CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited March 26, 2020 DOCUMENT INTENDED TO PROVIDE INSIGHT AND BEST PRACTICES RATHER THAN SPECIFIC CLIENT ADVICE COVID-19: GCC Board of Directors Institute webinar

Transcript

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company

is strictly prohibited

March 26, 2020

DOCUMENT INTENDED TO PROVIDE INSIGHT AND BEST PRACTICES RATHER THAN SPECIFIC CLIENT ADVICE

COVID-19: GCC Board of Directors Institute webinar

McKinsey & Company 2

Agenda

01 Covid-19 the situation and possible scenarios

How is the private sector reacting to the crisis?04

How are governments reacting to the economic impacts?

03

How might the crisis impact the global economy?02

Q&A with panelist05

McKinsey & Company 3

COVID-19 has been expanding exponentially with devastating economic impact

It took the world 65

days to get to first

100,000 cases and only

2 for the last 100,000

cases

3

Within first two months

of the outbreak (Jan-

Feb) China’s economy

fell by 10-20%

32% of S&P500 index

wiped out since its

record closing high on

Feb 19

50% of COVID-19 ICU

patients are dying due to

scarcity of medical staff

and equipment

US is expecting a loss

of 5 million jobs —

unemployment rate

soaring to north of 10%

Current as of March 25, 2020

McKinsey & Company 4Source: World Health Organization, CDC, news reports

1.Previously counted only countries; now aligned with

new WHO reports; excluding cruise ship;

2.Previously noted as community transmission in

McKinsey documents; now aligned with WHO definition

The global spread is accelerating with more reports of local transmissionLatest as of March 25,

2020

Impact to date

>20,000

~80% >500.2%Europe’s share of new cases

reported globally on March

18th-25th

Countries that reported their

first case between March

18th-25th

China’s share of new cases

reported globally March 17th-

25th

Countries or territories with

evidence of local

transmission2

Countries or territories with

more than 100 reported

cases1

Countries or territories with

reported cases1

>150 >30>170

DeathsReported confirmed cases

>450,000

Current as of March 25, 2020

McKinsey & Company 5

COVID-19 appears to be more dangerous than the fluLatest as of March 25, 2020

Current as of March 25, 2020

1.Evidence on exact numbers are emerging, however expected to decrease as viral containment measures intensify and treatments are developed

2.WHO estimates 15% severe and 5% critical

3.WHO estimates the global average CFR at 3.4%, dependent on conditions such as patient age, community immunity, and health system capabilities. Latest

case fatality ratios were calculated as death/ cases

4.In outbreak setting or the introduction of a new disease

5.Estimates are very context and time-specific, however are provided from prior outbreaks based on academic lit review

6.Case Fatality numbers reflect outbreak settings and factors such as the patient's age, community immunity and health system capabilities

Source: World Health Organization, CDC, Nature, The Lancet, PLOS One The Journal of Infectious Diseases, BMC Infectious Diseases, Infectious Disease

Modelling, news reports

Case Fatality Ratio (CFR) in South Korea

after widespread testing. CFR appears

higher where cases are missed and is

higher when health systems are

overwhelmed3

~0.9%

Of cases are severe/critical2

Up to 20%Reproduction

number3

(average

number

of people

infected by

each infected

person

in outbreak

setting)

Medium (2-15%) High (>15%)Low (<2%)

Medium (2-4)

High (>4)

Low (0-2)

Case Fatality6 (proportion of deaths among confirmed cases)

D

G

K

I

A

E

FJ

Zika

Chickenpox

SARS-CoV

COVID-19

Polio5

Measles5

Influenza 1918

Smallpox

MERS-CoV

Ebola (West

Africa 2014)Influenza H1N1 2009

Influenza H2N2 1957B

C

H

Features of the disease to date1 Comparison to other diseases4

Early identification of the disease, intensification of viral control, and treatment, when available, will reduce

reproduction number and case fatality

Higher reproduction than the flu

1.5-2x

McKinsey & Company 6

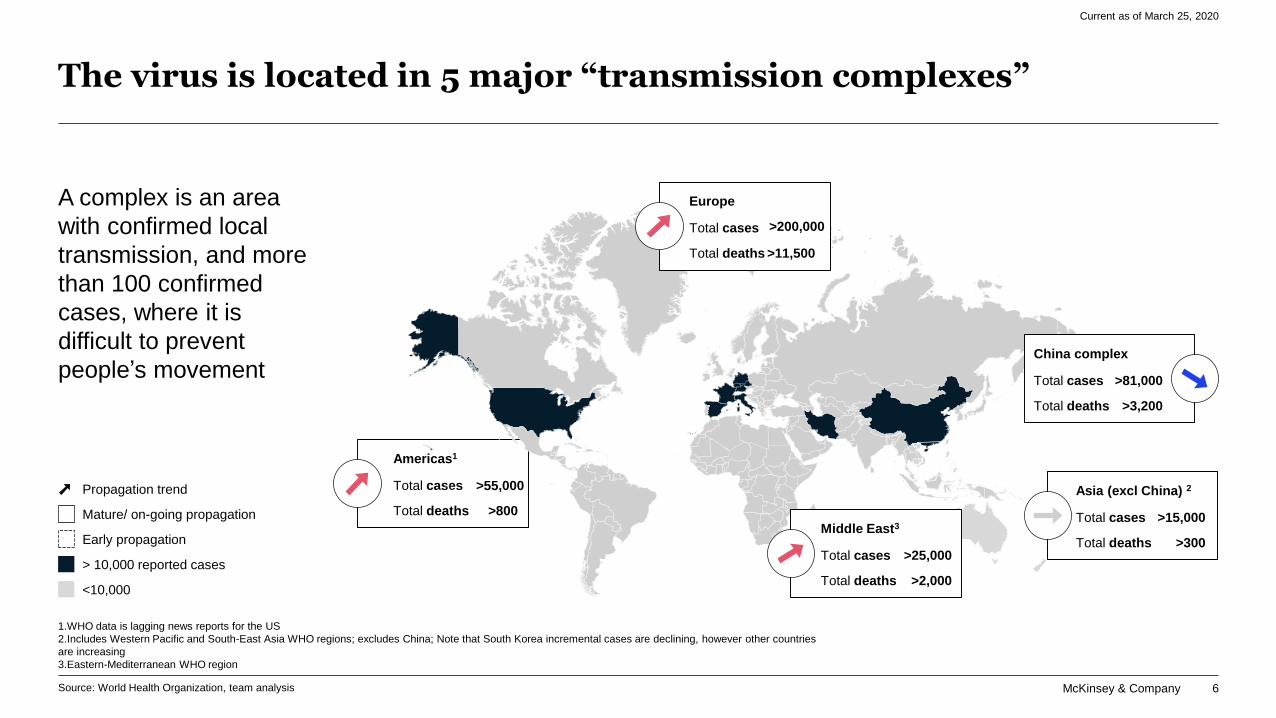

The virus is located in 5 major “transmission complexes”

Current as of March 25, 2020

Source: World Health Organization, team analysis

1.WHO data is lagging news reports for the US

2.Includes Western Pacific and South-East Asia WHO regions; excludes China; Note that South Korea incremental cases are declining, however other countries

are increasing

3.Eastern-Mediterranean WHO region

Americas1

Total cases

Total deaths

>55,000

>800

Asia (excl China) 2

Total cases

Total deaths

>15,000

>300Early propagation

Mature/ on-going propagation

Propagation trend

> 10,000 reported cases

<10,000

Middle East3

Total cases

Total deaths

>25,000

>2,000

Europe

Total cases

Total deaths

>200,000

>11,500

China complex

Total cases

Total deaths

>81,000

>3,200

A complex is an area

with confirmed local

transmission, and more

than 100 confirmed

cases, where it is

difficult to prevent

people’s movement

McKinsey & Company 7

Nations’ strategic approach in mitigating COVID-19 varies based on their testing, social distancing, and quarantine processes

McKinsey & Company 7

Delayed response Proactive

UK Italy China South Korea Singapore

1 2 3 54

First Adopted a limited

approach to social

distancing taking into

account short and long

term of contraction on

the economy, aiming to

preserve as much of

normal life as possible

But subsequently

aligned their approach

with the rest of the world

to adopt stringent policy

measures

Whole country under

lockdown with sever

travel and mobilization

restrictions

High focus on recruiting

healthcare workers to

deal with strain on the

system

Cancelled all large

gatherings, restricted

restaurant hours, and

closed schools

Responded forcefully by

implementing very

stringent rules to limit

the spread (strict

containment and

quarantine)

Implemented proactive

screening, testing, and

disinfection processes

Construction of

makeshift hospitals to

increase capacity and

meet increased demand

Strategy centers around

free, high volume testing

across 600 locations to

mitigate spread (passed

mandatory testing law)

Prevention measures

include an aggressive

and transparent

information campaign,

disinfection of

contaminated sites, and

quarantine of infected

persons

Decisive mobilizing

actions to trace, test,

isolate, and treat have

contributed to effective

containment of the

outbreak

Focusing on fostering

understanding and

social responsibility

4k+ close contact cases

quarantined

McKinsey & Company 8

The degree of lockdown (social distancing) best practice is assessed based on the health risk and economic impactBased on i/ level of criticality of the activity for society and ii/ contamination risk

Level 3

Level 2

Level 1

Low Medium High

Criticality

of

economic

activity

Critical enabler sectors (for a short period of time only): 39 types of economic activities – critical to maintain

Level 3 economic activities functioning

B2B: e.g. logistics / warehousing, wholesale of food and pharma, food and pharma plants

B2C: e.g. banking services

Critical sectors– always maintain operations: 38 types of economic activities – essential and critical for the

B2C: healthcare facilities, pharmacies, food retail stores, limited number of hotels, home delivery services

Other-Services A : 56 types of

economic activities

(E.g., professional services,

holding companies, hotels,

personal services)

Other-Manufacturing: 23 types

of economic activities

(e.g., fertilizer plants,

downstream oil, building

materials)

Other-Services B: 51types of

economic activities

e.g., schools, leisure, sports and

entertainment

Risk of spreading contagion

McKinsey & Company 9

Internationally a range of strategies are being employed to rapidly increase supply

Source: Expert interviews

Existing and repurposing

supply of ventilators

1 USRe-deploying older

ventilators, which work

but do not connect to

modern electronic

records systems

2 ItalyDrafting army

technicians to

production lines to

increase production

3 SingaporeExemptions for foreign

workers from Malaysia

to increase production

capacity

Innovations

Open source ventilator

using readily available

materials (PLA plastic),

3D printing and open-

source hardware

resources

4 Ireland

Precise 3D printing for

critical components to

manage shortages5 Italy

Consortium of auto and

aerospace

manufacturers to create

a new low cost ventilator

in 2 weeks3

6 U.K.

McKinsey & Company 10

Confirmed /

Suspected case Close contact

Secondary

contactCasual contact

Self monitoring (until

suspected case tests

negative)

Rest & recovery

Follow public health

authorities guidelines

Self-isolation (until

suspected case tests

negative)

Self monitoring (until

suspected case tests

negative)

Close and prolonged

interaction

Close and prolonged

interaction

Brief and distant

contact

An employee’s health status or degree of contact will result in differing outcomes

Example:

Living with confirmed /

suspected case

Sharing a room with a

confirmed / suspected

case

Example:

Rode elevator with a

confirmed/suspected

case

Attended event with

confirmed/suspected

case

Example:

Living with a close

contact of a confirmed

/ suspected case

Sharing a room with a

close contact of a

confirmed / suspected

case

McKinsey & Company 11

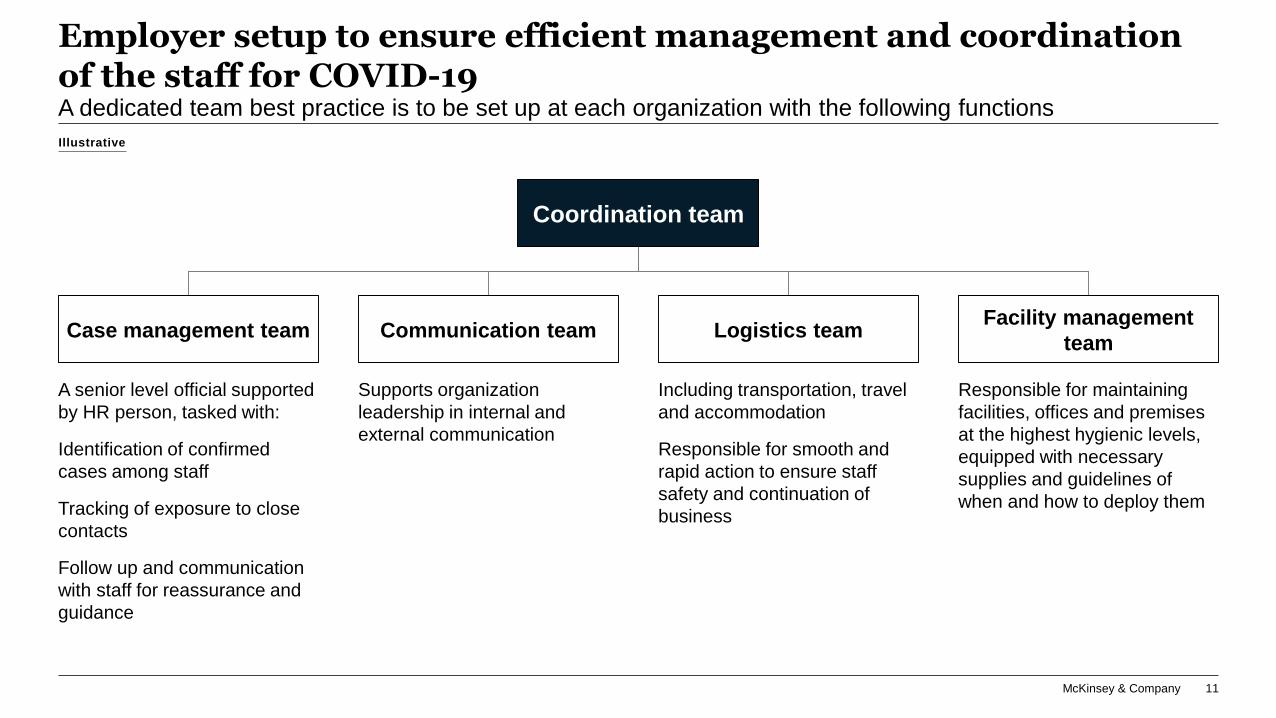

Employer setup to ensure efficient management and coordination of the staff for COVID-19 A dedicated team best practice is to be set up at each organization with the following functions

Illustrative

Coordination team

Case management team Communication team Logistics teamFacility management

team

A senior level official supported

by HR person, tasked with:

Identification of confirmed

cases among staff

Tracking of exposure to close

contacts

Follow up and communication

with staff for reassurance and

guidance

Supports organization

leadership in internal and

external communication

Including transportation, travel

and accommodation

Responsible for smooth and

rapid action to ensure staff

safety and continuation of

business

Responsible for maintaining

facilities, offices and premises

at the highest hygienic levels,

equipped with necessary

supplies and guidelines of

when and how to deploy them

McKinsey & Company 12

Agenda

01 Covid-19 the situation and possible scenarios

How is the private sector reacting to the crisis?04

How are governments reacting to the economic impacts?

03

How might the crisis impact the global economy?02

Q&A with panelist05

McKinsey & Company 13

The imperative of our time

Source: McKinsey analysis, in partnership with Oxford Economics

“Timeboxing” the virus and the economic

shock

Imperative 1: Safeguard our lives

1a. Suppress the virus as fast as possible

1b. Expand treatment and testing capacity

1c. Find “cures”; treatment, drugs, vaccines

Imperative 2: Safeguard our livelihoods

2a. Support people and businesses affected by

lockdowns

2b. Prepare to get back to work safely when the virus

abates

2c. Prepare to scale the recovery away from a ~ -10%

trough

1a

1b

1c

2a

2b

2c

~ -10%

Economic

Shock

McKinsey & Company 14

Potential scenarios for the Economic Impact of the COVID-19 CrisisGDP Impact of COVID-19 Spread, Public Health Response, and Economic Policies

Virus Spread &

Public Health

Response

Effectiveness of the

public health response

in controlling the

spread and human

impact

of COVID-19

Effective Response, but (regional)

Virus Resurgence

Public health response initially succeeds but

measures are not sufficient to prevent viral

resurgence so social distancing continues

(regionally) for several months

Rapid and effective Control of Virus

Spread

Strong public health response succeeds in

controlling spread in each country within 2-3

months

Broad Failure of Public Health

Interventions

Public health response fails

to control the spread of the virus

for an extended period of time

(e.g., until vaccines are available)

Knock-on Effects & Economic Policy Response

Speed and strength of recovery depends on whether policy moves can mitigate self-reinforcing recessionary dynamics (e.g., corporate defaults, credit

crunch)

Ineffective Interventions

Policy responses partially offset economic

damage; banking crisis

is avoided; recovery levels muted

Partially Effective Interventions

Self-reinforcing recession dynamics kick-in;

widespread bankruptcies and credit defaults;

potential banking crisis

Strong policy responses prevent structural

damage; recovery to pre-crisis fundamentals

and momentum

Highly Effective Interventions

Virus contained, slow recovery

A3

Virus contained; strong growth rebound

A4

Virus resurgence; slow long-term growth

Muted World Recovery

A1

Virus resurgence; return to trend growth

Strong World Rebound

A2

Virus resurgence; slow long-term growth

B2

Virus contained, but sector damage;

lower long-term trend growth

B1

Pandemic escalation; prolonged

downturn without economic recovery

B3

Pandemic escalation; slow progression

towards economic recovery

B4

Pandemic escalation; delayed but full

economic recovery

B5

McKinsey & Company 15

Potential scenario A1 Muted World Economy RecoveryReal GDP, Local Currency Indexed

1. Seasonally adjusted by McKinsey;

Source: McKinsey analysis, in partnership with Oxford Economics

105

85

100

90

110

95

Q1Q2Q1 Q3 Q4 Q2Q1 Q3 Q4 Q2 Q3 Q4

Real GDP Growth – COVID-19 CrisisLocal Currency Units Indexed, 2019 Q4=100

World Eurozone

United states China1

2019 2020 2021

-3.9%

-10.6%

-6.2%

-12.2%

2021 Q2

2023 Q1

2022 Q3

2023 Q3

-2.7%

-8.4%

-4.7%

-9.7%

Real GDP, Local Currency Indexed

China

USA

World

Eurozone

Time to Return

to Pre-Crisis

Quarter

Real GDP Drop

2019Q4-2020Q2

% Change

2020 GDP

Growth

% Change

McKinsey & Company 16

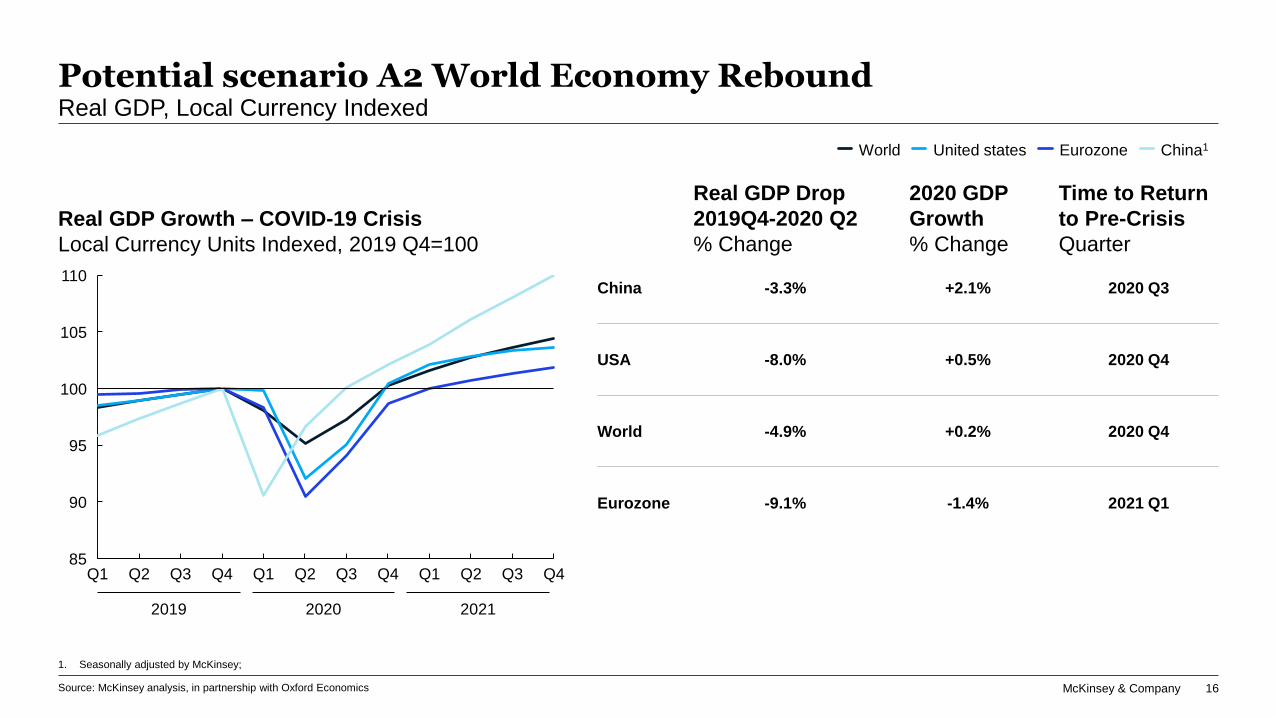

Potential scenario A2 World Economy ReboundReal GDP, Local Currency Indexed

95

85

90

100

105

110

Q4Q2Q2Q1 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q3

World United states Eurozone China1

1. Seasonally adjusted by McKinsey;

Source: McKinsey analysis, in partnership with Oxford Economics

Real GDP Growth – COVID-19 Crisis

Local Currency Units Indexed, 2019 Q4=100

Time to Return

to Pre-Crisis

Quarter

Real GDP Drop

2019Q4-2020 Q2

% Change

2020 GDP

Growth

% Change

-3.3% 2020 Q3China +2.1%

-8.0% 2020 Q4USA +0.5%

-4.9% 2020 Q4World +0.2%

-9.1% 2021 Q1Eurozone -1.4%

2019 2020 2021

McKinsey & Company 17

Agenda

01 Covid-19 the situation and possible scenarios

How is the private sector reacting to the crisis?04

How are governments reacting to the economic impacts?

03

How might the crisis impact the global economy?02

Q&A with panelist05

McKinsey & Company 18

The crisis will have an impact on potentially all parts of the economy

Primary

impact

Secondary

impact

Firms

Financial

System

Government

finances

Agent

Households

Cost increase drivers

Increased provisioning requirements due to

credit downgrades and non performing loans

Higher healthcare and other crisis-related costs

Higher input cost increases due to global supply

chains disruptions

Increased demand for social safety nets

Economic stimulus spending

Higher costs of some goods (due to surge in

demand or reduction in supply)

Income loss drivers

Lower tax/fee collection

Reduced loan and transaction volumes

Lower/no domestic sales due to lockdown

Lower exports due to less global demand

Reduced tax base

Lower revenues from government assets and

SOEs

Reduced production volume due to labor and

supply chain disruptions

Job reduction

Increased defaults and delinquencies

Lower interest rates

Work time / pay reduction

Reduced demand for services of self-employed

McKinsey & Company 19

Three primary objectives targeted by stimulus measuresannounced thus far

Maintain household

economic welfare

Help firms survive the crisis

Maintain financial stability

Not exhaustive

Prudential & financial measures

Employment safeguard

Firms liquidity / cash flow improvement

Value transfer to firms through cost

reduction

Monetary policy actions

Value transfer to firms through revenues

Value transfer to households Maintain household disposable income

Ease household expenses / financial obligations

Relax labor market regulations

Jobs redeployment

Postpone government fees/receivables and

accelerate payment of government’s bills

Manage/ease financial obligations

Gov. purchase of equity stakes in firms

Reduce/eliminate government-related fees

Compensate/reduce salaries’ cost

Stabilize supply chain costs

Relax adequacy requirements

Quantitative easing/liquidity injection

Reduce interest rates

Restore demand for firms’ goods & services

Transfer cash to firms

McKinsey & Company 20

~40 countries are introducing stimulus packagesSize of stimulus packages (including both monetary and fiscal measures)

1. This includes both fiscal and monetary measures (via SAMA) 2. This includes both fiscal and monetary stimulus measures; e.g. up to USD 108 mn of the package will be used to guarantee liquidity for Spanish businesses;

2. 3. GDP number for UK includes: increase in holdings by purchase of gov. and corporate bonds by BOE (amounting to $228B) 4. Current 2019 GDP

# USD bnX% As % of GDP4

Source: Official government sources and press coverage of official announcements; IHS for GDP (current) data

India 13.5 0.5%8

Indonesia 8.1 0.7%9

Italy 28.3 1.6%10

Japan 14.4 0.3%11

Malaysia 4.8 1.3%12

New Zealand 7.8 4.2%13

Philippines 0.5 0.1%14

Saudi Arabia1 32 4.2%15

Singapore 3.9 1.2%16

Australia 100 7.5%2

Abu Dhabi 2.4 0.9%1

Canada 57 3.5%3

China 320 2.3%4

15.4%France5

Germany6

Hong Kong 12.3 3.5%7

18 17

13

15

5 2510

12 9

1

16

2

8

3

14

11

6

20

4

19

23

26

21

UK319

USA20

Sweden N/A21 N/A

Morocco 2.322 2.2%

Nigeria 2.723 0.6%

Netherlands N/A24 N/A

Luxembourg N/A N/A25

Kenya N/A N/A26

Argentina 10 2.7%27

Brazil 30 1.7%28

Chile 11.8 4.5%29

Colombia N/A N/A31

Peru N/A30 N/A

22

24

27

28

29

30

31

32

7

South Korea 1617 1.2%

Spain2 21918 16.8%

Denmark 6 2%32

South Africa N/A N/A33

UAE 34.4 8%35

Scotland N/A34 N/A

35

33

34

32

808

373

23.1%

626 25.1%

2,700 12.6%

Preliminary

Dubai 0.4 0.4%36

36

Uruguay 34.4 4.9%37

Paraguay 0.4 0.4%38

37

38

Current as of March 25, 2020

McKinsey & Company 21

Stimulus size proportional to number of COVID-19 cases, and several countries introducing additional stimulus as situation worsens

Current as of March 25, 2020

Total size of stimulus response1 vs. number of recorded Covid-19 cases

Total size of stimulus response2 (as % of GDP)

1. Total number made public, collected, and analyzed, to date

2. Countries are repeated in cases where stimulus packages or measures have been announced on different dates; size of stimulus response is the aggregate

amount spent at that point in time

3. Number of cases recorded on the day of the stimulus announcement

4. GDP number includes: Increase holdings by purchase of gov. and corporate bonds by BOE (amounting to $228B)

5. USA announcement on March 25 with case count from March 24 (to be updated upon release of information)

1

20

1,000

30

10,000

5

10 1000

100,000

25

10

15

Australia

MoroccoItaly

India

Brazil

Canada

UK

USA5

UK

Chile

Australia

China

France

Germany

South Korea

Indonesia

Saudi

Arabia

UAEAbu Dhabi

Argentina

JapanMalaysia

New Zealand

Nigeria

Spain

UAE

Singapore

Philipines

DenmarkAustralia USA

Saudi Arabia

UK4

Japan

Number of recorded Covid-19 cases3 (#)

Total stimulus size at time of first announcement Total stimulus size at time of second announcementTotal stimulus size at time of third announcement Total stimulus size at time of fourth announcement

Source: WHO Covid-19 Dashboard, IHS Data for GDP, Official government sources and press coverage of official announcements

Preliminary

McKinsey & Company 22

Agenda

01 Covid-19 the situation and possible scenarios

How is the private sector reacting to the crisis?04

How are governments reacting to the economic impacts?

03

How might the crisis impact the global economy?02

Q&A with panelist05

McKinsey & Company 23

Why companies fail at managing crises

Core problem: How can organization move from reacting to yesterday’s

news to proactively shaping tomorrow’s headlines?

Automotive manufacturer: Was

criticized for multiple aspects of

recall activity (e.g., unclear terms

and conditions, inadequate call

center staffing, other challenges)

Challenger disaster: In a now-

infamous phone call, NASA

engineers pressured Thiokol to

change their ‘no-launch’

recommendation (Thiokol shifted

their stance to satisfy their biggest

customer) in-spite of a well-

understood technical failure on O-

rings.

Energy company: Many public

failures to fix process safety issue

before success. Challenge was that

the fix needed new engineering

innovation

Industrial manufacturer: pushed

out fix timelines for failed product

more than 12 times. Top

management optimism bias was

called out multiple times by

regulators, politicians and other

observers

Optimism bias, lack of adequate

‘sensing mechanisms’ (e.g.,

escalation failures), over-reliance

on past patterns, risk rationalization

Many crises have a technical core,

which needs new solutions to be

invented (e.g., BP top hat) or

imported anew into the sector/

geography

Groupthink, political pressures,

high-emotion situations;

Unfamiliarity – pattern recognition-

driven thinking fails; Desire to wait

for more facts slows response

Chaos during disruptions frequently

translates to lack of accountability

and direction, ‘operations addiction’

on the part of top management,

leading to failures of execution

Inadequate Delivery

(Execution failure)

Slow or Bad Decision

Quality

Constrained Solution

DesignInadequate Discovery

McKinsey & Company 24

Observations of what great organizations do

Discover the current situation correctly through

multi-source ‘listening posts’, form an accurate view on how it

might evolve, and derive implications for the organization

Design a trigger-based portfolio of

actions – immediate and strategic - that minimizes false

optimism, maximizes speed, and installs a pragmatic

operating model to detail out plans

and act on them

Decide on strategic actions in a timely way, after ensuring

adequate stress-testing of hypotheses

& alternatives, and ensuring adherence to company

& societal values

Deliver in a disciplined, efficient way, keeping sufficient

flexibility for last minute pivots

McKinsey & Company 25

Observations of what great organizations doThe products in black are the minimum viable products you need

Urgent; do early

Less urgent; do later

Nerve Center Organization

Op. cadence

Response plan

Issues map

2

3

4

5

6

7

8

The simplest

way to conceive

of a Nerve

Center is to

think of the set

of “minimum

viable

products” that

are needed to

get it up and

running

Each minimum

viable product

is a “living part”

that is kept alive

throughout the

crisis

Stakeholder maps

Common Op Picture

KPI dashboard

1 Org chart w/ response lead & team members

Decision authority & roles

Weekly operating cadence

Meeting templates, goals, agenda, attendees

Situation Report

Goals – overall, by workstream (simple language)

Milestones for each workstream (dates, owners)

Portfolio of tactics w/ leading indicators

Risk map (known risks)

Threat map - Issues (major) w/ evolution

List of stakeholder orgs w/ key individuals

Convener for each org w/ supporting team

‘Single view’ of status of overall response (updated at fixed

times, or real time updates)

10-15 KPIs that provide confirmation that issue is getting

resolved, and that milestones are being met

Early warning indicators – gives rationale to pivotListening post

McKinsey & Company 26

Agenda

01 Covid-19 the situation and possible scenarios

How is the private sector reacting to the crisis?04

How are governments reacting to the economic impacts?

03

How might the crisis impact the global economy?02

Q&A with panelist05

Q&A with panelist

McKinsey & Company 28

Backup

McKinsey & Company 29

A: Households – Example measures introduced

Source: Official government sources and press coverage of official announcements

Value

transfer to

households

Employment

safeguard

Categories

Share of all countries

implementing

measure, %1

53

42

13

8

Maintain household

disposable income

Relax labor

market regulations

Ease household

expenses

Jobs

redeployment

Current as of March 24, 2020

Non Exhaustive

Italy: Companies are prohibited from laying off workers for the next two

months without "justified objective reasons"

KSA: Supporting 100,000 job-seekers in the private sector

Colombia: Reconnecting water service free of charge to nearly 1 mn

beneficiaries who had been cut off for not paying

UK: $1.2 bn additional funding, including a $600 mn local authority hardship

fund

Spain: Froze price of LPG, extended deadlines for utility bills

Hong Kong: Extra $300mn in disbursements to the Employees’ Training

Board to increase allowance for trainees

KSA: Extension of residency period of expatriates without any financial

compensation

Spain: Allows employees that accredit care duty of dependents

to reduce and/or adapt their working day

Chile: Income support bonus, equivalent to the family allowance, benefiting

2m people without formal work

Hong Kong: Extra payment of 1 month disability/old age support for those

eligible

South Korea: $1.9bn in consumption support provided in the form of

vouchers redeemable at local retailers

1. N=34 (Abu Dhabi and UAE considered as 1)

Countries implementing leverLever Example measures

McKinsey & Company 30

Firms’

liquidity /

cash flow

improve-

ment

Value

transfer to

firms

through

revenues

37

58

16

26

50

50

16Stabilize supply

chain costs

Postpone gov-related &

accelerate receivables’

collection fees

Transfer cash

to firms

Manage / ease

financial

obligations

Restore demand

for firms’ goods

& services

Support

employment /

salaries

Reduce / eliminate

government-

related fees

Value

transfer to

firms

through

cost

reduction

Source: Official government sources and press coverage of official announcements

B: Firms – Example measures introduced

1. N=34 (Abu Dhabi and UAE considered as 1)

Current as of March 24, 2020

Non Exhaustive

Categories

Share of all countries

implementing

measure, %1 Countries implementing leverLever Example measures

Brazil: Three-month deferral for SMEs corporate taxes, saving them $4.3 bn

China: Banks to extend the terms of business loans & commercial landlords

to reduce rents

Japan: Offer of funds at effectively no interest & without collateral, from gov-

ernment-affiliated lender, for small firms whose sales were hit due to the virus

Nigeria: Injection of $2.7 bn in Nigerian economy to boost local

manufacturing and import substitution

New Zealand: International tourism marketing to diversify the visitor market

Japan: USD 15 bn in special financing for small- and mid-size firms hit by the

virus

UK: Set up of a $2.7bn to provide a one-off $3600 payment to vulnerable

firms (SMEs and rural businesses)

Singapore: Property tax waivers of up to 30% for tourism and entertainment

related industries

KSA: Recovery of work visa fees incurred by employers, however, not utili-

zed due to travel bans (even if they were stamped or extended for 3 months)

Canada: Cover up to 90% of the purchase order amount to ease cash flow to

your suppliers

Japan: $1.8B war-chest to support companies re-locating production back to

Japan (supported by the Development Bank of Japan, among others)

Singapore: The government will co-fund wage increases for Singaporean

employees earning a gross monthly wage of up to $5,000

Brazil: Total of $12 bn devoted to companies to ensure jobs are kept

Includes AD

McKinsey & Company 31

34

43

29

Quantitative

easing / liquidity

injection

Reduce interest

rates

Relax adequacy

requirements

Prudential

& financial

measures

Monetary

policy

actions

Source: Official government sources and press coverage of official announcements

C: Financial market – Example measures introduced

1. N=34 (Abu Dhabi and UAE considered as 1)

Current as of March 24, 2020

Non Exhaustive

Categories

Share of all countries

implementing

measure, %1 Countries implementing leverLever Example measures

Abu Dhabi: Adjustments to capital reserve requirements to release $27bn

Japan: Reduced short-term policy and long-term interest rates on accounts

held by financial institutions at BOJ

Argentina: $5 bn credit line for companies to borrow at a preferential rate of

26% per year — less than the 38% benchmark rate — for 180 days to keep

their businesses afloat

Italy: Increase in size of fund guaranteeing loans to small and medium

businesses

UK: Increase in holdings by purchase of gov. and corporate bonds by BOE

(amounting to $228B)

UAE: The central bank will provide 50bn dirhams through collateralized loans

![Improving GCC Retargetability - CSE · GCC stands for GNU Compiler Collection. GCC is an integrated distribution of compilers for several programming languages[11]. GCC is one of](https://static.documents.pub/doc/80x56/5ed8c3576714ca7f4768857f/improving-gcc-retargetability-cse-gcc-stands-for-gnu-compiler-collection-gcc.jpg)