33

Country update: Australia Anthony Klein Partner, PwC Australia Liam Collins Partner, PwC Singapore www.pwc.com

Country update:Australia

Anthony KleinPartner, PwC Australia

Liam CollinsPartner, PwC Singapore

www.pwc.com

PwC

Agenda

1. Economic and social challenges

2. Tax and politics

3. Recent developments

4. 2015 Federal Budget – key announcements

5. Regulatory environment – changes at the ATO

6. Q&A

2Global Tax Symposium – Asia 2015

PwC

Economic and social challenges

3Global Tax Symposium – Asia 2015

PwC

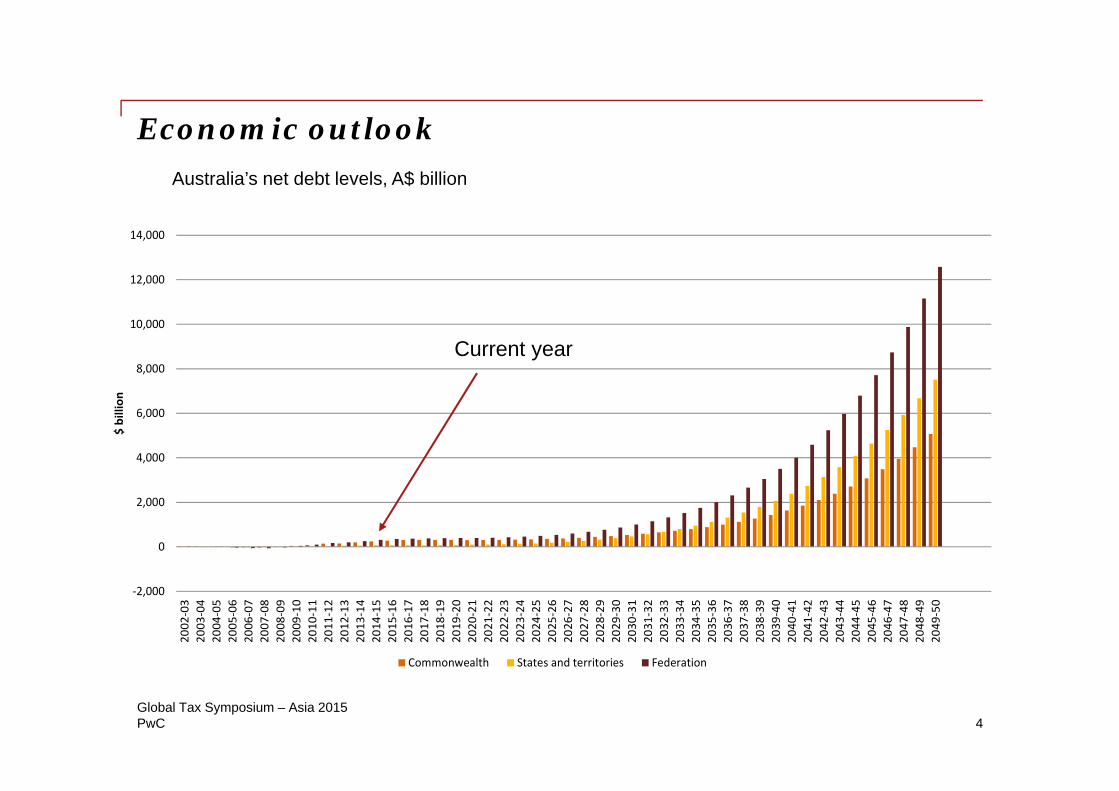

Economic outlook

4

‐2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2002

‐03

2003

‐04

2004

‐05

2005

‐06

2006

‐07

2007

‐08

2008

‐09

2009

‐10

2010

‐11

2011

‐12

2012

‐13

2013

‐14

2014

‐15

2015

‐16

2016

‐17

2017

‐18

2018

‐19

2019

‐20

2020

‐21

2021

‐22

2022

‐23

2023

‐24

2024

‐25

2025

‐26

2026

‐27

2027

‐28

2028

‐29

2029

‐30

2030

‐31

2031

‐32

2032

‐33

2033

‐34

2034

‐35

2035

‐ 36

2036

‐37

2037

‐38

2038

‐39

2039

‐40

2040

‐41

2041

‐42

2042

‐43

2043

‐44

2044

‐45

2045

‐46

2046

‐47

2047

‐48

2048

‐49

2049

‐50

$ billion

Commonwealth States and territories Federation

Australia’s net debt levels, A$ billion

Current year

Global Tax Symposium – Asia 2015

PwC

Impact of iron ore prices and AUD

5

1980 to 2015

0.1000

0.3000

0.5000

0.7000

0.9000

1.1000

1.3000

1.5000

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

200.00

Iron Ore Price

AUD:USD

Global Tax Symposium – Asia 2015

PwC

Domestic challenges

Domestic economy

• Declining per capita income

• Government spending previously underpinned by resources boom –now less affordable

• As a consequence, deficits ‘as far as the eye can see’

• A Government short on political capital

Demographic challenges

• Ageing population

• Declining ratio of working age individuals to retirees

6Global Tax Symposium – Asia 2015

PwC

What might tax reform look like

What’s on the table

• Everything, in theory

• Lower corporate tax rate?

• Broader base and higher rate for GST?

Challenges to reform

• A wide range of powerful interest groups

• Dysfunctional Senate

• Federation

• A misunderstanding that BEPS process will fix everything

7Global Tax Symposium – Asia 2015

PwC

Composition of the Senate

8Global Tax Symposium – Asia 2015

PwC

But it’s not all bad news (1/2)

Stable, mature market

• Relatively low sovereign risk

• Strong rule of law

• Strong financial sector

• Well regulated markets

• Highly educated and skilled workforce

• Good quality of life

9Global Tax Symposium – Asia 2015

PwC

But it’s not all bad news (2/2)

Opportunities for investment

• Continued infrastructure privatisation

• Real property sector strong

• Agriculture – clean, safe and plentiful

• Growing tech sector

10Global Tax Symposium – Asia 2015

PwC

Tax and politics

11Global Tax Symposium – Asia 2015

PwC

Tax and political events

Global Tax Symposium – Asia 201512

1 January 2017

Anti hybrid rules operative

1 January 2017

UK anti hybrid rules operative

1 January 2017

Anti hybrid rules operative

7 May 2015

UK election

1 January 2017

Anti hybrid rules operative

1 April 2015

UK Google Tax operative

1 January 2017

Anti hybrid rules operative

18 March 2015

UK announces anti hybrid

rules

1 January 2017

Anti hybrid rules operative

3 December 2014

UK Google Tax announced

1 January 2017

Anti hybrid rules operative

5 November 2014

“Lux Leaks”

1 January 2017

Anti hybrid rules operative

5 October 2014

7 Deliverables

1 January 2017

Anti hybrid rules operative

12 May 2015

Australian Federal Budget

1 January 2017

Anti hybrid rules operative

10 April 2015

“Netflix Tax” announced

1 January 2017

Anti hybrid rules operative

30 March 2015

Tax White Paper released1 January 2017

Anti hybrid rules operative

2 October 2014

Senate Inquiry announced

1 January 2017

Anti hybrid rules operative

26 September 2014

Tax Justice Report

released

1 January 2017

Anti hybrid rules operative

Late 2015

Green Paper to be released

1 January 2017

Anti hybrid rules operative

Late 2015ATO

mandatory reporting of

taxpayer information

1 January 2017

Anti hybrid rules operative

12 February 2013

BEPS

1 January 2017

Anti hybrid rules operative

19 April 2013

“Tax Transparency

and BEPS”

1 January 2017

Anti hybrid rules operative

19 July 2013

BEPs Action Plan

1 January 2017

Anti hybrid rules operative

8-10, 22 April 2015

Senate Hearings

1 January 2017

Anti hybrid rules operative

8 October 2015

Final 15 Deliverables

Dom

esti

cIn

tern

atio

nal

1 January 2017

Anti hybrid rules operative

14 May 2013

25-90 repeal announced

1 January 2017

Anti hybrid rules operative

November2013

25-90 retained

PwC

ATO needs to ‘man up’ on tax dodges

Michael WestSydney Morning Herald

Big business ‘shirks’ fair share of tax load

Sydney Morning Herald

Global Tax Symposium – Asia 201513

Senate inquiry demands answers from low-tax companies

Sydney Morning Herald “Ultimately, sustainable, well-run businesses should pay a fair level of tax, and avoid the reputational, legal and financial risks posed by overly aggressive tax planning. Doing so is in their interests, the interests of their shareholder and the interests of the long-term health of the global economy.”

Fiona Reynolds Managing Director, UN PRI Tax Justice Network’s

report on business is a hatchet job

Sydney Morning Herald

Tax on the front page

PwC

“When 29 per cent of Australia’s largest listed companies are paying an effective tax rate of 10 per cent or less, it’s clear that the system is broken”

David O’ByrneNational Security, United Voice

Tax minimisation practices of a minority of very large companies have a significant and disproportionate impact on Australia’s corporate tax revenue base

Who Pays For Our Common Wealth?

Global Tax Symposium – Asia 201514

…there should be a cohesive and clear legal framework that enables all taxpayers, large and small, to be confident that they are complying with their legal obligations.

Frank DrenthCorporate Tax Association

ASX 200 company tax avoidance bleeds Commonwealth coffers of billions a year, report finds

Heath Aston & Georgia WilkinsSydney Morning Herald

Tax on the front page

PwC

Recent developments

15Global Tax Symposium – Asia 2015

PwC

Australia’s international tax landscape

Corporate tax rate 30%

Withholding taxes

- Dividends 30% But, dividend imputation, conduit foreign income and lower for treaty residents

- Royalties 30% But, lower for treaty residents

- Interest 10% But, maybe lower for certain treaty residents (e.g. banks)

Taxation for foreign investors YesBut limited to: - Australian sourced income; and - CGT on Taxable Australian Property

Integrity measures

- Thin cap regime Yes Generally 1.5:1 safe harbour

- Anti avoidance measures Yes Existing GAAR and proposed multi-national anti avoidance rule (PE)

- BEPs agenda Yes Australia leading the charge – CbC, CRS,

- CFC regime Yes

16Global Tax Symposium – Asia 2015

PwC

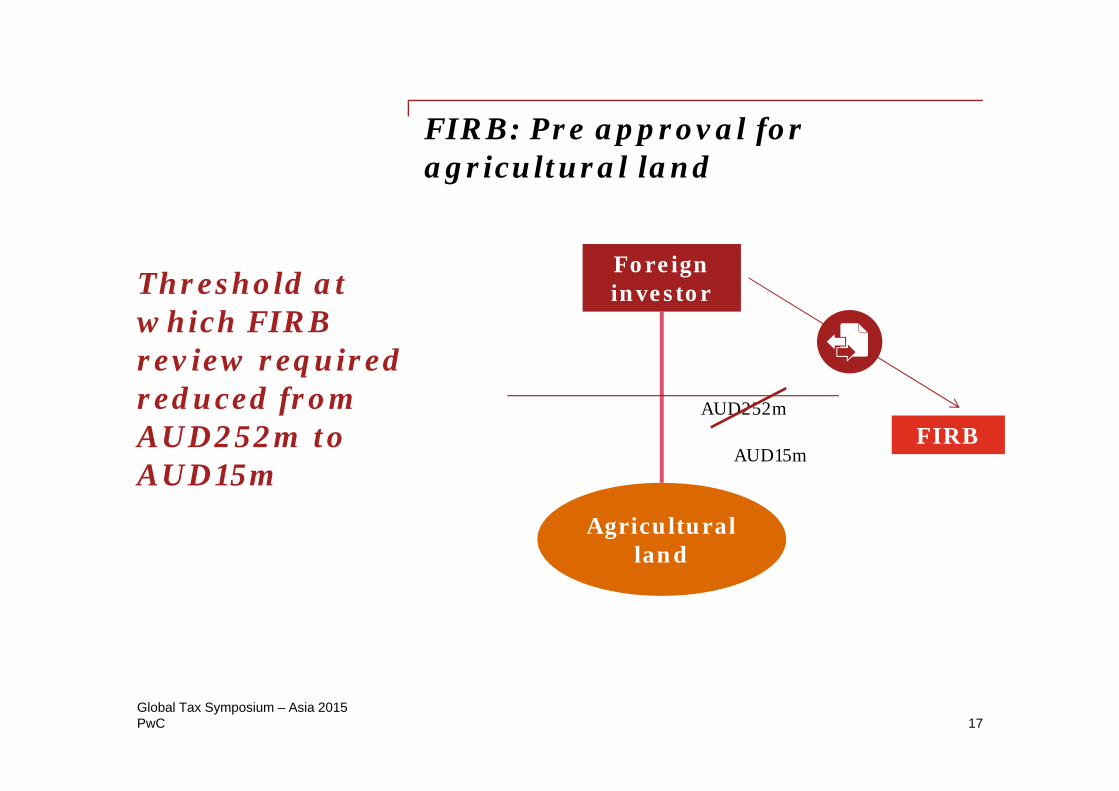

FIRB: Pre approval for agricultural land

Threshold at which FIRB review required reduced from AUD252m to AUD15m

17

Foreign investor

FIRB

Agricultural land

AUD252m

AUD15m

Global Tax Symposium – Asia 2015

PwC

Proposed fees for foreign investment applications

Minimum AUD5,000 application fee for FIRB review of real estate investments

18

Foreign investor

Rural land

AUD5,000

FIRB

Global Tax Symposium – Asia 2015

PwC

Proposed increase in Victorian stamp duty for foreign purchasers

Additional 3% stamp duty upon purchases of Victorian residential land

19

Foreign investor

5.5%

Vic SRO

$$

8.5%

Global Tax Symposium – Asia 2015

PwC

Investment Manager Regime

Provides certainty to foreign investors on taxation of Australian managed investments

20

Foreign investor

Australian manager

Management services

PE?Australian investments

Global Tax Symposium – Asia 2015

PwC

Premium Investor Visas

Significant Investor Visa (SIV) programme was introduced to compete effectively for high net work individuals seeking investment migration

Proposed to extend programme to include Premium Investor Visa (PIV) with effect from 1 July 2015.

PIV has:

• higher investment threshold (AUD15m)

• a more focused eligible investment class, including:

Private equity/start up funding; and

LICs and emerging ASX listed companies.

• shorter time frames (12 months)

Proposed new visa programme to attract entrepreneurial skill and talent to Australia

21Global Tax Symposium – Asia 2015

PwC

2015 Federal Budget – key announcements

22Global Tax Symposium – Asia 2015

PwC

Snapshot of budget changes

Measure Application Progress

Double penalties for large companies Income years from 1 July 2015

Multinational anti-avoidance law 1 January 2016

Transfer pricing documentation (country by country reporting) 1 January 2016

GST on digital B2C 1 July 2017

Targeting treaty abuse Apply to future treaties

Anti-hybrid measures Board of Tax consultation

Tax transparency code Board of Tax consultation

Global Tax Symposium – Asia 201523

PwC

Multinational anti-avoidance

Directly or indirectly related to

supply

ConnectionSupply

Foreign supplier

MNC

Low or No TaxNo Substantial

Activity

AustralianActivitiesCustomer

PE

Principal purpose

Reducing any taxes

Global Tax Symposium – Asia 201524

PwC

Goods and services tax (1/2)GST on digital products and services – the ‘Netflix Tax’

From 1 July 2017, GST will be payable on qualifying supplies of anything other than goods or real property to a non-registered ‘Australian consumer’, including:

• supplies of digital products such as streaming or downloading of movies, music, apps, games, e-books; and

• other services such as consultancy and professional services.

25Global Tax Symposium – Asia 2015

PwC

Goods and services tax (2/2)GST on digital products and services – the ‘Netflix Tax’

Supplies made through an online intermediary (such as websites, gateways, stores or market places).

• GST collected through a reverse charge mechanism.

• Intermediary to remit the GST.

Projected annual revenue of AUD150m – AUD200m

26Global Tax Symposium – Asia 2015

PwC

Regulatory environment – changes at the ATO

27Global Tax Symposium – Asia 2015

PwC

Changes at the ATO and what this means for you

• New Commissioner appointed (Jan 2013), first external to ATO

• Driving a massive cultural change agenda, including redundancy

programme and external hires at senior levels

• Alternative dispute resolution focus

• New ATO processes enable disputes to be resolved sooner

(e.g. independent review, settlements)

• Opportunities and challenges for taxpayers

Global Tax Symposium – Asia 201528

PwC

Tax transparency

• Australia to implement the OECD’s new transfer pricing documentation package, including requirement to file with ATO:

country by country reporting;

a master file; and

a local file that provides detailed information about the local taxpayer’s intercompany transactions.

• Many companies proactively considering their tax transparency strategy

Global Tax Symposium – Asia 201529

PwC

Assume three corporate tax entities (A1 Ltd, B1 Ltd and C1 Ltd) have total income of $100m or more in the 2013-14 income year, and a fourth company (Z Ltd) has a total income of $80m in the same income year.

The Commissioner will make the following information publicly available in relation to that income year.

30

Schedule 5 – tax secrecy and transparency

Name ABN Total Income Taxable Income Income Tax

A1 Ltd 10 234 567 890 $500,000,000 $200,000,000 $60,000,000B1 Ltd 97 876 543 210 $300,000,000 $150,000,000 $40,000,000C1 Ltd 10 293 847 756 $120,000,000 - -

T5

6S 7T

Global Tax Symposium – Asia 2015

PwC 31

Schedule 5 – transparency creating confusion

A CoB CoC CoD Co

Total Income

Taxable Income

Income Tax

1,000 10 31,000 150 451,000 300 901,000 250 75

%

0.3%4.5%9%

7.5%

Margin

1%15%30%25%

1 Retail2 Mining3 Technology 4 Banking

Global Tax Symposium – Asia 2015

PwC

Q&A

32Global Tax Symposium – Asia 2015

Thank you.

The information contained in this presentation is of a general nature only. It is not meant to be comprehensive and does not constitute the rendering of legal, tax or other professional advice or service by PricewaterhouseCoopers Ltd. ("PwC"). PwC has no obligation to update the information as law and practices change. The application and impact of laws can vary widely based on the specific facts involved. Before taking any action, please ensure that you obtain advice specific to your circumstances from your usual PwC client service team or your other advisers.

The materials contained in this presentation were assembled in May 2015 and were based on the law enforceable and information available at that time.

© 2015 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.