24

Credit Risk Analysis Prof Ian Giddy Stern School of Business New York University LIB

| Date post: | 21-Dec-2015 |

| Category: |

Documents |

| View: | 216 times |

| Download: | 0 times |

Credit Risk Analysis

Prof Ian Giddy

Stern School of Business

New York University

LIB

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 2

Returns, Standard Deviations, and Frequency Distributions: 1926-1996

Source: © Stocks, Bonds, Bills, and Inflation 1997 Yearbook™, Ibbotson Associates, Inc., Chicago (annually updates work by Roger G. Ibbotson and Rex A. Sinquefield). All rights reserved.

– 90% + 90%0%

Average Standard Series Annual Return Deviation Distribution

Large Company Stocks 12.7% 20.3%

Small Company Stocks 17.7 34.1

Long-Term Corporate Bonds 6.0 8.7

Long-Term Government Bonds 5.4 9.2

U.S. Treasury Bills 3.8 3.3

Inflation 3.2 4.5

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 3

Debt vs Equity Risk

Value

of future

cash flows

Value

of future

cash flows

Contractual int. & principal

No upside

Senior claims

Control via restrictions

Contractual int. & principal

No upside

Senior claims

Control via restrictions

Assets Liabilities

Debt

Residual payments

Upside and downside

Residual claims

Voting control rights

Residual payments

Upside and downside

Residual claims

Voting control rights

Equity

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 4

Total Firm Risk

Probability

Return on Assets

68%

95%

> 99%

– 3 – 48.2%

– 2 – 27.9%

– 1 – 7.6%

012.7%

+ 1 33.0%

+ 2 53.3%

+ 3 73.6%

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 5

Debt vs Equity Risk

Probability

Return on Assets

68%

95%

> 99%

– 3 – 48.2%

– 2 – 27.9%

– 1 – 7.6%

012.7%

+ 1 33.0%

+ 2 53.3%

+ 3 73.6%

Debt Risk Equity Risk

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 6

Credit Risk versus Market Risk

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 7

CreditMetrics Methodology

Establishes the exposure profile of each obligor in a portfolio.

Computes the volatility in value of each instrument caused by possible upgrades, downgrades, and defaults.

Taking into account correlations between each of these events, it combines the volatility of the individual instruments to give an aggregate portfolio volatility.

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 8

CreditMetrics Roadmap

Compute exposure profile of

each asset

Compute exposure profile of

each asset

Compute the volatility of value caused by

upgrades/downgrades and defaults

Compute the volatility of value caused by

upgrades/downgrades and defaults

Compute correlations

Compute correlations

Portfolio value-at-risk due to creditPortfolio value-at-risk due to credit

Exposures Value-at-risk due to credit Correlations

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 9

Provisions of Bonds

Secured or unsecured Call provision Convertible provision Put provision (putable bonds) Floating rate bonds Sinking funds

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 10

Default Risk and Ratings

Rating companiesMoody’s Investor ServiceStandard & Poor’sDuff and PhelpsFitch

Rating CategoriesInvestment gradeSpeculative grade

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 11

Bond Credit Ratings

Moody’sStandard &Poor’s Interpretation

AaaAa

AAAAA

High-quality debt instruments

ABaa

ABBB

Strong to adequate ability topay principal and interest

BaBCaaCaC

BBBCCCCCC

Ability to pay interest andprincipal speculative

D In default

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 12

Factors Used by Rating Companies

Coverage ratios Leverage ratios Liquidity ratios Profitability ratios Cash flow to debt

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 13

Medians of Key Ratios : 1993-1995

AAA AA A BBB BB B CCCPretax Interest Coverage 13.50 9.67 5.76 3.94 2.14 1.51 0.96

EBITDA Interest Coverage 17.08 12.80 8.18 6.00 3.49 2.45 1.51Funds from Operations / Total Debt

(%) 98.2% 69.1% 45.5% 33.3% 17.7% 11.2% 6.7%

Free Operating Cashflow/ TotalDebt (%) 60.0% 26.8% 20.9% 7.2% 1.4% 1.2% 0.96%

Pretax Return on Permanent Capital(%) 29.3% 21.4% 19.1% 13.9% 12.0% 7.6% 5.2%

Operating Income/Sales (%) 22.6% 17.8% 15.7% 13.5% 13.5% 12.5% 12.2%Long Term Debt/ Capital 13.3% 21.1% 31.6% 42.7% 55.6% 62.2% 69.5%Total Debt/Capitalization 25.9% 33.6% 39.7% 47.8% 59.4% 67.4% 69.1%

AAA AA A BBB BB B CCCPretax Interest Coverage 13.50 9.67 5.76 3.94 2.14 1.51 0.96

EBITDA Interest Coverage 17.08 12.80 8.18 6.00 3.49 2.45 1.51Funds from Operations / Total Debt

(%) 98.2% 69.1% 45.5% 33.3% 17.7% 11.2% 6.7%

Free Operating Cashflow/ TotalDebt (%) 60.0% 26.8% 20.9% 7.2% 1.4% 1.2% 0.96%

Pretax Return on Permanent Capital(%) 29.3% 21.4% 19.1% 13.9% 12.0% 7.6% 5.2%

Operating Income/Sales (%) 22.6% 17.8% 15.7% 13.5% 13.5% 12.5% 12.2%Long Term Debt/ Capital 13.3% 21.1% 31.6% 42.7% 55.6% 62.2% 69.5%Total Debt/Capitalization 25.9% 33.6% 39.7% 47.8% 59.4% 67.4% 69.1%

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 14

Process of Ratings and Rate Estimation

We use the median interest coverage ratios for large manufacturing firms to develop “interest coverage ratio” ranges for each rating class.

We then estimate a spread over the long term bond rate for each ratings class, based upon yields at which these bonds trade in the market place.

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 15

Interest Coverage Ratios and Bond Ratings

If Interest Coverage Ratio is Estimated Bond Rating> 8.50 AAA

6.50 - 8.50 AA

5.50 - 6.50 A+

4.25 - 5.50 A

3.00 - 4.25 A–

2.50 - 3.00 BBB

2.00 - 2.50 BB

1.75 - 2.00 B+

1.50 - 1.75 B

1.25 - 1.50 B –

0.80 - 1.25 CCC

0.65 - 0.80 CC

0.20 - 0.65 C

< 0.20 D

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 16

Spreads Over Long Bond Rate for Ratings Classes

Rating Coverage gtSpreadAAA 0.20%AA 0.50%A+ 0.80%A 1.00%A- 1.25%BBB 1.50%BB 2.00%B+ 2.50%B 3.25%B- 4.25%CCC 5.00%CC 6.00%C 7.50%D 10.00%

Rating Coverage gtSpreadAAA 0.20%AA 0.50%A+ 0.80%A 1.00%A- 1.25%BBB 1.50%BB 2.00%B+ 2.50%B 3.25%B- 4.25%CCC 5.00%CC 6.00%C 7.50%D 10.00%

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 17

Volatilities from “Transition Matrix”

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 18

Construction of Volatility Across Credit Horizons

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 19

Defaults and Recovery Rates

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 20

The Distribution of Returns

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 21

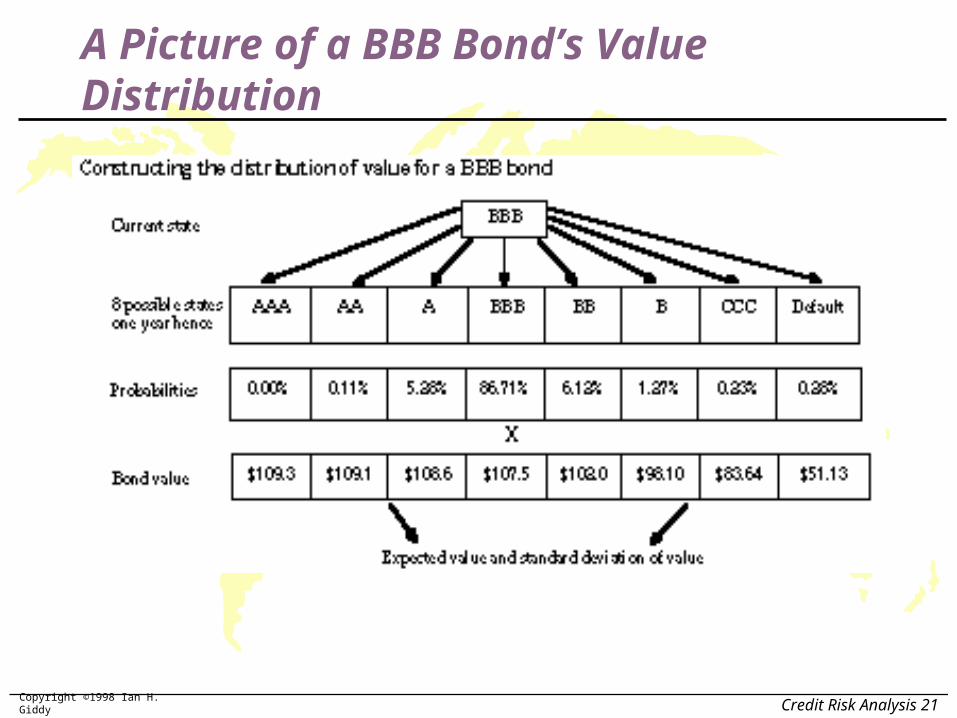

A Picture of a BBB Bond’s Value Distribution

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 22

Calculating Mean and Standard Deviation

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 23

CreditMetrics

creditmetrics.com

Copyright ©1998 Ian H. Giddy Credit Risk Analysis 29

Ian H. Giddy

Professor of Finance

Stern School of Business

New York University

44 West 4th Street, New York, NY 10012, USA

Tel 212-998-0332; Fax 212-995-4233

Email: [email protected]

World Wide Web: http://giddy.org