75

BY RACHELLE AGATHA, CPA, MBA Receivables Slides by Rachelle Agatha, CPA, with excerpts from Warren, Reeve, Duchac

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | zion-check |

| View: | 237 times |

| Download: | 0 times |

BY R A C H E L L E A G AT H A , C PA , M B A

Receivables

Slides by Rachelle Agatha, CPA, with excerpts from Warren, Reeve, Duchac

2

1. Describe the common classifications of receivables.

2. Describe the nature of and the accounting for uncollectible receivables.

3. Describe the direct write-off method of accounting for uncollectible receivables.

Objectives:

3

4. Describe the allowance method of accounting for uncollectible receivables.

5. Compare the direct write-off and allowance methods of accounting for uncollectible accounts.

Objective

4

6. Describe the nature, characteristics, and accounting for notes receivables.

7. Describe the reporting of receivables on the balance sheet.

Objectives:

5

Describe the common

classifications of receivables.

Objective 1

Objective 1

6

The term receivables includes all money

claims against other entities, including

people, business firms, and other

organizations.

Classification of Receivables

7

Accounts receivable are

normally expected to be collected

within a relatively short period, such as 30 or 60 days.

Accounts Receivable

8

Notes receivable are amounts that

customers owe for which a formal,

written instrument of credit has been

issued.

Notes Receivable

9

Other receivables expected to be collected

within one year are classified as current assets.

If collection is expected beyond one year, these

receivables are classified as noncurrent assets and

reported under the caption Investments.

Other Receivables

10

Describe the nature of and

the accounting for uncollectible

receivables.

Objective 2

Objective 2

11

Companies often sell their receivables to other

companies. This transaction is called factoring the

receivables, and the buyer of the receivables is called a

factor.

12

There are two methods of accounting for receivables

that appear to be uncollectible: the direct write off method and the

allowance method.

Uncollectible Receivables

13

The direct write off method records bad debt expense only when an account is judged to be worthless.

The allowance method records bad debt expense by estimating uncollectible accounts at the end of the accounting period.

14

Describe the direct write-off

method of accounting for uncollectible receivables.

Objective 3

Objective 3

15

May 10 Bad Debt Expense 4 200 00 Accounts Receivable—D. L. Ross 4 200 00

On May 10, a $4,200 accounts receivable from D. L. Ross has been determined to be uncollectible.

Direct Write-Off Method

16

The amount written off is later collected on November 21.

Nov. 21 Accounts Receivable—D. L. Ross 4 200 00 Bad Debt Expense

4 200 00

21 Cash 4 200 00

Accounts Receivable—D. L. Ross 4 200 00

17

Journalize the following transactions using the direct write-off method of accounting for uncollectible receivables.

July9 Received $1,200 from Jay Burke and wrote off the remainder owed of $3,900 as uncollectible.

Oct. 11 Reinstated the account of Jay Burke and received $3,900 cash in full payment.

18

July 9 Cash 1,200Bad Debt Expense 3,900

Accounts Receivable—Jay Burke 5,100

Oct.11 Accounts Receivable—Jay Burke3,900Bad Debt Expense 3,900

11 Cash 3,900Accounts Receivable—Jay Burke 3,900

19

Describe the allowance method of accounting for

uncollectible receivables.

Objective 4

Objective 4

20

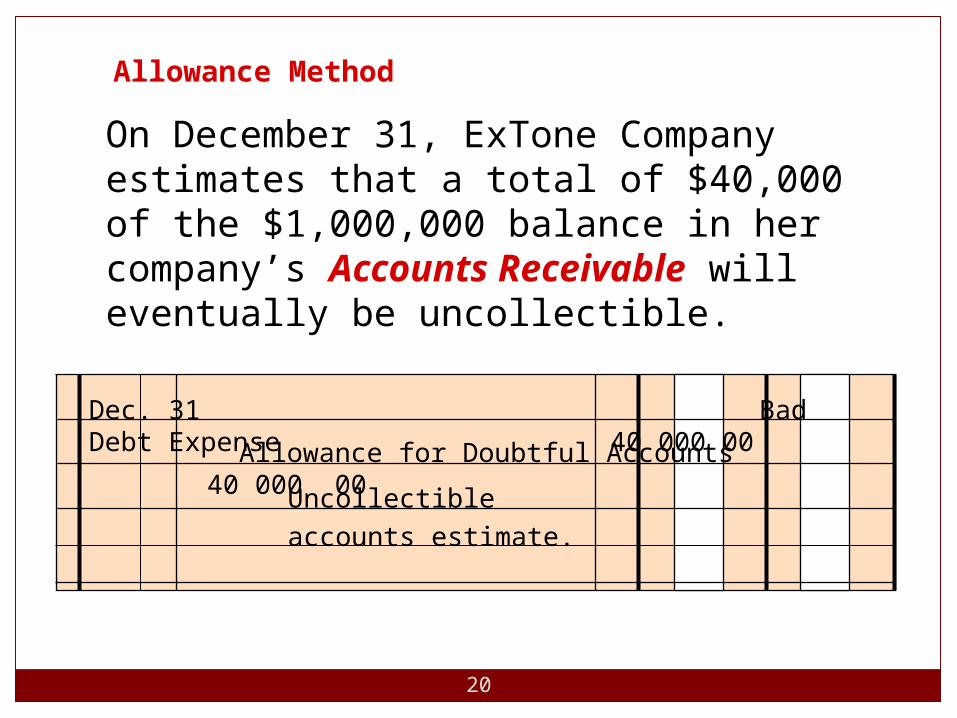

On December 31, ExTone Company estimates that a total of $40,000 of the $1,000,000 balance in her company’s Accounts Receivable will eventually be uncollectible.

Dec. 31 Bad Debt Expense 40 000 00 Allowance for Doubtful Accounts

40 000 00Uncollectible accounts estimate.

Allowance Method

21

The net amount that is expected to be collected, $960,000

($1,000,000 – $40,000), is called the net realizable value (NRV).

The adjusting entry reduces receivables to the NRV and

matches uncollectible expenses with revenues.

Net Realizable Value

22

Jan. 21 Allowance for Doubtful Accounts 6 000 00 Accounts Receivable—John Parker 6 000 00

To write off the uncollectible account.

On January 21, John Parker’s account totaling $6,000 is written off because it is uncollectible.

23

24

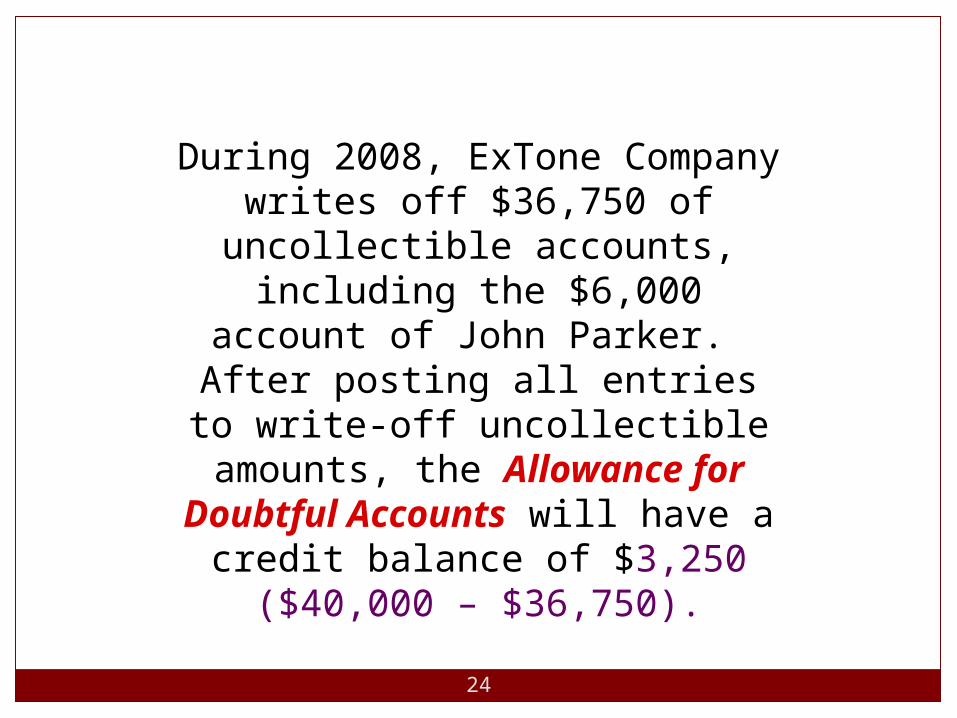

During 2008, ExTone Company writes off $36,750 of

uncollectible accounts, including the $6,000 account of John Parker. After posting all

entries to write-off uncollectible amounts, the Allowance for

Doubtful Accounts will have a credit balance of $3,250

($40,000 – $36,750).

25

ALLOWANCE FOR DOUBTFUL ACCOUNTS

Jan. 1, 2008 Bal.

40,000Jan. 21

6,000Feb. 2

3,900{

Total accounts written off $36,750

Dec. 31 Unadjusted bal

3,250

“ “ “ “

26

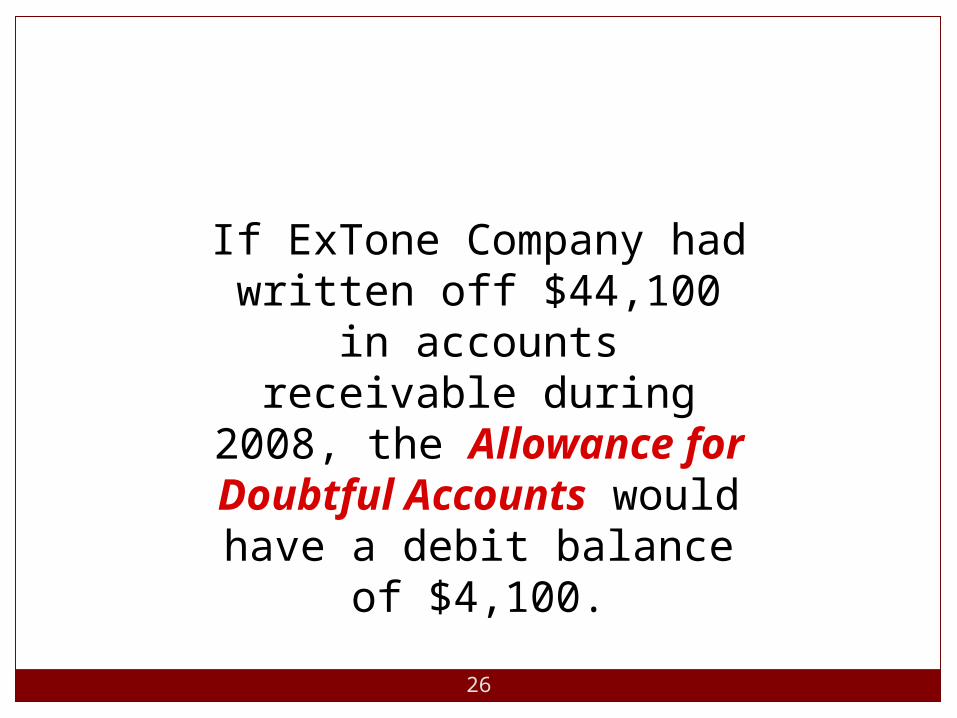

If ExTone Company had written off $44,100 in accounts receivable

during 2008, the Allowance for

Doubtful Accounts would have a debit balance of $4,100.

27

ALLOWANCE FOR DOUBTFUL ACCOUNTS Jan. 1, 2008 Bal.

40,000Jan. 21

6,000Feb. 2

3,900{

Total accounts written off $44,100Dec. 31 Unadjusted bal

4,100

“ “ “ “

28

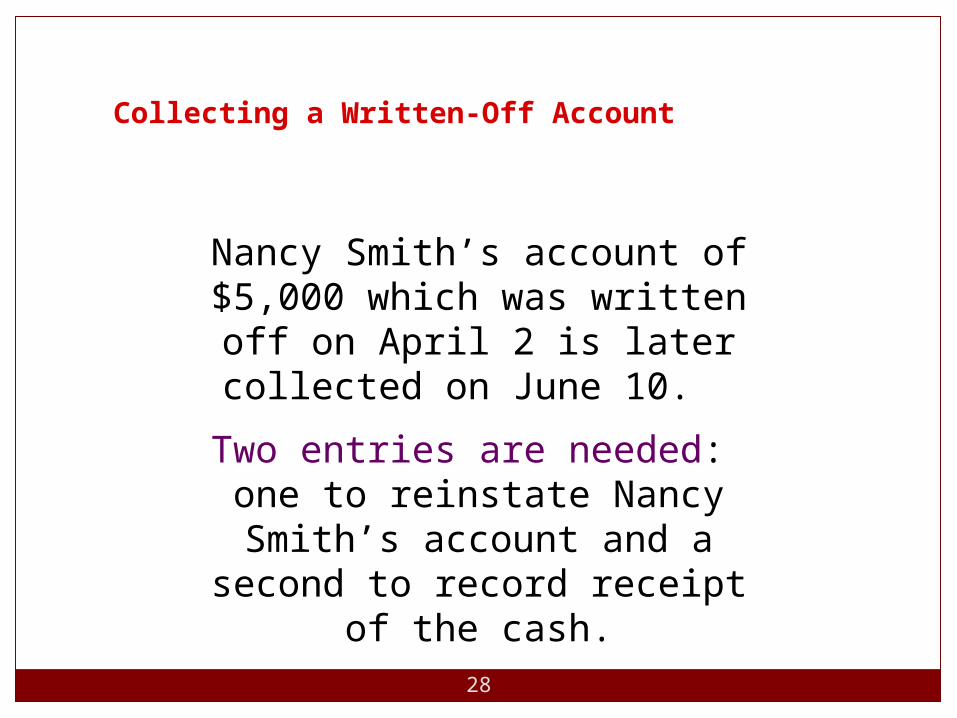

Nancy Smith’s account of $5,000 which was written off on April 2 is later collected

on June 10.

Two entries are needed: one to reinstate Nancy Smith’s

account and a second to record receipt of the cash.

Collecting a Written-Off Account

29

June 10 Accounts Receivable—Nancy Smith 5 000 00

To reinstate the account written off on Jan. 21.

Allowance for Doubtful Accounts 5 000 00

Entry 1: Reinstate the account.

30

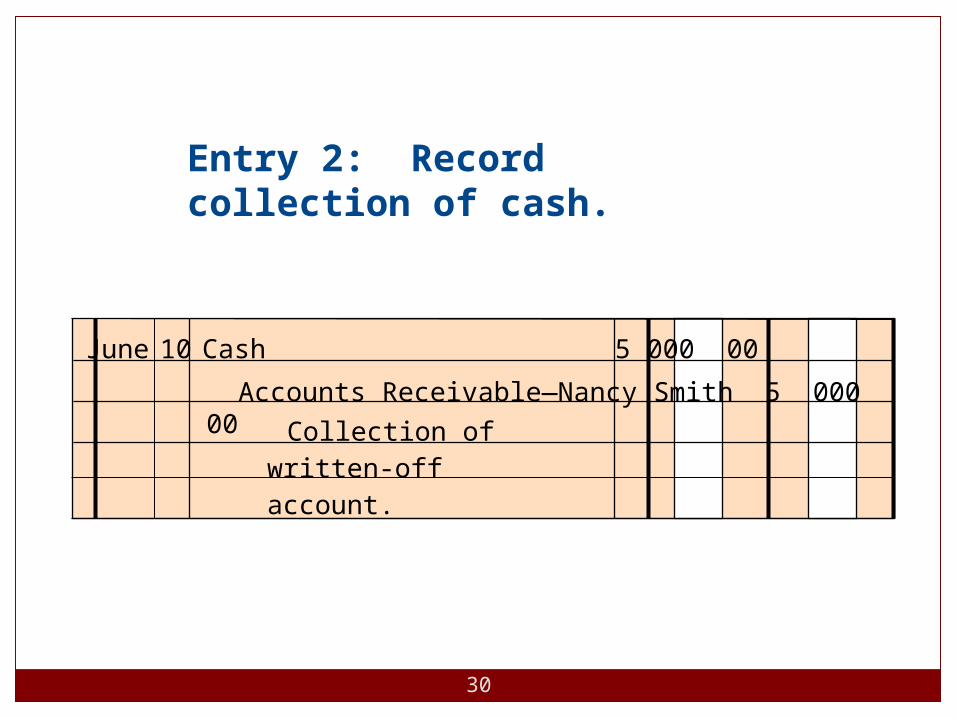

June 10 Cash 5 000 00

Collection of written-off account.

Accounts Receivable—Nancy Smith 5 000 00

Entry 2: Record collection of cash.

31

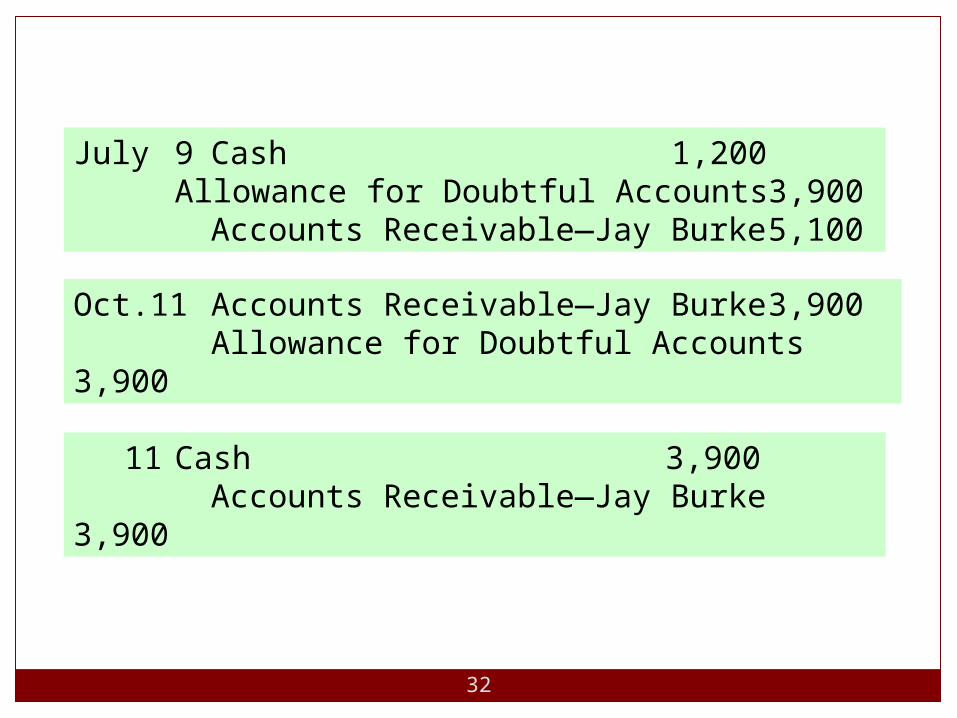

Journalize the following transactions using the allowance method of accounting for uncollectible receivables.

July9 Received $1,200 from Jay Burke and wrote off the remainder owed of $3,900 as uncollectible.

Oct. 11 Reinstated the account of Jay Burke and received $3,900 cash in full payment.

32

July 9 Cash 1,200Allowance for Doubtful Accounts3,900

Accounts Receivable—Jay Burke 5,100

Oct.11 Accounts Receivable—Jay Burke3,900Allowance for Doubtful Accounts 3,900

11 Cash 3,900Accounts Receivable—Jay Burke 3,900

33

1. Estimate based on a percentage of sales. (Income statement method)

2. Estimate based on analysis of receivables. (Balance Sheet Method)

The allowance method uses two ways to estimate the amount debited to Bad Debt Expense.

Estimating Uncollectibles

34

Estimate Based on a Percentage of Sales

If credit sales for the period are $3,000,000 and it is estimated

that 1½ % will be uncollectible, the Bad Debt Expense is

debited for $45,000 ($3,000,000 x .015). This approach

disregards the balance in the allowance account before the

adjustment.

35

After this adjusting entry is posted, Allowance for Doubtful Accounts will have a balance of $48,250.

Dec. 31 Bad Debt Expense 45 000 00

Allowance for Doubtful Accounts 45 000 00Uncollectible accounts ($3,000,000 x 0.015 = $45,000).

36

ALLOWANCE FOR DOUBTFUL ACCOUNTS Jan. 1, 2008 Bal. 40,000

Jan. 1 6,000

Feb. 23,900

{Total accounts written off $36,750

Dec. 31 Unadjusted bal

3,250Dec. 31 Adj. entry

45,000Dec. 31 Adjusted bal.

48,250

“ “

BAD DEBT EXPENSEDec. 31 Adj entry45,000Dec. 31 Adjusted bal.45,000

Income statement method calculates the adjustment

37

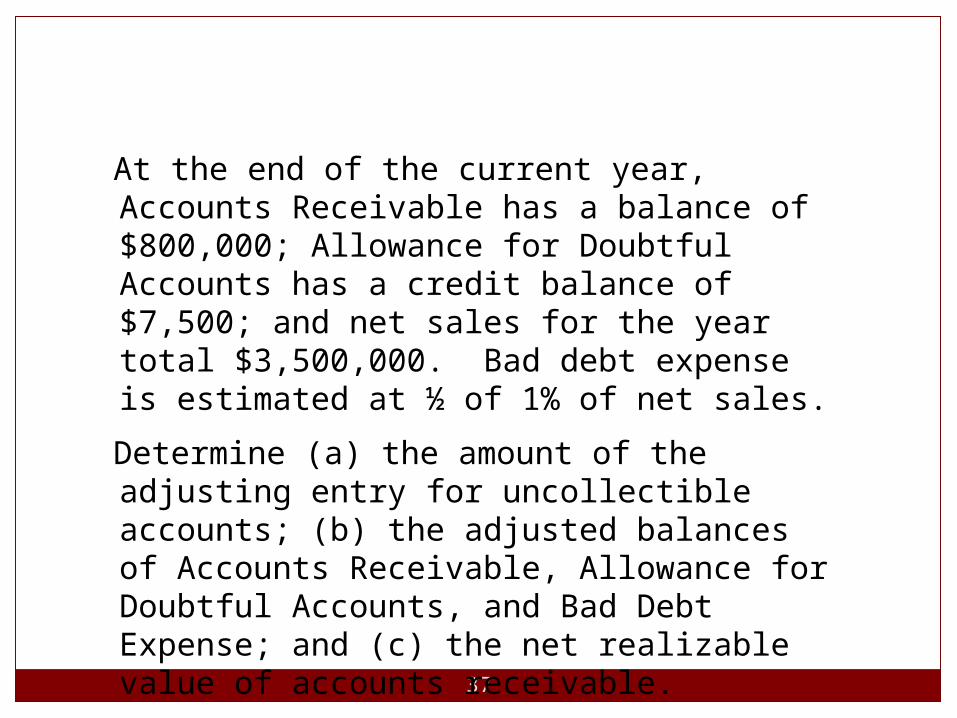

At the end of the current year, Accounts Receivable has a balance of $800,000; Allowance for Doubtful Accounts has a credit balance of $7,500; and net sales for the year total $3,500,000. Bad debt expense is estimated at ½ of 1% of net sales.

Determine (a) the amount of the adjusting entry for uncollectible accounts; (b) the adjusted balances of Accounts Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense; and (c) the net realizable value of accounts receivable.

38

(a) $17,500 ($3,500,000 x .005 ( ½ of 1%) )

Adjusted Balance(b)Accounts Receivable $800,000

Allowance for Doubtful Accounts ($7,500 + $17,500) 25,000Bad Debt Expense 17,500

(c) $775,000 ($800,000 – $25,000)

Adjusting entry (a)

Balances (b)

NRV (c)

39

The longer an account receivable is outstanding, the less likely that it

will be collected. Basing the estimate of uncollectible accounts on how long specific amounts have been outstanding is called aging

the receivables.

Estimating Uncollectibles Based on Analysis of Receivables

40

Aging of Accounts Receivables

41

Estimate of Uncollectible Accounts

42

Collection Rates by Number of Months Past Due

43

Estimate Based on Analysis of Receivables

If it is estimated that $3,390 of the receivables will be

uncollectible and the Allowance for Uncollectible

Accounts currently has a balance of $510, the Bad Debt Expense must be

debited for $2,880 ($3,390 – $510).

44

Estimate Based on Analysis of Receivables

Aug. 31 Bad Debt Expense 2 880 00

Allowance for Doubtful Accounts 2 880 00

Uncollectible accounts ($3,390 – $510).

45

BAD DEBT EXPENSEAug. 31 Adj. entry2,880Aug. 31 Adj. bal.2,880

ALLOWANCE FOR DOUBTFUL ACCOUNTSAug. 31 Unadj. bal.510Aug. 31 Adj. entry2,880Aug. 31 Adj. bal.3,390Balance sheet

method finds the ending balance and

adjust to that

46

If the unadjusted balance of Allowance for

Uncollectible Accounts had been a debit balance

of $300, the amount of the adjustment would have been $3,690 ($3,390 +

$300).

47

BAD DEBT EXPENSEAug. 31 Adj. entry3,690Aug. 31 Adj. bal.3,690

ALLOWANCE FOR DOUBTFUL ACCOUNTSAug. 31 Adj. entry3,690Aug. 31 Adj. bal.3,390

Aug. 31 Unadj. bal.300

48

At the end of the current year, Accounts Receivable has a balance of $800,000; Allowance for Doubtful Accounts has a credit balance of $7,500; and net sales for the year total $3,500,000. Using the aging method, the balance of Allowance for Doubtful Accounts is estimated as $30,000.

Determine (a) the amount of the adjusting entry for uncollectible accounts; (b) the adjusted balances of Accounts Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense, and (c) the net realizable value of accounts receivable.

49

(a) $22,500 ($30,000 – $7,500)

Adjusted Balance(b)Accounts Receivable $800,000

Allowance for Doubtful Accounts 30,000Bad Debt Expense 22,500

(c) $770,000 ($800,000 – $30,000)

50

Compare the direct write-off and

allowance methods of accounting for

uncollectible accounts

Objective 5

Objective 5

51

51

Comparing Direct-Write-Off and Allowance Methods

Direct Write-Off Method

Allowance Method

W/O Acct W/O Acct

Recvd partial pmt w/o rest Recvd partial pmt w/o rest

Recvd pmt of previously w/o acct Recvd pmt of previously w/o acct

W/O Acct W/O Acct

Co Used the % of credit sales and est uncoll exp

Co Used the % of credit sales and est uncoll exp

52

Comparing the Direct Write-Off and Allowance Methods

Direct Write-Off Method

When the actual accounts receivable are determined to be uncollectibleNo allowance account is used

Amount of bad debt expense recorded

Allowance account

Primary usersSmall companies and companies with relatively few receivables

53

Comparing the Direct Write-Off and Allowance Methods

Allowance Method

Using estimate based on either (1) a percentage of sales or (2) analysis of receivables.The allowance account is used

Amount of bad debt expense recorded

Allowance account

Primary users Large companies and those with a large amount of receivables

54

Describe the nature,

characteristics, and accounting for

notes receivable.

Objective 6

Objective 6

55

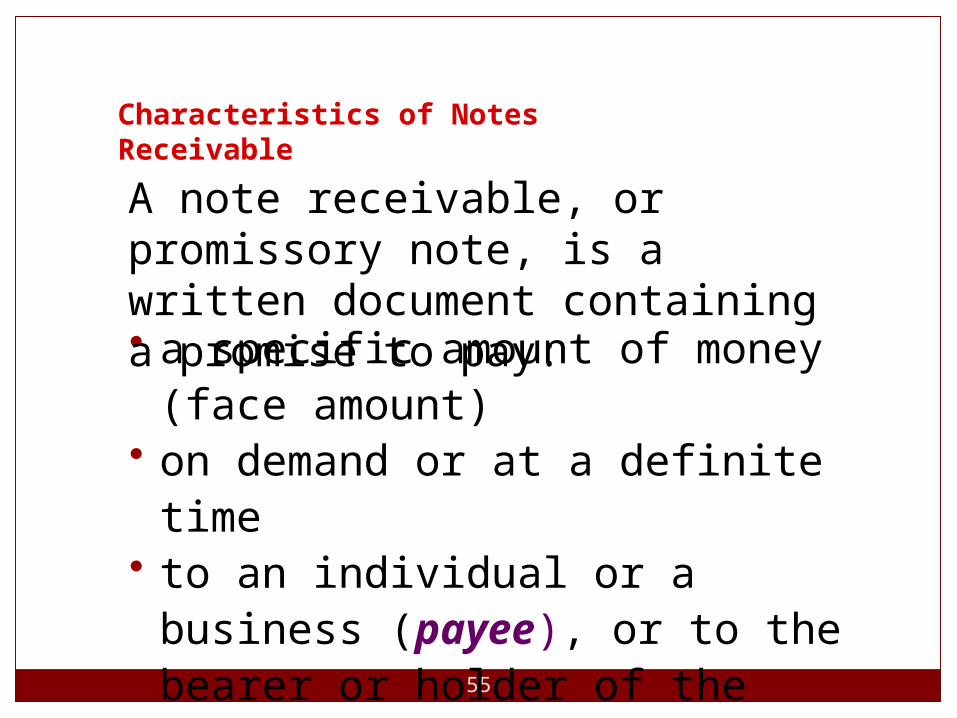

• a specific amount of money (face amount)

• on demand or at a definite time • to an individual or a business

(payee), or to the bearer or holder of the note.

A note receivable, or promissory note, is a written document containing a promise to pay:

Characteristics of Notes Receivable

56

The one making the promise is called the

maker. The date a note is to be paid is called the due date or maturity

date.

Characteristics of Notes Receivable

57

$_____________Fresno, California______________20___March 16 08

________________ _AFTER DATE _______ PROMISE TO PAY TO Ninety days

We

THE ORDER OF ____________________________________________ Judson Company

_________________________________________________DOLLARSTwo thousand five hundred 00/100---------------------------

PAYABLE AT ______________________________________________City National Bank

VALUE RECEIVED WITH INTEREST AT ____ 10%

2,500.00

NO. _______ DUE___________________14 June 14, 2008

TREASURER, WILLIARD COMPANY

H. B. Lane

MakerMaker

PayeePayee

58

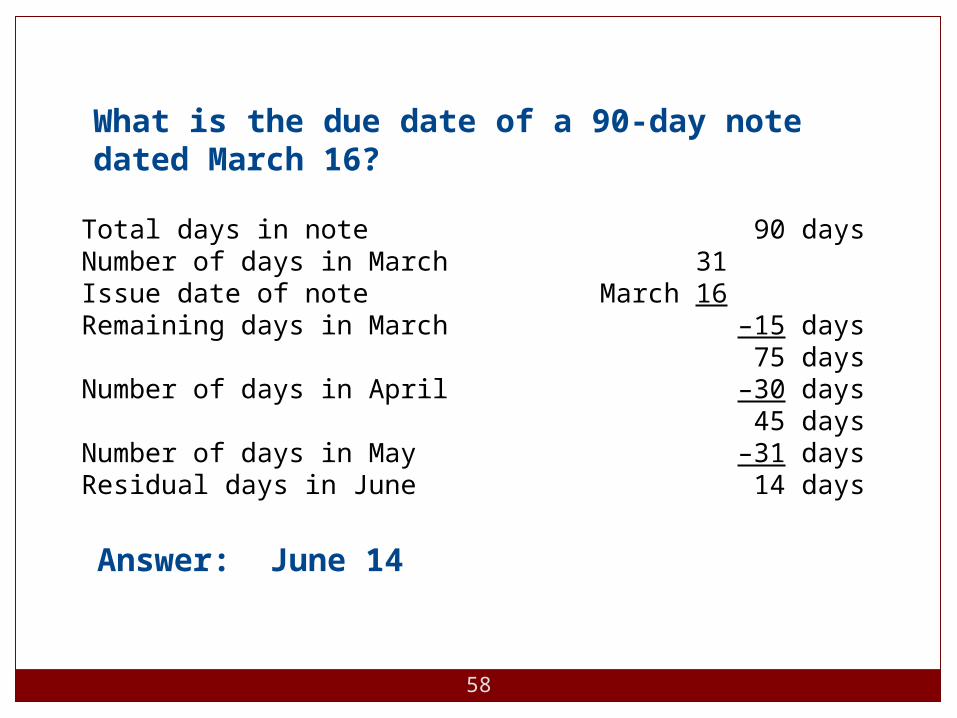

Total days in note 90 daysNumber of days in March 31Issue date of note March 16Remaining days in March –15 days

75 daysNumber of days in April –30 days

45 daysNumber of days in May –31 daysResidual days in June 14 days

Answer: June 14

What is the due date of a 90-day note dated March 16?

59

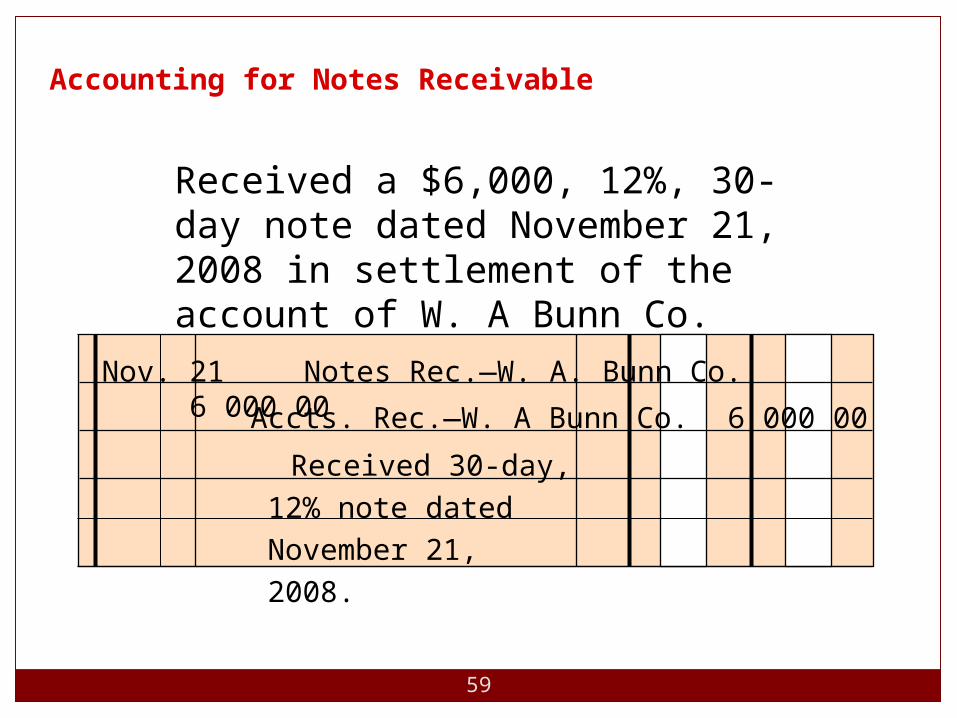

Received a $6,000, 12%, 30-day note dated November 21, 2008 in settlement of the account of W. A Bunn Co.

Accounting for Notes Receivable

Nov. 21 Notes Rec.—W. A. Bunn Co. 6 000 00 Accts. Rec.—W. A Bunn Co. 6 000 00

Received 30-day, 12% note dated November 21, 2008.

60

On December 21, when the note matures, the firm receives $6060 from W. A. Bunn Company ($6,000 plus $60 interest).

Dec. 21 Cash 6 060 00 Notes Rec.—W. A. Bunn Co. 6 000 00

Interest Revenue* 60 00

Received principal and

interest on matured

note.*$6,000 x 12% x 30/360 = $60

61

If W. A. Bunn Company fails to pay the note on the due date, it is considered a dishonored note receivable. The note and interest are transferred to the customer’s account.

Dec. 21 Accts Rec.—W. A. Bunn Co. 6 060 00 Notes Rec.—W. A. Bunn Co. 6 000 00

Interest Revenue 60 00

Recorded

dishonored note,

plus interest.

62

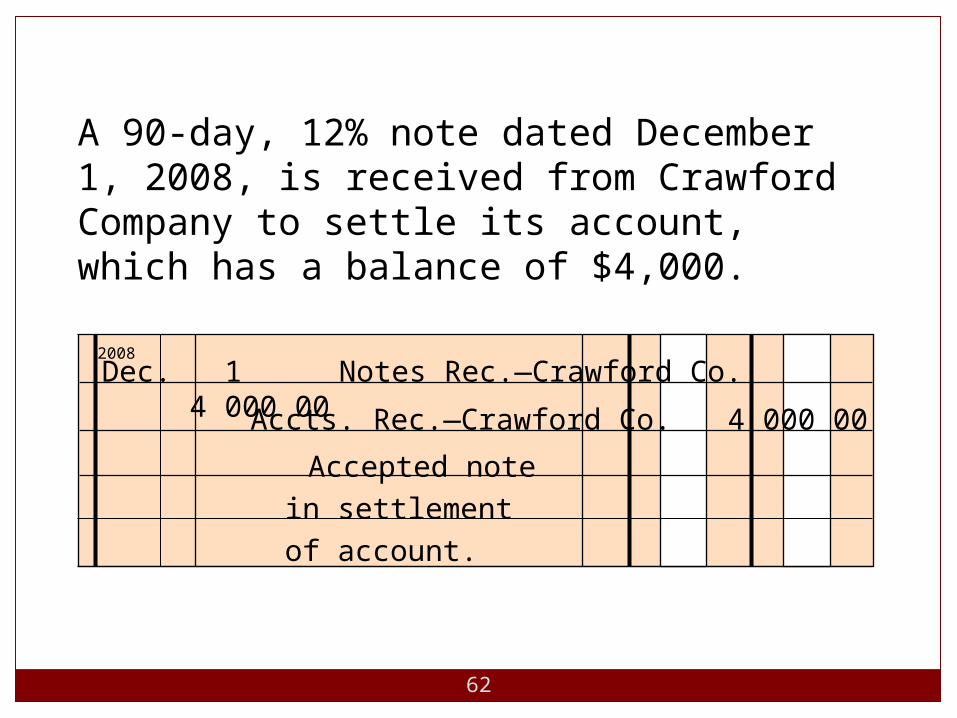

A 90-day, 12% note dated December 1, 2008, is received from Crawford Company to settle its account, which has a balance of $4,000.

Dec. 1 Notes Rec.—Crawford Co. 4 000 00 Accts. Rec.—Crawford Co. 4 000 00

Accepted note in settlement of account.

2008

63

Dec. 31 Interest Receivable 40 00 Interest Revenue 40 00

Accrued interest ($4,000 x 12% x 30/360).

2008

Assuming that the accounting period ends on December 31, an adjusting entry is required to record the accrued interest of $40 ($4,000 x 0.12 x 30/360).

64

Mar. 1 Cash 4 120 00 Notes Rec.—Crawford Co. 4 000 00

2009

On March 1, 2009, $4,120 is received for the note ($4,000) and interest ($120).

Interest Receivable 40 00

Interest Revenue 80 00

($4,000 x 12% x 30/360).

Collected note and accrued interest.

65

Same Day Surgery Center received a 120-day, 6% note for $40,000, dated March 14 from a patient on account.

a. Determine the due date of the note.

b. Determine the maturity value of the note.

c. Journalize the entry to record the receipt of the payment of the note at maturity.

66

b. $40,800 [$40,000 + ($40,000 x 6% x 120/360)]

c. Cash 40,800Notes Receivable 40,000Interest Revenue 800

a. July 12 determined as follows:

March 17 days (31 – 14)April 30 daysMay 31 daysJune 30 daysJuly 12 days Total 120 days

67

Describe the reporting of

receivables on the balance

sheet.

Objective 7

Objective 7

Receivables on Balance Sheet

69

Accounts Receivable Turnover

The accounts receivable turnover measures how frequently during the year the accounts receivable are being converted to cash.Accounts Receivable Turnover

Net sales Avg accounts receivable

=

70

Federal Express Corporation

Accounts Receivable Turnover (2004)

$17,383$2,337

=

Accounts Receivable Turnover (2004)

= 7.4

* [($2,475 + $2,199)/2]

2005 2004 2003Net sales $19,364 $17,383 ---

Accounts receivable 2,703 2,475 $2,199Avg accounts receivable 2,589 2,337

*

*

71

Federal Express Corporation

Accounts Receivable Turnover (2005)

$19,364$2,589

=

Accounts Receivable Turnover (2005)

= 7.5

2005 2004 2003

Net sales $19,364 $17,383 --- Accounts receivable 2,703 2,475 $2,199Avg accounts receivable* 2,589 2,337

* [($2,703 + $2,475)/2]

72

Use: To assess the efficiency in collecting receivables and in the management of credit.

Number of Days’ Sales in Receivables

Average Accounts receivableAverage daily sales

Number of Days’ Sales in Receivables

=

73

Federal Express Corporation

Number of Days’ Sales in Receivables (2004)

$2,337 47.6

=

Number of Days’ Sales in Receivables (2004)

= 49.1

2005 2004 2003

Net sales $19,364 $17,383

Accounts receivable 2,703 2,475 $2,199

Average accounts receivable2,589 2,337

Average daily sales 53.1 47.6

*

[($2,475 + $2,199)/2]

*

*

**

($17,383/365)**

---

[($2,703 + $2,475)/2]

*

74

Federal Express Corporation

Number of Days’ Sales in Receivables (2005)

$2,589 53.1

=

Number of Days’ Sales in Receivables (2005)

= 48.8

*

[($2,703+ $2,475)/2]*

($19,364/365)

**

2005 2004 2003 Net sales $19,364$17,383

Accounts receivable 2,7032,475

$2,199 Average accounts receivable

2,589 2,337Average daily sales 53.1 47.6

*

**

---

Summary

Classification of Receivables

Uncollectible A/R

Direct Write-Off Method

Allowance Method

Notes Receivable