SOVEREIGN & SUPRANATIONAL FEBRUARY 5, 2015 RATINGS IBRD (World Bank) Rating Outlook Long-term Issuer Aaa STA Short-term Issuer (P)P-1 STA Senior Unsecured Aaa STA Table of Contents: OVERVIEW AND OUTLOOK 1 ORGANIZATIONAL STRUCTURE AND STRATEGY 2 The World Bank Group’s Public-Sector Lender 2 Capital Increase Affects Voting Power and Supports Growth in Lending Operations 2 RATING RATIONALE 3 Capital Adequacy: Very High 3 Liquidity: Very High 7 Strength of Member Support: Very High 9 Rating Range 11 Comparatives 12 APPENDICES 13 Rating History 13 Annual Statistics 14 MOODY’S RELATED RESEARCH 16 RELATED WEBSITES 16 Analyst Contacts: NEW YORK +1.212.553.1653 Steven A. Hess +1.212.553.4741 Senior Vice President [email protected]Renzo Merino +1.212.553.0330 Analyst [email protected]» contacts continued on the last page This Credit Analysis provides an in-depth discussion of credit rating(s) for IBRD (World Bank) and should be read in conjunction with Moody’s most recent Credit Opinion and rating information available on Moody's website . IBRD (World Bank) Supranational Overview and Outlook This Credit Analysis elaborates on the International Bank for Reconstruction and Development’s (IBRD or World Bank, Aaa stable) credit profile in terms of Capital Adequacy, Liquidity and Strength of Member Support, which are the three main analytical factors in Moody’s Supranational Rating Methodology . Despite a slight deterioration in capitalization metrics in recent years, the IBRD’s financial position remains one of its primary strengths supporting the Aaa rating. The bank’s fundamentals reflect its robust risk management practices and reasonably conservative financial policies. These policies minimize asset/liability mismatch risks and result in strong and stable credit metrics in terms of capital adequacy and liquidity. Also contributing to the institution’s financial strength is its tested preferred creditor status, which translates into superb asset performance. Preferred creditor status means that most countries give priority to repaying their obligations to the IBRD. In addition to the bank’s very strong intrinsic financial strength, bondholders enjoy substantial protection in the form of the bank's large cushion of callable capital. Although a scenario where the IBRD had to call on capital appears to be extremely remote, currently the size of this buffer would be more than sufficient to repay the bank’s outstanding debt in its entirety without liquidating its assets. The above strengths are counteracted by several potential credit challenges that stem primarily from its lending activity. As a result of its development mandate and global scope, the bank lends to riskier sovereigns, some of which have no or very limited access to capital markets. As such, the bank could, albeit with low probability, experience significant spike in non-performing loans should there be simultaneous financial crises in several large borrowers or a regional crisis in one of the largest borrowing regions. Additionally, although the preferred creditor status does enhance asset quality, the IBRD still experiences arrears on debt service from its borrowers. However, these amounts have not exceeded 1% since 2007 and are amply covered by loan loss provisions. The outlook on the bank’s rating remains stable. The institution’s strong capital base should allow it to withstand crises in developing countries without impairing its ability to service its obligations. The rating could face downward pressure if several of the IBRD's largest borrowers end up in default and are unwilling or unable to meet their obligations to the bank.

Transcript

CREDIT ANALYSIS

SOVEREIGN & SUPRANATIONAL FEBRUARY 5, 2015

RATINGS

IBRD (World Bank) Rating Outlook

Long-term Issuer Aaa STA Short-term Issuer (P)P-1 STA Senior Unsecured Aaa STA

Table of Contents:

OVERVIEW AND OUTLOOK 1 ORGANIZATIONAL STRUCTURE AND STRATEGY 2

The World Bank Group’s Public-Sector Lender 2 Capital Increase Affects Voting Power and Supports Growth in Lending Operations 2

RATING RATIONALE 3 Capital Adequacy: Very High 3 Liquidity: Very High 7 Strength of Member Support: Very High 9 Rating Range 11 Comparatives 12

APPENDICES 13 Rating History 13 Annual Statistics 14

MOODY’S RELATED RESEARCH 16 RELATED WEBSITES 16

Analyst Contacts:

NEW YORK +1.212.553.1653

Steven A. Hess +1.212.553.4741 Senior Vice President [email protected]

» contacts continued on the last page This Credit Analysis provides an in-depth discussion of credit rating(s) for IBRD (World Bank) and should be read in conjunction with Moody’s most recent Credit Opinion and rating information available on Moody's website.

IBRD (World Bank) Supranational

Overview and Outlook

This Credit Analysis elaborates on the International Bank for Reconstruction and Development’s (IBRD or World Bank, Aaa stable) credit profile in terms of Capital Adequacy, Liquidity and Strength of Member Support, which are the three main analytical factors in Moody’s Supranational Rating Methodology.

Despite a slight deterioration in capitalization metrics in recent years, the IBRD’s financial position remains one of its primary strengths supporting the Aaa rating. The bank’s fundamentals reflect its robust risk management practices and reasonably conservative financial policies. These policies minimize asset/liability mismatch risks and result in strong and stable credit metrics in terms of capital adequacy and liquidity. Also contributing to the institution’s financial strength is its tested preferred creditor status, which translates into superb asset performance. Preferred creditor status means that most countries give priority to repaying their obligations to the IBRD. In addition to the bank’s very strong intrinsic financial strength, bondholders enjoy substantial protection in the form of the bank's large cushion of callable capital. Although a scenario where the IBRD had to call on capital appears to be extremely remote, currently the size of this buffer would be more than sufficient to repay the bank’s outstanding debt in its entirety without liquidating its assets.

The above strengths are counteracted by several potential credit challenges that stem primarily from its lending activity. As a result of its development mandate and global scope, the bank lends to riskier sovereigns, some of which have no or very limited access to capital markets. As such, the bank could, albeit with low probability, experience significant spike in non-performing loans should there be simultaneous financial crises in several large borrowers or a regional crisis in one of the largest borrowing regions. Additionally, although the preferred creditor status does enhance asset quality, the IBRD still experiences arrears on debt service from its borrowers. However, these amounts have not exceeded 1% since 2007 and are amply covered by loan loss provisions.

The outlook on the bank’s rating remains stable. The institution’s strong capital base should allow it to withstand crises in developing countries without impairing its ability to service its obligations. The rating could face downward pressure if several of the IBRD's largest borrowers end up in default and are unwilling or unable to meet their obligations to the bank.

The IBRD is one part of the larger World Bank Group, which also includes the International Development Association, the group’s soft-loan window; the International Finance Corporation (IFC), a vehicle for lending to or investing in private companies in emerging markets without the benefit of host country government guarantees; the Multilateral Investment Guarantee Agency, which insures certain investments against political risks in emerging markets; and the International Centre for Settlement of Investment Disputes.

The IBRD and IFC are currently the only global multilateral development banks (MDB). With 188 members, all of which are sovereigns, the IBRD’s member base is the largest in the MDB universe. While the IBRD does not lend to all of its members, it does have a significantly larger number of borrowing members than do other MDBs. As of 30 June 2014, there were 75 members with outstanding IBRD loans.

The IBRD was established in 1945 to help Europe rebuild after World War II. Today, its main goal is to promote sustainable economic development and reduce poverty in developing member countries. It does so by providing loans and guarantees and serving as a catalyst for additional external financial flows to those countries through co-financing arrangements. The bank finances both investment projects and development policy programs in support of policy reforms alongside borrowing governments, official aid agencies, and private financial institutions. The IBRD lends exclusively to member countries that meet eligibility requirements, or to borrowers in those jurisdictions under the guarantee of the member states. The bank does not aim to maximize profits, although it earns a significant net income.

Capital Increase Affects Voting Power and Supports Growth in Lending Operations

In March 2011, the Board of Governors approved a capital increase, which supported the IBRD’s intrinsic financial strength in light of the bank’s elevated level of lending after the global crisis. The capital increase also positioned the bank to be able to respond to any further global economic or financial turmoil. The bank’s large size (it is the second largest MDB, by assets, after the European Investment Bank) also enables it to fulfill its members’ request to serve as a counter-cyclical lender during recessions or periods of financial instability.

The capital increase includes a general component as well as a selective component that together boosted the bank’s total subscribed capital by $87 billion. The general component amounts to $58.4 billion, including $3.5 billion of paid-in capital. The selective component amounted to $28.7 billion, including $1.6 billion in paid-in capital. This component serves the goal of increasing the voice and participation of developing and transition countries by 4.6% from the FY 2008 level. These countries now have a total voting power of 44%. Begun in 2008, the Voice Reform has the long-term goal of achieving equitable voting power between developed and developing member countries.

Developments in the shareholdings of the United States and China illustrate the impact of the selective capital increase. Between FY-end 2011 and FY-end 2014, the US shareholding fell from 16.0% to 15.0%; at the same time, China’s shareholding increased from 2.7% to 5.3% . During this period, China moved up from being the sixth largest shareholder to the third largest. Although the US shareholding has dropped, the country retains its status as the largest shareholder and the only one with veto power.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action information and rating history.

Our determination of a supranational’s rating is based on three rating factors: Capital Adequacy, Liquidity and Strength of Member Support. For Multilateral Development Banks, the first two factors combine to form the assessment of Intrinsic Financial Strength, which provides a preliminary rating range. The Strength of Member Support can provide uplift to the preliminary rating range. For more information please see our Supranational Rating Methodology.

Capital Adequacy: Very High

Risk Management Mitigates Challenges Arising from Mandate

Factor 1

Scale Very High High Medium Low Very Low

+ -

Capital adequacy assesses the solvency of an institution. The capital adequacy assessment considers the availability of capital to cover assets in light of their inherent credit risks, the degree to which the institution is leveraged and the risk that these assets could result in capital losses.

The steady expansion of IBRD’s capital resources over the years, combined with strict lending limitations, means that the bank has sufficient capital to cope with its business risk. The bank views its capital adequacy as the ability of its equity to generate future net income to support normal loan growth and respond to a potential crisis without having to resort to a call on capital.

As of FY-end 2014, total subscriptions received from the capital increase amounted to $42.6 billion with the paid-in portion amounting to $2.5 billion, of which $0.6 billion was paid in during FY 2014. The remaining amounts should arrive by 30 June 2016, the end of the five-year capital increase period.

There are various safeguards used to protect capital adequacy. The statutory lending limit is defined in the IBRD charter and stipulates that the total amount outstanding of disbursed loans, participations in loans, and callable guarantees may not exceed the total value of subscribed capital (which includes callable capital), reserves, and surplus. The bank’s total exposure to borrowing countries was well below the limit at 59% as of June 30, 2014, up from 57% recorded at end of the preceding financial year.

We assess an MDB’s capital position using a narrower definition of capital. Our asset coverage ratio dimensions usable equity against total loans outstanding and risk-weighted liquid assets, where usable equity excludes callable capital. For the bank, this ratio steadily trended downward from 42.0% in 2008 to 26.9% in 2012. However, as a result of the capital increase, the ratio increased slightly to 27.5% by FY-end 2013. The downward trend resumed in FY 2014 as the ratio inched down to 25.3%. Despite the deterioration, these levels continually qualified as ‘High’ in our analysis, which we expect to remain so in the medium term.

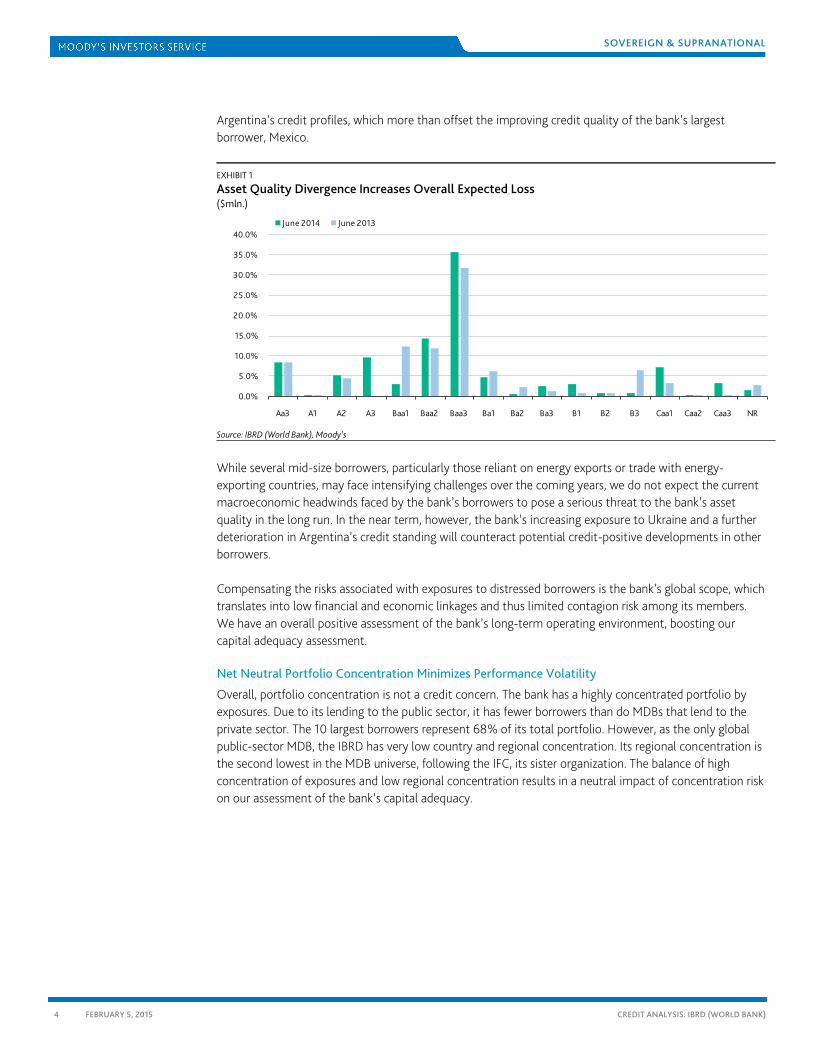

Geopolitical and Country-Specific Risks Weaken Overall Asset Quality

In addition to gradually the declining asset coverage ratio, the bank’s capital adequacy has recently come under some pressure from the asset quality front. The creditworthiness of many of the bank’s largest borrowers improved between 2008 and 2013, with the weighted average borrower rating of the total portfolio rising to Ba1 from Ba2. The trend reversed in 2014, reflecting deterioration in Ukraine and

Argentina’s credit profiles, which more than offset the improving credit quality of the bank’s largest borrower, Mexico.

EXHIBIT 1

Asset Quality Divergence Increases Overall Expected Loss ($mln.)

Source: IBRD (World Bank), Moody’s

While several mid-size borrowers, particularly those reliant on energy exports or trade with energy-exporting countries, may face intensifying challenges over the coming years, we do not expect the current macroeconomic headwinds faced by the bank’s borrowers to pose a serious threat to the bank’s asset quality in the long run. In the near term, however, the bank’s increasing exposure to Ukraine and a further deterioration in Argentina’s credit standing will counteract potential credit-positive developments in other borrowers.

Compensating the risks associated with exposures to distressed borrowers is the bank’s global scope, which translates into low financial and economic linkages and thus limited contagion risk among its members. We have an overall positive assessment of the bank’s long-term operating environment, boosting our capital adequacy assessment.

Net Neutral Portfolio Concentration Minimizes Performance Volatility

Overall, portfolio concentration is not a credit concern. The bank has a highly concentrated portfolio by exposures. Due to its lending to the public sector, it has fewer borrowers than do MDBs that lend to the private sector. The 10 largest borrowers represent 68% of its total portfolio. However, as the only global public-sector MDB, the IBRD has very low country and regional concentration. Its regional concentration is the second lowest in the MDB universe, following the IFC, its sister organization. The balance of high concentration of exposures and low regional concentration results in a neutral impact of concentration risk on our assessment of the bank’s capital adequacy.

[1] Weighted average borrower rating is calculated using probability of default rates associated with our foreign currency government bond ratings as of 30 June 2014.

Source: IBRD, Moody’s

Regarding exposure concentration risk, the IBRD limits its exposure (both development-related lending and treasury investments) to individual borrowers based on its risk-bearing capacity. In FY2014 the single-borrower exposure limit was increased to $20.0 billion for India and $19.0 billion for the other large borrowing countries deemed to be the most creditworthy by the IBRD (China, Indonesia, Brazil, and Mexico). In India’s case, a 50 basis-point surcharge is applied to loans in excess of $17.5 billion, while for the other four the surcharge threshold is set at $16.5 billion. Also, there is an equitable access limit of 10% of IBRD’s subscribed capital, reserves and unallocated surplus, which currently amounts to $26 billion. The overall country limit for the largest and most creditworthy borrowing countries is the lower of the single-borrower limit and the equitable access limit. The IBRD can continue to lend to a country that has reached its limit, provided arrangements are made so that the bank’s net exposure to it will not increase. As of 30 June 2014, China was the only country with which the bank had such an arrangement, and since it was below the limit the arrangement was not activated.

Leverage Influenced by Demand for IBRD Loans

The bank’s leverage has increased substantially in recent years, although the increase was interrupted in FY2011 and FY2013. Leverage ratios resumed their upward trajectory after inching down in FY2013. From 360.3% in FY2013 the ratio of gross debt to usable equity rose to 413.0% in FY2014, a historic high for the organization, The bank’s releveraging followed the Executive Directors’ decision to lower the minimum equity-to-loans ratio from 23% to 20% (as of FY-end 2014 the ratio stood at 25.7%).

The high level in FY2014 was driven by both numerator and denominator effects. Despite the capital increase’s positive impact on paid-in capital, usable equity fell by 1.4% due to unrealized losses detracting from total retained earnings. Excluding the impact of unrealized non-trading losses, the leverage ratio increased to 402.4%, with the remainder of the 62.7 percentage-point gain reflecting higher borrowing

SOVEREIGN & SUPRANATIONAL

6 FEBRUARY 5, 2015

CREDIT ANALYSIS: IBRD (WORLD BANK)

volumes. The bank raised $51 billion in medium- and long-term debt, up from $28 billion a year before, resulting in total outstanding borrowings expanding by $19 billion to $161 billion.

IBRD’s borrowing needs have been increasing in proportion to rising demand for loans and improving credit quality of its largest borrowers. In the run-up to the global crisis, IBRD’s borrowing needs decreased because it was experiencing negative net loan disbursements, meaning annual loan repayments from borrowers exceeded loan disbursements to borrowers. Since that trough, the bank has been reporting consistently positive net disbursements.

Problem Loans Remain Very Small

The bank’s assets continue to perform very well with only one country in nonaccrual status as of FY-end 2013, Zimbabwe. During the first half of FY 2014, the bank placed all loans outstanding from Iran, a total of $697 million in gross terms, on nonaccrual status, but the situation was resolved within three months and all overdue amounts were cleared.

The bank does not reschedule its loans. It has never written off a loan and continues to seek recovery on all arrears. Zimbabwe has been in nonaccrual status since FY 2001. As of FY-end 2014, the principal in nonaccrual status amounted to approximately $462 million, or 0.3% of total gross loans outstanding, and was amply covered by accumulated loan loss provisions of $1,626 million or 1.1% of gross loans. While the bank places its loans on non-performing status when a country is overdue on its payments by more than six months, the figures do not change if a 90-day period is used.

Problem loans have steadily decreased since FY 2005 when the ratio of non-performing loans (NPLs) to total loans outstanding reached 3.4%. This is notable given the bank’s counter-cyclical lending during the global crisis. IBRD has historically experienced higher NPL levels than have other Aaa-rated MDBs, such as the Asian Development Bank, European Investment Bank, Inter-American Development Bank and Nordic Investment Bank, all of which have long-term histories of zero or near-zero NPL ratios. However, the IBRD’s asset quality does benefit from preferred creditor status, in which members, who are also the borrowers, pledge to prioritize debt service to the IBRD over debt service to market and official bilateral creditors.

Despite its preferred creditor status, the IBRD has had periods of higher NPLs because its geographically broad lending scope and development mandate result in lending to financially weak sovereigns who only have access to multilateral debt. Therefore, when those borrowers run into problems, there are no market creditors to subordinate to the IBRD, only bilateral creditors. Given the bank’s lending distribution, with close to 13% of loans outstanding to sovereigns rated B3 or lower, or not rated, its NPL level would likely be much higher without the benefit of preferred creditor status.

SOVEREIGN & SUPRANATIONAL

7 FEBRUARY 5, 2015

CREDIT ANALYSIS: IBRD (WORLD BANK)

Liquidity: Very High

Strong Debt Service Coverage and Very Strong Market Access

Factor 2

Scale Very High High Medium Low Very Low

+ -

A financial institution’s liquidity is important in determining its shock absorption capacity. We evaluate the extent to which liquid assets cover debt service requirements and the stability of the institution’s access to funding.

Stability of Strong Liquidity Position Ensured by Policy

The IBRD has a high liquidity position when measured by our debt service coverage ratio. This ratio dimensions the stock of short-term and currently maturing long-term debt against the stock of liquid assets.1 Exhibit 3A shows the evolution of the ratio since 2006. Despite annual fluctuations, the ratio consistently falls in the 60%-100% range.

EXHIBIT 3A

Debt Service Coverage Stability Within a Range… (ST + CMLTD, % of Liquid Assets)

ST=Short term; CMLTD=Currently maturing long-term debt Liquid assets used for the calculation displayed here are not discounted. Source: IBRD and Moody’s

EXHIBIT 3B

…Supported by Debt Composition (maturity of outstanding borrowings, % of total)

Source: IBRD

The IBRD’s liquidity management influences the debt service coverage ratio. The goal is to ensure cash flows are available to meet all of the bank’s financial commitments. The liquidity policy stipulates that liquid assets must equal at least the highest consecutive six months of anticipated debt service plus one-half of the anticipated net loan disbursements over the relevant fiscal year, if positive. As such, it is possible for the debt service coverage ratio to exceed 100%, although that has not occurred in recent years. As a result of the policy, we expect the bank’s debt service coverage ratio will remain within the high assessment.

1 In our analysis, we discount liquid asset investments according to our expected loss rates at five years. However, for the entire sector, we publish the ratio without

the discounting applied.

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2006 2007 2008 2009 2010 2011 2012 2013 2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014

1 Year or Less 1-5 Years Over 5 Years

SOVEREIGN & SUPRANATIONAL

8 FEBRUARY 5, 2015

CREDIT ANALYSIS: IBRD (WORLD BANK)

Both the maturity profile of the bank’s borrowings and the historical precedence of over-compliance with its liquidity policy support our assessment of expected stability in the bank’s liquidity position. Exhibit 3B shows the evolution of the remaining time to maturity of the bank’s debt. Despite annual fluctuations, the ‘one year or less’ time bucket generally remains the smallest, averaging around 23% of the total debt portfolio. The recent shrinking of the ‘more than five years’ category occurred in response to increased market preference for medium-term notes.

The bank’s actual liquidity has tended to be comfortably above the minimum set by the policy and is conservatively managed to protect the principal amount of the investments while generating a reasonable return. For FY 2014, the prudential minimum was set at $24.5 billion. The threshold has been increased to $26 billion in FY 2015. IBRD’s policies also establish a soft upper limit on the size of its liquid portfolio, which generally should not exceed 150% of the policy minimum. As of FY-end 2014, however, the upper limit was intentionally breached, with the liquid portfolio amounting to 170% of the prudential minimum.

The aim of IBRD’s asset/liability management framework is to provide adequate funding for each loan and liquid asset at the lowest available cost and to manage the portfolio of liabilities supporting each loan and liquid asset within the prescribed risk guidelines. To that end, the bank uses derivatives to manage its exposure to interest and currency risks, manage repricing between loans and borrowings, extend the duration of equity, and assist borrowing member countries in managing their interest and currency risks. It does not enter into derivatives for speculative purposes. As mandated by its articles, the bank matches borrowings in any one currency with assets in the same currency.

Strong Brand Underpins Exceptional Market Access

The IBRD scores very high in our assessment of funding, or market access. It fulfills its borrowing needs via bond issuance in the international capital markets. Given its very long and solid track record of market debt issuance, brand recognition as a premier MDB, and global presence, the bank has unquestionable market access. Over the past few years, the strength of its market access was tested and proven. Developed nations were hit hard by the global crisis and several of the bank’s largest members experienced a deterioration of creditworthiness as evidenced by either downward movement or downward pressure2 on their bond ratings. Nevertheless, the IBRD did not experience market dislocation and actually benefitted from the market’s risk aversion to sovereign and affiliated debt as investors sought out its bonds as a safe investment during the sovereign turmoil. We expect the bank’s market access to remain very strong over the medium term.

The IBRD has a sizeable annual borrowing program and regularly issues benchmark bonds. Its FY 2014 funding program totaled $51 billion, well above its original $30.0 billion target. The target for FY 2015 has been set at $45 billion. During FY 2014, the bank issued bonds in 22 different currencies in a total of 300 transactions, including benchmark bonds in US, Canadian, Australian and New Zealand dollars. Netted against borrowing related derivatives, the IBRD’s weighted average cost of borrowing declined to 0.2% on June 30, 2014 from 0.3% a year before. The IBRD’s spreads have performed well in the market context and fluctuations have been more a result of general market conditions rather than reaction to IBRD-specific factors.

2 Downward pressure is indicated by negative outlooks or ratings being placed on review for downgrade.

SOVEREIGN & SUPRANATIONAL

9 FEBRUARY 5, 2015

CREDIT ANALYSIS: IBRD (WORLD BANK)

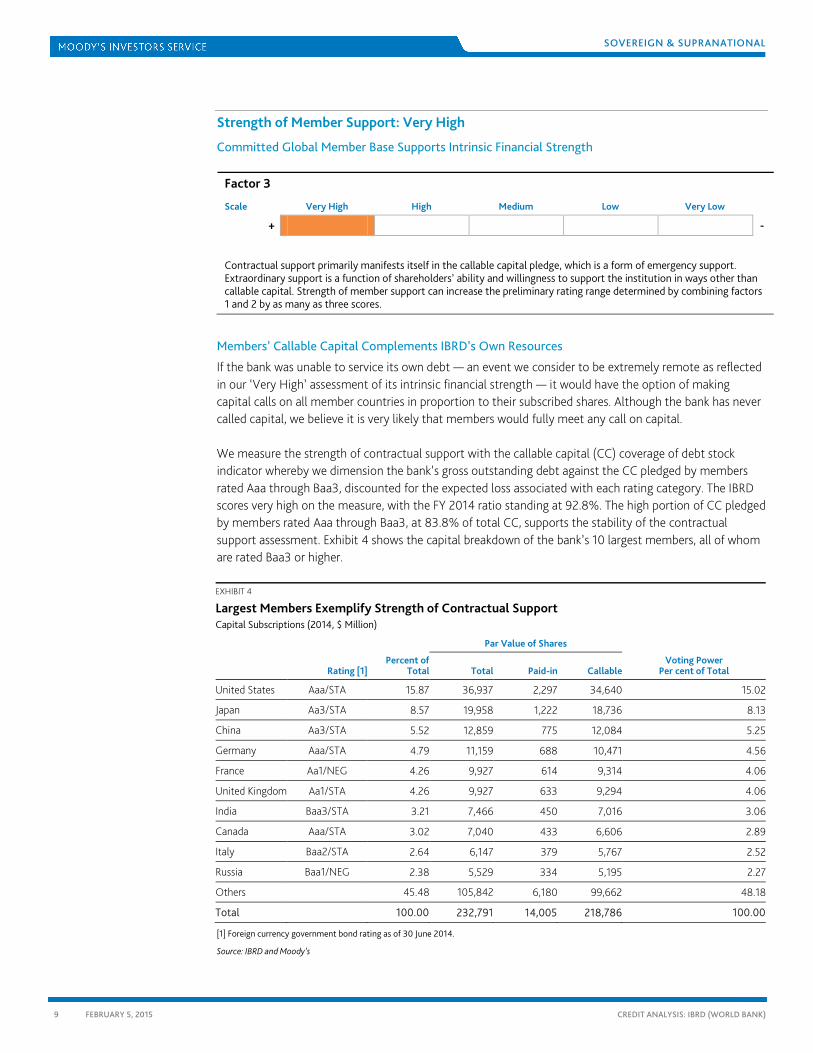

Strength of Member Support: Very High

Committed Global Member Base Supports Intrinsic Financial Strength

Factor 3

Scale Very High High Medium Low Very Low

+ -

Contractual support primarily manifests itself in the callable capital pledge, which is a form of emergency support. Extraordinary support is a function of shareholders’ ability and willingness to support the institution in ways other than callable capital. Strength of member support can increase the preliminary rating range determined by combining factors 1 and 2 by as many as three scores.

Members’ Callable Capital Complements IBRD’s Own Resources

If the bank was unable to service its own debt — an event we consider to be extremely remote as reflected in our ‘Very High’ assessment of its intrinsic financial strength — it would have the option of making capital calls on all member countries in proportion to their subscribed shares. Although the bank has never called capital, we believe it is very likely that members would fully meet any call on capital.

We measure the strength of contractual support with the callable capital (CC) coverage of debt stock indicator whereby we dimension the bank’s gross outstanding debt against the CC pledged by members rated Aaa through Baa3, discounted for the expected loss associated with each rating category. The IBRD scores very high on the measure, with the FY 2014 ratio standing at 92.8%. The high portion of CC pledged by members rated Aaa through Baa3, at 83.8% of total CC, supports the stability of the contractual support assessment. Exhibit 4 shows the capital breakdown of the bank’s 10 largest members, all of whom are rated Baa3 or higher.

EXHIBIT 4

Largest Members Exemplify Strength of Contractual Support Capital Subscriptions (2014, $ Million)

Par Value of Shares

Rating [1] Percent of

Total Total Paid-in Callable Voting Power

Per cent of Total

United States Aaa/STA 15.87 36,937 2,297 34,640 15.02

Japan Aa3/STA 8.57 19,958 1,222 18,736 8.13

China Aa3/STA 5.52 12,859 775 12,084 5.25

Germany Aaa/STA 4.79 11,159 688 10,471 4.56

France Aa1/NEG 4.26 9,927 614 9,314 4.06

United Kingdom Aa1/STA 4.26 9,927 633 9,294 4.06

India Baa3/STA 3.21 7,466 450 7,016 3.06

Canada Aaa/STA 3.02 7,040 433 6,606 2.89

Italy Baa2/STA 2.64 6,147 379 5,767 2.52

Russia Baa1/NEG 2.38 5,529 334 5,195 2.27

Others 45.48 105,842 6,180 99,662 48.18

Total 100.00 232,791 14,005 218,786 100.00

[1] Foreign currency government bond rating as of 30 June 2014.

Source: IBRD and Moody’s

SOVEREIGN & SUPRANATIONAL

10 FEBRUARY 5, 2015

CREDIT ANALYSIS: IBRD (WORLD BANK)

The United States has in place legislation (including the Bretton Woods Agreements Act) that allows the Secretary of Treasury to pay up to $7.7 billion of the $34.6 billion in CC pledged to the IBRD without any further congressional action.

CC is an unconditional and full faith obligation of each member country, the fulfillment of which is independent of the action of other shareholders. Should one or more of the member countries fail to meet this obligation, successive calls on the other members would be made until the full amounts needed were obtained. However, no country would be required to pay more than its total callable subscription. Based on this, we do not consider the IBRD to have support pledged on a joint-and-several basis.

Members’ Willingness Complements Strong Ability to Provide Extraordinary Support

We assess members’ extraordinary support of the IBRD to be very high. As Exhibit 4 shows, the creditworthiness of the bank’s largest members is very high. Overall, the weighted median shareholder rating of its 188 members was Aa3 at the end of FY 2014. This figure, while remaining strong, has trended downward over the past seven years, from Aaa in 2008. We expect stability in this indicator as the European sovereign debt crisis eases; we also believe a stronger European recovery could cause extraordinary support to improve mildly.

Members’ willingness to provide extraordinary support to the bank is very strong. The bank’s origins in the Bretton Woods Agreements, its status as the archetypal MDB, and its global member and lending base indicate very high political linkages and thus reputational risk should its members not support it during financial duress. Furthermore, the recent capital increase indicates that members remain supportive of the bank’s mandate and its ability to fulfill that mandate. All of these attributes also indicate that even when resources are scarce, members will likely prioritize supporting the IBRD over other MDBs that may require support at the same time.

Global Status and Separation of Credit Risk from Support Ensures Materialization of Support

Favorable characteristics of the bank’s member base support our ‘Very High’ assessment of the strength of member support. In view of the largest shareholders shown in Exhibit 4 and the fact that the IBRD has a global member base consisting of 188 sovereigns, the concentration of members as well as the financial and economic linkages among members are low. Regional MDBs with smaller member bases and narrower geographic mandates tend to have higher concentration of capital. As a global MDB, with good geographic distribution of members, the IBRD does not face the risk that regional crises will affect a large number of members due to contagion via financial and economic linkages.

Another favorable characteristic is that the bank has borrowing and non-borrowing members. Only three of the members in Exhibit 4 – China, India, and Russia – are borrowers; the rest have never borrowed or no longer borrow from the bank. In addition, there are other members not displayed who are highly rated non-borrowers. The largest risk the bank faces is credit risk from its lending activity. Therefore, the benefit of this separation of borrowing and non-borrowing members is that there is a high number of large shareholding members who will be called upon to provide financial assistance that are not the same ones that caused the financial stress in the first place.

SOVEREIGN & SUPRANATIONAL

11 FEBRUARY 5, 2015

CREDIT ANALYSIS: IBRD (WORLD BANK)

Rating Range

Combining the scores for individual factors provides an indicative rating range. While the information used to determine the grid mapping is mainly historical, our ratings incorporate expectations around future metrics and risk developments that may differ from the ones implied by the rating range. Thus, the rating process is deliberative and not mechanical, meaning that it depends on peer comparisons and should leave room for exceptional risk factors to be taken into account that may result in an assigned rating outside the indicative rating range. For more information please see our Supranational Rating Methodology.

Supranational Rating Metrics: IBRD (World Bank)

Capital Adequacy How strong is the capital buffer?

Intrinsic Financial Strength

Sub-Factors: Capital Position, Leverage, Asset Performance

Very High High Medium Low Very Low

+ -

Liquidity How strong is the institutions’ shock absorption capacity?

Very High High Medium Low Very Low

+ -

Sub-Factors: Position, Funding

Very High High Medium Low Very Low

+ -

Strength of Member Support

How strong is members’ support of the institution?

Sub-Factors: Contractual Support, Extraordinary Support

This section compares credit relevant information regarding IBRD (World Bank) with other supranationals rated by Moody’s Investors Service. It focuses on a comparison with supranationals within the same rating range and shows selected credit metrics and factor scores.

Second largest institution in our rated universe, IBRD ranks towards the upper end of its peer group in terms of asset base. Meanwhile, the bank’s capital adequacy, liquidity and member support indicators are in line with its comparables, consistent with its ‘Very High’ assessment across the three rating factors.

Notes: [1] Usable equity is total shareholder's equity and excludes callable capital [2] Non-performing loans [3] Short-term debt and currently-maturing long-term debt [4] Callable capital pledged by members rated Baa3 or higher, discounted by Moody's 30-year expected loss rates associated with ratings Source: Moody’s, IBRD (World Bank)

SOVEREIGN & SUPRANATIONAL

16 FEBRUARY 5, 2015

CREDIT ANALYSIS: IBRD (WORLD BANK)

Moody’s Related Research

Credit Opinion:

» IBRD (World Bank)

Rating Methodologies:

» Multilateral Development Banks and Other Supranational Entities, December 2013 (161372)

» Sovereign Bond Ratings, September 2013 (157547)

Moody’s Website Links:

» Sovereign Risk Group Webpage

» Supranational Ratings List

To access any of these reports, click on the entry above. Note that these references are current as of the date of publication of this report and that more recent reports may be available. All research may not be available to all clients.

Related Websites

For additional information, please see:

» The IBRD (World Bank) website: www.worldbank.ord

MOODY’S has provided links or references to third party World Wide Websites or URLs ("Links or References") solely for your convenience in locating related information and services. The websites reached through these Links or References have not necessarily been reviewed by MOODY’S, and are maintained by a third party over which MOODY’S exercises no control. Accordingly, MOODY’S expressly disclaims any responsibility or liability for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on any third party web site accessed via a Link or Reference. Moreover, a Link or Reference does not imply an endorsement of any third party, any website, or the products or services provided by any third party.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATING AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY’S (“MOODY’S PUBLICATIONS”) MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS FOR RETAIL INVESTORS TO CONSIDER MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS IN MAKING ANY INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc., have, prior to assignment of any rating, agreed to pay to Moody’s Investors Service, Inc., for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

For Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail clients. It would be dangerous for “retail clients” to make any investment decision based on MOODY’S credit rating. If in doubt you should contact your financial or other professional adviser.

For Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it fees ranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.