32

Credit Ratings for Real Estate Backed Securities Diane K.Y. Lam, CFA Tel: 852-2533-3522 Email: [email protected] Standard & Poor’s October 2003

| Date post: | 31-Dec-2015 |

| Category: |

Documents |

| Upload: | lillith-park |

| View: | 28 times |

| Download: | 0 times |

Credit Ratings for Real Estate Backed Securities

Diane K.Y. Lam, CFATel: 852-2533-3522

Email: [email protected] & Poor’s

October 2003

• Trends in debt capital markets for real estate backed securities

• Evaluation of REIT

• Evaluation of commercial mortgage backed securities (CMBS)

• What are the implications for Taiwan?

Today’s Agenda

3

Structured Finance (insolvency remote issuer; risk is asset

related)Secured Corporate Debt

Unsecured Corporate Debt (risk is default of entity)

Reduced Credit Risk

Credit Risk Spectrum

CMBS Rating vs.LPT Corporate Rating

4

Residential M ortgageBacked Securities

(RMBS)

P oo l T ransactions

Single Borrower /S ingle P roperty

S ingle Borrower /M ultiple P ropertie s

M ultiple Borrowers /M ultiple P ropertie s

P rope rty S pec ificT ransactions

Commercial M ortgageBacked Securities

Credit LeaseTransactions

Real EstateStructured Finance

Corporate IssuerRatingsREITS

Debt Capital Markets Offerings forReal Estate

5

Issuers Intermediaries Investors

• Facilitate the pricing and placement of securities

• Monitor counterparty risk

• Global measure of credit risk

• Benchmark for risk premium

• Portfolio monitoring

• Enlarge the universe of potential investors

• More favorable credit terms

The Value of Credit Ratings

Performance of REITs in other Countries

7

Case Study: US

Real Estate Investment Trusts (REITs) in the United States:

– Created in 1960 to enable small investors to invest in real estate.

– Slow start but picked up in the 1990s after tax reforms and property downturn (companies saw them as an efficient way to access capital).

– There are currently 300 REITs operating in the United States.– Total assets under management currently over US$300 billion.– Approximately two-thirds are trade on the national stock

exchange.

8

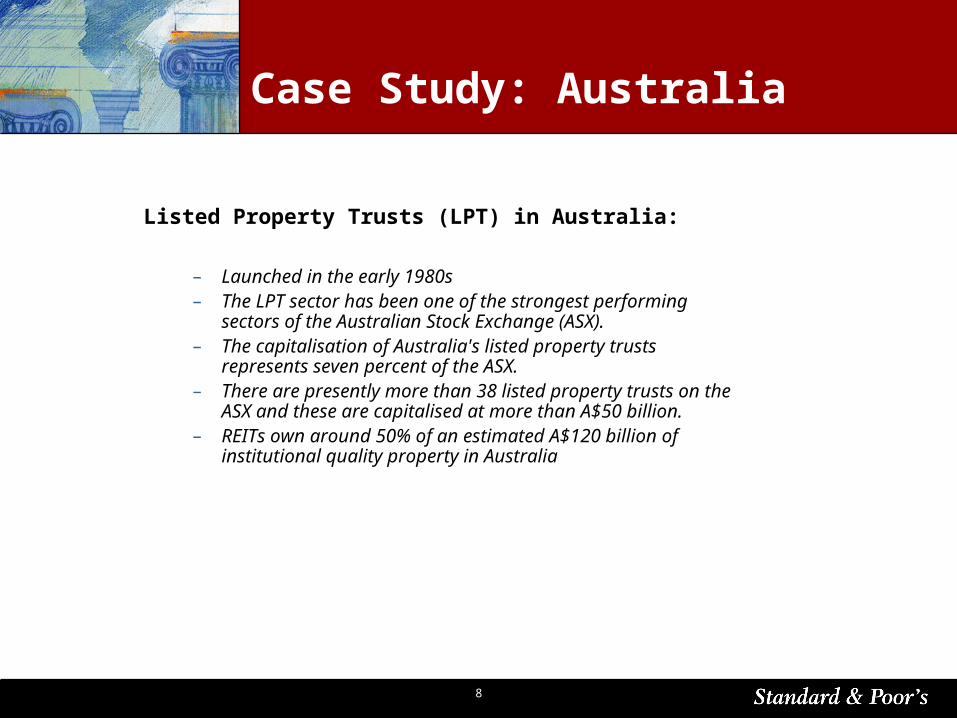

Case Study: Australia

Listed Property Trusts (LPT) in Australia:

– Launched in the early 1980s– The LPT sector has been one of the strongest performing

sectors of the Australian Stock Exchange (ASX).– The capitalisation of Australia's listed property trusts

represents seven percent of the ASX.– There are presently more than 38 listed property trusts on the

ASX and these are capitalised at more than A$50 billion.– REITs own around 50% of an estimated A$120 billion of

institutional quality property in Australia

9

Case Study: Asia

Japan– J-REITs were launched in Japan in 2000– Real estate to account for more than 50% of total assets.– There are currently six registered J-REITs in the market.

Korea– Property trusts were launched in Korea in 2001.– There are two types of trust: K-REITs and CR-REITs. – K-REITs are not preferred by investors because dividend

income is taxable (there are some exemptions).

Singapore– S-REITs were launched in 2002.– Three S-REITs in the market CapitaMall (retail) and

Ascendas (industrial) and Fortune Reits (retail).

Hong Kong– Enabling legislation launched in 2003

10

Start Date Distribution Gearing Development

US 1960 >90% restricted

Netherlands 1970 >80% <60% no

Australia 1970 100% <60% no

Belgium 1990 >80% <50% no

Canada 1994 85% - 100% <50% restricted

Singapore 1999 0-100% <35% no

Japan 2000 >90% <25% no

Korea 2002 [varies] [varies] restricted

Hong Kong 2003 >90% <35% restricted

France 2003 >85% no limit no

Global REIT Overview

11

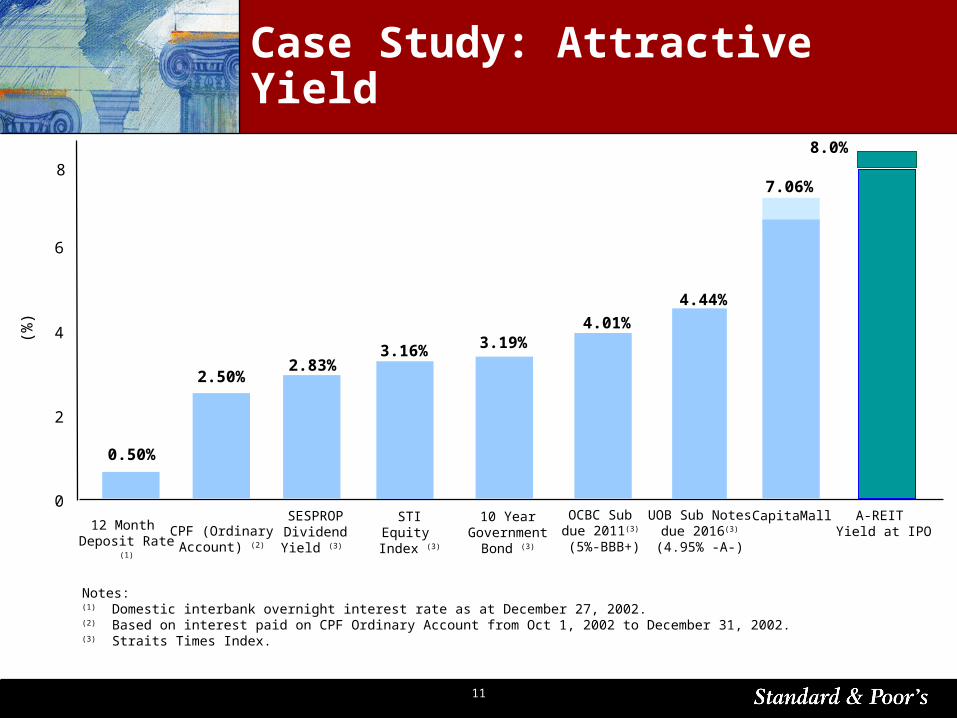

Case Study: Attractive Yield

Notes:(1) Domestic interbank overnight interest rate as at December 27, 2002.(2) Based on interest paid on CPF Ordinary Account from Oct 1, 2002 to December 31, 2002.(3) Straits Times Index.

0

2

4

6

(%

)

8

8.0%

A-REIT Yield at IPO

UOB Sub Notes due 2016(3)

(4.95% -A-)

4.44%

OCBC Sub due 2011(3) (5%-BBB+)

4.01%

10 YearGovernment

Bond (3)

3.16%2.83%

SESPROPDividendYield (3)

CPF (Ordinary Account) (2)

2.50%

12 Month Deposit Rate (1)

0.50%

STIEquity Index (3)

3.19%

CapitaMall

7.06%

12

Global CMBS Issuance 1985-2002

13

CMBS Market in Australia

14

CMBS Market In Japan

• Growth Factors:

• Corporate restructuring—divesting owned real estate

• Establishment of JREIT market

• Efforts of the RCC to securitise non-performing pools

• Liquidations of real estate portfolios by failed companies

• Emergence of some performing loan conduits—still sporadic

• Challenges:

• Securitization continues to be lender of last resort

• Still faces competition from direct lending market

15

CMBS Market In Korea

• Growth Factors:

• Corporate restructuring—divesting owned real estate

• Establishment of REITS enabling legislation

• Securitization of non-performing NPL loans held by private equity firms

• Challenges:

• Tenant Rights and Tenant Senior Liens (Chonsae)

• Still faces competition from direct lending market

16

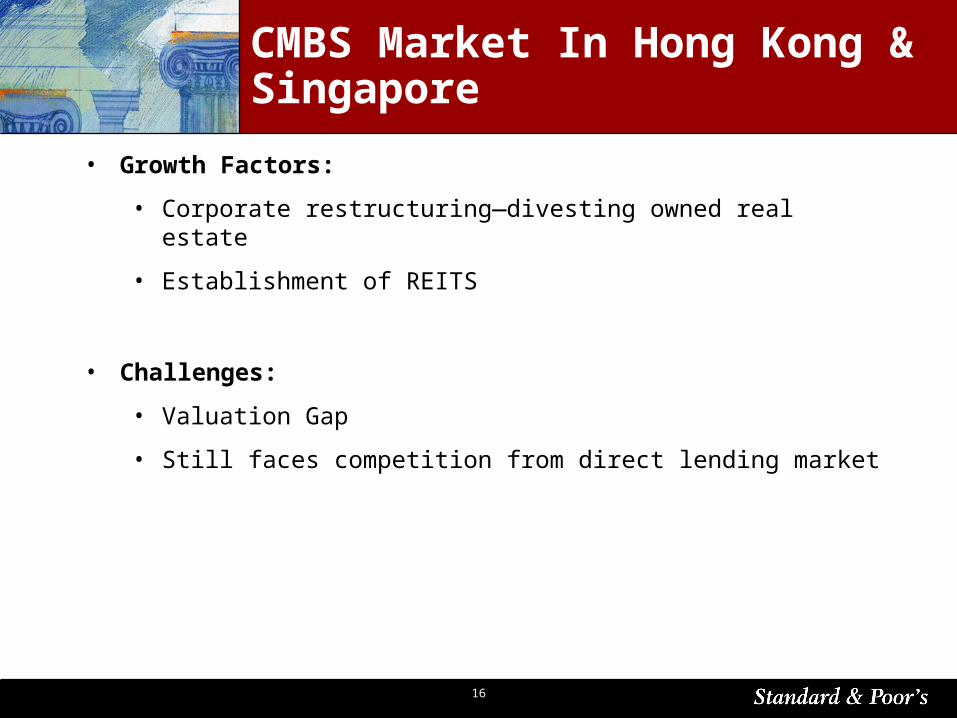

CMBS Market In Hong Kong & Singapore

• Growth Factors:

• Corporate restructuring—divesting owned real estate

• Establishment of REITS

• Challenges:

• Valuation Gap

• Still faces competition from direct lending market

17

What is a REIT?

• Equity - The shares or unit trusts are usually traded on the stock exchange.

• Most REITs remit at least 90% of their income to shareholders.• REITs are usually not required to pay income tax.• A REIT is a company that owns and, in most cases, operates

income producing real estate.• Laws differ across geographic locations, but broad parameters

are similar.

18

Structure of REITs

19

The REITS Ratings Approach

Industry CharacteristicsIndustry Characteristics

Trust Operational RiskTrust Operational Risk

Financial Risk/FlexibilityFinancial Risk/Flexibility

Degree of Operating Risk

The company’s business risk profile determines the level of financial risk

appropriate for a rating category.

Specific trust risk factors. .

Financial risk is portrayed largely through quantitative ratios.

20

Rated REITs in Asia Pacific

Credit Rating Outlook BusinessSingaporeCapitaMall Trust A- Stable Property trust

AustraliaAMP Diversified Property Trust A Stable Property trustAMP Office Trust A- Stable Property trustAMP Shopping Centre Trust A Stable Property trustCFS Gandel Retail Trust A- Positive Property trustCommonwealth Property Fund A- Stable Property trustDeutsche Office Trust BBB+ Stable Property trustGeneral Property Trust A+ Stable Property trustMacquarie Office Trust (Class-A notes) AAA N.A. Commercial (mortgage-backed securities)Principal Office Fund A- Stable Property trustStockland Trust Group A- Stable Property trustWestfield Trust A Stable Property trust

JapanJapan Real Estate Investment Corp. A+ Stable Property trustOffice Building Fund of Japan, Inc. A Stable Property trust

Rated Property Trusts in Asia Pacific

21

What is a CMBS

• Debt -- Fixed Income Securities backed by real estate• Issuer contracts to pay a stated coupon to investor• Issuer contracts to repay principal to investor over the tenor of the

bond• Issuer is typically tax neutral• Issuer is a SPV company that either owns operates income

producing real estate or owns a secured loan backed by real estate.

22

CMBS Characteristics

Noteholders

Issuer(SPV)

Owner/Borrower(eg. REIT)

Property Assets

Tenants

LiquidityFacility

SwapCounterparty

PropertyManagement

SecurityTrustee

Capex, Relet & Other Reserves

Trustee

SecuredLoan

Interest &Principal

Payments

LeasePayments ($)

Notes

23

The CMBS Rating Approach

• Transaction enquiry

• Desk top review of collateral, indicative ranges provided

• Staged engagement entered into

• Detailed review of collateral, site visits, underwriting

• S&P assessed collateral values, stabilised cash flows, loan-to-value and debt-service-coverage-ratio’s assigned

• Proceed onto second stage – YES/NO??

• Review of building condition, environmental and general due diligence information (including requirements for reserves)

• Transaction documents

• Ratings assigned

24

Major Issues to Examine

Property industry characteristics: Structural Considerations:Cyclical trends Interest rate risks, F/X riskCompetition Insurance requirementsEconomic outlook Liquidity Lines, Reserves

Collections Management/Commingling RisksRefinancing RiskAmortizing Debt or Bullet Debt

Asset Quality and Stability of Cash Flow: Asset Valuation ConsiderationDiversification Stabilized cashflows & yieldsRent review details Determine valuationTenant quality Is loan to value appropriate for the target ratingLease maturity profileVacancy & Re-letting reservesCash Flow ConsiderationCapital expenditures Determine refinancing constant

Is the debt service coverage ratio appropriate for the target rating

Management evaluations: Legal Considerations:Property Manager’s Expertise Creditor’s rights on real estate securityRental Manager’s Expertise Liquidation process and timeframeCredit control and administration Bankruptcy remoteness of the Issuer (SPV)

25

• Issuer rating vs. issue rating

• Corporate approach incorporates REIT’s business strategy and asset profile for a rolling five year period. It is our opinion of an issuers capacity to pay its financial obligations

• CMBS seeks to protect the bondholder from the REIT’s insolvency risk. CMBS rates to the bond documents underpinned by income from the rental property. The rating takes into account recovery prospects

• Default rating vs. ultimate recovery

Distinction with a CMBS Rating

26

CMBS Rating vs. REIT/Real Estate Issuer Rating

CMBS Issuer/CCR

First registered mortgages Security not required

Detailed analysis of security value and cashflows Portfolio-wide analysis of assets

Explicit LTV and DSCR thresholds No LTV and DSCR controls

Finite tenor of bonds “Reasonable” term (ie open duration)

Liquidity facility (may be required) No liquidity facility required

Bankruptcy remote SPV issuer Corporate risk considered

Dealing with assets – prescribed limits and controls Dealing with assets – corporate strategy related

Predetermined limitations regarding additional debt Corporate strategy regarding debt considered

Provisioning for potential liabilities (capex and relet) No cashflow provisioning for potential liabilities

Cashflow and waterfall controls No cashflow controls required

Rating reflects probability of default (inc. recovery) Rating reflects probability of default

27

Case Study: CMBS and REITS

28

Case Study: CapitaMall Trust

Trust: CapitaMall Country: Singapore Type: Shopping malls Lettable area: 813,352 sq. ft Management: CapitaMall Trust Management Sponsor: Subsidiary of CapitaLand Listed: July 2002 S&P rating: A-/stable Placement: 60-70% institutionalListed yield: 7.2%

29

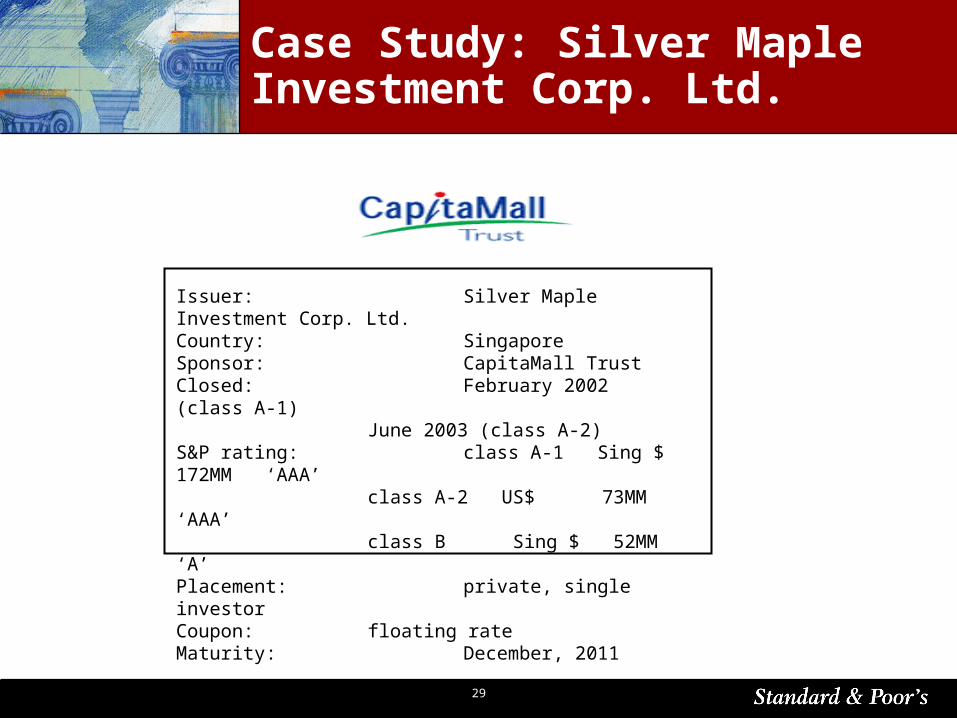

Case Study: Silver Maple Investment Corp. Ltd.

Issuer: Silver Maple Investment Corp. Ltd. Country: Singapore Sponsor: CapitaMall TrustClosed: February 2002 (class A-1)

June 2003 (class A-2) S&P rating: class A-1 Sing $ 172MM ‘AAA’

class A-2 US$ 73MM ‘AAA’class B Sing $ 52MM ‘A’

Placement: private, single investorCoupon: floating rateMaturity: December, 2011

30

• Diversification in portfolio

• Can offer high income and stable yields (example: REITS)

• Can offer bond backed by real estate security which are immune

to event risks (example: CMBS)

• Demands of investor base (pension funds, insurance

companies, banks)

• Demographics (aging population seeks income, preservation of

capital)

Outlook for Real Estate Backed Securities in Asia

31

Implications for Taiwan?

Lessons From Global Trends:• Capital markets can allocate funds efficiently for real estate assets –

RMBS, CMBS and REITS vs. corporate bond vs. equity

• Real estate backed securities provide high quality investments for investors

• New source of funding for real estate would alleviate the concentrated risk of Taiwan bank to real estate

• New source of stable revenue (property management fees) is beneficial to developers

• Setting clear legal, security, accounting and tax legislations are critical to establishing REIT and CMBS markets in Taiwan

• Capital market transaction propels the industry to higher levels of standard and accountability (valuation, management and reporting)

• Capital market is efficient in pricing risk and return (and will differentiate high quality assets from poor quality assets)

• Cultivate and educate the investors

32