22

Acosta Deep Mine – Day of Grand Opening, Somerset County, Pennsylvania Corsa Coal Corp. Investor Presentation September 2018

Acosta Deep Mine – Day of Grand Opening, Somerset County, Pennsylvania

Corsa Coal Corp. Investor Presentation

September 2018

Certain statements and information set forth in this presentation constitute "forward-looking statements" and "forward-looking information" under applicable securities laws (collectively, "forward-looking statements"). Except for statements of historical fact, certain information contained herein constitutes forward-looking statements which include management's assessment of future plans and operations and are based on current internal expectations, estimates, projections, assumptions and beliefs, which may prove to be incorrect. Some of the forward-looking statements include, but is not limited to, statements regarding the pro forma projections and information for Corsa and future oriented financial information. When used in this presentation, forward-looking statements may be identified by words such as "estimates", "expects" "anticipates", "believes", "projects", "plans", "pro forma" and similar expressions. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, many of which are beyond Corsa's control and may causeCorsa's actual performance and financial results in future periods to differ materially from any projections of future performance or results expressed or implied by such forward-looking statements. These risks and uncertainties include, but are not limited to: liabilities inherent in coal mine development and production; geological, mining and processing technical problems; inability to obtain required mine licenses, mine permits and regulatory approvals or renewals required in connection with the mining and processing of coal; unexpected changes in coal quality and specification; risks that the coal preparation plants will not operate at production capacity during the relevant period; variations in the coal preparation plants' recovery rates; dependence on third party coal transportation systems; competition for, among other things, capital, acquisitions of reserves, undeveloped lands and skilled personnel; incorrect assessments of the value of acquisitions; changes in commodity prices and exchange rates; changes in the regulations in respect to the use, mining and processing of coal; changes in regulations on refuse disposal; the effects of competition and pricing pressures in the coal market; the oversupply of, or lack of demand for, coal; currency and interest rate fluctuations; various events which could disrupt operations and/or the transportation of coal products, including labor stoppages and severe weather conditions; the demand for and availability of rail, port and other transportation services; and management's ability to anticipate and manage the foregoing factors and risks. The forward-looking statements and information contained in this presentation are based on certain assumptions regarding, among other things, coal sales being consistent with expectations; future prices for coal; future currency and exchange rates; Corsa's ability to generate sufficient cash flow from operations and access capital markets to meet its future obligations; the regulatory framework representing royalties, taxes and environmental matters in the countries in which Corsa conducts business; coal production levels; and Corsa's ability to retain qualified staff and equipment in a cost-efficient manner to meet its demand. While these assumptions, risks and uncertainties do not represent a complete list of factors which may cause events to be materially different than those expressed or implied by forward-looking statements in this presentation, they should be considered carefully. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. The forward looking statements will not be updated unless required by law. The reader is cautioned not to placeundue reliance on forward-looking statements. Unless otherwise specifically indicated, all references in this presentation to dollars or to "$" or "$USD" are to the currency of the United States, and all references to "$CAD" are to the currency of Canada.

Forward-looking Statements

1

Corsa Coal Corporation: Overview

Growth-oriented premium quality metallurgical coal producer

Corporate headquarters: Canonsburg, PA Operations headquarters: Somerset, PA

Approximately 400 employees

Operations in Maryland and Pennsylvania (3 active deep mines,2 active surface mines active)

2018E Metallurgical Sales: 2.1 – 2.3 million tons

Metallurgical Coal Customer Base: Steel and coke producers inthe United States, Asia, South America, and Europe

LTM Revenue: $248.5 million LTM Adjusted EBITDA: $35.5 million

Selling coal that Corsa produces from its active mine sites

Purchasing and reselling coal sourced within trucking distance

Purchasing and reselling coal purchased from the CAPP region

Company Produced Tons

Value Added Services

Sales & Trading Volumes

1

2

3

Producer / Trader Business Model

Corsa NAPP Division Pennsylvania

Baltimore

Norfolk

High Quality Equity Sponsors

Quintana Capital Group (45% fully diluted)

Quintana affiliates are the largest owners of coalreserves in the United States

Sprott Resource Coal Holdings (16%)

Leading resource-focused investor and prior ownerof PBS Coals prior to Severstal acquisition

Family of Lukas Lundin (15%)

Highly successful investor and operator of miningand oil & gas companies

2

Metallurgical Coal Overview

Role of Met Coal in Steel Making

25-45% Premium Met Coal Known as Low / Mid Vol Or

Hard Coking Coal

55-75% Lower Grade Met Coal Known as High Vol Or Semi-

Soft Coking Coal

Highly sensitive to coal blends Coal requires 2-3 years of

testing before approval Focus on strength and safety

Seaborne Metallurgical Coal Overview (~300 Million Mt)

China & India Japan & S. Korea

EU & Brazil OtherAustralia USA Canada Other

Demand Supply

Metallurgical vs. Thermal Coal Comparison

+

(a) Met coal price reference to prime hard coking coal and thermal price reference to NewcastleSource: Industry Research

Metallurgical Coal Thermal Coal

Used in the steelmaking process Used to generate electricity

No substitute in the blast furnace Substitutes: natural gas & renewables

Premium qualities are scarce globally Supply abundant

Current Spot Price (FOB Mine): >$120/short ton Current Price (FOB Mine): $60/short ton

3

Urbanization Drives Steel and Metallurgical Coal Demand

Source: United Nations, World Steel Association

Historical and Projected Urbanization Rates

Metallurgical coal is necessary for the production of steel, which historically has shown a high correlation to urbanization. Overthe long term, urbanization rates of emerging markets are forecasted to approach those of developed nations.

Steel Production vs. Urban Population (1980-2010)

716 719 770 753

851

1,148

1,433

400

600

800

1,000

1,200

1,400

1,600

1.5 2.0 2.5 3.0 3.5 4.0

Glo

bal S

teel

Pro

duct

ion

(mm

Mt)

World Urban Population (Billions)

26% 31%

40%

26%

49%

69% 75%

82% 86% 77%

91% 97%

1990A 2010A 2030E

India China US Japan

4

1.

2.

3.

Global Crude Steel Demand Drivers

Global steel production growth 5.0% 2018 YTD

Global population growth and urbanization

China and India infrastructure

Rebuilding America Source: worldsteel.org

(1) Source: World Steel Association

Steel Use1,500 Mt /

year

5

Seaborne Metallurgical Coal Pricing

Historical Quarterly LV Metallurgical Coal Benchmark Pricing (2006 – 2018)

Prices expressed on a $/metric ton, FOB Port basis

Current Drivers: Strong Steel Market, Fragile Supply Chain

10-Year Average: $186/mt

2019: $188

2020: $170

6

NAPP Division Overview

• Active Mines / 2018E Production Forecast

• Casselman: 380,000 tons

• Acosta: 365,000 tons

• Quecreek: 132,000 tons

• Surface Mines: 100,000 tons

• 2018 Forecast

• Metallurgical Production: 1.0 million tons (includes Quecreek)

• Value Added Services Purchased Coal: 0.45 million tons

• Sales & Trading Tons: 0.75 million tons

NAPP Division Operating Locations Operations

• Up to 4 million clean tons per year of processing plant capability

• Only regional producer with CSX rail loading access

• Three preparation plants with refuse disposal sites and rail loadouts

• Cambria Preparation Plant (CSX)

• Shade Creek Preparation Plant (NS)

• Rockwood Preparation Plant (CSX) (Plant currently idle)

• Significant refuse disposal capacity with expansion opportunities

Infrastructure

Pittsburgh 70 miles NW of Somerset

7

NAPP Margin Streams

Company Produced Tons% of Company Gross Margin: 68%

Value Added Services% of Company Gross Margin: 28%

Sales &Trading% of Company Gross Margin: 3%

8

1.

2.

3.

Diversified growth strategy to increase coal sales

Tonnage by Segment

8

AssumptionsShifts 3Hours/Shift 8Days/Week 7Weeks/Year 50Plant Availability 95%Hours/Years 7,980

Plant TPH HPY Raw Tons Recovery Clean TonsShade Creek 450 7,980 3,591,000 50% 1,795,500 Cambria 325 7,980 2,593,500 50% 1,296,750 Rockwood 325 7,980 2,593,500 50% 1,296,750

8,778,000 4,389,000

NAPP Division – Infrastructure

• Shade Creek Preparation Plant

• Norfolk Southern Rail

• Toll processing for third parties

• Used for export blend shipments and truck business todomestic customers

• Cambria Preparation Plant

• CSX Rail

• Used for export shipments and truck and rail to domesticcustomers

• Rockwood Preparation Plant

• Idle status; Could be moved to a future reserve base

Preparation Plants Shade Creek Preparation Plant

Preparation Plant Throughput (Maximum)

Cambria Preparation Plant

9

Corsa Coal Growth Story

Casselman Acosta Horning Keyser NorthMine

Status Fully Developed Fully Developed In Development Permitting Permitting

Annual Production 520,000 430,000 140,000 570,000 480,000

Start-up CapEx Funded Funded Funded $24 million $25 million

Project Beginning 2011 2017 2018 2019 2020

Corsa is in the 5th inning of its organic growth plan and is focused on the development of the high-returning Keyser and North mines

Corsa has the mining projects, preparation plant capacity and customer base to double company producedtons over the next 3 years

Corsa has opened two mines in the last 15 months, Acosta and Horning, and plans to begin one mine in eachof the next two years.

All of these mines are metallurgical projects within transportation range of Corsa’s preparation plants

As Corsa builds out its mines in the region, economies of scale will benefit overall costs per ton through fixedcost absorption

10

Value Added Services Purchased Coal

Value Added Services Purchased Coal Platform Highlights

Initiative launched in October 2016

Gross Margin Contribution

2017: $12 million

1H 2018: $7 million

VAS tons supplement Corsa’s overall blends and tonnages for export vessels

Increased volume through the preparation plants absorbs fixed costs and lowers per unit costs

Corsa purchases coal locally from third parties, provides the value added services, and sells the coal on the export market

Washing Loading Blending Storing

Corsa’s Value Added Services for Local Purchased Coal

11

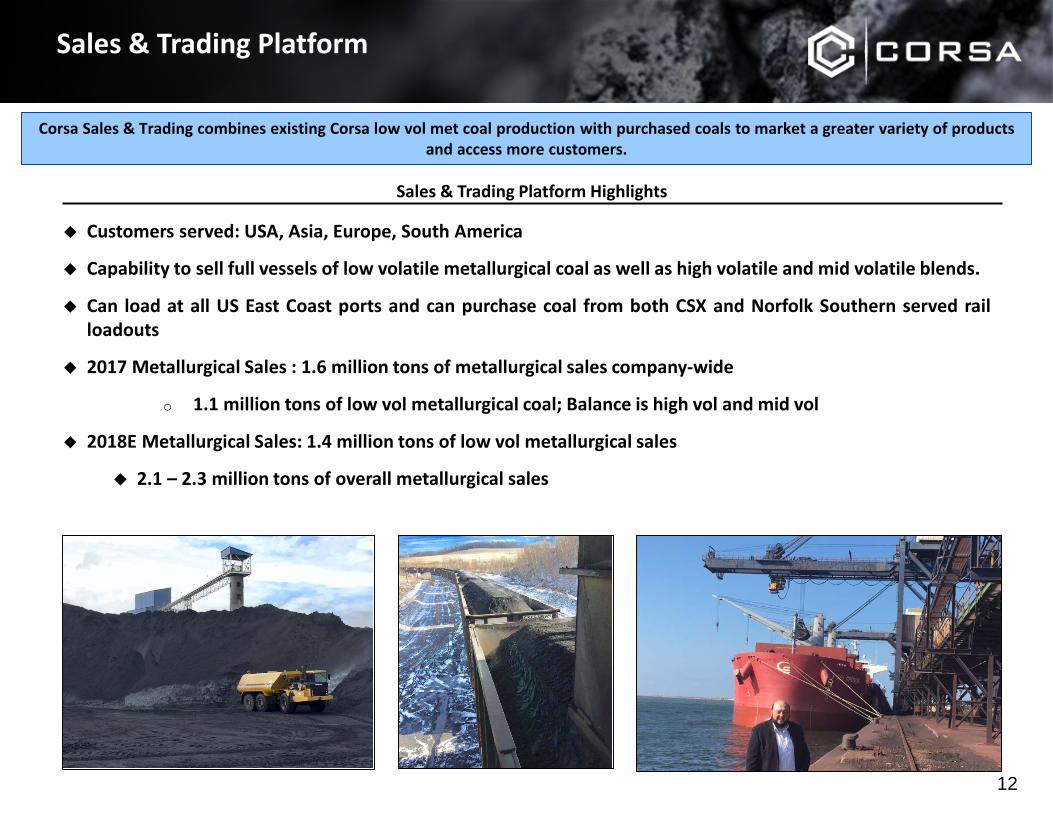

Sales & Trading Platform

Sales & Trading Platform Highlights

Customers served: USA, Asia, Europe, South America

Capability to sell full vessels of low volatile metallurgical coal as well as high volatile and mid volatile blends.

Can load at all US East Coast ports and can purchase coal from both CSX and Norfolk Southern served railloadouts

2017 Metallurgical Sales : 1.6 million tons of metallurgical sales company-wide

o 1.1 million tons of low vol metallurgical coal; Balance is high vol and mid vol

2018E Metallurgical Sales: 1.4 million tons of low vol metallurgical sales

2.1 – 2.3 million tons of overall metallurgical sales

Corsa Sales & Trading combines existing Corsa low vol met coal production with purchased coals to market a greater variety of products and access more customers.

12

Expanded Sales and Trading Platform

Extensive international relationships

Expanding customers in more countries

Mix of spot pricing and index pricing

Gaining access to additional purchased coal suppliers

Delivering more customized products adjusted to customer needs

Ability to sell on a delivered basis or FOB US East Coast

13

Infrastructure drives our sales, value added services and trading

Advantaged logistics to both domestic and export markets

Ability to deliver coal domestically by truck, rail, and barge

Proximity to the largest metallurgical coal buying region in the U.S.

Logistics: Our Transportation Advantage

14

Source: Industry Research, Management

ArcelorMittal U. S. SteelAK Steel

ArcelorMittal & SunCoke Energy

ArcelorMittal, SunCoke Energy & AK Steel

AK Steel & SunCoke Energy

DTE

Within this shaded region there is ~15mm tons of met coal demand from coke batteries of which ~4mm tons is low volatile met coal.

Lower delivery cost to consumers = higher realized price

Transportation Advantaged Domestic Market

14

Corsa’s growth will accelerate as the Horning, Keyser and North mines begin in the next 3 years

NAPP Division Met Sales Plan: Company Produced + Value Added Services tons only (no Sales & Trading tons included)

NAPP Division Organic Growth Forecast

Growth CapEx per Year $16 mm $24 mm

$9 mm

$- mm $- mm

15

Forecasted gross margin using forward price curve: >$30/ton

16

2018 Sales and Operational Guidance

Total Metallurgical Coal Sales Tons(1):

2.1-2.3 million short tons

Cash Productions Costs per Ton Sold (FOB Mine):

Metallurgical Coal - $82-$84 per short ton(2)(3)

General and Administrative Expenses(4):

NAPP $9.0 - 10.0 millionCorporate $6.5 - 7.0 millionTotal Corsa $15.5 – 17.0 million

Maintenance Cap/Ex per short ton sold(5):

2018 Full Year - $9 2018-2020 Forecasted Average -$4

1) Corsa's metallurgical coal sales figures are comprised of three types of sales: (i) selling coal that Corsa produces ("Company Produced"); (ii) selling coal that Corsa purchases and provides value added services (storing, washing, blending, loading) tomake the coal saleable ("Value Added Services"); and (iii) selling coal that Corsa purchases on a clean or finished basis from suppliers outside the Northern Appalachia region ("Sales and Trading").

2) This is a non-GAAP financial measure. See "Non-GASP Financial Measures" below.3) Cash Production Cost per ton sold excludes purchased coal.4) Exclusive of stock-based compensation and selling related commissions, bank fees and finance charges.5) Tons sold excludes purchased coal used in the Sales and Trading platform.

Positive Supply and Demand Fundamentals for Steel Raw MaterialsClear Path for Corsa to Double Sales OrganicallyAccess to North American and International Markets

17

Acosta Deep Mine – Day of Grand Opening, Somerset County, Pennsylvania

Corsa Coal Corp. Investor Presentation

September 2018Appendix

19

Financial Highlights

Q1 2017 Q2 2017 Q3 2017 Q4 2017Total Year

2017 Q1 2018 Q2 2018LTM

6/30/18

Revenues ($ million) $52.4 $54.3 $62.9 $47.9 $217.5 $80.4 $57.3 $248.5

Adjusted EBITDA(1) ($ million) $16.2 $11.3 $12.2 $8.1 $47.8 $10.9 $4.3 $35.5

Capital Expenditures - Maintenance ($ million) $1.1 $1.6 $1.5 $2.3 $6.5 $2.6 $3.8 $10.2

Capital Expenditures - Growth ($ million) $2.3 $6.3 $5.8 $5.3 $19.7 $4.5 $1.7 $17.3

Metallurgical Coal Sales

Average Realized Price / Metallurgical Ton Sold(1) $156.12 $121.77 $112.15 $122.25 $125.56 $118.46 $115.52 $116.75

Sales Volumes (short tons)

Company Produced Tons 196,777 194,075 248,798 172,255 811,905 242,511 194,051 857,615

Corsa Value Added Services Tons 63,940 79,523 81,115 92,257 316,835 145,856 88,393 407,621

Sales & Trading Tons 34,545 96,329 157,905 57,378 346,158 169,354 109,890 494,527

Total Metallurgical Coal Tons Sold 295,262 369,927 487,818 321,890 1,474,898 557,721 392,334 1,759,763

Cash Cost / Metallurgical Ton Sold(1)

Cash Production Cost Per Ton Sold(2) $74.67 $65.34 $70.30 $89.23 $74.18 $91.72 $93.46 $85.40

Cash Costs per Tons Sold $88.45 $82.40 $80.29 $89.43 $84.45 $90.83 $97.65 $89.17

Cash Margin per Metallurgical Ton Sold(1) $67.67 $39.37 $31.86 $32.82 $41.11 $27.63 $17.87 $27.58

(1) Non-GAAP Financial Measure(2) Excludes Purchased Coal

Flexible Debt Light Covenants No Amortization, 100% Bullet Payment

at Maturity August 2019 Maturity Common Ownership Between

Debt and Equity

Balance Sheet: Conservative Leverage

Note: Ownership percentages on a fully diluted basis. Source: Company Disclosure, Capital IQ

(45%)

(16%)

(15%)

Equity Sponsorship

As of June 30, 2018

Capitalization ($mm)

Cash and Equivalents $7.8

Sprott Non-Revolving Facility $32.0

Capital Lease Obligations $3.6

Notes Payable - Equipment $0.4

Notes Payable - Alumbaugh $0.5

Total Debt $36.5

Net Debt $28.7

20

Corsa Coal – Poised for Success

1.

2.

3.

Favorable position on the cost curve despite operating at far less than full capacity utilization. Premium metallurgical coal quality due to low pressure and high coke strength (CSR) Dual rail service and infrastructure enables blending and purchased coal opportunities for exports.

Domestic customers can be reached by truck, barge or rail. Advantaged logistics to 50% of domestic market and to Baltimore terminals.

Free cash flow positive; Significant operating leverage to increases in prices Strong balance sheet with low Debt-to-EBITDA level; Private equity partners No self bonding and no union liabilities

Organic growth plan to increase production with infrastructure in place to support over 4.0 million tons of preparation plant throughput at the NAPP division

Successful track record of asset integration and realized cost savings (e.g. acquisition of PBS Coals)

Emerging Sales & Trading platform with outstanding results to date

Sustainable Competitive Advantages

EBITDA &Balance Sheet Strong

Growth Opportunities

21