104

INTERNSHIP REP ORT ON CREDIT OPERATING PROCEDURE OF BASIC BANK LTD. ASIC Bank Limite S e r v i n g p e o p l e f o r p r o g r e s s 1

| Date post: | 03-Apr-2018 |

| Category: |

Documents |

| Upload: | alamin-bali |

| View: | 222 times |

| Download: | 0 times |

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 1/104

INTERNSHIP REPORT

ON

CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.

ASIC Bank Limite

S e r v i n g p e o p l e f o r p r o g r e s s

1

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 2/104

Submitted to: Department of Management Studies

University of Dhaka

Supervisor- PROFESSOR SYED GOLAM MAOLA

Department of Management Studies

University of Dhaka.

Submitted by:

RUBANA NASRIN M.B.A (HRM), 6 TH Batch

Roll no.- 438, SL. no.-59

Department of Management Studies

UNIVERSITY OF DHAKA.

Date of Submission: 15 February, 2007.

2

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 3/104

LETTER OF TRANSMITTAL

Date: 15.02.07

To

Syed Golam Maola

Professor

Department of Management StudiesUniversity of Dhaka.

Sub: Submission of Internship Report.

Dear Sir,

I am highly satisfied to submit my report on “credit operating system” of BASIC

Bank Limited. This report is an integral part of our academic courses in

completion of the MBA program, which has given me the opportunity to have an

insight into the nature of loan, credit policy & practice, loan recovery and credit

problems of BASIC Bank Ltd. For preparing this report I tried my level best to

accumulate relevant and up graded information from all available sources.

In completing the Report I have tried my best in imparting every available details

of the Bank avoiding unnecessary amplification of the report. I hope that this

report will meet the standards of your judgments.

Faithfully yours,

_______ Rubana Nasrin

M.B.A (HRM), 6th Batch

3

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 4/104

ACKNOWLEDGEMENT

First of all I would like to express my gratitude to omnipotent and almighty Allah, whose

invisible guidance helped me to complete this report. Although, time was very limited for

getting the sufficient knowledge about all of banking service, but the short experience

that I gathered as an internee, in BASIC Bank Limited is an asset for all the time to come

in my life. I take the opportunity to express my deep sense of gratitude of my reverend

supervisor, Professor Syed Golam Maola for his invaluable suggestions and guidance

during the study period that has greatly inspired me in preparing this report successfully.

I am very much grateful to the authority of BASIC Bank Limited to assign me as an

internee in this reputed bank and have the opportunity to learn theoretical as well as

practical knowledge related to overall banking system and complete such an ambitious

study for my internship program as well as for preparation of this report. I am deeply

grateful to all concerned persons who provide valuable guidance, suggestions and advises

in collecting information, analyzing and preparing the report. I am particularly indebted

to them whose efforts and cordial cooperation made the report possible.

It couldn’t possible to thank all of those marvelous people who have contributed for the

preparation of this report. All of BASIC Bank employees are very frank and helpful. I

couldn’t think a single moment that I am working here as an internee. They helped me astheir employee. There are of course some very special people who can’t go without

mention. I am grateful to Mr. Mobarak Hossain Chowdhury, Deputy General Manager,

Mr.Masum Ahmed, Manager, Mr. Faruque Ahmed, Manager, Mr.Saidur Rahman Sohel,

Deputy Manager, Mr. Al-Amin, Deputy Manager and Mr. Motin Hossain, Officer, Mrs.

Asia Khanam, Assistant Officer, Mr. Billal Hossain, Officer of Dilkusha Branch of

BASIC for their cordial attitude and extending their helping hand to my problem

regarding internship program. Without their generous support I could hardly achieve my

cherished goals.

I am grateful to the Department of Management Studies, University of Dhaka for

providing me such opportunity to come closer to real situation. Finally, I want to express

my deep gratitude to my family members and also remember my friends whose enormous

help assisted me to complete my report.

4

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 5/104

Executive Summary

The present Internship Report “Credit Operating System”- A case study on Bangladesh

Small Industries and Commerce Bank Limited (BASIC) has been prepared under the

dynamic supervision of Professor Syed Gulam Maola, Department of Management

studies, University of Dhaka. The period of internship lasted for three months.

BASIC Bank Limited started its operation from January 21, 1989. Although the

Government of Bangladesh took over 100 percent ownership of BASIC in the year 1992,

the bank is yet not nationalized; it operates like a private bank. One of the significant

characteristics of BASIC is that the Bank’s Memorandum and Articles of Association

stipulates that 50 percent of loan -able fund is required to be invested in Small and

Cottage industries sector.

Credit is the most fundamental issue in our banking sector. Default culture is the most

common phenomenon in the banking sector of Bangladesh. Like other Govt. banks,

private banks also suffer from this problem. But, the Credit Management in BASIC is

relatively sound compared to all other similar banks operating in the country. As a result,

the bank has a very low rate of classified loans, which is around 4% only.

Although the amount of classified loans in BASIC is less than that of other banks, it stillremains a concern for the management because of its increasing trend during the last

three years. One of the major causes of classified loans in BASIC is the unwillingness of

the borrowers to repay loans in the backdrop of political unrest of the country. Other

causes include high rate of interest, entrepreneur’s inability to market their products, lack

of proper supervision by the bank officials, sickness of industries due to loss of

competitiveness in price with the similar imported products, lengthy bureaucratic

procedures of the other govt. agencies etc.

Since the process of recovery of classified loan involves lengthy legal procedures, the

percentage of recovery of such loans is very low. BASIC therefore emphasizes on

persuasion rather than going for legal action in order to recover its classified loans. Bank

considers the practical aspects of the projects being sick and extends further finance or

reschedules the repayment period.

5

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 6/104

BASIC should therefore establish a review process to examine the changing

circumstances of borrowers to determine the position of loans. The bank should also keep

in touch with any changes in the management structure of borrower organizations,

changes in industry trend and changes in overall economy of the country.

Before sanctioning a loan, the Bank should make survey on customers, suppliers and

competitors. Regular visits to borrower’s places and close monitoring of the activities of

the borrowers are more useful than having meetings in the bank.

6

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 7/104

CONTENTS

CHAPTER – 1 [Introduction] PAGE

NO.

[1.1] Background of the Study 1

[1.2] Objective of the Study 2

[1.3] Scope of the Study 2[1.4] Methodology of the Study 2

[1.5] Limitations of the Study 4

CHAPTER – 2 [Company Profile] 5-13

[2.1] Historical Background 5

[2.2] Functions 5

[2.3] Corporate Strategy 5

[2.4] Organizational Goal 6

[2.5] Lending Criteria 6

[2.6] Organizational Structure 6

[2.6.1] Board of Directors 6[2.6.2] Management 7

[2.7] Resources & Capabilities 9

[2.7.1] Physical & Technological Resources 9

[2.7.2] Human Resources 9

[2.8] Financial Resource 10

[2.8.1] Mobilization of Fund 10

[2.8.2] Utilization of Fund 11

[2.9] Performance of Bank 13

[2.10] Dividend 13

CHAPTER – 3 [Commercial Banking in Bangladesh] 14-17

[3.1] Historical Perspective of the Commercial Bank 14[3.2] Commercial Banking at Present 15

[3.3] Some Selected Indicator of Commercial Bank 16

[3.3.1] Branch Expansion 16

[3.3.2] Employment Generation 16

[3.3.3] Net Profit Performance 17

[3.3.4] Total Productivity 17

CHAPTER – 7 [Findings of the Study] 46-51

[7.1] Credit Policy of BASIC Bank 46

[7.2] Comparative Analysis of BASIC’s Credit Policy with other Bank 49

[7.3] SWOT Analysis of BASIC 51CHAPTER – 8 [Recommendation and Conclusions] 56-59

Conclusion 56

Recommendation 59

Appendix 60

Bibliography 63

7

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 8/104

CHAPTER ONE

1.1 Origin of the report

1.2 Background of the report

1.3 Objective of the report

1.4 Reason for the report

1.5 Scope of the report

1.6 Methodology of the report

1.7 Limitations of the report

8

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 9/104

1.1 Origin of the report

Reporting means the written presentation of the evidence and findings of a research.

After completion of the internship program report submission is essential. The report is

based on a topic that can satisfy both organization and my academic institution.

Internship is the last part of my MBA course. Being a MBA student internship and report

submission is essential for me. Without completion of internship and submission of

report I cannot be able to complete my MBA course.

This report is submitted to my internship supervisor, Syed Gulam Maola, Professor,

Department of Management Studies, University of Dhaka, after completion of the three

months internship program in the BASIC Bank Limited ( Dilkusha Branch). I have

assigned a topic “Credit Operating Procedure of BASIC Bank Ltd.” and the BASIC Bank

authority gave me the opportunity to work at the Dilkusha Branch for three months on

the topic.

1.2 Background of the Study

In the later 19th century, finance was a part of the Economics. But due to the globalization

and more expansion of international trade, Finance plays the major role for the economic

development. The development of a modern economy would not have been possible

without the use of money. Bank is an important and essential financial institution for the

necessity of the use of money and the protection of money.

Due to the globalization and technological innovation, banking business has become

competitive. To cope up with this, Bankers should have professional knowledge as well

as technical basic. As a MBA student Bank is one of the most appropriate field to gather

the experience. With a view to supply skilled personnel in Banking arena, DhakaUniversity has undertaken the internship training program for MBA students. As a part of

the MBA program, I was sent to BASIC Bank Ltd., Dilkusha Branch for having practical

exposure in the Bank for three months internship program.

9

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 10/104

1.3 Objective of the Report

The main objective of practical orientation is to get a clear-cut idea about Ban, how it

runs and what function it does i.e., to be acquainted with practical everyday function of

banking business. Along with the main objective, other objectives of report are:

1. To apply theoretical knowledge with practical situation.

2. To familiar with banking environment, clients, working hours, values, conditionsand other things related to bank

3. To understand the real management situation and to gather practical knowledge.

4. To explain the procedures, systems of credit management of BASIC Bank.

5. To determine the factors that influences the choice of a bank by the customers.

6. To evaluate the various loan programs of BASIC bank

7. To identify the problems faced by the customers and the bankers.

8. To evaluate whether the customer service provided by BASIC Bank is goodenough for its congenial existence and growth.

9. To get acquainted with the loan structure, size, system of loan sanction,classification and recovery of BASIC Bank.

10. To examine the profitability and productivity of the bank.

11. To acquire knowledge about the everyday banking operation of BASIC Bank.

12. To have a glance at the commercial banking system in Bangladesh.

1.4 Reason for the report

Bankers are the most important part for the economy. They play a vital role in the

economic development of the country. They keep the wheel of the economy for movingforward. So, efficient and qualified persons are needed for doing such development. To

build up potential future Banker MBA program can help a lot. Internship program can

help to be acquainted with day-to-day affairs of such people.

10

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 11/104

1.5 Scope of the report

There is certain boundary to cover this report. To achieve the objective of the report, i.e.

through knowledge about the organizational functions and its management, it is not

possible to cover each and every activity performed in the organization. The report has

covered only the general overview of the organization. Moreover the company itself and

financial institutions have got some confident information which are not possible to

disclose publicly, so those data and information had to be ignored for this report.

1.6 Methodology of the report

For making any report or statistical survey most of the data should be taken that reflect

actual situation. For my report I have collected various types of primary and secondarydata while I was performing my job. I have collected various data from various sources.

In a disciplined way I can say that the report input were collected from two sources-

Primary Sources:i) Practical deskwork

ii) Face to face conversation with the officers.

iii) Face to face conversation with the clients.

Secondary Sources:

i) Annual report of BASIC Bank

ii) Brochures of BASIC Bank iii) Prospectus of BASIC Bank

iv) Published or unpublished or personally collected data from

officers, Dilkusha Branch and Head Office of BASIC Bank v) Training institution’s papers those are supplied to the trainee.

vi) Various files and documents of credit division of BASIC Bank

Ltd.vii) Articles related to credit management in different journals and

magazines.

1.7 Limitations of the report

The study is done on the basis of survey in only one branch

Unavailability of relevant data and information.

Up-to- date information were not so available

Time is important issue in report writing. Schedule time span was not sufficient to

carry out an internship project of this big magnitude.

Some essential data could not be gathered because of confidentiality concerns.

11

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 12/104

The report was limited by the size of sample.

CHAPTER – TWOCOMMERCIAL BANKING IN BANGLADESH

2.1 Historical perspective of the commercial Banking

2.2 Commercial Banking and Recent Changes of Banking Sector

2.3 Some selected Indicators of Commercial Banks

12

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 13/104

2.1 Historical perspective of the commercial Banking

At the time of liberation there were around thirteen domestic scheduled banks and a few

foreign banks operating in the region of Bangladesh. Two of the smaller commercial

banks, namely, Eastern Banking Corporation and Eastern Mercantile Bank had their headoffices in the East Pakistan. The major banks only had their regional offices in Dhaka.

The management accepts the two East Pakistani banks were, however, almost solely in

the hands of non-Bangalis. All these banks except National Bank of Pakistan were in the private sector. The Government owned even National Bank of Pakistan only to the extent

of 25 percent. However, the management of the National Bank of Pakistan was almost

totally free from interference by the Government. Interestingly, the then central bank namely, the State Bank of Pakistan was owned by general public to the extent of 49

percent.

After the emergence of Bangladesh, all the banks except the foreign banks were

nationalized. The commercial banks were merged into six larger banks namely, Sonali,Janata, Agrani, Rupali, Pubali and Uttara bank. With the exodus of Pakistanis who

manned the top and upper middle echelon of management, a sudden vacuum emerged inthe effective top management of the nationalized banks. As the banks departed from

following the standard norms and practices, the state of affairs of the banks became

vulnerable leading to large-scale loan defaults. The loans taken by the public sector bodies like Bangladesh jute Mills Corporation, Bangladesh Textile mills corporation and

other state- owned enterprises were stuck- up at these institutions used bank loans mostly

for loss- financing.

During early 1980s the role of banks in the private sector was felt as an important factor

to invigorate the economy. A good number of new private banks were allowed tofunction. Banks following Islamic tends also started functioning. Most notabledevelopment was de-nationalization of two of the six NCBs, namely, Uttara and Pubali.A

few more foreign banks were also allowed to operate in the capital and port cities. During

mid 1980s when the private banks started to expand its lending activities, these banksexperienced somewhat new situation. The sponsor directors were especially interested to

use their influences for taking the loans for their own business houses or for enterprises

owned by their relatives or accomplices. Though the executives were free from thedictates of the bureaucrats, but had to show their allegiance to their new masters.

To correct the above-mentioned problems and to ensure the maximum benefits that

should be achieved from banking sector in 1990, the Bangladesh Government startedwith a five-year Financial Sector Reform Project (FSRP) with the following ten agenda:

I. Introduce a more liberal interest rate policyII. Introduce and implement an improved loan classification system

III. Introduce capital adequacy requirement and enforce these on the banking system

IV. Develop improved supervision systems for identify problem areas within the banking system

13

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 14/104

V. Develop money market instruments and initiate the auctioning of a short term

money market instrument

VI. Improve the operation of the capital markets and take the regulatory steps neededto improve such markets

VII. Clean up the jute debt in the commercial banking system and eliminate any risk to

the commercial bank portfolioVIII. Reform the NCBs in a three step process: 1) Recapitalize the NCBs2) Improve

their operating systems 3) Develop strategic approaches to their future

developmentIX. Improve loan recovery through introduction of better legislation

X. And courts to collect delinquent loans, improve the bankruptcy law to ease the

problems of liquidating companies, improve the flow of credit information for

new loans, and required the NCBs to improve their debt collectionXI. Initiate an immediate program of improvement to manpower through upgraded

training for bankers

2.2 Commercial Banking and Recent Changes of Banking Sector

Bangladesh Bank, the central bank of the country is the guardian of banking institutionsof Bangladesh. Bangladesh Bank (BB) head office is located at Motijheel, Dhaka. There

are two branches in Dhaka and there is one branch in each of the divisions. The structure

of the banking system is present in table-1.In Bangladesh around 75% people live in rural areas. Urban- rural ratio for NCBs is 585,

which is in line with the necessity of rural branches in our country. There are no FCBs in

rural area and PCBs had very few branches in rural area. FCBs are guided by the policyof their parent company but private banks should open their branches in rural areas.

Table 1: The Structure of Commercial Banking System In BangladeshType Number of institution.

Nationalized Commercial Banks (NCBs) 4

Specialized Bank/Dev.Banks 5

Foreign Commercial Banks (FCBs) 10

Private Commercial Banks (PCBs) 30

Source: Annual Report 2002-2003,Bangladesh Bank, GOB

Recent Changes:

Rupali Bank is a Government and public joint ownership bank, transformed from

nationalized to Public Ltd Company with 51% government ownership, which is

increased to94.5% in 1996.

RAKUB, created by the bifurcation of BKB in march1987.

ANZ Grindlays bank has merged in the Indian sub-continent and Middle East,

with standard Chartered Bank and has become ANZ Grindlays StandardChartered Bank in 2000.

Woori Bank is the renamed bank in Jan 2003,of Hanvit Bank Ltd, of formerly

Hanil Bank of South Korea, renamed in May1999.

14

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 15/104

Muslim Commercial Bank Ltd. (Pakistan) recently merged with Bank Asia in

2003.

Shamil Bank E.C (merged bank of Faisal Islamic Bank of Bahrain)

Credit Agricole Indosuez is the French Bank, formerly known as Bank Indosuez,

now this has been purchased by the Commercial Bank of Cylon.

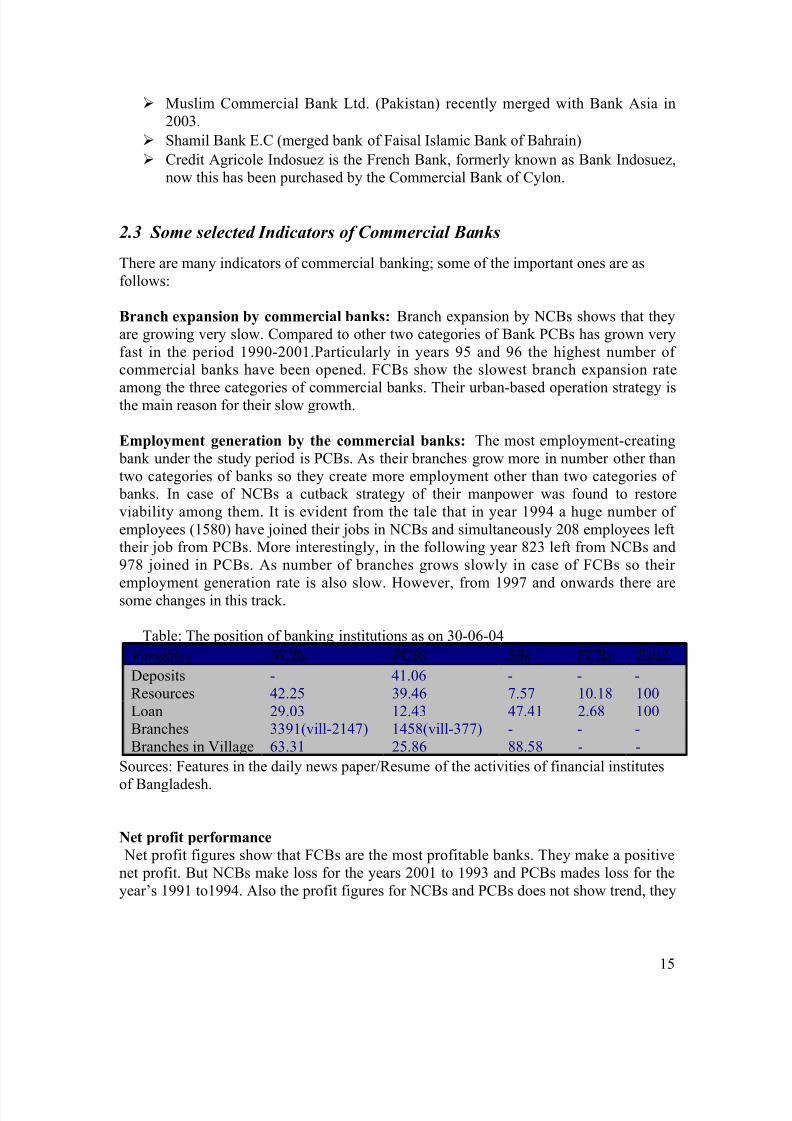

2.3 Some selected Indicators of Commercial Banks

There are many indicators of commercial banking; some of the important ones are as

follows:

Branch expansion by commercial banks: Branch expansion by NCBs shows that they

are growing very slow. Compared to other two categories of Bank PCBs has grown very

fast in the period 1990-2001.Particularly in years 95 and 96 the highest number of commercial banks have been opened. FCBs show the slowest branch expansion rate

among the three categories of commercial banks. Their urban-based operation strategy isthe main reason for their slow growth.

Employment generation by the commercial banks: The most employment-creating

bank under the study period is PCBs. As their branches grow more in number other than

two categories of banks so they create more employment other than two categories of banks. In case of NCBs a cutback strategy of their manpower was found to restore

viability among them. It is evident from the tale that in year 1994 a huge number of

employees (1580) have joined their jobs in NCBs and simultaneously 208 employees lefttheir job from PCBs. More interestingly, in the following year 823 left from NCBs and

978 joined in PCBs. As number of branches grows slowly in case of FCBs so their

employment generation rate is also slow. However, from 1997 and onwards there aresome changes in this track.

Table: The position of banking institutions as on 30-06-04

Variables NCBs PCBs SBs FCBs Total

Deposits - 41.06 - - -

Resources 42.25 39.46 7.57 10.18 100

Loan 29.03 12.43 47.41 2.68 100Branches 3391(vill-2147) 1458(vill-377) - - -

Branches in Village 63.31 25.86 88.58 - -

Sources: Features in the daily news paper/Resume of the activities of financial institutes

of Bangladesh.

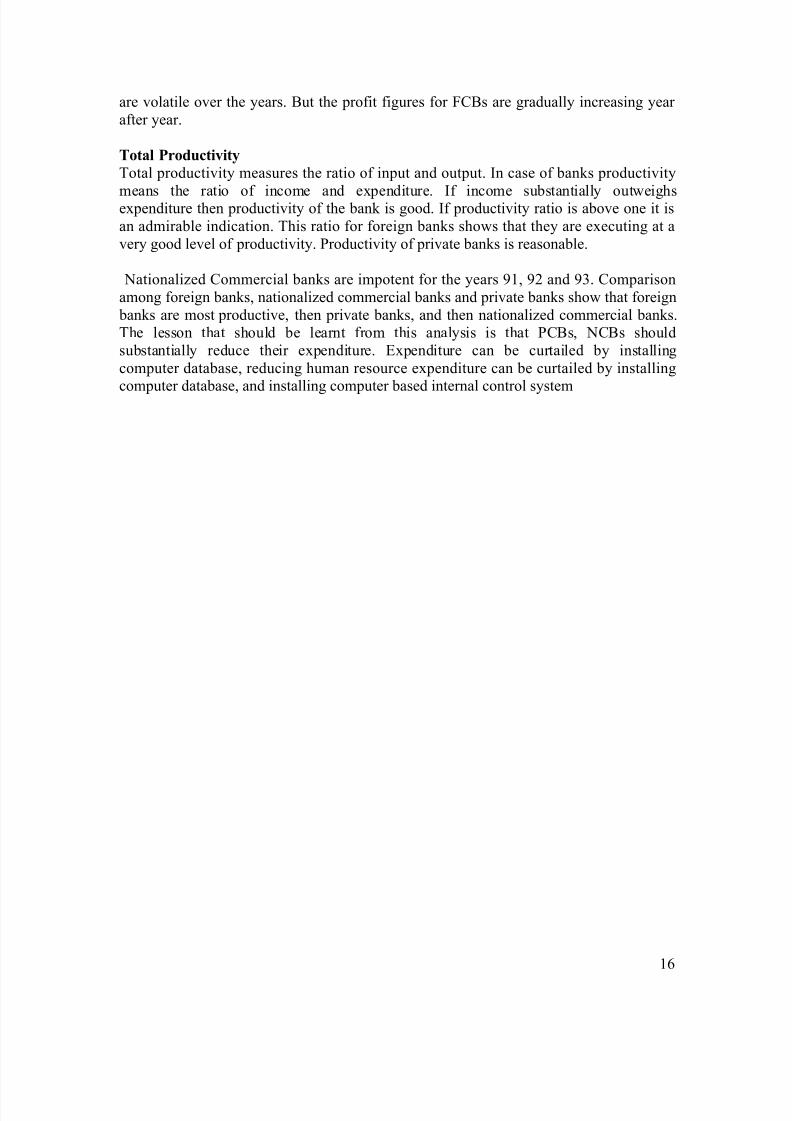

Net profit performance

Net profit figures show that FCBs are the most profitable banks. They make a positive

net profit. But NCBs make loss for the years 2001 to 1993 and PCBs mades loss for the

year’s 1991 to1994. Also the profit figures for NCBs and PCBs does not show trend, they

15

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 16/104

are volatile over the years. But the profit figures for FCBs are gradually increasing year

after year.

Total Productivity

Total productivity measures the ratio of input and output. In case of banks productivity

means the ratio of income and expenditure. If income substantially outweighsexpenditure then productivity of the bank is good. If productivity ratio is above one it is

an admirable indication. This ratio for foreign banks shows that they are executing at a

very good level of productivity. Productivity of private banks is reasonable.

Nationalized Commercial banks are impotent for the years 91, 92 and 93. Comparison

among foreign banks, nationalized commercial banks and private banks show that foreign

banks are most productive, then private banks, and then nationalized commercial banks.The lesson that should be learnt from this analysis is that PCBs, NCBs should

substantially reduce their expenditure. Expenditure can be curtailed by installing

computer database, reducing human resource expenditure can be curtailed by installing

computer database, and installing computer based internal control system

16

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 17/104

Chapter- Three

3.1Profile of BASIC Bank

3.2 Objectives of BASIC

3.3 BASIC’s Approach

3.4 Strategies of the BASIC Bank

3.5 Mission & Vision of BASIC

3.6 Organizational Goal

3.7 Organizational Structure

3.8 Corporate Culture of BASIC Bank

3.9 Human And Financial Resources of BASIC

3.10 Performance of The BASIC Bank limited

3.11 View of BASIC Bank, Dilkusha Branch

17

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 18/104

3.1 Profile of BASIC

The Bank of Bangladesh Small Industries & Commerce Limited (BASIC) established as

a Banking Company under the Companies Act 1913 launched its operation 1989, 21

January, incorporated by 1988, August 2. It is governed by The Banking companies Act

1991. The Bank started as a joint venture enterprise of the Bangladesh Credit Commerce

(BCC) foundation with 70 percent shares and the Government of Bangladesh (GOB) with

30 percent shares. The BCC Foundation being nonfunctional following the closure of the

BCCI, the Government of Bangladesh took over 100 percent ownership of the Bank on

4th June 1992.

Adjudged as one of the soundest banks in Bangladesh, BASIC Bank is unique in its

objectives. . It is a blend of development and Commercial Banking functions.

Steady growth in client base and their high retention rate since Bank’s inception testify to

the immense confidence they repose on its services. Diversified products in both liability

and assets sides particularly a wide range of lending products related to development of

small industries and micro enterprises, and commercial and trading activities attract

entrepreneurs from varied economic fields. Along with promotion of products special

importance is given to individual clients through providing personalized services. In fact

individuals matter in this Bank. This motto has been followed for development of clientele as well as human resources of the Bank.

The bank was established as the policy makers of the country felt the urgency for a bank

in the private sector for financing Small scale Industries (SSI). The memorandum and

Articles of Association of the Bank stipulate that 50% of Loan- able funds shall be

invested in Small and Cottage industries Sector.

BASIC Bank Ltd. at a Glance:

Established 1989Activity Starts Incorporated January 21, 1989

August 2, 1988

Legal Status Public Limited Company

Authorized Capital Tk. 2000.00 (Million) –2005

Paid-up Capital Tk.810.00 (Million) –2005

Deposit, Loans & Advances and Profit (Million) of BASIC Bank

18

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 19/104

2005 2004 2003

Deposit 22,326 15,509 11,267

Loans & Advances 15,339 12,000 9,283

Profit 872 689 616

* Profit before tax & provision

3.2 Objectives of BASIC :

BASIC Bank fully appreciates the importance and implication of the rapidly emerging

competition in the banking and finance sector of Bangladesh. It intends financing its

customer Suited to his or her place in the market. In this regards BASIC Bank

emphasizes competence among its Banking professional to cater to varied customer

requirements to the modern time.

The core objectives are:

- To carry on transact, undertake and conduct the business of Banking in all its

branches and to transact and do all matters and things incidental there to in

Bangladesh and abroad.

- To receive, borrow or raise money on deposits, loan or otherwise, upon such terms as

the company may approve and to hive guarantees and indemnities in respect of all

debts and contracts.

- To establish welfare oriented Banking systems.

- To play a vital role in human development and employment generation.

- To invest money in such manner as may from time to time be thought proper

- To carry on the business of buying and selling bullion, gold, and other valuable

assets.

3.3 BASIC’s Approach:

As a blend of development and commercial banking BASIC provides their clients with

full range of service to help them grow their assets and net worth. BASIC places

particular emphasis on small balance sheet size composed of quality assets and Steady

and sustainable growth. BASIC offers term loans to clients especially to develop small-

scale enterprises and also provide full-fledged commercial banking services like

19

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 20/104

collection of deposits, short term trade finance, working capital finance in processing and

manufacturing units and financing and facilitating international trade.

BASIC attaches special importance to technical and advisory support to small scale

industries in order to enabling them to run their enterprise successfully.

Micro Credit to the urban poor through linkage with NGO’s with a view to facilitating

their access to the formal financial market for the mobilization of resources is another

diversification of our services.

We provide an environment in which our staff members feel they can exercise their

initiative and judgement within a clearly established framework. Our Bank is the leader

in offering excellent career opportunity in transparent and participate management

culture.

Coping with the competitive and rapidly changing financial market of the country,

BASIC Bank maintains close connections with its clients, the regulatory authority

authorities, the shareholders (the government of Bangladesh), other banks and financial

institutions.

3.4 Strategies of the BASIC Bank:

The business of banking consists of borrowing and lending. As in other businesses,

operation must be based on capital, but Bank employs comparatively little of their owncapital in relation to the total volume of their transactions. The purpose of capital and

reserve accounts is primarily providing an ultimate cover against losses on loans and

investments.

Introduction of online Banking services, ATM cards, etc. are something that the Bank

looks forward to introducing as soon as possible because of the current demand in the

market place. Hence rapid innovation is definitely a key strategy of this Bank.

3.5 Vision and Mission of BASIC Bank:

Vision of the Bank

The gist of our vision is ‘Together towards Tomorrow’. BASIC Bank of Bangladesh

Limited, as the name implies, is not a type of Bank in some countries on the globe, but is

the first of its kind in Bangladesh. It believes in togetherness with its customers, in its

20

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 21/104

march on the road to growth and progress with services. to achieve the desired goal, there

will be pursuit of excellence at all stages with a climate of continuous improvement,

because, in BASIC Bank, we believe, the line of excellence is never ending. Bank’s

strategic plans and networking will strengthen its competitive edge over others in rapidly

changing competitive environments. Its personalized quality services to the customers

with the trend of constant improvement will be cornerstone to achieve our operational

success.

Mission of the Bank

The bank has chalked out the following corporate objectives in order to ensure smooth

achievement of its goals:

-To be the most caring and customer friendly and service oriented bank.

-To create a technology based most efficient banking environment for our customers.

-To ensure ethics and transparency in all levels

-To ensures sustainable growth and establish full value of the honorable shareholders and

-Above all, to add effective contribution to the national economy

As a part of the said issues, the bank also emphasizes on the following area of

services, such as: - Provide high quality financial services in export and import trade

-provide defect free quality customer service

-Maintenance of corporate and business ethics

-Become trusted repository of customers’ money and their financial advisor

-Make our stock superior and rewarding to the customers

-Display team spirit and professionalism

-Sound Capital Base

-Enhance shareholders wealth

2.6 Organizational Goal

• To employ funds for profitable purposes in various fields with special emphasison small-scale industries.

• To undertake project promotion to identify profitable areas of investment.

• To search for newer avenues for investment and develop new products to suit

such needs.

• To establish linkage with other institutions which are engaged in financing micro

enterprises.

21

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 22/104

• Adoption of new banking technology

3.7 Organizational Structure

To achieve its organizational goals, the bank conducts its operation in accordance with

the major policy guidelines laid down by the Board of Directors, the highest policy

making body. The management looks after the day-to-day operation of the bank.

3.7.1 Board of Directors

The Government holds 100% ownership of the bank. The Government of Bangladeshappoints all the directors’ of the Board. The Secretary of the Ministry of Industries is the

chairman of the bank. Other directors of the bank are high government and central Bank

executives. The Managing Director is an ex.-official member of the Board of Directors.There are at present 7 directors including the Managing Directors of the Board. The

present Board of Directors of the Bank consists of the following members.

[1]

Mr.Md. Nurul Amin

Chairman,BASIC Bank Limited& Secretary, Ministry of

Industries, Govt. of the People’sRepublic of Bangladesh.

[2]

Mr. Md. Sikander Ali Mondal

Director BASIC Bank Limited &Chairman, Bangladesh Small and

Cottage Industries Corporaion

[3]

Dr.Mohammad Tareque

Director, BASIC Bank Limited& Joint Secretary, Ministry of Finance, Govt. of the Peoples’

republic of Bangladesh

[4]

Mr. Mahmudul Karim

Director, BASIC Bank Limited

& Economic Minister, PermanentMission to the United Nations

[5]

Mr. Md. Mosharraf Hossain

Bhuiyan

Director, BASIC Bank Limited &Joint SecretaryMinistry of Commerce

Govt. of the ÿÿopleÿÿRepublic of Bangladesh

[6]

Mr. Asaduzzaman Khan

Director BASIC Bank Limited

&Executive Director

Bangladesh Bank.

[7] Mr. A. H. EKBAL HOSSAIN.

Managing Director

BASIC Bank Limited.

Head Office

Dhaka.

3.7.2 Management

The management is headed by the Managing Director. He is assisted by the General

Manager and Departmental heads in the head office. BASIC is different in respect to

hierarchical structure from other bank in that it is much more vertically integrated as for as reporting to the chief Executive is concerned. The Branches in charge of the Bank

report directly to the Managing Director and for functional purposes, to the Head of

Department consequently, quick decision making in disposal of cases is ensured.

22

NAME OF BOARD OF DIRECTORS:

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 23/104

[ORGANOGRAM OF BASIC BANK ]

23

GM(Operation)

Industria

l Credit

Division

Perso

nal

Central

Accounts

Establishment &

Branch Control

GM(Audit & Inspection)

DEVELOPMENT

GM

Credit

Division

Internati

onal

Division

BOARD OF DIRECTORS

Manager

Deputy Manager

Assistant Manager

Assistant Officer

Senior Officer

Officer

Clerical Staff:• Banking Staff

-

Non-Clerical Staff:• Messenger Staff

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 24/104

1996

1998

2000

2002

2004

2006

463 497 510 523 578 601

No. of employees

Y e a r

3.8 Corporate culture of BASIC Bank

This bank is one of the most disciplined Banks with a distinctive corporate culture. Here

we believe in shared meaning, shared understanding and shared sense making. Our

people can see and understand events, activities, objects and situation in a distinctive way

.They mould their manners and etiquette, character individually to suit the purpose of the

Bank and the needs of the customers who are of paramount importance to us. The people

in the Bank see themselves as a tight knit team/family that believes in working together

for growth. The corporate culture we belong has not been imposed; it has rather been

achieved through our corporate conduct.

3.9 Human And Financial Resources of BASIC

BASIC has a well-diversified pool of human resources, which is composed of people

with high academic background. Also, there is a positive demographic characteristic -

most employees are comparatively young in age yet mature in experience. In the

increasingly competitive market for highly skilled staff, BASIC focuses on providing a

stimulating compare environment and an attractive compensation package. The number

of employees has increased gradually to 453, 497, 510, 523,578 and 601 at the end of

2000, 2001, 2002, 2003, 2004 and 2005 respectively.

24

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 25/104

Mix of deposit at the end of 2005

793

207019462

Savings

Current

Term

582.82676.51 690.95

839.61937.52

0

500

1000

2001 2002 2003 2004 2005

Borrowing (million Tk.)

Financial Resources

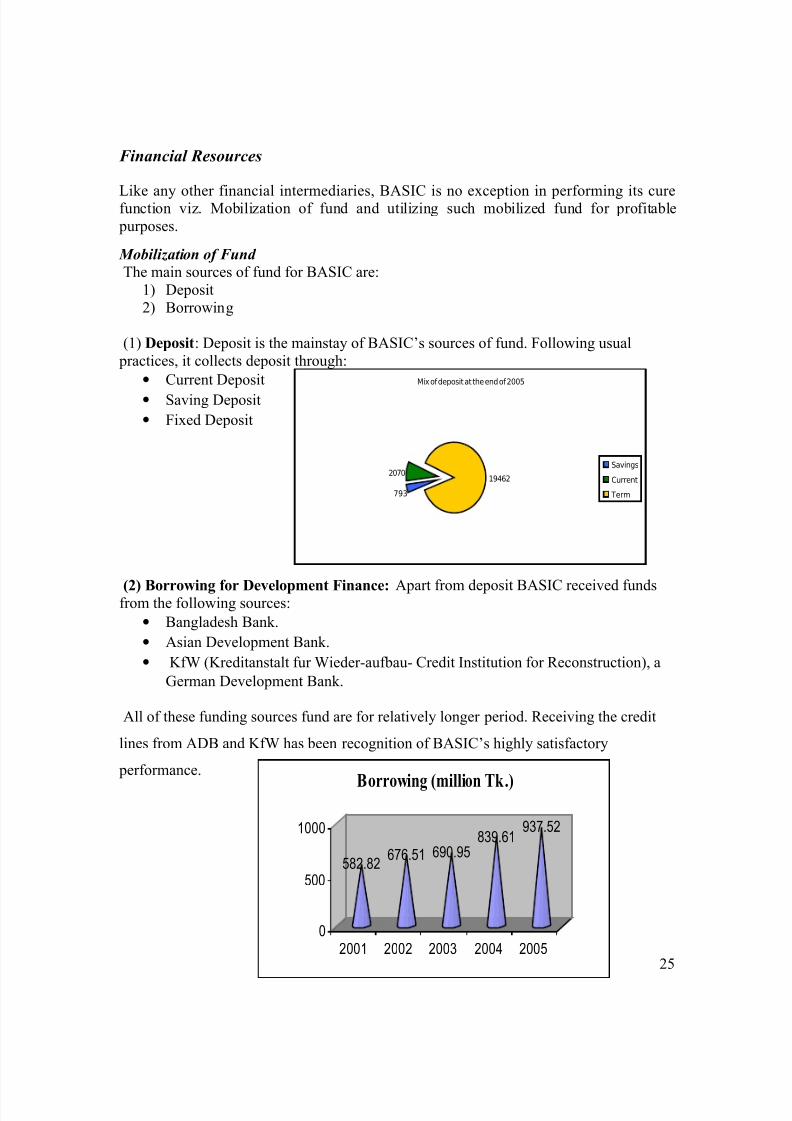

Like any other financial intermediaries, BASIC is no exception in performing its curefunction viz. Mobilization of fund and utilizing such mobilized fund for profitable

purposes.

Mobilization of Fund

The main sources of fund for BASIC are:

1) Deposit

2) Borrowing

(1) Deposit: Deposit is the mainstay of BASIC’s sources of fund. Following usual

practices, it collects deposit through:

• Current Deposit

• Saving Deposit

• Fixed Deposit

(2) Borrowing for Development Finance: Apart from deposit BASIC received fundsfrom the following sources:

• Bangladesh Bank.

• Asian Development Bank.

• KfW (Kreditanstalt fur Wieder-aufbau- Credit Institution for Reconstruction), a

German Development Bank.

All of these funding sources fund are for relatively longer period. Receiving the credit

lines from ADB and KfW has been recognition of BASIC’s highly satisfactory

performance.

25

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 26/104

Assets Composition end of 2005

17%

4%

1%

1%

56%

15%6%

Investment

Cash

Other

Premises & Fixed assets

Advance

Balance with other banks

Money at call & Short notice

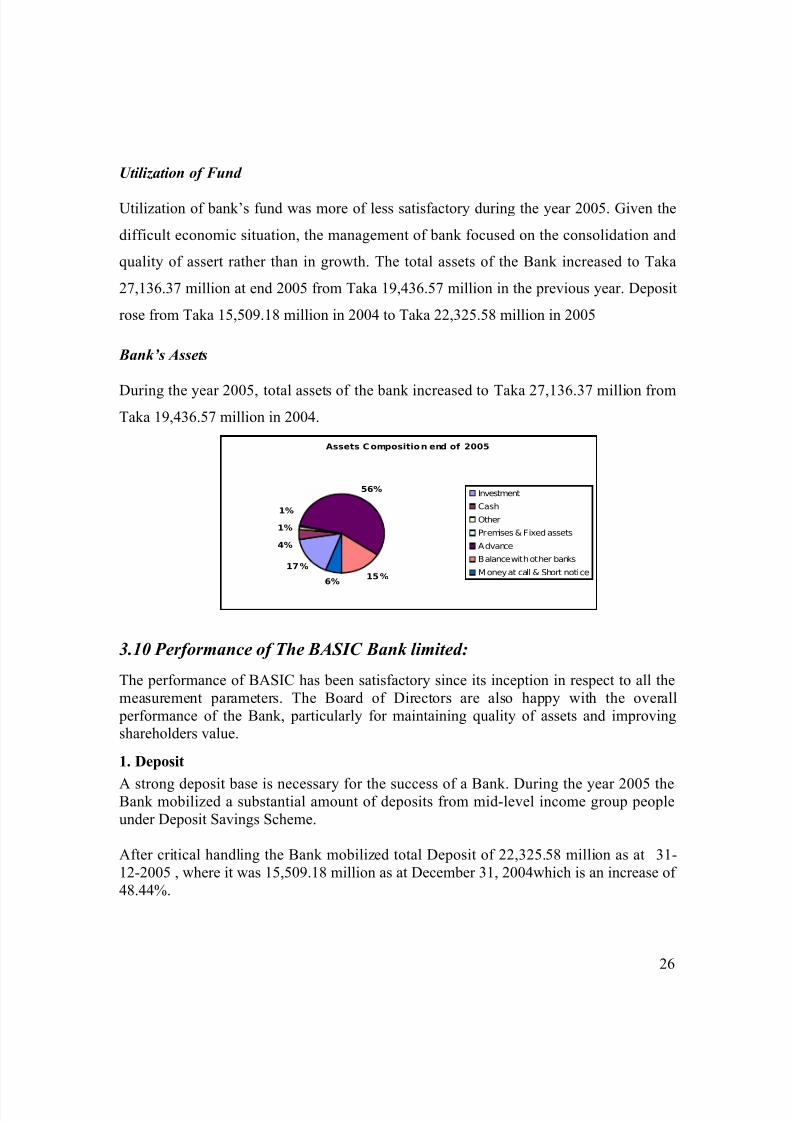

Utilization of Fund

Utilization of bank’s fund was more of less satisfactory during the year 2005. Given the

difficult economic situation, the management of bank focused on the consolidation and

quality of assert rather than in growth. The total assets of the Bank increased to Taka

27,136.37 million at end 2005 from Taka 19,436.57 million in the previous year. Deposit

rose from Taka 15,509.18 million in 2004 to Taka 22,325.58 million in 2005

Bank’s Assets

During the year 2005, total assets of the bank increased to Taka 27,136.37 million from

Taka 19,436.57 million in 2004.

3.10 Performance of The BASIC Bank limited:

The performance of BASIC has been satisfactory since its inception in respect to all the

measurement parameters. The Board of Directors are also happy with the overall

performance of the Bank, particularly for maintaining quality of assets and improvingshareholders value.

1. Deposit

A strong deposit base is necessary for the success of a Bank. During the year 2005 theBank mobilized a substantial amount of deposits from mid-level income group people

under Deposit Savings Scheme.

After critical handling the Bank mobilized total Deposit of 22,325.58 million as at 31-

12-2005 , where it was 15,509.18 million as at December 31, 2004which is an increase of

48.44%.

26

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 27/104

2. Capital and reserve fund:

The authorized capital of the Bank is 2,000.00 million. Total shareholders equity at theend of December 2005 stood at 1,726.14 million. The capital and reserve of the Bank as

on December 2005 stood at 916.14 million and paid up capital of 810.000 million. The

Bank also made provision on unclassified investment which is amounted to 10,236.82

million.

3. Investment

The total investment of the Bank stood at Tk. 4,540,550,760 as on 31-12-2005 as against

Tk. 2,252,964,460 in the previous year showing an increase of Tk. 22,875,863 with

growth rate of 100%. Investment is the core asset of a Bank. The bank gives emphasis toacquire quality asset and does appropriate lending risk analysis while approving

commercial and trade investment to clients.

4. Advance

The Bank’s Loans &Advances portfolio also indicates an impressive growth. Total loansand advances amounted to Tk. 12,000.15 million in 2004 as against Tk. 15,339.35million in 2004 and the growth is 27.08%. This is due to increased commercial and trade

financing, term lending and working capital support. The classified loan position is

almost nil. This was achieved by rendering due attention and monitoring high-risk advances. The Bank is trying to operate its credit activities with the target of achieving

Zero classified loans. The sectors financed include manufacturing, trading, construction,

transport, agriculture, fishing & forestry, edible oil, pharmaceutical, information

technology, consumer credit amongst others.

5. Dividend

As per Article number 130 the Memorandum and Articles of Association of Bank, unlessotherwise decided by the shareholders at least fifty percent (50%) of the net profit (after

tax)

to be reinvested in the capital of the company and to that extend bonus shares to beissued to the shareholders in lieu of cash divided. Also in maintaining the competitive

edge and creating a strong financial base the Board of directors with a view to improving

its equity by issuing bonus shares to its existing shareholders and accordingly, is pleasedto propose to its sole shareholders, the Ministry of Finance, subject to approval of the

Annual General Meeting, one bonus share against each 5 shares General Meeting, one

bonus share against each 5 shares amounting to Tk. 162.00 million and 6.25% cash

dividend amounting to Tk. 50.63 million.

6. Foreign Exchange Business

International Trade constitutes the main stream of business activities of BASIC Bank. It

offers a full range of trade financial services namely, Issue, Advice and Confirmation of

Documentary credit; arranging forward exchange coverage; Pre-shipment and Post-shipment finance; Negotiation and Purchase of Export Bills; Discounting bill of

Exchange; collection of bills, and outward remittance etc.

27

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 28/104

Import Business

In 2005 the Bank opened 14,094.96 million import letter of credit and the import volume

stood at Tk. 12,508 million with a growth of 12.00% in comparison with previous year.

Export Business

The growth of the export business has significantly been increased by40%. It stood at Tk.

11,097.23 million as on December 31, 2005 against Tk. 7,908.00 million of the previous

year.

Foreign Correspondents

BASIC Bank has correspondent Banking relationships with over 78 Banks spread across68 countries to facilitate trade and payment related services. So far the Bank’s total

correspondents are 180. The Bank has maintained relationship with leading internationalBanks and has successfully established credit lines with major Banks to support globalForeign Trade Business.

The Bank has earned an operating profit (after tax) of Tk. 285,494,793 during 2005 after

all provisions including the 1% General Provision on unclassified Loans Advances.

Provision for Income tax for the year amounted to Tk. 342,943,664 resulting in a net profit, after tax, of Tk. 285,494,793.

28

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 29/104

Performance at a glance (BASIC Bank limited):Particulars 2005 2004

From the Balance Sheet(Million Taka)

Authorized Capital 2,000.00 2,000.00Paid-up Capital 810.00 675.00

Reserve and Surplus 9,116.14 816.23

Shareholder’s Equity 1,726.14 1,491.23

Fixed Assets 135.00 101.41

Total Assets 27,136.37 19,436.57

Deposits 22,325.58 15,509.18

Long term Debt. 937.51 839.61

Loans & Advances 15,339.35 12,000.15

Placement & Investment 10,236.82 6,098.51

From the Income Statement

Gross Income 2,228.21 1,758.85

Gross Expenditure 1,599.77 1,241.63

Profit before tax 628.44 527.22Profit after tax 285.49 291.48

Tax paid (Cumulative) 1,777.70 1,434.76

Others (Million taka)

Income Business 14,094.96 12,508.00

Export Business 11,097.23 7,908.00

Financial Ratios (Percentage)

Capital Adequacy ratio 11.66 12.49

Capital fund to deposit liabilities 10.36 10.47

Liquid assets to deposit liabilities 58.01 50.36

Loan to Deposit Liabilities 69.74 77.37

Earning Assets to Deposits Liabilities 114.56 116.70

After tax return on average assets 1.23 1.70 Net Profit to gross income 12.81 16.48

Interest margin cover 214.56 205.07

After tax return on equity 17.75 21.27

SM/SSI Loan & Micro credit 67.00 62.21

Number of Branches 29 29

Number of Employees 601 601

3.11 View of BASIC Bank (Dilkusha Branch):

In the world of consumerism, the business organization of the world try for the consumer

satisfaction as a number one business strategy whatever may be the product of the

organization either service or non-service. Service is the product of Bank. There is a

saying that fustom service starts right from the stairs of the Bank building. The guard at

the door is the first person represents the Bank, receives a customer with wishes in

smiling face.

29

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 30/104

There are mainly three divisions in this Branch. The General Banking Division deals the

day-to-day transactions. The loan and advance division gives advance to the customer a

monitor whether he repays regularly or not. The Foreign Exchange Division is the highest

earning division among all the three division that deals their operations by two sub

departments Export (EXP) and (IMP).

Structure of BASIC Bank (Dilkusha Branch):

Deputy General Manager

Manager

Deputy Manager

Assistant Manager

Officer

Assistant Officer

CHAPTER- FOUR

CREDIT OPERATING SYSTEM OF BASIC BANK LTD.

30

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 31/104

Part- (i) Introduction

Part-(ii) Different type of credit facilities of BASIC Bank Ltd.

Funded and Non-funded Credit.

Part-(iii) Selection of Borrower, Preparation of credit reports, Processing of credit proposal.

Part- (iv) Selection, Valuation , Control & Charges on Securities

Part-(v) Documentation: Importance, execution, and safe-keeping

Part-(vi) Credit Planning, Pricing, Monitoring

Part-(vii) Micro Finance Scheme of BASIC Bank Limited

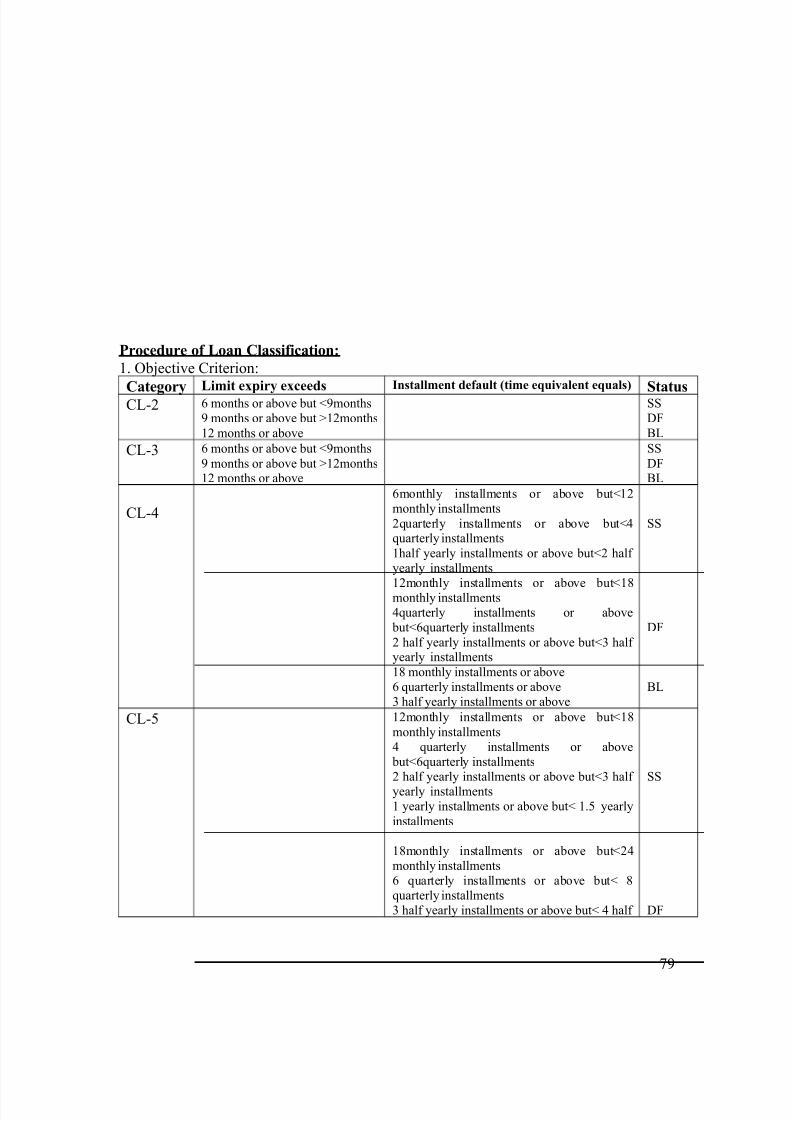

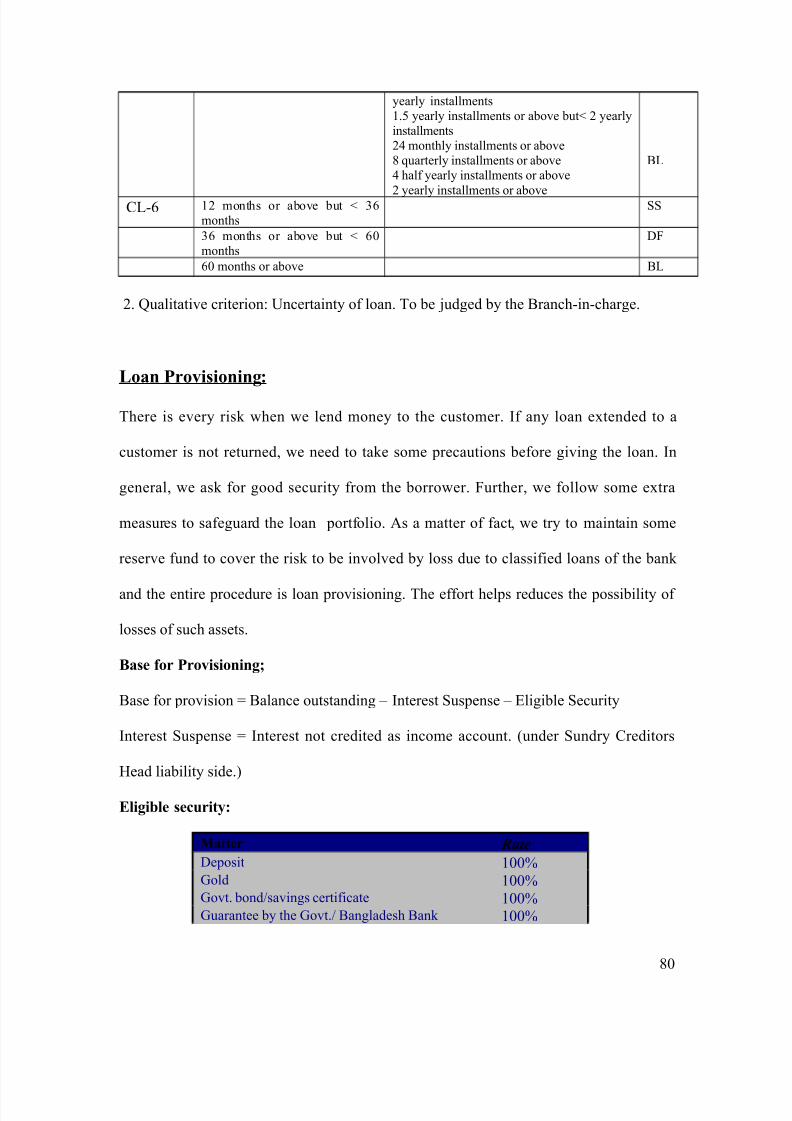

Part-(viii) Loan Classification, Provisioning and Declassification

Part- (ix) Supervision and Recovery of loans and advances of BASIC Bank Ltd.

Part-(i)

Introduction

BASIC Bank Limited is a new generation Bank. It is committed to provide high quality

financial services/products to contribute to the growth of G.D.P of the country through

stimulating trade & Commerce, accelerating the pace of industrialization, boosting up

export, creation employment opportunity for the educated youth, poverty alleviation,

raising standard of living of limited income group and overall sustainable socioeconomic

31

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 32/104

development of the country. In achieving the aforesaid objectives of the Bank, Credit

operation of the Bank is of paramount importance as the greatest share of total revenue of

the Bank is generated from it, maximum risk is centered in it and even the very existence

of Bank depends on prudent management of its credit portfolio.

Purpose and Importance of Bank Credit:

Bank performs various functions. Lending of money to different kinds of

borrowers is one of the most important functions of commercial bank. Not only this, it is

the most profitable business of the commercial bank and the major source of income.

Although all lending involve risks yet a bank has to go with it for earning profit and

economic upliftment as well.

The principal reason banks are chartered by state is to make loans to their customers.Banks are expected to support their local communities with an adequate supply of credit

for all legitimate business and consumer financial needs and to price that credit

reasonably in line with competitively determined interest rates. Indeed, making loans is

the principal economic function if banks-to fund consumption and investment spending

by business, individuals, and units of government.

For most banks, loans account for half or ore of their total assets and about half to two-

thirds of their revenues. When banks get into serious financial trouble, its problems

usually spring from loans that have become uncollectible due to mismanagement, illegal

manipulation of loans, misguided lending policies, or an unexpected economic downturn.

Banks make a wide variety of loans to a wide variety of customers for many different

purposes-from purchasing automobiles and buying new furniture, taking dream vacations

or pursuing college education to construction homes and office buildings. In practice

most of the banks make following types of loans:

1. Real Estate Loans

2. Financial Institutions Loans

3. Agriculture Loans

4. Commercial and Industrial Loans

5. Loans to Individuals

6. Lease Financing Receivables

32

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 33/104

Regulation of Lending

The loan portfolio of any bank is heavily influenced by regulation, because the quality of

a bank’s loan portfolio has more to do with risk and safety than any other aspect of the

banking

business. Some loans are restricted or prohibited by law.

When an examiner finds some loans that carry an immediate risk of not paying out as

planned, these credits are adversely classified. Typically, examiners will place adversely

classified loans into one of the three groupings: Sub-standard Loans, Doubtful Loans and

Loss Loans

A common procedure for examiners is to multiply the total of all substandard loans by

0.20, the total of all doubtful loans by 0.50 and the total of all loans by 1.00, then sum

these weighted amounts and compare their grand total with the bank’s sum of loan-loss

reserves and equity capital.

The quality of loans and other bank assets is only one dimension of a bank’s

performance. Numerical ratings are also assigned based on examiner judgement of the

bank’s capital adequacy, management quality, earnings record, liquidity position, and

sensitivity to market exposure. All five dimensions of bank performance are combined

into one overall numerical rating popularly referred to as the CAMELS rating. The letters

CAMELS are derived from:

C=Caspital adequacy

A=Asset q\uality

M=Management quality

E= Earnings record

L= Liquidity positiopn

S= Sensitivity to market risk

Banks whose overall CAMELS rating is toward the low, riskier end of the numerical

scale- an overall rating of 4 to 5- are examined more frequently than the highest –rated

banks, whose ratings of 1,2, or 3.

Credit Policy:

33

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 34/104

“Credit is a promise of future payment in kind or in money given in exchange for present

money, goods, or services.”

Or,“In general credit means the granting of a period of time by a creditor to a debtor at the

expiration of which the latter must pay the debt due.”

The credit policy of any banking institution is a combination of certain accepted time

tested standards, and some other dynamic factors determined by the realities of varying

and changing situations in the market place. The accepted standards relate to the aspects

of security and liquidity whereas the dynamic factors relate to such other aspects as the

nature of risk, interest margins, credit concentration, credit dispersal, and bank’s own

capabilities.

It is, therefore, necessary that the credit policy be kept under constant review by the Head

office Credit committee that is responsible for evolving and recommending a sound,

healthy and realistic credit policy and its due implementation.

As is true for any other institution, BASIC may have certain unique characteristic relating

to its operations, such as its age, and geographical concentration. These unique features

may require certain amount of flexibility in the credit policy, but as a rule, the general

standards of security and liquidity should not be allowed to be impaired and the

operations must be carried out in strict conformity with local laws and supervisory

requirements as stipulated. Credit policy lays down the basic principal and broad

parameters of the lending operations.

The key to a sound, healthy and profitable credit operation, however, lies in the quality

of judgment and sense of proportion of the officers making lending decisions, and their

knowledge of the borrowers and the market place. The following pages contain only a

statement of the basic principles of BASIC’s credit policy. Reference may be made to the

following other documents existing for the operation and administration aspects of

management of the credit function:

Basic Principles of Loans & Advances in BASIC Bank

“Loans and Advances” shall mean any debit balances on customer’s accounts excluding

debit balances on the accounts of other banks and excluding loans under specific counter finance arrangement. Basic Principles of Loans & Advances in BASIC Bank are:

34

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 35/104

1. Aggregate loans and advances shall not exceed the Bank’ s net worth or 65% of

customers deposit whichever is lower (excluding loans and advances covered by specific

counter - finance arrangements).

2. Within the aggregate limit of loans and advances as mentioned in (1) above 50% of

lending will be small industry sector in accordance with prescribed norms of thegovernment and the Central Bank in terms of the banks objectives with 50% to the

commercial sector. No term loans will be approved for the commercial sector. Exceptions

will be rare and will require approval of the Executive Committee.

3. All lending will be adequately secured with acceptable security and margin

requirement as laid down by the Head office credit committee.

4. The bank shall not incur any uncovered foreign exchange risk (currency exposure) in

the lending of funds.

5. The Bank shall not incur any risk of exposure in respect of unmatched rates of Interestof funding of loans and advances beyond 15% of outstanding loans and Advances.

6. End - Use of working capital facilities will be closely monitored to ensure lending used

for the purpose for which they were advanced

7. Country risk in loans and advances will be accurately identified and shall be within the

country limits if any approved for the bank.

The same treatment will be given to country risk arising out of contingent liabilities

relatingto Letters of credit and letters of guarantee.

8. Loans and advances shall be normally funded from customers’ deposits of a permanentnature, and not out of short-term temporary funds of borrowings from other banks or

through short-term money market operations.

9. The aggregate outstanding loans and advances (excluding loans advances covered by

specific counter – finance arrangement) shall be dispersed according to the following

guidelines (subject to item above whereby 50% of lending being to small industry

sector):(a) Short term commercial lending (to include self Liquidating and other short term

finance to retail and wholesale business clients to finance their usual Domestic and

international trade \ shipping of goods). This category to include working capital to hoteland tourism

(b) Facilities to shipping and transport (facilities for the purchase and construction of

ship / vessels and other modes of transport both by land and air)10. Spreads over cost of funds on loans and advances and commissions and fees on other

transactions should be commensurate with the rating of the borrower, quality or risk and

the prevailing market conditions.

35

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 36/104

11. Credit risk evaluation will include an accurate appraisal of risk in any credit exposure

is highly subjective matter involving quantitative and qualitative judgments. The

financial statements of the borrower do not always provide a complete picture of the borrower.

Therefore the bank has to use all financial data available and combine this with a number of qualitative factors analyzing the borrower’s financial position.

Part-(ii) Different type of credit facilities of BASIC Bank Ltd.

Funded and Non-funded Credit

The Government of Bangladesh has incorporated several changes in its Industrial policy2005. Let’s have a look of the major changes made in redefining small, medium and large

industries as under:

Scale of Industry Criteria

Small Fixed asset vale/replacement cost is less than Tk.1.50

Crore excluding land & Building

36

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 37/104

Loan Portfolio

338.3

5,013.55

9,987.50

Commercial Credit Micro Credit Industrial

Medium Fixed asset vale/replacement cost is in between Tk.1.50 Crore and 10.00 Crore excluding land &

Building

Large Fixed asset vale/replacement cost is more than Tk.

10.00 Crore excluding land & Building

Due to this radical change, BASIC Bank also had to amend its Articles of Association

regarding finance. In line with the government’s intention, amendment has been made byreplacing “Small & Cottage industry sector” with “Small & medium industry sector” .

So, now BASIC is entitled to finance a small scale industry as well as medium scale

industry.

BASIC Bank offers following credit facilities:

a. Project loans to small scale and medium scale industry.

b. Full-fledged commercial banking service including short term trade finance,working capital finance in processing and manufacturing units and financing andfacilitating international trade.

c. Micro credit to the urban poor through linkage with NGO.

Industrial credit:

The main concern of the basic bank is industrial/manufacturing loan. The industrial loan

reflected a significant growth of 29.85% over the previous year. Total outstanding

industrial loans including term and working capital stood at Taka 9,987.50 million at the

end of 2005 compared to Taka 7,691.20 million of 2004. BASIC Bank’s services are

specially directed towards promotion and development of small & medium industries. Its

exposure to small industries sector accounted for 51.70 percent of the total loans and

advances. During the year total of 175 projects were sanctioned term loan. Out of which

109 were new and the rest were under BMRE (Balancing Modernization, Revamping and

Expansion) of the existing projects.

The textile sector including garments being one of the major contributors to national

economy dominated the loan portfolio of the Bank. Other sectors financed include

engineering, food and allied industries, chemicals, pharmaceuticals and allied industries,

paper, board, printing and packaging, glass, ceramic and other non-metallic goods , jute

yarn and jute products. Recovery rate of project loan was 89 percent.

37

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 38/104

b. Commercial Credit

The Bank also supports development of trade, business and other commercial activities in

the country. It covers the full variety of services to the exporters and importers extending

various facilities such as cash credit, LTR, LIM, packing credit, short term loans, local

bills purchase and foreign bills purchase facilities. As on December 31 2005, total

outstanding commercial loans stood at Taka 5,013.55 million compared to Taka 4,024.70

million Crore in 2004.

c. Micro Credit :

BASIC Bank launched a Micro Credit Scheme in 1994. Micro Credit Scheme provides

for the poor for generation of employment and income on a sustainable basis particularly

in urban and suburban areas. At the end of 2005,total amount of Tk. 338.30 million

remained outstanding as against Tk. 284.10 million in 2004.Recovery rate during this period remained at a satisfactory level of 100.00 percent.

Perhaps we have got the essence of the credit portfolio of BASIC bank .Now we may go

to the topic: Funded and non funded Credit facilities.

Funded facilities are the credit facilities where bank has to outlay cash. non-funded

facilities are those in which bank has not to put in any cash, rather than merely giving acommitment or promise to pay.

Funded facilities:

Term Loan:

Term loan is allowed for procuring fixed assets of the project; hence term loan can be

said as project loan also. Right now BASIC Bank is in practice to finance term loan @49:51 debt-equity ratio. But, this is not hard and fast rule. There are occasions that bank

finances @ 60:40, 70:30 or 80:20. But for new project, if the debt portion is less than the

equity portion, that is well and good practice. Generally bank doesn’t finance land, land

38

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 39/104

development and civil construction. Generally Bank shows more interest to finance a

portion /full value of capital machinery.

Term loan is secured by registered mortgage of immovable property i.e. land, building,hypothecation of machinery. Term loan is generally disbursed once (or several times in

special cases). Repayment of term loan is generally made into some installments.

Generally grace period is allowed before commencement of installment. Generally 6months grace period is allowed. But it may be more or less depending on the tenure of

construction period, nature of industry and obviously on cash in flow of the project.

In BASIC Bank monthly repayment installment is common practice for term loan.

Followings are the type of Term loan:

• Short term loan

• Mid Term Loan

• Long Term Loan

Short term loan: The tenure of Short term loan is one year. Generally short term loan is

allowed to an existing project for procuring additional equipment/machinery where cashin flow is adequate to repay the loan within a year.

Mid term loan: The tenure of mid term loan is greater than one year up to 3 years.Generally Mid term loan is allowed where the bank thinks the project has a higher rate of

return (IRR).

Long term Loan: Long term loan is allowed for 5 years. Most of the cases we sanction

this sort of term loan. For a new project where substantial capital machinery is to be

financed by a bank and IRR is not too much high to repay the loan within less than 5

years.

So, we must do financial analysis i.e. to calculate financial parameter like NPV, IRR and

pay back period. In this regard cash flow statement should be observed verymeticulously.

Working Capital:

Working capital is needed by a concern for its current operational purposes. It is regarded

as life blood of the concern. The banker needs to assess the working capital requirement

in prudent and positive way. Several factors to be considered while assessing the workingcapital requirement of a concern like operating cycle, manufacturing cycle, operating

efficiency, market credit policies, competition in market, growth and expansion, pricehike etc.

Forms of working capital finance:

• Secured Over Draft(SOD)

• Cash Credit(Hypothecation)

• Cash Credit(Pledge)

• Loan General

39

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 40/104

Secured Over Draft (SOD):

This is an over draft facility secured by encashable securities like FDR, Government

Bond, wage earner bond etc. It represents permission to overdraw in current account upto

a sanctioned limit. The loan is allowed keeping some margin, generally 5%. Sometimes,overdraft is allowed without any security for a very short period to meet the exigency of

the trusted client with high standing and integrity. Bankers must ensure proper turnover

in an overdraft limit account.

Cash Credit

Like overdraft credit it is a continuous loan which is usually sanctioned for 6 months/oneyear, which is further renewable as per requirement of the borrower. After assessing the

working capital requirement and keeping proper margin (say 30%), a limit is sanctioned

and the borrower use to do withdrawal and deposit in the account provided that theoutstanding is within the sanctioned limit.

Two types of Cash Credit are discussed below:

Cash Credit (Hypothecation):

When cash credit facility is sanction under hypothecation of stock of goods it is called as

CC (Hypo). In the case of hypothecation, the stock remains under the possession andownership of the borrower. Only the right belongs to the bank through creating charge of

hypothecation. In case of CC (H) the client has to submit stock report regularly which is

to be verified by the bankers time to time. As the nature of security is movable type,

bankers are encouraged to take collateral security in case of hypothecation. In BASICBank hypothecation is more preferable practice than pledge.

Cash Credit (Pledge):In case of Cash Credit (Pledge), only the ownership belongs to the borrower. The

possession, control and right remain with bank. The nature of operation in CC (Pledge)

account is different than that of CC (H). CC (Pledge) is not a common practice in BASICBank. In fact CC (P) is more preferable in case of commercial trading rather than

industrial project.

Loan General:

In nature Loan general facility is like term loan. But, the purpose of this loan is meeting

requirement of working capital. It is generally given for 1-year period. Repayment is

made in installment basis or lump sum basis. The loan general facility some time may becalled as short-term loan.

International Trade Finance

International Trade dealings are one of the major business activities undertaken by

BASIC Bank Ltd. To facilitate international trade transactions, it has arrangedcorrespondent relationship with large number of international banks, which are active

across the globe. The Bank with its worldwide correspondent network and close

40

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 41/104

relationships with key financial institutions provides an extensive trade services network

to handle transactions efficiently.. BASIC offers following trade finances:

• Issuing, advising and confirming of Documentary Credits.

• Pre-shipment and post-shipment finance.

• Negotiation and purchase of Export Bills.

• Discounting of Bills of Exchange.• Collection of Bills.

Import finance:

Loan is given to the importer to provide liquidity for buying imported items. Each loan

must be related to one specific import transaction and the term of the financing can varydepending on the type of products imported on the needs of the importer.

BASIC Bank extends finance to the importers in the form of:

1. Opening of Import L/C

2. Payment against document(PAD)

3. Loan against Imported Merchandise (LIM)

4. Loan against Trust Receipt for retirement of import bills. (LTR)

5. Short term, medium term & Long term loans for installation of imported

machineries & production thereof.

Payment against document (PAD):

After establishing the Letter of Credit, the bank is bound to honor its commitment to pafor import bills when these are presented for payment. The foreign correspondent, who

negotiates the documents, gets payment as per stipulated reimbursement terms of the L/Cto the debit of the account of L/C opening bank ‘s F.C. account .The opening bank lodgesthe shipping documents in their books and responds debit advice originated by foreign

correspondent to the debit of payment against document (PAD) account. In fact, the

amount stands as advance to the importer which is adjusted by delivery of documents

against cash payment or by allowing post import finance such as LIM, LTR or even byterm loan /Loan general (if sanction is made so).

Loan against Imported Merchandise (LIM):

Loan against Imported Merchandise (LIM) is allowed against imported merchandise

storing the same in bank’s custody. There may be an existence of agreement or the partymay propose to the bank for having LIM facilities after arriving the goods in the port.

The merchandise is cleared by the bank through its approved clearing agent. . If the party

doesn't have any godown facilities or he has the shortage of money to clear the goods

from the port, then he wants bank loan. The advance is adjusted by delivering the goodsagainst payment by the importer. The documents remain with the bank. LIM facilities are

usually allowed for 90 days for each case. It may vary depending on the marketability of

the goods. A party may have LIM limit for one year but each LIM must have to beadjusted within the specific expiry date of that particular LIM.

41

7/28/2019 CREDIT OPERATING PROCEDURE OF BASIC BANK LTD.doc

http://slidepdf.com/reader/full/credit-operating-procedure-of-basic-bank-ltddoc 42/104

Loan against Trust Receipt for retirement of import bills. (LTR)

Depending on the relationship with the client, he may ask for LTR facilities instead of

LIM. Party has to submit proper securities. Documents are given to the party to retire

goods from the port on good faith. After selling the goods to the market the party adjustthe LTR alongwith the interest. It is a form of short-term loan. LTR facilities are usually

allowed for 90 days for each case. For trading purpose the tenure may be shorter like 60

days. Each LTR must have to be adjusted within the specific expiry date of that particular LTR.

Export Finance:

Preshipment finance

Loan given by BASIC Bank to the exporter to provide liquidity for buying or processing

Goods to be exported.

Pre-Shipment finance in the form of:

• Back-to-Back L/C

• Packing credit (PC)

Back-to-Back L/C: Will be discussed in the non-funded facility section.

Packing credit (PC):

Pre-shipment finance allowed under the name of "Packing Credit", is essentially a very

short-term advance granted by the bank to an exporter to enable him to procure, process,manufacture pack and ship the goods to the buyers abroad in conformity with the termsof export L/C /contract.

Post-shipment Finance:

Loan provided to the exporters against their export receivables.