54

Credit Cards and Financial Health Member-Exclusive Report from CFSI’s Consumer Financial Health Study

Credit Cards and Financial Health Member-Exclusive Report from CFSI’s Consumer Financial Health Study

2

We provide this CFSI Member Exclusive as a resource to create new products, calibrate existing ones, and communicate the benefits of their use to improve consumers’ financial health. The information is designed for use by product managers, segment managers, marketing managers, and community development/affairs managers to better understand consumers’ needs.

The data and visuals in this presentation are easy to use to inform ideation and business strategies that support consumer financial health. We encourage you to share this asset widely within your organization, and to use the data and visuals in external presentations and communications. When you use an excerpt of this report, please cite CFSI as the source: “Credit Cards and Financial Health: Member Exclusive Report from CFSI’s Consumer Financial Health Study” CFSI, February 2016.

Per your CFSI Network membership agreement, we ask that you refrain from distributing this report in its entirety outside your organization. If you have any questions about this, please contact your CFSI relationship manager.

Table of Contents

3

Key Findings………………………………………………………………………………………...…4

Addressing Customer Needs with Credit Cards…………………………………………..10

Financial Health Recap…………………………………………………………………….………..14

KF1: Nearly half of credit card holders are struggling financially……………..…………...…..21

KF2: A portion of credit card holders struggle with daily finances and resilience……………..30

KF3: Former credit card holders struggle with debt and poor credit scores………………..40

Credit Card Holder Demographics…………….………….…………………..…….……47

Company Logo

Key Findings

1. Credit card holders have higher incomes and more manageable debt levels than non card holders, but nearly half are struggling financially.

2. Credit cards can help consumers weather shocks and balance borrowing and saving.

3. Many former credit card holders struggle with high rates of non-mortgage debt and poor credit scores.

On average, credit card holders have higher incomes and more sustainable debt levels than non-holders

5

75% of American adults have a credit card

More than half of credit card holders have annual incomes in the top two income quartiles, compared with just a quarter of non credit card holders.

Just over a quarter (27%) of credit card holders have a non-mortgage debt-to-income ratio of 40% or more, compared with 37% of non credit card holders.

Still, nearly half of credit card holders are struggling financially

6

182 million Americans have credit cards, and 87 million are struggling financially.

For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America

While many credit hard holders thrive, others struggle

7Formoredetail,refertoslides:21-29

Credit cards can help consumers weather shocks and balance borrowing and saving

8

15% of credit card holders would first turn to their card to cover a $600 emergency expense and pay it off over time. 19% of non-holders do not know where they would turn to cover a $600 expense.

While card holders split about evenly between those who do and do not carry a balance, 39% sometimes leave a balance instead of using savings to pay it off.These customers report a higher frequency of unexpected expenses than their peers who do not report this behavior.

Research – including the USFD – shows that low- to moderate-income consumers need, but often struggle to accumulate, large lump sums. Accumulating lump sums through small contributions over time is a core aim of financial services, formal and informal. This can be accomplished by either saving money gradually or borrowing a lump sum and then paying it off bit by bit.

Categorizing a financial vehicle as “credit” or “savings” is less important than its ability to aid in accumulating a lump sum for when it is needed.

US Financial Diaries Issue Brief, “How Households Use Financial Tools of Their Own Making”, Morduch & Schneider, August 2014

Formoredetail,refertoslides:30-39

Credit card providers have an opportunity to enhance products with features that support cash flow management, planning ahead, responsible use of credit, and building resilience—key aspects of financial health.

Many former card holders struggle with high rates of non-mortgage debt and poor credit scores

9

Former credit card holders acknowledge having difficulty managing their cards.

These financial challenges are reflected in their levels of debt and credit quality. More than 4 in 10 former card holders report a non-mortgage debt-to-income ratio over 40%, and the same proportion report having poor or very poor credit scores.

Formoredetail,refertoslides:40-46

Credit card providers can leverage robust monitoring and predictive analytics to help customers identify risky behaviors and trends early, so they can adopt strategies to prevent larger financial challenges later.

Company Logo

What could your financial institution do to help credit card holders improve their financial health?

Value-Added Tools and Services

11

While credit cards can be an important tool for financial management, those who carry a balance are less likely to be financially healthy.

Card holders who carry a balance also budget more than those who do not carry a balance. However, they do not plan for large, irregular expenses – a key characteristic of financial health – with the same frequency. Many say they would plan ahead if they could, perhaps indicating that they do not have the tools or capabilities to plan.

How could you provide tools to help customers plan for large irregular expenses and/or adopt and maintain other financially healthy habits?

Benefits include deepening your customer relationships, helping them better manage their financial lives, and contributing to the longevityand long-term profitability of these relationships.

12

Guidance and Prevention

Consumers who have not owned a credit card before are a source of new business for card providers. However, these customers may not fully understand how to responsibly use the product or the ramifications of misuse.

Those who have never had a credit card are the most likely to say they do not know their credit quality or did not know they had a credit score. Young Americans, age 18-25, are most likely to have never had a credit card.

Could you provide new card owners with guidance and tools – alerts, guardrails, or other features – enabling positive credit behavior for your customers and long-term customer relationships for your organization?

13

Credit Repair and Rebuilding

Many former credit card customers had difficulty managing the product and struggle with indebtedness and poor credit scores.

Former credit card holders are four times more likely to have used a payday loan in the last year vs. current card holders and they are more likely to have unhealthy non-mortgage debt-to-income ratios and poor credit quality.

Could your organization provide former and at-risk card holders debt repayment plans and tools to rebuild their credit so they can regain access to high-quality, low-cost credit?

Company Logo

Financial Health Recap

Recap: Financial Health

15

Day-to-DayManagement

Resilience Opportunity

Financial health comes about when your daily systems help you build resilience and pursue opportunities.

Are you prepared for the unexpected?

Are you able to pursue your financial aspirations?

Do your financial products support resilience and opportunity?

For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America. For more on the four financially struggling segments, download the segment briefs.

The Consumer Financial Health Study includes a segmentation analysis that groups individuals based upon patterns of responses to a range of survey questions corresponding with subjective and objective indicators of financial health.

The seven consumer segments derived from the segmentation analysis were grouped into three tiers: Healthy, Coping and Vulnerable, with the four Coping and Vulnerable segments sometimes referred to in aggregate as the segments comprised of consumers who are “struggling” financially.

Though income significantly influences financial health, consumer behaviors— particularly those related to planning ahead and saving—also have a significant impact on consumers’ financial health segment.

16

Recap: Financial Health Segmentation

Recap: Financial Health Segmentation

17

138 million American adults struggle financially.

For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America

Recap: Financially Healthy Segments

18

Financially Healthy Segments tend to do well across all indicators of financial health. Individuals in these segments are able to manage their day-to-day financial lives; they have a significant financial cushion in case of an emergency; and they are better positioned to seize financial opportunities. They demonstrate the highest rates of checking account, savings account, and credit card ownership of all segments.

For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America

Recap: Financially Coping Segments

19

Financially Coping segments generally exhibit more moderate behaviors and attitudes across the financial health indicators, compared with their Financially Healthy counterparts. These individuals are more likely to struggle in managing their day-to-day financial lives, have less financial cushion for an emergency, and be less well positioned to take advantage of financial opportunities. Individuals in these segments tend to use a variety of financial products and services—traditional, nonbank, and new technology-enabled—to manage their financial lives.

For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America

Recap: Financially Vulnerable Segments

20

The two Financially Vulnerable segments are doing the least well across financial health indicators. These individuals are more likely to be struggling with their day-to-day financial lives; they have little or no financial cushion in case of an emergency; and they are not prepared to seize financial opportunities for security and mobility. They are the least likely of all segments to own a credit card and the most likely to be unbanked.

For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America

Company Logo

A closer look at the data…

Key Finding 1: Credit card holders have higher incomes and more manageable debt levels than non-holders, but nearly half struggle financially.

Financially Struggling

22

Nearly half of credit card holders struggle financially.

Learn more about the financially struggling segments here.

For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America

Financial Stress

23

Nearly 60% of consumers without a card are in a financially vulnerable segment.

58% of them have never owned a credit card.

For more on the financial health segmentation, download the whitepaper: bit.ly/ConsumerFinHealth

Learn more about the financially struggling segments here.

For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America

Financial Stress

24

Almost a quarter of card holders say their finances are a cause of significant stress.

Another 30% neither agree nor disagree with that statement.

Finances Cause Me Significant Stress

Respondents were asked: On a scale of 1 to 5, where 1 is strongly disagree, 3 is neither agree nor disagree, and 5 is strongly agree, how much do you agree or disagree with the following statement: My finances cause me significant stress.

Credit Card Fees and Financial Stress

25

11% of card holders say they were occasionally charged a late fee in the last year due to forgetting to pay.

7% say they were charged a late fee in some months because they did not have the money to pay on time.

4% say they paid an over-the-limit fee for exceeding the credit line.

Of these three groups, those who occasionally forget to pay their credit card bill are the least financially stressed (30%).

Chart shows: The degree to which credit card owners who were charged a fee for the reasons listed agreed with the statement, “My finances cause me significant stress.”

Financial Confidence: Short-Term Goals

26

More than 4 in 10 card holders lack confidence about achieving short-term savings goals.

Respondents were asked: On a scale of 1 to 5, where 1 is strongly disagree, 3 is neither agree nor disagree, and 5 is strongly agree, how much do you agree or disagree with the following statement: I am confident that I can meet my short-term saving goals.

Financial Confidence: Long-Term Goals

27

Half of credit card holders lack confidence about meeting long-term goals for becoming financially secure.

Respondents were asked: On a scale of 1 to 5, where 1 is strongly disagree, 3 is neither agree nor disagree, and 5 is strongly agree, how much do you agree or disagree with the following statement: I am confident that I can meet my long-term goals for becoming financially secure.

Living Paycheck to Paycheck

28

More than a quarter of credit card holders report always living paycheck to paycheck.

Another 24% neither agree nor disagree with that statement.

Respondents were asked: On a scale of 1 to 5, where 1 is strongly disagree, 3 is neither agree nor disagree, and 5 is strongly agree, how much do you agree or disagree with the following statement: I always find myself living paycheck to paycheck.

Cash Flow

29

Almost one-third (31%) of credit card holders sometimes run out of money before the end of the month.

Company Logo

A closer look at the data…

Key Finding 2: Credit cards can help consumers weather shocks and balance borrowing and saving.

Credit Card Payments

31

Financial Health of Balance-Carriers vs. Non-Carriers

32

Credit card customers who carry a balance are less likely to be financially healthy, compared with those who do not.

Balance-carriers were also slightly more likely to have had a health emergency, used savings for bills, or lost a job in the last five years.3% indicated that they both pay in full and carried a balance; they may have more than one card or simply were not paying close attention. For simplicity, we removed these respondents.

Respondents were asked: During the past 5 years, has your household experienced any of the following significant majorlife changes or financial events?

Budgeting and Planning: Balance-Carriers vs Non-Carriers

333% indicated that they both pay in full and carried a balance; they may have more than one card or simply were not paying close attention. For simplicity, we removed these respondents.

While those who carry a balance are just as likely to use a budget as those who do not carry a balance, they feel less able to plan ahead for large, irregular expenses.

Credit Card Use: Convenience vs. Cushion

34

Respondents were asked: Thinking about the past 12 months, which of the following describes your experience with credit cards?

Those who do not carry a balance appear to use the card for convenience (and rewards); the vast majority (82%) would use savings or a credit card they pay off in full to cover a $600 emergency.

Those who carry a balance would be less likely to turn to savings. Instead, they would use their credit card to weather the shock and pay off the balance over time.

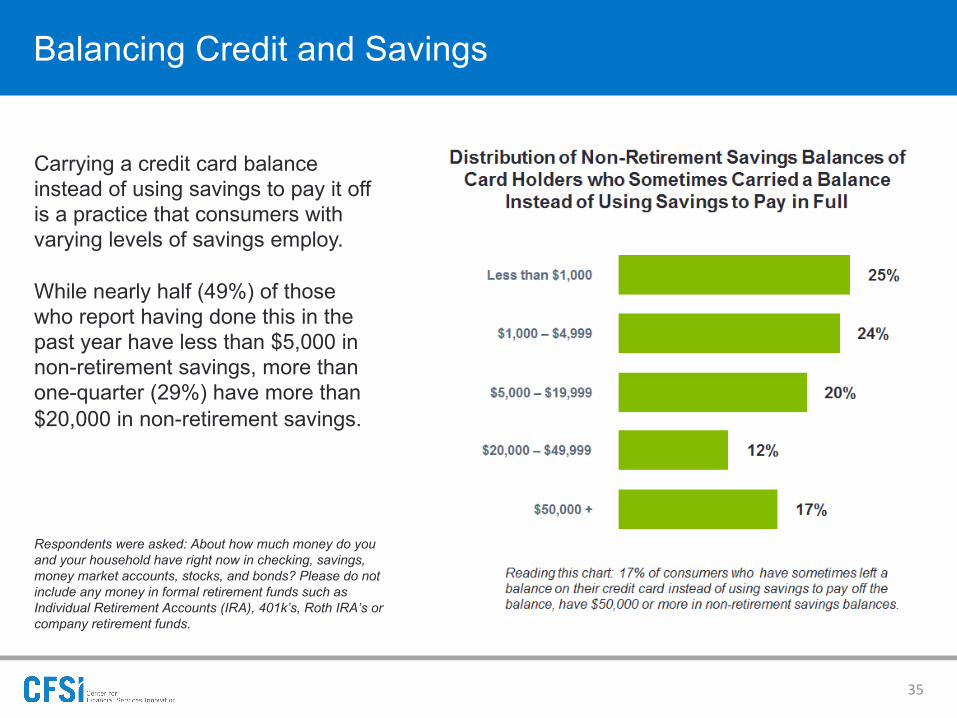

Balancing Credit and Savings

35

Carrying a credit card balance instead of using savings to pay it off is a practice that consumers with varying levels of savings employ.

While nearly half (49%) of those who report having done this in the past year have less than $5,000 in non-retirement savings, more than one-quarter (29%) have more than $20,000 in non-retirement savings.

Respondents were asked: About how much money do you and your household have right now in checking, savings, money market accounts, stocks, and bonds? Please do not include any money in formal retirement funds such as Individual Retirement Accounts (IRA), 401k’s, Roth IRA’s or company retirement funds.

Balancing Credit and Savings

36Respondents were asked: In the past 12 months, how often have you and your household had an unexpected expense crop up? & How long could your household make ends meet if you faced unemployment, a longer-term illness, job loss, economic downturn, or other emergency that caused a drop in income?

Consumers who carry a balance instead of using savings experience unexpected expenses more frequently and could weather a sudden income drop for less time than those who do not. This sheds light on why and how consumers balance credit and saving to manage their financial lives.

Non-Retirement Savings

37

Respondents were asked: About how much money do you and your household have right now in checking, savings, money market accounts, stocks, and bonds? Do not include money in formal retirement funds such as Individual Retirement Accounts (IRA), 401k’s, Roth IRA’s or company retirement funds.

Many factors contribute to ability to weather financial ups and downs: savings, access to low-cost credit, and help from family and friends.

Credit card holders have accrued significantly more non-retirement savings than non-card holders. More than 62% of card holders have savings balances greater than $5,000, compared with 25% of non-holders.

Coming Up With $600 in One Week

38

Respondents were asked: If you had one week to pay $600 for an emergency expense, such as a car repair or medical bill, where would you turn first to get the money? 3% of non-credit card holders said they would turn to a credit card, perhaps indicating that they might open an account or that they were simply were not paying close attention.

Consistent with card holders having higher incomes and non-retirement savings, more than 6 in 10 would use cash or a credit card they pay off in full to fund a $600 emergency.

However, 15% of credit card holders say they would use their credit card and pay off the expense over time.

19% of non-card holders do not know how they would cover the expense, and 13% say they could not meet it.

Coming Up With $2,000 in One Month

39Respondents were asked: How confident are you that you could come up with $2,000 if an unexpected need arose within the next month?

Card holders are most confident they could come up with $2,000 in one month for an emergency.

However, more than one-quarter of card holders are slightly or not at all confident.

Former card holders exhibit the least confidence, followed by those who have never owned a credit card.

Among never-holders, those who said they don’t need or want a card are slightly more confident.

Company Logo

A closer look at the data…

Key Finding 3: Many former card holders struggle with high rates of non-mortgage debt and poor credit scores.

Credit Card Ownership

41

Never Had A Credit Card

42

Respondents were asked: Is each of the following a reason or not a reason why you don’t have a credit card?

Consumers who have never had a credit card are most likely to cite not needing or wanting one.

More than one-third say they would qualify for a card, though more than 4 in 10 could not assess their credit quality.

11% indicated that they have excellent or good credit.

No Longer Have a Credit Card

43

Respondents were asked: Is each of the following a reason or not a reason why you no longer have a credit card?

Consumers who had a credit card in the past, but no longer do, are most likely to report having had difficulty managing the card.

Borrowing In the Last Year

44

Respondents were asked: In the past 12 months, have you and your household used any of the following to borrow money?

Card holders are less likely to borrow from members of their social networks. Non-holders are more likely to use payday and pawn loans.

Non-Mortgage Debt-to-Income Ratio

45

Non-mortgage debt-to-income ratio calculated by aggregating a household’s student loan debt, medical debt, and other non-mortgage debt, then dividing that number by the household’s annual income. A non-mortgage DTI of less than 10% is considered manageable; a ratio between 10% and 40% is considered high but manageable; a ratio over 40% is considered unhealthy.

The highest proportion of consumers with no non-mortgage debt have never had a card.

More than 4 in 10 former credit card holders report a non-mortgage DTI over 40%, the highest of the three groups.

Credit Quality: Subjective vs. Objective

46*Unscorable VantageScore records reflect deceased consumers or those with credit inquiries only. Unmatchable VantageScore records include: (a) consumers who don’t have a credit file with the bureau and (b) those for whom Experian did not receive sufficient identifying information. For details see http://bitly.com/creditscorecfsi.

Card holders are most likely to have both a high credit-quality self-assessment and a prime or super prime VantageScore®.

Former card holders are most likely to have a low self-assessment and a subprime or deep subprime score.

Those who never had a credit card are most likely to not know their credit quality or that they have a credit score; they were also the most likely to be unscorable and unmatchable by Experian.*

Company Logo

Card Holder Demographics

Account Mix

48

Credit Card account holders also have …

Notable Facts About Credit Card Holders

49

• Income: 16% earn less than $30,000, compared with 48% of non-holders.

• Demographics: Black and Hispanic populations represent 40% of non-holders, compared with 19% of card holders.

• Marital Status: 60% are married, while only 29% of non-holders are.

• Age: 43% of those who have never owned a credit card are 18-25 years old, compared with 9% of card holders.

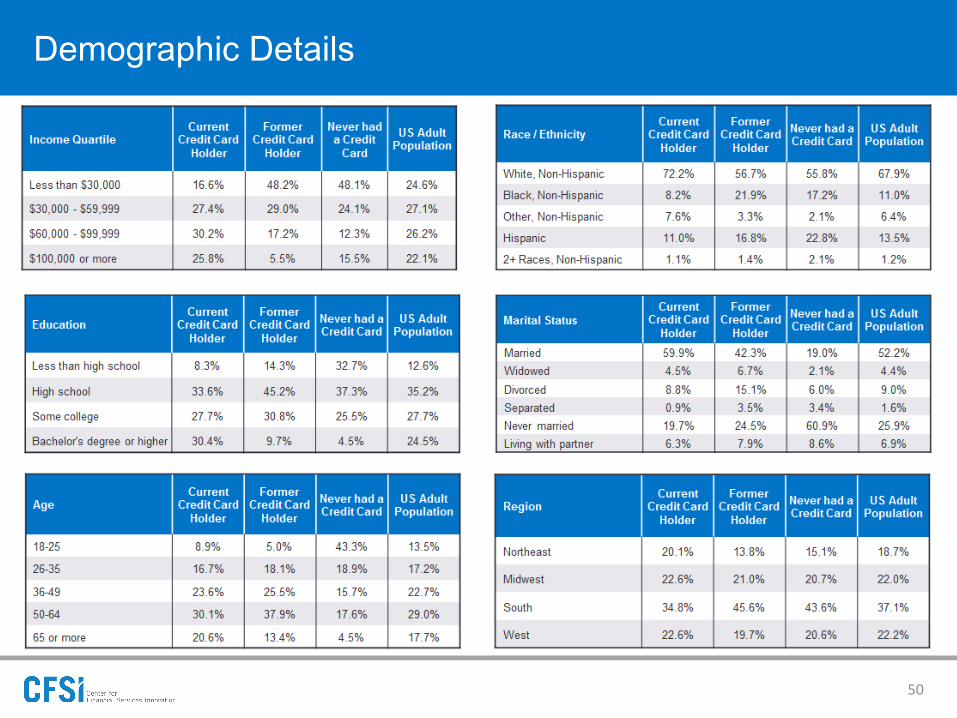

Demographic Details

50

Consumer Financial Health Study

51

The Consumer Financial Health Study survey data was captured from June – August 2014. The nationally representative survey sample includes more than 7,000 consumers.

The Consumer Financial Health Study benefited from the financial support of its funders, which include CFSI founding funder, the Ford Foundation, and MetLife Foundation.

• Segmentation whitepaper

• Segment briefs

• Credit score whitepaper

• Survey instrument

• Financial health and child well-being whitepaper

MetLife Foundation is a major sponsor of CFSI’s ongoing consumer financial health work.

Consumer Financial Health Study Methodology

52

• Segmentation whitepaper

• Segment briefs

• Credit score whitepaper

• Survey instrument

• Financial health and child well-being whitepaper

• CFSI partnered with GfK, a global market and consumer research firm, to field the Consumer Financial Health Study survey.

• E-mail invitations were sent to a random sample of GfK’s KnowledgePanel® participants June-August 2014, yielding 7,152 survey respondents. KnowledgePanel® is a large national, probability-based panel that provides a representative sample for online research.

• The sample is comprised of adults (18 and older) residing in the U.S. at all levels of the income spectrum; consumers with annual incomes under $50,000 were over-sampled to provide a robust set of data on consumers in the lower half of the income distribution. The target over-sample was 1,500 consumers with incomes under $50,000, to augment the generally representative pool of respondents. All data contained in this report has been weighted back to the total U.S. population to ensure that it is nationally representative.

• Standard, baseline incentives were given to respondents for survey completion; in addition to a sweepstakes entry, respondents each received between 1,000 and 1,500 points. Panelists typically receive 1,000 points for every survey session they complete, which is equal to $1. Respondents were offered a $10 incentive to provide consent to pull their credit score range.

• For more information about the survey instrument and methodology, download the segmentation whitepaper: bit.ly/ConsumerFinHealth

Want More?

53

The Consumer Financial Health Study data set contains a host of demographic, behavioral and product information, in addition to some information about financial institution relationships.

Looking for some targeted information to help you make product or marketing decisions? Reach out to your CFSI Relationship Manager to discuss how we can help.

Chicago New York San Francisco Washington, DC

Connect with us

cfsinnovation.com

@cfsinnovation

#finhealth

Linked In: Center for Financial Services Innovation