23

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008 Basic Cost-Management Concepts Chapter Three

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | varun-mehrotra |

| View: | 30 times |

| Download: | 2 times |

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

Basic Cost-Management Concepts

Chapter Three

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

2

• Understand the strategic role of basic cost concepts

• Explain cost-driver concepts at the activity, volume, structural, and executional levels

• Explain the cost concepts used in product and service costing

• Demonstrate how costs flow through the formal accounting system

Learning Objectives

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

3

• Prepare and interpret an income statement for both a manufacturing firm and a merchandising firm

• Explain the cost concepts related to the use of cost information in planning and decision-making

• Explain the cost concepts related to the use of cost information for control/feedback purposes

Learning Objectives (continued)

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

4

• A cost is incurred when a firm uses a resource for some purpose

• Costs are assembled into meaningful groups called cost pools (e.g., by type of cost or source)

• Any factor that has the effect of changing the level of total cost is called a cost driver

• A cost object is any product, service, customer, activity, or organizational unit to which costs are assigned for some management purpose

Basic Definitions

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

5

There are four main ways to classify costs (“different costs for different purposes”):

– For product and service costing (GAAP) – For strategic decision-making (cost-driver

analysis)– For planning and decision-making – For control/feedback

Cost Concepts: Overview

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

6

The process of assigning costs to cost pools or from cost pools to cost objects– Direct costs can be conveniently and economically

traced to a cost pool or a cost object

– Indirect costs cannot be traced conveniently or economically to a cost pool or a cost object

– Because indirect costs cannot be traced, assignment is made through the use of cost drivers (cost allocation)

– These cost drivers are often called allocation bases

Product/Service Costing: Cost Assignment

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

7

Cost Assignment: General Principles

Costs

Electric Motor

Materials Handling

Supervision

PackingMaterials

Cost Pools

AssemblyAssembly

PackingPacking

Cost Objects

Dishwasher

Washing Machine

FinalInspection

Cost Drivers and Cost Assignment

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

8

• Product costs include only the costs necessary to complete the product at the manufacturing step in the value chain (manufacturing) or to purchase and transport the product to the location of sale (merchandising)

• Period costs include all other costs incurred by the firm in managing or selling the product (indirect costs outside the manufacturing step of the value chain)

Product and Service Costing Concepts (GAAP)

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

9

• Direct material costs = cost of materials that can be readily traced to outputs = purchase price of materials + freight – purchase discounts + reasonable allowance for scrap and defective units

• Indirect material costs = cost of materials that cannot readily be traced to outputs (e.g., rags, lubricants, and small tools)

• Direct labor costs = labor that can be readily traced to outputs = wages paid plus a reasonable allowance for nonproductive time

• Indirect labor costs = labor costs that cannot be readily traced to outputs (i.e., they are manufacturing support costs)

Direct and Indirect Product Costs for a Manufacturer

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

10

• All indirect costs for the manufacturer, including indirect materials, indirect labor, and other indirect items are often combined in a cost pool referred to as overhead (or, factory overhead, or indirect manufacturing costs)

• The three main types of costs, direct materials, direct labor, and overhead, are often condensed even further:– Direct materials + Direct labor = “Prime costs”– Direct labor + Overhead = “Conversion costs”

Direct and Indirect Product Costs: Further Comments

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

11

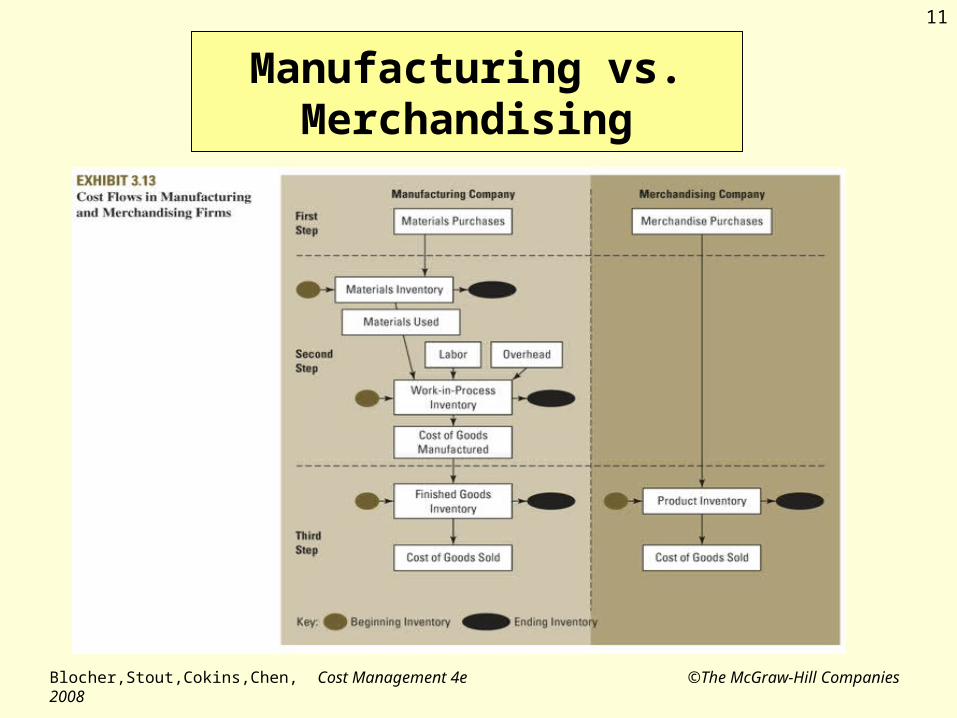

Manufacturing vs. Merchandising

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

12

Inventory and Related Expense Accounts

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

13

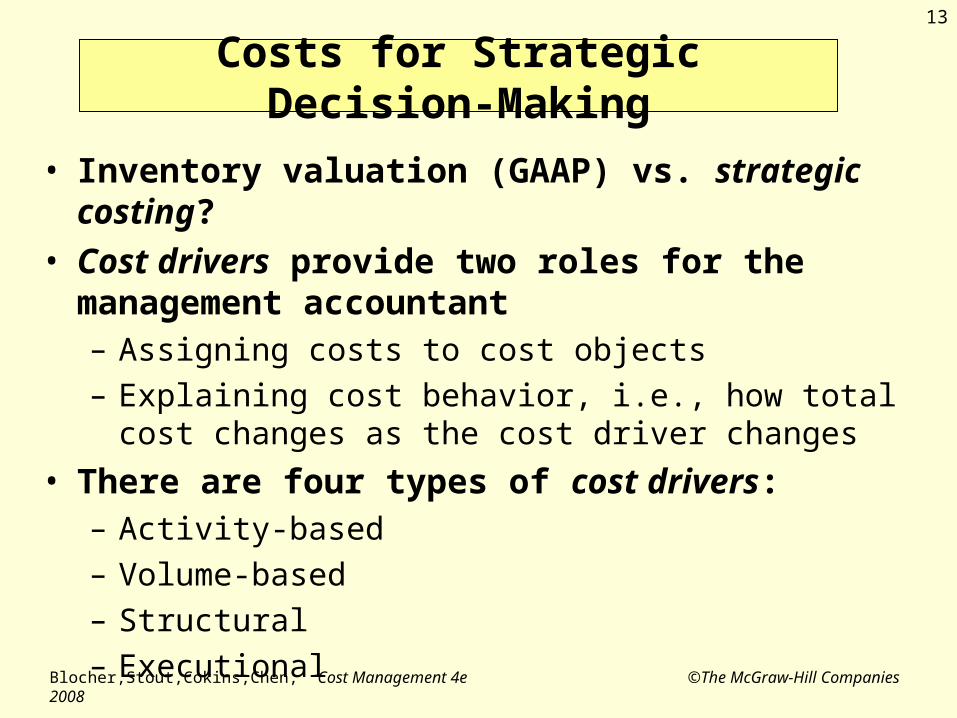

Costs for Strategic Decision-Making

• Inventory valuation (GAAP) vs. strategic costing?

• Cost drivers provide two roles for the management accountant– Assigning costs to cost objects– Explaining cost behavior, i.e., how total cost changes as

the cost driver changes

• There are four types of cost drivers:– Activity-based– Volume-based– Structural– Executional

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

14

Cost Drivers

• Activity-based cost (ABC) drivers are developed at a detailed level of operations using activity analysis–a cost driver is determined for each activity

• Volume-based cost drivers relate to the amount produced or quantity of service provided: – The relationship between the cost driver and total cost

is approximately linear within the relevant range– Outside of the relevant range, the Law of Diminishing

Marginal Returns generally applies (i.e., non-linearities exist)

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

15

• Structural cost drivers facilitate strategic decision making because they involve plans and decisions that have long-term effects– Scale, experience, technology, and complexity are

considered in hopes of improving competitive position

• Executional cost drivers facilitate operational decision making by focusing on short-term effects– Workforce involvement, design of the production

process, and supplier relationships are considered in an attempt to reduce costs

Cost Drivers (continued)

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

16

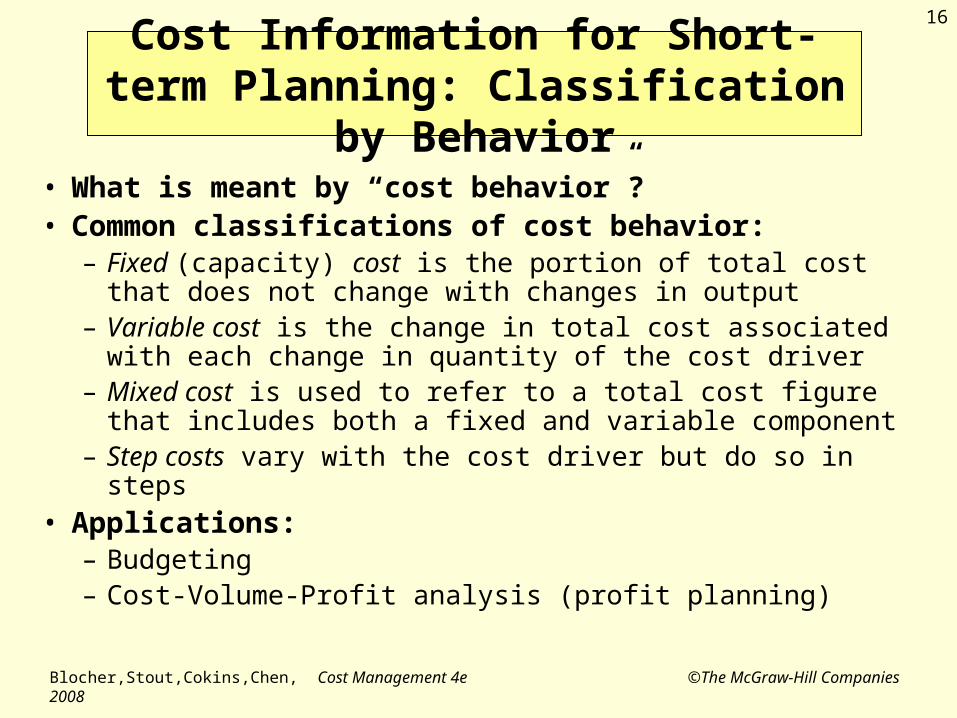

Cost Information for Short-term Planning: Classification by Behavior

• What is meant by “cost behavior”?• Common classifications of cost behavior:

– Fixed (capacity) cost is the portion of total cost that does not change with changes in output

– Variable cost is the change in total cost associated with each change in quantity of the cost driver

– Mixed cost is used to refer to a total cost figure that includes both a fixed and variable component

– Step costs vary with the cost driver but do so in steps• Applications:

– Budgeting– Cost-Volume-Profit analysis (profit planning)

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

17

Fixed Costs

$6,600

$6,500

$3,000

3,500 3,600Units of the Cost Driver

Total Cost

Total Fixed Cost

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

18

Variable Costs

Total Variable Cost

$6,600

$6,500

$3,000

Units of the Cost Driver

Total Cost Total CostTotal Cost

3,500 3,600

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

19

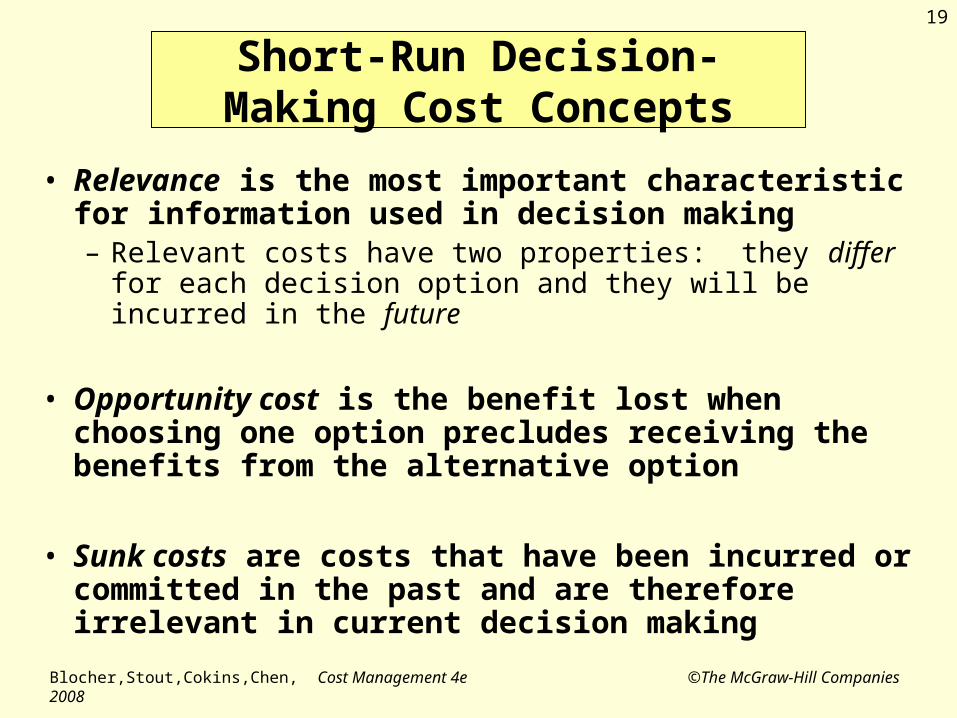

• Relevance is the most important characteristic for information used in decision making– Relevant costs have two properties: they differ for each

decision option and they will be incurred in the future

• Opportunity cost is the benefit lost when choosing one option precludes receiving the benefits from the alternative option

• Sunk costs are costs that have been incurred or committed in the past and are therefore irrelevant in current decision making

Short-Run Decision-Making Cost Concepts

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

20

There are three other characteristics that are important for planning and decision making

– Accuracy (and the need to monitor internal accounting controls)

– Cost and value of cost information (the cost of information should be monitored by the management accountant to ensure that costs do not outweigh the associated benefits)

– Timeliness (often involves sacrificing in the other two areas)

Qualitative Characteristics of Cost Information for Planning

and Decision-Making

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

21

• Controllability is a basic consideration in evaluating managers and providing feedback– A cost is considered “controllable” if the manager

or employee has discretion in choosing to incur it or can influence the amount in a short period of time

• The controllability of some costs is subject to debate, for example, changes in interest rates, foreign exchange fluctuations, or changes in state or local taxes; should the manager be responsible for these changes?

Cost Information for Control/Feedback Purposes

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

22

• There are different ways to classify (or categorize) cost information, depending on the information needs of management (“different costs for different purposes”):

– To prepare financial statements (GAAP)– For strategic decision-making– For short-term planning– For short-term decision-making– For control/feedback purposes

• Product and service costing (GAAP) focuses on differentiating product costs from period costs

• Costs flow through three inventory accounts in a manufacturing firm; merchandising firms have one inventory account

Chapter Summary

Blocher,Stout,Cokins,Chen, Cost Management 4e ©The McGraw-Hill Companies 2008

23

Chapter Summary (continued)

• For strategic decision-making, we think about costs in terms of the following types of drivers: activity-based, volume-based, structural, and executional

• Cost concepts used in short-term planning relate to the behavior of costs (i.e., how they change in response to one or more activities)

• For decision-making we generally classify costs into one of the following categories: relevant, opportunity, or sunk– Relevance, accuracy, timeliness, and value that exceeds cost

are important information characteristics

• Controllability and risk preferences must be assessed when using cost information for management and operational control