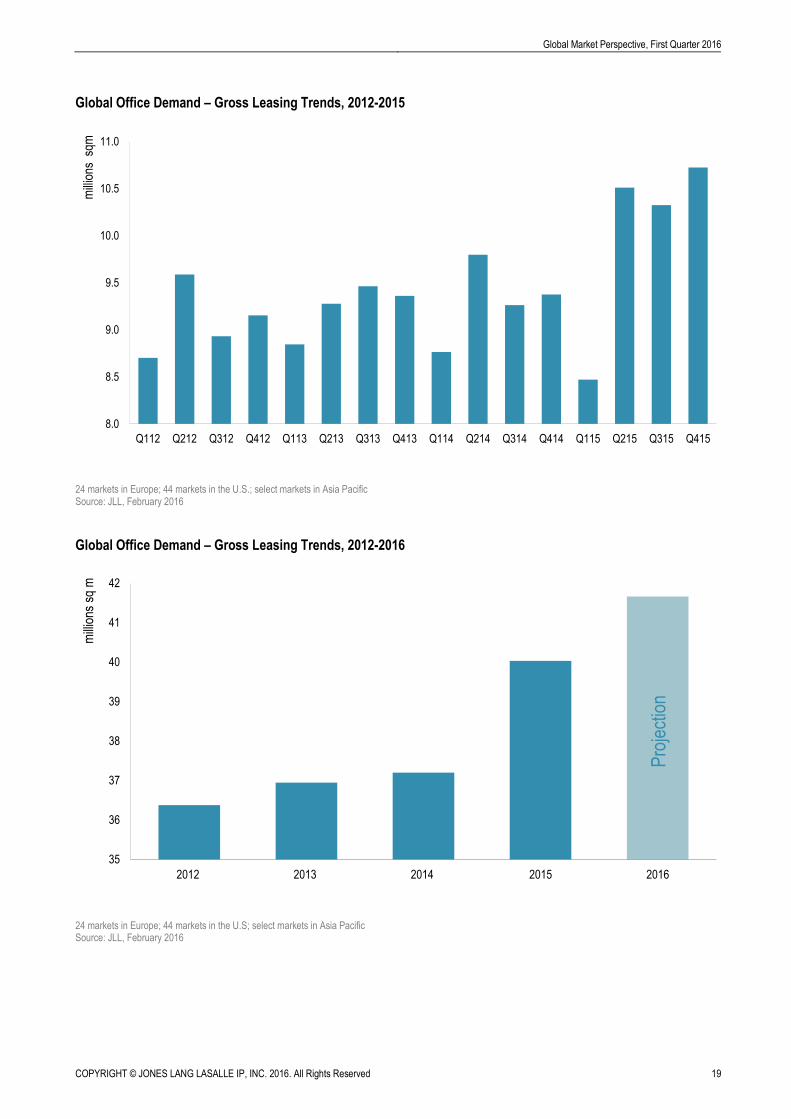

Global office leasing volumes in the final quarter of 2015 were 14% higher year-on-year and, as a result, full-year

volumes exceeded expectations, registering 8% growth on 2014 levels. The Asia Pacific region has seen a strong

rebound, with its full-year 2015 leasing volumes 19% higher. Leasing activity has also been notably robust in Europe,

posting 13% growth in 2015. Meanwhile, the U.S. has maintained its robust leasing activity, with nearly half of volumes

comprising expansion demand.

Demand for offices has been healthiest in innovation-oriented economies such as Boston, Berlin and Bangalore – but

is also extending to a more diversified range of cities. Despite the much documented slowdown in the China economy,

leasing activity has been remarkably buoyant in Shanghai and Beijing. India (and notably Delhi) has also posted high

levels of activity.

Notwithstanding the geopolitical concerns, there will continue to be progress towards expansion demand during 2016 as

tenants move away from cost containment, consolidation and renewals. As a consequence, global office leasing

volumes are projected to be around 5% higher than 2015, with Asia Pacific recording the strongest uplift over the year.

Tightening office supply supporting rental growth

Another 20 basis points were shaved off the global office vacancy rate in Q4, which stood at 12.1% at the end of 2015.

A further fall is in prospect during 2016, particularly in the U.S. and Europe. With a modest increase in new deliveries

expected in 2016 and 2017, the global vacancy rate is projected to settle at around 12% during the next two years.

Rental growth on prime office assets accelerated during the second half of 2015 as supply tightened and demand

strengthened. Growth of 3.7% was recorded for the full-year (across 26 major markets), matching the levels of 2014.

Further rental uplifts of 3%-4% across major markets are anticipated for 2016, with Boston and Tokyo vying for the top

positions.

0

100

200

300

400

500

600

700

800

Americas EMEA Asia Pacific Global

US

$ bi

llion

s

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 (F)

xx%

~5%

~0%

5-10%

0-5%

Projected Change, 2015-2016

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 5

Global Office Demand – Gross Leasing Trends, 2012-2016

24 markets in Europe; 44 markets in the U.S; select markets in Asia Pacific Source: JLL, February 2016

Consumer optimism boosts retail sales

Improved consumer confidence and healthy retail sales are fuelling optimism in the U.S., Europe and selectively in Asia

Pacific. Several U.S. markets, primarily gateway cities, are now witnessing conditions typical of a peaking market as

rents see assertive growth and vacancy continues to compress. Meanwhile, UK regional markets and Berlin

experienced the strongest rental growth over the year’s final quarter in Europe, while increases were also recorded in the

recovery markets of Italy and Spain. In Asia Pacific the demand picture remains varied, with the acceleration in retail

spending in Australia contributing to leasing demand, although rental growth has been limited in most regional markets

over the quarter.

Technology and realignment of logistics networks heightens demand

The ongoing robust growth in online sales and the wider impact of technology trends are driving the need for realignment

of supply chain networks and boosting global warehousing demand. In the U.S., absorption is still outpacing new supply

with continued velocity likely across nearly every market in 2016. Similarly, sustained strong occupier demand in Europe

resulted in record take-up volumes in 2015. In Asia Pacific, third-party logistics companies and e-commerce retailers are

bolstering rental levels in China and Tokyo.

Robust growth in global hotel investment

2015 marked the second-highest year on record for hotel transactions globally, with trades topping US$86 billion and

posting 50% growth on 2014. With 2015 surpassing all expectations in terms of the amount of capital flowing into the

hotel sector, we expect transaction volumes in 2016 to reach US$70 billion, marking the second-highest level of the

cycle.

Unprecedented vitality in U.S. rental apartments

Rental apartments are still outperforming in the U.S., with rental growth accelerating to its highest pace this cycle and all

major markets registering positive absorption. Institutional investment volumes continue to grow in Europe, with

Germany achieving a record year for transaction volumes and the UK market expected to gather speed through 2016.

Sales activity has continued to decline in Dubai, although falls in prices have been modest. In Asia, an accommodative

policy stance, including a cut in interest rates, has provided support for high-end sales volumes in China.

35

36

37

38

39

40

41

42

2012 2013 2014 2015 2016

mill

ions

sq

m

Pro

ject

ion

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 6

Global Market Perspective, First Quarter 2016

Global Economy

Global headwinds return in early 2016

Despite fairly upbeat expectations 12 months ago, 2015 marked a continuation of a relatively disappointing global growth

trend stretching back from 2011 rather than the anticipated lift-off. There were brighter spots, as lower oil prices helped

to revive domestic demand in many of the developed economies. But the outlook deteriorated through 2015, largely

because of worsening prospects in the key emerging markets and the start of 2016 has been a time of heightened

anxiety as plunging equity prices signalled a lurch into bear market territory for the first time since the financial crisis.

China worries have been one of the primary causes as poor sentiment figures and sharp declines on its stock markets

rekindled concerns about the pace of economic slowdown. Despite this, China was the only one of our major markets to

see a forecast upgrade since the last quarter. However, this was in part due to stronger-than-expected demand in late

2015, and unease remains about negative spillovers to emerging markets from the world’s second largest economy.

Even so, these have yet to impact in India, where growth is forecast to stay above 7%, driving Asian activity for a

second consecutive year.

Meanwhile, the developed economies received another fillip in the New Year, as geopolitical rumblings sent oil prices

tumbling below US$30pb. This positive shock to incomes and inflation has been particularly helpful for the recovery in

Europe, where growth reached a four-year high last year. Recent downgrades to the outlook for the Eurozone are

modest and a consequence of the weaker external environment. Although the UK continues to perform well, concerns

about momentum have grown and reflect softer post-election data, Brexit uncertainties and worries about the underlying

balance of recovery.

Elsewhere, U.S. growth expectations have been edged down slightly following less buoyant data in late 2015, even as

the Fed announced its first interest rate rise in almost a decade. Nevertheless, the U.S. remains the most dynamic of

the larger developed economies, with GDP set to rise by 2.6% this year. By contrast, Japan’s economy still disappoints.

After 0.7% growth during 2015, this year’s forecast has been sharply downgraded to 1.2% as sluggish domestic demand

in Japan continues to undermine prospects.

GDP Projections for 2016 in Major Economies – Recent Movements

Australia China France Germany India Japan UK U.S.

October 2015 2.8 5.9 1.7 2.2 7.5 1.8 2.6 2.8

January (Latest) 2.7 6.3 1.5 2.2 7.4 1.2 2.4 2.6

Change (bps) -10 +40 -20 0 -10 -60 -20 -20 Source: Oxford Economics, January 2016

Fed signals the upturn in the global cycle, but few will follow in 2016

The decision to raise the U.S. Federal Funds rates by 25 basis points on 16 December ended months of feverish

speculation. This was a historic move, arriving nine years after the previous hike and ending an unprecedented period

of stable rates globally. Early market reaction was favourable after clear signalling by the authorities. The decision was

based on the confidence about the robustness of the economic recovery and concerns that the tightening of labour

markets will threaten inflation further out.

It appears that the Fed’s move will mark a temporary divergence in Central Bank policy. This difference in part reflects

varying speeds of economic recovery and inflation rates. Of the other major Central Banks, none look set to follow in the

short term. Japan is expected to maintain its zero rate stance for the foreseeable future, while the ECB recently

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 7

extended its special liquidity programme and is unlikely to consider rate rises much before 2017. Even the Bank of

England has back-pedalled on previously bullish rate talk. With subdued domestic inflation, the market expectation is

now that the UK will not tighten before the end of 2016, at the earliest.

Global demand lift-off in 2016

As noted earlier, the global economy has been stuck in a low-growth rut almost since the turn of the decade and 2015

was no exception. The building contribution from the advanced economies over recent years brought hope that growth

would accelerate (albeit slowly), but this has been thwarted by the reversal in emerging market fortunes. The latest

forecasts now show a steadily improving profile for world growth over the next two years, as demand in both emerging

and developed economies picks up, though short-term risks will persist especially in the developing world.

Asia Pacific is expected to maintain its position as the fastest-growing region globally, but underlying this will be some

important shifts. Active policy is likely to avert a hard landing in China, though the long-established deceleration is

forecast to take growth rates down towards 6% by 2017. As a result, India will consolidate its position as the fastest-

growing Asian market over the medium term, though downside risks will re-emerge if there is any loss of momentum in

the reform process. In contrast, Japan’s economy has been hurt by slowing exports and sluggish domestic demand.

Further stimulus should lift growth from its 2015 lows, but upside potential is limited with growth rates stalling at 1%.

The most recent demand data in the United States were slightly disappointing and 2015 estimates have edged lower.

But the revival in consumer demand and healthy labour markets in the U.S. are expected to sustain performance over

the next two years against the challenges of external headwinds and a gradually tightening monetary stance. Although

slightly below-par by pre-crisis standards, annual U.S. growth forecasts are predicted to outpace those of most

competitor economies across the developed world.

The European recovery has been one of the more encouraging global trends of the last year or so, especially the

increasing resilience of domestic demand in the Eurozone. In the single currency area, the stately recovery is projected

to continue into this year, with Germany leading in the core and France reviving more gradually. The most dynamic

performance will remain on the fringes, however, notably in Spain and Ireland. Outside the Eurozone, the UK economy

had a slightly disappointing 2015 with growth becoming uneven in recent quarters. This is seen as a temporary dip and

output is forecast to rise by 2.4% during 2016, provided any Brexit uncertainty is contained.

Global Outlook, GDP Change, 2015-2017

2015 2016 2017

Global 3.0 3.4 3.7

Asia Pacific 5.3 5.3 5.3

Australia 2.4 2.7 2.9

China 6.9 6.3 6.0

India 7.4 7.4 7.2

Japan 0.7 1.2 1.2

Americas 1.4 1.8 2.5

U.S. 2.5 2.6 2.6

MENA 2.2 2.7 3.3

Europe 2.0 2.1 2.2

France 1.2 1.5 1.7

Germany 1.5 2.2 1.9

UK 2.2 2.4 2.5 Source: Oxford Economics, January 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 8

Global Market Perspective, First Quarter 2016

Real Estate Capital Markets

Investment Volumes

Final quarter disappoints as headwinds stiffen into 2016

Alongside other asset classes in the final quarter of 2015, the pace of investment into commercial properties globally

slowed slightly compared to a year ago. There has also been a noticeable shift in investor sentiment, particularly for

fully-priced core assets, where the number of genuine buyers has dwindled. Transactional activity in the fourth quarter

was US$209 billion, 8% lower than the record final quarter of 2014. However, full-year volumes have only been

marginally affected, with 2015 totalling US$704 billion, just 1% below 2014. The strength of the U.S. dollar continues to

underplay the true level of market activity; with fixed exchange rates, full-year volumes would be US$765 billion, 8%

ahead of 2014 and a new record, surpassing the previous peak of US$758 billion in 2007.

Real estate remains a force as the Fed awakens

Despite a pullback in the global numbers, the Americas region as a whole set a new transactional record in 2015,

although some momentum was lost in the final quarter where US$85 billion was transacted, 9% below a year ago. This

brought full-year activity to US$314 billion, 4% above 2014 and ahead of the 2007 previous peak of US$304 billion. All

of the outperformance came from the U.S. where activity was 9% ahead of 2014 at US$294 billion, itself a new record.

Elsewhere, the volatile nature of commodity-driven and emerging market economies was demonstrated with volumes

lower in each and every other market we track, Canada being the best of the rest with volumes 21% lower.

European outperformance united, despite growing list of problems to diverge performance

While in U.S. dollar terms European volumes were 4% lower in 2015 at US$267 billion, in local currency they were much

more buoyant with 14% growth over 2014 levels. The final quarter of the year once again proved to be pivotal; volumes

stood 12% higher than Q4 2014, setting a new record of €81 billion, with Germany and the Nordics being the standout

markets.

Greater China real estate markets seem to welcome the volatility

Asia Pacific full-year volumes were 6% lower than 2014 at US$124 billion with the final quarter 19% down on a year ago.

However, it was a mixed picture across the region with weaker currencies in Japan and Australia playing a part.

Despite increased capital market and political volatility, China, Hong Kong and Taiwan bounced back strongly from

2014 with volumes up 47%, 66% and 18% respectively.

Risks look to be on the downside as the New Year starts

The final quarter of 2015 was characterised by a slight moderation in investment activity globally, albeit from the record

highs of Q4 2014. As we move into 2016, investor sentiment seems to be more cautious with a combination of

economic and political uncertainty, six years of consistent transactional growth, a turning credit cycle and record-high

pricing in many core markets making decisions more challenging. However, there is certainly no sign of investors pulling

back; rather we should anticipate growth from these levels to be more measured. With this backdrop, we expect 2016

global volumes to be broadly in line with 2015 at between US$720-730 billion, with any potential upside (0%-5%) coming

from the deployment of the significant capital from numerous sources still to be allocated to the sector.

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 9

Direct Commercial Real Estate Investment – Regional Volumes, 2014-2015

Source: JLL, February 2016

Direct Commercial Real Estate Investment – Largest Markets, 2014-2015

Source: JLL, February 2016

REGIONS IN FOCUS

New record volumes for Americas in 2015

The Americas set a new high-water mark in total transaction volumes in 2015. Total volumes in the fourth quarter

reached US$85 billion, up 12% on the third quarter, although down 9% from the frenetic pace of the fourth quarter of

2014. Indeed, the forward growth in deal activity decelerated over the course of the year as investors digested the

tremendous uplift in volumes and pricing to-date this cycle. Still, the Americas did soar to a new annual record

transaction volume of US$314 billion for 2015, an increase of 4% over 2014 and above the historical record-high

reached in 2007. Given the continuing momentum in the asset class, and sustained strong and diverse investor

demand, we forecast that total volumes will grow by 5%-10% in the Americas region overall in 2016.

US$ Billions Q3 15 Q4 15

% change

Q3 15-Q4 15 Q4 14

% change

Q4 14-Q4 15 2014 2015

% change

2014-2015

Americas 76 85 12% 94 -9% 302 314 4%

EMEA 65 89 38% 91 -2% 278 267 -4%

Asia Pacific 32 36 11% 44 -19% 131 124 -6%

TOTAL 173 209 21% 228 -8% 711 704 -1%

TOTAL Fixed FX 188 223 19% 228 -2% 711 765 8%

US$ Billions Q3 15 Q4 15

% change

Q3 15-Q4 15 Q4 14

% change

Q4 14-Q4 15 2014 2015

% change

2014-2015

U.S. 70.6 77.8 10% 85.4 -9% 269.1 293.7 9%

UK 20.8 27.7 33% 34.0 -19% 106.9 95.3 -11%

Germany 14.6 17.4 19% 16.5 5% 46.3 52.7 14%

France 9.0 10.7 19% 11.4 -6% 33.1 27.9 -16%

China 7.3 10.5 44% 7.0 49% 19.2 28.3 47%

Australia 7.8 6.2 -21% 7.9 -22% 26.8 21.1 -21%

Japan 8.9 5.8 -35% 14.8 -61% 43.4 34.0 -22%

Canada 4.4 5.0 14% 6.7 -26% 19.0 15.1 -21%

Hong Kong 2.7 4.5 67% 2.2 106% 7.2 12.0 66%

Norway 0.7 4.4 562% 2.3 88% 6.2 9.5 54%

Italy 1.7 3.6 104% 3.2 12% 7.0 9.2 31%

Netherlands 1.4 3.5 142% 2.9 21% 9.5 8.1 -14%

Sweden 3.0 3.4 15% 4.6 -26% 13.9 11.1 -20%

Spain 2.9 2.9 3% 3.0 -2% 9.7 10.6 9%

South Korea 1.8 2.3 25% 4.9 -53% 10.8 8.0 -26%

Taiwan 0.4 2.2 420% 0.9 150% 3.2 3.8 18%

Poland 1.0 2.2 118% 1.6 42% 4.3 4.2 -2%

Austria 0.3 2.0 638% 1.0 105% 3.6 2.5 -31%

Switzerland 0.5 1.9 240% 1.0 83% 3.1 4.3 38%

Singapore 1.3 1.9 41% 1.2 55% 8.1 7.0 -13%

Finland 0.9 1.8 103% 0.9 113% 2.9 4.5 53%

Belgium 1.8 1.6 -16% 1.5 1% 4.1 5.3 27%

Ireland 1.3 1.4 8% 1.6 -11% 5.4 4.5 -17%

New Zealand 0.6 1.1 91% 1.9 -39% 4.5 2.7 -39%

Mexico 0.4 1.1 191% 0.8 42% 7.5 2.4 -68%

Brazil 0.6 1.1 90% 0.8 32% 5.7 2.5 -55%

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 10

Global Market Perspective, First Quarter 2016

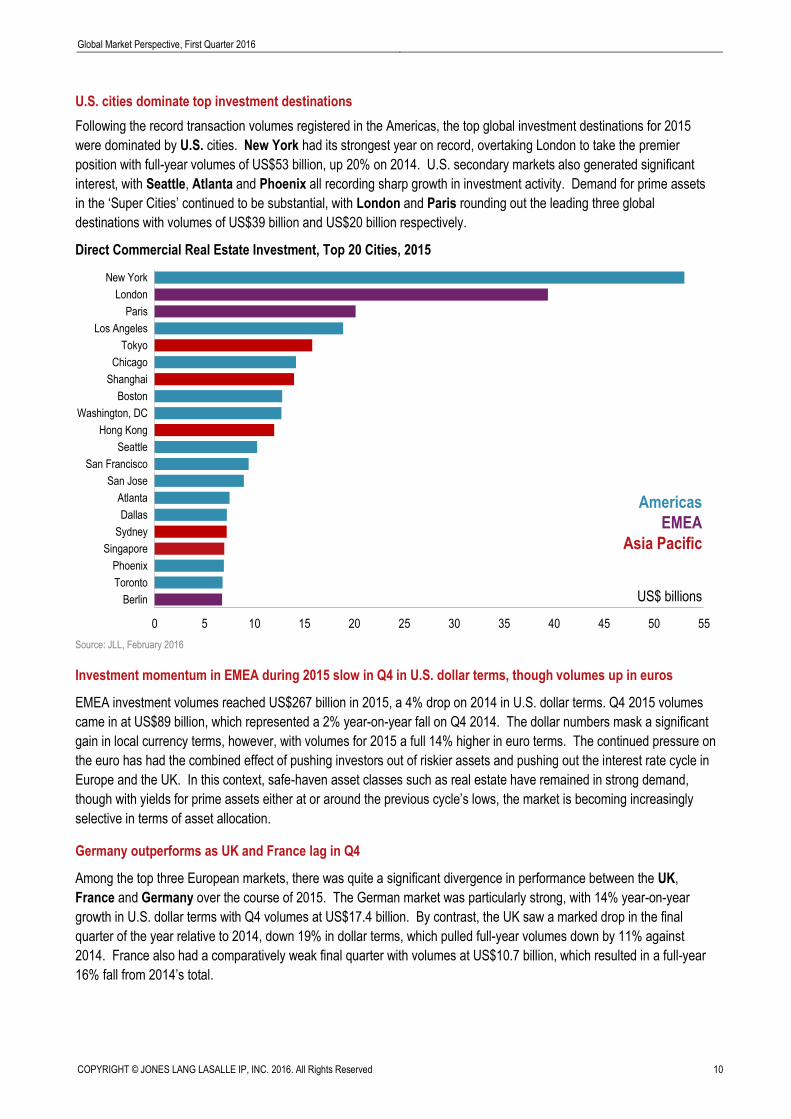

U.S. cities dominate top investment destinations

Following the record transaction volumes registered in the Americas, the top global investment destinations for 2015

were dominated by U.S. cities. New York had its strongest year on record, overtaking London to take the premier

position with full-year volumes of US$53 billion, up 20% on 2014. U.S. secondary markets also generated significant

interest, with Seattle, Atlanta and Phoenix all recording sharp growth in investment activity. Demand for prime assets

in the ‘Super Cities’ continued to be substantial, with London and Paris rounding out the leading three global

destinations with volumes of US$39 billion and US$20 billion respectively.

Direct Commercial Real Estate Investment, Top 20 Cities, 2015

Source: JLL, February 2016

Investment momentum in EMEA during 2015 slow in Q4 in U.S. dollar terms, though volumes up in euros

EMEA investment volumes reached US$267 billion in 2015, a 4% drop on 2014 in U.S. dollar terms. Q4 2015 volumes

came in at US$89 billion, which represented a 2% year-on-year fall on Q4 2014. The dollar numbers mask a significant

gain in local currency terms, however, with volumes for 2015 a full 14% higher in euro terms. The continued pressure on

the euro has had the combined effect of pushing investors out of riskier assets and pushing out the interest rate cycle in

Europe and the UK. In this context, safe-haven asset classes such as real estate have remained in strong demand,

though with yields for prime assets either at or around the previous cycle’s lows, the market is becoming increasingly

selective in terms of asset allocation.

Germany outperforms as UK and France lag in Q4

Among the top three European markets, there was quite a significant divergence in performance between the UK,

France and Germany over the course of 2015. The German market was particularly strong, with 14% year-on-year

growth in U.S. dollar terms with Q4 volumes at US$17.4 billion. By contrast, the UK saw a marked drop in the final

quarter of the year relative to 2014, down 19% in dollar terms, which pulled full-year volumes down by 11% against

2014. France also had a comparatively weak final quarter with volumes at US$10.7 billion, which resulted in a full-year

16% fall from 2014’s total.

0 5 10 15 20 25 30 35 40 45 50 55

Berlin

Toronto

Phoenix

Singapore

Sydney

Dallas

Atlanta

San Jose

San Francisco

Seattle

Hong Kong

Washington, DC

Boston

Shanghai

Chicago

Tokyo

Los Angeles

Paris

London

New York

Americas

EMEA

Asia Pacific

US$ billions

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 11

Gains for Nordics and Southern Europe, while Benelux flat

The momentum that slipped in the Nordic region during Q3 2015 returned with force in the final quarter with

US$10.1 billion of investment transactions. This reflects a quarter-on-quarter pick up of 83% across the region, largely

due to a 562% increase in Norway. Meanwhile, investment in Southern Europe was up 18% in U.S. dollar terms for

2015, with US$20.1 billion of investment over the year (the key growth markets being Portugal and Italy). In the

Benelux countries, volumes in dollar terms were lower for the full year by 3%, although the region saw a pickup in euro

terms of 16% with €13.1 billion of investment.

Asia Pacific full-year 2015 investment volumes continue to climb in local currency terms

Investment volumes across Asia Pacific’s commercial real estate markets finished the full-year 2015 slightly down (by

6% year-on-year) at US$124 billion. This is largely in line with our revised full-year estimate of US$125 billion, which

took into consideration the strength of the U.S. dollar. In local currency terms, investment volumes continue to climb as

the weight of capital allocated to investing in real estate within the region remains high. Cross-border investors

maintained their activity on both sides of the ledger in Q4 2015, accounting for 39% of total investment volumes.

Although the year has started with renewed volatility in the global financial markets, we are confident that investment

volumes across Asia Pacific will remain stable this year as more institutional investors look towards multi-asset portfolios

in light of subdued performance across traditional asset classes such as equities and fixed income. Hence, we forecast

growth of 5% year-on-year to US$130 billion in 2016. The start of U.S. interest rate normalisation could see assets trade,

with cyclical investors taking profits and long-term income-seeking investors taking new positions as yield spreads over

benchmark rates continue to be attractive in some markets.

Foreign investor interest remains high in Australia and Japan

Investment volumes in Australia reached US$6.2 billion in the final quarter of 2015, down 22% year-on-year. Full-year

volumes fell 21%, on the back of a record 2014 and weakness in the Australian dollar. Cross-border purchasers were

active throughout Q4 2015, accounting for 54% of deals by volume. In Japan, J-REITs transaction volumes for Q4 were

much lower than the first three quarters, with the weak finish pushing full-year 2015 volumes down 22% year-on-year to

US$34 billion. We anticipate that international investor demand will buoy transaction volumes in 2016, supported by a

competitive exchange rate, the low cost of borrowing and a good yield spread.

China closed a record 2015 year with US$28 billion worth of deals

Despite the macro headlines, transaction volumes in China closed the year robustly, reaching US$10.5 billion in Q4, up

49% year-on-year. Although equities and the renminbi were under pressure, the real estate investment market

rebounded strongly, driven by domestic corporates and financial institutions as well as foreign PERE funds. Looking

ahead, we do not foresee any shortage of fund availability as domestic players should remain active.

Hong Kong and Singapore end year strongly, while India falls on lack of availability of quality assets

Hong Kong’s investment activity in Q4 2015 doubled on a year-on-year basis to US$4.5 billion, with full-year volumes

up 66% to US$12 billion, led by Chinese investors looking to invest offshore. Singapore also ended 2015 on a strong

note with investment volumes in Q4 up 55% year-on-year at US$1.9 billion, although full-year volumes were down 13%

to US$7 billion amid weak real estate fundamentals. Elsewhere, India’s transaction volumes fell 81% year-on-year to

only US$0.2 billion due to a lack of quality assets available.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 12

Global Market Perspective, First Quarter 2016

Direct Commercial Real Estate Investment – Quarterly Trends, 2007-2015

Source: JLL, February 2016

Prime Office Yield Shift, 2014-2015

Source: JLL, February 2016

0

30

60

90

120

150

180

210

240Q

107

Q20

7

Q30

7

Q40

7

Q10

8

Q20

8

Q30

8

Q40

8

Q10

9

Q20

9

Q30

9

Q40

9

Q11

0

Q21

0

Q31

0

Q41

0

Q11

1

Q21

1

Q31

1

Q41

1

Q11

2

Q21

2

Q31

2

Q41

2

Q11

3

Q21

3

Q31

3

Q41

3

Q11

4

Q21

4

Q31

4

Q41

4

Q11

5

Q21

5

Q31

5

Q41

5

Americas EMEA Asia Pacific Rolling Four-Quarter Average

US

$ bi

llion

s

205

107110100

113

7369666666

100

118120

159

204

190

119

91

110100

163

41 4335

108

124

146

211

143

166174

228

154

168173

209

-100 -50 0 50

TokyoSydney

SingaporeShanghai

SeoulMumbai

Hong KongBeijing

Mexico CitySao Paulo

Washington DCToronto

San FranciscoNew York

Los AngelesChicagoBoston

StockholmParis

MoscowMilan

MadridLondon

FrankfurtBrussels

Q3 2015 - Q4 2015

Q4 2014 - Q3 2015

Basis point change

Am

eric

asE

uro

pe

Asi

a P

acif

ic

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 13

Capital Values and Yields

Further yield compression

Robust demand for core assets compressed yields yet further during Q4 2015. The mean prime office yield (across 21

major office markets) stood at 4.83% in the fourth quarter, a fall of 200 basis points since mid-2009. Sydney and

Brussels registered 15-25 basis points’ compression during Q4, while Tokyo’s yields came in another 10 basis points to

stand at a low of 3.0%. With more solid market fundamentals and high levels of unplaced capital, prime yields could

tighten further during 2016, although our projections indicate a broadly flat trend in yields during 2016.

Capital appreciation expected to slow in 2016

Capital value appreciation on prime assets (across 26 markets) stood at 8.5% in 2015, broadly matching the levels of

2014. Strongest year-on-year growth was recorded in Madrid, Stockholm, Sydney and Tokyo.

Annual capital appreciation is expected to slow to about 4% in 2016, driven primarily by income growth. Star capital

value performers in 2016 are likely to be the Boston, Madrid, Brussels, Tokyo and Shanghai office markets.

Prime Office Yields, 2007-2015

*Across 21 Major Office Markets

Source: JLL, February 2016

-30

-10

10

30

50

70

Q12007

Q22007

Q32007

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Yield Compression (bps)

4.8

5.2

5.6

6.0

6.4

6.8

7.2

Mean Prime Office Yields*

5.44%

4.83%

%

bps

6.83%

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 14

Global Market Perspective, First Quarter 2016

Corporate Occupiers

Occupier expansion despite geopolitical concerns

In the context of the increased financial market volatility and rising geopolitical risks that have marked the start of 2016,

recent surveys have highlighted executives’ concerns over the geopolitical instability and security issues – this will

continue to weigh heavily on corporates over the coming months. Nonetheless, at least for now, corporate occupiers

remain in growth mode across the majority of global markets. JLL’s corporate sentiment surveys reveal little sign of any

slowing in the robust and broad-based growth of occupier leasing activity.

‘Access to talent’ driving location strategy

‘Access to talent’ is increasingly driving corporate real estate and location strategy, with corporate occupiers becoming

far more forensic in their analysis of talent clusters. In the U.S., many companies are making greater efforts to align

location strategy with the future talent requirements of their businesses, with downtown and urban submarkets the most

desired locations as companies pursue millennial talent and renewed corporate energy.

In Asia Pacific, where proximity is often key to employee retention, tech companies are more and more occupying

traditional CBD premises which were formerly occupied by the financial community. Well-connected locations that are

close to amenities and talent are also seeing competition for space intensifying more rapidly in Europe, as portfolio

optimisation continues unabated and companies seek to better align location strategies with talent clusters. High-quality

space options remain constrained in many markets, and this increased pressure on availability is driving occupier

mobility, which is likely to become more widespread over 2016.

M&A resulting in portfolio disruption

Mergers and acquisitions continue to cause churn and change in corporate portfolios. With cross-border M&A activity at

record levels in 2015, a growing number of companies are seeing disruption of their real estate portfolios. With

divestments also at record highs, expansionary activity will continue to be matched with restructuring and disposals.

Technology reshaping real estate

Technology and the future of work are further factors reshaping occupier demand for real estate. The ubiquity of digital

technology is having a profound impact on real estate, with the weighting of tech and media companies and disruptive

digital industries dramatically increasing across global office markets. In the U.S., tech companies accounted for 20% of

all office leasing in 2015, more than all government, insurance and consulting firms combined. The expansion of tech

and digital industry companies is also occurring rapidly in Asia Pacific, with major U.S. entities finding their Asian

equivalents such as Flipkart (India’s Amazon) to be even more aggressive.

Flexible working solutions expanding rapidly

Digitisation and emerging technologies are also paving the way for more flexible working solutions, with corporate

adoption of co-working, an increased focus on user experience and productivity dominating workplace discussions. Co-

working is now the fastest-growing segment of the leasing market in many U.S. cities; in 2005 there was only one co-

working space nationally, while today there are over 3,000. This trend is exemplified by companies such as WeWork,

which was founded in 2010 and now has 61 locations in 18 cities. Co-working companies are now appearing in other

regions and are looking for significant space in the key cities; however, rapid growth in this space is leading some to

question its sustainability. More broadly, digitisation and emerging technology is poised to impact building design and

function, CRE strategy and ultimately real estate requirements.

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 15

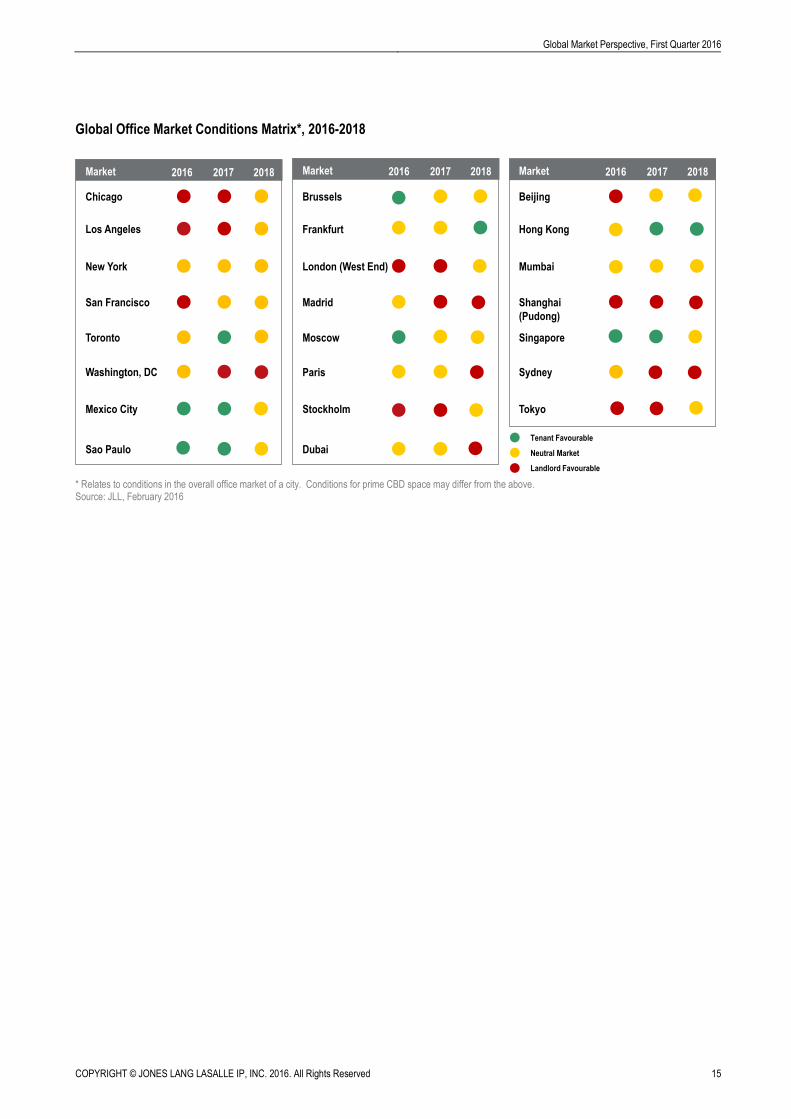

Global Office Market Conditions Matrix*, 2016-2018

* Relates to conditions in the overall office market of a city. Conditions for prime CBD space may differ from the above. Source: JLL, February 2016

MARKET

Brussels Beijing

Frankfurt Hong Kong

London (West End) Mumbai

Madrid Shanghai

(Pudong)

Moscow Singapore

Paris Sydney

Stockholm

Dubai

Market 2016 2017 2018 Market 2016 2017 2018

Tokyo

Neutral Market

Landlord Favourable

Tenant Favourable

Market

Chicago

Los Angeles

New York

San Francisco

Toronto

Washington, DC

Mexico City

Sao Paulo

2016 2017 2018

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 16

Global Market Perspective, First Quarter 2016

Global Real Estate Health Monitor

Economy Real Estate Investment Markets Real Estate Occupier Markets

Metro

Area

GDP

OECD

Leading

Indicator

City

Investment

Volumes

Capital

Value

Change

Prime

Yield Yield Gap

Rental

Change

Net

Absorption

Vacancy

Rate

Supply

Pipeline

Beijing 7.1% -0.1 44% 3.7% 6.3% 351 3.7% 2.8% 2.7% 13.3%

Boston 2.9% -0.2 -13% 13.0% 3.8% 153 7.4% 1.8% 13.8% 3.2%

Chicago 2.6% -0.2 5% 8.3% 4.6% 153 3.7% 1.5% 15.0% 1.3%

Dubai 4.1% na 24% 15.4% 7.5% na 15.4% na 19.1% 8.3%

Frankfurt 2.2% -0.1 -6% 7.3% 4.4% 372 1.4% 0.2% 9.1% 2.1%

Hong Kong 2.5% na 66% 5.5% 3.1% 155 13.3% 3.3% 2.9% 4.4%

London 3.4% -0.2 -12% 11.8% 3.5% 154 4.3% 2.3% 3.4% 5.8%

Los Angeles 2.6% -0.2 8% 14.4% 4.2% 153 9.2% 1.4% 15.5% 1.0%

Madrid 3.2% 0 76% 25.7% 4.3% 247 6.9% 2.7% 10.6% 1.3%

Mexico City 3.4% -0.2 -92% -2.7% 7.5% 123 0.0% 8.0% 13.0% 18.0%

Milan 1.6% 0 258% 8.9% 4.5% 290 2.1% 0.9% 13.4% 2.4%

Moscow -1.5% -0.1 -4% -15.3% 10.5% 76 -11.1% 4.2% 16.9% 9.0%

Mumbai 7.4% 0.1 143% -0.7% 9.9% 197 -2.4% 7.0% 19.7% 14.4%

New York 2.8% -0.2 20% 9.1% 3.3% 153 2.9% 0.0% 9.6% 1.1%

Paris 1.7% 0.1 -10% 11.5% 3.3% 227 -3.4% -0.6% 7.4% 4.2%

San Francisco

3.0% -0.2 -25% 11.0% 3.4% 153 7.8% 2.9% 8.2% 3.9%

Sao Paulo -3.3% 0.1 -77% -7.8% 9.8% 260 -5.4% 5.1% 23.6% 13.6%

Seoul 2.8% 0 -20% 3.4% 4.6% 254 -1.0% 0.3% 11.0% 3.2%

Shanghai 6.1% -0.1 79% 12.9% 5.7% 351 9.4% 17.9% 9.5% 38.1%

Singapore 2.5% na -13% -4.4% 3.9% 128 -10.5% 1.8% 5.0% 11.4%

Stockholm 3.4% 0 -31% 22.8% 4.0% 301 15.6% 3.1% 7.1% 1.5%

Sydney 2.7% -0.1 -31% 19.9% 5.5% 254 13.0% 2.3% 8.4% 3.7%

Tokyo 2.0% -0.1 -48% 18.4% 3.0% 275 7.6% 4.9% 2.0% 9.2%

Toronto 2.8% 0 -9% 12.7% 4.7% 331 3.8% 0.0% 9.7% 2.3%

Washington DC

2.7% -0.2 -7% 8.5% 4.1% 153 3.4% 0.4% 17.0% 1.5%

Real estate data as at end Q4 2015

Definitions and Sources

Metro Area GDP: Change in Real GDP. Metropolitan Area Projection, 2016. Source: Oxford Economics

OECD Leading Indicator: Composite Leading Indicator. Change in Index. Latest Month. Source: OECD

City Investment Volumes: Direct Commercial Real Estate Volumes. Metro Area Data. Rolling Annual Change. Source: JLL

Capital Value Change: Notional Prime Office Capital Values. Year-on-Year Change. Latest Quarter. Source: JLL

Prime Yield: Indicative Yield on Prime/Grade-A Offices. Latest Quarter. Source: JLL

Yield Gap: Basis Points that Prime Office Yields are above or below 10-year Government Bond Yields. Latest Quarter. Source: JLL, Datastream

Rental Change: Prime Office Rents. Year-on-Year Change. Latest Quarter. Source: JLL

Net Absorption: Annual Net Absorption as % of Occupied Office Stock. Rolling Annual. Source: JLL

Vacancy Rate: Metro Area Office Vacancy Rate. Latest Quarter. Source: JLL

Supply Pipeline: Metro Area Office Completions (2016-2017) as % of Existing Stock. Source: JLL

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 17

Office Markets

Office Demand Dynamics

Robust office market fundamentals

Office market fundamentals have continued to improve across all three global regions, with buoyant leasing activity and

tightening supply supporting solid rental growth. Global leasing volumes in the final quarter of 2015 were 14% higher

year-on-year and, as a result, full-year volumes exceeded expectations, registering 8% growth on 2014 levels. The Asia

Pacific region has seen a strong rebound, with its full-year volumes 19% higher. Leasing activity has also been

remarkably vigorous in Europe, posting 13% growth in 2015. Meanwhile, the U.S. has maintained its robust leasing

activity, with nearly half of volumes comprising expansion demand. Technology, banking and financial services and

outsourcing are the key drivers of demand.

Momentum builds into 2016

Despite global economic headwinds, there will continue to be progress towards expansion demand as tenants move

away from cost containment, consolidation and renewals. As a consequence, 2016 global office leasing volumes are

projected to be around 5% higher than 2015, with Asia Pacific likely to record the greatest uplift.

Innovation-oriented economies drive growth in the United States

At 1.7 million square metres in Q4, office net absorption in the United States was the highest of the current cycle, up

28% on Q3 2015. Strong expansion activity is concentrated in particular in the innovation-oriented economies of the

country’s West and Northeast Coasts. Even so, demand is now spreading into the U.S.’s Sunbelt Markets on the heels

of demographic, financial and professional business services’ growth:

Pricing and competition is encouraging tenants to look to markets like Atlanta, Charlotte, Dallas and Raleigh-

Durham.

Strongest occupancy gains in Q4 were found in Los Angeles, Phoenix, Boston and Philadelphia.

CBDs remain the premier location for tenants, but there is now a greater balance in demand between CBD and

suburban markets.

At the industry level, demand is firmly with technology and banking and financial services.

2016 is expected to be another year of strong demand, with increasing new supply providing large tenants with much

needed opportunities for expansion.

European office take-up in Q4 strongest since 2006

The acceleration in European leasing activity continued in Q4, with take-up totalling 3.6 million square metres. This

represents a 18% year-on-year increase and is the strongest fourth quarter since 2006. Virtually all major office markets

registered growth in 2015, underlining the positive momentum built through the year. We expect this upward movement

to be maintained into 2016 as a more widespread recovery takes hold:

European take-up was again boosted by robust activity in Paris, which saw a rebound in volumes after a

disappointing H1. Q4 take-up was 20% higher year-on-year on the back of a gradually improving economic

outlook in the city.

A buoyant Q4 capped off another stellar year for the Central London leasing market, propelling take-up to over

1.1 million square metres for the full-year 2015, up by 7% on 2014.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 18

Global Market Perspective, First Quarter 2016

Meanwhile, the office markets in Germany show no signs of slowing, with the combined take-up for the five

largest markets up 20% year-on-year in Q4. Berlin continues to be the front runner with full-year volumes up

43% on the previous record level of 2014. Leasing volumes across Germany are likely to stay robust in 2016.

In Southern Europe, sentiment also remained positive. Q4 2015 take-up in Madrid was up 42% year-on-year

and in Milan final quarter office leasing volumes were the strongest on record.

Other noteworthy performances in Q4 in terms of leasing volumes included Stockholm (+64% year-on-year)

and Amsterdam (+38%).

In cities such as London, Dublin, Berlin and Munich we have seen that constraints in the most sought-after locations

are forcing occupiers to widen their search to high-quality space in well-connected areas. This has caused demand to

spill over into secondary areas (often supporting rental growth in these submarkets). This increased occupier mobility is

likely to become more widespread across Western Europe during 2016.

Leasing activity continues to recover in Asia Pacific

Overall leasing activity in the fourth quarter improved strongly year-on-year in Asia Pacific on both a gross and net basis,

with technology, domestic financial firms and offshoring activity continuing to be key sources of demand. Net absorption

in Q4 across the region was up 38% year-on-year:

Vigorous demand has been recorded in India (particularly Delhi) and China (all Tier I markets). The Chinese

and Indian cities accounted for around two-thirds of Q4 net absorption in the region. Despite a slowing

economy, the Shanghai and Beijing leasing markets have been remarkably resilient with leasing volume

growth during 2015 of 48% as their service sectors expanded.

Manila was also very active, particularly driven by offshoring activity.

In Australia, leasing surged by a hefty 104%, led by the largest markets - Sydney and Melbourne.

Slow economic activity and weak commodity prices have impacted Southeast Asian markets.

Singapore, Kuala Lumpur and Seoul saw negative net absorption in Q4 2015.

Asia Pacific office leasing volumes in 2016 are forecast to increase by around 15% on 2015 levels, with similar demand

drivers as last year.

Tenant-friendly markets in Latin America

Office fundamentals are weaker throughout most major markets in Latin America:

Tenant demand is depressed in Sao Paulo, although leasing activity is likely to rise over the next few quarters

as demand for space is induced by the wide array of options and incentives available in an oversupplied

market.

Mexico City’s office market, on the other hand, has experienced more consistent and robust demand from

tenants. However, market leverage is expected to increasingly fall into the hands of tenants in 2016 as the

supply pipeline surges.

Demand stable in MENA markets

Cairo and Jeddah have been the strongest performing office markets in MENA over 2015, with Cairo continuing to

witness a movement of tenants from the central city to new suburban locations. The office markets in Dubai and Abu

Dhabi have kept relatively stable and are experiencing sustained demand for high-quality space.

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 19

Global Office Demand – Gross Leasing Trends, 2012-2015

24 markets in Europe; 44 markets in the U.S.; select markets in Asia Pacific Source: JLL, February 2016

Global Office Demand – Gross Leasing Trends, 2012-2016

24 markets in Europe; 44 markets in the U.S; select markets in Asia Pacific Source: JLL, February 2016

8.0

8.5

9.0

9.5

10.0

10.5

11.0

Q112 Q212 Q312 Q412 Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414 Q115 Q215 Q315 Q415

mill

ions

sqm

35

36

37

38

39

40

41

42

2012 2013 2014 2015 2016

mill

ions

sq

m

Pro

ject

ion

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 20

Global Market Perspective, First Quarter 2016

Office Supply Trends

Office Construction

Office supply pipeline under control

14.0 million square metres of new office space was delivered globally (across 93 major markets) during 2015, the

highest level since 2009 and representing a 29% increase on 2014. The market has nonetheless successfully absorbed

this additional new space and global vacancy rates have continued to decline.

New office deliveries during 2016-2018 are likely to range between 15-16 million square metres per year, well below the

previous development peaks of 2001 and 2009. At this stage, there is little sign that this will result in a surge in available

space in the world’s dominant office markets.

Robust fundamentals are encouraging developer activity in the U.S.

Development volumes in the U.S. fell to 8.2 million square metres during Q4, but the underlying trend in construction is

still upward. This trend will continue into 2016 as improving fundamentals in secondary and tertiary markets encourage

developers to move forward. 2016 will see the U.S. receive 5.2 million square metres of new supply, but nearly half of

this space is already pre-leased.

Limited speculative construction in Europe, with the exception of London

In Europe the final quarter of the year witnessed the largest amount of office completions in 2015, with 1.7 million square

metres of new office space added to the market, accounting for 39% of the annual total. Nevertheless, most office

markets experienced a further tightening of space, with the majority recording a decrease in vacancy.

The lack of quality space is unlikely to be resolved in the immediate future with a limited speculative pipeline reported in

most markets. London is one of the few European cities seeing a significant development response in the short term,

with high levels of speculative space under construction. In Warsaw and Prague, significant development volumes will

sustain the existing high vacancy levels.

Healthy office supply additions in Asia. Pre-leases ease impact of new completions

Asia Pacific stock additions were up 65% in 2015 to 5.6 million square metres. The lion’s share of completions was in

India and China, while strong pre-commitment rates mitigated the impact of new supply on vacancy in markets such as

Tokyo and Manila. Regional completions are expected to peak in 2016 at 6.8 million square metres, up 21% on 2015

levels.

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 21

Global Office Completions, 2000-2018

24 markets in Europe; 25 markets in Asia Pacific; 44 markets in the U.S. Asia relates to Grade A only. Source: JLL, February 2016

Office Supply Pipeline – Major Markets, 2016-2017

Covers all office sub-markets in each city. Tokyo – CBD - 5 kus Source: JLL, February 2016

0

5

10

15

20

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016(F)

2017(F)

2018(F)

U.S. Europe Asia Pacific

mill

ions

sq

m

Average

0 5 10 15 20 25 30 35 40

Los AngelesNew York

MadridChicago

Washington DCStockholm

FrankfurtToronto

MilanSeoul

BostonBrusselsSydney

San FranciscoParis

Hong KongLondon

DubaiMoscow

TokyoSingapore

BeijingSao Paulo

MumbaiMexico City

Shanghai

Completions as % of existing stock

2016 2017

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 22

Global Market Perspective, First Quarter 2016

Office Vacancy

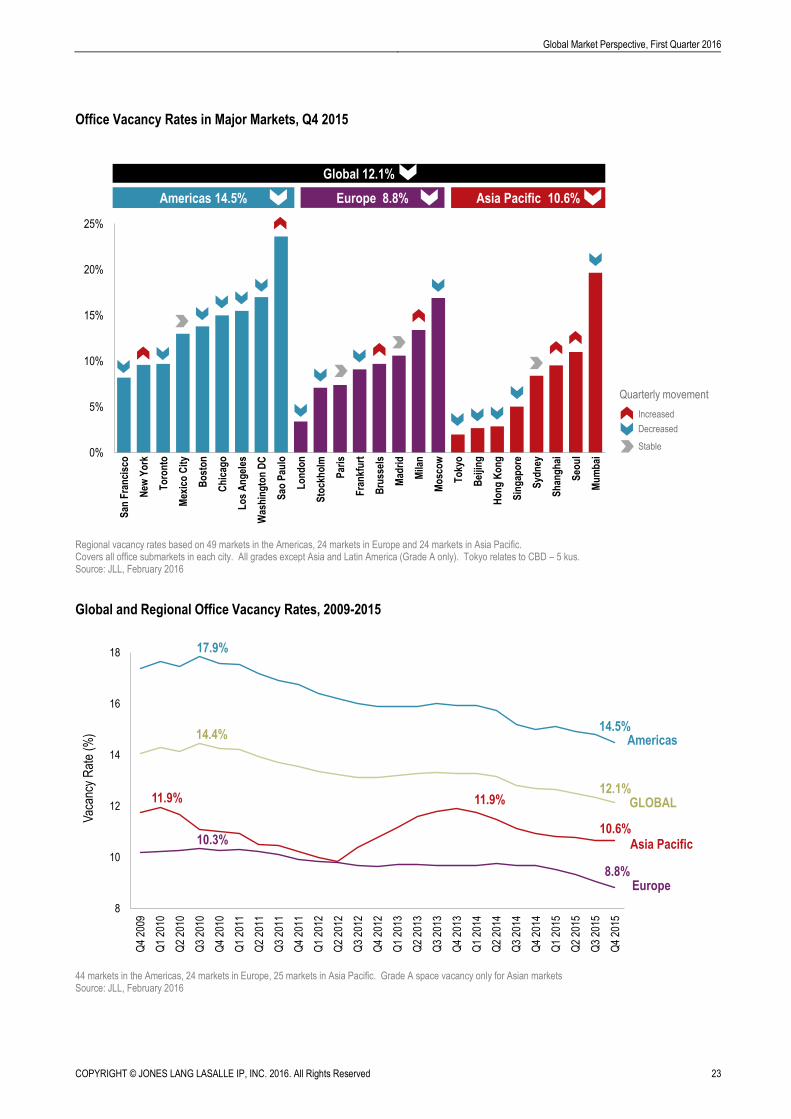

Global vacancy rates continue to trend downwards

Another 20 basis points were shaved off the global office vacancy rate (across 98 markets) in Q4 2015, which stood at

12.1% at the end of the year. This marks a quickening in the downward trend in vacancy rates since Q3 2010 (when it

was at a peak rate of 14.4%). A further fall is in prospect during 2016, notably in the U.S. and potentially in Europe.

With a modest increase in new office deliveries anticipated in 2016 and 2017, the global vacancy rate is projected to

settle at around 12% during the next two years.

U.S. office vacancy rate at lowest for eight years

Vacancy in the U.S. has declined to 14.7%, its lowest level for eight years and despite 4.1 million square metres of new

supply delivered across the country in 2015. The vacancy rate is inching towards the pre-recession low of 13.8%.

Lowest vacancies are found in urban locales in cities such as New York, San Francisco and Portland.

Surprise drop in European vacancy

The European office vacancy rate dropped by 30 basis points in Q4 2015 to 8.8%, the lowest since Q1 2009. The 90

basis points drop in 2015 was stronger than anticipated at the start of the year. The bounce in leasing activity had a

particularly hefty impact on vacancy in Western Europe markets including Dublin, Dusseldorf and Stockholm.

Furthermore, supply tightened well below the long-term averages in some of the best-performing European office

markets, including London (to 3.4%), Berlin (to 6.3%) and Munich (to 5.3%). European office vacancy is expected to

edge down further in 2016 on the back of strengthening occupier markets and a lack of new completions.

Asia Pacific vacancy edging down

Despite relatively high levels of new completions in Asia Pacific, improving absorption helped the regional vacancy rate

to edge down further to 10.6% in Q4. But, with a further modest increase in new completions in 2016, the rate could

move back up above 11% during 2016. Nonetheless, vacancy rates are low in many of the region’s major markets, with

Hong Kong Central’s rate of 1.2% at its lowest since the Global Financial Crisis. At the other extreme, Delhi’s current

vacancy rate is 31.9%, followed by Perth at 23.5%.

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 23

Office Vacancy Rates in Major Markets, Q4 2015

Regional vacancy rates based on 49 markets in the Americas, 24 markets in Europe and 24 markets in Asia Pacific. Covers all office submarkets in each city. All grades except Asia and Latin America (Grade A only). Tokyo relates to CBD – 5 kus. Source: JLL, February 2016

Global and Regional Office Vacancy Rates, 2009-2015

44 markets in the Americas, 24 markets in Europe, 25 markets in Asia Pacific. Grade A space vacancy only for Asian markets Source: JLL, February 2016

0%

5%

10%

15%

20%

25%

San

Fra

nci

sco

New

Yo

rk

To

ron

to

Mex

ico

Cit

y

Bo

sto

n

Ch

icag

o

Lo

s A

ng

eles

Was

hin

gto

n D

C

Sao

Pau

lo

Lo

nd

on

Sto

ckh

olm

Par

is

Fra

nkf

urt

Bru

ssel

s

Mad

rid

Mila

n

Mo

sco

w

To

kyo

Bei

jing

Ho

ng

Ko

ng

Sin

gap

ore

Syd

ney

Sh

ang

hai

Seo

ul

Mu

mb

ai

Europe 8.8% Asia Pacific 10.6%Americas 14.5%

Quarterly movement

Increased

Decreased

Stable

Global 12.1%

8

10

12

14

16

18

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Vac

ancy

Rat

e (%

)

Americas

Asia Pacific

Europe

GLOBAL

17.9%

14.5%14.4%

12.1%11.9%

10.6%

11.9%

10.3%

8.8%

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 24

Global Market Perspective, First Quarter 2016

Office Rental Trends

Rental growth moves at a steady pace

Rental growth on prime office assets accelerated during the second half of 2015 as supply tightened and demand

strengthened. Growth of 3.7% was recorded for the full-year (across 26 major markets), matching the levels of 2014.

The star performer among the major markets during 2015 was Stockholm, where a sharp fall in vacancy rate and near

record take-up levels pushed rents up by 15.6%. In Asia Pacific, Hong Kong (+13.3%), Sydney (+13.0%) and

Shanghai (+9.4%) posted strong rental performance, while the U.S. West Coast markets of Los Angeles (+9.2%) and

San Francisco (+7.8%) outperformed in the Americas. By contrast, Moscow (-11.1%), Singapore (-10.5%) and Sao

Paulo (-5.4%) registered a decline in prime rents during 2015.

U.S. markets to dominate top slots in 2016

Further rental growth of 3%-4% is in prospect for 2016 across the major global office markets. The gateway U.S

markets are likely to dominate the top positions in 2016, with Boston, Los Angeles, San Francisco, Chicago and New

York all expected to exceed 5% growth. Robust prime rental growth is also in prospect in Tokyo, Sydney, Hong Kong

and Shanghai, while Madrid and London are projected to be the standout markets in Europe.

Landlord confidence builds in the U.S.

In the U.S., asking rents increased by 2.2% during Q4 2015. This represents the largest quarterly gain of the current

cycle, with further growth anticipated for the next two years as new quality space sets higher rental benchmarks.

Sustained tenant demand will give landlords of existing buildings leverage to raise rents further and create a more

challenging negotiating environment for tenants.

Continued growth in Europe

The European Office Rent Index rose by 0.8% during Q4 2015, but the increase was dragged down by the weak

performance of Moscow and Paris, two of Europe’s largest markets. Excluding Moscow (where currency volatility

continues to impact on rents), Europe recorded rental growth of 2.7% in 2015, well above the 10-year average rise of

1.7%. Elsewhere across Europe, sentiment is largely positive. In Spain, Barcelona (+2.6%) and Madrid (+2.8%)

registered their fifth and seventh consecutive quarters of rental uplifts respectively. Meanwhile in Germany, Berlin and

Hamburg experienced a strong Q4, fuelled by record levels of take-up.

Rental growth of 2%-3% a year is projected for prime European offices in both 2016 and 2017. There is some upside

potential, in the case of a more pronounced and widespread demand-side recovery. We foresee rental growth in

London outperforming the European average in the year ahead, but growth rates are expected to ease from their recent

levels.

Rental growth accelerates across Asia Pacific

Following a lacklustre Q3, average net effective rental growth across Asia Pacific accelerated to 1.3% in Q4 2015.

Growth for the full-year averaged 3.7%, led by Hong Kong (+13.3%). The strongest quarterly uplift was seen in Sydney

(+5.4%), followed by Bangalore (+3.8%) on the back of robust tenant demand. Improved business sentiment also

contributed to rental growth gathering pace in Tokyo (+2.8%). Across the region, single-digit rental growth is generally

predicted for 2016, led by Sydney and Tokyo. Singapore and a few Australian cities may see further declines due to

muted tenant demand and/or upcoming supply.

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 25

Prime Offices – Rental Change, Q4 2014-Q4 2015

Based on rents for Grade A space in CBD or equivalent. In local currency. Source: JLL, February 2016

Prime Offices – Rental Change, 2010-2016

Prime office rental growth: unweighted average of 25 major markets. * 2015 forecast excludes Moscow Source: JLL, February 2016

-15 -10 -5 0 5 10 15 20

Moscow

Singapore

Sao Paulo

Paris

Mumbai

Seoul

Mexico City

Brussels

Frankfurt

Milan

New York

Washington DC

Beijing

Chicago

Toronto

London

Madrid

Boston

Tokyo

San Francisco

Los Angeles

Shanghai

Sydney

Hong Kong

Dubai

Stockholm

% change

Americas

EMEA

Asia Pacific

0

1

2

3

4

5

6

7

8

9

10

2010 2011 2012 2013 2014 2015 2016

8.6%

7.7%

1.6%

0.7%

Ren

tal c

hang

e (y

-o-y

%)

3-4%3.7% 3.7%

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 26

Global Market Perspective, First Quarter 2016

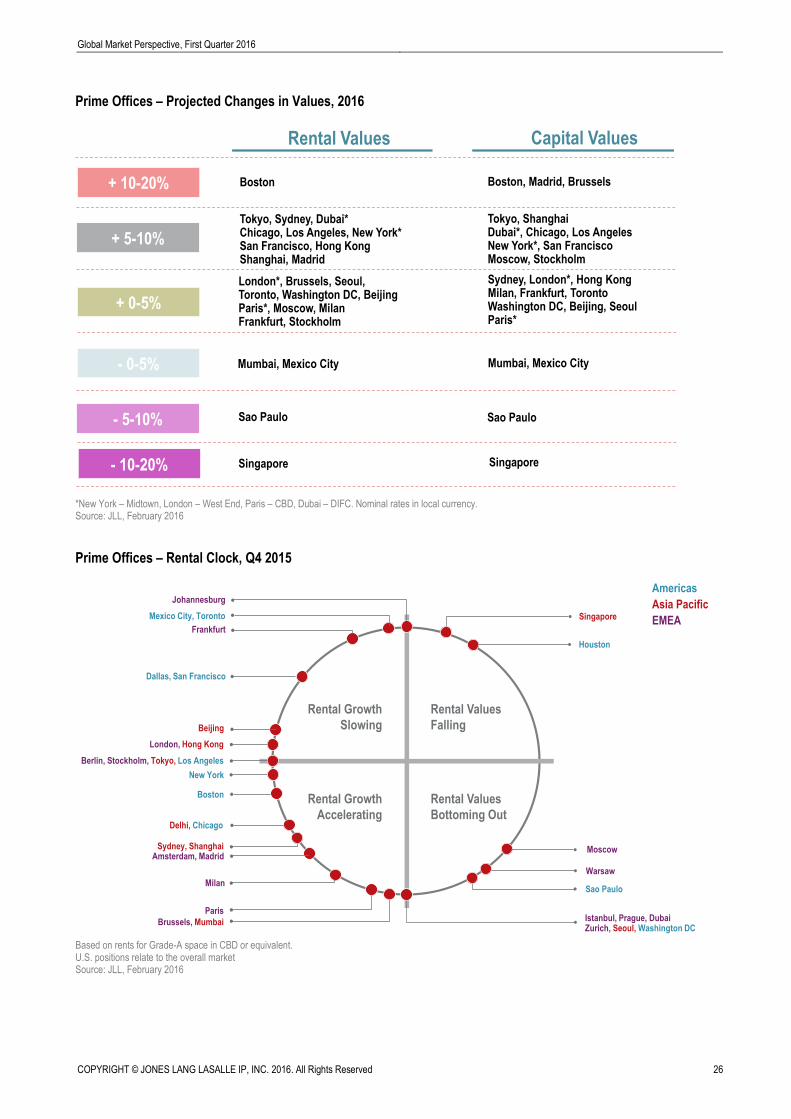

Prime Offices – Projected Changes in Values, 2016

*New York – Midtown, London – West End, Paris – CBD, Dubai – DIFC. Nominal rates in local currency. Source: JLL, February 2016

Prime Offices – Rental Clock, Q4 2015

Based on rents for Grade-A space in CBD or equivalent. U.S. positions relate to the overall market Source: JLL, February 2016

+ 10-20%

+ 5-10%

+ 0-5%

- 0-5%

- 5-10%

Tokyo, Sydney, Dubai*Chicago, Los Angeles, New York* San Francisco, Hong KongShanghai, Madrid

Capital ValuesRental Values

London*, Brussels, Seoul, Toronto, Washington DC, Beijing Paris*, Moscow, MilanFrankfurt, Stockholm

Boston, Madrid, Brussels

Tokyo, ShanghaiDubai*, Chicago, Los AngelesNew York*, San FranciscoMoscow, Stockholm

Sydney, London*, Hong KongMilan, Frankfurt, TorontoWashington DC, Beijing, SeoulParis*

Mumbai, Mexico City

- 10-20%

Sao Paulo Sao Paulo

Mumbai, Mexico City

Singapore Singapore

Boston

Rental Values

Bottoming Out

Rental Growth

Slowing

Rental Values

Falling

Rental Growth

Accelerating

Americas

Asia Pacific

EMEA

Moscow

Berlin, Stockholm, Tokyo, Los Angeles

ParisIstanbul, Prague, DubaiZurich, Seoul, Washington DC

Sao Paulo

Sydney, Shanghai

Boston

Amsterdam, Madrid

Frankfurt

Mexico City, Toronto

Houston

Dallas, San Francisco

Milan

Warsaw

Johannesburg

Singapore

Brussels, Mumbai

Delhi, Chicago

London, Hong Kong

Beijing

New York

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 27

Retail Markets

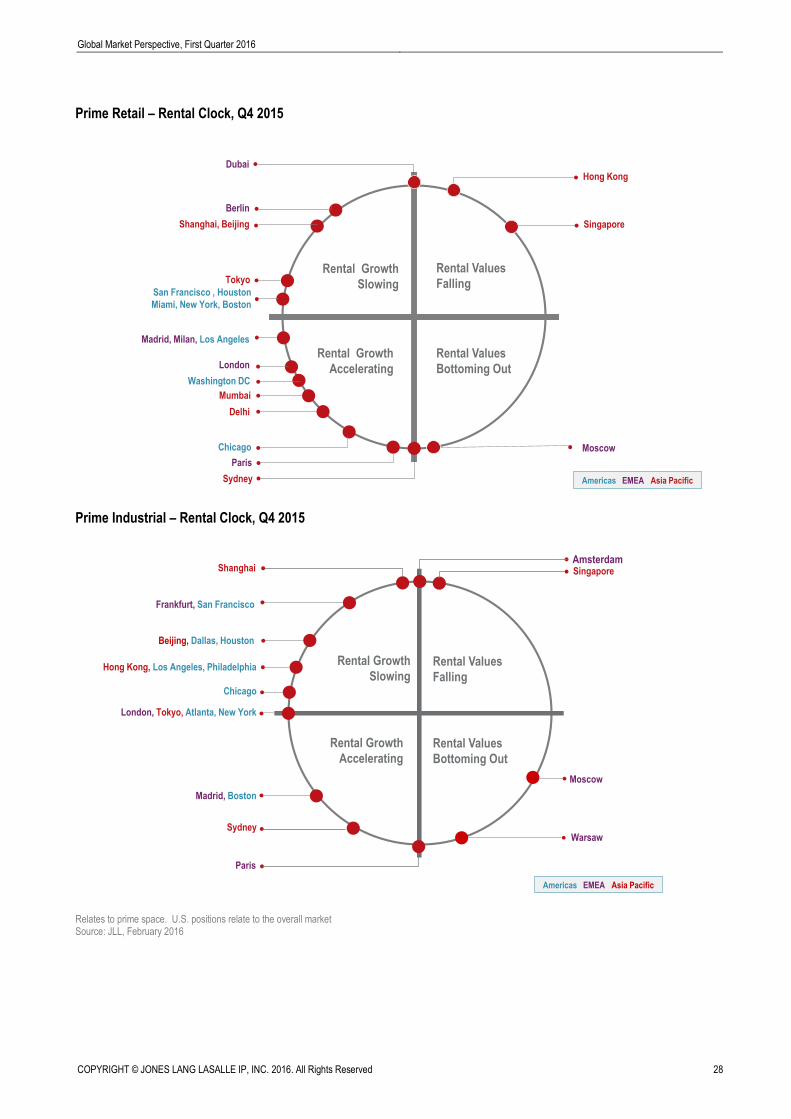

U.S. retail market gradually tightening despite surging e-commerce

The U.S. vacancy rate inched down to 5.6% in the fourth quarter of 2015. Demand has comfortably exceeded supply in

three of the past four quarters, resulting in sustained vacancy compression. Rents increased 0.5% quarter-on-quarter

and grew 1.6% year-on-year. Among U.S. shopping centre types, power centres are still experiencing the tightest

overall market conditions, with total vacancy of 4.5%. Several standout markets like Miami, New York, Houston,

Dallas, Fort Lauderdale, Boston and San Francisco are now witnessing conditions typical of a peaking market, as

rents see assertive growth and vacancy continues to compress.

Consumer confidence remains robust in Europe

Improved consumer confidence is still evident across Europe with the Eurozone showing signs of economic recovery.

Increasing employment opportunities, improved real wage growth, lower fuel and energy prices, and low interest rates

are driving disposable income growth. Europe’s retail sales are forecast to grow by 2.0% in 2016, with demand led by

the UK, Turkey, Spain, Sweden, CEE markets and the Baltics.

UK regional cities show strongest rental growth in Europe

UK regional cities - Edinburgh (+9.1% quarter-on-quarter), Birmingham (+5.4%) and Manchester (+5.3%) - and Berlin

(+6.7%) recorded the strongest rental growth during Q4, driven by vigorous retailer demand. Increases were also

registered in the recovery markets of Milan (+7.5%) and Barcelona (+2.0%). Prime high street rents maintained their

stability in most major European cities. Dublin, Rome, London, Leeds, Munich and Dusseldorf are expected to see

the healthiest prime rental growth in 2016.

Varied demand picture in Asia; limited rental growth in most markets

Retailer demand for space in China continues to be supported by fast fashion retailers and F&B. Demand from luxury

retailers remained weak during the fourth quarter, despite a cut in Chinese import duties for luxury goods. In Hong

Kong, declining tourist arrivals from China kept the downward pressure on retail sales. In Tokyo, there was solid

demand from affordable luxury apparel brands for space in prime retail areas. Challenging market conditions persisted

in Singapore with subdued retailer demand and weak consumer sentiment. Market conditions in India were generally

stable, with F&B and apparel still the most active retailer categories. The acceleration in discretionary retail spending

growth is positive for Australia’s specialty store leasing demand but rents stayed largely unchanged outside of the CBD

and bulky goods sub-sectors.

Average rental growth edged up across the Asia Pacific region in Q4, but further declines were recorded in Singapore

and Hong Kong’s high street shops. Over the short term, we see limited scope for much rental growth in most markets,

and Hong Kong is likely to witness the biggest decline in rents for high street space.

Rental growth slowing in Dubai

While retail spending levels have maintained their upward momentum, the level of growth has slowed in the UAE as

tourist spending has been hit by the strength of the U.S. dollar. Following robust rental growth over the past two years,

retail rents in Dubai are now stabilising as the balance of power shifts in favour of brand owners. With significant

additions to the retail supply continuing in Dubai, rental uplifts over the next year are likely to be primarily in the form of

turnover rentals, which will work in the favour of the best-performing malls.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 28

Global Market Perspective, First Quarter 2016

Prime Retail – Rental Clock, Q4 2015

Prime Industrial – Rental Clock, Q4 2015

Relates to prime space. U.S. positions relate to the overall market Source: JLL, February 2016

Rental Growth

Slowing

Rental Values

Falling

Rental Growth

Accelerating

Rental Values

Bottoming Out

Americas EMEA Asia Pacific

Delhi

Mumbai

Hong Kong

Madrid, Milan, Los Angeles

Dubai

Shanghai, Beijing

Berlin

Sydney

MoscowChicago

Singapore

Tokyo

Washington DC

San Francisco , Houston

Miami, New York, Boston

Paris

London

Rental Growth

SlowingRental Values

Falling

Rental Values

Bottoming Out

Warsaw

Americas EMEA Asia Pacific

Rental Growth

Accelerating

Paris

Madrid, Boston

Frankfurt, San Francisco

London, Tokyo, Atlanta, New York

Hong Kong, Los Angeles, Philadelphia

Amsterdam

Beijing, Dallas, Houston

Shanghai

Sydney

Chicago

Moscow

Singapore

Global Market Perspective, First Quarter 2016

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 29

Industrial Warehousing Markets

U.S. continues its stellar performance

The industrial market in the U.S. is enjoying a remarkable stretch of good health. There have been 23 straight quarters

of positive net absorption with market fundamentals remaining strong throughout 2015. Active tenant requirements

(potential absorption) exceeded underway speculative construction by a factor of over two-to-one by year-end, and

absorption is forecast to stay positive in 2016 with continued velocity across nearly every U.S. market.

U.S. rental growth accelerated in 2015

The average asking warehouse rental rate in the U.S. was up 5.5% year-on-year in 2015. Ten markets now have sub-

5.0% vacancies with a handful under 3.0%. These include a few West Coast markets such as Los Angeles (2.2%),

which had an annual warehouse rental increase of 9.5% in 2015. Countrywide, rental growth will drive value in 2016;

even with an increase in new construction, we forecast overall rental growth will be 4.5%. Some U.S. markets – where

vacancies are especially tight – will post double-digit gains.

Industrial solid across North America

Apart from oil-related weak markets in Alberta, the industrial market in Canada is performing well with the national

vacancy rate declining 50 basis points to just 3.6% during the fourth quarter. Strength is most pronounced across the

Greater Toronto area, while Vancouver is also experiencing solid growth. The industrial sector in Mexico is witnessing

significant investment related to the automotive manufacturing industry, with Toyota among the latest major players to

announce a new plant (in Guanajuato). Total industrial vacancy across the country was stable in Q4 2015 at 6.1%.

Continued occupier demand and city logistics expected to define 2016 in Europe

The ongoing vigorous growth in online sales and the wider impact of technology trends (including the digitisation of retail,

‘Big Data’ and the ‘Internet of Things’) are driving occupier demand for logistics across Europe. In 2015, take-up

volumes were estimated at over 16 million square metres, a new record. We anticipate similar levels to be sustained in

the current year.

Sturdy occupier demand supported growth in the development pipeline through 2015 and levels of new supply are

anticipated to be similarly strong this year. Finding suitable land and obtaining planning permission for big box logistics

will, however, become more challenging across a growing number of markets in Europe. The still scarce levels of

modern supply may pose a downside risk to overall occupier activity in the year ahead.

Nevertheless, developers will continue to benefit from supply chain alignment. This is driving consolidation into large

units and pushing logistics facilities ever closer to parcel hubs to service online sales. We expect 2016 to be the year

when logistics starts to move into large cities. This trend is being driven by ever quicker options for online purchases -

with one-hour delivery being the new frontier for many retailers. This is putting huge pressure on the ‘last mile’ and is

leading to demand for a network of small inner-city units to increase flexibility.

Demand from third-party logistics companies and e-commerce firms support warehouse rents in Asia Pacific

Generally healthy leasing activity was observed in Asia Pacific in Q4, propelled mainly by third-party logistics (3PLs) and

e-commerce companies, especially in China and Tokyo. Leasing demand in Hong Kong was lacklustre, with activity

largely driven by 3PLs’ cost-saving relocation requirements. In Singapore, robust relocation and renewal demand for

business park space stemmed from research and IT firms. Competitive development markets continue to limit rental

growth in Australian markets.

Across the Asia Pacific region, rents were mainly flat, with the highest quarterly rental growth of 1.1% in Beijing. A flat

to moderate uplift in rents is projected for most markets over the short term on the back of generally subdued export and

retail sales growth.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All Rights Reserved 30

Global Market Perspective, First Quarter 2016

Hotel Markets

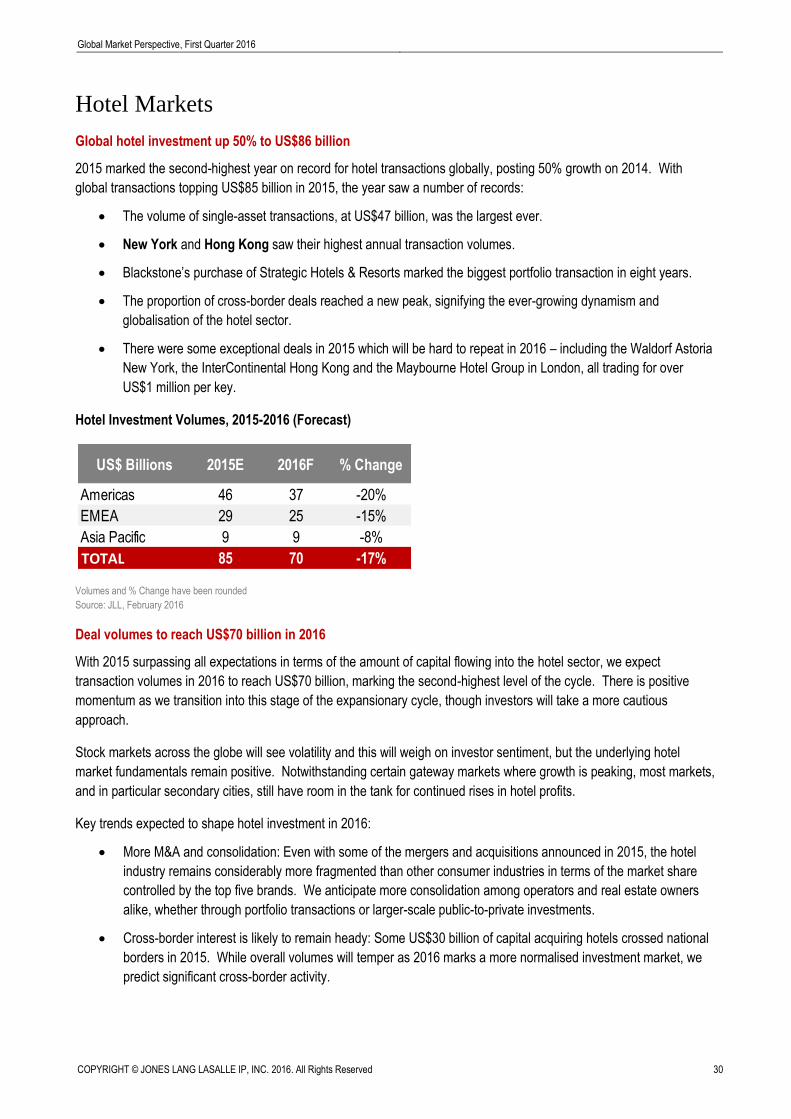

Global hotel investment up 50% to US$86 billion

2015 marked the second-highest year on record for hotel transactions globally, posting 50% growth on 2014. With

global transactions topping US$85 billion in 2015, the year saw a number of records:

The volume of single-asset transactions, at US$47 billion, was the largest ever.

New York and Hong Kong saw their highest annual transaction volumes.

Blackstone’s purchase of Strategic Hotels & Resorts marked the biggest portfolio transaction in eight years.

The proportion of cross-border deals reached a new peak, signifying the ever-growing dynamism and

globalisation of the hotel sector.

There were some exceptional deals in 2015 which will be hard to repeat in 2016 – including the Waldorf Astoria

New York, the InterContinental Hong Kong and the Maybourne Hotel Group in London, all trading for over

US$1 million per key.

Hotel Investment Volumes, 2015-2016 (Forecast)

Volumes and % Change have been rounded

Source: JLL, February 2016

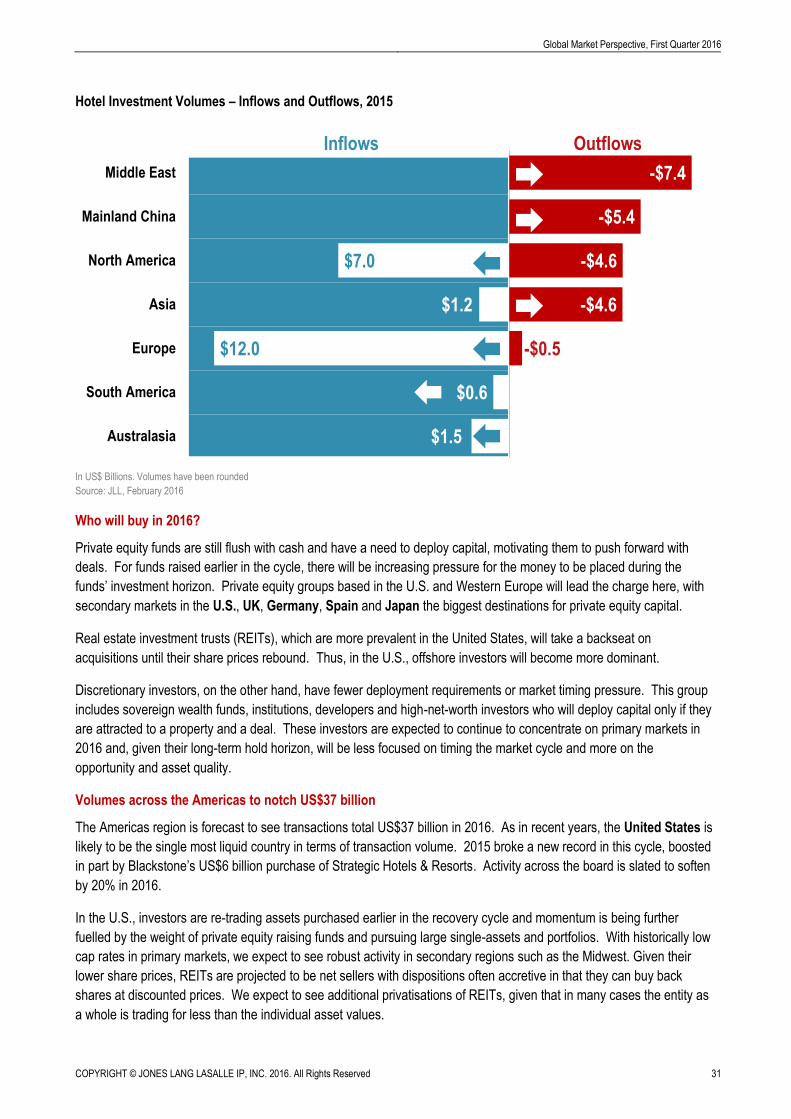

Deal volumes to reach US$70 billion in 2016

With 2015 surpassing all expectations in terms of the amount of capital flowing into the hotel sector, we expect