23

y/i'^ COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA ANNUAL FINANCIAl REPORT FOR THE YEAR ENDED DECEMBER 31.2011 Release Date.

y/i'^

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR

CANKTON. LOUISIANA ANNUAL FINANCIAl REPORT

FOR THE YEAR ENDED DECEMBER 31.2011

Release Date.

T A B L E O F C O N T E N T S

PAGE

Independent Accountant's Compilation Report 1

Basic Financial Statements

Go^mment*wlde Financial Statements Statement of Net Assets 2 Statement of Actratles 3

Fund Financial Statements Balance Sheet - Governmental Fund 4 Reconciliation ofthe Governmental Funcfs Balance Sheet

to the Stat^nent of Net Assets 5 Statements of Revenues, Expenditures, and Charge in Fund Balance 6 Reconciliation of the Statements of Revenues, Expenditures,

and Change In Fund Balance to the Statement of Activities 7

Notes to Uie Financial Stat&nents 8-14

l^quiPBd Supplementaiy Infomnation Statement of Revenues and Expenditures

Budget and Actual (Cash Basis) - General Fund 15

Chizai S. Fomenoi. CPA James L, Nicholson* Jn, CPA G. Kannelh Pavy, If, CPA Midtael A. Roy, CPA Lisa TrouiDe Manuel. CPA Dana D. Quebedeaux. CPA JOHN S. DOWLING 8E COMPANY

A CORPORATION OF CERTIRED PUBUC ACCOUNTANTS

1 John S. Dowling, CPA

1904-1984 ' John Newton Stout, CPA

1d3$*2005

Retired

Harord Dupre, CPA 1996

Owtgtrt Ledoux, CPA 1998

Joel Landos, Jr., CPA 2003

Russell J. Stelty, CPA 2005

INDEPENDENT ACCOUNTANTS COMPILATION REPORT

The Board of Commissioners Coulee Croche Fire Protection District No. Four Cankton, Louisiana

We have compiled the aooompanying financial statements of the governmental activities and the aggregate, remaining fund Infomiation of Coulee Croche Fire Protection District No. Four, a component unit of the Village of Cankton, as of and for the year ended Decemt)er 31. 2011 vi^lch collectively comprise the District's basic financial statements as listed in the table of contents. We have not audited or revlevired the accompanying financial staten:ients and, aooordingly, do not express an opinion or provide any assurance about whether the financial statenients are in accordance with the accounting principles generally accepted in the United States of America.

The management of Coulee Croche Fire Protection District No. Four is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentatton of the financial statements.

Our responsibility is to conduct the compilation in accordance vtrith the Statennents on Standards for Accounting and Review Services issued by the Anrterican Institute of Certified Public Accountants. The objective of a oomptlation is to assist the management in presenting financial information in the form of financial statements without undertaking to obtain or provide any assurance that there are no material modiftcations that should be made to the financial statements.

The budgetary comparison infomiation on page 15 is presented for the purpose of additnnal analysis. Such infbmnation. although not a required part of the basic financial statentents, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting and for placing the basic financial statements in an appropriate operational, economic, or historical context. The supplementary information has been compiled from information that is the representation of management. W^ have not audited or reviewed the supplementary information and accordingly, we do not express an opinion or provide any assurance on such supplementary information.

Management has not presented the management's discussion and analysis infbrmatbn that the Governmental AcoounUng Standards Board has determined is required supplement, although not required to be a part of, the basic financial statements.

He 6v> 5 O o u i ^ x x ^ C o OpeiDusas. Louisiana March 21,2012

p. 0. Box 1549 47661-49 North Service Road Opetousas, Louisiana 70571-t$49 Telephone 337'94$-464d Tefefax 337'946-6109

BASIC FINANCIAL STATEMENTS

GOVERNMENT-WIDE FINANCIAL STATEMENTS

COULEE CROCHE FIRE PROTECTION DISTRICT NO FOUR CANKTON. LOUISIANA

STATEMENT OF NET ASSETS DECEMBER 31. 2011

ASSETS

GOVERNMENTAL ACTtVmES

Cash Certificates of deposit Taxes receivable (net) Capital assets (net)

$ 2J62 41.271 23,304 70.618

Total assets 137,945

LIABILITIES

NET ASSETS Investment in general fixed

assets, net of related debt Unrestricted

70.616 67.327

Total net assets 137.945

See accompanying notes and independent encountant's compilation report.

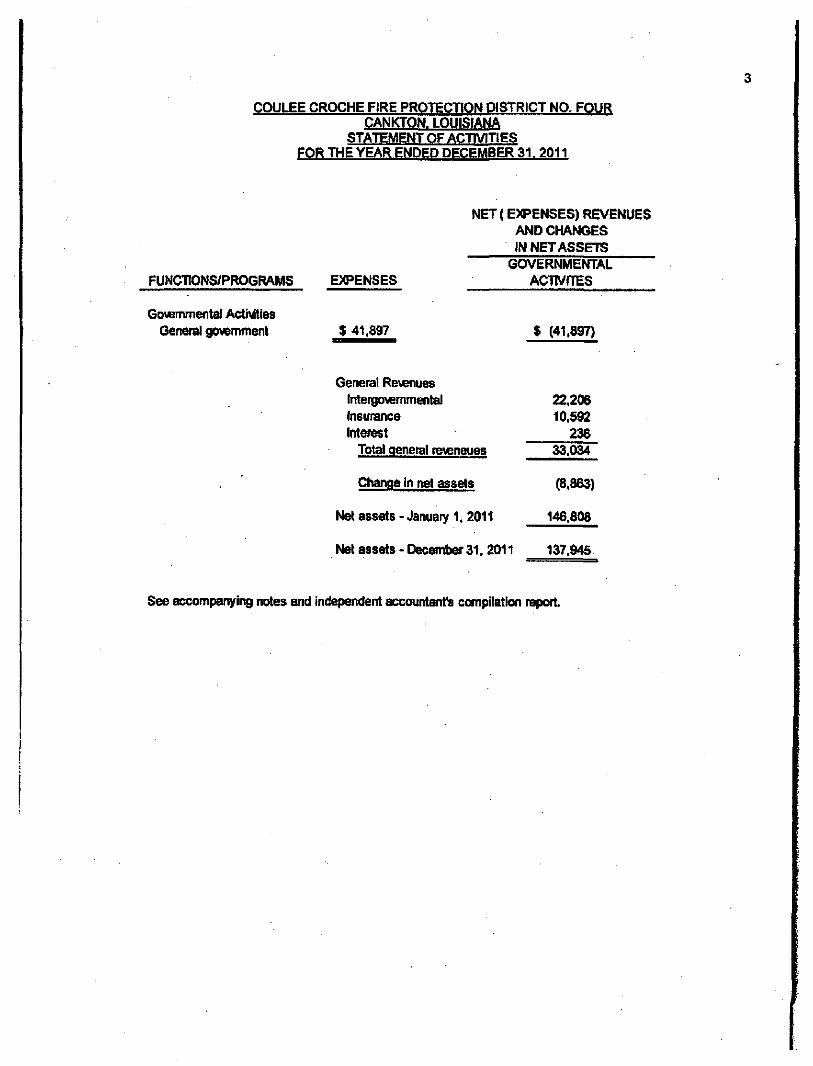

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

STATEMENT OF ACTIVITIES FOR THE YEAR ENDED DECEMBER 31. 2011

NET(EXPENSES) REVENUES AND CHANGES IN NET ASSETS

FUNCTIONS/PROGRAMS

Governmental Activities General govemment

•

E>^ENSES

$ 41,897

General Revenues lntergo>emmental Insurance Interest

Total qenetal reveneues

Change in net assets

Net assets - January 1, 2011

GOVERNMENTAL

Net assets - December 31, 2011

ACTTVflES

$ (41.897)

22,206 10,592

236 33.034

(8,863)

146.808

137.945

See accompanying notes and ind^)endent accountants compilation report.

FUND FINANCIAL STATEMENTS

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

BALANCE SHEET - GOVERNMEI^AL FUND DECEMBER 31. 2011

ASSETS

Cash Certificates of deposit Taxes receivable Less allowance for doubtful

accounts

Total assets

LiftBILfTIES AND FUND BALANCE

LIABiLrnES

FUND BALANCE

Fund balance Unassigned

Total fiind balance

Total liabilities and fund balance

GOVERNMENTAL FUNDTYPE GENERAL

$ 2.752 41,271 25.418

(2,114)

67,327

$ 67,327 67,327

67.327

See accc^panying notes and independent accountant's compilation report.

COULEE CROCHE FIRE PROTECTION DISTRICT ^O. FOUR CANKTON. LOUISIANA

RECONCILIATION OF THE GOVERMENTAL FUND'S BALANCE SHEET TO THE STATEMENT OF NET ASSETS

DECEMBER 31. 2011

Total fiind balance for governmental fiinds

at December 31. 2011 $ 67,327

Cost of capital assets at December 31, 2011 S 221.113

Less: Accumulated depreciation (150,495) 70.618

Net assets of governmental activities at December 31,2011 137,945

See accompanying notes and independent accountant's compilation report.

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

STATEMENT OF REVENUES. EXPENDITURES. AND CHANGE IN FUND BALANCE FOR THE YEAR ENDED DECEMBER 31. 2011

REVENUES Taxes

Property taxes $22,206 Intergovsmmental

Fire insurance tax 10,592 Interest

Interest earned on property taxes 73 Interest earned on checking 62 Interest eamed on CD 101

Total revenues 33.034

EXPENPrrURES Public safi^y

Current operating Accounting 930 Gas. oil. repairs, and maintenance 10,670 insurance 8,563 Miscellaneous 200 Supplies 11.405 Telephone 2,201 Lease 10

Capital outlay Equipment 11,897

Total expenditures 45,876

NET CHANGE IN FUND BALANCE (12,842)

FUND BALANCE, beoinninq of year 80.169

FUND BALANCE, end of vear 67,327 \

See accompanying notes and independent accountant's compilation report.

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

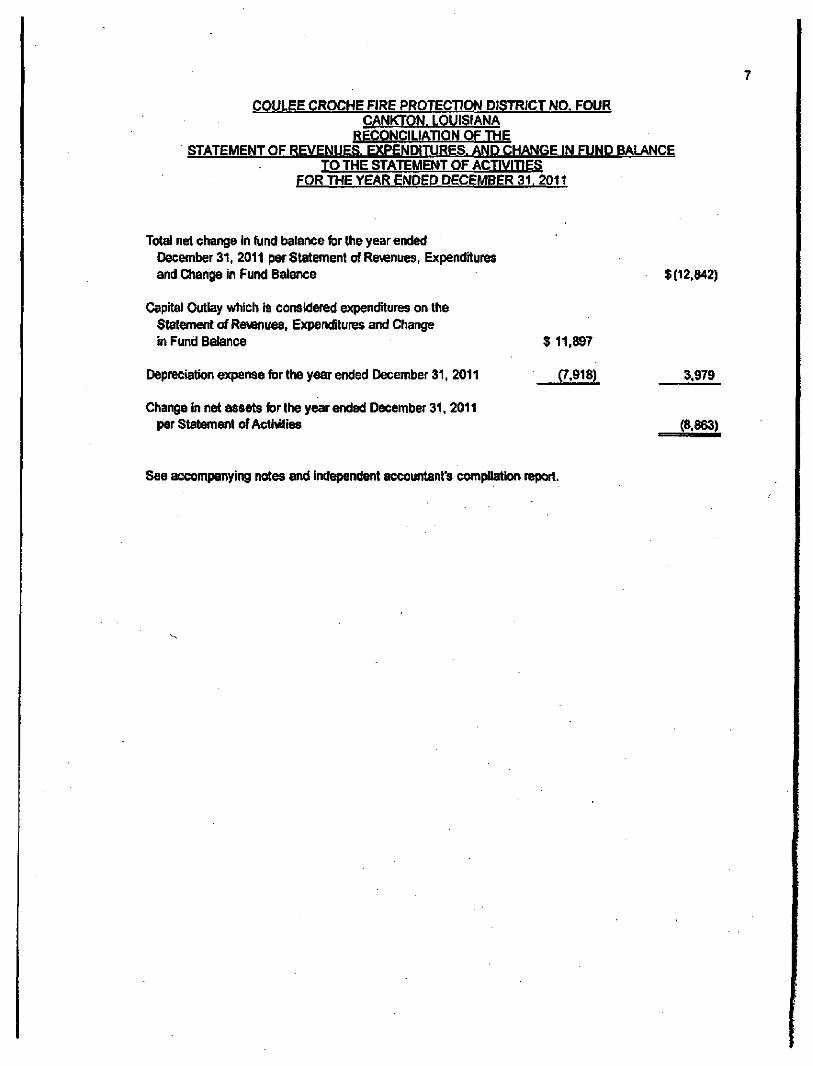

RECONCILIATION OF THE STATEMENT OF REVENUES. EXPENDITURES. AND CHANGE IN FUND BALANCE

TO THE STATEMENT OF ACTIVITIES FOR THE YEAR ENDED DECEMBER 31. 2011

Total net chartge in fund t^alance for the year ended December 31, 2011 per Statement of Revenues. Expenditures and Oiang^ in Fund Balance $(12,842)

Capital Outlay which is considered expenditures on the Statement of Revenues, Expenditures and Change in Fund Balance $ 11,897

Depreciation expense for the year ended December 31, 2011 (7,918) 3.979

Change in net assets for the year ended December 31. 2011 per Statement of Activities (8.863)

See accompanying notes and ind^>endent accountant's compilation report.

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31. 2011

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The aooompanying component unit financial statements of the Coulee Croche Fire Protection District No. Four have been prepared in conformity with generally accepted accounting principles (GAAP) as applied to governmental units. The Governir^ntal Accounting StandanJs Board (GASB) is the accepted standards-setting body for establishing governmental accounting and financial reporting principles.

A. REPORTING ENTITY

As the governing auttiority of the Village, for reporting purposes, the Village of Cankton, Louisiana is tiie financial reporting entity. The financial reporting entity consists of (a) ttie primary government, (b) organizations fbr which the primary government is financially accountable, and (c) otiier organizations for which nature and significance of tiieir relationship with tiie primary government are such tiiat exclusion would cause the reporting entit/s financial statenients to be misleading or incomplete.

Govemrrtental Accounting Standards Board Statement No. 14 established criteria for determining which component units should be considered part of the Village for financial reporting purposes. The basic criterion for including a potential component unit witiiin tiie reporting entity is financial accountaUlity. The GASB has set fbrtt) critena to be considered in determining financial accountability. This criteria includes:

1. Appointing a voting majority of an organization's governing body, and

a. The ability of tiie Village to impose its will on that organization and/or

b. The potential fbr tiie organization to pn^vide specific financial benefits to or impose specific finandal burdens on the Village.

2. Organizations for which the Village does not appoint a voting majority but are fiscally dependent on the Village.

3. Organizations for which the reporting entity financial statements would be misleading if data of the organization is not included because of tiie nature or significance of tiie relationship.

The Coulee Croche Fire Protectton District No. Four consists of five commissioners. Tvvo of the commissioners are appointed by tiie Parish Government and anotiier two are appointed by the Village of Cankton. The fifth commissioner Is selected by the other four members.

Coulee Croche Fire Protection District No. Four leases land from ttie Village of Cankton under a 99 year lease fbr $10 per year Because the District receives a reimbursement from the Village of Cankton. leases land from tiie Village and the Village appoints two commissioners, tiie District is considered to be a component unit of the Village of Cankton. tiie financial reporting entity. The accompanying financial statements present information only on tiie funds maintained by the District and do not present infomiation on tiie Village of Cankton, tiie general government services provided by that government unit, or the otiier governmental units that comprise tiie financial reporting entity.

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31. 2011

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Continued

B. BASIS OF PRESENTATION

Government-wide Rnancial Statements fGWFSV The Statement of Net Assets and tiie Statement of Activities display infomnaition on all of the nonfidudary activities of Coulee Croche Fire Protection District No. Four. They include all funds of the reporting entity. For the most part, tiie effect of interfund activity has been removed from tiiese statements. Governmental activities, which normally are supported by taxes and intergovernmental revenues, are reported separately from business-type activities, which rely to a significant extent on fees and charges for support. Fiduciary funds are not included in the GWFS.

The Statement of Activities demonstrates the degree to which tiie direct expenses of a given fiinctbn or segment are offeet by program revenues. Direct expenses are Uiose that are speclficaity associated witii a progranfi or function and, ttierefore, are clearly identifiable to a particular fijnction. Program revenues include (a) fees and charges paid by the redpients of goods or services offered by the programs, and (b) grants and contributions that are restilcted to meeting the operational or capital requirements of a particular program. Revenues tiiat are not classified as program revenues, induding all tajoes, are presented as general revenues.

Fund Finandal Statements. Coulee Croche Fire Protection District No. Four uses funds to report on its financial position and the results of Its operations. A fund is an Independent fiscal and accounting entity witti a separate set of self-balandng acoounte that comprise its assets, liabilities, fund equity, revenues, and expenditures, or expenses, as appropriate. Government resources are allocated to and accounted for in individual funds based upon the purposes for which tiiey are to be spent and the means by which spending activities are controlled. The fund presented in the finandal statements te described as follows:

Governmental Fund

General Fund - The General Fund is the general operating fund. It is used to account for ail finandal resources.

C. MEASUREMENT FOCUS/BASIS OF ACCOUNTING

Measurement focus is a tenn used to describe "which" ti^nsactions are recorded within the varknis finandal statements. Basis of accounting refers to "when" transactions are recorded regardless of the measurement focus applied.

Measurement Focus

On tiie govemment-wide Statement of Net Assets and ttie Statement of Activities, tiie governmental activities are presented using tiie economic resources measurement focus.

In the fijnd finandal statements, the "current finandal resources* measurement focus or ttie "economic resources" measurement focus is used as appropriate:

a. The fund financial statements utilize a 'current financial resources* measurement focus. Only current finandal assets and liabilities are generally included on Uieir balance sheets. Their operating statements present sources and uses of available spendable finandal resources during a given period. These funds use fijnd balance as tiieir measure of available spendable financial resources at the end ofthe pericKi.

10

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

NOTES TO FfNANClAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31. 2011

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Continued

C. MEASUREMENT FOCUS/BASIS OF ACCOUNTING - Continued

Measurement Focus - Continued

b. The govemment-wide finandal statements utilize an "economic resources* measurement focus. The accounting objective of this measurement focus is the determinatton of operating income, changes in net assets and financial position. All assets and liabilities (whetiier current or noncunent) assodated witii their activities are reported.

Basis of Accounting

In the govemment-wide Statement of Net Assets and Statement of Activities, the governmental activities are presented uaing tiie accnjal basis of accounting. Under tiie accnial basis of accounting, revenues are recognized when eamed and expenses are recorded when tiie liability is incurred or economic asset used. Revenues, expenses, gains, tosses, assets, and liabilities resulting from exchange and exdiange-tike transactions are recognized when the exchange takes place.

Governmental fund finandal statements are reported using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are cdlectible witiiin the current perk)d or soon enough thereafter to pay liabilities of tiie current period. For ttiis purpose, tiie government considers revenues to be available if they are cotleded witiiin 60 days of tiie end of the current fiscal pertod. Expenditures (induding capital outiay) generally are recorded when a liability is incurred, as under accmal accounting.

D. REVENUES. EXPENDITURES. AND EXPENSES

Expenditures/Expenses

In tiie govemment-wide finandal statements, expenses are dassified by fiinction fbr the governmental activities.

In the fund financial statem^its, expenditures are classified as follows:

Governmental Fund - By Character

In the fund financial statements, governmental funds report expenditures of finandal resources:

E- CASH AND INVESTMENTS

Cash and Investments are recorded at cost, which approximates market Louisiana statutes authorize the Distrtet to invest In United States bonds, treasury notes or certificates, time certificates of deposit in state and national banks, or any otiier federally insured investment.

F. RECEIVABLES

In tiie govemment-wide and fiind finandal statements, receivables consist of all revenues earned at year-end and not yet received. Allowances for uncollectible accounts receivable are based upon historical trends.

11

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31. 2011

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Continued

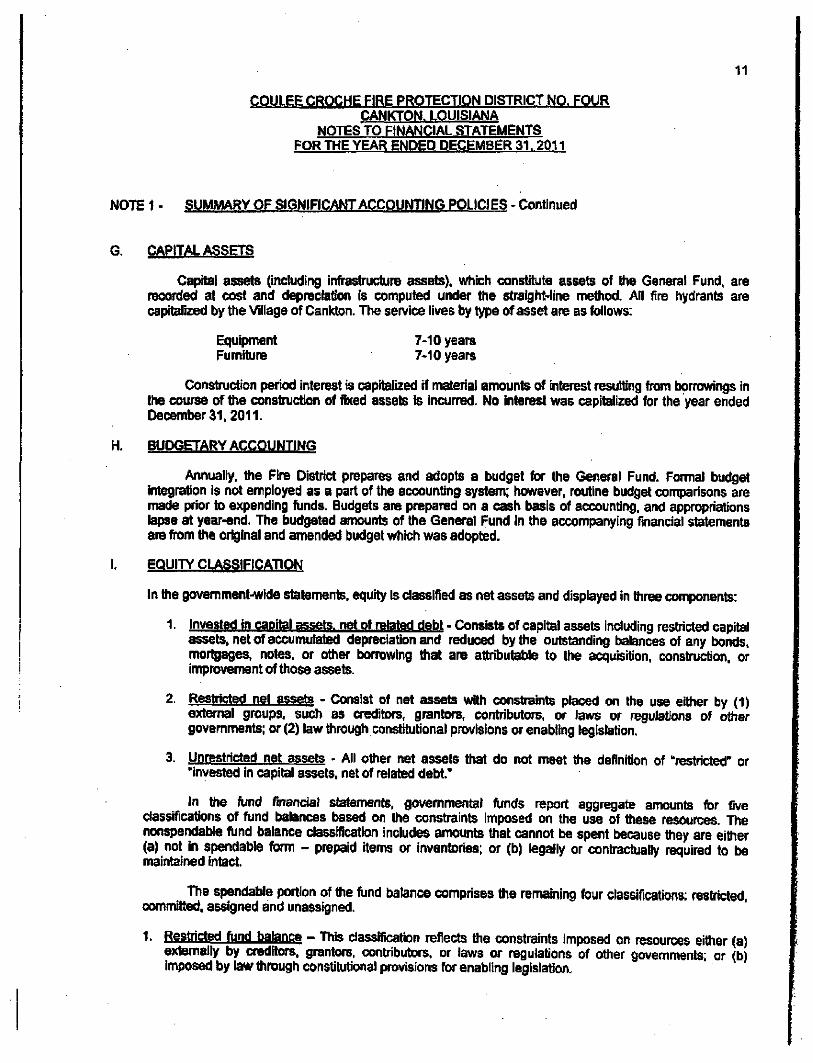

G. CAPITAL ASSETS

Capital assets (induding Infrastructure assets), which constitute assets of tiie General Fund, are recorded at cost and depredation is computed under the straight-line method. All fire hydrants are capitalized by the Village of Cankton. The sen/ice lives by type of asset are as follows:

Equipment 7-10 years Furniture 7*10 years

Construction period interest is capitalized if material amounts of interest resulting from borrowings in tiie «}urse of the construction of fixed assets is incun^. No interest was capitalized for the year ended December 31,2011.

H. BUDGETARY ACCOUNTING

Annually, tiie Fire District prepares and adopts a budget for ttie General Fund. Formal budget integration is not employed as a part of tiie accounting system; however, routine budget comparisons are made prior to expending fiinds. Budgets are prepared on a cash basis of accounting, and appropriations lapse at year-end. The budgeted amounts of tiie General Fund in tiie accompanying financial statements are from tiie crtginat and amended budget which was adopted.

I. EQUITY CLASSIFICATION

In ttie govemment-wlde statements, equity is dassified as net assets and displayed in tiiree components:

1 Invested in caoital assets, net of related debt - Con»sts of capital assets induding restricted capital assets, net of accumulated depreciation and reduced by the outstanding balmices of any bonds, mortgages, notes, or otiier borrowing titat are attributable to the acquisition, constiuction, or improvement of those assets.

2. Restricted net assets - Consist of net assets witii constraints placed on tiie use eitiier by (1) external groups, sudi as creditors, grantors, contributors, or laws or regulations of otiier governments; or (2) law tiirough constitutional provisions or enabling legislation,

3. Unrestricted net assets - All other net assets that do not meet tiie definitk)n of ''restricted* or "invested in capital assets, net of related debt."

In the fund finandal statements, governmental fijnds report aggregate amounts for five classifications of fund balances based on tiie constraints Imposed on ttie use of tiiese resources. The nonspendable fund balance dassificatton indudes amounts ttiat cannot be spent because ttiey are eittier (a) not in spendable form - prepaid items or inventories; or (b) legally or contt-actually required to be maintained intact.

The spendable portion of the ftind balance comprises the remaining four classificatkms; restricted, committed, assigned and unassigned.

t> Restricted fund balance - This dassificatton reflects the constraints imposed on resources eitiier (a) externally by creditore, grantors, oontiibutors. or laws or regulations of otiier governments; or (b) imposed by law tiirough constitutional provisions for enabling legislation.

12

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31. 2011

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Continued

I. EQUITY CLASSIFICATION - Continued

2. Committed fund balance - These amounts can only be used for spedfic purposes pursuant to constraints Imposed by formal resolutions or ordinances of tiie Board- tiie government's highest level of dedsion making authority. Those committed amounts cannot be used for any other purpose unless the judge removes the specified use by taking the same ty(% of action imposing the commitment This classification also includes contractual obligations to the extent that existing resources in the fund have been specifically committed for use in satisfying tiiose conb-actual requirements.

3. Assigned fund balance - This classification reflects tite amounts const^ined by tiie Boarvj's Intent* to be used for spedfic purposes, but are neitiier restricted nor committed. The Board has ttie auttiorHy to assign amounts to be used for spedfic purposes. Assigned fund balances Indude all remaining amounts (except negative balances) tiiat are reported in governmental funds, ottier ttian ttie General Fund, that are not classified as nonspendable and are neittier restilcted nor committed.

4. Unassigned fund balance - This fund balance is the residual dassificatton for the General Fund. It is also used to report negative fund balances in ottier governmental fonds.

When botii restricted and unrestricted resources are available for use. it is ttie Board's polk:y to use externally restricted resources first, then unrestricted resources - committed, assigned and unassigned - in order as needed.

J. BUDGETARY ACCOUNTING

The revenues and expenditures shown on Page 6 are recondled with ttie amounts reflected on the budget comparison on Pages 15 as follows:

2011

Page 6 Revenues $33,034 Add: Property tax received 19,923 Less: Current year revenue - page 6 (22,206)

Page 15 Revenues 30,751

Page 6 Expenditures

Page IS Expenditures

ENCUMBRANCES

The District does not employ the encumbrance system of accounting.

ESTIMATES

The preparation of financial statements in conformity witii accounting prindples generally accepted in ttie United States of America require management to make estimates and assumptions tiiat affect the reported amounts of assets and liabilities and disdosure of contingent assets and liabilities at tiie date of the finandal statements and tiie reported amounts of revenue, expenditures, and expenses during the reporting period. Actual results couki difl^rfi^m tiiose estintatos.

13

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31. 2011

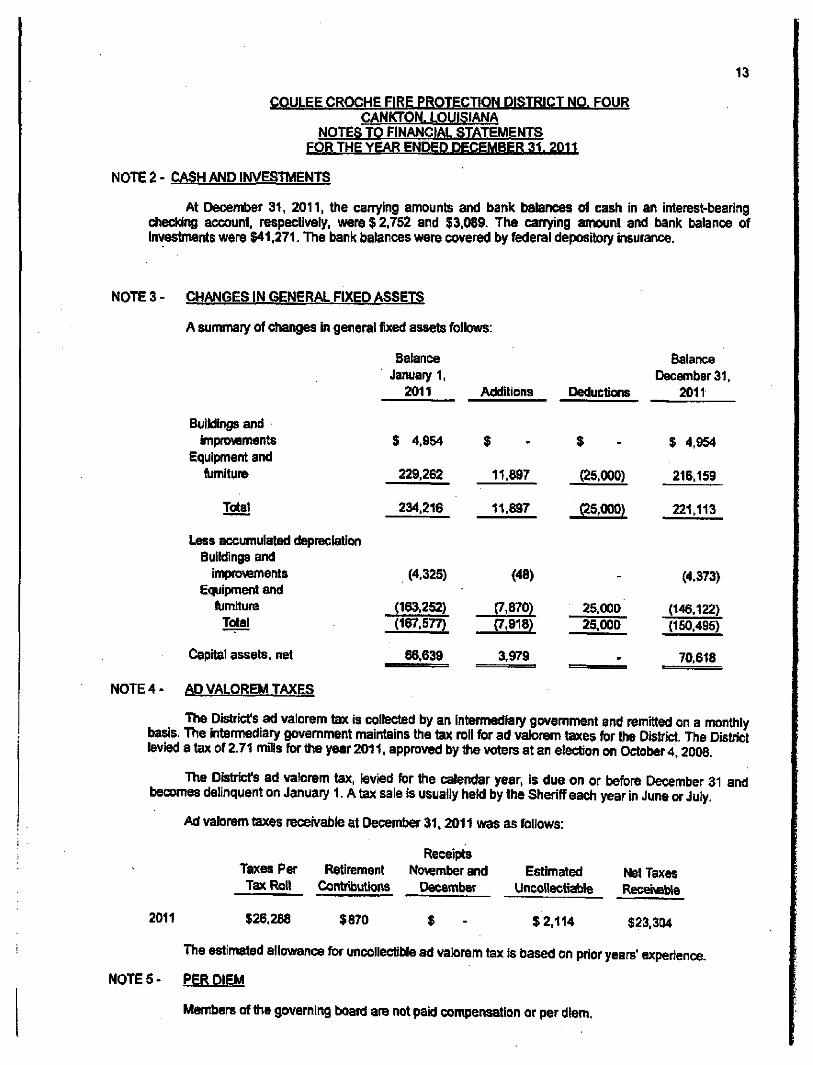

NOTE 2 - CASH AND INVESTMENTS

At Decemt>er 31. 2011, the carrying amounts and bank balances of cash in an interest-bearing cheddng account, respectively, were $ 2,752 and $3,069. The carrying amount and bank balance of investments were $41,271. The bank balances were covered by federal depository insurance.

NOTE 3- CHANGES IN GENERAL FIXED ASSETS

A summary of changes i

Buikfingsand Improvements

Equipment and furniture

Total

n general fixed assets foltows:

Less accumulated depreciation Buildings and

improvements Equipment and

furniture Total

Capital assets, net

Balance January 1,

2011

S 4.954

229,262

234.216

(4.325)

(163,252) (167,577)

66,639

Additions

$

11.897

11.897

(48)

(7.670) (7,918)

3.979

Deductions

$

(25.000)

(25.000)

-

26,000 25.000

•

Balance December 31,

2011

$ 4.954

216,159

221,113

(4.373)

(146.122) (150,495)

70,618

N0TE4- AD VALOREM TAXES

The Dislrtaf s ad valorem tax is collected by an intermediary government and remitted on a montiily basis. The intennediary government maintains the tax roll for ad vakjrem taxes for ttie DIstrtet. The District levied a tax of 2.71 mills for ttie year 2011, approved by ttie voters at an election on October 4,2008.

The Distiicfs ad valorem tax, levied for tiie calendar year, is due on or before December 31 and becomes delinquent on January 1. A tax sale is usually heW by the Sheriff each year in June or July.

Ad valorem taxes receivable at December 31,2011 ui/as as follows:

2011

Taxes Per Tax Roll

$26,268

Retirement Contributions

$870

Receipts November and

December Estimated

Uncollectiable Net Taxes Receivable

$ - $2,114 $23,304

The estimated allovranoe for uncollectible ad valorem tax is based on prior years' experience.

NOTES- PER DIEM

Members of ttie governing board are not paid compensation or per diem.

14

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31. 2011

N0TE6- FUND BALANCE

For ttie year ended December 31, 2011, Coulee Croche Fire Protection Distinct No. Four did not have a defidt fund balance and the fund balance was unassigned.

NOTE 7- COST-SHARING AGREEMENT

On November 7, 2000 tiie Board entered into an agreement witii ttie Village of Cankton and ttie Cankton Volunteer Fire Department to share tiie cost equally of all vehicles used in the conticl of fires wittiin the Fire District These vehteles consist of the two pumper titJCks owned by Coulee Croche Fire Protection Distilct No. Four. The costs include all repairs, operating costs, maintenance and insurance for said vehicles.

It was further resolved that ttie Coulee Croche Fire Protection District No. Four will pay ttie monthly bills for the operation, ete., of these vehides. The two otiier entities will reimburse ttieir one-tiiird share once a year on or about October 31, upon tiie submisston of a stetement from the Disti-ict of tiie expenses for ttie year,

NOTE 8 - OTHER POST - EMPLOYMENT BENEFITS

Coulee Croche Fire Protection District No. Four does not provide any post-employment benefits to retirees otiier ttian pension and ttierefore is not required to report under GASB Statement No. 45, Aocountino and Financial Reoortina fav Employers for Post-emolovment Benefits Other Than Pensions.

N0TE9- SUBSEQUENT EVENTS

Subsequent events were evaluated tiirough March 21, 2011, which is the date the finandal statements were available to be issued. As of March 21,2011 ttiere were no subsequent events noted.

REQUIRED SUPPLEMENTARY INFORMATION

BUDGETARY COMPARISON SCHEDULE

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR CANKTON. LOUISIANA

STATEMEr^ OF REVENUES. EXPENDITURES BUDGET AND ACTUAL fCASH BASIS^ - GENERAL FUND

FOR THE YEAR ENDED DECEMBER 31. 2011

15

REVENUES Taxes

Piopeityt^es Intergovernmental

Rieinsuancetax interest

hterest earned on property taxes Interest eamed on checking Merest ^ m e d on CD

Total revenues

E)PENDrTURES Public safety

Cum^ opeiating Accounting Gas, d l , repairs, and maintenanoe Insuance Supplies Telephone Utilities

Miscdianeous Capitat outlay

Eqiipment Total expenditures

NETCHANGE IN FUND BALANCE

ORIGINAL

$24,750

11,500

400

36,650

GENERAL FUND

FINAL

S 15.143

10,538

261

25.942

ACTUAL

$19,923

10,592

73 62

101 30.751

VARIANCE FAVORABLE

(UNFAVORABLE)

$ 4,780

54

(188) 62

101 4.B09

975 6.500 9.000

400 1.600

96 10

200

2.000 20.781

15.669

930 10.719 6,750

86 2,201

96 10

104

23,216 44.112

(18.170)

930 10.670 8.563

11,405 2.201

-10

200

11.897 45,876

(15,125)

49 (1.813)

(11.319)

96

(96)

11.319 (1.764)

3.045

Affidavit and Revenue Certification

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR ENTITY NAME

ST LANDRY PARISH

CANKTON. LOUISIANA

ANNUAL SWORN FINANCIAL STATEMENTS AND CERTIFICATION OF REVENUES $50,000 OR LESS (if applicable)

The annual sworn financial statement are required by Louisiana Revised Statute 24:514 to t>e filed with the Legislative Auditor within 90 days after the close ofthe fiscal year. If applicable, the certification of revenues $50,000 or less is required by Louisiana Revised Statute 24:513(l)(1)(c)(i). (The threshold is $200,000 for Justices of the Peace and Constables,)

»»*»*»«*****»•***•***»»*»»*»»»»* * * • » * • * * * * ' * * * * * * * *» in i irtminnniiniiitimmminnrt***** • * *»< * * * >*»***»****<

Personally came and appeared before the undersigned authority, ELMO BROUSSARD. JR (name), who, duly sworn, deposes and says that the financial statements herewith given present fairly the finandal position of COULEE CROCHE FIRE PROTECTION D»STRICT NO. FQUR(entitv name) as of DECEMBER 31.2011. and the results of operations for the year then ended, in accordance with the basis of accounting described within the accompanying financial statements.

(Complete if applicable) In addition, ELMO BROUSSARD. JR. (name), who. duly sworn, deposes and says that COULEE CROCHE FIRE PROTECTION DISTRICT NO, FOURfentitv name) received $50,000 or less in revenues and other sources for the year ended DECEMBER 31.2011. and accordingly, is not required to have an audit for the previously mentioned year.

Signature

Swom to and subscribed before me this j f l day of hMl({r i 20i^.

Officer Name ELMO BROUSSARD. JR

Title SECRETARY/ TREASURER ^

Address 628 MAIN STREET-

CANKTON. LOUISIANA 70584

Telephone No. 337-668^373

Fax No. NONE