22

LETTER TO SHAREHOLDERS 1999 INTERIM RESULTS

| Date post: | 12-Apr-2017 |

| Category: |

Economy & Finance |

| Upload: | quarterlyearningsreports2 |

| View: | 358 times |

| Download: | 4 times |

LETTER TO SHAREHOLDERS1999 INTERIM RESULTS

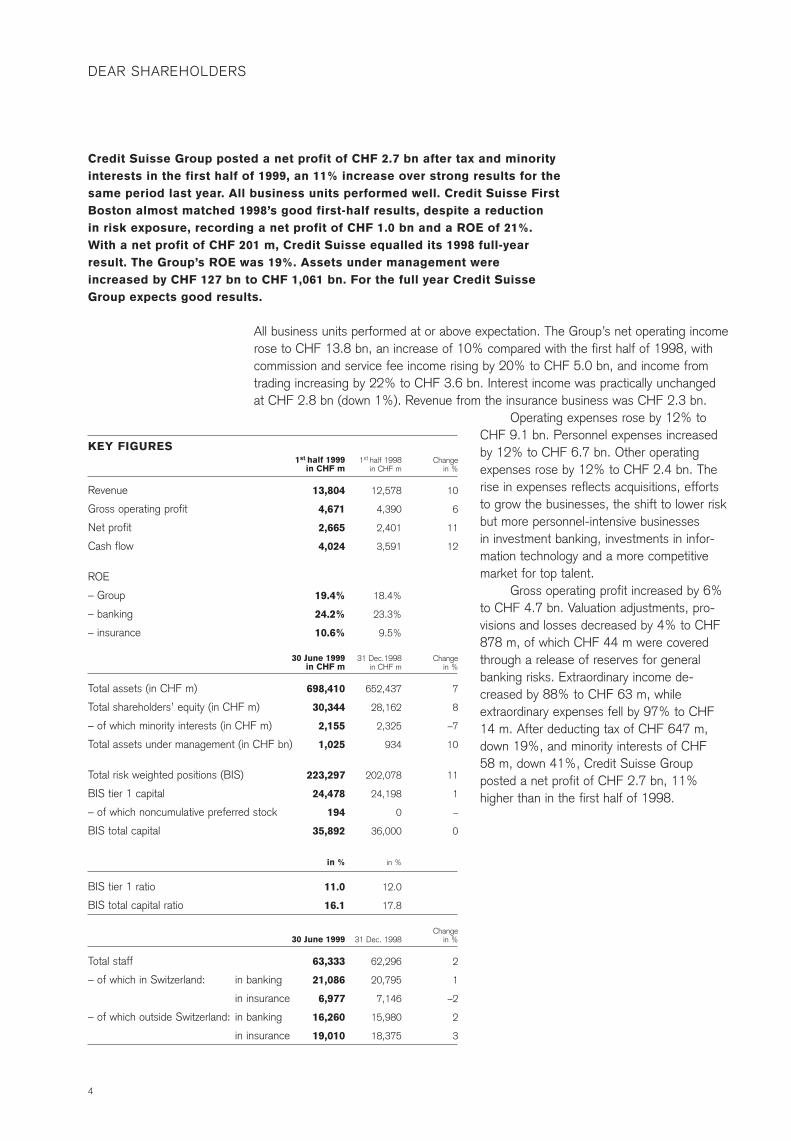

ChangeShare data 30 June 1999 31 Dec. 1998 in %

Number of shares issued 272,101,488 269,086,369 1

Shares ranking for dividend 272,101,488 269,086,369 1

Market capitalisation (CHF m) 73,195 57,854 27

Share price (CHF) (at 3 Sept. 1999: 294) 269 215 25

high January – June 1999 310

low January – June 1999 211.8

Change1sthalf 1999 1st half 1998 in %

Earnings per share (CHF) 9.85 9.02 9

Average shares ranking for dividend 270,490,439 266,340,880 2

Financial calendar

Announcement of 1999 results Tuesday, 14 March 2000

2000 Annual General Meeting Friday, 26 May 2000

Contents

Commentary on the consolidated results 4

Consolidated income statement 8

Consolidated balance sheet 9

Consolidated off-balance-sheet business, selected notes to the consolidated financial statements 10

Credit Suisse 12

Credit Suisse Private Banking 14

Credit Suisse First Boston 16

Credit Suisse Asset Management 19

Winterthur 20

Closing 22

Share performance

400350300

250

200

150

100

1996 1997 1998 1999

Credit Suisse GroupSwiss Market Index

3

All business units performed at or above expectation. The Group’s net operating incomerose to CHF 13.8 bn, an increase of 10% compared with the first half of 1998, withcommission and service fee income rising by 20% to CHF 5.0 bn, and income fromtrading increasing by 22% to CHF 3.6 bn. Interest income was practically unchangedat CHF 2.8 bn (down 1%). Revenue from the insurance business was CHF 2.3 bn.

Operating expenses rose by 12% toCHF 9.1 bn. Personnel expenses increasedby 12% to CHF 6.7 bn. Other operatingexpenses rose by 12% to CHF 2.4 bn. Therise in expenses reflects acquisitions, effortsto grow the businesses, the shift to lower riskbut more personnel-intensive businesses in investment banking, investments in infor-mation technology and a more competitivemarket for top talent.

Gross operating profit increased by 6%to CHF 4.7 bn. Valuation adjustments, pro-visions and losses decreased by 4% to CHF878 m, of which CHF 44 m were coveredthrough a release of reserves for generalbanking risks. Extraordinary income de-creased by 88% to CHF 63 m, while extraordinary expenses fell by 97% to CHF14 m. After deducting tax of CHF 647 m,down 19%, and minority interests of CHF 58 m, down 41%, Credit Suisse Group posted a net profit of CHF 2.7 bn, 11%higher than in the first half of 1998.

DEAR SHAREHOLDERS

Changein %

10

6

11

12

Changein %

7

8

–7

10

11

1

–

0

Changein %

2

1

–2

2

3

1st half 1999in CHF m

13,804

4,671

2,665

4,024

19.4%

24.2%

10.6%

30 June 1999in CHF m

698,410

30,344

2,155

1,025

223,297

24,478

194

35,892

in %

11.0

16.1

30 June 1999

63,333

21,086

6,977

16,260

19,010

1st half 1998in CHF m

12,578

4,390

2,401

3,591

18.4%

23.3%

9.5%

31 Dec.1998in CHF m

652,437

28,162

2,325

934

202,078

24,198

0

36,000

in %

12.0

17.8

31 Dec. 1998

62,296

20,795

7,146

15,980

18,375

KEY FIGURES

Revenue

Gross operating profit

Net profit

Cash flow

ROE

– Group

– banking

– insurance

Total assets (in CHF m)

Total shareholders’ equity (in CHF m)

– of which minority interests (in CHF m)

Total assets under management (in CHF bn)

Total risk weighted positions (BIS)

BIS tier 1 capital

– of which noncumulative preferred stock

BIS total capital

BIS tier 1 ratio

BIS total capital ratio

Total staff

– of which in Switzerland: in banking

in insurance

– of which outside Switzerland: in banking

in insurance

Credit Suisse Group posted a net profit of CHF 2.7 bn after tax and minorityinterests in the first half of 1999, an 11% increase over strong results for thesame period last year. All business units performed well. Credit Suisse FirstBoston almost matched 1998’s good first-half results, despite a reduction in risk exposure, recording a net profit of CHF 1.0 bn and a ROE of 21%. With a net profit of CHF 201 m, Credit Suisse equalled its 1998 full-yearresult. The Group’s ROE was 19%. Assets under management wereincreased by CHF 127 bn to CHF 1,061 bn. For the full year Credit SuisseGroup expects good results.

4

In the first six months of 1999, total assets under management grew by CHF 91 bn (up 9.7%) to CHF 1,025 bn. Including the acquisition of Warburg Pincus AssetManagement, total assets under management for the Group stood at CHF 1,061 bn.

Earnings per share amounted to CHF 9.85 (up 9%), while book value per sharerose by 8% to CHF 103.6 since the beginning of 1999. As at 30 June 1999, CreditSuisse Group had 63,333 employees.

Good performances from all business units

Credit Suisse, which is responsible for Swiss corporate and individual customers, con-firmed the turnaround it achieved in 1998. With a net profit of CHF 201 m, it exceeded1998 first-half results by CHF 150 m. Revenue rose by 8% to CHF 1.7 bn, whileoperating expenses declined by 4% to CHF 1.1 bn. The cost-income ratio improvedfurther to 66.8%, a fall of 7.7 percentage points. The risk profile of the loan bookagain developed favourably.

Credit Suisse Private Banking continued to build on 1998’s good results, posting a net profit of CHF 859 m, an increase of 4% on the same period last year.Revenue rose by 5% to CHF 2.3 bn, while operating expenses rose by 8% to CHF 1.1 bn owing mainly to investment in human resources and information technology. Inthe first half of the year, assets under management grew by 9.2% to CHF 440 bn, ofwhich CHF 12.6 bn or 3.1% was the result of a net inflow of new business and 6.1%due to market performance.

Credit Suisse First Boston continued its momentum despite the market turbulence in the third quarter of 1998, with a good performance in the first six monthsof 1999. Through organic growth and the swift integration of last year’s acquisitions,the firm gained considerable market share. Credit Suisse First Boston posted a netprofit of CHF 1.0 bn (down 4%), or USD 700 m (down 2%), in line with the goodresults for the first half of 1998. Revenue rose by 14% to CHF 7.4 bn, (or by 16% toUSD 5.1 bn). Operating expenses increased by 16% to CHF 5.2 bn (or by 18% toUSD 3.6 bn), reflecting efforts to build the business, higher bonus accruals in line with revenue growth and a shift in the business mix. While fixed income and derivatives revenues declined by 6% (4% in USD terms), revenues from equity increased by 74%(76% in USD terms), and revenues from corporate and investment banking increasedby 13% (15% in USD terms). In geographic terms, earnings showed a balanced split,with 39% generated in North America, 35% in Europe and 26% in the rest of theworld.

Credit Suisse Asset Management posted net profit of CHF 111 m in the firsthalf, 8% down on 1998’s first-half results. The decline is due primarily to a greatershare of the mutual fund revenue contributed to Credit Suisse Group distribution chan-nels. Increased investments in information technology and growth initiatives in turn ledto 11% higher operating expenses at CHF 319 m. Revenue increased by 5% to CHF462 m. Discretionary assets under management grew strongly by 17.9% to CHF 250bn, of which CHF 18.2 bn, or 8.6%, was from net new business. Total assets undermanagement rose by 13.1% to CHF 336 bn. Following the closure of the acquisition inJuly 1999 of Warburg Pincus Asset Management, total assets under managementamounted to CHF 372 bn.

26%

21%

36%

17%

REVENUE COMPOSITION 1 half 1999

Balance sheet businessCommissionTrading

Insurance

st

5

6

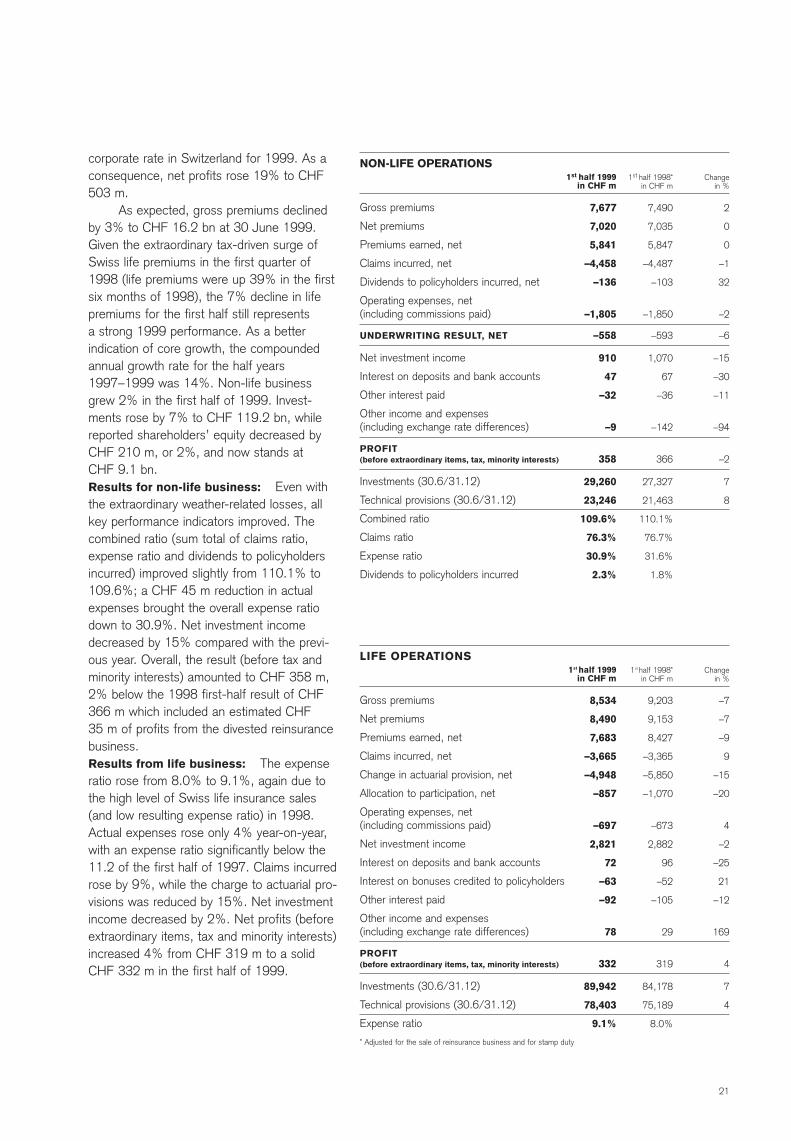

Winterthur achieved a net profit of CHF 503 m, up 19%, benefiting from a lower effective tax rate and good operating results, up 1% to CHF 690 m, in spite ofsevere weather losses, lower investment income as a result of lower realised capitalgains, and the absence of profits from the divested reinsurance business. Gross premiums declined, as expected, by 3% to CHF 16.2 bn in the first half of 1999. Given the extraordinary tax-driven surge of Swiss life premiums in the first quarter of1998 (life premiums were up 39% in the first six months of 1998), the 7% decline to CHF 8.5 bn in life premiums for the first half still represents a strong 1999 perform-ance. As a better indication of core growth, the compounded annual growth rate for the half years 1997–1999 was 14%. Non-life business grew 2% to CHF 7.7 bn in thefirst half of 1999. Lower expenses in non-life operations reduced the combined ratiofrom 110.1% to 109.6%. Assets under management rose by 7% to CHF 119.2 bn.

Adjustments in risk management and compliance

Following the turmoil in international financial markets in 1998, Credit Suisse Groupreviewed its risk exposure, particularly at Credit Suisse First Boston, with the objectiveof reducing risk concentrations and earnings volatility. With respect to market risk, mea-surement methodologies have been harmonised and total adjusted exposure reducedsince the beginning of the year. At Credit Suisse First Boston, average allocated capitalis down from 1998 to the first half of 1999 and the balance sheet is down by 5% inUSD terms from the end of 1998. A more significant system of monitoring and manag-ing country risk exposure has been introduced. In addition, limits and relevant expo-sures have been cut back significantly. With respect to the recently restructured US realestate business, risk concentration has been reduced as a precautionary measure andprovisions increased.

The emphasis at Credit Suisse First Boston is on continuing to grow the client-driven businesses involving less capital and risk. On a Group level, the contribution tonet profit from the less volatile asset accumulation and asset management businesses(including insurance) increased from 58% for the first half of 1998 to 62% for the firsthalf of 1999.

The examination of Credit Suisse Group’s entities in Japan by the FinancialSupervisory Agency of Japan (FSA) led among other things to the revocation of the licence of the Tokyo branch of Credit Suisse Financial Products. Following the completion of the FSA’s examination, Credit Suisse Group initiated structural andorganisational adjustments as well as remedial measures to strengthen its compliance.

CreditSuisseGroup

13,804

6,723

2,410

9,133

4,671

472

878

3,321

63

14

647

2,723

58

2,665

Adjustmentsincluding

CorporateCentre

–202

248

–280

–32

–170

158

39

–367

35

–6

–303

–23

0

–23

CreditSuisseAsset

Management

462

184

135

319

143

5

0

138

0

5

22

111

0

111

241

n/a

294

0

WinterthurLife

774

255

164

419

355

23

0

332

WinterthurNon-life

1,415

633

399

1,032

383

25

0

358

CreditSuisse

1,685

680

424

1,104

581

21

303

257

19

5

69

202

1

201

4,409

9.2

4,389

–12

CreditSuisse

FirstBoston

7,420

4,010

1,200

5,210

2,210

219

497

1,494

0

0

478

1,016

2

1,014

9,910

20.5

10,555

58

CreditSuissePrivate

Banking

2,250

713

368

1,081

1,169

21

39

1,109

9

7

243

868

9

859

2,689

n/a

2,753

–9

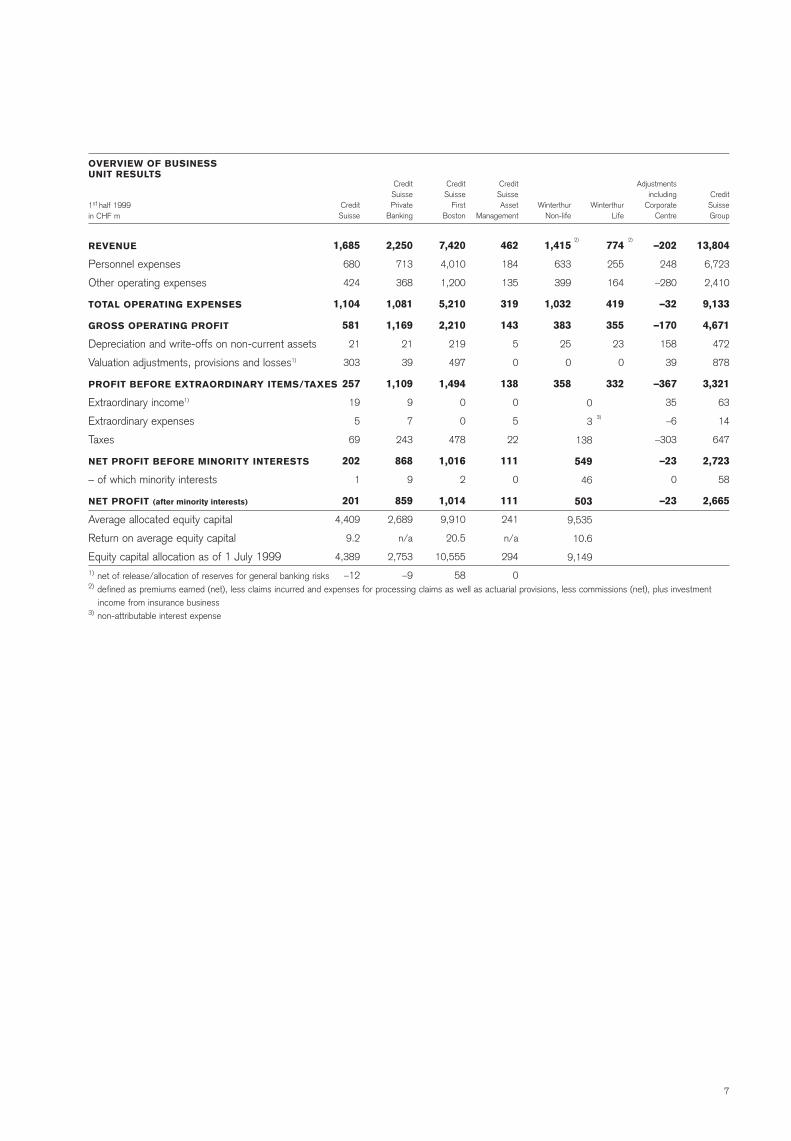

OVERVIEW OF BUSINESSUNIT RESULTS

1st half 1999in CHF m

REVENUE

Personnel expenses

Other operating expenses

TOTAL OPERATING EXPENSES

GROSS OPERATING PROFIT

Depreciation and write-offs on non-current assets

Valuation adjustments, provisions and losses1)

PROFIT BEFORE EXTRAORDINARY ITEMS/TAXES

Extraordinary income1)

Extraordinary expenses

Taxes

NET PROFIT BEFORE MINORITY INTERESTS

– of which minority interests

NET PROFIT (after minority interests)

Average allocated equity capital

Return on average equity capital

Equity capital allocation as of 1 July 19991) net of release/allocation of reserves for general banking risks2) defined as premiums earned (net), less claims incurred and expenses for processing claims as well as actuarial provisions, less commissions (net), plus investment

income from insurance business3) non-attributable interest expense

2) 2)

3)

0

3

138

549

46

503

9,535

10.6

9,149

7

Changein %

–25

–25

21

–31

–1

37

19

11

22

20

22

–13

–12

–19

–7

–5

18

–23

–59

–

80

51

81

–46

10

12

12

12

6

64

–

–4

13

4

–88

–97

–19

9

–41

11

Changein CHF m

–2,631

–757

42

–3,305

–41

77

764

20

43

818

664

–1,938

–1,878

–237

–286

–109

37

–20

–42

22

8

135

266

–106

1,226

695

250

945

281

185

39

–34

151

130

–479

–421

–152

224

–40

264

1st half 1998in CHF m

10,398

2,973

198

10,711

2,858

209

3,977

174

195

4,165

2,954

15,463

15,943

1,256

4,105

2,369

201

87

71

16

10

263

329

232

12,578

6,028

2,160

8,188

4,390

287

1

912

1,199

3,191

542

435

799

2,499

98

2,401

1st half 1999in CHF m

7,767

2 216

240

7,406

2,817

286

4,741

194

238

4,983

3,618

13,525

14,065

1,019

3,819

2,260

238

67

29

38

18

398

595

126

13,804

6,723

2,410

9,133

4,671

472

40

878

1,350

3,321

63

14

647

2,723

58

2,665

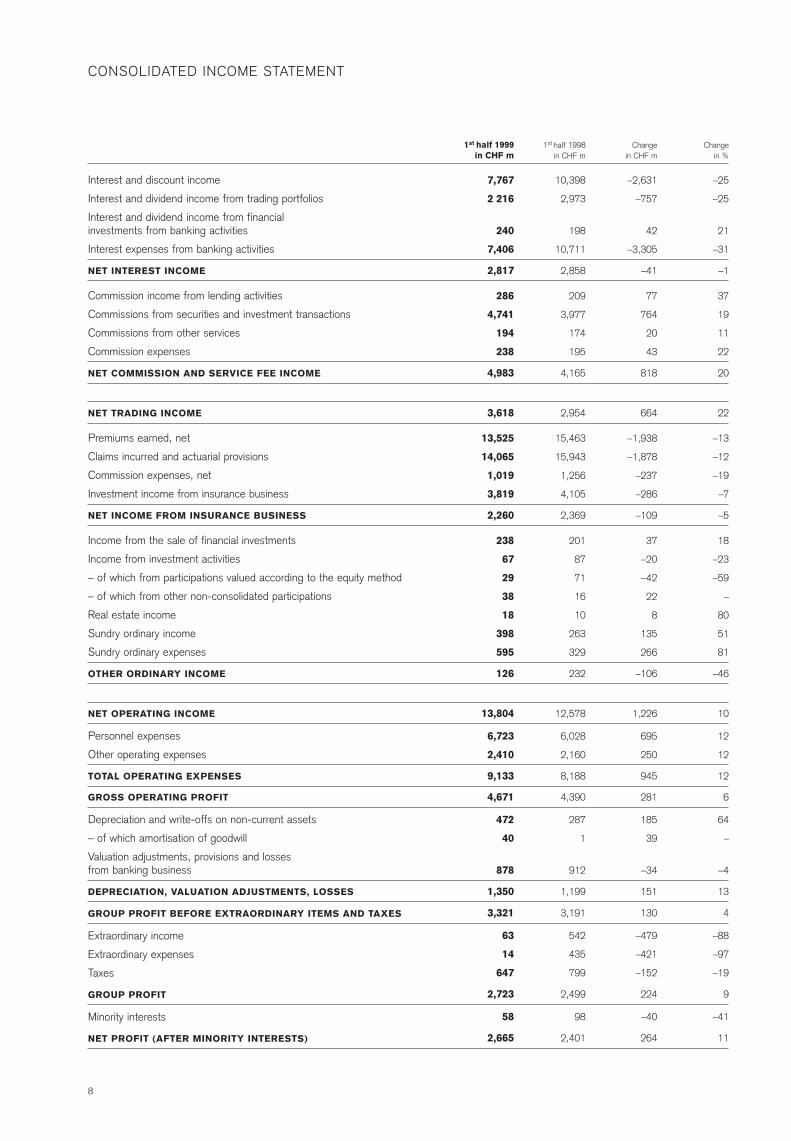

Interest and discount income

Interest and dividend income from trading portfolios

Interest and dividend income from financial investments from banking activities

Interest expenses from banking activities

NET INTEREST INCOME

Commission income from lending activities

Commissions from securities and investment transactions

Commissions from other services

Commission expenses

NET COMMISSION AND SERVICE FEE INCOME

NET TRADING INCOME

Premiums earned, net

Claims incurred and actuarial provisions

Commission expenses, net

Investment income from insurance business

NET INCOME FROM INSURANCE BUSINESS

Income from the sale of financial investments

Income from investment activities

– of which from participations valued according to the equity method

– of which from other non-consolidated participations

Real estate income

Sundry ordinary income

Sundry ordinary expenses

OTHER ORDINARY INCOME

NET OPERATING INCOME

Personnel expenses

Other operating expenses

TOTAL OPERATING EXPENSES

GROSS OPERATING PROFIT

Depreciation and write-offs on non-current assets

– of which amortisation of goodwill

Valuation adjustments, provisions and losses from banking business

DEPRECIATION, VALUATION ADJUSTMENTS, LOSSES

GROUP PROFIT BEFORE EXTRAORDINARY ITEMS AND TAXES

Extraordinary income

Extraordinary expenses

Taxes

GROUP PROFIT

Minority interests

NET PROFIT (AFTER MINORITY INTERESTS)

CONSOLIDATED INCOME STATEMENT

8

30 June 1999in CHF m

2,387

29,974

149,967

7,277

117,069

86,369

112,459

18,012

109,775

1,741

6,649

1,519

10,391

44,821

698,410

2,406

726

31 Dec.1998in CHF m

2,313

26,594

140,152

7,482

103,183

80,558

102,515

17,467

102,316

1,331

6,362

802

9,628

51,734

652,437

3,048

227

Changein CHF m

74

3,380

9,815

–205

13,886

5,811

9,944

545

7,459

410

287

717

763

–6,913

45,973

–642

499

Changein %

3

13

7

–3

13

7

10

3

7

31

5

89

8

–13

7

–21

–

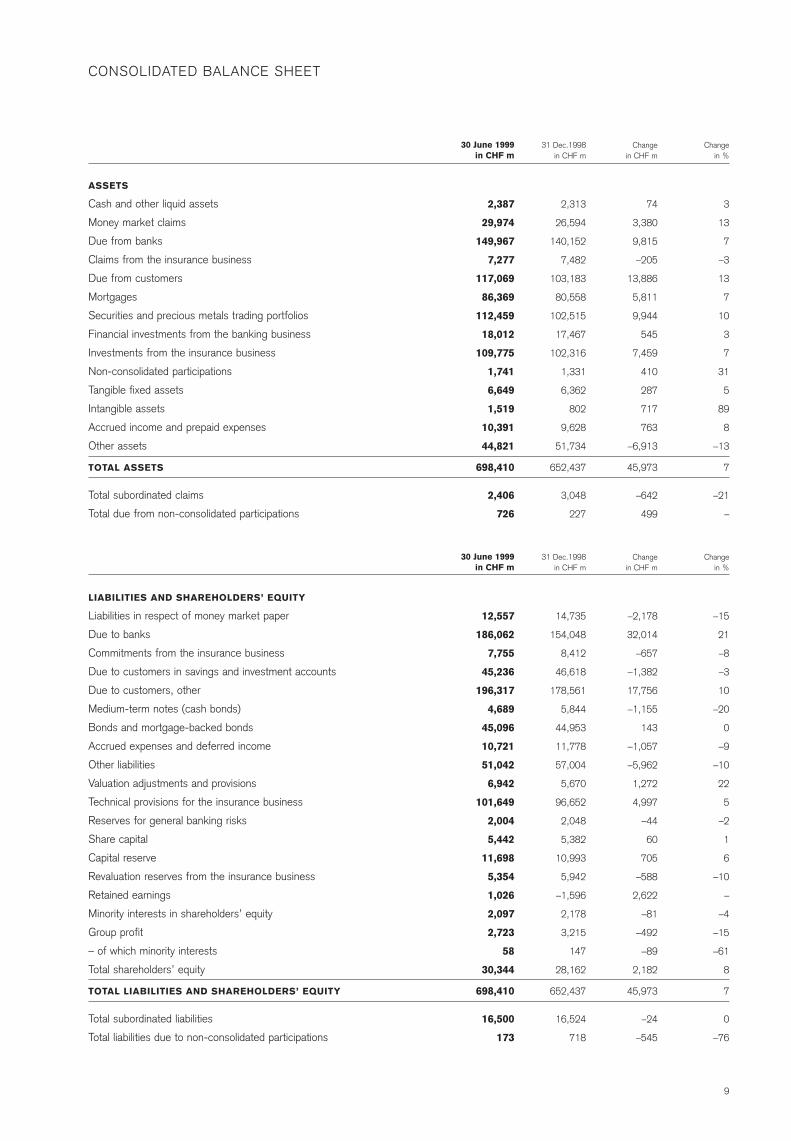

ASSETS

Cash and other liquid assets

Money market claims

Due from banks

Claims from the insurance business

Due from customers

Mortgages

Securities and precious metals trading portfolios

Financial investments from the banking business

Investments from the insurance business

Non-consolidated participations

Tangible fixed assets

Intangible assets

Accrued income and prepaid expenses

Other assets

TOTAL ASSETS

Total subordinated claims

Total due from non-consolidated participations

30 June 1999in CHF m

12,557

186,062

7,755

45,236

196,317

4,689

45,096

10,721

51,042

6,942

101,649

2,004

5,442

11,698

5,354

1,026

2,097

2,723

58

30,344

698,410

16,500

173

31 Dec.1998in CHF m

14,735

154,048

8,412

46,618

178,561

5,844

44,953

11,778

57,004

5,670

96,652

2,048

5,382

10,993

5,942

–1,596

2,178

3,215

147

28,162

652,437

16,524

718

Changein CHF m

–2,178

32,014

–657

–1,382

17,756

–1,155

143

–1,057

–5,962

1,272

4,997

–44

60

705

–588

2,622

–81

–492

–89

2,182

45,973

–24

–545

Changein %

–15

21

–8

–3

10

–20

0

–9

–10

22

5

–2

1

6

–10

–

–4

–15

–61

8

7

0

–76

LIABILITIES AND SHAREHOLDERS’ EQUITY

Liabilities in respect of money market paper

Due to banks

Commitments from the insurance business

Due to customers in savings and investment accounts

Due to customers, other

Medium-term notes (cash bonds)

Bonds and mortgage-backed bonds

Accrued expenses and deferred income

Other liabilities

Valuation adjustments and provisions

Technical provisions for the insurance business

Reserves for general banking risks

Share capital

Capital reserve

Revaluation reserves from the insurance business

Retained earnings

Minority interests in shareholders’ equity

Group profit

– of which minority interests

Total shareholders’ equity

TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY

Total subordinated liabilities

Total liabilities due to non-consolidated participations

CONSOLIDATED BALANCE SHEET

9

Changein %

0

2

25

–2

3

16

0

–10

9

Changein CHF m

–35

96

565

–86

540

13,184

0

–27

3,337

31 Dec. 1998in CHF m

8,870

4,471

2,225

3,710

19,276

84,775

59

262

35,216

30 June 1999in CHF m

8,835

4,567

2,790

3,624

19,816

97,959

59

235

38,553

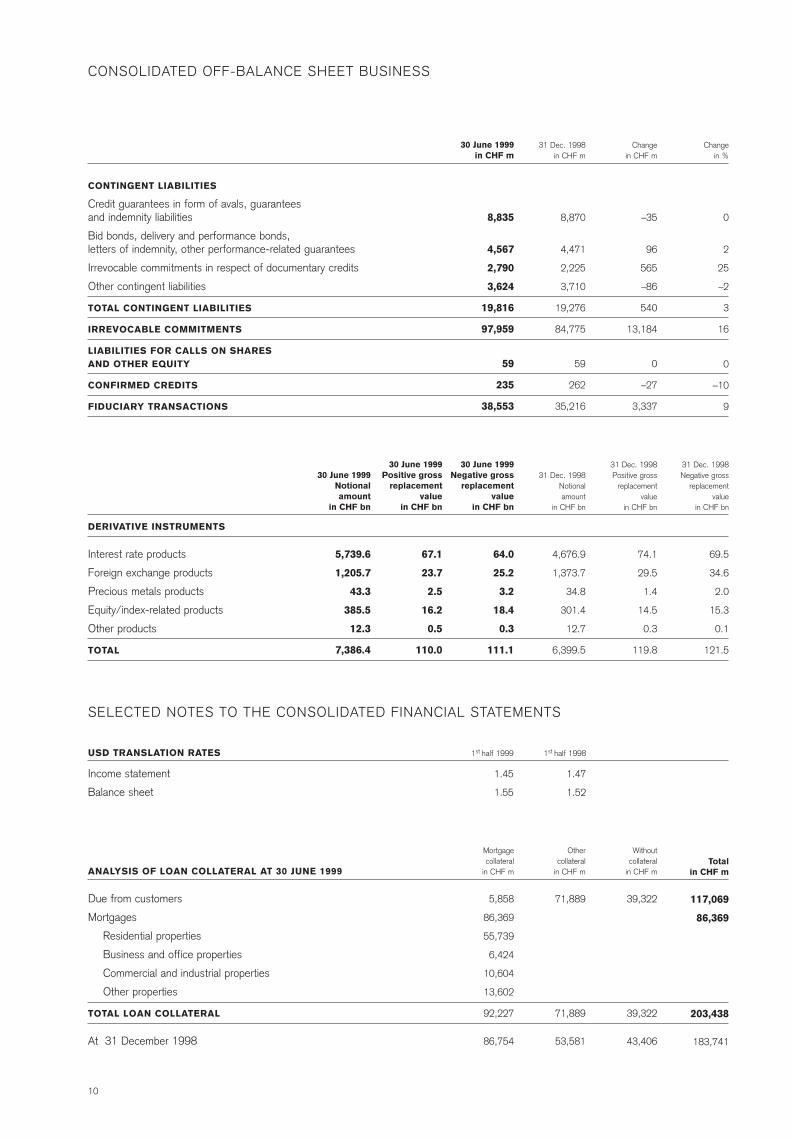

CONTINGENT LIABILITIES

Credit guarantees in form of avals, guarantees and indemnity liabilities

Bid bonds, delivery and performance bonds, letters of indemnity, other performance-related guarantees

Irrevocable commitments in respect of documentary credits

Other contingent liabilities

TOTAL CONTINGENT LIABILITIES

IRREVOCABLE COMMITMENTS

LIABILITIES FOR CALLS ON SHARES AND OTHER EQUITY

CONFIRMED CREDITS

FIDUCIARY TRANSACTIONS

CONSOLIDATED OFF-BALANCE SHEET BUSINESS

31 Dec. 1998Negative gross

replacementvalue

in CHF bn

69.5

34.6

2.0

15.3

0.1

121.5

31 Dec. 1998Positive gross

replacementvalue

in CHF bn

74.1

29.5

1.4

14.5

0.3

119.8

31 Dec. 1998Notionalamount

in CHF bn

4,676.9

1,373.7

34.8

301.4

12.7

6,399.5

30 June 1999Negative gross

replacementvalue

in CHF bn

64.0

25.2

3.2

18.4

0.3

111.1

30 June 1999Positive gross

replacementvalue

in CHF bn

67.1

23.7

2.5

16.2

0.5

110.0

30 June 1999Notionalamount

in CHF bn

5,739.6

1,205.7

43.3

385.5

12.3

7,386.4

Mortgagecollateral

in CHF m

5,858

86,369

55,739

6,424

10,604

13,602

92,227

86,754

Othercollateral

in CHF m

71,889

71,889

53,581

Without collateral

in CHF m

39,322

39,322

43,406

Totalin CHF m

117,069

86,369

203,438

183,741

DERIVATIVE INSTRUMENTS

Interest rate products

Foreign exchange products

Precious metals products

Equity/index-related products

Other products

TOTAL

ANALYSIS OF LOAN COLLATERAL AT 30 JUNE 1999

Due from customers

Mortgages

Residential properties

Business and office properties

Commercial and industrial properties

Other properties

TOTAL LOAN COLLATERAL

At 31 December 1998

SELECTED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

USD TRANSLATION RATES 1st half 1999 1st half 1998

Income statement 1.45 1.47

Balance sheet 1.55 1.52

10

SELECTED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

1st half 1998in CHF m

2,858

4,165

2,954

2,369

232

12,578

6,028

2,160

8,188

4,390

287

912

1,199

3,191

542

435

799

2,499

98

2,401

1st half 1999in CHF m

2,817

4,983

3,618

2,260

126

13,804

6,723

2,410

9,133

4,671

472

878

1,350

3,321

63

14

647

2,723

58

2,665

1st half 1998in CHF m

0

0

0

2,369

–188

2,181

920

576

1,496

685

0

0

0

685

0

14

211

460

37

423

1st half 1999in CHF m

0

0

0

2,260

–73

2,187

888

560

1,448

739

48

0

48

691

0

0

138

553

46

507

1st half 1998in CHF m

2,858

4,165

2,954

0

420

10,397

5,108

1,584

6,692

3,705

287

912

1,199

2,506

542

421

588

2,039

61

1,978

1st half 1999in CHF m

2,817

4,983

3,618

0

199

11,617

5,835

1,850

7,685

3,932

424

878

1,302

2,630

63

14

509

2,170

12

2,158

Banking business Insurance business TotalSPLIT OF INCOME STATEMENT INTO BANKINGAND INSURANCE BUSINESS

Net interest income

Net commission and service income

Net trading income

Net income from insurance business

Other ordinary income/expenses net

NET OPERATING INCOME

Personnel expenses

Other operating expenses

Total operating expenses

GROSS OPERATING PROFIT

Depreciation and write-offs on non-current assets

Valuation adjustments, provisions and losses

Total depreciation, valuation adjustments

GROUP PROFIT BEFORE EXTRAORDINARYITEMS AND TAXES

Extraordinary income

Extraordinary expenses

Taxes

GROUP PROFIT

Minority interests

NET PROFIT (AFTER MINORITY INTERESTS)

30 June 1999in CHF m

76,928

44,608

32,320

201

34,112

3,591

1,419

112,459

44,997

31 Dec. 1998in CHF m

68,830

41,138

27,692

333

31,886

2,344

1,799

102,515

28,186

Changein CHF m

8,098

3,470

4,628

–132

2,226

1,247

–380

9,944

16,811

Changein %

12

8

17

–40

7

53

–21

10

60

SECURITIES AND PRECIOUS METALS TRADING PORTFOLIOS

Interest bearing securities and rights

listed on stock exchange

unlisted

– of which own bonds and medium-term notes

Equities

– of which own shares

Precious metals

TOTAL SECURITIES AND PRECIOUS METALS TRADING PORTFOLIOS

– of which securities rediscountable or pledgeable at central banks

11

CORPORATE AND INDIVIDUAL CUSTOMERS IN SWITZERLAND

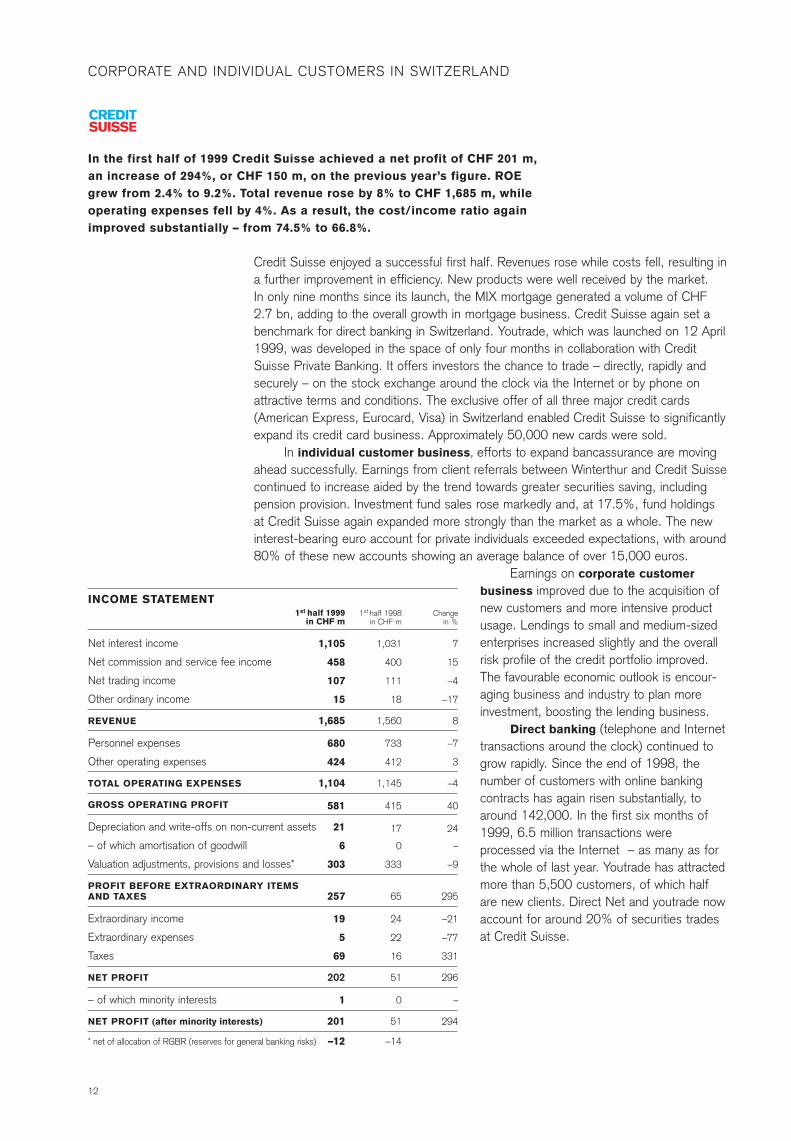

Credit Suisse enjoyed a successful first half. Revenues rose while costs fell, resulting ina further improvement in efficiency. New products were well received by the market. In only nine months since its launch, the MIX mortgage generated a volume of CHF2.7 bn, adding to the overall growth in mortgage business. Credit Suisse again set abenchmark for direct banking in Switzerland. Youtrade, which was launched on 12 April1999, was developed in the space of only four months in collaboration with CreditSuisse Private Banking. It offers investors the chance to trade – directly, rapidly andsecurely – on the stock exchange around the clock via the Internet or by phone onattractive terms and conditions. The exclusive offer of all three major credit cards(American Express, Eurocard, Visa) in Switzerland enabled Credit Suisse to significantlyexpand its credit card business. Approximately 50,000 new cards were sold.

In individual customer business, efforts to expand bancassurance are movingahead successfully. Earnings from client referrals between Winterthur and Credit Suissecontinued to increase aided by the trend towards greater securities saving, includingpension provision. Investment fund sales rose markedly and, at 17.5%, fund holdingsat Credit Suisse again expanded more strongly than the market as a whole. The newinterest-bearing euro account for private individuals exceeded expectations, with around80% of these new accounts showing an average balance of over 15,000 euros.

Earnings on corporate customer business improved due to the acquisition ofnew customers and more intensive productusage. Lendings to small and medium-sizedenterprises increased slightly and the overallrisk profile of the credit portfolio improved.The favourable economic outlook is encour-aging business and industry to plan moreinvestment, boosting the lending business.

Direct banking (telephone and Internettransactions around the clock) continued togrow rapidly. Since the end of 1998, thenumber of customers with online bankingcontracts has again risen substantially, toaround 142,000. In the first six months of1999, 6.5 million transactions wereprocessed via the Internet – as many as forthe whole of last year. Youtrade has attractedmore than 5,500 customers, of which halfare new clients. Direct Net and youtrade nowaccount for around 20% of securities tradesat Credit Suisse.

In the first half of 1999 Credit Suisse achieved a net profit of CHF 201 m,an increase of 294%, or CHF 150 m, on the previous year’s figure. ROEgrew from 2.4% to 9.2%. Total revenue rose by 8% to CHF 1,685 m, whileoperating expenses fell by 4%. As a result, the cost/income ratio againimproved substantially – from 74.5% to 66.8%.

1st half 1998in CHF m

1,031

400

111

18

1,560

733

412

1,145

415

17

0

333

65

24

22

16

51

0

51

–14

Changein %

7

15

–4

–17

8

–7

3

–4

40

24

–

–9

295

–21

–77

331

296

–

294

1st half 1999in CHF m

1,105

458

107

15

1,685

680

424

1,104

581

21

6

303

257

19

5

69

202

1

201

–12

INCOME STATEMENT

Net interest income

Net commission and service fee income

Net trading income

Other ordinary income

REVENUE

Personnel expenses

Other operating expenses

TOTAL OPERATING EXPENSES

GROSS OPERATING PROFIT

Depreciation and write-offs on non-current assets

– of which amortisation of goodwill

Valuation adjustments, provisions and losses*

PROFIT BEFORE EXTRAORDINARY ITEMS AND TAXES

Extraordinary income

Extraordinary expenses

Taxes

NET PROFIT

– of which minority interests

NET PROFIT (after minority interests)

* net of allocation of RGBR (reserves for general banking risks)

12

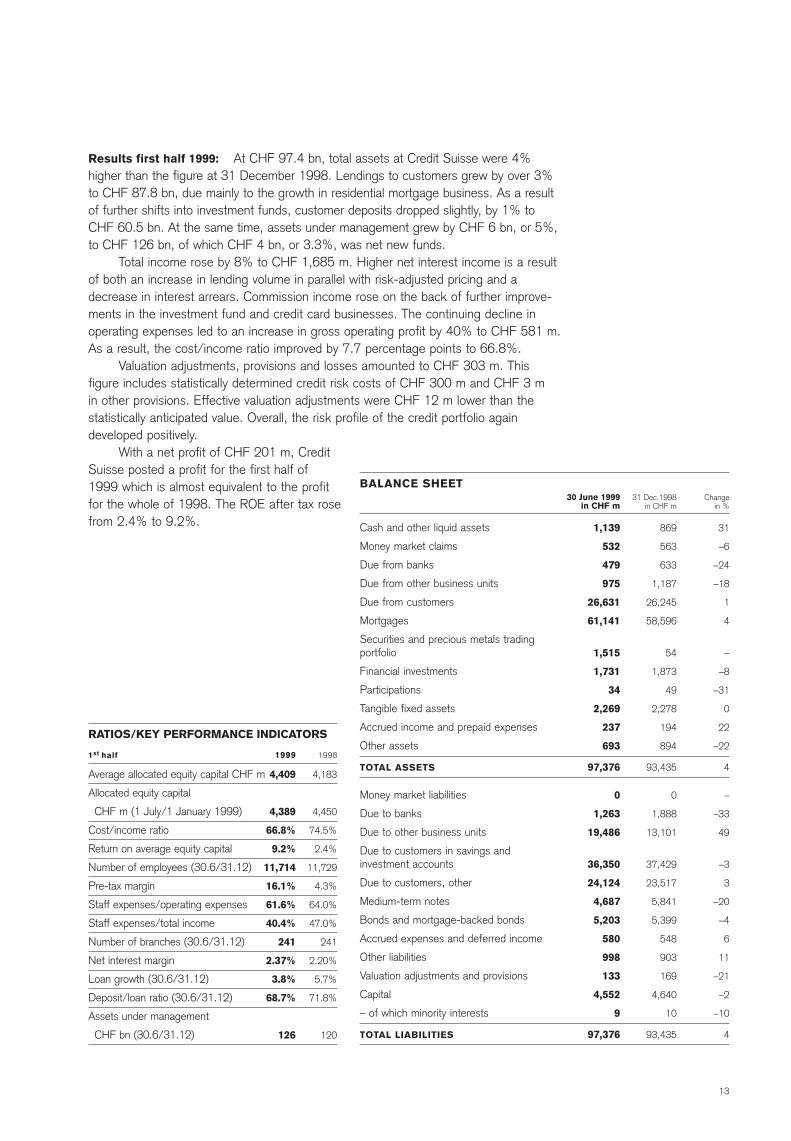

Results first half 1999: At CHF 97.4 bn, total assets at Credit Suisse were 4% higher than the figure at 31 December 1998. Lendings to customers grew by over 3%to CHF 87.8 bn, due mainly to the growth in residential mortgage business. As a resultof further shifts into investment funds, customer deposits dropped slightly, by 1% toCHF 60.5 bn. At the same time, assets under management grew by CHF 6 bn, or 5%,to CHF 126 bn, of which CHF 4 bn, or 3.3%, was net new funds.

Total income rose by 8% to CHF 1,685 m. Higher net interest income is a resultof both an increase in lending volume in parallel with risk-adjusted pricing and adecrease in interest arrears. Commission income rose on the back of further improve-ments in the investment fund and credit card businesses. The continuing decline in operating expenses led to an increase in gross operating profit by 40% to CHF 581 m.As a result, the cost/income ratio improved by 7.7 percentage points to 66.8%.

Valuation adjustments, provisions and losses amounted to CHF 303 m. This figure includes statistically determined credit risk costs of CHF 300 m and CHF 3 m in other provisions. Effective valuation adjustments were CHF 12 m lower than the statistically anticipated value. Overall, the risk profile of the credit portfolio again developed positively.

With a net profit of CHF 201 m, CreditSuisse posted a profit for the first half of1999 which is almost equivalent to the profitfor the whole of 1998. The ROE after tax rosefrom 2.4% to 9.2%.

BALANCE SHEET

Cash and other liquid assets

Money market claims

Due from banks

Due from other business units

Due from customers

Mortgages

Securities and precious metals tradingportfolio

Financial investments

Participations

Tangible fixed assets

Accrued income and prepaid expenses

Other assets

TOTAL ASSETS

Money market liabilities

Due to banks

Due to other business units

Due to customers in savings andinvestment accounts

Due to customers, other

Medium-term notes

Bonds and mortgage-backed bonds

Accrued expenses and deferred income

Other liabilities

Valuation adjustments and provisions

Capital

– of which minority interests

TOTAL LIABILITIES

RATIOS/KEY PERFORMANCE INDICATORS

1st half 1999 1998

Average allocated equity capital CHF m 4,409 4,183

Allocated equity capital

CHF m (1 July/1 January 1999) 4,389 4,450

Cost/income ratio 66.8% 74.5%

Return on average equity capital 9.2% 2.4%

Number of employees (30.6/31.12) 11,714 11,729

Pre-tax margin 16.1% 4.3%

Staff expenses/operating expenses 61.6% 64.0%

Staff expenses/total income 40.4% 47.0%

Number of branches (30.6/31.12) 241 241

Net interest margin 2.37% 2.20%

Loan growth (30.6/31.12) 3.8% 5.7%

Deposit/loan ratio (30.6/31.12) 68.7% 71.8%

Assets under management

CHF bn (30.6/31.12) 126 120

30 June 1999in CHF m

1,139

532

479

975

26,631

61,141

1,515

1,731

34

2,269

237

693

97,376

0

1,263

19,486

36,350

24,124

4,687

5,203

580

998

133

4,552

9

97,376

31 Dec.1998in CHF m

869

563

633

1,187

26,245

58,596

54

1,873

49

2,278

194

894

93,435

0

1,888

13,101

37,429

23,517

5,841

5,399

548

903

169

4,640

10

93,435

Changein %

31

–6

–24

–18

1

4

–

–8

–31

0

22

–22

4

–

–33

49

–3

3

–20

–4

6

11

–21

–2

–10

4

13

1st half 1998in CHF m

446

1,350

265

84

2,145

644

358

1,002

1,143

17

4

67

1,059

35

27

230

837

8

829

58

Changein %

–6

9

9

–20

5

11

3

8

2

24

0

–42

5

–74

–74

6

4

13

4

1st half 1999in CHF m

420

1,474

289

67

2,250

713

368

1,081

1,169

21

4

39

1,109

9

7

243

868

9

859

–9

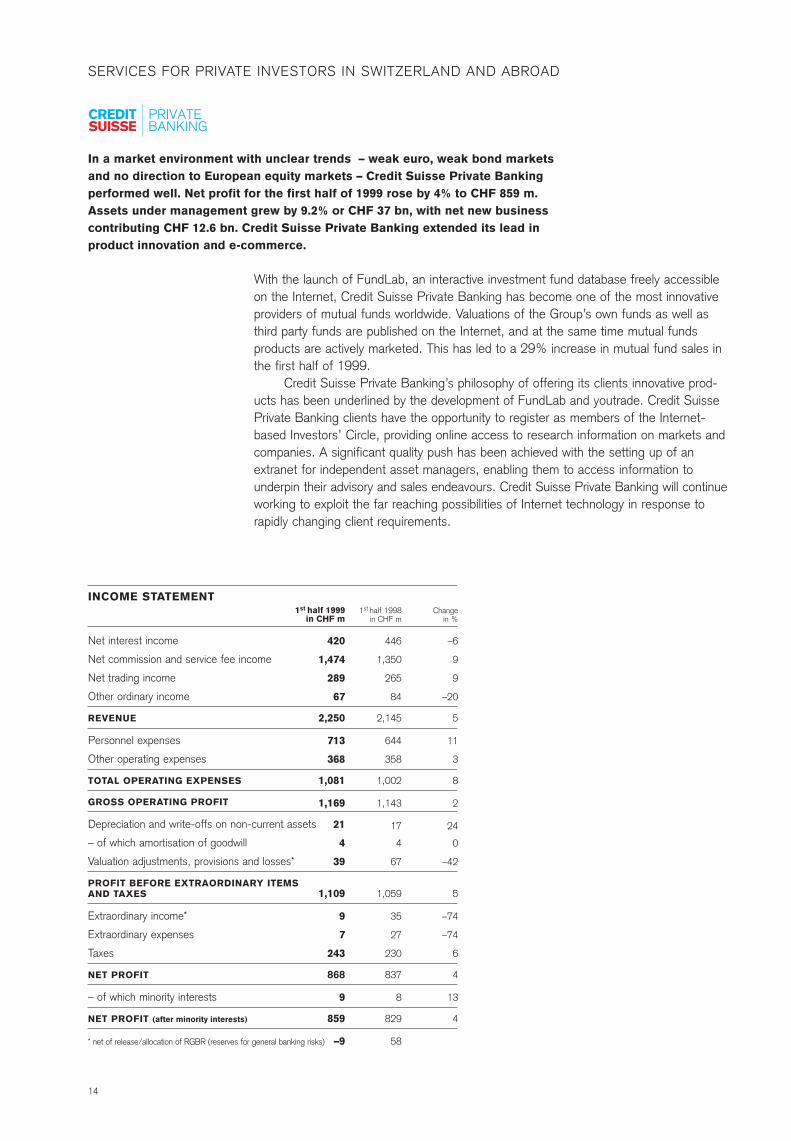

INCOME STATEMENT

Net interest income

Net commission and service fee income

Net trading income

Other ordinary income

REVENUE

Personnel expenses

Other operating expenses

TOTAL OPERATING EXPENSES

GROSS OPERATING PROFIT

Depreciation and write-offs on non-current assets

– of which amortisation of goodwill

Valuation adjustments, provisions and losses*

PROFIT BEFORE EXTRAORDINARY ITEMSAND TAXES

Extraordinary income*

Extraordinary expenses

Taxes

NET PROFIT

– of which minority interests

NET PROFIT (after minority interests)

* net of release/allocation of RGBR (reserves for general banking risks)

With the launch of FundLab, an interactive investment fund database freely accessibleon the Internet, Credit Suisse Private Banking has become one of the most innovativeproviders of mutual funds worldwide. Valuations of the Group’s own funds as well asthird party funds are published on the Internet, and at the same time mutual fundsproducts are actively marketed. This has led to a 29% increase in mutual fund sales inthe first half of 1999.

Credit Suisse Private Banking’s philosophy of offering its clients innovative prod-ucts has been underlined by the development of FundLab and youtrade. Credit SuissePrivate Banking clients have the opportunity to register as members of the Internet-based Investors’ Circle, providing online access to research information on markets andcompanies. A significant quality push has been achieved with the setting up of anextranet for independent asset managers, enabling them to access information tounderpin their advisory and sales endeavours. Credit Suisse Private Banking will continueworking to exploit the far reaching possibilities of Internet technology in response torapidly changing client requirements.

In a market environment with unclear trends – weak euro, weak bond marketsand no direction to European equity markets – Credit Suisse Private Banking performed well. Net profit for the first half of 1999 rose by 4% to CHF 859 m.Assets under management grew by 9.2% or CHF 37 bn, with net new businesscontributing CHF 12.6 bn. Credit Suisse Private Banking extended its lead inproduct innovation and e-commerce.

SERVICES FOR PRIVATE INVESTORS IN SWITZERLAND AND ABROAD

14

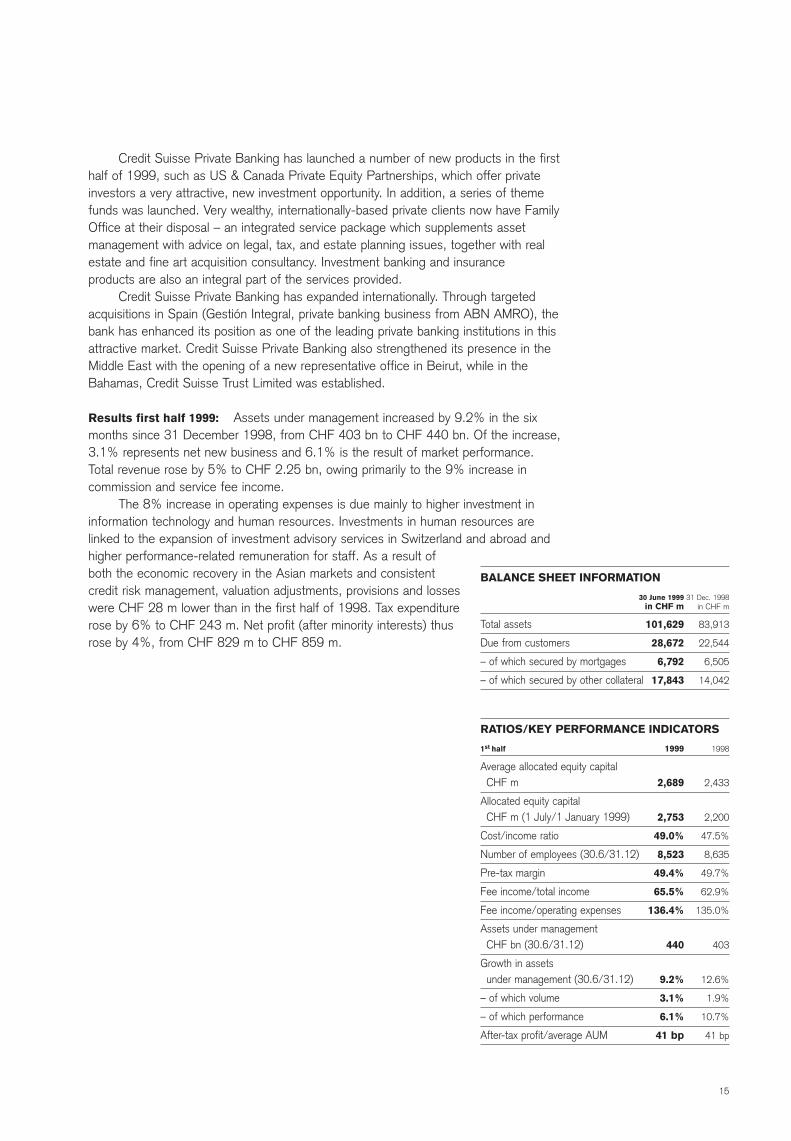

Credit Suisse Private Banking has launched a number of new products in the firsthalf of 1999, such as US & Canada Private Equity Partnerships, which offer privateinvestors a very attractive, new investment opportunity. In addition, a series of themefunds was launched. Very wealthy, internationally-based private clients now have FamilyOffice at their disposal – an integrated service package which supplements asset management with advice on legal, tax, and estate planning issues, together with realestate and fine art acquisition consultancy. Investment banking and insurance products are also an integral part of the services provided.

Credit Suisse Private Banking has expanded internationally. Through targeted acquisitions in Spain (Gestión Integral, private banking business from ABN AMRO), thebank has enhanced its position as one of the leading private banking institutions in thisattractive market. Credit Suisse Private Banking also strengthened its presence in theMiddle East with the opening of a new representative office in Beirut, while in theBahamas, Credit Suisse Trust Limited was established.

Results first half 1999: Assets under management increased by 9.2% in the sixmonths since 31 December 1998, from CHF 403 bn to CHF 440 bn. Of the increase,3.1% represents net new business and 6.1% is the result of market performance. Total revenue rose by 5% to CHF 2.25 bn, owing primarily to the 9% increase in commission and service fee income.

The 8% increase in operating expenses is due mainly to higher investment ininformation technology and human resources. Investments in human resources arelinked to the expansion of investment advisory services in Switzerland and abroad andhigher performance-related remuneration for staff. As a result ofboth the economic recovery in the Asian markets and consistentcredit risk management, valuation adjustments, provisions and losseswere CHF 28 m lower than in the first half of 1998. Tax expenditurerose by 6% to CHF 243 m. Net profit (after minority interests) thusrose by 4%, from CHF 829 m to CHF 859 m.

BALANCE SHEET INFORMATION

30 June 1999 31 Dec. 1998in CHF m in CHF m

Total assets 101,629 83,913

Due from customers 28,672 22,544

– of which secured by mortgages 6,792 6,505

– of which secured by other collateral 17,843 14,042

RATIOS/KEY PERFORMANCE INDICATORS

1st half 1999 1998

Average allocated equity capital CHF m 2,689 2,433

Allocated equity capitalCHF m (1 July/1 January 1999) 2,753 2,200

Cost/income ratio 49.0% 47.5%

Number of employees (30.6/31.12) 8,523 8,635

Pre-tax margin 49.4% 49.7%

Fee income/total income 65.5% 62.9%

Fee income/operating expenses 136.4% 135.0%

Assets under management CHF bn (30.6/31.12) 440 403

Growth in assets under management (30.6/31.12) 9.2% 12.6%

– of which volume 3.1% 1.9%

– of which performance 6.1% 10.7%

After-tax profit/average AUM 41 bp 41 bp

15

Changein %

–4

76

15

538

991

16

21

8

18

11

61

–

97

–7

–100

–100

–7

–7

–97

–2

1st half 1999in CHF m

3,564

2,450

1,506

74

–174

7,420

4,010

1,200

5,210

2,210

219

32

497

1,494

0

0

478

1,016

2

1,014

58

1st half 1998in CHF m

3,775

1,411

1,331

11

–16

6,512

3,366

1,128

4,494

2,018

138

1

256

1,624

9

4

521

1,108

57

1,051

82

Changein %

–6

74

13

573

988

14

19

6

16

10

59

–

94

–8

–100

–100

–8

–8

–96

–4

1st half 1999in USD m

2,458

1,690

1,038

51

–120

5,117

2,766

827

3,593

1,524

151

22

343

1,030

0

0

330

700

1

699

40

1st half 1998in USD m

2,568

960

905

8

–11

4,430

2,290

767

3,057

1,373

94

0

174

1,105

6

3

354

754

39

715

56

INCOME STATEMENT

Fixed Income & Derivatives

Equity

Corporate and Investment Banking

Private Equity

Other

REVENUE

Personnel expenses

Other operating expenses

TOTAL OPERATING EXPENSES

GROSS OPERATING PROFIT

Depreciation and write-offs on non-current assets

– of which amortisation of goodwill

Valuation adjustments, provisions and losses*

PROFIT BEFORE EXTRAORDINARY ITEMS AND TAXES

Extraordinary income*

Extraordinary expenses

Taxes

NET LOSS/PROFIT

– of which minority interests

NET PROFIT (after minority interests)

* net of release of RGBR (reserves for general banking risks)The business unit income statement differs from the Group’s legal accounts in presenting brokerage, execution and clearing expenses as part of operating expenses incommon with US competitors, rather than netted against revenues.

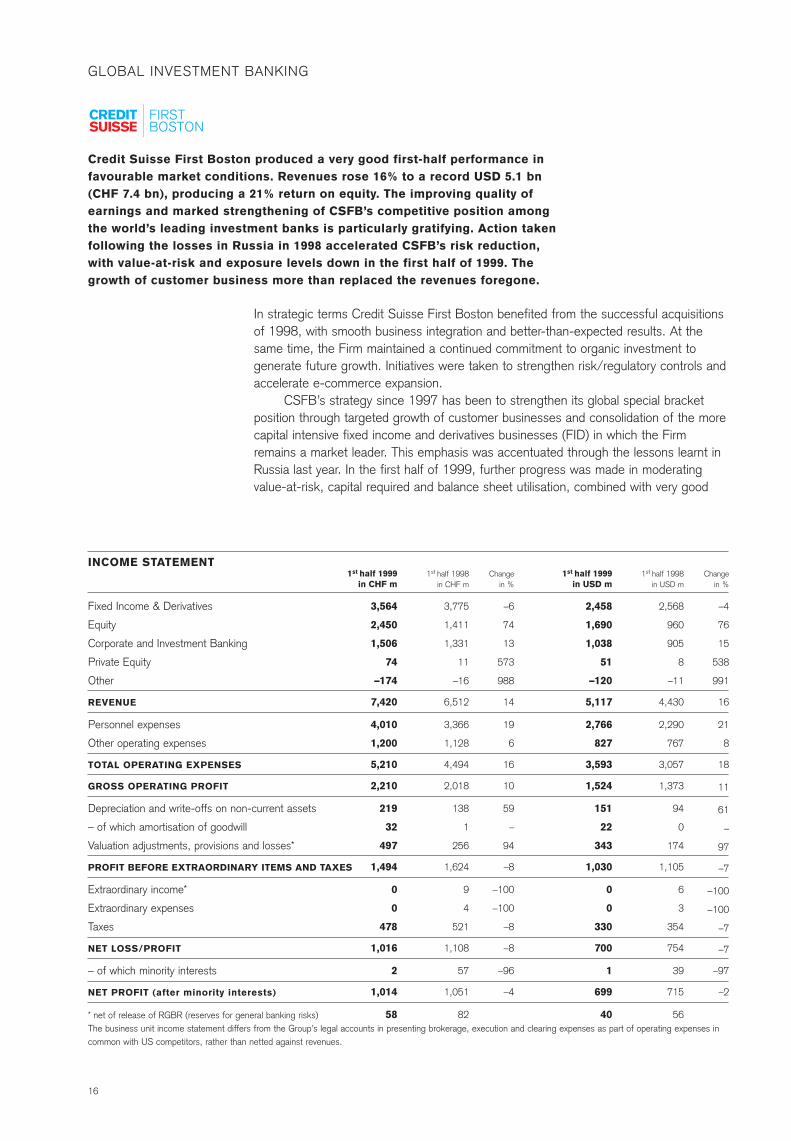

Credit Suisse First Boston produced a very good first-half performance infavourable market conditions. Revenues rose 16% to a record USD 5.1 bn(CHF 7.4 bn), producing a 21% return on equity. The improving quality ofearnings and marked strengthening of CSFB’s competitive position amongthe world’s leading investment banks is particularly gratifying. Action takenfollowing the losses in Russia in 1998 accelerated CSFB’s risk reduction,with value-at-risk and exposure levels down in the first half of 1999. Thegrowth of customer business more than replaced the revenues foregone.

GLOBAL INVESTMENT BANKING

In strategic terms Credit Suisse First Boston benefited from the successful acquisitionsof 1998, with smooth business integration and better-than-expected results. At thesame time, the Firm maintained a continued commitment to organic investment to generate future growth. Initiatives were taken to strengthen risk/regulatory controls andaccelerate e-commerce expansion.

CSFB’s strategy since 1997 has been to strengthen its global special bracket position through targeted growth of customer businesses and consolidation of the morecapital intensive fixed income and derivatives businesses (FID) in which the Firmremains a market leader. This emphasis was accentuated through the lessons learnt inRussia last year. In the first half of 1999, further progress was made in moderating value-at-risk, capital required and balance sheet utilisation, combined with very good

16

growth in customer business. The new “Strategic Risk Management” function hasalready made a strong contribution, especially to improving the quality of risk review andin reducing risk concentrations.

Credit Suisse First Boston has come through a very demanding period with anexcellent earnings recovery underpinned by strong market share advances and furtherinvestment in the future. Stability of people, strategic direction and investment supportthis achievement. The second half is unlikelyto offer such strong market conditions, butthe Firm is increasingly well positioned to faceits competitive challenges.

Results first half 1999: The conditions inthe financial markets were good overall duringthe first six months of the year, although theydeteriorated during the second quarter in anumber of fixed income areas. Strong rev-enue growth (16%) off 1998’s record first-half base reflects market share gains acrossthe board. The Firm’s quality of earningsimproved, with diversification in favour ofequities and investment banking and the cus-tomer segments of fixed income and deriva-tives businesses. Precautionary credit andrelated reserves were high based on anincreased medium-term cautionary outlook.The Firm’s business mix changed to greaterclient orientation reflecting a less capital-intensive, more people-intensive strategy.Consequently, average allocated equity forthe first half of 1999 declined 6% comparedto 1998, whilst a strong 8.4%* BIS tier 1 ratio was maintained; the pre-tax margindeclined due to this mix change, with employee headcount up 5% over the last

* applies to the bank Credit Suisse First Boston; core capital in-cludes USD 125 m noncumulative preferred stock issued by a subsidiary and sold to unaffiliated investors

30 June 1999in CHF m

822

21,811

154,773

107,771

1,837

70,221

37,140

9,658

108,389

7,343

754

2,372

526

6,895

43,732

40,262

429,133

276,860

18,887

215,904

66,894

17,722

134

77,481

36,373

33,233

7,638

44,715

41,217

2,107

11,312

2,263

429,133

276,860

RATIOS/KEY PERFORMANCE INDICATORS

1st half 1999 1998

Average allocated equity capital CHF m 9,910 10,567

Allocated equity capital CHF m (1 July/1 January 1999) 10,555 9,340

BIS tier 1 ratio* 8.4% 8.4%

Cost/income ratio 73.2% 71.1%

Return on average equity capital 20.5% 21.0%

Number of employees (30.6/31.12) 14,394 14,126

Pre-tax margin 20.1% 25.0%

Staff expenses/total expenses 77.0% 74.9%

Staff expenses/total income 54.1% 51.7%

Changein %

–30

16

12

38

–3

14

30

35

7

–27

73

22

–2

1

–12

–13

7

–5

–5

16

–11

8

–26

9

60

–1

–14

–16

–17

29

15

30

7

–5

31 Dec. 1998in CHF m

1,175

18,860

138,726

78,303

1,894

61,522

28,634

7,178

100,963

10,072

436

1,947

535

6,845

49,555

46,347

399,708

290,697

19,923

185,335

74,915

16,350

180

71,157

22,714

33,464

8,844

53,007

49,481

1,638

9,810

1,743

399,708

290,697

BALANCE SHEET

Cash

Money market paper

Due from banks

– of which securities lending andreverse repurchase agreements

Due from other business units

Due from customers

– of which securities lending andreverse repurchase agreements

Mortgages

Securities and precious metalstrading portfolio

Financial investments

Participations

Tangible fixed assets

Goodwill

Accrued income and prepaid expenses

Other assets

– of which replacement value of derivatives

TOTAL ASSETS

TOTAL ASSETS in USD m

Money market liabilities

Due to banks

– of which securities borrowing and repurchase agreements

Due to other business units

Due to customers, in savingsand investment deposits

Due to customers, other

– of which securities borrowing andrepurchase agreements

Bonds and mortgage-backed bonds

Accrued expenses and deferred income

Other liabilities

– of which replacement value of derivatives

Valuation adjustments and provisions

Capital

– of which minority interests

TOTAL LIABILITIES

TOTAL LIABILITIES in USD m

17

18

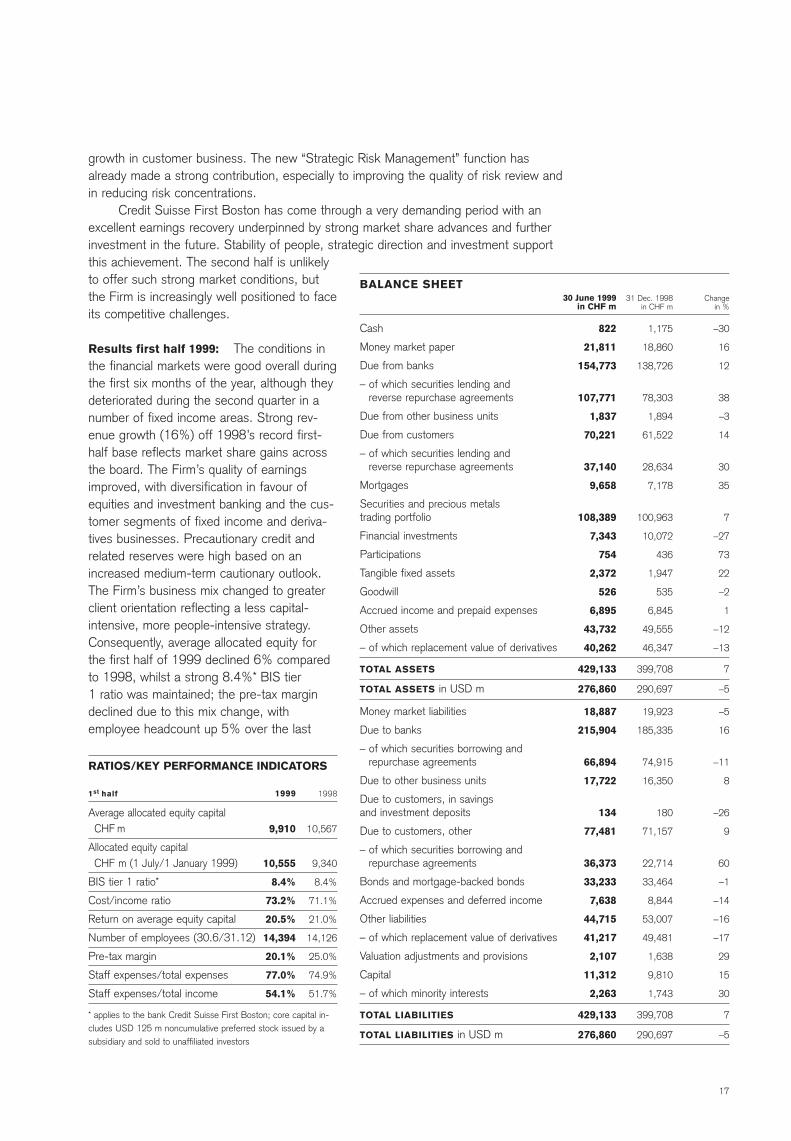

12 months. Operating expenses pre-bonuses rose 9%, owing to the headcountincrease. Total compensation accruals rose as a result of revenue increases, businessmix and competitor accruals.

In geographic terms, CSFB’s unique balance was again reflected by revenuessplit 39% North America, 35% Europe and 26% the rest of the world. The individualdivisions performed as follows (percentages reflect dollar figures):Equities: Revenues increased 76%, with ROE significantly exceeding 30% despitecontinued investment in people for further growth. The “cash” businesses boosted revenues by over 100% from the previous year’s record first-half base, while derivativesand other equity businesses also saw strong gains. Growth came from all geographicregions. Excellent gains in primary and secondary market shares and in research rank-ings around the world underpin this success. The positive impact of CSFB’s expandedtechnology industry activities particularly benefited Equities (and Investment Banking).Fixed Income & Derivatives (FID): In the first half, FID successfully tackled themajor challenges of integrating Credit Suisse Financial Products (following the repur-chase of the 20% minority stake from Swiss Re in April) and restructuring the divisionto accommodate tighter risk disciplines and capital availability. Despite reduced profitpotential following this risk reduction, revenues were held at the record levels of thefirst half of 1998, achieving a creditable 23% ROE. The merged activities in InterestRate and Credit Products enjoyed excellent growth, while Emerging Markets’ earningsstayed similar to the previous year’s first half. The outstanding performance in LatinAmerica offset the Russian gap and complemented good results from other regions.

A good recovery in Distressed Securities’ performance compensated declines inForeign Exchange and Money Markets. Real Estate products did not contribute to prof-its (compared to 15% of CSFB’s total in the first half of 1998), reflecting a precau-tionary reduction in risk concentration and increased provisioning levels. CSFB’s debtcapital markets underwriting position strengthened further to a global ranking of four.Investment Banking (IBD): Revenues increased 15%, with improved profitabilitydespite large reductions in net interest income due to a smaller loan book and theresultant 66% reduction in capital employed since 1997 (now on target at below USD1 bn). Underlying growth was excellent, with M&A revenues the star performer, up79% on the comparable 1998 period, and other investment banking product resultsalso rose. Credit Suisse First Boston has expanded its client coverage capacity in IBDsubstantially during the last 18 months. While this heavy investment implies an initialdrag on profits, the resultant market share gains, complementing those of Equities,enhance CSFB’s prospects for growth and diversified earnings.Private Equity: The investment of CSFB’s globally managed private equity funds,totalling USD 3.6 bn, is now accelerating. The current level of revenues reflect limitedharvesting of previous investments. Personnel was strengthened further in Europe.

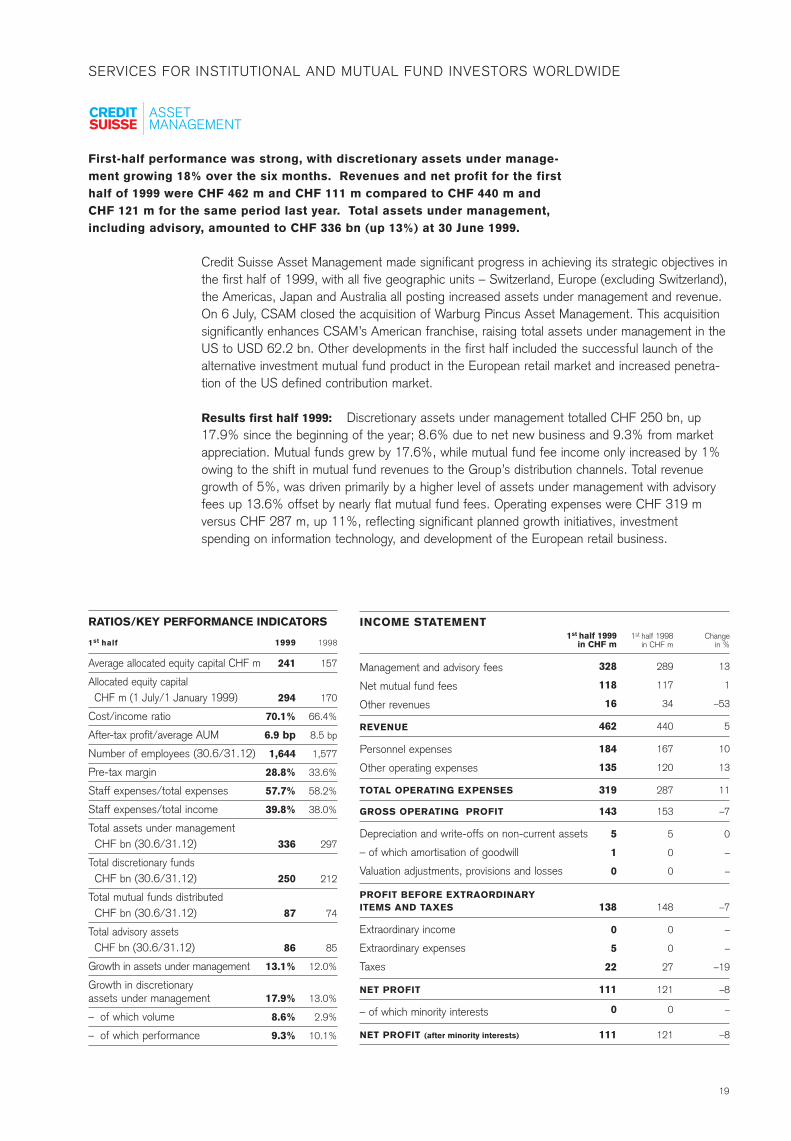

First-half performance was strong, with discretionary assets under manage-ment growing 18% over the six months. Revenues and net profit for the firsthalf of 1999 were CHF 462 m and CHF 111 m compared to CHF 440 m andCHF 121 m for the same period last year. Total assets under management,including advisory, amounted to CHF 336 bn (up 13%) at 30 June 1999.

SERVICES FOR INSTITUTIONAL AND MUTUAL FUND INVESTORS WORLDWIDE

Credit Suisse Asset Management made significant progress in achieving its strategic objectives inthe first half of 1999, with all five geographic units – Switzerland, Europe (excluding Switzerland),the Americas, Japan and Australia all posting increased assets under management and revenue.On 6 July, CSAM closed the acquisition of Warburg Pincus Asset Management. This acquisitionsignificantly enhances CSAM’s American franchise, raising total assets under management in theUS to USD 62.2 bn. Other developments in the first half included the successful launch of thealternative investment mutual fund product in the European retail market and increased penetra-tion of the US defined contribution market.

Results first half 1999: Discretionary assets under management totalled CHF 250 bn, up17.9% since the beginning of the year; 8.6% due to net new business and 9.3% from marketappreciation. Mutual funds grew by 17.6%, while mutual fund fee income only increased by 1%owing to the shift in mutual fund revenues to the Group’s distribution channels. Total revenuegrowth of 5%, was driven primarily by a higher level of assets under management with advisoryfees up 13.6% offset by nearly flat mutual fund fees. Operating expenses were CHF 319 m versus CHF 287 m, up 11%, reflecting significant planned growth initiatives, investment spending on information technology, and development of the European retail business.

1st half 1998in CHF m

289

117

34

440

167

120

287

153

5

0

0

148

0

0

27

121

0

121

Changein %

13

1

–53

5

10

13

11

–7

0

–

–

–7

–

–

–19

–8

–

–8

1st half 1999in CHF m

328

118

16

462

184

135

319

143

5

1

0

138

0

5

22

111

0

111

INCOME STATEMENT

Management and advisory fees

Net mutual fund fees

Other revenues

REVENUE

Personnel expenses

Other operating expenses

TOTAL OPERATING EXPENSES

GROSS OPERATING PROFIT

Depreciation and write-offs on non-current assets

– of which amortisation of goodwill

Valuation adjustments, provisions and losses

PROFIT BEFORE EXTRAORDINARYITEMS AND TAXES

Extraordinary income

Extraordinary expenses

Taxes

NET PROFIT

– of which minority interests

NET PROFIT (after minority interests)

RATIOS/KEY PERFORMANCE INDICATORS

1st half 1999 1998

Average allocated equity capital CHF m 241 157

Allocated equity capital CHF m (1 July/1 January 1999) 294 170

Cost/income ratio 70.1% 66.4%

After-tax profit/average AUM 6.9 bp 8.5 bp

Number of employees (30.6/31.12) 1,644 1,577

Pre-tax margin 28.8% 33.6%

Staff expenses/total expenses 57.7% 58.2%

Staff expenses/total income 39.8% 38.0%

Total assets under managementCHF bn (30.6/31.12) 336 297

Total discretionary fundsCHF bn (30.6/31.12) 250 212

Total mutual funds distributed CHF bn (30.6/31.12) 87 74

Total advisory assetsCHF bn (30.6/31.12) 86 85

Growth in assets under management 13.1% 12.0%

Growth in discretionaryassets under management 17.9% 13.0%

– of which volume 8.6% 2.9%

– of which performance 9.3% 10.1%

19

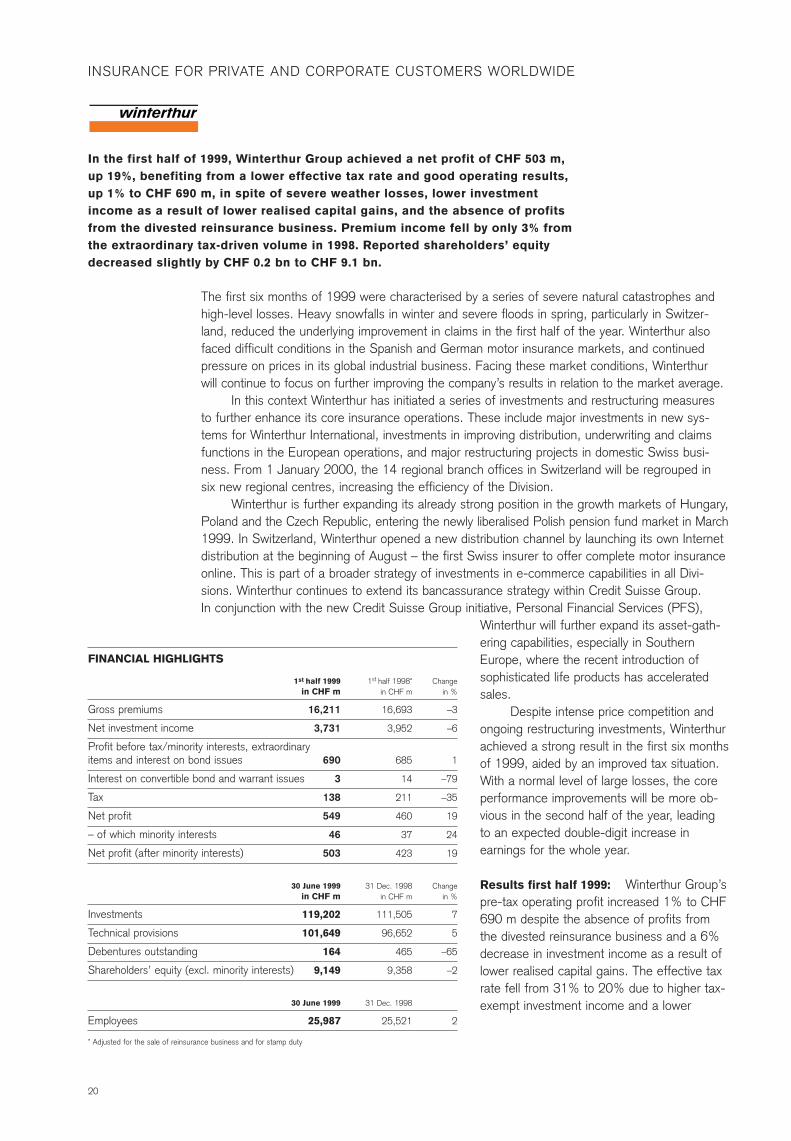

In the first half of 1999, Winterthur Group achieved a net profit of CHF 503 m,up 19%, benefiting from a lower effective tax rate and good operating results,up 1% to CHF 690 m, in spite of severe weather losses, lower investmentincome as a result of lower realised capital gains, and the absence of profitsfrom the divested reinsurance business. Premium income fell by only 3% fromthe extraordinary tax-driven volume in 1998. Reported shareholders’ equitydecreased slightly by CHF 0.2 bn to CHF 9.1 bn.

INSURANCE FOR PRIVATE AND CORPORATE CUSTOMERS WORLDWIDE

The first six months of 1999 were characterised by a series of severe natural catastrophes andhigh-level losses. Heavy snowfalls in winter and severe floods in spring, particularly in Switzer-land, reduced the underlying improvement in claims in the first half of the year. Winterthur alsofaced difficult conditions in the Spanish and German motor insurance markets, and continuedpressure on prices in its global industrial business. Facing these market conditions, Winterthur will continue to focus on further improving the company’s results in relation to the market average.

In this context Winterthur has initiated a series of investments and restructuring measuresto further enhance its core insurance operations. These include major investments in new sys-tems for Winterthur International, investments in improving distribution, underwriting and claimsfunctions in the European operations, and major restructuring projects in domestic Swiss busi-ness. From 1 January 2000, the 14 regional branch offices in Switzerland will be regrouped insix new regional centres, increasing the efficiency of the Division.

Winterthur is further expanding its already strong position in the growth markets of Hungary,Poland and the Czech Republic, entering the newly liberalised Polish pension fund market in March1999. In Switzerland, Winterthur opened a new distribution channel by launching its own Internetdistribution at the beginning of August – the first Swiss insurer to offer complete motor insuranceonline. This is part of a broader strategy of investments in e-commerce capabilities in all Divi-sions. Winterthur continues to extend its bancassurance strategy within Credit Suisse Group. In conjunction with the new Credit Suisse Group initiative, Personal Financial Services (PFS),

Winterthur will further expand its asset-gath-ering capabilities, especially in SouthernEurope, where the recent introduction ofsophisticated life products has acceleratedsales.

Despite intense price competition andongoing restructuring investments, Winterthurachieved a strong result in the first six monthsof 1999, aided by an improved tax situation.With a normal level of large losses, the coreperformance improvements will be more ob-vious in the second half of the year, leadingto an expected double-digit increase in earnings for the whole year.

Results first half 1999: Winterthur Group’spre-tax operating profit increased 1% to CHF690 m despite the absence of profits fromthe divested reinsurance business and a 6%decrease in investment income as a result oflower realised capital gains. The effective taxrate fell from 31% to 20% due to higher tax-exempt investment income and a lower

FINANCIAL HIGHLIGHTS

1st half 1999 1st half 1998* Changein CHF m in CHF m in %

Gross premiums 16,211 16,693 –3

Net investment income 3,731 3,952 –6

Profit before tax/minority interests, extraordinaryitems and interest on bond issues 690 685 1

Interest on convertible bond and warrant issues 3 14 –79

Tax 138 211 –35

Net profit 549 460 19

– of which minority interests 46 37 24

Net profit (after minority interests) 503 423 19

30 June 1999 31 Dec. 1998 Changein CHF m in CHF m in %

Investments 119,202 111,505 7

Technical provisions 101,649 96,652 5

Debentures outstanding 164 465 –65

Shareholders’ equity (excl. minority interests) 9,149 9,358 –2

30 June 1999 31 Dec. 1998

Employees 25,987 25,521 2

* Adjusted for the sale of reinsurance business and for stamp duty

20

corporate rate in Switzerland for 1999. As aconsequence, net profits rose 19% to CHF503 m.

As expected, gross premiums declinedby 3% to CHF 16.2 bn at 30 June 1999.Given the extraordinary tax-driven surge ofSwiss life premiums in the first quarter of1998 (life premiums were up 39% in the firstsix months of 1998), the 7% decline in life premiums for the first half still represents a strong 1999 performance. As a better indication of core growth, the compounded annual growth rate for the half years1997–1999 was 14%. Non-life businessgrew 2% in the first half of 1999. Invest-ments rose by 7% to CHF 119.2 bn, whilereported shareholders’ equity decreased byCHF 210 m, or 2%, and now stands at CHF 9.1 bn.Results for non-life business: Even withthe extraordinary weather-related losses, allkey performance indicators improved. Thecombined ratio (sum total of claims ratio,expense ratio and dividends to policyholdersincurred) improved slightly from 110.1% to109.6%; a CHF 45 m reduction in actualexpenses brought the overall expense ratiodown to 30.9%. Net investment incomedecreased by 15% compared with the previ-ous year. Overall, the result (before tax andminority interests) amounted to CHF 358 m,2% below the 1998 first-half result of CHF 366 m which included an estimated CHF 35 m of profits from the divested reinsurance business.Results from life business: The expenseratio rose from 8.0% to 9.1%, again due tothe high level of Swiss life insurance sales(and low resulting expense ratio) in 1998.Actual expenses rose only 4% year-on-year,with an expense ratio significantly below the11.2 of the first half of 1997. Claims incurredrose by 9%, while the charge to actuarial pro-visions was reduced by 15%. Net investmentincome decreased by 2%. Net profits (beforeextraordinary items, tax and minority interests)increased 4% from CHF 319 m to a solidCHF 332 m in the first half of 1999.

1st half 1999in CHF m

8,534

8,490

7,683

–3,665

–4,948

–857

–697

2,821

72

–63

–92

78

332

89,942

78,403

9.1%

Changein %

–7

–7

–9

9

–15

–20

4

–2

–25

21

–12

169

4

7

4

1st half 1998*in CHF m

9,203

9,153

8,427

–3,365

–5,850

–1,070

–673

2,882

96

–52

–105

29

319

84,178

75,189

8.0%

LIFE OPERATIONS

Gross premiums

Net premiums

Premiums earned, net

Claims incurred, net

Change in actuarial provision, net

Allocation to participation, net

Operating expenses, net(including commissions paid)

Net investment income

Interest on deposits and bank accounts

Interest on bonuses credited to policyholders

Other interest paid

Other income and expenses (including exchange rate differences)

PROFIT(before extraordinary items, tax, minority interests)

Investments (30.6/31.12)

Technical provisions (30.6/31.12)

Expense ratio

1st half 1999in CHF m

7,677

7,020

5,841

–4,458

–136

–1,805

–558

910

47

–32

–9

358

29,260

23,246

109.6%

76.3%

30.9%

2.3%

Changein %

2

0

0

–1

32

–2

–6

–15

–30

–11

–94

–2

7

8

1st half 1998*in CHF m

7,490

7,035

5,847

–4,487

–103

–1,850

–593

1,070

67

–36

–142

366

27,327

21,463

110.1%

76.7%

31.6%

1.8%

NON-LIFE OPERATIONS

Gross premiums

Net premiums

Premiums earned, net

Claims incurred, net

Dividends to policyholders incurred, net

Operating expenses, net(including commissions paid)

UNDERWRITING RESULT, NET

Net investment income

Interest on deposits and bank accounts

Other interest paid

Other income and expenses(including exchange rate differences)

PROFIT(before extraordinary items, tax, minority interests)

Investments (30.6/31.12)

Technical provisions (30.6/31.12)

Combined ratio

Claims ratio

Expense ratio

Dividends to policyholders incurred

* Adjusted for the sale of reinsurance business and for stamp duty

21

Internet banking and web insuranceCredit Suisse Group is highly focused on developing the Internet as a key distribution channel. In thefirst few months of 1999, Credit Suisse Group launched additional online services. Youtrade, devel-oped by Credit Suisse and Credit Suisse Private Banking, was the first online discount brokeragefacility in Switzerland. The number of customers and transactions via youtrade are well ahead of plan.Through FundLab, an interactive investment fund database on the Internet, Credit Suisse PrivateBanking has become one of the most innovative fund distributors in the world. Credit Suisse FirstBoston remains a leader in institutional market making via the Internet, has extended its partnershipwith Charles Schwab and offers its research publications to customers online. At Winterthur, cus-tomers can now buy motor insurance policies on the web. In addition, plans are well advanced forWinterthur to become the first Swiss insurer to offer a complete line of insurance products over theInternet.

Personal Financial Services EuropeThrough the “Personal Financial Services Europe” strategy announced in March 1999, Credit SuisseGroup aims to combine the existing distribution and product capability of Credit Suisse Group withtechnology rich channels to directly target the needs of affluent customers in selected European mar-kets. The implementation of this strategy started well in the first half 1999, with the formation of adedicated team and work on the operations platform, product range and logistics. The pilot project inItaly, the new Credit Suisse (Italy), was officially launched in April 1999 and already has assets undermanagement of EUR 1.6 bn, well above expectations. The strategy will be implemented step by stepin key European markets.

Ready for the new millenniumCritical-system readiness is complete and non-critical systems are 96–99% complete in a Group-wide effort requiring more than 1,000 person years and costs of CHF 570 m. In addition, plans havebeen drawn up for processes and procedures which are dependent on the smooth functioning ofthird-party systems. Credit Suisse Group’s primary goal for the year 2000 is ensuring business asusual in all areas.

OutlookGiven the less favourable conditions on the financial markets since the beginning of the summer andexpectations of a challenging operating environment for the rest of the year, Credit Suisse Group’soverall performance in the second half of the year is not expected to match the strong results of thefirst six months. Nonetheless, the Group remains confident of achieving good results for the year as awhole and of making further advances in reaching its targets.

Yours sincerely

CLOSING

Rainer E. Gut Lukas MühlemannChairman of the Board of Directors Chief Executive Officer

22

CREDIT SUISSE GROUPParadeplatz 8 P.O. Box 1 8070 Zurich Switzerland

Telephone: + 41 1 212 16 16 Fax: + 41 1 333 25 87 Internet: http://www.csg.ch