32

Modes of Securing Bank Advances: Charge Creation, guarantee etc S.M. Abdul Hakim DGM, BBTA

Modes of Securing Bank Advances:

Charge Creation, guarantee etc

S.M. Abdul HakimDGM, BBTA

2

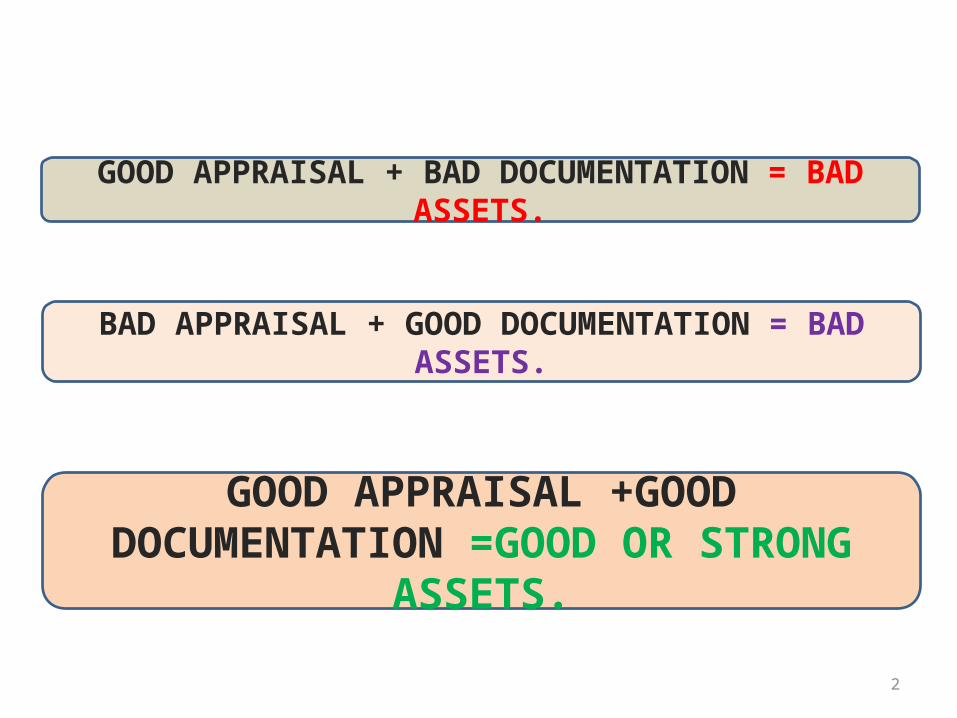

GOOD APPRAISAL + BAD DOCUMENTATION = BAD ASSETS.

BAD APPRAISAL + GOOD DOCUMENTATION = BAD ASSETS.

GOOD APPRAISAL +GOOD DOCUMENTATION =GOOD OR STRONG ASSETS.

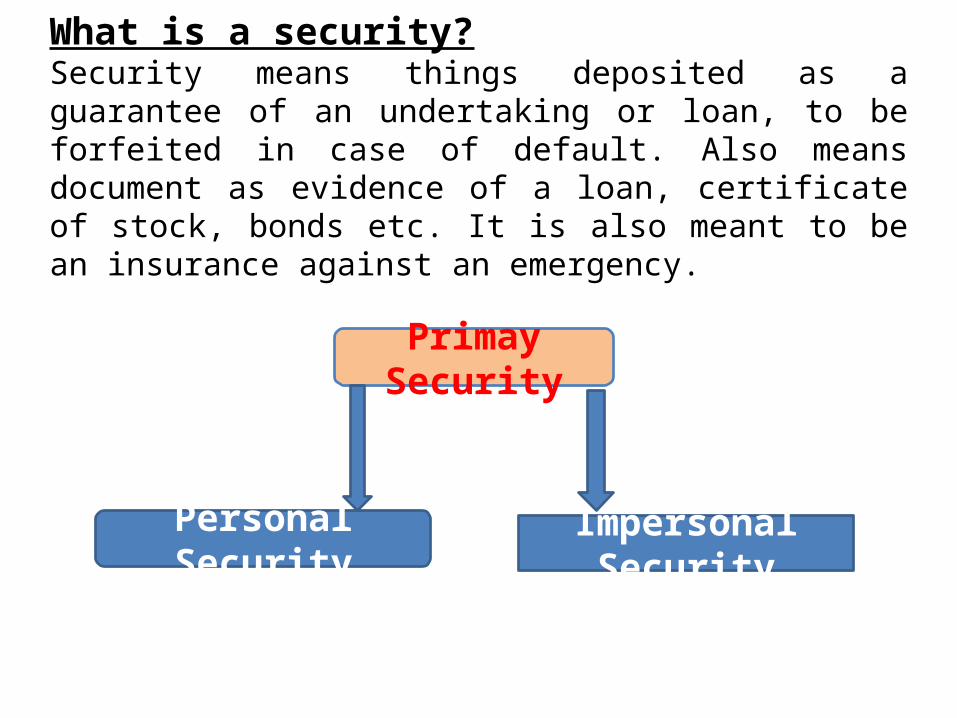

What is a security?Security means things deposited as a guarantee of an undertaking or loan, to be forfeited in case of default. Also means document as evidence of a loan, certificate of stock, bonds etc. It is also meant to be an insurance against an emergency.

Primay Security

Personal Security Impersonal Security

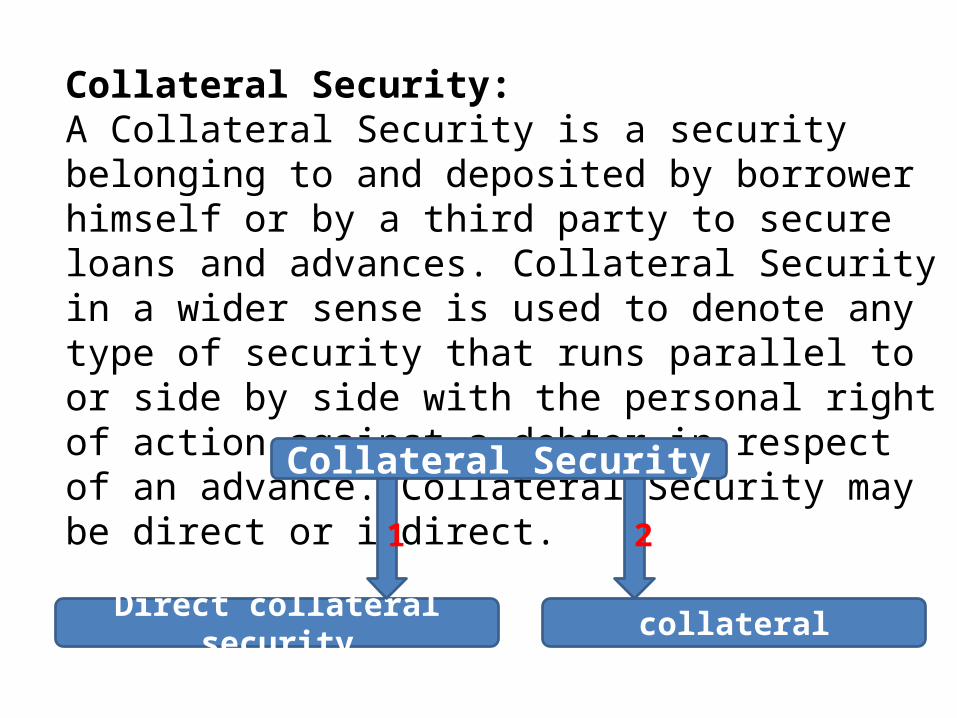

Collateral Security: A Collateral Security is a security belonging to and deposited by borrower himself or by a third party to secure loans and advances. Collateral Security in a wider sense is used to denote any type of security that runs parallel to or side by side with the personal right of action against a debtor in respect of an advance. Collateral Security may be direct or indirect.

Collateral Security

Direct collateral security Indirect collateral security

1 2

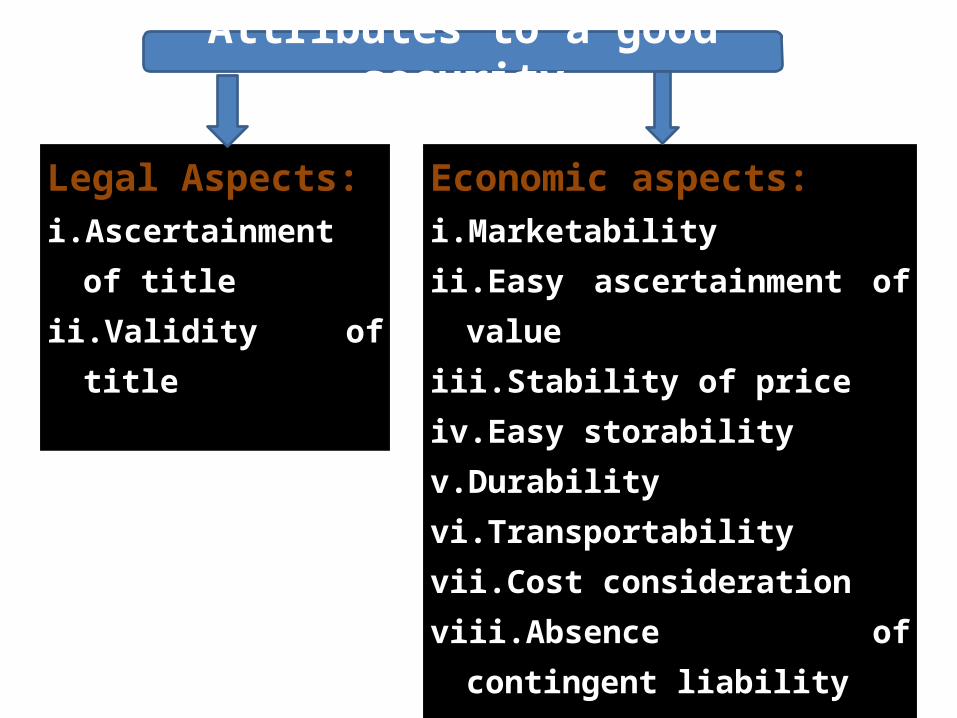

Attributes to a good security

Legal Aspects:i. Ascertainment of titleii. Validity of title

Economic aspects:i. Marketabilityii. Easy ascertainment of valueiii. Stability of priceiv. Easy storability v. Durabilityvi. Transportabilityvii.Cost considerationviii.Absence of contingent liabilityix. Yield

Charge:Charge means right of payment out of certain property. In a charge there is no transfer of interest or property. It is a right over some tangible asset of the borrower. It is a legal transaction as a result of which the lender acquires certain rights over the property and the borrower is refrained from dealing in them. In a charge there must be a notice to the subsequent transferees, otherwise the charge is not effective as to the subsequent transferees.

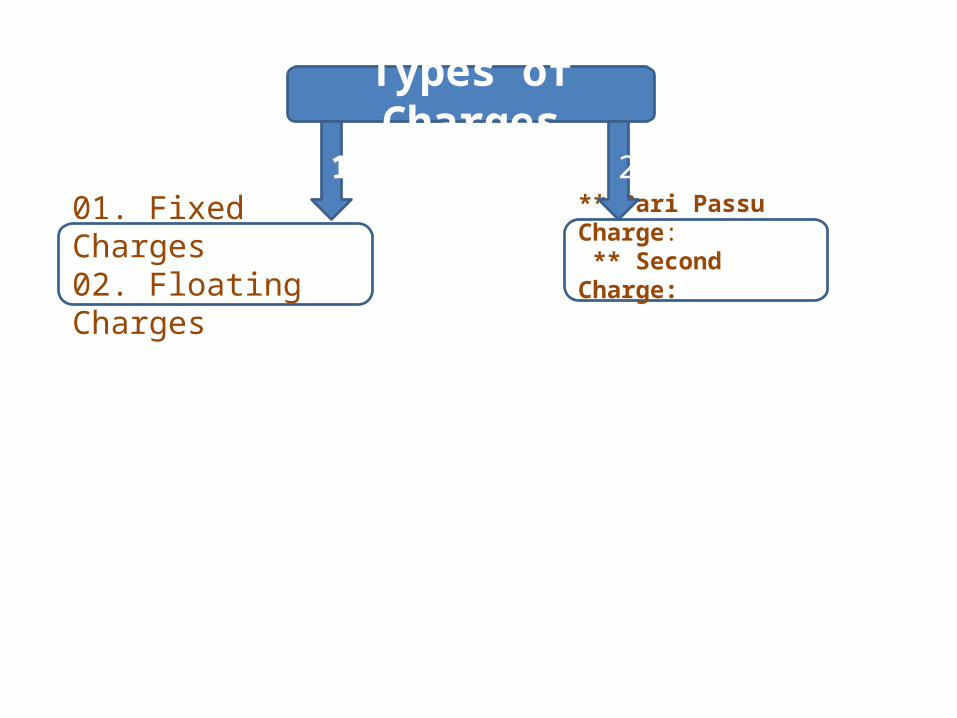

01. Fixed Charges02. Floating Charges

** Pari Passu Charge: ** Second Charge:

Types of Charges

1 2

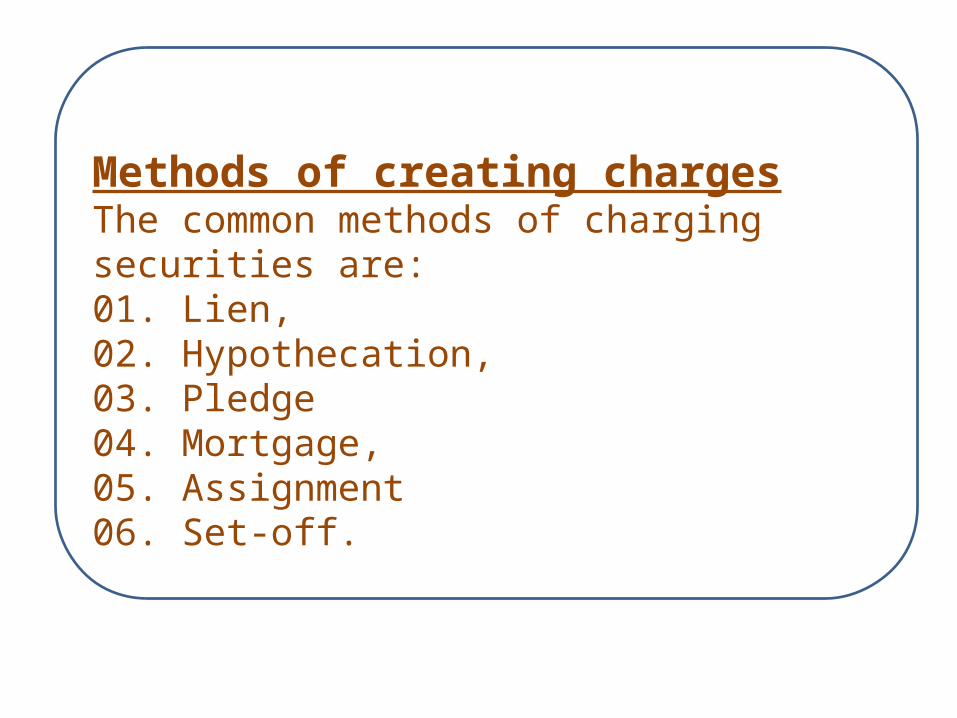

Methods of creating chargesThe common methods of charging securities are:01. Lien,02. Hypothecation,03. Pledge04. Mortgage,05. Assignment 06. Set-off.

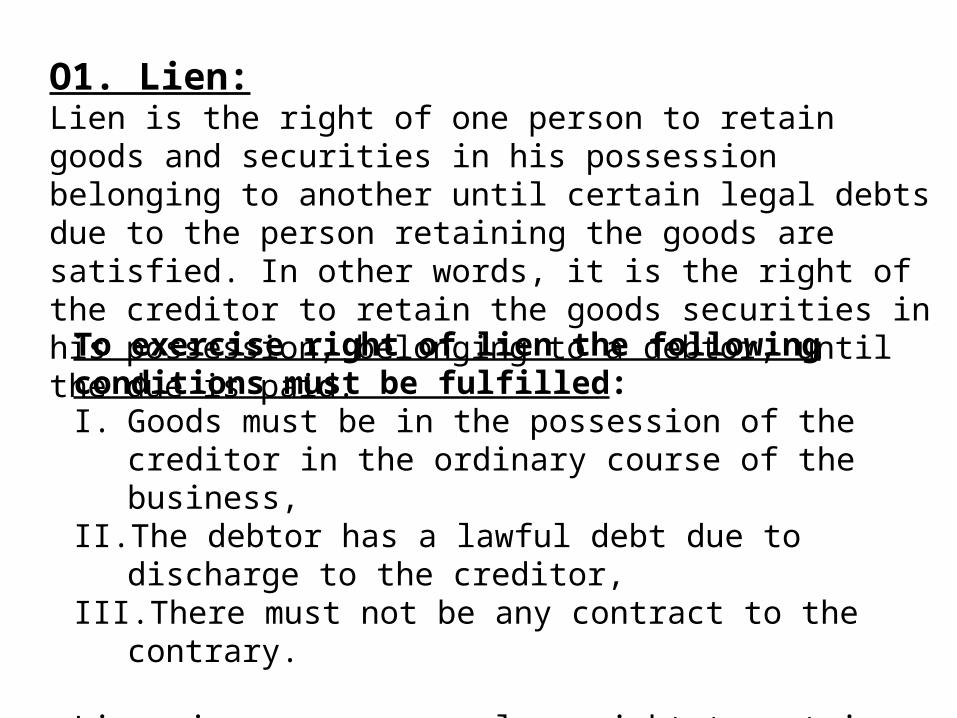

O1. Lien:Lien is the right of one person to retain goods and securities in his possession belonging to another until certain legal debts due to the person retaining the goods are satisfied. In other words, it is the right of the creditor to retain the goods securities in his possession, belonging to a debtor, until the due is paid.

To exercise right of lien the following conditions must be fulfilled:I. Goods must be in the possession of the creditor in the ordinary

course of the business,II. The debtor has a lawful debt due to discharge to the creditor,III. There must not be any contract to the contrary.

Lien gives a person only a right to retain the possession of goods and not the power to sell unless such a right is expressly conferred by statute or by custom or usage.

Types of lien: There are two kinds of lien:

i. Particular Lienii. General Lien

Other types: Banker’s Lien Negative Lien

Exception to the right of lien:i. Valuables lying in safe deposit vault.ii. Bills of exchange or other documents for special purpose.iii. Money deposited for special purpose.iv. Documents for valuable left in the banks.v. Securities deposited before loan sanctioned.vi. Trust account.vii. Any security left in the banker’s hand to cover a proposed

advance which is subsequently declined.

02. Hypothecation:Hypothecation is a charge against property for an amount of debt where neither ownership nor possession is passed to the creditor. Though the borrower is an actual physical possession but the constructive possession remains with bank as per the deed of hypothecation. The borrower holds the possession not in his own right as the owner of the goods but as the agent of the bank.

Features of Hypothecation: Charge against a property for a amount of debt, Goods remains in the possession of the borrower, Equitable charge to the bank under document (Letter of credit), Borrower bind himself to give possession of the hypothecated

goods to the bank when called upon to do so, It is a floating charge, It is rather precarious.

Precautions to be taken by the banker while granting loans on hypothecation :The position of the banker under hypothecation is not as safe as under a pledge. The borrower may fail to give possession of the goods hypothecated to the bank, or sells the entire stock or borrows from another banker on the security of the same goods. This facility should be given only persons or business houses of

high reputation and sound financial standing, The banker must periodically inspect the hypothecated goods

and the account books, The borrower should be asked to submit a statement of stock

periodically giving correct position about the stocks, An undertaking should be taken from the borrower that he shall

not charge the same goods to some other bank or persons, A nameplate of the bank, mentioning that the stocks are

hypothecated to it, must be displayed at a prominent place, Stocks should be fully insured against fire and other risk.

03. Pledge:Pledge is the “Bailment of goods as security for payment of a debt or performance of promise”(sec-172 of Cont. Act)Bailment is the delivery of goods by one person to another for some purpose, under a contract that the goods shall, when the purpose is accomplished, be returned or otherwise disposed of, according to the direction of the persons delivering them (sec-148 of Cont. Act).

Who can pledge the goods?i. The owner of the goods himselfii. Mercantile agent (sec-178 of Contract Act, 1872)iii. Joint-owner with consent of other co-owneriv. If a buyer leaves the goods or document of title after sale in the

possession of the seller, the latter may make a valid pledge of the goods provided the pledge acts in good faith and he has no notice of the sale of goods to the buyer.

v. A pledgee can himself re-pledge the goods.

Rights/Obligations of Pledger i. To claim back the security pledged on repayment of the debt

with interest and other charges,ii. To receive reasonable notices in case the pledgee intends to

sell the goods,iii. In case of sale, the pledger is entitled to receive from the

pledgee any surplus after debt is completely paid off,iv. A pledger must disclose the pledge any material faults or extra

ordinary risk involved in the goods.v. Any loss caused to the goods, because of mishandling or

negligence on the part of the pledge, the pledger has the right to claim the same,

vi. Pledger is responsible to meet the expenditure for the preservation of the goods,

vii. The pledger is liable for any loss caused to the pledgee because of defect in his pledgers title to the goods.

Rights/Obligations of Pledgeei. The pledgee has a right to retain the goods pledged to him by the

pledger till the debt, together with the interest due therein and the expenses for preservation of the goods, are fully paid by the pledger.

ii. In case of default by the pledger to make payment of the debt, the pledgee has the right either –

a) To file a suit against the pledger for the amount due and retain the goods as a collateral security; or

b) To sell the goods pledged after giving the pledger reasonable notice of sale(sec-176).

iii. The pledgee must take care of the goods pledged to himiv. The pledgee can not make unauthorized use of the pledged goods.v. The pledgee is bound to return the goods on payment of the debtvi. The pledgee will pay the pledger any benefit accrued from the

pledged goods.vii. The pledgee is responsible to the plegor for any loss, destruction or

deterioration of the goods, if the goods are not returned by the pledgee at proper time (Sec-161).

Documents required for Pledged:i. Demand Promissory Noteii. Letter of continuityiii. Agreement for pledgeiv. Letter of lien (containing set-off clause)v. Letter of guarantee (if any)vi. Insurance policy covering all riskvii. Invoice of goods pledgedviii.Latest stock reportix. Another document as per sanction letter.

04. MortgageAs per T.P. Act, 1882 sec-58(a) A ‘Mortgage’ is the transfer of an interest in specific immovable property for the purpose of securing:i. The payment of money advanced or to be advanced by way of

loan,ii. An existing or future debt, iii. The performance of an engagement which may give rise to

pecuniary liability,iv. The transferor is called `Mortgagor’, the transferee is called

`Mortgagee’, the principal money & the interest of which payment is secured for the time being are called `Mortgage money’ and the instrument by which the transfer is effect called `Mortgage deed’.

Procedure of legal mortgage: i. Mortgage Deed, signed by the mortgagor and two witnesses,ii. Registration of mortgage deed,iii. Effective from the date of execution.

Procedure of equitable mortgage: a) Deposit of original title deeds,b) Sending a covering letter by the mortgagor.c) All documents should be in original,d) Maintaining equitable mortgage register,e) Periodically submission of encumbrance certificate,f) Periodical tax receipts shall also be verified,g) If mortgagor is a Ltd. Co., must be registered within 21 days

and charge with joint stock Co.

Documents In Case Simple /Legal Mortgage:i. Chain of documents regarding title (if available),ii. Original title deed of the mortgagor (if available),iii. C.S., S.A., & R.S. Parcha,iv. Up to date rent receipt,v. Valuation certificate from concerned authority,vi. Clearing certificate from local body/Dev. body,vii. Non-encumbrance certificate,viii. Legal opinion from legal adviser,ix. Power of attorney authorizing the bank to sell the mortgage

property,x. Site plan/Location map,xi. Certified copy of mortgage deed along with receipt.

Documents in Case of Equitable Mortgage:All documents of legal mortgage except mortgage deed and the additional following documents required:i. Original title deed,ii. Memorandum of deposit of original title deed,iii. A registered power of attorney,iv. Any other documents as stated in the sanction letter.

05. Assignment: An assignment means a transfer by one person of a right, property or debt (existing or future) to another person. The person who assigns the right, property or debt is called the assignor. The person to whom the right etc. is assigned is called the assignee.

"actionable claim" means a claim to any debt, other than a debt secured by mortgage of immovable property or by hypothecation or pledge of movable property, or to any beneficial interest in movable property not in the possession, either actual or constructive, of the claimant, which the civil courts recognise as affording grounds for relief, whether such debt or beneficial interest be existent, accruing, conditional or contingent;

Legal Assignment and Equitable Assignment:Legal assignment: Section 130 of the transfer of property Act states a legal assignment is one where:i. Assignment Deed is in writing duly signed by the assignor and the intention to pass

by assignment is clear.ii. The transfer of actionable claim is absolute.iii. The assignee informs the assignor’s debtor about the assignment and also gets the

confirmation of the notice and the debt.

Equitable Assignment: An equitable Assignment is one which does not fulfill any of the above requirements. The assignee in legal assignment can sue in his own name but the assignee of an equitable assignment cannot do so. A legal assignee can also give a valid discharge for the debt without the concurrence of the assignor.

Common assignmentThe most common types of assignment are:i. Book debt,ii. Contract money due from government or semi government

bodies,iii. Supply bills,iv. Life insurance policies.

Assignment as security:Assignment is not good security for following reasons:v. Value of the assignment depends on the integrity and credit

worthiness of assignor and his debtor,vi. In case assignor’s debtor exercise right of set off, Assignee’s

position becomes vulnerable. Assignee cannot have better rights than those which the assignor possessor.

vii. Right of assignee may be repudiated by breach of contract between assignor and his debtor.

Necessary Precaution:As assignment is not good security following precautions to be taken by banks:

i. Assignor to give irrevocable letter to debtor to pay debt to banker.

ii. Banker must get assignment acknowledged by debtor.iii. Banker must get clear notice of prior assignment iv. Banker must sent notice of assignment to debtor to prevent

subsequent assignmentv. Constant follow-up necessary.vi. Assignment for whole.

06. Set-off:Set-off means the total or partial merging of a claim of one person against another in a counter claim by the later against the former. It is in effect the combining of accounts between a debtor and a creditor so as to arrive at the net balance payable to one or the other. It is a right which accrues to the banker as a result of the banker customer relationship.Set-off arises when a debtor or his creditor wishes to arrive at the net figure owing between them when separate accounts or debt are involved.

Ingredients of Set-off:i. Mutual debts for sums certain,ii. Debts must be due immediately,iii. Debts must be in the same right,iv. No agreement to the contrary.

Notice of Set-off:As already stated the right of set-off accrues to the banker as a result of banker customer relationship. When a customer opens two or more accounts, it may be his intention to keep them separate. So his different accounts cannot be arbitrarily combined without proper notice to the customer. Under such situation, it is advisable to take prior letter of set-off so a banker can combine them at its discretion without giving the customer any notice. It also serves as a proof that the banker’s right of set-off exists and the customer has not waived it. However, in actual practice the bank sends a notice to the customer as soon as the right of set-off is exercised.

Automatic Right of set-off:The following are the situations where the banker’s right of set-off automatically accrues and no notice of set-off is necessary:i. On the death, insanity or insolvency of the customer,ii. On the insolvency of a partner of a firm,iii. On receipt of a garnishee order,iv. On the winding up of a company,v. On receipt of notice of assignment of the credit balance of the customer. Banker’s Right of Set-off: The decision and judgment in different cases reveal that the following cases where the branches can exercise the right of set-off: To combine two or more accounts of the same customer in the same branch of

a bank. To combine two or more accounts of a customer maintained in different

branches of the same bank. To adjust the surplus amount of the sale proceeds or realization of the

securities held as cover for one particular debt for liquidation of any other debt after realization of the particular debt.

GUARANTEES A guarantee is a promise by a person (the guarantor) to settle a debt or fulfill the promise of someone else. The person to whom the promise is made is called the creditor or lender and the person on whose behalf of the promise is made is called the principal debtor or borrower.

Important Aspects of Guarantees Most standard bank and finance company guarantees are “all

obligations guarantees”. This means that the guarantor is liable for all the borrower’s obligations to the creditor and the guarantee is not limited to the particular transaction which gave rise to the guarantee. The guarantor’s liability extends not only to all future lending but also to all debts that the principal debtor already owes to the creditor.

Under a standard all obligations guarantee the guarantor is also liable for the borrower’s obligations to the lender. If, for example, the borrower has given the lender a guarantee in respect of another person or company, the guarantor will be liable for all claims brought against the borrower by the lender in respect of the borrower’s guarantee.

Under a standard all obligations guarantee the guarantor will also be liable for any interest payable by a borrower, and any legal costs incurred by the lender in enforcing the principal obligation against either the borrower or the guarantor, or realizing any security given to the lender.

In some instances a guarantee will be limited in amount. In most standard all obligations guarantees there is a limitation clause, which if left blank, will mean that the guarantor’s liability is unlimited.

If the guarantor has given an all obligations mortgage or other charge as security for the guarantor’s obligations to the lender, that security will extend to the debts for which the guarantor has given a guarantee.

Where there are co-guarantors under the one all obligations guarantee, the liability of each co-guarantor is joint and several so that each co-guarantor will be individually liable to the lender for all of the guaranteed obligations.

Release of a Guarantee The guarantor is not liable unless the borrower is liable. If the principal obligation has been performed the guarantee is discharged. For example, when the borrower pays the lender the full amount of the guaranteed debt. Such a payment will normally discharge the guarantor. The guarantee may also be discharged by an express agreement between the lender and the guarantor. In some circumstances a guarantee may be terminated if the guarantor gives written notice to the lender. In such a case the guarantor will remain liable for the debts or liabilities that have accrued up to the giving of such notice. However, generally the guarantor will not be released from his or her obligations until the lender gives written notice.