44

Credit Management

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | corey-aubrie-reynolds |

| View: | 215 times |

| Download: | 0 times |

Credit Management

Why Credit ?????

Credit is a marketing tool to strengthen the company’s competitive position in the market, facilitating growth of it’s business.

Credit is given much against our will due to competitive forces and as a value addition.

Why Credit

Management

Creditors don’t give the dues in time and show annoyance, if reminded.

Creditors have much less than they owe and choose to live & thrive on the tolerance of the suppliers.

Some customers take a very long time to pay and some may finally not pay at all.

We don’t ask creditors for payments in time fearing that we may lose the business.

Additional cost to the company in terms of man-hours, interest cost.

What is Credit Management ?

The task is to get our money in our coffers in agreed time.

A sale can be considered complete only when the last rupee due is in our hands.

Tools for Credit Management

Payment terms Credit evaluation Credit organisation Collection / Monitoring

activities Recovery of outstandings

Payment Terms Letter of credit Post dated cheque in advance Credit against bank guarantee /

collateral security Zero credit terms Bill discounting / marketing system Factoring Product exchange system

(Bartering) Trade finance

Credit Evaluation Financial statements

– Liquid ratio– Current ratio– ROCE

Trade reference Bank reference Sales Officer report Press reports Self developed ratings Ratings by professional agencies.

Credit Organisation Credit Manager

– Goals : • Maximum profitable sales • Steady turnover of accounts receivables.

– Knowledge :• Thorough with company policies.• Principles & practices of marketing• Principles of accounting & economics• Business problems & needs• Credit & collection management• Statutory Acts & rules / Legal formalities

Credit Organisation (cont’d….) Credit Manager (cont’d….)

– Special Qualities• Knack of getting money from unwilling

customers.• Art of writing good reminder letters.• Motivation of field staff for timely

collection.• Dealing firmly with weak customers.

– The person • In our existing setup, the Manager –

Marketing is ideal person for this job.

Collection / Monitoring Activities

Action by field officers– Ascertaining

customer track record

– Follow – up with customer for payments.

– Immediate settlement of disputes

– Coordination with finance for reconcilliation.

Collection / Monitoring Activities

Action by RO– Credit rating.– Regular reconciliation– Follow – up with banks

in case of LC– Take up with bank for

avoiding late credit– Maintaining

transaction records at RO and comparing with supply locations.

Recovery of

Outstandings

Recovery of outstandings Arbitration. Civil suit. Winding up petition. Factoring Joint action with industry members. Product exchange Channel for collection of bad debts. Additional payments with ongoing

supplies.

Refunds to

Customers

SBI Banking Arrangement Dishonoured Instruments:

– OMC account will be debited with the amount of instrument and the interest beyond 13 days at PLR

– Original instrument to be handed over to OMC local representative.

– Dishonoured instrument will not be presented again even if requested by drawee bank or local representative of OMC.

Scale of charges:– Transfer of funds:

• upto Rs 1 Lakh- Rs 3 per thousand•Over Rs 1 Lakh – Rs 2 per

thousand•Subject to a minimum of Rs 250

with a cap of Rs 500 per TT– For DD Purchase of all outstation

cheques:•A composite rate of 70 paise

percent (Interest Rs 0.45, collection charges including P&T charges Rs 0.25) with a minimum of Rs 15

Overdue interest on purchase of outstation cheques:– PLR will be recovered for the

period in excess of 13 days– No interest to be charged if it is

drawn on SBI or drawn on Bank at the center where clearing arrangement with SBI exists.

– In case of dishonoured instruments, in all cases, overdue interest at PLR will be recovered for the period in excess of 13 days

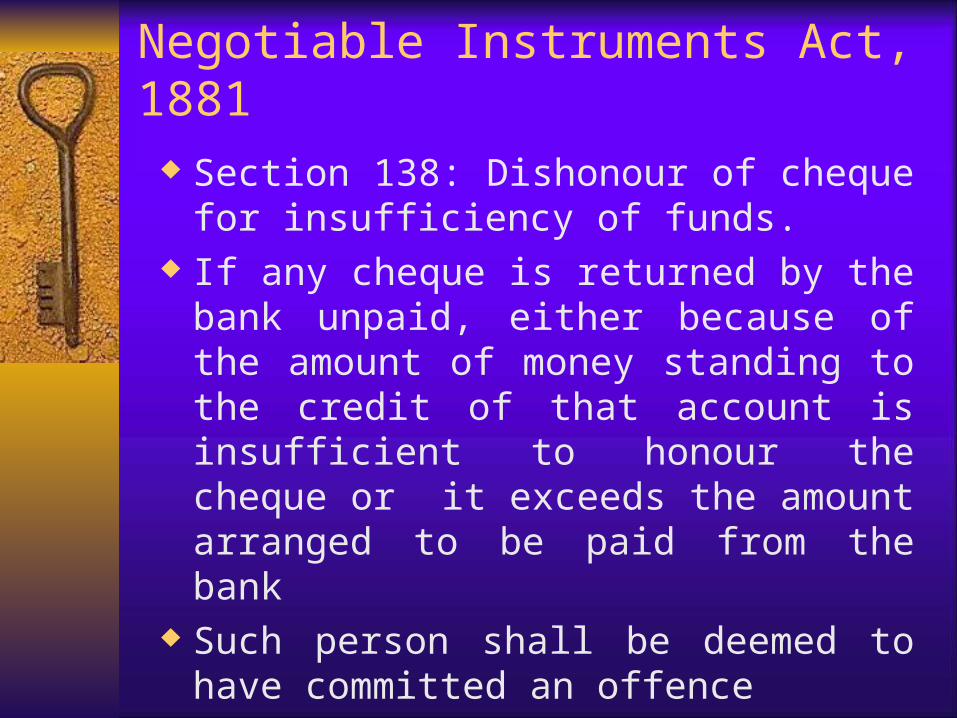

Negotiable Instruments Act, 1881

Section 138: Dishonour of cheque for insufficiency of funds.

If any cheque is returned by the bank unpaid, either because of the amount of money standing to the credit of that account is insufficient to honour the cheque or it exceeds the amount arranged to be paid from the bank

Such person shall be deemed to have committed an offence

He will be punished with imprisonment for a term which may extend to one year, or with fine which may extend to twice the amount of the cheque, or both.

Provided– the cheque is presented within a

period of six months – a demand is made within fifteen

days of the receipt of information from the bank

– the drawer of such cheque fails to make the payment within fifteen days of the receipt of the said notice.

Section 142: Cognizance of offences– No court shall take cognizance

of any offence punishable under section 138 except upon a complaint made by the payee.

– Such complaint is made within one month of the date on which the cause of action arises.

– No court inferior to that of a Metropolitan Magistrate or a Judicial Magistrate of the first class shall try any offence punishable under section 138.

Recommendations Each RO must have credit ratings

of its customers. MOU or customer acceptance for

the credit terms must be ensured. Instead of open credit, PDC to be

insisted. Periodic credit evaluation thru

professional agency for all CCR customers.

Comprehensive credit policy to be developed.

Issues

Credit To Be Perceived As A Necessary Evil

Competitive Pressures Driving Credit Credit Vs Discount Not Always

Accepted Approved Credit Going Beyond Limits Delays/Defaults/Unilateral

Deductions/Matching Competition

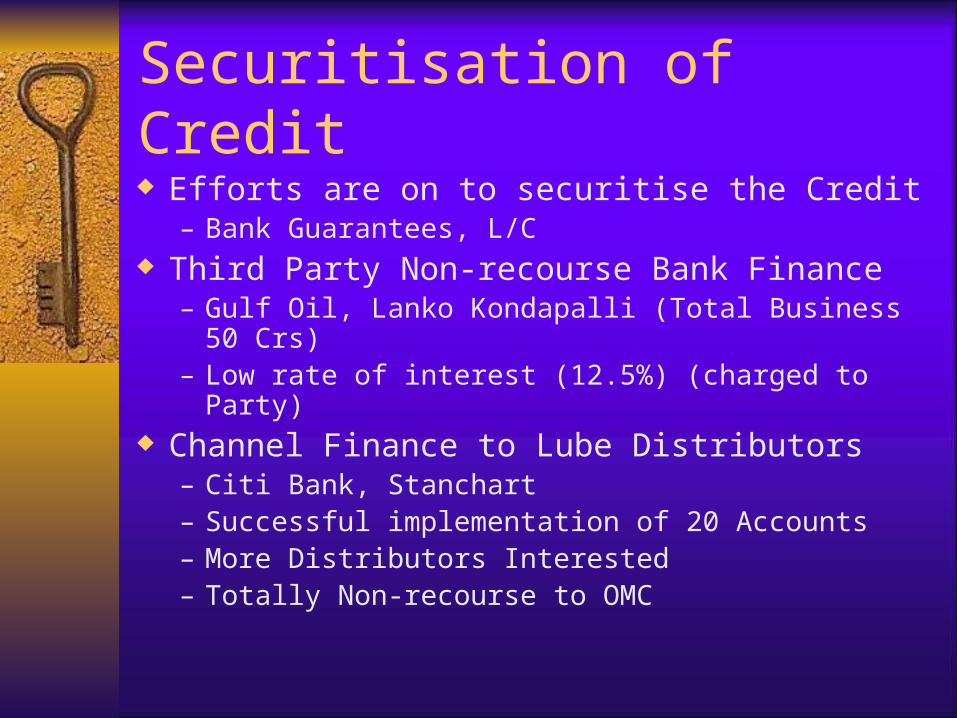

Securitisation of Credit Efforts are on to securitise the Credit

– Bank Guarantees, L/C Third Party Non-recourse Bank Finance

– Gulf Oil, Lanko Kondapalli (Total Business 50 Crs)

– Low rate of interest (12.5%) (charged to Party) Channel Finance to Lube Distributors

– Citi Bank, Stanchart – Successful implementation of 20 Accounts– More Distributors Interested– Totally Non-recourse to OMC

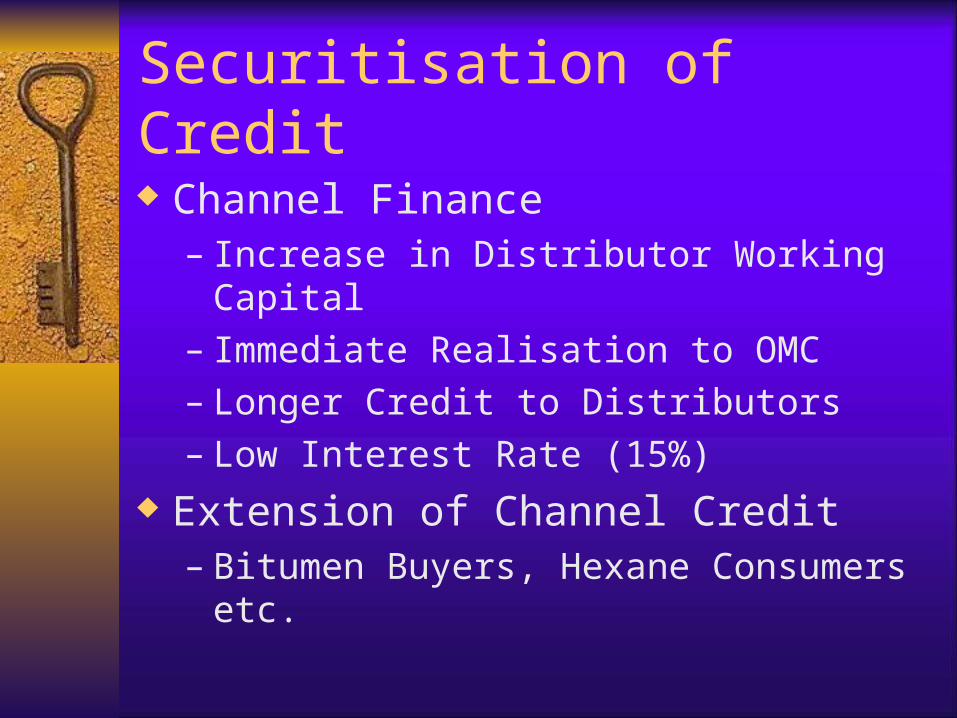

Securitisation of Credit

Channel Finance– Increase in Distributor Working

Capital– Immediate Realisation to OMC– Longer Credit to Distributors– Low Interest Rate (15%)

Extension of Channel Credit– Bitumen Buyers, Hexane Consumers

etc.

Securitisation of Credit

New Finance Instruments– Class I Companies Invoice Discount w/o L/C– Use of Consumers’ limits with the same

bankers– Usance Bill Discounting– Trust and Retention Accounts/Escrow

Accounts– Convince Consumers to avail Alternate

Finance Credit by OMC with Interest

Credit Rating Monitoring Health of 8 Major Industries

– Crisil Studies Monitoring Financial Strength (thru

Crisil)– 100 Major Consumers– Current &Potential Consumers

Basic Credit Evaluation Package to R Os– How to read Financial Statements– Basic Financial Ratios and Norms

Credit Rating

Tied up with Dunn & Bradstreet– Evaluating Small and Medium Units– Including Potential

Dealers/Distributors Regular Communication from HQO Involve Consumer to Get Himself

Rated

Control Mechanisms Credit As Item of Evaluation in MOU Each RO is Given Targets & Rating

– Credit to Be Brought Down to 60% of Opening Balance

– Total Credit Exposure to RO– Incentive for Collection of Old Dues– Incentive for Reversal of Earlier Provisions– Credit As No. Of Days Sale– CCR/SOA Reconciliation

Credit Must be Brought Down With Approved Limits– Propose for Realistic Credit, Regularise Thru Approval

Controls thru Software Conversion of SOA CDs into Data-base files SOA Reconciliation thru small matching

programs Collection of CCR data from Dispatch

terminal in soft form using DDP Consolidation of CCR data at R O thru

simple software Generation of various MIS reports of CCR

thru the same software Roll Out of Software Across the Country by

Dec

Accounts & Credit ControlInterface Special Emphasis on SOA Reconciliation Constant Monitoring/periodic Review

– HQO Commercial– Zonal Finance

Co-ordination Between Dispatch Location/R O– On Invoice and Collection Confirmation

Efforts to Bring Credibility to SOA Exceptional Cases Hire Out Side Help Instructions to Complete All Major Accounts in Each

RO Expedite Refunds to Enhance Corp. Image Some Hard Decision on Very Old/unreconciled

Accounts

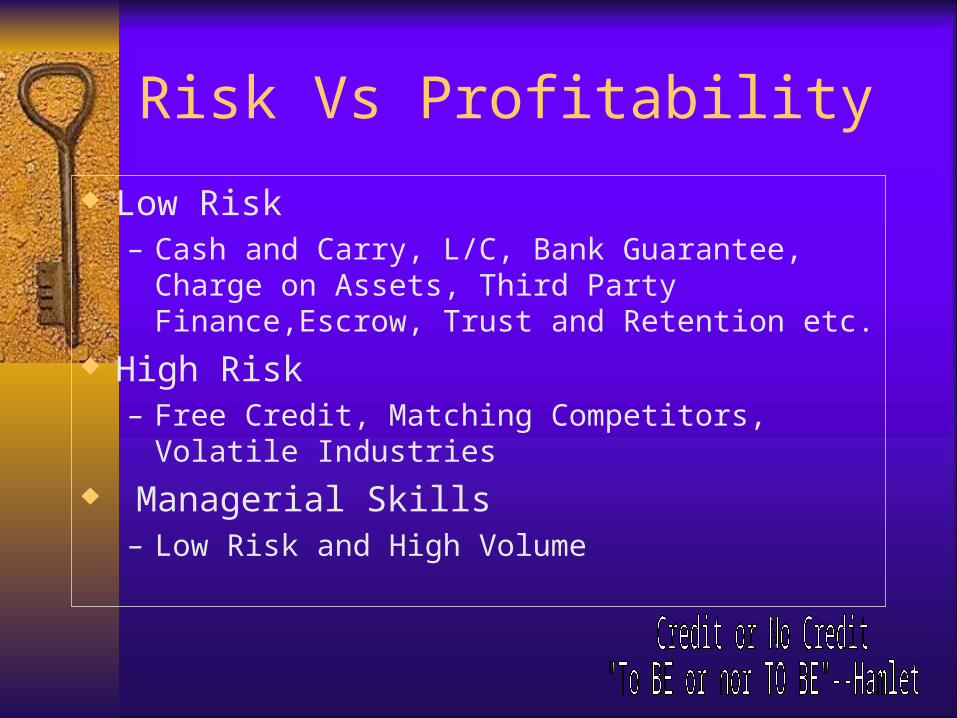

Risk Vs Profitability

Low Risk– Cash and Carry, L/C, Bank Guarantee,

Charge on Assets, Third Party Finance,Escrow, Trust and Retention etc.

High Risk – Free Credit, Matching Competitors, Volatile

Industries Managerial Skills

– Low Risk and High Volume

Risk Vs Profitability Ground Reality

– Surplus Products Chasing Few Consumers– Recession in Economy– Market Completion

• Marketers, Refiners, Crude Producers, Traders, Direct Imports

• Free Credit/Low Interest Credit

– Alternatives• Credit/Discounts• Uneconomic Exports

Risk Vs Profitability Develop Corporate Risk Index Assess Credit Risk Calculate Incremental Volumes to Be

Generated Thru Very Judicious Credit Calculate Incremental Volume Additional

Margin As Compared to Export Loss Arrive at the Total Credit Exposure (No.

of Days)– Business Line-wise, Product-wise– Regional Office-wise, Corporate

Risk Vs Profitability Let Risk Free Sale be = x Let Additional Credit Sales be = y Say Product Margin is 1000 and Export

Loss is 3000 on Sale Price Contribution to Risk= x X 1000 +y X1000 Contribution in Export= x X1000-y x

3000 Depending on Selling Price of Product An

Incremental Volume can be worked out for Judicious Credit

Risk Vs ProfitabilityCase Study

FO Demand Lost By MRO III for a want of Credit– 10,000 tons/month (Standard, Mukund, Reliance,

Float Glass) Diff. Between Domestic Price and Export (Say)

Rs. 3000/Ton One Month Exposure and Credit Risk 10 Crores Loss Due to Export 3000 * 10000 = 3 Crores Loss of Losing the Entire Recoverable = 10

Crores Break-even for no risk Business = 3,300 mt. Applying Safety Factor The Full Business Can

be Retained at 33% Bank Guarantee/LC

Some More Thoughts

Control Credit thru Exception– Beyond Approval Terms

A B C Analysis of Outstanding– Accounts More than 1 Crore

Upfront Provide for Doubtful Debts– Say 1% of the Total Outstanding

Expect and Budget for Unforeseen Failures

Cover the Out standings thru Insurance (if possible)

Way Forward Bring Discipline in Field Force Accountability for SOA Reconciliation

– SOA Availability to be made Current Develop Skills in Credit Evaluation Rope in Professional Help Monitor

– Select Industries, Select Business Groups,External Environment, Competition

Expect Failure and Act Rather Than React Not to Compromise

– Accepted Contractual Obligations, Due dates, Financial Instruments, PDCs, Bounced Cheques

FINALLY Yesterday is a cancelled

cheque.

Tomorrow is a promissory note.

Today is a cash….

Collect it wisely.

RM

CASH

RM

Thank you