282

ANNUAL REPORT 2004 TOGETHER

| Date post: | 13-Apr-2017 |

| Category: |

Documents |

| Upload: | quarterlyearningsreports2 |

| View: | 155 times |

| Download: | 0 times |

ANNUAL REPORT 2004

TOGETHER

TOGETHER

We set ourselves ambitious targets in 2004, and accomplished a great deal. Our success wasattributable to the considerable efforts of each and every one of us, and it was all the more meaningful because we achieved it together: as a team, in our dialog with clients, across ourindividual businesses, and through a combination of our individual strengths.

The renowned Swiss photographic artist Beat Streuli (born 1957) captured

images of Credit Suisse Group employees at various international locations

during January and February 2005. The Group’s financial publications for

2005 are illustrated with the work that resulted from this project.

Titel: Ketan Mehta, Reby Gulcan, Torun Mathias, Robert Arsov – Mergers & Acquisitions, Credit Suisse First Boston, New York

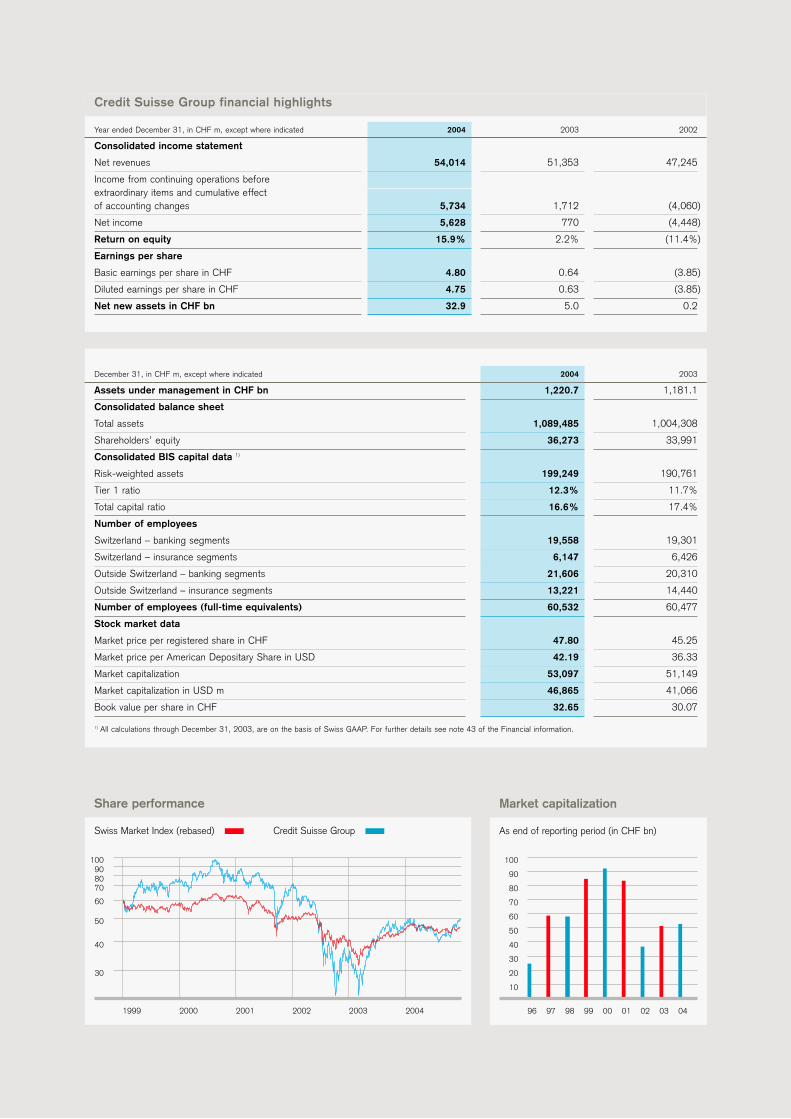

Credit Suisse Group financial highlights

Year ended December 31, in CHF m, except where indicated 2004 2003 2002

Consolidated income statement

Net revenues 54,014 51,353 47,245

Income from continuing operations before extraordinary items and cumulative effect of accounting changes 5,734 1,712 (4,060)

Net income 5,628 770 (4,448)

Return on equity 15.9% 2.2% (11.4%)

Earnings per share

Basic earnings per share in CHF 4.80 0.64 (3.85)

Diluted earnings per share in CHF 4.75 0.63 (3.85)

Net new assets in CHF bn 32.9 5.0 0.2

December 31, in CHF m, except where indicated 2004 2003

Assets under management in CHF bn 1,220.7 1,181.1

Consolidated balance sheet

Total assets 1,089,485 1,004,308

Shareholders’ equity 36,273 33,991

Consolidated BIS capital data 1)

Risk-weighted assets 199,249 190,761

Tier 1 ratio 12.3% 11.7%

Total capital ratio 16.6% 17.4%

Number of employees

Switzerland – banking segments 19,558 19,301

Switzerland – insurance segments 6,147 6,426

Outside Switzerland – banking segments 21,606 20,310

Outside Switzerland – insurance segments 13,221 14,440

Number of employees (full-time equivalents) 60,532 60,477

Stock market data

Market price per registered share in CHF 47.80 45.25

Market price per American Depositary Share in USD 42.19 36.33

Market capitalization 53,097 51,149

Market capitalization in USD m 46,865 41,066

Book value per share in CHF 32.65 30.07

1) All calculations through December 31, 2003, are on the basis of Swiss GAAP. For further details see note 43 of the Financial information.

96 97 98 99 00 01 02 03 04

10

20

30

40

50

60

70

80

90

100

Market capitalization

As end of reporting period (in CHF bn)

1999 2000 2001 2002 2003 2004

Share performance

Swiss Market Index (rebased) Credit Suisse Group

30

50

40

70

60

9080

100

Ticker symbols / Stock exchange listings

Bloomberg Reuters Telekurs

SWX Swiss Exchange/virt-x CSGN VX CSGN.VX CSGN,380

New York (ADS) 1) CSR US CSR.N CSR,065

1) 1 ADS represents 1 registered share.

CSG share ADS

Swiss security number 1213853 570660

ISIN number CH0012138530 US2254011081

CUSIP number 225 401 108

Financial calendar

Annual General Meeting Friday, April 29, 2005

First quarter results 2005 Wednesday, May 4, 2005

Dividend payment Friday, May 6, 2005

Second quarter results 2005 Wednesday, August 3, 2005

Third quarter results 2005 Wednesday, November 2, 2005

Ratings

Moody’s Standard & Poor’s Fitch Ratings

Credit Suisse Group

Short term – A-1 F1+

Long term Aa3 A AA-

Outlook Stable Stable Stable

Credit Suisse

Short term P-1 A-1 F1+

Long term Aa3 A+ AA-

Outlook Stable Stable Stable

Credit Suisse First Boston

Short term P-1 A-1 F1+

Long term Aa3 A+ AA-

Outlook Stable Stable Stable

Winterthur

Insurer Financial Strength A1 A- A+

Rating WatchOutlook Negative Stable Negative

Share data

December 31 2004 2003

Shares issued 1,213,906,217 1,195,005,914

Treasury shares (103,086,736) (64,642,966)

Shares outstanding 1,110,819,481 1,130,362,948

Share price

in CHF 2004 2003 2002

High (closing price) 49.50 48.70 73.60

Low (closing price) 37.35 20.70 20.60

ANNUAL REPORT 2004

The Business Review 2004 provides further insight into

the Credit Suisse Group business, strategy and market

environment from a management, client and employee

perspective. It is being published for the first time in

2005 and is targeted at a wide readership including

shareholders, clients and other parties with an interest

in the Group. Included in the Business Review is a

condensed presentation of the Group's results, which

should be read in conjunction with the financial

statements as disclosed in the Annual Report 2004.

BUSINESS REVIEW 2004

TOGETHER

Content

4 Message from the Chairman

6 Message from the Chief Executive Officer

9 INFORMATION ON THE COMPANY10 Credit Suisse Group

14 Credit Suisse

21 Credit Suisse First Boston

29 Winterthur

37 OPERATING AND FINANCIAL REVIEW38 Overview

40 Summary of Group results

41 Summary of segment results

43 Credit Suisse Group

50 Credit Suisse

51 Private Banking

53 Corporate & Retail Banking

56 Credit Suisse First Boston

57 Institutional Securities

62 Wealth & Asset Management

66 Winterthur

67 Life & Pensions

73 Non-Life

79 Corporate Center

81 RISK MANAGEMENT

109 FINANCIAL INFORMATION110 Consolidated financial statements

221 Parent company financial statements

231 CORPORATE GOVERNANCE

273 MAIN OFFICES

Message from the Chairman4

Dear shareholders

2004 marked another year of progress for Credit Suisse Group. We have delivered agood business and financial performance in the face of a mixed market environment,we also made some significant changes to our top management team andannounced our strategic plan drafted by the CEO, Oswald J. Grübel, and his teamand approved by the Board. There is much more to do, but we are now well on theway to achieving a sustainable position as a leading competitor in the global financialmarketplace.

We reported net income of CHF 5.6 billion for the full year. The Board of Directorswill propose a dividend of CHF 1.50 per share to the Annual General Meeting onApril 29, 2005 and will also ask for approval for a share buyback program for up toCHF 6 billion.

The context for our strategic deliberations was our belief that the financial servicesindustry will continue to experience change driven by technology and theglobalization of markets. This means that the business environment will becomemore complex and less predictable and this change will continue to transform theneeds of our clients. Our continued success will depend on a swift and flexiblestrategic response. We believe that we have put in place an appropriate strategicplan and the management capability to deliver it.

This plan will enable us to unlock the considerable experience and knowledge offinancial markets from across Credit Suisse Group to fulfill the expectations of ourclients. We will do this by managing our banking businesses as a fully integratedbank rather than separate business units. This will enable us to use our resourcesmore effectively and allow our people to work together on a global basis. We willhave three banking business areas: private client services, corporate and investmentbanking and asset management, supported by integrated corporate center functions.The transition to the new structure will be completed at the latest by the end of2006.

In addition to our plans for integration we have identified priorities for our growingeach of our businesses. In private banking, we intend to expand our position as aleading global institution. We also plan to strengthen the position in our core Swissmarket, both in private and in corporate and retail banking. In investment banking,we are focusing on profitable growth and want to be among the leading institutionsoffering a wide spectrum of investment banking services worldwide. We use our

Walter B. Kielholz

Chairman of the

Board of Directors

Credit Suisse Group

Message from the Chairman 5

existing strengths more effectively and aim to expand our presence throughprofitable growth – particularly in Europe and Asia.

We also defined the strategy for our insurance business. Winterthur’s ability todeliver solid earnings has increased considerably. This was reflected in its results for2004. However, we believe that earnings at Winterthur could still further improve. Asthe integrated management of banking and insurance is no longer our strategy, wehave decided to manage Winterthur as a financial investment and prepare ourinsurance group – market conditions allowing – for a possible public offering.

During 2004 we made a number of changes to the executive team to ensure thatwe can realize the benefits of becoming a more integrated bank and implement ourgrowth plans. By mid-year, Oswald Grübel, who has been with Credit Suisse for over30 years and has an outstanding track record in both investment banking and privatebanking, became sole CEO of Credit Suisse group. John Mack left the Group at theend of his three-year contract in early July 2004. John Mack had joined CreditSuisse Group as CEO of Credit Suisse First Boston in 2001 and was appointed Co-CEO of Credit Suisse Group as per January 1, 2003. I would like to thank Mr. Mackfor his most valuable contributions to both the restructuring of Credit Suisse FirstBoston and the turnaround of the Group.

Walter Berchtold was appointed CEO of Credit Suisse and Brady Dougan CEO ofCredit Suisse First Boston. Both have occupied leading positions within our companyfor many years. In addition, our executive team gained two experienced managersfrom outside the company with the appointment of Urs Rohner as General Counseland Head of the Corporate Center and Renato Fassbind as Chief Financial Officer.Together with Leonhard Fischer, CEO of Winterthur, these individuals form thecommittee of the Group Executive Board, which provides the leadership of CreditSuisse Group.

The Board is confident that following our return to profitability in 2003, a goodfinancial result in 2004 has provided further reassurance that we are on track tocontinue to deliver attractive returns to our shareholders.

Our financial results show that we have a solid operating business and strong capitalbase upon which to build our strategy. It is equally important for us to have acorporate culture that is able to adapt successfully to the rapid changes within ourindustry and turn it to our clients’ advantage. Consequently, foresight, a willingnessto innovate, and an ability to accurately assess and take a disciplined approach torisk are all factors governing success in our business. These are qualities, which ouremployees have demonstrated in 2004, and I would like to thank them all for theirconsiderable commitment and contribution to the Group. We want to be at the veryforefront of our industry and, together, we are working to create a ’one bank’organization and culture that will generate real benefits for our clients andshareholders.

Yours sincerely

Walter B. Kielholz

March 2005

Message from the Chief Executive Officer6

Dear shareholders

The year 2004 put the flexibility of the financial services industry to the test: marketsentiment improved in the first half, only to be replaced by a lack of clear trends,reduced volumes and historically low volatility in the second half – compounded bythe weakening of the US dollar. Our Group successfully navigated these challengesand generated net income of CHF 5.6 billion for 2004 – despite an increase inprovisions related to the sale of Winterthur International, a loss on the disposal of aminority holding and severance costs at Credit Suisse First Boston. This good 2004result underscores our ability to capture opportunities and to capitalize on change ina mixed market environment.

Credit Suisse Group’s overall 2004 performance reflects progress on many fronts.All of our banking units reported increased profitability compared to 2003, driven inpart by efficiency gains and cost containment efforts. Improved business momentumwas also evident at Winterthur, which delivered solid 2004 results and madecontinued progress towards sustained profitability.

Our Private Banking business posted strong annual results in 2004, due primarily toasset-driven revenue generation and efficiency improvements. The segment’s strongfull-year net income was accompanied by excellent gross margins and healthy netnew asset inflows across all regions. While cost containment and processenhancement remained a priority throughout the year, Private Banking continued toinvest in key growth opportunities in selected international markets.

Corporate & Retail Banking recorded very good net income in 2004, coupled with animproved cost/income ratio and an increased return on average allocated capital.The enhanced profitability of our business with private and corporate clients inSwitzerland was mainly attributable to efficiency improvements and a low level ofcredit provisions. Moreover, by reallocating resources to the client segments offeringthe greatest potential, Corporate & Retail Banking succeeded in strengthening itsclient focus and in improving the quality of its products and services.

Credit Suisse First Boston reported improvements in its financial performance in2004, with moderate revenue growth and continued cost discipline in both of itssegments. At Institutional Securities, the year-on-year rise in net income wasattributable to higher fixed income and equity trading results, higher debtunderwriting revenues, gains on legacy investments, lower credit provisions and

Oswald J. Grübel

Chief Executive Officer

Credit Suisse Group

Message from the Chief Executive Officer 7

lower income tax expense. Meanwhile, improved 2004 net income at Wealth & AssetManagement was driven primarily by private equity investment-related gains.

Credit Suisse First Boston also continued to lay the foundations for the futuredevelopment of the business. As well as implementing key organizational changes,the firm launched a new strategy aimed at achieving a leadership position in selectedmarkets by delivering a more focused franchise.

Our insurance business, Winterthur, recorded a solid result in 2004. Both the Life &Pensions and the Non-Life segment delivered improved underwriting results –reflecting cost containment and efficiency improvements – and stable investmentincome with lower levels of realized losses. Despite being impacted by theaforementioned increase in provisions relating to the sale of Winterthur International,these results underscore that Winterthur is advancing towards its goal of sustainedprofitability.

The Group’s positive 2004 performance enabled it to further strengthen its capitalbase – resulting in a consolidated BIS tier 1 ratio of 12.3% as of December 31,2004. This will not only enable us to fund our ambitious growth strategy but will alsoallow us to return capital to our shareholders.

In view of the progress we have achieved during the 2004 financial year and ourproven ability to respond rapidly, flexibly and – in particular – creatively to marketdevelopments, I believe that we have a strong basis upon which to implement ourkey strategic objectives. Moreover, with the unfaltering commitment and expertise ofour employees, I am confident that we will continue to satisfy the diverse needs ofour clients and the expectations of our shareholders going forward.

Yours sincerely

Oswald J. Grübel

March 2005

This page has been intentionally left blank.

INFORMATION ON THE COMPANY

Credit Suisse Group

Institutional Securities

Wealth & Asset Management

Life & Pensions

Non-Life

Credit Suisse First Boston Winterthur

Credit Suisse First Boston legal entity Winterthur legal entity

Credit Suisse

Private Banking

Corporate & Retail Banking

Credit Suisse legal entity

Information on the company Credit Suisse Group10

INFORMATION ON THE COMPANY

Credit Suisse Group

OVERVIEW

Credit Suisse Group is a global financial services company domiciled in Switzerland.The activities of Credit Suisse Group are structured into three main business units,described below.

CREDIT SUISSE GROUP STRUCTURE

Credit Suisse Group comprises three business units with six reporting segments:Credit Suisse, including the Private Banking and Corporate & Retail Bankingsegments; Credit Suisse First Boston, including the Institutional Securities andWealth & Asset Management segments; and Winterthur, including the Life &Pensions and Non-Life segments.

The structuring of the organization into three business units resulted from acorporate reorganization in July 2004 designed to accelerate the integration of thecore businesses and to sharpen the Group’s strategic focus. The new structurecame into effect on July 13, 2004. The reorganization also included the designationof a single CEO and the elimination of the Credit Suisse Financial Services businessunit. The individual financial reporting segments remained unchanged.

The organization presented below reflects the segment structure in place as of July2004.

Credit Suisse Group

Credit Suisse

PRIVATE BANKING

CORPORATE & RETAIL BANKING

INSTITUTIONAL SECURITIES

WEALTH & ASSET MANAGEMENT

LIFE & PENSIONS

NON-LIFE

Credit Suisse First Boston Winterthur

Credit Suisse legal entity Credit Suisse First Boston legal entity Winterthur legal entity

Information on the company Credit Suisse Group 11

Credit SuisseThe Credit Suisse business unit is a leading provider of comprehensive financialservices in Europe and several other markets globally. Under its main brands CreditSuisse and Credit Suisse Private Banking, it offers comprehensive financial servicesto private and corporate clients.

Credit Suisse operates through two segments, Private Banking and Corporate &Retail Banking:

– Private Banking, providing high-net-worth individuals in Switzerland and innumerous other markets around the world with wealth management products andservices.

– Corporate & Retail Banking, offering banking products and services tocorporate and retail clients in Switzerland.

Credit Suisse First BostonThe Credit Suisse First Boston business unit serves global institutional, corporate,government clients and high-net-worth individuals as a financial intermediary,providing a broad range of products and services including securities underwriting,sales and trading, financial advisory, private equity investments, full servicebrokerage, derivatives and risk management products, asset management andresearch.

Credit Suisse First Boston operates through two segments, Institutional Securitiesand Wealth & Asset Management:

– Institutional Securities, providing financial advisory and capital raising servicesand sales and trading for global users and suppliers.

– Wealth & Asset Management, offering international asset managementservices to institutional, mutual fund and private investors, making private equityinvestments and managing private equity funds, and providing financial advisoryservices to high-net-worth individuals and corporate investors.

WinterthurThe Winterthur business unit provides insurance and pension solutions for privateand corporate clients in Europe, North America and selected Asian markets.

Winterthur operates through two segments, Life & Pensions and Non-Life:

– Life & Pensions, offering life insurance products through multiple distributionchannels to private and corporate clients in Switzerland and selected markets inEurope and Asia.

– Non-Life, providing non-life insurance products to private and small and medium-sized corporate clients in Switzerland, North America and certain markets inEurope.

Information on the company Credit Suisse Group12

Corporate Center The Credit Suisse Group Corporate Center performs typical holding companyfunctions for the benefit of the Group as a whole and includes parent companyoperations, certain centrally managed functions and consolidation adjustments.

The Corporate Center consists of the following functions reporting directly to theGroup’s Chief Executive Officer, with the exception of Group Internal Audit, whichreports to the Audit Committee:

– Group-level functions assigned to the Group General Counsel and Head of theCorporate Center, including Legal and Compliance, Human Resources,Communications and Corporate Development;

– Group-level functions assigned to the Chief Financial Officer, includingAccounting and Financial Reporting, Tax, Capital and Liquidity Management andInvestor Relations;

– Group Risk Management; and– Group Internal Audit.

ACQUISITIONS AND DIVESTITURES

In December 2004, Credit Suisse Group agreed to sell its 19.9% stake in theprivate equity activities of Warburg Pincus, which it acquired in July 1999. Theinvestment was repurchased by Warburg Pincus with effect from January 1, 2005.

OUTSOURCING OF SERVICES

Where the outsourcing of services through agreements with external serviceproviders is considered significant under the terms of Swiss Federal BankingCommission Circular 99/2 “Outsourcing,” those agreements comply with allregulatory requirements with respect to business and banking secrecy, dataprotection and customer information. Credit Suisse Group has no significantoutsourcing relationships with external service providers.

STRATEGY

Credit Suisse Group’s strategy is to strengthen its global position in asset gatheringand investment banking by being a leader in private wealth management, globalinstitutional asset management, retail banking in Switzerland and global investmentbanking. The Group intends to meet its financial targets by accelerating organicgrowth and strengthening its competitive position in its core banking businesses. TheGroup will continue to manage Winterthur in order to generate profitable growth. Inaddition, Credit Suisse Group expects to continue its role as a leader in the evolutionof the global financial services industry.

Information on the company Credit Suisse Group 13

Business unit strategies Within the framework of the overall Group strategy, the three business units alsopursue their own more specific strategies designed to meet the needs of theircustomers, as well as their particular operating and competitive environment. Thesestrategies are discussed in more detail in the respective descriptions of the businessunits.

RealignmentA key strategic initiative announced in December 2004 is the formation of a fullyintegrated bank, with three distinct lines of business: Private Client Services,Corporate and Investment Banking, and Asset Management. Components of thisinitiative, which is expected to be completed by the end of 2006, include a mergerof the two main banking legal entities, greater emphasis on Corporate Centerfunctions and the focus of management on the Group as a whole, to enhancecooperation across the whole company. In addition, Asset Management activitiesthroughout the Group will be brought together and thereby positioned as a corestrength and will represent a key component of our value proposition in all ourbusinesses.

COMPANY HISTORY AND LEGAL STRUCTURE

The history of Credit Suisse Group dates back to the formation of SchweizerischeKreditanstalt, founded in 1856. The first branch was opened in Basle in 1905 andthe first branch outside of Switzerland was opened in New York in 1940. In 1978, acooperation with First Boston, Inc. began and in 1990, a controlling stake wasacquired. A controlling stake in Bank Leu was purchased in 1990, SchweizerischeVolksbank was purchased in 1993, Neue Aargauer Bank was purchased in 1994,and the acquisition of Winterthur took place in 1997. Another key acquisition wasDonaldson, Lufkin & Jenrette Inc., or DLJ, in 2000.

Credit Suisse Group’s three business units, Credit Suisse, Credit Suisse First Bostonand Winterthur, are aligned within the following three principal legal entities:

– Credit Suisse (Private Banking and Corporate & Retail Banking segments);– Credit Suisse First Boston (Institutional Securities and Wealth & Asset

Management segments); and – Winterthur (Life & Pensions and Non-Life segments).

The Board of Directors of Credit Suisse Group, Credit Suisse and Credit Suisse FirstBoston have resolved to merge legal entity Credit Suisse with legal entity CreditSuisse First Boston in Switzerland during the second quarter of 2005.

Credit Suisse Group is registered as a corporation in the commercial register of, andhas registered offices in, Zurich, Switzerland. The address of the principal executiveoffices is: Paradeplatz 8, P.O. Box 1, CH-8070, Zurich, Switzerland; the telephonenumber is: +41 44 212 1616.

Information on the company Credit Suisse14

Credit Suisse

OVERVIEW

The Credit Suisse business unit is comprised of the Private Banking and Corporate& Retail Banking segments. These two segments offer comprehensive financialservices to private and corporate clients.

As discussed in the Credit Suisse Group section above, as part of the corporatereorganization in July 2004, the banking and insurance businesses of the formerCredit Suisse Financial Services business unit were reorganized under the CreditSuisse and Winterthur business units, respectively.

– Private Banking provides high-net-worth individuals in Switzerland and innumerous other markets around the world with wealth management products andservices. Private Banking is one of the largest private banking operationsworldwide, with a leading client-centric service model and recognized innovationcapabilities.

– Corporate & Retail Banking offers banking products and services to corporateand retail clients in Switzerland. Corporate & Retail Banking is the second-largestbank in Switzerland, with a nationwide branch network and leading multi-channeldistribution capabilities.

As of December 31, 2004, the Credit Suisse distribution network consisted of 214branches serving Corporate & Retail Banking and Private Banking clients inSwitzerland and approximately 50 Private Banking locations abroad.

As a result of the reorganization in 2004, Credit Suisse is structured as follows:

– Four dedicated front-office divisions: one division serving Corporate & RetailBanking clients and three divisions serving Private Banking clients (PrivateBanking Switzerland, Private Banking International and Private Banking Europe);

– Four middle and back-office divisions, each serving all front-office divisions:Investment Management, Trading & Sales, Information Technology andOperations;

– A Chief Operating and Chief Financial Officer division (COO & CFO), whichincludes the Treasury function and nearly all Corporate Center functions of theCredit Suisse business unit;

– Three departments for Marketing, Human Resources and the Business School,which report directly to the CEO of Credit Suisse; and

– Four separately branded private banks reporting directly to the CEO of CreditSuisse: Bank Leu, Clariden Bank and Bank Hofmann, all headquartered inZurich; and BGP Banca di Gestione Patrimoniale, headquartered in Lugano.

Client relationships were not affected by this reorganization.

Information on the company Credit Suisse 15

STRATEGY

Credit Suisse’s mission is to be the leading global private bank and the leading bankin Switzerland in terms of client satisfaction, employee excellence and shareholderreturns.

Credit Suisse’s strategy is to:

– Invest in markets and businesses with above-average growth or growth potential;– Secure its earnings strength by further expanding its position in the Swiss home

market;– Secure long-term growth by diversifying its geographic mix;– Lead the industry in terms of innovative products and solutions;– Further develop an integrated business model across segments and divisions by

leveraging client relations, products and infrastructure;– Finance growth investments through continuous productivity improvements; and– Continue to be an important cash flow contributor to Credit Suisse Group.

With respect to its two segments, Credit Suisse pursues the following strategies:

Private Banking intends to expand in the international onshore and offshore business(Asia, Middle East, Central & Eastern Europe and Latin America) and to growprofitably in the European onshore business where it aims to reach break-even by2007. In addition, Private Banking aims to maintain a strong position and to increaseits profitability in the European offshore business. Furthermore, Private Bankingintends to expand its market share in the Swiss onshore business by a greater focuson increasing its share of managed assets (discretionary mandates, funds, structuredproducts) and by further building on premium positioning in value-added clientservices.

Corporate & Retail Banking intends to gain market share in the high-end retailbusiness through attractive anchor products such as private mortgages andinvestment products. Furthermore, Corporate & Retail Banking aims to increase itsprofitability in the low-end retail business and to grow in the consumer financebusiness including the credit card business. In addition, the segment is looking toexpand its strong position with large corporate clients and to further gain marketshare with small and medium-sized corporate clients that have attractive risk-returnprofiles. Corporate & Retail Banking intends to have a superior positioning in value-added client services, aligned to specific client needs for each of the above-mentioned client segments.

PRIVATE BANKING

Overview Private Banking is one of the world’s largest private banking organizations, withbranches in Switzerland and numerous international locations, and providescomprehensive wealth management products and services to high-net-worthindividuals through a network of relationship managers and specialists. It also offersvarious services directly over the Internet through its portal located at www.credit-suisse.com/privatebanking.

Information on the company Credit Suisse16

Each one of the approximately 600,000 Private Banking clients has a designatedrelationship manager as a primary point of contact. As of December 31, 2004, thePrivate Banking segment had approximately 12,000 employees worldwide, of whichapproximately 2,600 were relationship managers and financial advisors. As of thatdate, Private Banking had CHF 539.1 billion of assets under management.

Private Banking has three front-office divisions, focusing on clear strategic marketpriorities:

– Private Banking Switzerland comprises the Swiss domestic market, internationalprivate clients from neighboring countries, and booking centers in Luxembourg,Guernsey, Monaco and Gibraltar;

– Private Banking International comprises international private clients in AsiaPacific, the Middle East, the Americas, Northern Europe, Eastern Europe, SouthAfrica and Iberia. It includes the Global Private Banking Center in Singapore, aswell as operations in Hong Kong, the Bahamas and Frye-Louis CapitalManagement, Inc. in Chicago. In addition to these activities, Private BankingInternational operates Credit Suisse Trust, which provides independent advice anddelivers integrated wealth management solutions to ultra high-net-worthindividuals, as well as Credit Suisse Advisory Partners, which offers highlydeveloped special financing, corporate advisory and family office services to ultrahigh-net-worth individuals; and

– Private Banking Europe comprises onshore banking operations in the five largestEuropean markets: Germany, Italy, the United Kingdom, France and Spain, andalso includes JO Hambro Investment Management Limited in London.

The four separately branded private banks – Bank Leu, Clariden Bank, BankHofmann and BGP Banca di Gestione Patrimoniale – also form part of the PrivateBanking segment.

Private Banking intends to pursue the following in order to implement its strategy:

– Expand geographic coverage by opening or upgrading further locations; – Strengthen international management capabilities and resources;– Continue to hire and develop senior relationship managers for key growth

markets;– Further expand capabilities and offerings for the ultra high-net-worth individuals

segment;– Leverage the client base of other Credit Suisse Group businesses;– Further expand investment product skills and offerings;– Further develop and deploy Credit Suisse’s structured advisory process;– Benefit from continued investments in client relationship management and

workplace tools; and– Further improve customer experience along all points of contact and interfaces.

Products and services Private Banking offers customized solutions that address the full range of clients’wealth management needs. This includes providing comprehensive financial advicefor each phase of life, as well as addressing issues relating to clients’ non-liquidassets such as business and property interests.

Information on the company Credit Suisse 17

In 2004, Private Banking fully integrated and further improved its “Private BankingAdvisory Process” in Switzerland. Using a structured approach, the client’s personalfinances are analyzed and an investment strategy is prepared based on the client’srisk profile, service profile and level of “free assets” after dedicated assets are setaside to cover the client’s fixed and variable liabilities. In accordance with theInvestment Committee’s guidelines, Private Banking’s investment professionalsdevelop their specific investment recommendations. The subsequent implementationand monitoring of the client’s portfolio are carried out by the relationship managerusing a continuously improving financial tool, which is closely linked to PrivateBanking’s award-winning customer relationship management platform.

Private Banking’s core service is managing liquid assets through investment adviceand discretionary asset management. Investment advice covers a wide range oftopics from portfolio consulting to advice on single securities. For clients who areinterested in a more active management of their portfolios, Private Banking offersdedicated investment consultants who continuously analyze the latest marketinformation to develop investment recommendations, enabling clients to takeadvantage of market opportunities across all asset categories. For clients with morecomplex requirements, Private Banking offers investment portfolio structuring andthe implementation of individual strategies, including a wide range of investments instructured products, alternative investments, private equity and real estate.

Discretionary asset management is designed for clients who wish to delegate theresponsibility for investment decisions to the bank. Private Banking offers a numberof standardized portfolio management mandates linked to the client’s riskpreferences and reference currency. Four types of mandates are offered: Classic,Funds & Alternative Investments, Total Return Strategy and Premium. Depending onthe type of mandate, direct investments, investments in funds or investments inalternative products are executed. Predefined investment strategies such as capitalpreservation and growth or current return, and customized solutions that meetclients’ identified investment goals, are offered within the Premium Mandate.

Private Banking remains at the forefront of product innovation and open productplatforms. The latter allows us to offer tailor-made, client-specific solutions, whichare bundled from a wide range of own and third-party best-in-class products andservices. Structured investment products are intended to provide market-neutralinvestments and access to Private Banking’s own and third-party international assetmanagers through a fund-of-funds approach. Market-neutral means that assetmanagers pursue investment strategies that offer positive returns in economicclimates in which traditional assets perform poorly. Private Banking currently offersmutual fund products covering around 2,500 funds from around 55 fund providers.

For financing needs, Private Banking offers two basic financing services, securities-backed financing (repo-business) and margin lending, which allows clients to borrowagainst their investment portfolios, and real estate financing of clients’ residentialproperties.

Private Banking’s advisory services comprise tax planning, pension planning andwealth and inheritance advice, including the establishment of Private Banking trustsand foundations, as well as advice on life insurance. Private Banking’s corporateadvisory services are aimed at entrepreneurs seeking to sell their businesses or toraise additional capital. In either case, Private Banking provides valuation services

Information on the company Credit Suisse18

and seeks to find potential investors in the public and private markets. PrivateBanking also offers “Family Office” services, a variety of tailor-made products andadvice for individuals and families generally with minimum assets of USD 50 million.

Marketing and distributionPrivate Banking has a global franchise and a strong presence in Europe, Asia, LatinAmerica and the Middle East. As of December 31, 2004, Private Banking served itsclients through approximately 120 locations around the world, of which approximately70 locations are in Switzerland (not including the locations of Bank Leu, BankHofmann, Clariden Bank and BGP Banca di Gestione Patrimoniale).

In 2004, Credit Suisse opened offices in various locations (including Moscow, Jerseyand Brazil). Offices in Bangkok and Dubai are in the process of being opened.Credit Suisse is the first foreign bank to have been granted a license to offer fullPrivate Banking services in the Dubai International Financial Centre starting in April2005. This branch will offer onshore and offshore services as well as Sharia-compliant banking services.

Operating environment and competitionOperating environmentCredit Suisse expects reduced, but still significant, growth rates in the privatebanking market in the near future. Growth is expected to be higher in onshore thanin offshore markets. This is the result of greater political stability in manyindustrialized and newly industrialized countries, as well as the deregulation of localmarkets coupled with tighter restrictions and ongoing pressure on traditional offshorelocations. The positive trends affecting the private banking industry over the nextseveral years are expected to include a growing demand for pension provisions,which can no longer be guaranteed through general social security. As a result,governments will increasingly encourage the accumulation of private wealth. Inaddition, entrepreneurs are using the services of private banks to diversify theirassets, while, at the same time, the next generation is inheriting an increasingvolume of wealth from the baby-boom generation.

Competitive pressure in the financial services industry remains high. The need toinvest in quality advice, product innovation and tools for front-office employeesunderlines this situation. In addition, the costs of doing business (e.g. compliance,accounting, competition for talented employees) are increasing. The Group expectsmain growth to be achieved through acquisitions of relationship managers and otherbanks as well as through net new asset generation.

CompetitionThe private banking market is highly fragmented and consolidation, especially inSwitzerland, is expected to proceed at a higher pace. Competitors in the privatebanking business include major financial institutions with dedicated private bankingactivities such as UBS, HSBC and Citigroup, as well as domestic banks within theirrespective markets. In the ultra high-net-worth individuals business, there are majorcompetitors including US investment banks, which are building upon their investmentbanking expertise and their client relationships. In the Swiss market, the largestcompetitor is UBS, followed by a number of independent private banks, as well asretail banks providing private banking services.

Information on the company Credit Suisse 19

CORPORATE & RETAIL BANKING

OverviewCorporate & Retail Banking serves both corporate and retail clients through a multi-channel distribution approach.

As of December 31, 2004, Corporate & Retail Banking had approximately 1.8million retail clients and approximately 100,000 corporate clients. As of that date,the segment had total loans of CHF 86.7 billion.

Corporate & Retail Banking intends to pursue the following in order to implement itsstrategy:

– Acquire new clients through attractive anchor products as well as targetedmarketing campaigns and events;

– Increase product penetration, tailored to the financial abilities of target clients, bydatabase marketing and by product bundling;

– Strengthen sales force effectiveness through focused training and targetedincentives;

– Continuously optimize branch network, upgrade e-banking offerings and extendthird-party distribution channels;

– Improve client service delivery through optimized end-to-end processes (higherquality, improvements in speed, and a lower cost base);

– Shift resources from mid and back-office functions to client teams and hiresales-oriented relationship managers;

– Launch further retail investment products and continuously improve lendingproduct offerings; and

– Invest in workplace tools, leveraging best-in-class technology from PrivateBanking.

The results of operations of Corporate & Retail Banking include the activities ofNeue Aargauer Bank, a separately branded regional retail bank in the canton ofAargau, Switzerland.

Products and servicesCorporate & Retail Banking offers corporate and retail clients a wide range offinancing products and services, such as mortgages, secured and unsecuredcorporate loans, trade finance, consumer loans, leasing and credit cards, as well asinvestment products and services, payment transactions, foreign exchange, lifeinsurance and pension products. Corporate & Retail Banking also offers clients e-banking solutions. In some cases, such as investment and insurance product sales,Corporate & Retail Banking sells these products jointly with other Credit SuisseGroup businesses.

In the credit card business, Corporate & Retail Banking has entered into a jointventure, Swisscard AECS, with American Express Travel Related Services Companyfor the purpose of issuing cards, processing transactions and acquiring merchants.As a market leader in credit cards in Switzerland in terms of turnover, SwisscardAECS offers Mastercard, Visa and American Express cards. These credit cards aredistributed through Corporate & Retail Banking and Private Banking sales channels,as well as through those of Swisscard AECS.

Information on the company Credit Suisse20

Corporate & Retail Banking offers sophisticated payment products tailored to theneeds of all customer segments. The variety of payment products ranges from IT-based, fully automated transaction solutions for large corporate clients to cost-efficient and convenient schemes for private clients.

For its lending products, Corporate & Retail Banking often requires a pledge ofcollateral. The amount of collateral required is determined by the type and amount ofthe loan, as well as the risk profile of the specific customer. As of December 31,2004, 84% of its loan portfolio was secured by collateral, including marketablesecurities, commercial and residential properties as well as bank and clientguarantees.

Marketing and distributionAs of December 31, 2004, Corporate & Retail Banking served its clients through214 banking branches, including 33 branches of Neue Aargauer Bank inSwitzerland. Corporate & Retail Banking markets its products to clients under theCredit Suisse brand, primarily through its branch network and direct channels,including the Internet and telephone banking.

Advisors for small and medium-sized corporate clients are based in 43 of theCorporate & Retail Banking branches. Large domestic corporate clients are servedthrough two regional offices in Zurich and Lausanne, Switzerland.

Operating environment and competitionOperating environmentThe Swiss corporate and retail banking industry is, to a significant extent, dependenton the overall economic development in Switzerland. For the retail and corporatebanking market, growth in line with the development of the economy is expected.Generally, Swiss retail banking clients have comparatively high incomes and savingsrates, resulting in a high demand for personal investment management. In recentyears, the Swiss private mortgage business has developed positively, and this trendis expected to continue. The home ownership rate in Switzerland is still low atapproximately 36%, thus offering further potential for mortgage business growth butdeclining margins may limit further revenue potential.

CompetitionIn the Swiss corporate and retail banking business, competition has increasedconsiderably over the past few years, especially in the field of private mortgages,which is characterized by an aggressive pricing policy by existing competitors andmarket entry of new competitors. The need to invest heavily in quality advisorycapabilities, product innovation and open architecture underlines this development.The largest competitor in the Swiss Corporate and Retail Banking segment remainsUBS. Other competitors include the Cantonal banks, many of which have stateguarantees, as well as regional savings and loan institutions, the Raiffeisen andother cooperative banks.

Information on the company Credit Suisse First Boston 21

Credit Suisse First Boston

OVERVIEW

Credit Suisse First Boston operates through two segments, Institutional Securitiesand Wealth & Asset Management. Effective January 1, 2004, Credit Suisse FirstBoston reorganized its operations by transferring the private equity and private fundsgroup activities previously in the Institutional Securities segment to the CSFBFinancial Services segment, which was renamed Wealth & Asset Management.Credit Suisse First Boston also reorganized the businesses within the InstitutionalSecurities segment along the lines of its investment banking and trading businessesand realigned the businesses within the Wealth & Asset Management segment tobring together its alternative investment activities, including the private equity andprivate funds groups.

The Credit Suisse First Boston business unit serves global institutional, corporate,government and high-net-worth clients as a financial intermediary, providing a broadrange of products and services including:

– Securities underwriting, sales and trading;– Financial advisory services;– Private equity investments;– Full service brokerage;– Derivatives and risk management products; – Asset management; and– Research.

The Institutional Securities segment provides financial advisory and capital raisingservices and sales and trading for global users and suppliers of capital. TheInstitutional Securities segment includes:

– Trading, which includes sales and trading in equity and debt securities andderivatives, and other related activities; and

– Investment Banking, which raises and invests capital, provides financial and otheradvisory services, manages and underwrites securities offerings and arrangesprivate placements.

The Wealth & Asset Management segment provides international assetmanagement services to institutional, mutual fund and private investors, makesprivate equity investments and manages private equity funds, and provides financialadvisory services to high-net-worth individuals and corporate investors. Wealth &Asset Management includes:

– The institutional asset management business, which operates under the brandCredit Suisse Asset Management and offers a wide array of products, includingfixed income, equity, balanced, money-market and indexed products;

– Alternative Capital, which invests in, manages and provides capital raising andother services to hedge funds, private equity funds and other alternativeinvestment vehicles; and

– Private Client Services, a financial advisory business which serves high-net-worthindividuals and corporate investors with a wide range of proprietary and third-party investment management products and services.

Information on the company Credit Suisse First Boston22

STRATEGY

Credit Suisse First Boston seeks to build on its improved financial results whilemaintaining a high priority on controls, risk management and the firm’s reputation.Credit Suisse First Boston’s strategy is geared towards winning where it chooses tocompete by delivering a more focused franchise. Credit Suisse First Boston expectsto achieve this by identifying and allocating resources to its most valuable clients andpursuing excellence in selected high-margin and strategically important services suchas leveraged finance, mergers and acquisitions, initial public offerings, derivativesand mortgage securitization, which are areas in which it has competitive strengthsand attractive growth opportunities. Credit Suisse First Boston believes increasedearnings and a stronger capital base will allow it to capture trading opportunitiesthrough extended, disciplined and diversified risk-taking. Institutional Securities andWealth & Asset Management will also make a number of structural changes withintheir various businesses to promote greater bottom-line accountability, improve costdiscipline and capitalize on the integration with the Group’s other bankingbusinesses. Credit Suisse First Boston intends to build a strong, performance-basedownership culture with a structured approach to attracting, developing and retainingtalent.

Consistent with this strategy, Institutional Securities will provide differentiated, full-service coverage to a smaller number of clients who value more service, establishmore unified offerings across certain fixed income and equity products and build onexisting leadership positions in selected areas. Key initiatives include the formationof a unified global proprietary trading group under a single management structureacross equity and fixed income and the creation of a consolidated derivativesstructuring group. Institutional Securities intends to grow its leading leveragedfinance business and commercial mortgage franchises by expanding into Europe.Institutional Securities also plans to build a commodities unit, continue to grow itsmortgage securitization business and add senior cross-product resources to topclients. In Investment Banking, Institutional Securities will adjust its coverage modelto better meet client needs, pursue a disciplined, client-centric approach to itsproduct offering and improve execution and client management. Specific coverageinitiatives include flexible client coverage with product coverage where appropriate,vertical integration of financial institutions coverage and increased share in atargeted subset of large-capitalization clients. In the Investment Banking area,Institutional Securities will focus on its high-margin, strategic products and create anintegrated capital markets group to deliver solutions to clients more effectively.

In Wealth & Asset Management, Credit Suisse First Boston will build on its leadingalternative capital franchise and leverage existing strengths to promote growth inCredit Suisse Asset Management and Private Client Services. In Alternative Capital,Credit Suisse First Boston expects to build on a broad diversity of funds, focusincreasingly on international markets, such as Asia, that display strong seculargrowth, spin out funds that could benefit from an independent platform and establisha new services platform for limited partners. Credit Suisse Asset Management willseek to grow European distribution, expand global product offerings, restoreprofitability to its U.S. franchise and streamline its Asian presence. Key initiatives inPrivate Client Services include leveraging a strong global brand and investmentbanking franchise, and building upon a leading position in volatility management.

Information on the company Credit Suisse First Boston 23

In Europe, Credit Suisse First Boston intends to strengthen its position by expandingsuccessful products such as leveraged finance and commercial mortgage-backedsecurities. In Asia, Institutional Securities and Wealth & Asset Management will buildon an already strong platform to capture business in a growth market. Initiatives inAsia will include the exploration of acquisition and joint venture opportunities,expanded derivatives capabilities throughout the region and strengthened positions inselected markets.

Credit Suisse First Boston is committed to complying fully with laws and regulationsand vigorously reviews ways to ensure continued professionalism and integrity in theconduct of its businesses. Furthermore, Credit Suisse First Boston remainscommitted to adhering to the highest professional standards and providing top-quality execution and investment performance, while developing and retainingoutstanding employees.

INSTITUTIONAL SECURITIES

OverviewInstitutional Securities provides financial advisory and capital raising services, andsales and trading for users and suppliers of capital around the world. The operationsof Institutional Securities include debt and equity underwriting and financial advisoryservices, and the equity and fixed income trading businesses.

For the year ended December 31, 2004, according to Thomson Financial,Institutional Securities ranked:

– Eleventh in global mergers and acquisitions advisory services in US dollar volumeof announced transactions;

– Sixth in global mergers and acquisitions advisory services in number ofannounced transactions;

– Fifth in US dollar value of global debt underwriting;– Second in US dollar value of global high-yield debt underwriting;– Eighth in US dollar value of global equity and equity-linked underwriting;– Third in US dollar value of global asset-backed financing; and– First in Swiss franc-denominated international debt issuances.

Products and servicesInstitutional Securities’ clients demand high-quality products and services for theirfunding, investing, risk management and financial advisory needs. In response tothese needs, Institutional Securities has developed a global product-based structuredelivered through regional teams.

The principal products and activities of Institutional Securities are:

Information on the company Credit Suisse First Boston24

Trading– Credit products, including investment-grade debt securities and credit derivatives;– Equity securities and equity derivatives, including convertible bonds;– Foreign exchange services including currency derivatives;– Interest rate products, including global government securities and interest rate

derivatives;– Leveraged finance, including high-yield and distressed debt;– Margin lending;– Market making in securities and options;– Matched book activities, in which the firm acts as an intermediary between

borrowers and lenders of short-term funds, mainly through repurchase and resaleagreements, to earn a positive spread between interest rates and to fundinventory positions;

– Money market instruments;– Prime services, including dealer-to-dealer financing, covering proprietary and

client short positions through securities borrowing and lending arrangements,margin lending, prime brokerage to attract client borrowings of cash andsecurities, the facilitation of financing, clearance, settlement and custody ofsecurities transactions and the provision of flexible solutions for clients to enablethem to use more than one broker for the execution of trading strategies but oneprime broker for efficient margining and consolidated position reporting;

– Proprietary trading;– Real estate activities, such as financing real estate and real estate-related

products and originating loans secured by commercial and residential properties;– Risk arbitrage in the equity securities of companies involved in publicly

announced corporate transactions;– Securities lending;– Securities, futures and options clearing services; – Structured products, including structuring and trading of asset-backed securities,

such as collateralized debt obligations, and origination, structuring and trading ofcommercial and residential mortgage-backed securities and mortgages; and

– Trading of syndicated, defaulted, distressed and other loans.

Investment Banking– Mergers and acquisitions and other advisory services, including corporate sales

and restructuring, divestitures and take-over defense strategy; and– Capital raising services, including equity and debt underwriting.

OtherOther products and activities of Institutional Securities that are not part of Trading orInvestment Banking are lending and legacy investments, including legacy privateequity and real estate investments and the distressed asset portfolios. Lendingincludes senior bank debt in the form of syndicated loans and commitments toextend credit to investment grade and non-investment grade borrowers.

Global investment researchCredit Suisse First Boston provides in-depth research on companies and industries,macroeconomics and debt strategy globally. The core strengths of Credit Suisse FirstBoston research include focused company and business model analysis andcustomized client service. Equity analysts perform differentiated informationgathering and value-added information processing and provide high-quality

Information on the company Credit Suisse First Boston 25

investment recommendations. Credit Suisse First Boston’s equity research alsoincludes extensive data resources, analytical frameworks and methodologies thatleverage the firm’s global platform and enable its analysts to customize theirproducts for institutional customers. Credit Suisse First Boston’s fixed incomeresearch provides clients with credit portfolio strategies and analysis, forecasts ofswaps and generic spread movements and outstanding credit strategy research forboth high-grade and high-yield products. Credit Suisse First Boston analysts’ in-depth understanding of markets, companies, investment instruments and local,regional and global economies forms a strong foundation for the firm’s innovativeweb-based analytical tools and technology.

Operating environment and competitionOperating environmentThe operating environment for Institutional Securities is expected to remainchallenging in the near term, reflecting expected continued slow securities marketgrowth in developed countries, fee compression and commoditization acrossproducts, and the ongoing importance of balance sheet commitments for clients. Inaddition, the regulatory environment remains difficult, with significant new reportingrequirements and increasing complexity in managing potential conflicts of interestacross its evolving businesses. Credit Suisse First Boston is well-positioned tobenefit from a number of trends in the industry. The move towards electronicexecution plays to the firm’s strengths in technology and its advanced executionservices platform. Credit Suisse First Boston is also likely to continue to benefit fromleveraging its leadership position with financial sponsors and alternative investments,both of which are expected to gain greater importance in the market.

CompetitionCredit Suisse First Boston faces intense global competition across each of itsbusinesses. Institutional Securities competes with investment and commercial banks,broker-dealers and other firms offering financial services. New entrants into thefinancial services and execution markets, such as commercial banks and technologycompanies, have contributed to further market fragmentation, fee and spreadcompression and product commoditization. In addition, Credit Suisse First Bostonfaces continued competitive pressure to make loans or commit capital to clients.

Information on the company Credit Suisse First Boston26

WEALTH & ASSET MANAGEMENT

OverviewWealth & Asset Management provides international asset management services toinstitutional, mutual fund and private investors, makes private equity investments andmanages private equity funds, and provides financial advisory services to high-net-worth individuals and corporate investors.

Credit Suisse Asset Management is a leading global asset manager focusing oninstitutional, investment fund and private client investors, providing investmentproducts and portfolio advice in three regions: the Americas, Asia Pacific andEurope. With CHF 386.7 billion in assets under management at December 31,2004, Credit Suisse Asset Management has investment capabilities in all majorasset classes, including equities, fixed income and balanced products.

Alternative Capital invests in, manages and provides capital raising and otherservices to hedge funds, private equity funds and other alternative investments.

Private Client Services serves high-net-worth and corporate investors with significantfinancial resources and specialized investment needs. Private Client Services had246 investment advisors and managed or advised clients on approximately CHF 59.1billion in assets as of December 31, 2004.

Products and servicesThe following is a discussion of the key global products and services of Wealth &Asset Management and the businesses through which they are delivered.

Asset management and advisory servicesThe asset management business offers its clients discretionary asset managementservices through segregated or pooled accounts. The investment policies of portfoliomanagers are generally focused on providing maximum return within the investor’scriteria, while maintaining a controlled risk profile and adherence to high-qualitycompliance and investment practices. The advisory services of the assetmanagement business include advice on customized investment opportunities, newproduct and risk management strategies and global investment reporting. Globalinvestment reporting involves the use of a global custodian, acting as a centraldepositary for all of a client’s securities. Once custody has been centralized, clientsare offered a series of value-added services, including cash management, securitieslending, performance measurement and compliance monitoring. Clients may choosefrom a wide array of products, including:

– Fixed income and equity products in local and global markets;– Balanced products, comprising a mixed portfolio of fixed income and equity

investments according to pre-defined risk parameters set by the customer or theinvestment guidelines of the fund;

– Money market products in multiple currencies;– Quantitative indexed products;– Derivatives and commodities; and– Real estate portfolio management.

Information on the company Credit Suisse First Boston 27

FundsThe asset management business offers a wide range of open-end funds. Thesefunds are marketed under the main brand name Credit Suisse. The largest complexof funds, which is domiciled in Luxembourg and marketed mainly in Europe, includesa full range of equity, balanced, fixed income and money market funds. In addition tothese pan-European mutual funds, the asset management business offers domesticregistered funds in the United States, Switzerland, the United Kingdom, Germany,Italy, France, Poland, Japan and Australia.

The asset management business acts primarily as a wholesale distributor of mutualfunds, and the majority of the Credit Suisse brand funds are marketed through ourother businesses and third-party distributors, including third-party banks andinsurance companies and other financial intermediaries.

Alternative CapitalAlternative Capital invests in, manages and provides capital raising and otherservices to, hedge funds, private equity funds and other alternative investmentvehicles. Alternative Capital includes the private equity group, the private fundsgroup and the capital markets group.

The private equity group manages a wide array of private equity funds includingleveraged buyout funds, mezzanine funds, real estate funds, secondary funds andfunds of funds. The private equity group invests primarily in unlisted or illiquid equityor equity-related securities in privately negotiated transactions, making investmentsacross the entire capital structure, from venture capital equity to investments in thelargest leveraged buyouts. In addition to debt and equity investments in companies,the private equity group invests in real estate and third-party-managed private equityfunds. Investments are made directly or through a variety of investment vehicles.

The private funds group raises capital for hedge funds, private equity funds andreal estate funds.

The capital markets group has direct hedge funds and invests in hedge funds offunds and collateralized debt obligations.

The strategic objectives of Alternative Capital include creating and growing aportfolio of investment management businesses for alternative assets (includingprivate equity, real estate and hedge funds) that generate attractive returns oncapital and provide a full array of product offerings to alternative asset investors.Alternative Capital intends to launch new businesses and expand its capabilitiesglobally. Alternative Capital also intends to spin out certain funds (including theCredit Opportunities Fund, the Diversified Credit Strategies Fund and the Sproutfunds) that could benefit from an independent platform. Alternative Capital has alsodetermined that certain investment professionals from the private equity business willestablish independent private equity firms to provide certain consulting services tothe Merchant Banking Partners funds, which Alternative Capital will continue tomanage as general partner of the funds. Following these transactions, AlternativeCapital intends to maintain significant investment commitments and financialinterests in, and strategic relationships with, each of these funds.

Information on the company Credit Suisse First Boston28

Private Client ServicesThe Private Client Services business offers a range of services, including brokerage,hedging and sales of restricted securities. Private Client Services also offers itsclients a wide range of investment management products, including third-party-managed accounts and alternative investments.

Operating environment and competitionOperating environmentThe operating environment for asset management improved somewhat during thelast year as equity indices generally posted gains and interest rates remained low,particularly in the United States. The demographic profile of most developedcountries suggests medium-term growth opportunities as aging populations seek toinvest for retirement. Nevertheless, the continuing development of markets makes itincreasingly difficult for active asset managers to outperform, and the regulatoryenvironment for mutual funds remains uncertain. Structured and alternativeinvestments are expected to continue to gain in importance.

CompetitionIn asset management, Credit Suisse First Boston faces competition primarily fromretail and institutional fund managers. Passive investment strategies are gainingshare at the expense of active managers as markets develop, and a larger share ofnew investment flows are being directed to a small number of fund managers.Competition for attractive alternative investments, including private equityinvestments, will likely remain intense and contribute to increasingly large privateequity investments.

Information on the company Winterthur 29

Winterthur

OVERVIEW

The Winterthur business unit consists of the Life & Pensions and Non-Lifesegments. The two segments offer insurance and pension solutions for private andcorporate clients.

As discussed in the Credit Suisse Group section above, as part of the corporatereorganization in July 2004, the banking and insurance businesses of the formerCredit Suisse Financial Services business unit were reorganized under the CreditSuisse and Winterthur business units, respectively.

– Life & Pensions offers life insurance products through multiple distributionchannels to private and corporate clients in Switzerland and other markets inEurope and Asia; and

– Non-Life offers non-life insurance products to private and small and medium-sized corporate clients in Switzerland, North America and certain markets inEurope.

Both segments are market leaders in Switzerland and hold solid market positions inBelgium, Spain and Germany.

In 2004, Winterthur completed the following reorganizations and disposals:

– First, Winterthur restructured its Life & Pensions and Non-Life organization inSwitzerland, bringing management responsibility for the unified organizationtogether. This reorganization is more in line with current customer requirementsand is intended to improve operating efficiency;

– Second, Winterthur put its Life & Pensions cross-border businesses in Bermudaand Luxembourg into run-off; and

– Finally, Winterthur divested various operations in the course of the year, includingPersonal Pension Management Limited (PPML), its Life & Pensions subsidiary ofWinterthur Life UK, which manages pension services; Rhodia Assurances S.A,the French Non-Life subsidiary; L’Unique Compagnie d’Assurances Générales,one of its two Canadian operations, based in Quebec; and the Dutch branch ofLes Assurés Réunis (LAR), Belgium. These divestitures reflect its strategy ofstreamlining its international business portfolio, thereby focusing more strongly onits principal markets, and taking advantage of opportunities for growth andprofitability.

Information on the company Winterthur30

STRATEGY

Winterthur’s life and non-life operations expect to maintain their focus on selectedcore markets that are believed to offer the best opportunities to achieve scale andprofitability. In addition, Winterthur aims to further develop its active approach toinvestment management, continue innovation in asset/liability matching and tocontinue improvements in claims and cost management efficiency.

LIFE & PENSIONS

Overview Winterthur’s Life & Pensions segment provides life insurance and pension solutionsfor private and corporate clients through multiple distribution channels.

The principal market units of the Life & Pensions segment are in Western Europe,where the focus is on Switzerland and Germany, and, to a lesser extent, the UnitedKingdom, Belgium, Spain and the Netherlands. In addition, it has operations inCentral and Eastern Europe and in selected Asian markets. All Life & Pensionsoperations are managed as part of the combined Life & Pensions and Non-Lifemarket units in the individual countries. The merger of the Life & Pensions and Non-Life operations in Switzerland took place in 2004. In terms of 2003 total businessvolume, Life & Pensions ranked as the eleventh largest life insurer in Europe.

Within its home market of Switzerland, Life & Pensions was the leading provider oflife insurance, based on 2003 total business volume. The majority of total businessvolume of the Swiss market unit is derived from traditional group life business.

The Life & Pensions operations in Germany principally sell traditional insuranceproducts to individual clients. In the United Kingdom, Life & Pensions offers a widerange of unit-linked products and is one of the leading providers of tailor-madepersonal pension schemes, predominantly for affluent private clients.

The majority of total business volume in Belgium relates to the traditional individuallife business, while the market unit continues to develop its unit-linked business. InSpain, traditional individual business is also the primary line of business, as is thecase in the Netherlands. In its Central and Eastern European markets, where it isthe leader in the Czech Republic’s pension market and where there have beensignificant developments in terms of pension reform over the past several years,Winterthur administers pension funds and seeks to offer supplementary personalpension schemes as well as unit-linked life insurance policies. Winterthur also hasoperations in Japan, Hong Kong, Taiwan and Indonesia.

Information on the company Winterthur 31

Products and servicesLife & Pensions’ products consist of traditional and non-traditional life insurance,both of which are offered on an individual and group basis. The majority of Life &Pensions’ products are participating products, which provide guaranteed benefits anddividends based on legal or contractual obligations, or at management’s discretion.Life & Pensions also provides disability insurance, as well as a number of additionalproducts, to group pension funds, on a defined benefit or defined contribution basis.Winterthur is continuing to develop innovative solutions for its key markets and totake measures to increase sales of non-traditional products, which are primarily unit-linked.

Traditional products Traditional products consist of endowments and annuities for which the investmentrisk is borne by the insurer and not by the policyholder. The insurer also bearsmortality risk for the life of the product. These products include pure protection, orterm insurance, designed to provide a lump sum at the end of a fixed term anddeath coverage during the term. Endowments and annuities can be regular or singlepremium products. For traditional with-profit products, the insurer investspolicyholder premiums in a range of assets, including equities, real estate and fixedincome securities. With-profit policyholders receive a share of the profits, resultingfrom the insurance company’s business. In 2004, Life & Pensions’ gross premiumswritten from traditional products represented approximately 71% of its total businessvolume.

Non-traditional productsNon-traditional products are medium-term to long-term savings products with lifeinsurance coverage for which the investment risk is borne in whole or in part by thepolicyholder, depending upon whether there is a guaranteed minimum payment.These products include variable annuities and guaranteed investment contracts.Non-traditional products may be regular or single premium and either with-profit orunit-linked.

With-profit policyholders receive a share of the profits resulting from the insurancecompany’s investments. Unit-linked policyholders are entitled to a return based uponthe performance of segregated accounts. In 2004, Life & Pensions’ gross premiumsand policyholder deposits from non-traditional products represented approximately29% of its total business volume.

Disability insuranceThe most significant disability products that Life & Pensions offers are waiver ofpremium and disability pensions, on a stand-alone basis or as policy riders. In theapplication, the policyholder typically may choose the period following disability afterwhich the payments begin.

Information on the company Winterthur32

Group pensions Winterthur offers a variety of group pension solutions, either with-profit or unit-linked, on a defined benefit or defined contribution basis for small, medium-sizedand large companies. These products include asset accumulation or investmentvehicles, protection for death and disability and income or annuity components.Swiss group pension plans, which are part of the “second pillar” of the Swissretirement savings system, are subject to a minimum return which is set by theSwiss government on the basis of the Swiss federal law on occupational benefitplans (second pillar). This rate was initially reduced from 4% to 3.25% as of January1, 2003, to 2.25% as of January 1, 2004, and increased to 2.50% effectiveJanuary 1, 2005. As of December 31, 2004, the share of business subject to theminimum rate of return represented 11% of Life & Pensions’ technical reserves.

Effective January 1, 2004, Life & Pensions introduced its new employee benefitbusiness model for Swiss group pension plans, as announced in the first half of2003. This new model is more closely aligned with the current economicenvironment and developments in terms of life expectancy. The key elements of thismodel comprise a separation of the insurance and pensions relationship, bringingabout partial independence and strengthening of the collective foundations, whichadminister the pension schemes, and a distinction between mandatory and non-mandatory occupational benefits.

On March 24, 2004, the Swiss government passed legislation that provides for amandatory participation in profits to policyholders in respect of the regulatedemployee benefit business in Switzerland. In addition to the ongoing allocation topolicyholders in respect of this business, initial provisions reflecting this change inlegislation were recorded in the first quarter of 2004 and amounted to CHF 117million, with an after-tax impact of CHF 91 million.

Marketing and distribution Sharing many of the same distribution channels with the Non-Life segment, Life &Pensions products are distributed principally through tied or exclusive agents,brokers and banks. In 2004, approximately 60% of Life & Pensions’ total businessvolume production was derived from tied agents, including agents of the Non-Lifesegment, approximately 27% was derived from brokers and approximately 7% wasderived from banks, including Credit Suisse. Other channels accounted for theremaining 6%.

Group life products are sold principally through tied agents for small and medium-sized companies, and through brokers and an organization of employee benefitconsultants with insurance and banking skills, for multinational corporate customers.

Following the restructuring of the sales organization in Switzerland in 2003,Winterthur restructured its Life & Pensions and Non-Life organization in Switzerlandin 2004, bringing management responsibility for the unified organization together.This reorganization is more in line with current customer requirements and isintended to improve operating efficiency.

Information on the company Winterthur 33