54

COVID Scenarios for Treasury Risks: Integrating ALM & Liquidity Behavioural Models September, 2020

COVID Scenarios for Treasury Risks:

Integrating ALM & Liquidity Behavioural

Models

September, 2020

2

Introduction & Speakers

Olga Loiseau-Aslanidi, PhD

Head of Business Analytics, APAC

Karen Moss

BSM/ALM Senior Practitioner

Juan Licari, PhD

Managing Director

Risk & Finance Solutions and Economics & Business Analytics

Petr Zemcik, PhD

Senior Director

3

1. Economic and Interest Rate Outlook for the U.K.

2. Analytical Framework: Scenarios and Behavioral Models

3. Balance Sheet Impacts: The Pandemic and Beyond

Agenda

1 Economic and Interest Rate

Outlook for the U.K.

5

Global Real GDP, Trillions 2012$

Global Economy Struggles To Gain Traction

76

78

80

82

84

86

88

90

Jan 19 Apr Jul Oct Jan 20 Apr Jul Oct Jan 21 Apr Jul Oct

Sources: Government sources, Moody’s Analytics

Recessio

n

Re

-op

en

ing

s

Post-Pandemic

Recovery

Pandemic-

Recovery

6

Sources: Good Judgment Project, Moody’s Analytics

When Will There Be an Effective VaccineProbability, timeframe for 25 million inoculations in the U.S. (8/20)

0

10

20

30

40

50

60

70

80

90

100

4/24 5/15 6/5 6/26 7/17 8/7

After Apr 1 2022Oct 1 2021-Mar 31 2022Apr 1 2021-Sep 30 2021Oct 1 2020-Mar 31 2021Before Oct 1 2020

7

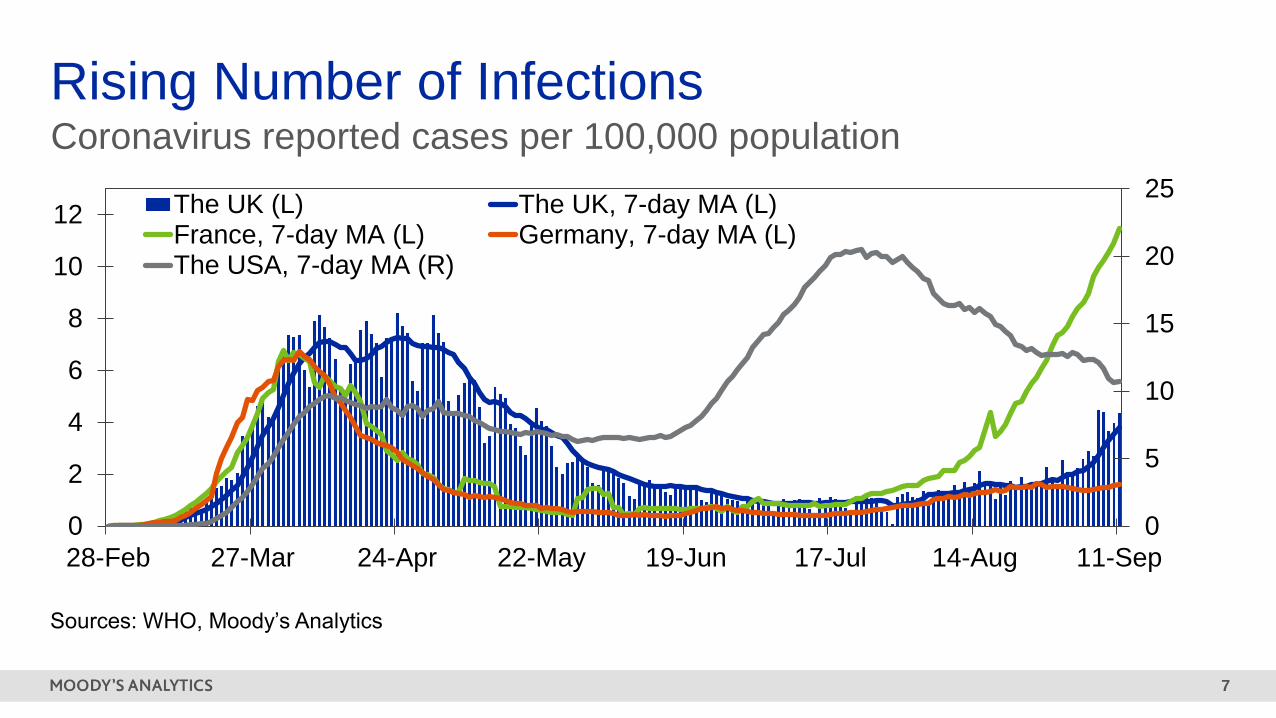

Rising Number of InfectionsCoronavirus reported cases per 100,000 population

0

5

10

15

20

25

0

2

4

6

8

10

12

28-Feb 27-Mar 24-Apr 22-May 19-Jun 17-Jul 14-Aug 11-Sep

The UK (L) The UK, 7-day MA (L)France, 7-day MA (L) Germany, 7-day MA (L)The USA, 7-day MA (R)

Sources: WHO, Moody’s Analytics

8

Brazil

Canada Chile

Denmark

Finland

Germany

Great Britan

Peru

Poland Russia

Sweden

Switzerland

USA

y = 0.0005x + 0.2954R² = 0.6212

0

2

4

6

8

10

12

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000

Sources: WHO, Government sources, Moody’s Analytics

Cha

ng

e in u

ne

mp

loym

en

t ra

te, Ju

ne

/Ju

ly 2

02

0 v

s.

20

19

Q4

More Infections…Weaker EconomyConfirmed infections vs. change in unemployment

Infections per million inhabitants

Malaysia

Hungary

South Korea

JapanNetherlands

Israel

9

Output Declines Dramatically in Q2Deviation from normal level of activity, ppts, by industry

Sources: Moody’s Analytics calculated

-28

-23

-18

-13

-8

-3

2

Mar Apr May Jun Jul Aug Sep-Dec

Arts Accom. Transp. Wholesale Manufact. Real Est. EnergyConstr. Educ. Finance Public admin. Prof. Other service Water SupplyAgric. Admin. Households ICT Mining Health Total

10

Global Economic Body BlowReal GDP growth, % change, baseline scenario

2020Q1 2020Q2 2020Q3 2020Q4 2019 2020

United StatesFebruaryMay

0.3-1.2

0.5-9.4

0.53.8

0.40.2

2.32.3

1.7-5.7

September -1.3 -9.1 6.1 0.7 2.2 -4.3

Euro ZoneFebruaryMay

0.4-3.8

0.4-12.4

0.412.7

0.40.5

1.21.2

1.3-7.0

September -3.7 -12.3 9.8 1.0 1.2 -8.0

UKFebruaryMay

0.3-2.3

0.3-14.2

0.310.9

0.32.2

1.31.4

1-7.4

September -2.2 -20.4 17.3 1.8 1.4 -9.8

ItalyFebruaryMay

0.2-4.8

0.2-16.4

0.218.0

0.21.7

0.20.3

0.4-9.0

September -5.5 -12.8 11.6 1.8 -0.3 -9.5

SpainFebruaryMay

0.4-3.4

0.4-15.7

0.518.4

0.50.4

2.02.0

1.8-6.7

September -5.2 -18.5 13.7 2.6 2.0 -12.0

IrelandFebruaryMaySeptember

2.1-2

1.2-15.9

0.511.8

-0.31.2

5.65.5

4.0-6.5

1.17 -19.87 11.56 -0.11 5.54 -7.26

Global OutputFebruaryMaySeptember

0.4-3.1

0.9-6.7

0.85.2

0.71.6

2.52.4

2.4-4.5

-2.93 -7.58 6.10 1.94 2.38 -4.63

11

Unemployment IncreasesShift of baseline scenarios

0.0

5.0

10.0

15.0

20.0

25.0

Germany UnitedKingdom

France Greece Spain Italy Netherlands Portugal RussianFederation

Poland UnitedStates

Unemployment in 2019Q4Max of 2020-22 Unemployment (Feb)Max of 2020-22 Unemployment (Sep)

CountryUnemployment

in 2019Q4

Max of 2020-22

Unemployment (Feb)

Max of 2020-22

Unemployment (Sep)

Value Date Value Date

Germany 5.00 5.36 2022Q4 6.25 2020Q4

United Kingdom 3.80 4.64 2022Q4 8.38 2021Q1

France 8.10 8.51 2020Q1 10.59 2021Q1

Greece 16.53 16.34 2020Q1 19.83 2020Q4

Spain 13.81 14.06 2020Q2 19.61 2020Q3

Italy 9.57 10.52 2022Q4 12.79 2022Q2

Netherlands 3.40 4.48 2021Q3 6.66 2021Q3

Portugal 6.62 6.29 2020Q1 9.45 2020Q4

Russian Federation 4.58 5.78 2021Q1 6.45 2020Q3

Poland 2.85 3.91 2022Q4 6.34 2021Q3

United States 3.53 4.37 2022Q2 13.03 2020Q2

Source: Moody’s Analytics

12

Policy Response

Country Fiscal policy Monetary policy

United

Kingdom

Coronavirus Job Retention Scheme & Self-employment Income Support Scheme

State-backed loans £330bn

£7bn to support the self-employed, businesses and vulnerable people; £5bn

emergency response fund to help the National Health Service (NHS) and other

public services; £18 billion of “fiscal loosening” to support the economy this year

Deferring VAT and Income Tax payments; Statutory Sick Pay relief package for

small and medium sized businesses (SMEs);

12-month business rates holiday for all retail, hospitality, leisure and nursery

businesses in England; Small business grant funding of £10,000 for all business in

receipt of small business rate relief or rural rate relief; The Coronavirus Business

Interruption Loan Scheme offering loans of up to £5 million for SMEs through the

British Business Bank

June - Increase capital spending to 3% of GDP, speed up £5 billion of repairs on

roads, schools, hospitals.

June – additional £50 borrowing plans (2.5% of GDP)

BoE:

Monetary policy rate at 0.1%

Reduced capital (banks shall not pay dividends in 2020) –

release lending up to £190 billion

Covid Corporate Financing Facility will provide a quick and

cost-effective way to raise working capital for those large firms

who need it

Quantitative Easing (March 2020) – the target holding of

government bonds is £645 billion

QE (June) – expand by £100 billion

Baseline Assumptions

» The catalysts are the COVID-19 crisis, turmoil in equity markets, and the plunge in global oil prices

» In June and May, the decline is driven almost entirely by the government’s lockdown measures in a bid to contain the

virus, with the tourism and entertainment sectors taking the hardest hit.

» The lockdown is lifted by summer and the supply side of the economy starts to recover

» Real estate sector will produce 20% less output in the second quarter of 2020 compared to the period prior to the crisis.

» The U.K. economy should rebound in 2021 following the resolution of the coronavirus crisis and signing of the trade deal

13

Regional Shocks to Unemployment Rate (NUTS3)UK regions: level 2019 vs. 2020 (baseline forecast)

2019Q4 Historical value <= 3%

3% to 5%

>= 5%

2020Q4 Forecasted value (Baseline Scenario)

4% to 7%

7% to 9%

9% to 11%

14

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

15Q1 15Q3 16Q1 16Q3 17Q1 17Q3 18Q1 18Q3 19Q1 19Q3 20Q1 20Q3 21Q1 21Q3

Inte

rest

rate

s a

nd

CP

I

BoE policy rate10Y Bond yield3 Months LIBORCPI (y/y %)

Key interest rates and Inflation

UK Interest Rates Remain Low

Sources: BoE, ONS, Moody’s Analytics

15

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20

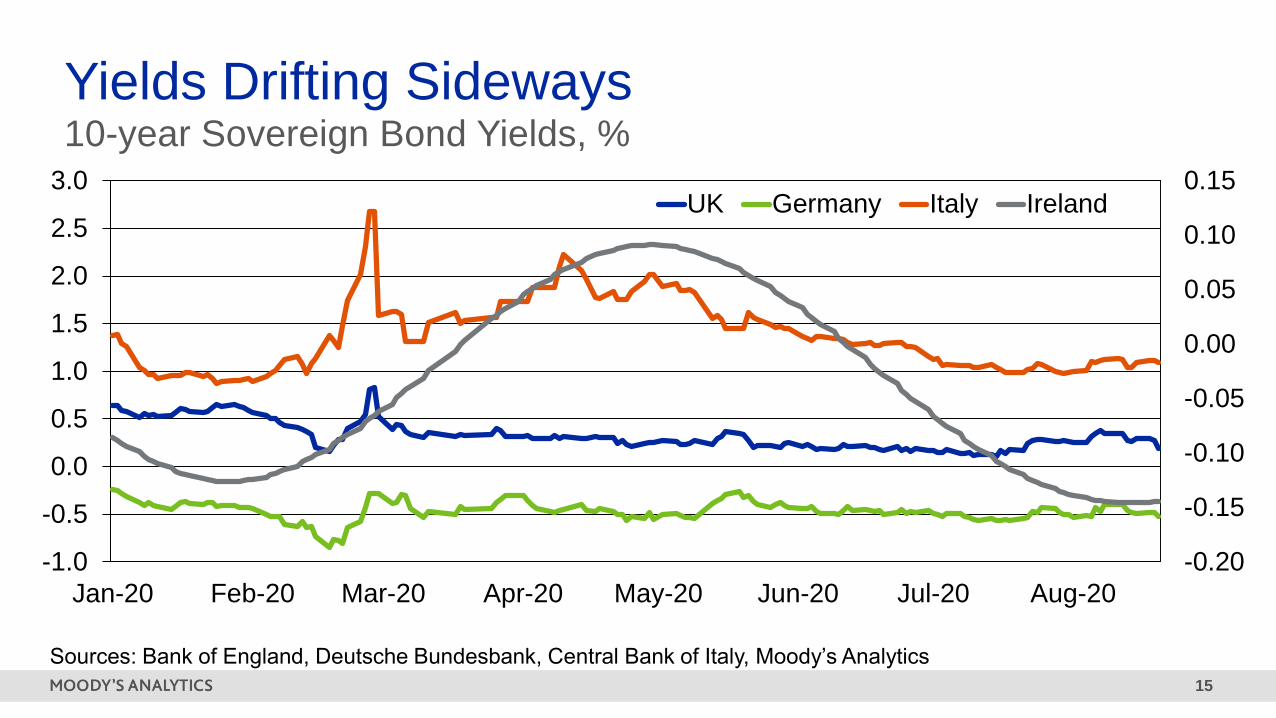

UK Germany Italy Ireland

Sources: Bank of England, Deutsche Bundesbank, Central Bank of Italy, Moody’s Analytics

Yields Drifting Sideways10-year Sovereign Bond Yields, %

16

Spread: Libor – Policy Rate

Sources: Central banks, Moody’s Analytics

-0.5

0.0

0.5

1.0

1.5

2.0

2007Q1 2012Q1 2017Q1 2022Q1

Spread 3m Libor -policy rate

Spread 6m Libor -policy rate

Spread 12m Libor -policy rate

Spreads, % Level, %

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2007Q1 2012Q1 2017Q1 2022Q1

3M Libor 6M Libor 12M Libor

Key drivers of the spread of 12M Libor from the policy rate are the

following factors:

• Spread of the US 12M Libor from the Fed policy rate

• Spread of the UK 3M Libor from the BoE policy rate

• As the spread is increasing in the USA Libor, the spread in the UK

Libor will be increasing too

17

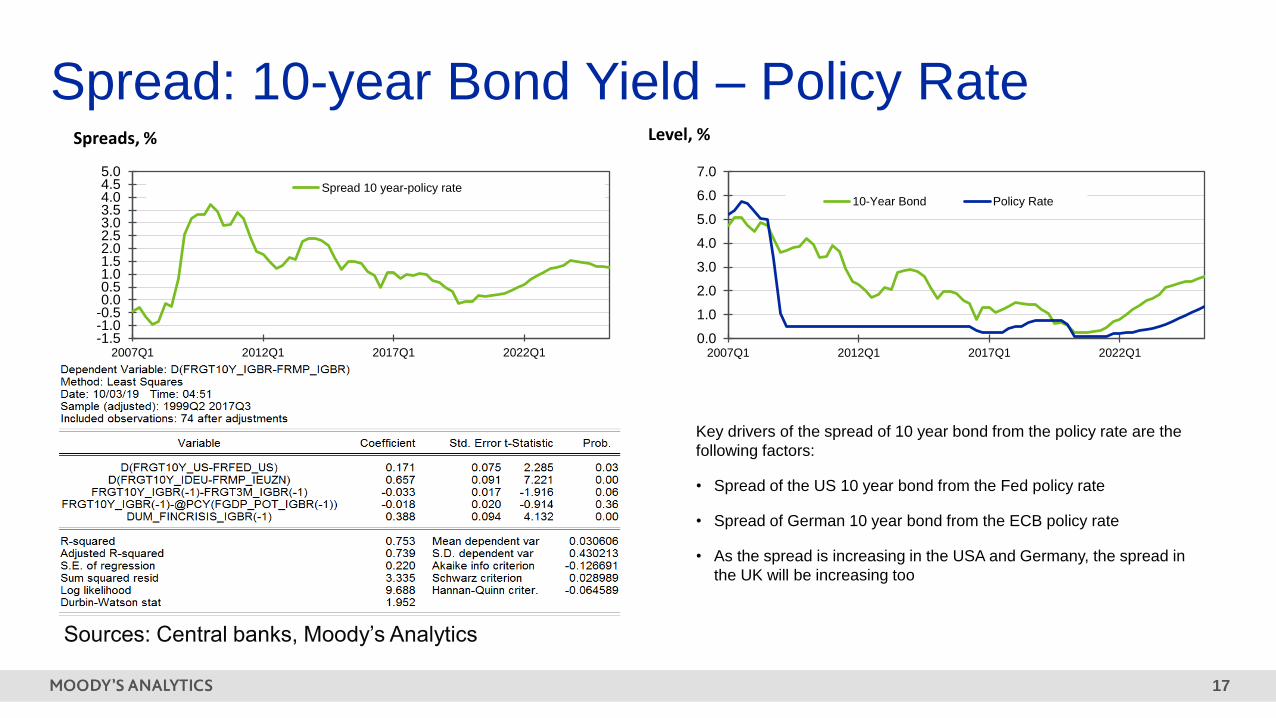

Spread: 10-year Bond Yield – Policy Rate

Sources: Central banks, Moody’s Analytics

-1.5-1.0-0.50.00.51.01.52.02.53.03.54.04.55.0

2007Q1 2012Q1 2017Q1 2022Q1

Spread 10 year-policy rate

Spreads, % Level, %

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2007Q1 2012Q1 2017Q1 2022Q1

10-Year Bond Policy Rate

Key drivers of the spread of 10 year bond from the policy rate are the

following factors:

• Spread of the US 10 year bond from the Fed policy rate

• Spread of German 10 year bond from the ECB policy rate

• As the spread is increasing in the USA and Germany, the spread in

the UK will be increasing too

18

Risks: Epidemiological U.K. Assumptions

COVID-19: Upside

S1 Scenario

» 450K confirmed infections

» 4,5mil total cases

» 63K total deaths

» Infections abate by Feb 2021

COVID-19

Baseline Forecast

» 500K confirmed infections

» 5mil total cases

» 75K total deaths

» Infections abate by May 21

COVID-19: Downside

S3 Scenario

» 660K confirmed infections

» 5.7mil total cases

» 138K total deaths

» Infections abate by Oct 2021

19

Severity, avg. deviations from baseline, %

BL AugustS4 August S3 August BL Feb

S4 Feb S3 Feb

20

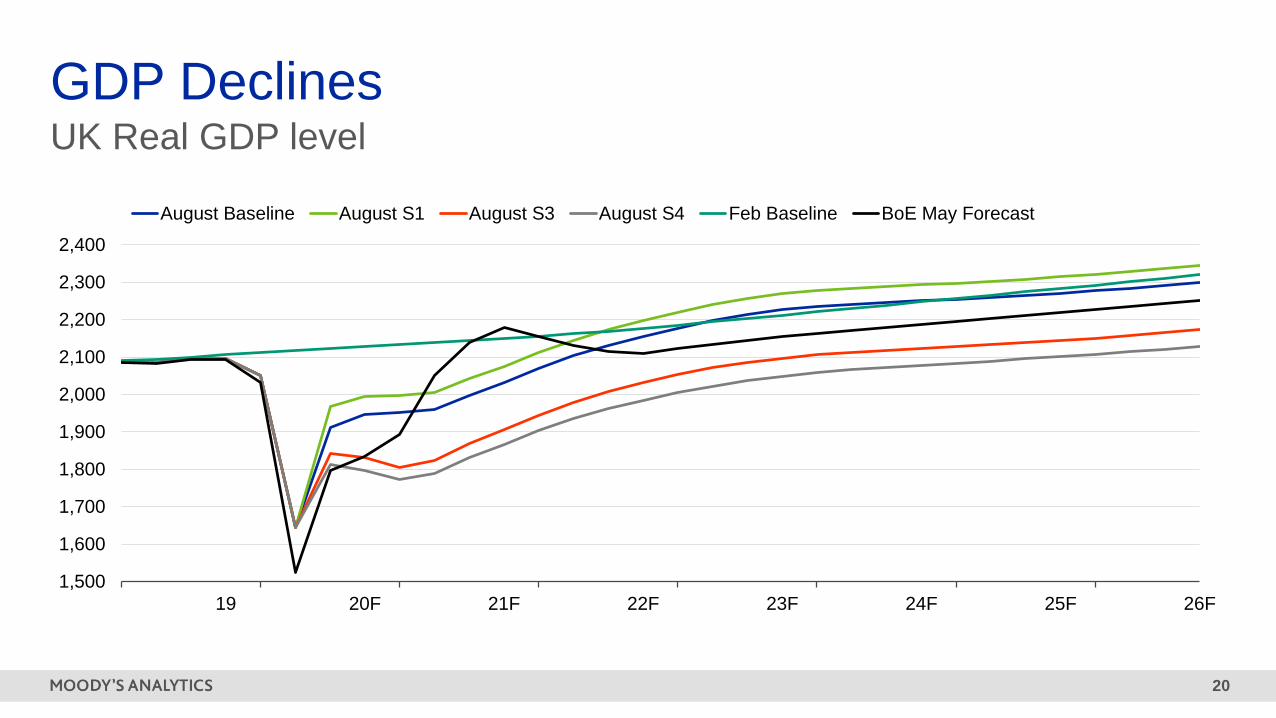

UK Real GDP level

GDP Declines

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

19 20F 21F 22F 23F 24F 25F 26F

August Baseline August S1 August S3 August S4 Feb Baseline BoE May Forecast

21

Unemployment rate

Unemployment Rises

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

18 19 20F 21F 22F 23F 24F 25F 26F 27F 28F 29F 30F 31F 32F 33F 34F

August Baseline August S1 August S3 August S4 Feb Baseline

22

House Prices DecreaseHouse price growth, % change yr ago

-25

-20

-15

-10

-5

0

5

10

15

19 20F 21F 22F 23F 24F 25F 26F

August Baseline August S1 August S3 August S4 Feb Baseline

23

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

19 20F 21F 22F 23F 24F 25F 26F 27F 28F 29F 30F 31F 32F 33F 34F 35F

August Baseline August S1 August S3 August S4 Feb Baseline

3-months Libor level

3-months LIBOR

24

Swap Rates: UK Pound Sterling Interest Rate Swap, Month average,

(% p.a., NSA)

Impact on the Yield Curve

-0.5

0.0

0.5

1.0

1.5

2.0

1Y 5Y 10Y 25Y

Sep 2020

Baseline Stress

-0.5

0.0

0.5

1.0

1.5

2.0

1Y 5Y 10Y 25Y

Sep 2023

Baseline Stress

-1

0

1

2

3

4

5

2010 2013 2016 2019 2022 2025

1Y 5Y 10YS3: Donwside

Sources: Refinitiv; Moody's Analytics Calculated and Forecasted

-1

0

1

2

3

4

5

2010 2013 2016 2019 2022 2025

1Y 5Y 10YBaseline

2Analytical Framework:

Scenarios and Behavioral

Models

26

Analytics: Behavioral Models and ScenariosSatisfy regulation and make results more credible for IRRBB

∆ Net Interest

Income

∆ Economic

Value of Equity

Am

en

ab

le

Fixed rate

instrument

Floating rate

instruments

No

t a

me

na

ble Non-maturing

instruments

Prepayment,

drawdown and

redemption

Le

ss

am

en

ab

le Automatic interest

rate options

Embedded

Automatic Interest

Rate Option

Behavioral

Models

Add-on

for

options

Inte

rest

rate

sen

sit

ive

Projection

of cash

flows

Shock

scenarios

27

Challenges of Behaviour Models and ScenariosFor interest rate risk in the banking book, liquidity and credit metrics

Data Availability

Granularity, frequency, consistency,

completeness, and quality

Limitations can put constraints on the

type of modeling techniques

Macroeconomic scenarios historical

data and forecast.

Framework Integrity

Single view of risk across the bank

Enforce consistency of results by

establishing and common modeling

framework

Model governance, re-calibration

updates, monitoring, use test

Model Design

Building robust models using

relevant quantitative methods

Finding appropriate model

specification using variable

search algorithms

Detailed documentation and

knowledge transfer

Model Implementation

Implementation into key interest

rate risk and liquidity metric

calculations

Implementation into credit risk

metric calculation

Ensuring continuity through detailed

user manuals

28

Approach to Link Scenarios with ModelsCritical for forward-looking planning

• Baseline scenario forecast

• Alternative stress scenarios

• Alternative upside scenarios

• Event-driven scenarios

• Regulatory stress testing scenarios

Macroeconomic Indicators

• Interest rate term structure

• Customer behavior

• Liquidity risk

• Credit risk and provisioning for regulatory capital, IFRS9

• Early warning indicators

Risk Models

• Liquidity risk gaps, survival period

• Interest risk gaps

• Net interest income

• Economic value of equity

• Balance sheet, P&L, RWA projections

• Expected credit loss

• Internal and regulatory capital requirement

Key Measures

2.1 Scenario Generation for

Behavioural Factors

30

Achieving an Integrated Balance Sheet ViewCross-discipline scenario alignment

IRRBB

Standardized shock

scenarios

Bank’s risk profile

ICAAP

Historical worst and IR

stress scenarios

ICAAP

Stress scenarios based

on Bank’s Pillar 1 &

Pillar II risks

IFRS 9

Typically 3-5 scenarios

for baseline, upside,

downside

Not tail event, relatively

probable

Not bank-specific but

representing global risk

ILAAP

Typically 3 stress

scenarios based on the

Bank’s individual

business model, risk

profile,

and market wide stress

Risk factors external to

the Bank (COVID-19

paths, trade-wars,

climate change, etc.)

Scenarios might include

baseline, mild and

severe outcomes

Additional bespoke

stress scenarios

relevant for the Bank

Typically baseline and

stress scenarios

Short and protracted

stress scenarios,

severe but plausible

Standalone Regulatory

Stress Tests

Specific scenarios provided

by regulators on a regular

basis/ad hoc such as EBA,

PRA, CCAR, MAS, etc.

Narratives and scenario

path but for specific

variables only

Stress testing across

different risk departments

31

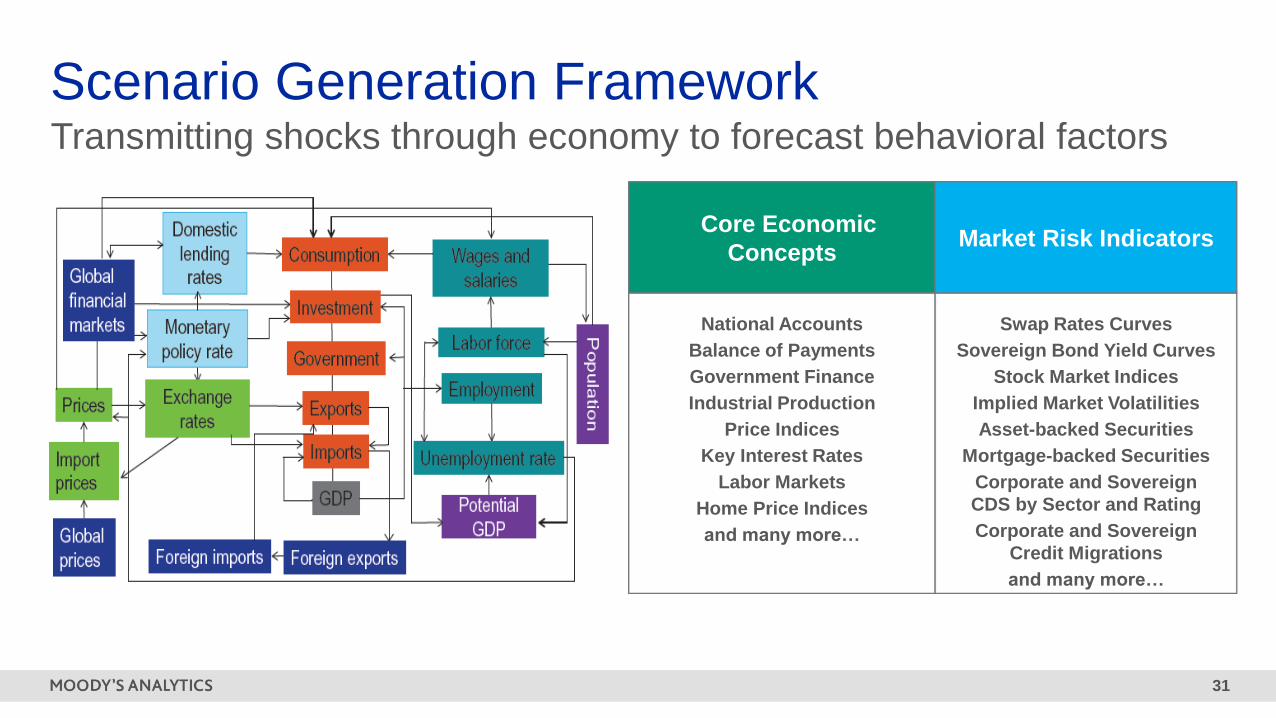

National Accounts

Balance of Payments

Government Finance

Industrial Production

Price Indices

Key Interest Rates

Labor Markets

Home Price Indices

and many more…

Core Economic

Concepts

Swap Rates Curves

Sovereign Bond Yield Curves

Stock Market Indices

Implied Market Volatilities

Asset-backed Securities

Mortgage-backed Securities

Corporate and Sovereign

CDS by Sector and Rating

Corporate and Sovereign

Credit Migrations

and many more…

Market Risk Indicators

Scenario Generation FrameworkTransmitting shocks through economy to forecast behavioral factors

32

-50

-40

-30

-20

-10

0

10

20

30

40

2006Q1 2012Q1 2018Q1 2024Q1 2030Q1

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2006Q1 2012Q1 2018Q1 2024Q1 2030Q1

-30

-25

-20

-15

-10

-5

0

5

10

15

20

2006Q1 2012Q1 2018Q1 2024Q1 2030Q1

2

4

6

8

10

12

14

2006Q1 2012Q1 2018Q1 2024Q1 2030Q1

Unemployment Rate

Monetary Policy RateStock Price, % year ago

House Price Index, % year ago

-1

0

1

2

3

4

5

6

2006Q1 2012Q1 2018Q1 2024Q1 2030Q1

10-year Government Bond Yield

Forecast of Selected Behavioural FactorsSeverity shift for baseline and two alternative scenarios, examples

-1

0

1

2

3

4

5

6

7

2006Q1 2012Q1 2018Q1 2024Q1 2030Q1

SONIA

33

Modelling Term Structure of Interest RatesModified Nelson-Siegel methodology

Satellite

Model 1(x,y)→ z1

Satellite

Model 2(x,y)→ z2

Satellite

Model 3(x,y)→ z3

Satellite

Model S(x,y)→ zS

Global

Macroeconomic

Model(x,ε)→y

34

Forecast of Selected Key Behavioural FactorsGovernment bonds & swaps scenario examples

-1

0

1

2

3

4

5

2011 2013 2015 2017 2019 2021 2023 2025

Baseline

-1

0

1

2

3

4

5

2011 2013 2015 2017 2019 2021 2023 2025

S4: Severe Downside

-1

0

1

2

3

4

5

2011 2013 2015 2017 2019 2021 2023 2025

S4: Severe Downside

0

1

2

3

4

5

2011 2013 2015 2017 2019 2021 2023 2025

Baseline

Interest rate swaps, 1-year to 50-year maturities

Government bonds, 1-month to 50-year maturities

2.2 Forward-looking

Behavioural Models

36

Modelling Expected BehavioursLinking scenarios with net cash-flows from assets and liabilities

DATA INPUT

Economic Scenarios:

Deterministic

Simulations

Bank’s Data:

Customer Characteristics

Product Characteristics

MODELS

Call deposits withdrawal

Term deposits early withdrawal

Loan commitments drawdown

OUTPUT

Account-level, forward-looking, scenario-

conditional projections of behavioural risk

metrics

Portfolio-level, forward-looking, scenario-

conditional projections of cash flows

Portfolio-

level

Segment-

level

Account-

level

Loan prepayment

Probability of default, delinquencies

Loss given default, exposure at default

37

Example Factors for Different Behavioural ModelsFor interest rate risk in banking book, liquidity and credit risks

Loans subject to prepayment risk

• Loan size, LTV

• Borrower characteristics

• Contractual and current interest rates

• Geographical location

• Demography

• Taxes

• Changes in family composition

• Original and remaining maturity

• Seasoning

• Macroeconomic variables (e.g. stock price index,

unemployment rates, inflation and HPI)

Loan commitments drawdowns

• Borrower characteristics

• Geographical location, including competitive environment and

local premium conventions

• Customer relationship with bank

• Remaining maturity of the commitment

• Seasoning and remaining term

• Macroeconomic variables

Call deposits

• Responsiveness of product rates to changes in market interest

rates

• Current level of interest rates

• Spread between a bank’s offer rate and market rate

• Competition from other banks

• Bank’s reputation, geographical location and demographic

characteristics of customer base

• Insurance coverage

• Macroeconomic variables

Term deposits subject to early withdrawal risk

• Deposit size, depositor characteristics

• Funding channel

• Contractual interest rates

• Seasonal factors, geographical location and competitive

environment

• Remaining maturity and other historical factors

• Insurance coverage

• Bank’s reputation

• Macroeconomic variables

38

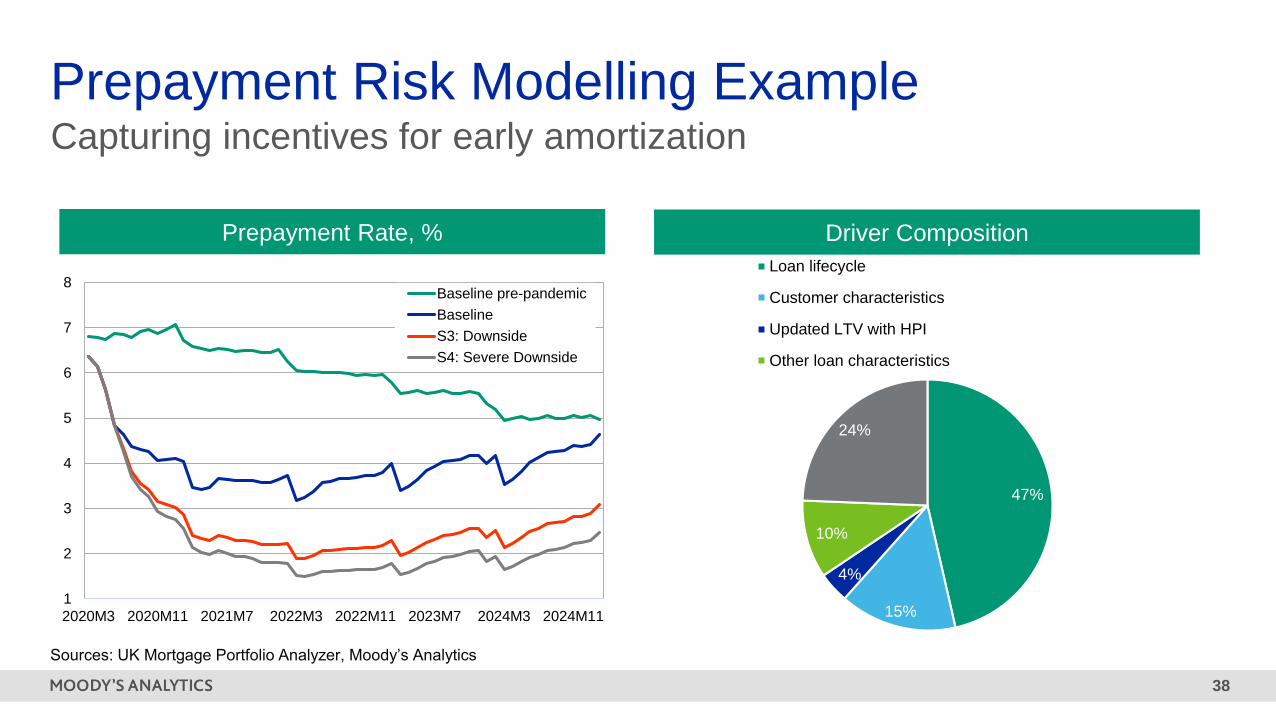

Prepayment Risk Modelling ExampleCapturing incentives for early amortization

Prepayment Rate, %

Sources: UK Mortgage Portfolio Analyzer, Moody’s Analytics

47%

15%

4%

10%

24%

Loan lifecycle

Customer characteristics

Updated LTV with HPI

Other loan characteristics

Driver Composition

1

2

3

4

5

6

7

8

2020M3 2020M11 2021M7 2022M3 2022M11 2023M7 2024M3 2024M11

Baseline pre-pandemic

Baseline

S3: Downside

S4: Severe Downside

39

Deliquency and Credit Loss Modelling ExampleCapturing borrowers’ ability to repay and corresponding losses

Expected Credit Loss, %Probability of Default, %

Sources: UK Mortgage Portfolio Analyzer, Moody’s Analytics

0

1

2

3

4

5

6

7

8

9

2020M3 2020M11 2021M7 2022M3 2022M11 2023M7 2024M3 2024M11

Baseline pre-pandemic

Baseline

S3: Downside

S4: Severe Downside

0

10

20

30

40

50

60

70

Current 30 daysdelinquent

60 daysdelinquent

Defaulted

Baseline pre-pandemic

Baseline

S3: Downside

S4: Severe Downside

40

Propensity to Withdraw Modelling ExampleCapturing motives for willingness to withdraw and place funds

Percentage change year ago

-50

-40

-30

-20

-10

0

10

20

30

2019M01 2020M01 2021M01 2022M01 2023M01

History

Baseline pre-pandemic

Baseline

S3: Downside

S4: Severe downside10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

2017M01 2021M01 2025M01 2029M01

Mill

ion m

oneta

ry u

nits

History

Baseline pre-pandemic

BL: Baseline

S3: Downside

S4: Severe downside

*Assuming complete pass-through

Level of deposits

41

Non-maturing Deposits Modeling ExampleProduct-specific approach for IRRBB

(3) Duration

Analysis

Non-Maturing

Deposits

Stable Non-stable

Non-coreCore

Non-pass through Pass through

WholesaleRetail

transactional

Retail

non-transactional

(2) Sensitivity

Analysis

(1) Volatility

Analysis

(1) Examine the distribution of Stable Deposit

Rate across observation windows

(2) Analyze the relationship between market

rates, deposit rates and deposit volumes to

determine Core Deposit Rate

(3) Determine the optimal Behavioral Duration

Deposit

Rates

Deposit

Volumes

Market

Rates

3 Balance Sheet Impacts:

The Pandemic and Beyond

43

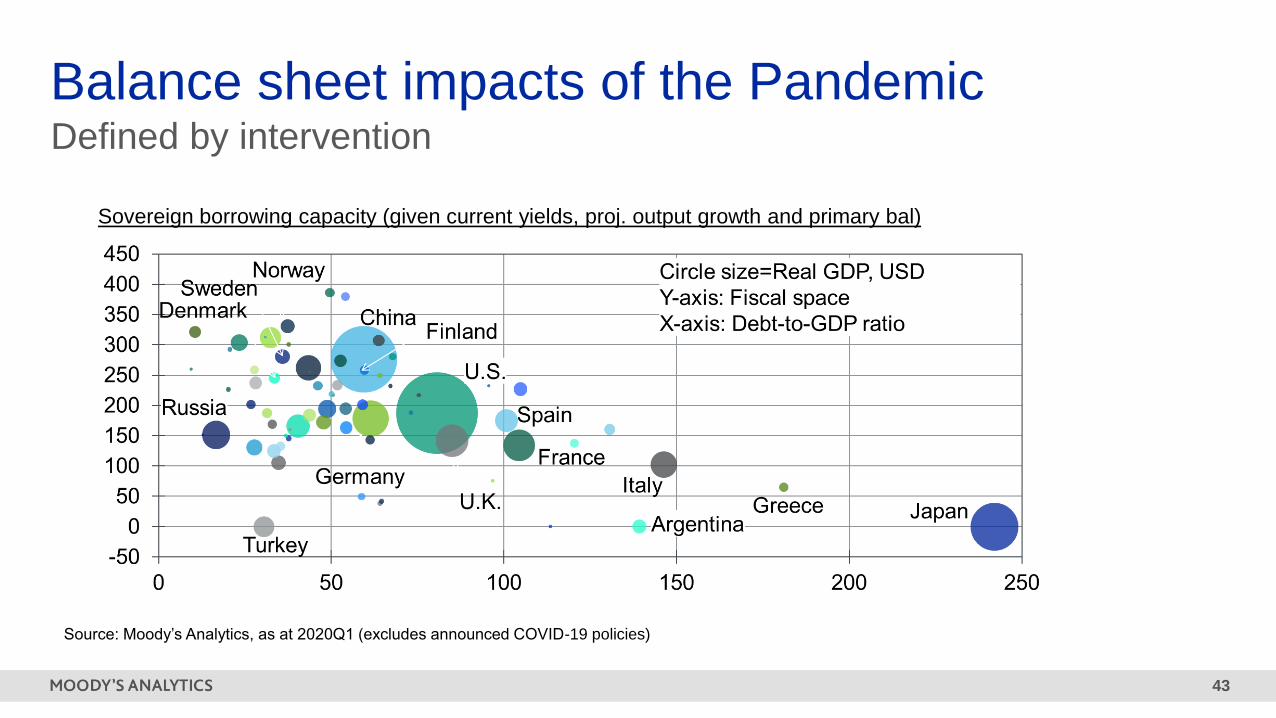

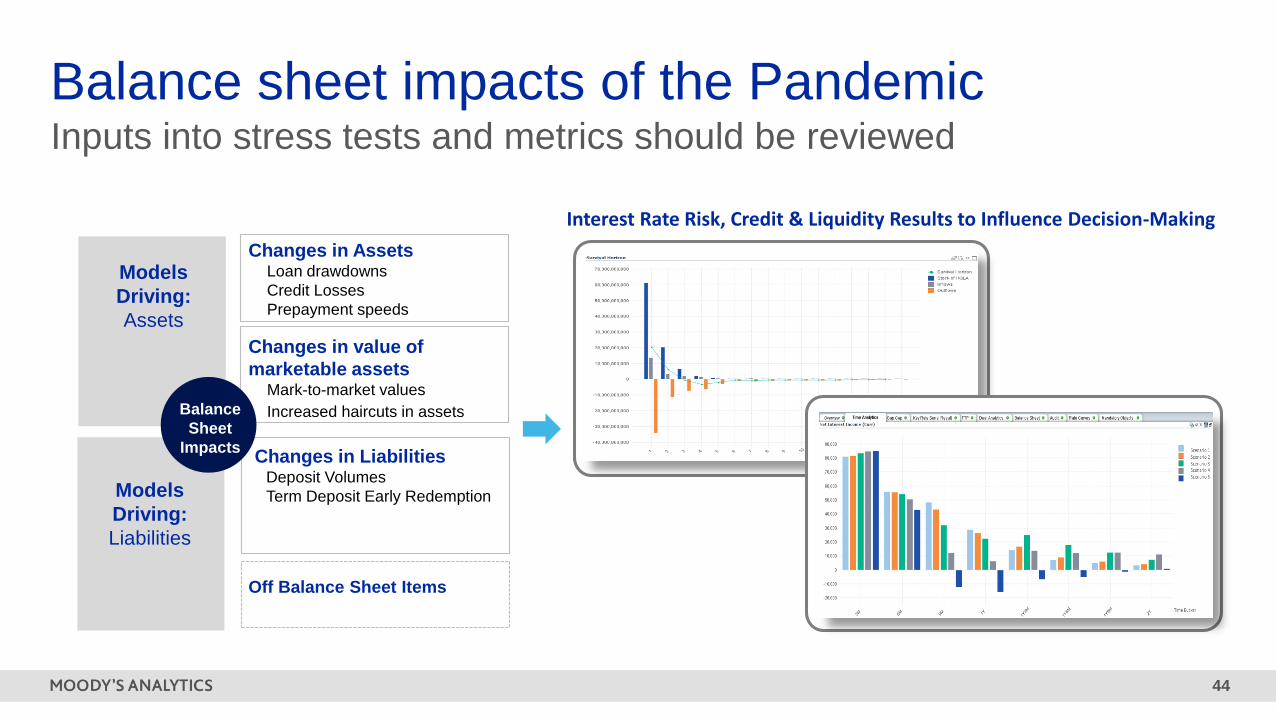

Balance sheet impacts of the PandemicDefined by intervention

Sovereign borrowing capacity (given current yields, proj. output growth and primary bal)

Source: Moody’s Analytics, as at 2020Q1 (excludes announced COVID-19 policies)

44

Changes in AssetsLoan drawdowns

Credit Losses

Prepayment speeds

Changes in value of

marketable assetsMark-to-market values

Increased haircuts in assets

Changes in LiabilitiesDeposit Volumes

Term Deposit Early Redemption

Off Balance Sheet Items

Models

Driving:

Assets

Models

Driving:

Liabilities

Balance

Sheet

Impacts

Balance sheet impacts of the PandemicInputs into stress tests and metrics should be reviewed

Interest Rate Risk, Credit & Liquidity Results to Influence Decision-Making

45

-£155bn

-£135bn

-£115bn

-£95bn

-£75bn

-£55bn

-£35bn

-£15bn

Q1 2020Q2 2020

Q3 2020Q4 2020

20212022

20232024

-£155bn

-£135bn

-£115bn

-£95bn

-£75bn

-£55bn

-£35bn

-£15bn

Q1 2020Q2 2020

Q3 2020Q4 2020

20212022

20232024

Equilibrium returns

Shock

Stress period

begins Deposit OutflowDeposit recovery as

rate environment

normalises

£100

£50

Equilibrium returns

ShockStress period

begins

Asset Prepayment/Credit lossAsset recovery as

rate environment

normalises

£100

Modelling Impact on balance sheet

Balance sheet impacts of the PandemicWhat will happen next?

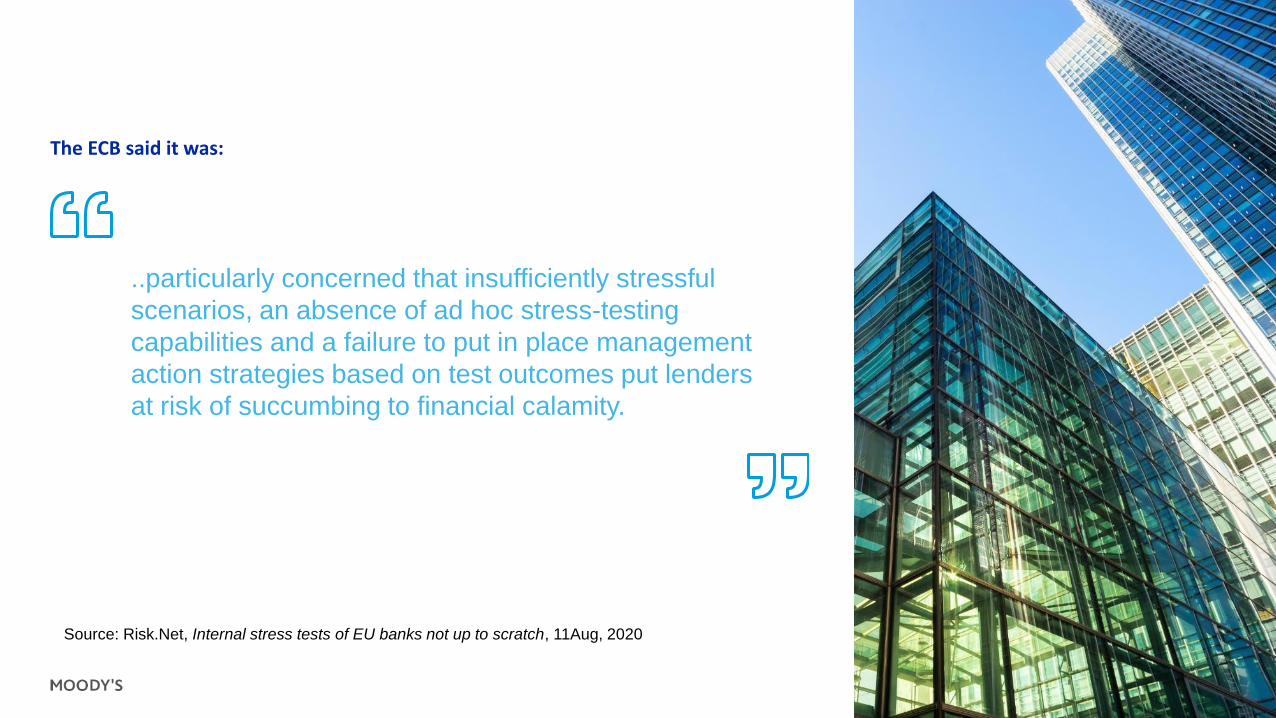

..particularly concerned that insufficiently stressful

scenarios, an absence of ad hoc stress-testing

capabilities and a failure to put in place management

action strategies based on test outcomes put lenders

at risk of succumbing to financial calamity.

The ECB said it was:

Source: Risk.Net, Internal stress tests of EU banks not up to scratch, 11Aug, 2020

47

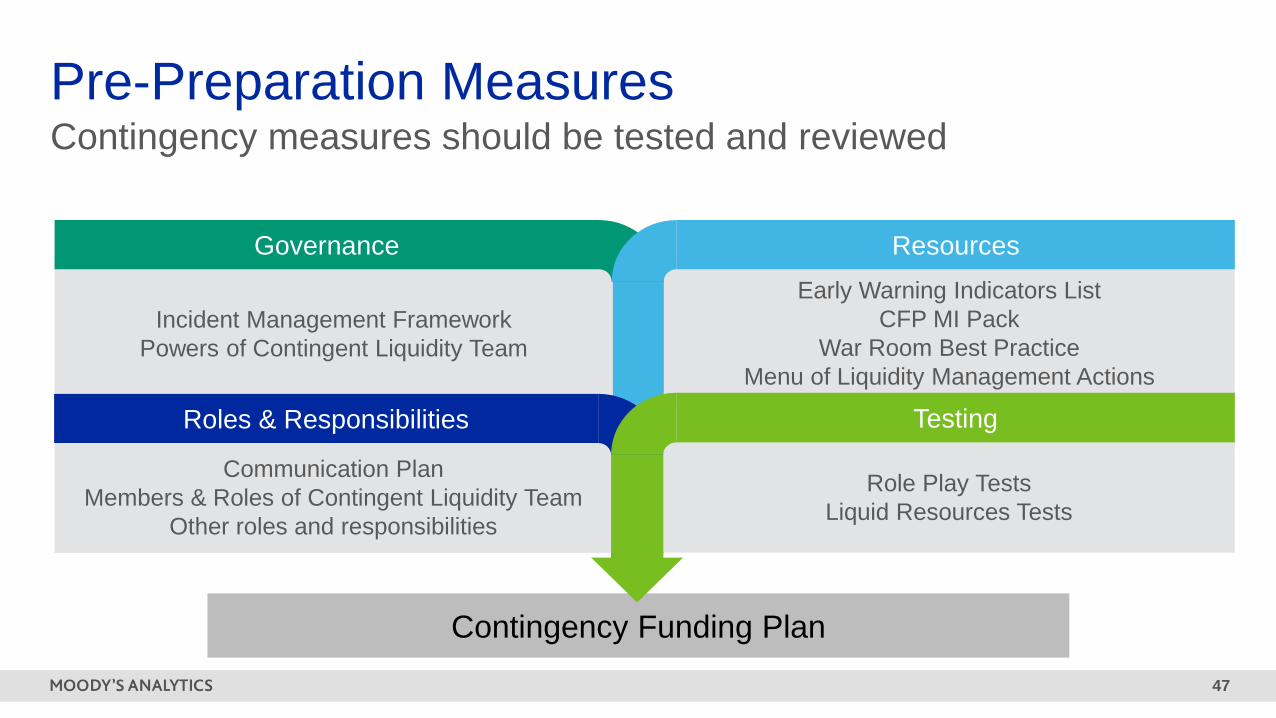

Contingency Funding Plan

Communication Plan

Members & Roles of Contingent Liquidity Team

Other roles and responsibilities

Incident Management Framework

Powers of Contingent Liquidity Team

Early Warning Indicators List

CFP MI Pack

War Room Best Practice

Menu of Liquidity Management Actions

Governance Resources

Roles & Responsibilities

Role Play Tests

Liquid Resources Tests

Testing

Contingency measures should be tested and reviewed

Pre-Preparation Measures

48

Other Headwinds

2017 2019 2021

2018 2020 2022

Jun: SOFR

selected as

ARR

How near is the end of LIBOR?

US Regulatory Timeline

UK Regulatory Timeline

Apr: SONIA

selected as

ARR

Apr: FRBNY

began

publishing

SOFR

Mar: FRBNY

began

publishing

SOFR index

Oct: Clearing

Houses to

move to

SOFR

discounting

LIBOR panel no longer

required to submit quotes

SOFR term

reference

rate?

Jul: BOE

begins

publishing

SONIA Index

Sep: Non-

LIBOR linked

loans

available for

customers

Mar: End

date to book

LIBOR loans

expiring post

2021

Apr: SONIA

methodology

reform

Credit

sensitive

benchmark?

49

Source: Time to switch rates, Jun 2019, Oliver Wyman

The market is moving to align.. but slowly…

Other Headwinds

50

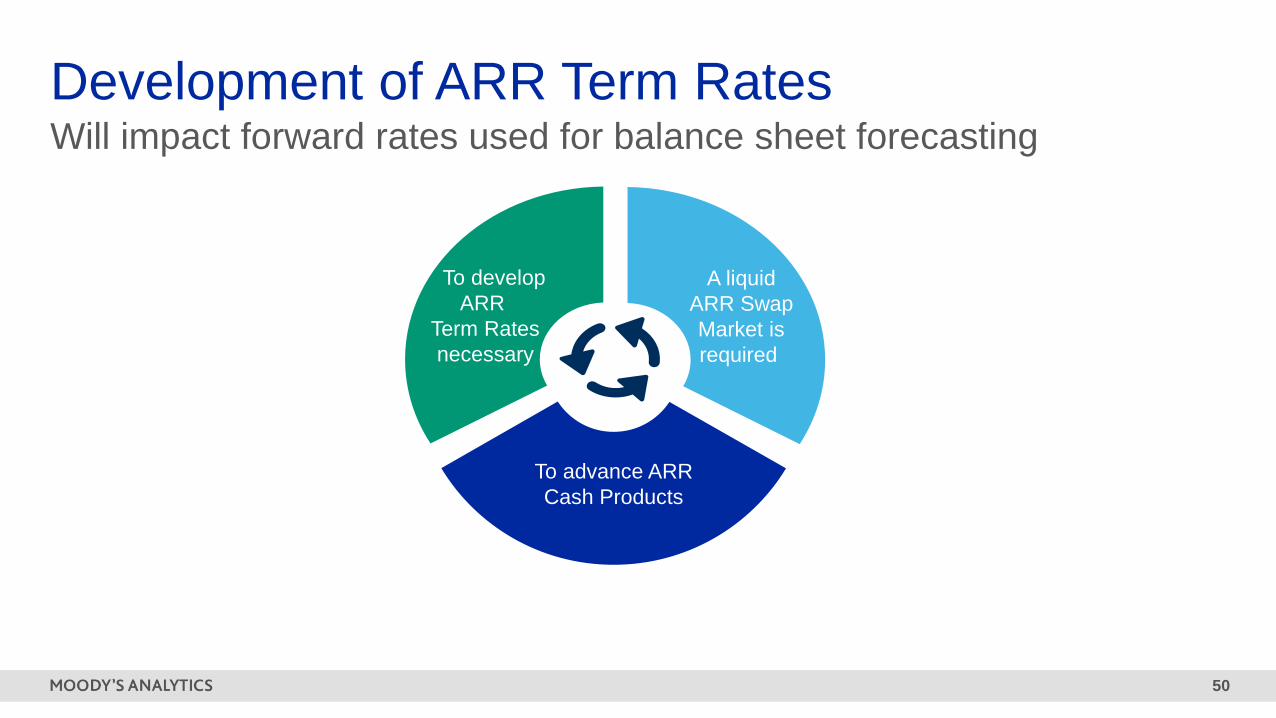

Will impact forward rates used for balance sheet forecasting

Development of ARR Term Rates

To advance ARR

Cash Products

To develop

ARR

Term Rates

necessary

A liquid

ARR Swap

Market is

required

51

ARRs must sit alongside other rates in stress tests and forecasts

Building IBOR curves

» IBOR Futures at short end

» IRS swaps or Fed Funds Basis Swaps at long end

Building ARR curves

» ARR Futures at short end

» OIS at long end- Liquidity is low! FF or LIBOR Basis swaps as an

alternative?

Source: FINCAD

Development of ARR Term Rates

52

Key Takeaways1.Despite the current recovery phase, the U.K. economy is forecast to contract 9.7%

in 2020.

2.QE and schemes to support the customer franchise helped to both dissipate any

wholesale market stress and contain a surge in impairments, but have impacted

banks’ balance sheets.

3.With the end of intervention (including the end of the payment holiday scheme in

October), banks should expect a tsunami effect on their provisions.

4.Modelling this in a balance sheet context, as well as taking account of other

headwinds, such as IBOR transition, are the next challenges for those dealing with

Treasury risks.

Q&AEmail us at [email protected]

moodysanalytics.com

West Chester, EBA-HQ+1.610.235.5299

121 North Walnut Street, Suite 500

West Chester PA 19380

USA

New York, Corporate-HQ+1.212.553.1653

7 World Trade Center, 14th Floor

250 Greenwich Street

New York, NY 10007

USA

London+44.20.7772.5454

One Canada Square

Canary Wharf

London E14 5FA

United Kingdom

Toronto+1.416.681.2133

200 Wellington Street West, 15th Floor

Toronto ON M5V 3C7

Canada

Prague+420.23.474.7500

Pernerova 691/42

186 00 Prague 8 - Karlin,

Czech Republic

Sydney+61.2.9270.8111

Level 10

1 O'Connell Street

Sydney, NSW, 2000

Australia

Singapore+65.6511.4400

6 Shenton Way

#14-08 OUE Downtown 2

Singapore 068809

Shanghai+86.21.6101.0172

Unit 2306, Citigroup Tower

33 Huayuanshiqiao Road

Pudong New Area, 200120

China

Contact Us: Content Solutions - Economics & Business Analytics Offices

54

© 2020 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All

rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND/OR ITS CREDIT RATINGS AFFILIATES ARE MOODY’S CURRENT

OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND

MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED BY MOODY’S (COLLECTIVELY, “PUBLICATIONS”) MAY INCLUDE SUCH

CURRENT OPINIONS. MOODY’S INVESTORS SERVICE DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS

CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR

IMPAIRMENT. SEE MOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL

FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’S INVESTORS SERVICE CREDIT RATINGS. CREDIT RATINGS DO NOT ADDRESS ANY

OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS, NON-

CREDIT ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF

CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK

AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. AND/OR ITS AFFILIATES. MOODY’S CREDIT RATINGS,

ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS

TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND

PUBLICATIONS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS

CREDIT RATINGS, ASSESSMENTS AND OTHER OPINIONS AND PUBLISHES ITS PUBLICATIONS WITH THE EXPECTATION AND

UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS

UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS, AND PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS

AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER

OPINIONS OR PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER

PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH

INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED,

REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR

MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A

BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM

BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or

mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all

necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable

including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or

validate information received in the rating process or in preparing its Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any

person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information

contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives,

licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective

profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any

direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful

misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the

control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the

information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY

PARTICULAR PURPOSE OF ANY CREDIT RATING, ASSESSMENT, OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY

FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt

securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc.

have, prior to assignment of any credit rating, agreed to pay to Moody’s Investors Service, Inc. for credit ratings opinions and services rendered by it fees

ranging from $1,000 to approximately $2,700,000. MCO and Moody’s investors Service also maintain policies and procedures to address the independence

of Moody’s Investors Service credit ratings and credit rating processes. Information regarding certain affiliations that may exist between directors of MCO

and rated entities, and between entities who hold credit ratings from Moody’s Investors Service and have also publicly reported to the SEC an ownership

interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and

Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S

affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL

383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act

2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a

representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to

“retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt

obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is

wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating

agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ

are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not

qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency and

their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and

commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any credit rating, agreed to pay to MJKK or

MSFJ (as applicable) for credit ratings opinions and services rendered by it fees ranging from JPY125,000 to approximately JPY250,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.