DISCLOSURE APPENDIX CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, INFORMATION ON TRADE ALERTS, ANALYST MODEL PORTFOLIOS AND THE STATUS OF NON-U.S ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 08 October 2009 Americas/United States Equity Research Homebuilding / MARKET WEIGHT Monthly Survey of Real Estate Agents CHANNEL CHECK The Flurry before the Lull First-time buyers rush to take advantage of the tax credit; expecting slowdown in October. Our September survey of real estate agents showed a slight increase in traffic (our buyer traffic index increased to 44.8 in September, from 44.5 in August). We think this was nearly completely tied to first-time buyers attempting to purchase a home before the expiration of the first-time buyer tax credit on November 30th. We now have significantly greater concern that this tax credit has pulled forward demand and that we will likely see a lull in buyer traffic over the next several months and leads us to expect risk to homebuilding stocks in the near-term. Traffic from mid-October onward will be crucial. We think that traffic trends from mid-October onward will likely indicate if demand will continue at current levels after the tax credit expires, or if demand has been pulled forward. We saw a sharp decline in low-end new home traffic in September, as buyers of to-be-built homes needed to start the purchase process before September in order to close on the home prior to the end of November. With existing homes, it was feasible to sign a contract through September (and possibly early October) and to still have the closing before the end of November. Thus, we think that it will be crucial to see what happens to existing home traffic from mid-October onward, as it will then generally be too late for a buyer of an existing home to take advantage of the tax credit. Tax credit likely to be extended, but traffic will still suffer. We see a significant chance that the tax credit will be extended, but even so, we think that demand will fall off, as we do not think that consumers assumed that the credit would be extended so that most first-time buyers contemplating a purchase planned so that closing could occur prior to November 30th. Markets with strong traffic levels broaden out due to first-time buyers. Our survey pointed to the highest levels of traffic in Ft Myers, Seattle, Los Angeles, Orlando, Washington, D.C., Minneapolis, and Las Vegas. Several of these markets (Ft Myers, Los Angeles, Orlando, Washington, D.C., and Las Vegas) are repeats from past months based on the tremendous affordability resulting from the sharp home price declines, but others (Seattle and Minneapolis) saw strong demand, as the first-time buyer tax credit increased the activity. Research Analysts Daniel Oppenheim, CFA 212 325 5726 [email protected]Michael Dahl 212 325 5882 [email protected]

Transcript

DISCLOSURE APPENDIX CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, INFORMATION ON TRADE ALERTS, ANALYST MODEL PORTFOLIOS AND THE STATUS OF NON-U.S ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

08 October 2009Americas/United States

Equity ResearchHomebuilding / MARKET WEIGHT

Monthly Survey of Real Estate Agents

CHANNEL CHECK

The Flurry before the Lull ■ First-time buyers rush to take advantage of the tax credit; expecting

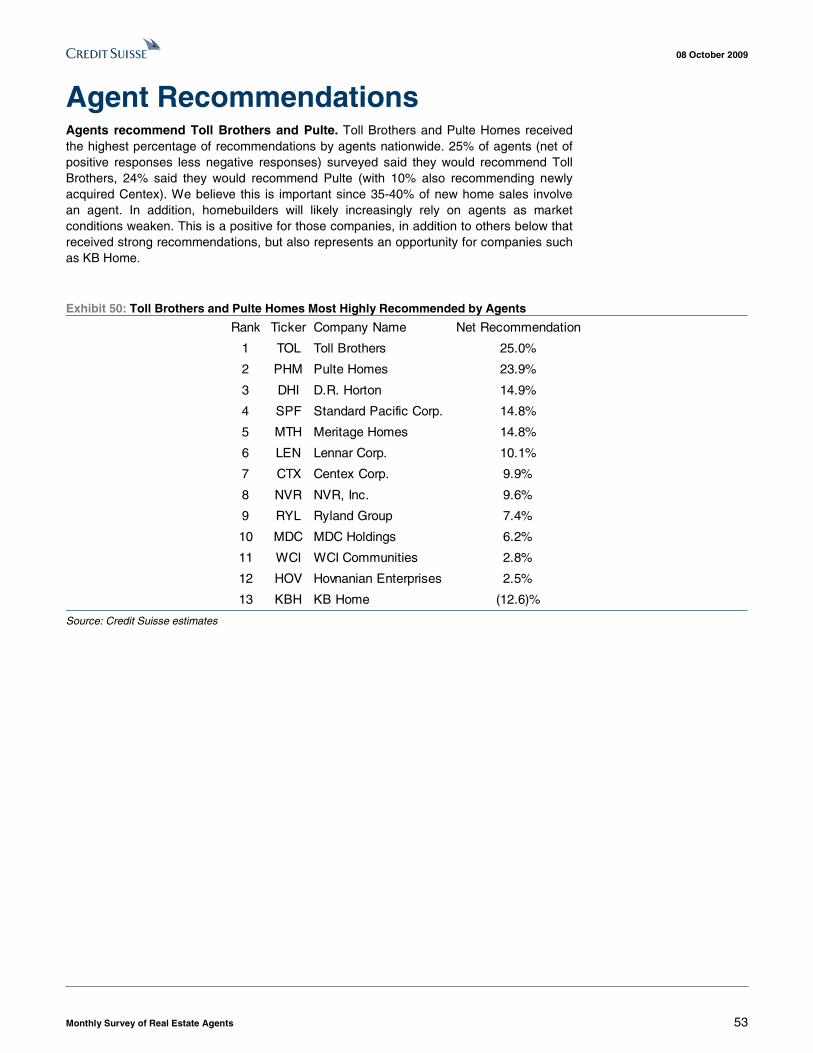

slowdown in October. Our September survey of real estate agents showed a slight increase in traffic (our buyer traffic index increased to 44.8 in September, from 44.5 in August). We think this was nearly completely tied to first-time buyers attempting to purchase a home before the expiration of the first-time buyer tax credit on November 30th. We now have significantly greater concern that this tax credit has pulled forward demand and that we will likely see a lull in buyer traffic over the next several months and leads us to expect risk to homebuilding stocks in the near-term.

■ Traffic from mid-October onward will be crucial. We think that traffic trends from mid-October onward will likely indicate if demand will continue at current levels after the tax credit expires, or if demand has been pulled forward. We saw a sharp decline in low-end new home traffic in September, as buyers of to-be-built homes needed to start the purchase process before September in order to close on the home prior to the end of November. With existing homes, it was feasible to sign a contract through September (and possibly early October) and to still have the closing before the end of November. Thus, we think that it will be crucial to see what happens to existing home traffic from mid-October onward, as it will then generally be too late for a buyer of an existing home to take advantage of the tax credit.

■ Tax credit likely to be extended, but traffic will still suffer. We see a significant chance that the tax credit will be extended, but even so, we think that demand will fall off, as we do not think that consumers assumed that the credit would be extended so that most first-time buyers contemplating a purchase planned so that closing could occur prior to November 30th.

■ Markets with strong traffic levels broaden out due to first-time buyers. Our survey pointed to the highest levels of traffic in Ft Myers, Seattle, Los Angeles, Orlando, Washington, D.C., Minneapolis, and Las Vegas. Several of these markets (Ft Myers, Los Angeles, Orlando, Washington, D.C., and Las Vegas) are repeats from past months based on the tremendous affordability resulting from the sharp home price declines, but others (Seattle and Minneapolis) saw strong demand, as the first-time buyer tax credit increased the activity.

Table of Contents Overview of Results………………………………..…..3

Survey Methodology…………………………………...5

Top 20 Housing Markets Atlanta, Georgia 7 Austin, Texas 8 Charlotte, North Carolina 9 Chicago, Illinois 10 Dallas, Texas 11 Denver, Colorado 12 Fort Myers, Florida 13 Houston, Texas 14 Jacksonville, Florida 15 Las Vegas, Nevada 16 Los Angeles, California 17 Miami, Florida 18 Minneapolis, Minnesota 19 New York-Northern New Jersey 20 Orlando, Florida 21 Phoenix, Arizona 22 Riverside-San Bernardino [Inland Empire], California 23 Seattle, Washington 24 Tampa, Florida 25 Washington, D.C. 26

Additional Key Housing Markets…………………… 27 Baltimore, Maryland 28 Boston, Massachusetts 29 Charleston, South Carolina 30 Cincinnati, Ohio 31 Columbus, Ohio 32 Detroit, Michigan 33 Nashville, Tennessee 34 Philadelphia-Southern New Jersey 35 Port St. Lucie, Florida 36 Portland, Oregon 37 Raleigh, North Carolina 38 Richmond, Virginia 39 Sacramento, California 40 San Antonio, Texas 41 San Diego, California 42 San Francisco, California 43 Sarasota, Florida 44 Tucson, Arizona 45 Virginia Beach, Virginia 46 Wilmington, North Carolina 47

Historical Survey Trends by Market……………… 48

*Markets are characterized based on permit activity and listed in Alphabetical order

08 October 2009

Monthly Survey of Real Estate Agents 3

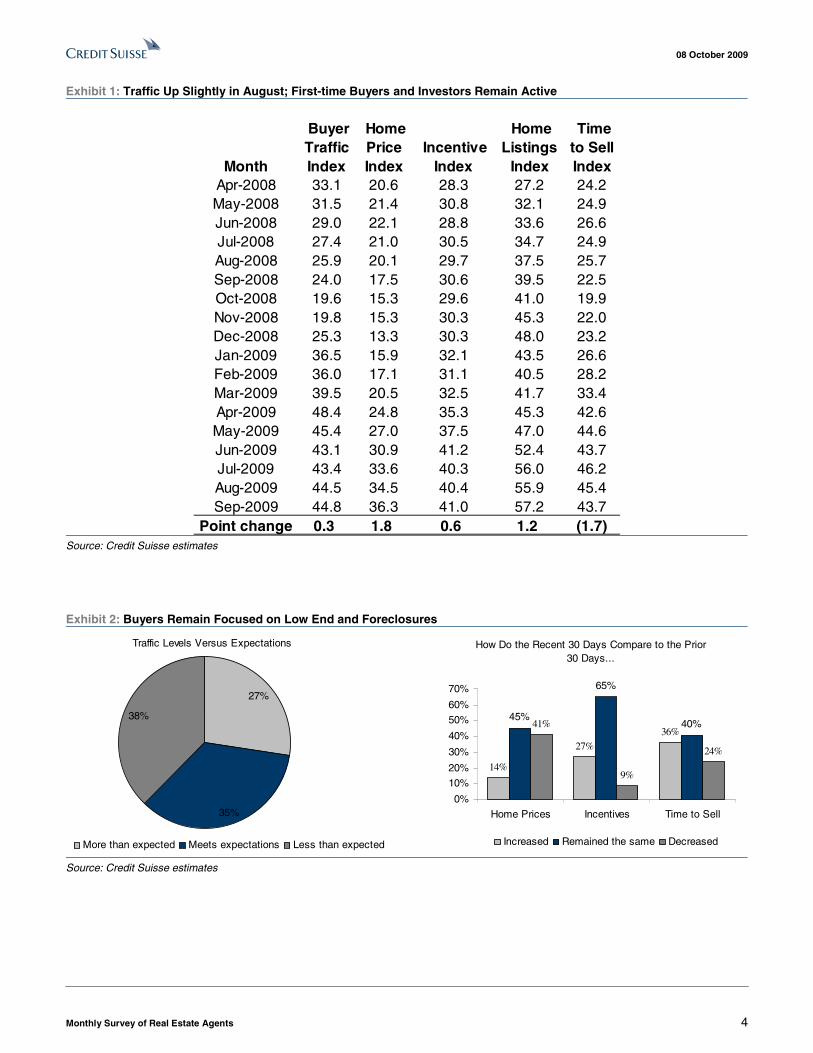

The Flurry before the Lull For those who may be unfamiliar with our survey, we center our indices around 50 so that readings above 50 indicate positive or improving trends and readings below 50 indicate negative or worsening trends. Please see page 5 for a full description of our survey methodology.

First-time buyers rush to take advantage of the tax credit; expecting slowdown in October. Our September survey of real estate agents showed a slight increase in traffic (our buyer traffic index increased to 44.8 in September, from 44.5 in August). We think this was nearly completely tied to first-time buyers attempting to purchase a home before the expiration of the first-time buyer tax credit on November 30th. We now have significantly greater concern that this tax credit has pulled forward demand and that we will likely see a lull in buyer traffic over the next several months and leads us to expect risk to homebuilding stocks in the near-term.

Traffic from mid-October onward will be crucial. We think that traffic trends from mid-October onward will likely indicate if demand will continue at current levels after the tax credit expires, or if demand has been pulled forward. We saw a sharp decline in low-end new home traffic in September, as buyers of to-be-built homes needed to start the purchase process before September in order to close on the home prior to the end of November. With existing homes, it was feasible to sign a contract through September (and possibly early October) and to still have the closing before the end of November. Thus, we think that it will be crucial to see what happens to existing home traffic from mid-October onward, as it will then generally be too late for a buyer of an existing home to take advantage of the tax credit.

Tax credit likely to be extended, but traffic will still suffer. We see a significant chance that the tax credit will be extended, but even so, we think that demand will fall off, as we do not think that consumers assumed that the credit would be extended so that most first-time buyers contemplating a purchase planned so that closing could occur prior to November 30th.

Markets with strong traffic levels broaden out as first-time buyers are active. Our survey pointed to the highest levels of traffic in Ft Myers, Seattle, Los Angeles, Orlando, Washington, D.C., Minneapolis, and Las Vegas. Several of these markets are repeats from past months based on the tremendous affordability resulting from the sharp home price declines, but others saw strong traffic, as the first-time buyer tax credit increased the activity.

Price stabilization at low end of the market, but will it last? Our price index moved slightly higher in September to 36.3, from 34.5 in August. We heard of the best pricing trends on low-end homes, likely due to the strength of the first-time buyer market and interest from investors. Agents indicated rising prices over the past 30 days in Ft Myers, the Inland Empire, Los Angeles, Phoenix, San Diego, San Francisco, and Washington, D.C. However, this price improvement may fall back should buyer traffic fall off (as expected following the end of the tax credit).

08 October 2009

Monthly Survey of Real Estate Agents 4

Exhibit 1: Traffic Up Slightly in August; First-time Buyers and Investors Remain Active

Exhibit 2: Buyers Remain Focused on Low End and Foreclosures

Traffic Levels Versus Expectations

35%

38%

27%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

14%

27%36%

45%

65%

40%41%

9%

24%

0%

10%

20%

30%

40%

50%

60%

70%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

08 October 2009

Monthly Survey of Real Estate Agents 5

Survey Methodology We survey real estate agents, as we believe that agents will provide an accurate assessment of housing market trends in both the new and existing home markets. Even though homebuilders sell new homes, we believe that it is crucial to have an understanding of the existing home market as the existing home market is substantially larger than the new home market (approximately 85%/15%) and trends in the existing home market dictate trends in the new home market.

Each month we ask five main questions, which are all listed below. In September, we received responses from 1,500 real estate agents across the country. We then review these responses and calculate an index for each of the questions with high numbers indicating positive or improving trends and low numbers indicating negative or worsening trends. An index of 50 would indicate a neutral trend. Note that for items such as incentives, a low index level would indicate a higher level of incentives, as higher incentives represent a negative trend. Similarly, for the number of listings and the length of time needed to sell a house, an increase in listings (a negative trend) and an increase in the time needed to sell a house (a negative trend) both correspond to low index values.

1) Are traffic levels in-line with, above, or below your expectations for this time of year? (Because of seasonality to traffic trends – generally more traffic in Spring and less in Fall/Winter – we ask about traffic relative to the expectations for this time of year rather than how traffic compared to the prior month.) A traffic index above 50 means that traffic was above the expectations of agents, a traffic index of 50 means that traffic was in-line with expectations, and a traffic index below 50 means that traffic was below expectations.

2) Have prices remained the same, increased, or decreased over the past 30 days? A price index above 50 indicates that prices increased over the past 30 days, a price index of 50 indicates that prices were flat, and a price index below 50 indicates that prices decreased.

3) Have incentives remained the same, increased, or decreased over the past 30 days? An incentive index above 50 indicates that incentives decreased over the past 30 days, an incentive index of 50 indicates that incentives were unchanged, and an incentive index below 50 indicates that incentives increased.

4) Do you see the same, more, or fewer, listings as compared with 30 days ago? An inventory (listings) index above 50 indicates that the inventory of homes for sale decreased over the past 30 days, an inventory index of 50 indicates that inventories were unchanged, and an inventory index below 50 indicates that inventories increased.

5) Does it take the same, more, or less time to sell a house? A time to sell index above 50 indicates that the time needed to sell a home decreased over the past 30 days, a time to sell index of 50 indicates that the time needed to sell a home was unchanged, and a time to sell index below 50 indicates that the time needed to sell a home increased.

08 October 2009

Monthly Survey of Real Estate Agents 6

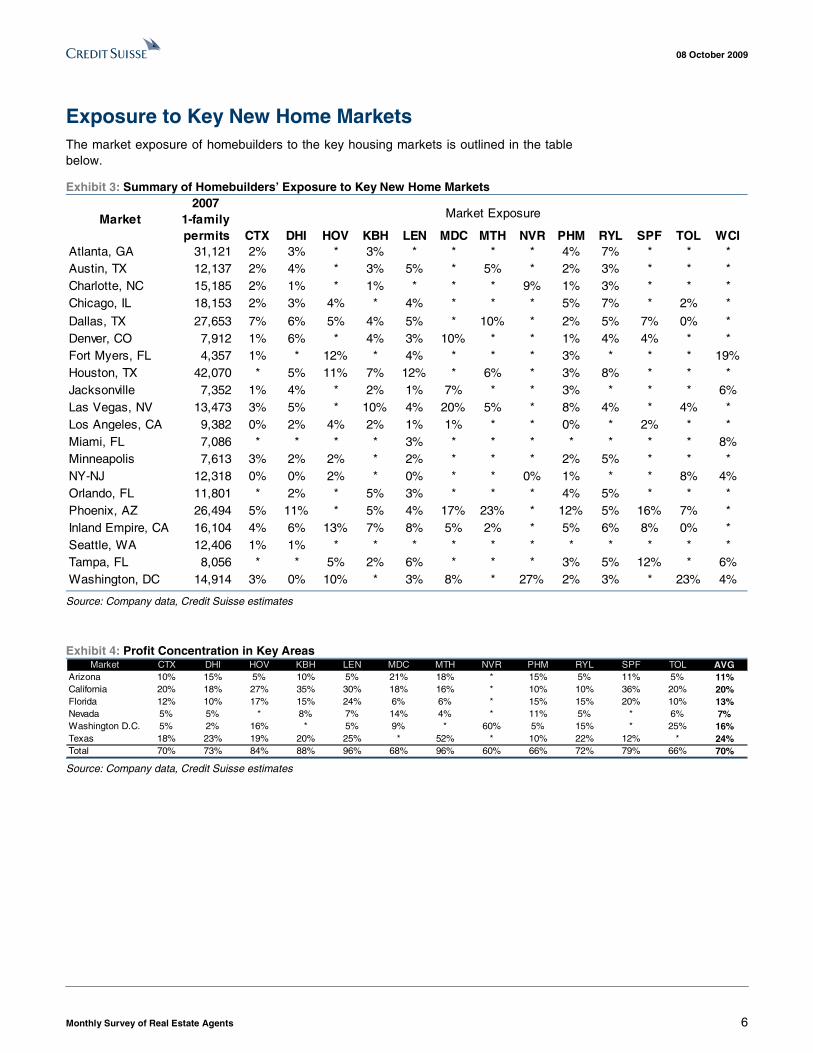

Exposure to Key New Home Markets The market exposure of homebuilders to the key housing markets is outlined in the table below.

Exhibit 3: Summary of Homebuilders’ Exposure to Key New Home Markets

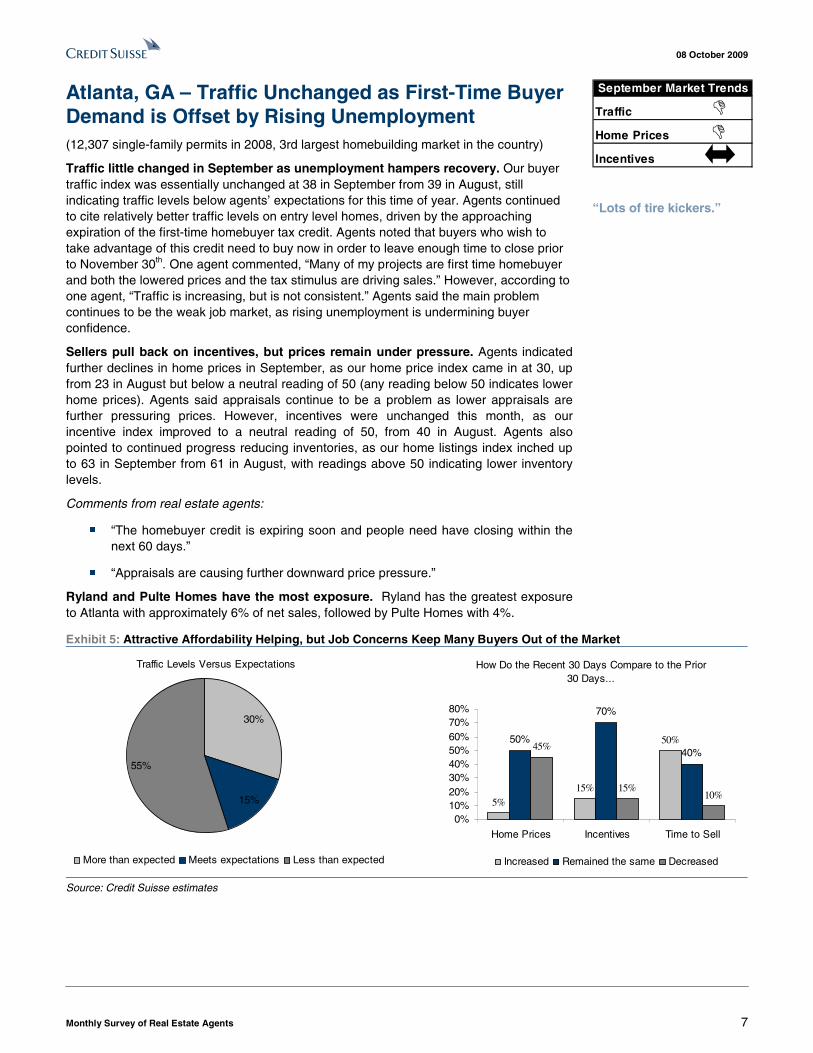

Atlanta, GA – Traffic Unchanged as First-Time Buyer Demand is Offset by Rising Unemployment (12,307 single-family permits in 2008, 3rd largest homebuilding market in the country)

Traffic little changed in September as unemployment hampers recovery. Our buyer traffic index was essentially unchanged at 38 in September from 39 in August, still indicating traffic levels below agents’ expectations for this time of year. Agents continued to cite relatively better traffic levels on entry level homes, driven by the approaching expiration of the first-time homebuyer tax credit. Agents noted that buyers who wish to take advantage of this credit need to buy now in order to leave enough time to close prior to November 30th. One agent commented, “Many of my projects are first time homebuyer and both the lowered prices and the tax stimulus are driving sales.” However, according to one agent, “Traffic is increasing, but is not consistent.” Agents said the main problem continues to be the weak job market, as rising unemployment is undermining buyer confidence.

Sellers pull back on incentives, but prices remain under pressure. Agents indicated further declines in home prices in September, as our home price index came in at 30, up from 23 in August but below a neutral reading of 50 (any reading below 50 indicates lower home prices). Agents said appraisals continue to be a problem as lower appraisals are further pressuring prices. However, incentives were unchanged this month, as our incentive index improved to a neutral reading of 50, from 40 in August. Agents also pointed to continued progress reducing inventories, as our home listings index inched up to 63 in September from 61 in August, with readings above 50 indicating lower inventory levels.

Comments from real estate agents:

■ “The homebuyer credit is expiring soon and people need have closing within the next 60 days.”

■ “Appraisals are causing further downward price pressure.”

Ryland and Pulte Homes have the most exposure. Ryland has the greatest exposure to Atlanta with approximately 6% of net sales, followed by Pulte Homes with 4%.

Exhibit 5: Attractive Affordability Helping, but Job Concerns Keep Many Buyers Out of the Market

Traffic Levels Versus Expectations

15%

55%

30%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

5%15%

50%50%

70%

40%45%

15%10%

0%10%20%30%40%50%60%70%80%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!!

“Lots of tire kickers.”

08 October 2009

Monthly Survey of Real Estate Agents 8

Austin, TX – Traffic Improves as Lower Prices, End of Tax Credit Spur Demand (8,025 single-family permits in 2008, 7th largest market in the country)

Traffic improves as buyers look to purchase ahead of the tax credit expiration. Buyer traffic improved in September versus August, as our traffic index increased to 40 from 27, although this still indicates traffic modestly below agents’ expectations (a reading of 50 would suggest traffic in-line with expectations). Agents widely cited the upcoming expiration of the first-time homebuyer tax credit as the driving force behind better traffic levels as time is running out for buyers to sign contracts, secure financing and close by the end of November. Speaking of financing, agents continued to note challenges getting buyers qualified for loans, leading one agent to quip, “We are no longer in a buyer’s or seller’s market. We are experiencing a lender’s market.” Agents said the majority of loans they see done are still FHA-backed, and that the Home Valuation Code of Conduct appraisal standard continues to cause problems.

Prices fall as sellers look to entice buyers. Our home price index was little changed at 26 in September from 25 in August, similar to the index levels we’ve seen for much of this year and still indicating falling home prices (readings below 50 point to lower home prices over the past 30 days). Our sense is that prices remained under pressure as sellers looked to draw in buyers and offload inventory ahead of the tax credit expiration. Our home listings index suggests some success there, jumping to 63 in September from 47 in August and indicating sequentially lower inventory levels (readings above 50 indicate lower inventory). This is a positive step towards price stabilization.

Comments from real estate agents:

■ “While the high end market is dead, under $400k buyers are pretty active.”

■ “We’re seeing greater urgency due to the first-time buyer tax credit.”

Meritage and D.R. Horton have the most exposure. Meritage has the greatest exposure to Austin with approximately 7% of net sales, followed by D.R. Horton with 5%.

Exhibit 6: Prices Fell in September, but Lower Inventory Levels are a Positive Leading Indicator

Traffic Levels Versus Expectations

37%

21%

42%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

0%

37%

63%

53% 53%

32%

47%

11%5%

0%

10%

20%

30%

40%

50%

60%

70%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!!!

“People think we have hit bottom.”

08 October 2009

Monthly Survey of Real Estate Agents 9

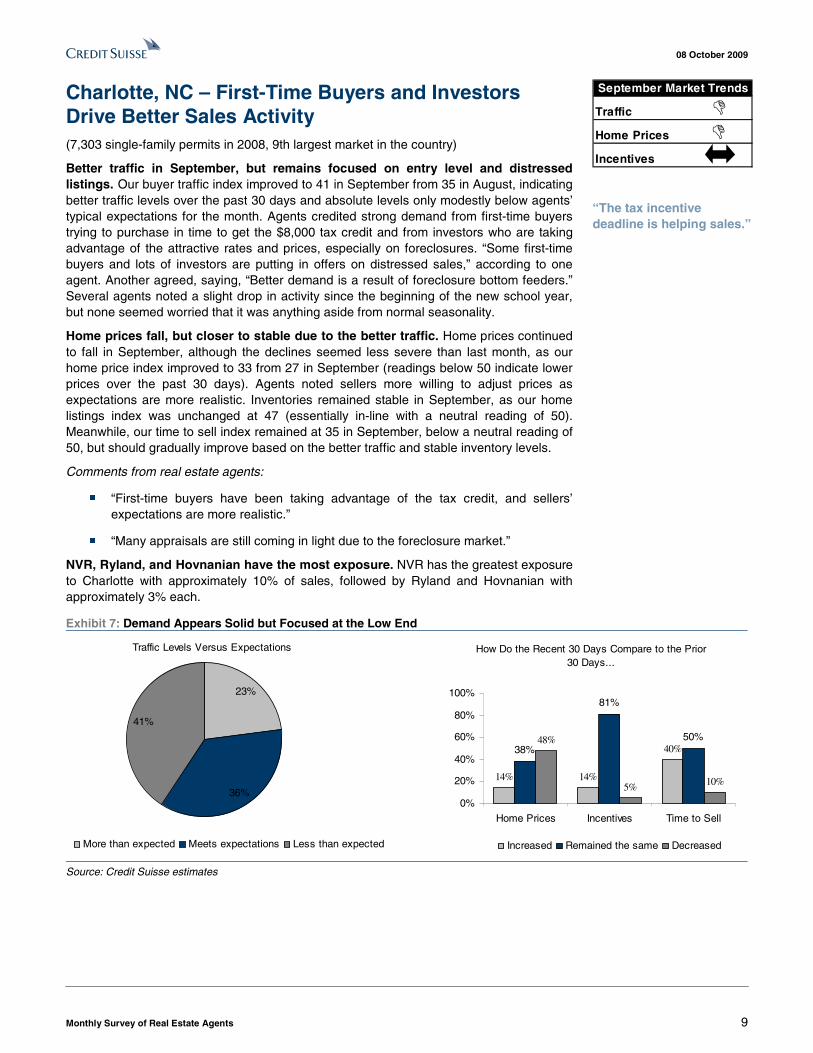

Charlotte, NC – First-Time Buyers and Investors Drive Better Sales Activity (7,303 single-family permits in 2008, 9th largest market in the country)

Better traffic in September, but remains focused on entry level and distressed listings. Our buyer traffic index improved to 41 in September from 35 in August, indicating better traffic levels over the past 30 days and absolute levels only modestly below agents’ typical expectations for the month. Agents credited strong demand from first-time buyers trying to purchase in time to get the $8,000 tax credit and from investors who are taking advantage of the attractive rates and prices, especially on foreclosures. “Some first-time buyers and lots of investors are putting in offers on distressed sales,” according to one agent. Another agreed, saying, “Better demand is a result of foreclosure bottom feeders.” Several agents noted a slight drop in activity since the beginning of the new school year, but none seemed worried that it was anything aside from normal seasonality.

Home prices fall, but closer to stable due to the better traffic. Home prices continued to fall in September, although the declines seemed less severe than last month, as our home price index improved to 33 from 27 in September (readings below 50 indicate lower prices over the past 30 days). Agents noted sellers more willing to adjust prices as expectations are more realistic. Inventories remained stable in September, as our home listings index was unchanged at 47 (essentially in-line with a neutral reading of 50). Meanwhile, our time to sell index remained at 35 in September, below a neutral reading of 50, but should gradually improve based on the better traffic and stable inventory levels.

Comments from real estate agents:

■ “First-time buyers have been taking advantage of the tax credit, and sellers’ expectations are more realistic.”

■ “Many appraisals are still coming in light due to the foreclosure market.”

NVR, Ryland, and Hovnanian have the most exposure. NVR has the greatest exposure to Charlotte with approximately 10% of sales, followed by Ryland and Hovnanian with approximately 3% each.

Exhibit 7: Demand Appears Solid but Focused at the Low End

Traffic Levels Versus Expectations

36%

41%

23%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

14% 14%

40%38%

81%

50%48%

5% 10%

0%

20%

40%

60%

80%

100%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!!

“The tax incentive deadline is helping sales.”

08 October 2009

Monthly Survey of Real Estate Agents 10

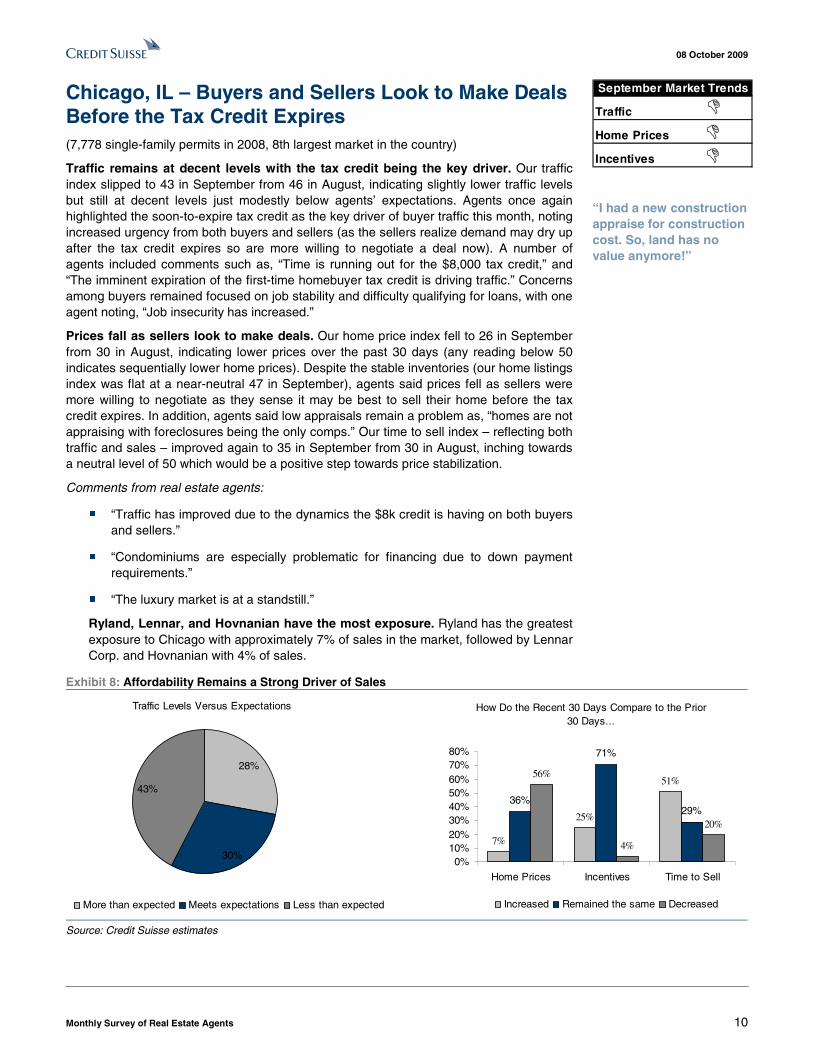

Chicago, IL – Buyers and Sellers Look to Make Deals Before the Tax Credit Expires (7,778 single-family permits in 2008, 8th largest market in the country)

Traffic remains at decent levels with the tax credit being the key driver. Our traffic index slipped to 43 in September from 46 in August, indicating slightly lower traffic levels but still at decent levels just modestly below agents’ expectations. Agents once again highlighted the soon-to-expire tax credit as the key driver of buyer traffic this month, noting increased urgency from both buyers and sellers (as the sellers realize demand may dry up after the tax credit expires so are more willing to negotiate a deal now). A number of agents included comments such as, “Time is running out for the $8,000 tax credit,” and “The imminent expiration of the first-time homebuyer tax credit is driving traffic.” Concerns among buyers remained focused on job stability and difficulty qualifying for loans, with one agent noting, “Job insecurity has increased.”

Prices fall as sellers look to make deals. Our home price index fell to 26 in September from 30 in August, indicating lower prices over the past 30 days (any reading below 50 indicates sequentially lower home prices). Despite the stable inventories (our home listings index was flat at a near-neutral 47 in September), agents said prices fell as sellers were more willing to negotiate as they sense it may be best to sell their home before the tax credit expires. In addition, agents said low appraisals remain a problem as, “homes are not appraising with foreclosures being the only comps.” Our time to sell index – reflecting both traffic and sales – improved again to 35 in September from 30 in August, inching towards a neutral level of 50 which would be a positive step towards price stabilization.

Comments from real estate agents:

■ “Traffic has improved due to the dynamics the $8k credit is having on both buyers and sellers.”

■ “Condominiums are especially problematic for financing due to down payment requirements.”

■ “The luxury market is at a standstill.”

Ryland, Lennar, and Hovnanian have the most exposure. Ryland has the greatest exposure to Chicago with approximately 7% of sales in the market, followed by Lennar Corp. and Hovnanian with 4% of sales.

Exhibit 8: Affordability Remains a Strong Driver of Sales

Traffic Levels Versus Expectations

30%

43%

28%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

7%

25%

51%

36%

71%

29%

56%

4%

20%

0%10%20%30%40%50%60%70%80%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!!!

“I had a new construction appraise for construction cost. So, land has no value anymore!”

08 October 2009

Monthly Survey of Real Estate Agents 11

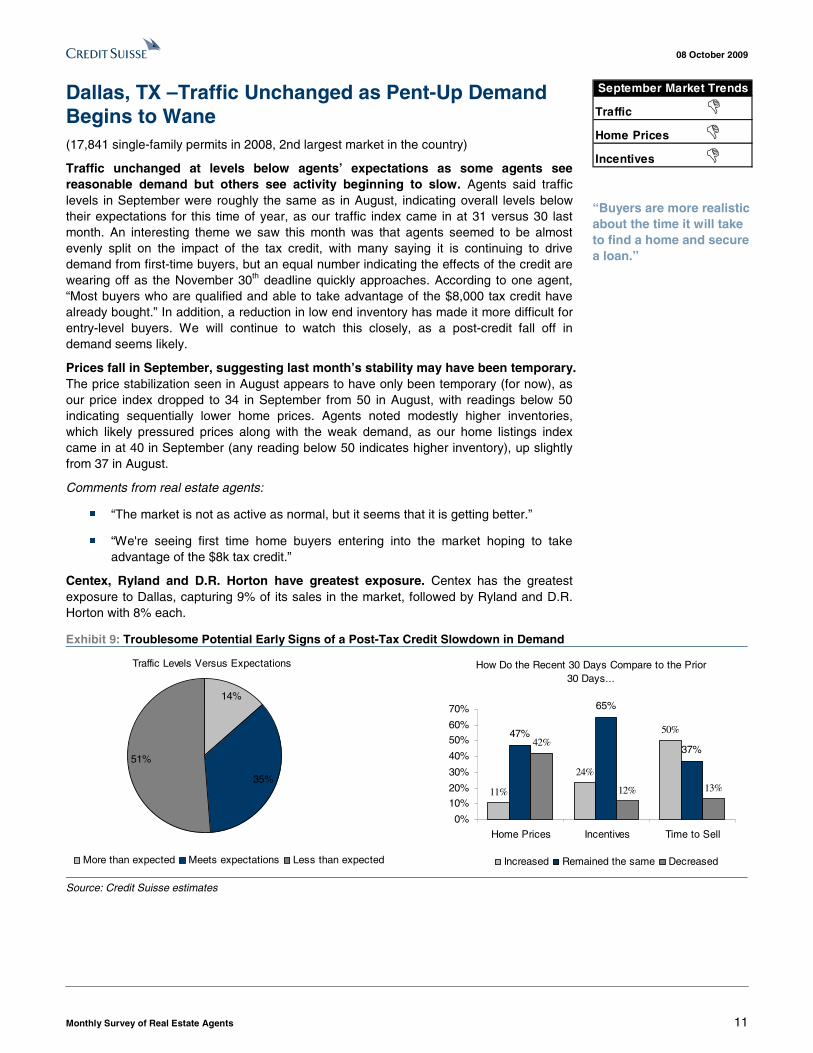

Dallas, TX –Traffic Unchanged as Pent-Up Demand Begins to Wane (17,841 single-family permits in 2008, 2nd largest market in the country)

Traffic unchanged at levels below agents’ expectations as some agents see reasonable demand but others see activity beginning to slow. Agents said traffic levels in September were roughly the same as in August, indicating overall levels below their expectations for this time of year, as our traffic index came in at 31 versus 30 last month. An interesting theme we saw this month was that agents seemed to be almost evenly split on the impact of the tax credit, with many saying it is continuing to drive demand from first-time buyers, but an equal number indicating the effects of the credit are wearing off as the November 30th deadline quickly approaches. According to one agent, “Most buyers who are qualified and able to take advantage of the $8,000 tax credit have already bought.” In addition, a reduction in low end inventory has made it more difficult for entry-level buyers. We will continue to watch this closely, as a post-credit fall off in demand seems likely.

Prices fall in September, suggesting last month’s stability may have been temporary. The price stabilization seen in August appears to have only been temporary (for now), as our price index dropped to 34 in September from 50 in August, with readings below 50 indicating sequentially lower home prices. Agents noted modestly higher inventories, which likely pressured prices along with the weak demand, as our home listings index came in at 40 in September (any reading below 50 indicates higher inventory), up slightly from 37 in August.

Comments from real estate agents:

■ “The market is not as active as normal, but it seems that it is getting better.”

■ “We're seeing first time home buyers entering into the market hoping to take advantage of the $8k tax credit.”

Centex, Ryland and D.R. Horton have greatest exposure. Centex has the greatest exposure to Dallas, capturing 9% of its sales in the market, followed by Ryland and D.R. Horton with 8% each.

Exhibit 9: Troublesome Potential Early Signs of a Post-Tax Credit Slowdown in Demand

Traffic Levels Versus Expectations

35%

14%

51%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

11%

24%

50%47%

65%

37%42%

12% 13%

0%

10%

20%

30%

40%

50%

60%

70%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!!!

“Buyers are more realistic about the time it will take to find a home and secure a loan.”

08 October 2009

Monthly Survey of Real Estate Agents 12

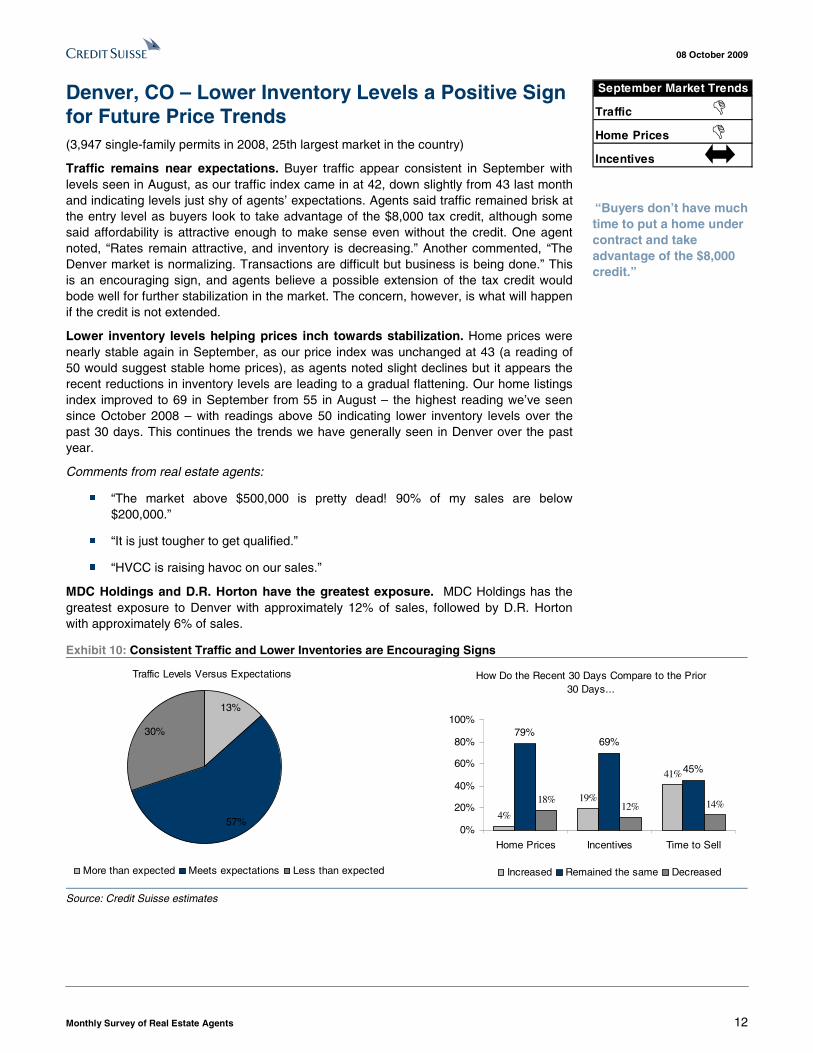

Denver, CO – Lower Inventory Levels a Positive Sign for Future Price Trends (3,947 single-family permits in 2008, 25th largest market in the country)

Traffic remains near expectations. Buyer traffic appear consistent in September with levels seen in August, as our traffic index came in at 42, down slightly from 43 last month and indicating levels just shy of agents’ expectations. Agents said traffic remained brisk at the entry level as buyers look to take advantage of the $8,000 tax credit, although some said affordability is attractive enough to make sense even without the credit. One agent noted, “Rates remain attractive, and inventory is decreasing.” Another commented, “The Denver market is normalizing. Transactions are difficult but business is being done.” This is an encouraging sign, and agents believe a possible extension of the tax credit would bode well for further stabilization in the market. The concern, however, is what will happen if the credit is not extended.

Lower inventory levels helping prices inch towards stabilization. Home prices were nearly stable again in September, as our price index was unchanged at 43 (a reading of 50 would suggest stable home prices), as agents noted slight declines but it appears the recent reductions in inventory levels are leading to a gradual flattening. Our home listings index improved to 69 in September from 55 in August – the highest reading we’ve seen since October 2008 – with readings above 50 indicating lower inventory levels over the past 30 days. This continues the trends we have generally seen in Denver over the past year.

Comments from real estate agents:

■ “The market above $500,000 is pretty dead! 90% of my sales are below $200,000.”

■ “It is just tougher to get qualified.”

■ “HVCC is raising havoc on our sales.”

MDC Holdings and D.R. Horton have the greatest exposure. MDC Holdings has the greatest exposure to Denver with approximately 12% of sales, followed by D.R. Horton with approximately 6% of sales.

Exhibit 10: Consistent Traffic and Lower Inventories are Encouraging Signs

Traffic Levels Versus Expectations

57%

30%

13%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

4%

19%

41%

79%69%

45%

18%12% 14%

0%

20%

40%

60%

80%

100%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!!

“Buyers don’t have much time to put a home under contract and take advantage of the $8,000 credit.”

08 October 2009

Monthly Survey of Real Estate Agents 13

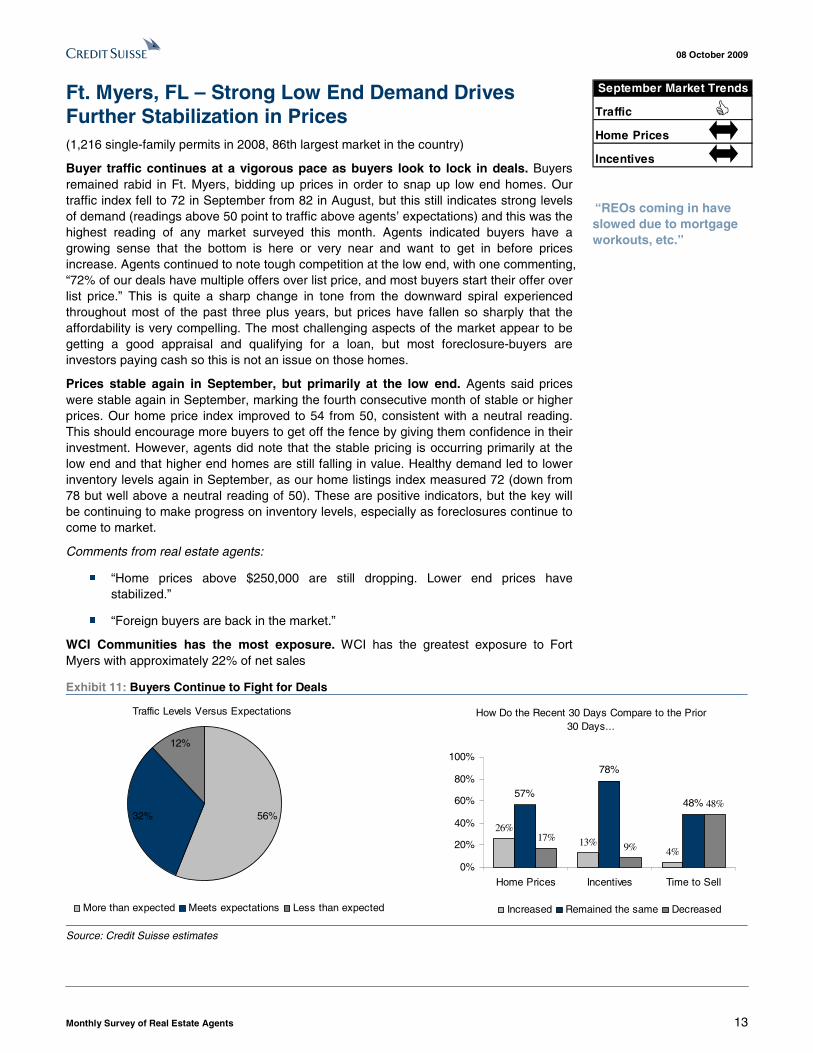

Ft. Myers, FL – Strong Low End Demand Drives Further Stabilization in Prices (1,216 single-family permits in 2008, 86th largest market in the country)

Buyer traffic continues at a vigorous pace as buyers look to lock in deals. Buyers remained rabid in Ft. Myers, bidding up prices in order to snap up low end homes. Our traffic index fell to 72 in September from 82 in August, but this still indicates strong levels of demand (readings above 50 point to traffic above agents’ expectations) and this was the highest reading of any market surveyed this month. Agents indicated buyers have a growing sense that the bottom is here or very near and want to get in before prices increase. Agents continued to note tough competition at the low end, with one commenting, “72% of our deals have multiple offers over list price, and most buyers start their offer over list price.” This is quite a sharp change in tone from the downward spiral experienced throughout most of the past three plus years, but prices have fallen so sharply that the affordability is very compelling. The most challenging aspects of the market appear to be getting a good appraisal and qualifying for a loan, but most foreclosure-buyers are investors paying cash so this is not an issue on those homes.

Prices stable again in September, but primarily at the low end. Agents said prices were stable again in September, marking the fourth consecutive month of stable or higher prices. Our home price index improved to 54 from 50, consistent with a neutral reading. This should encourage more buyers to get off the fence by giving them confidence in their investment. However, agents did note that the stable pricing is occurring primarily at the low end and that higher end homes are still falling in value. Healthy demand led to lower inventory levels again in September, as our home listings index measured 72 (down from 78 but well above a neutral reading of 50). These are positive indicators, but the key will be continuing to make progress on inventory levels, especially as foreclosures continue to come to market.

Comments from real estate agents:

■ “Home prices above $250,000 are still dropping. Lower end prices have stabilized.”

■ “Foreign buyers are back in the market.”

WCI Communities has the most exposure. WCI has the greatest exposure to Fort Myers with approximately 22% of net sales

Exhibit 11: Buyers Continue to Fight for Deals

Traffic Levels Versus Expectations

32% 56%

12%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

26%13%

4%

57%

78%

48%

17%9%

48%

0%

20%

40%

60%

80%

100%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

“REOs coming in have slowed due to mortgage workouts, etc.”

08 October 2009

Monthly Survey of Real Estate Agents 14

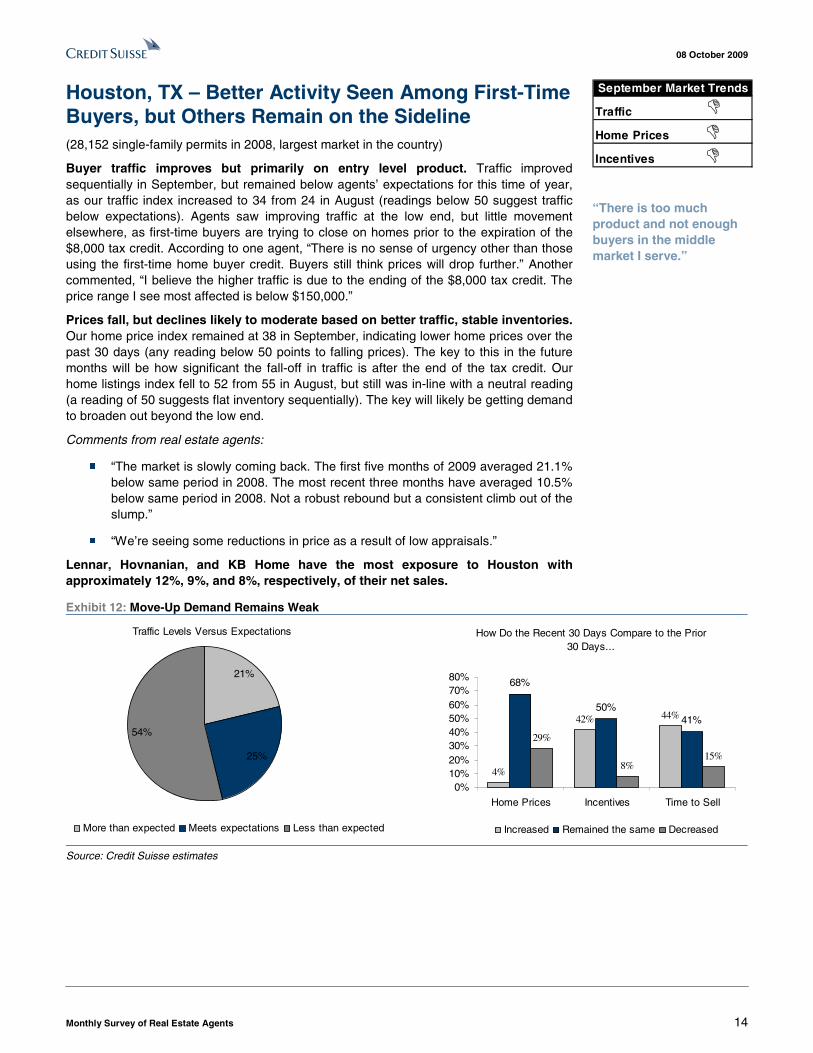

Houston, TX – Better Activity Seen Among First-Time Buyers, but Others Remain on the Sideline (28,152 single-family permits in 2008, largest market in the country)

Buyer traffic improves but primarily on entry level product. Traffic improved sequentially in September, but remained below agents’ expectations for this time of year, as our traffic index increased to 34 from 24 in August (readings below 50 suggest traffic below expectations). Agents saw improving traffic at the low end, but little movement elsewhere, as first-time buyers are trying to close on homes prior to the expiration of the $8,000 tax credit. According to one agent, “There is no sense of urgency other than those using the first-time home buyer credit. Buyers still think prices will drop further.” Another commented, “I believe the higher traffic is due to the ending of the $8,000 tax credit. The price range I see most affected is below $150,000.”

Prices fall, but declines likely to moderate based on better traffic, stable inventories. Our home price index remained at 38 in September, indicating lower home prices over the past 30 days (any reading below 50 points to falling prices). The key to this in the future months will be how significant the fall-off in traffic is after the end of the tax credit. Our home listings index fell to 52 from 55 in August, but still was in-line with a neutral reading (a reading of 50 suggests flat inventory sequentially). The key will likely be getting demand to broaden out beyond the low end.

Comments from real estate agents:

■ “The market is slowly coming back. The first five months of 2009 averaged 21.1% below same period in 2008. The most recent three months have averaged 10.5% below same period in 2008. Not a robust rebound but a consistent climb out of the slump.”

■ “We’re seeing some reductions in price as a result of low appraisals.”

Lennar, Hovnanian, and KB Home have the most exposure to Houston with approximately 12%, 9%, and 8%, respectively, of their net sales.

Exhibit 12: Move-Up Demand Remains Weak

Traffic Levels Versus Expectations

25%

54%

21%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

4%

42% 44%

68%

50%41%

29%

8%15%

0%10%20%30%40%50%60%70%80%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!!!

“There is too much product and not enough buyers in the middle market I serve.”

08 October 2009

Monthly Survey of Real Estate Agents 15

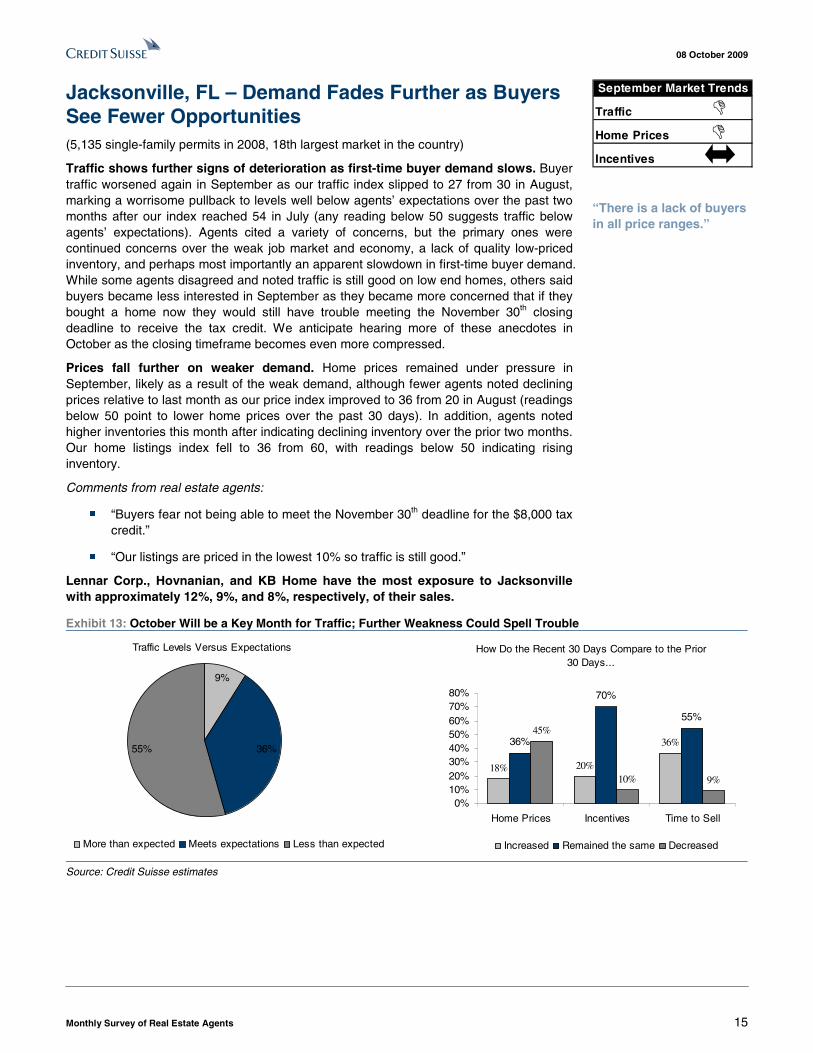

Jacksonville, FL – Demand Fades Further as Buyers See Fewer Opportunities (5,135 single-family permits in 2008, 18th largest market in the country)

Traffic shows further signs of deterioration as first-time buyer demand slows. Buyer traffic worsened again in September as our traffic index slipped to 27 from 30 in August, marking a worrisome pullback to levels well below agents’ expectations over the past two months after our index reached 54 in July (any reading below 50 suggests traffic below agents’ expectations). Agents cited a variety of concerns, but the primary ones were continued concerns over the weak job market and economy, a lack of quality low-priced inventory, and perhaps most importantly an apparent slowdown in first-time buyer demand. While some agents disagreed and noted traffic is still good on low end homes, others said buyers became less interested in September as they became more concerned that if they bought a home now they would still have trouble meeting the November 30th closing deadline to receive the tax credit. We anticipate hearing more of these anecdotes in October as the closing timeframe becomes even more compressed.

Prices fall further on weaker demand. Home prices remained under pressure in September, likely as a result of the weak demand, although fewer agents noted declining prices relative to last month as our price index improved to 36 from 20 in August (readings below 50 point to lower home prices over the past 30 days). In addition, agents noted higher inventories this month after indicating declining inventory over the prior two months. Our home listings index fell to 36 from 60, with readings below 50 indicating rising inventory.

Comments from real estate agents:

■ “Buyers fear not being able to meet the November 30th deadline for the $8,000 tax credit.”

■ “Our listings are priced in the lowest 10% so traffic is still good.”

Lennar Corp., Hovnanian, and KB Home have the most exposure to Jacksonville with approximately 12%, 9%, and 8%, respectively, of their sales.

Exhibit 13: October Will be a Key Month for Traffic; Further Weakness Could Spell Trouble

Traffic Levels Versus Expectations

36%

9%

55%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

18% 20%

36%36%

70%

55%45%

10% 9%

0%10%20%30%40%50%60%70%80%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!!

“There is a lack of buyers in all price ranges.”

08 October 2009

Monthly Survey of Real Estate Agents 16

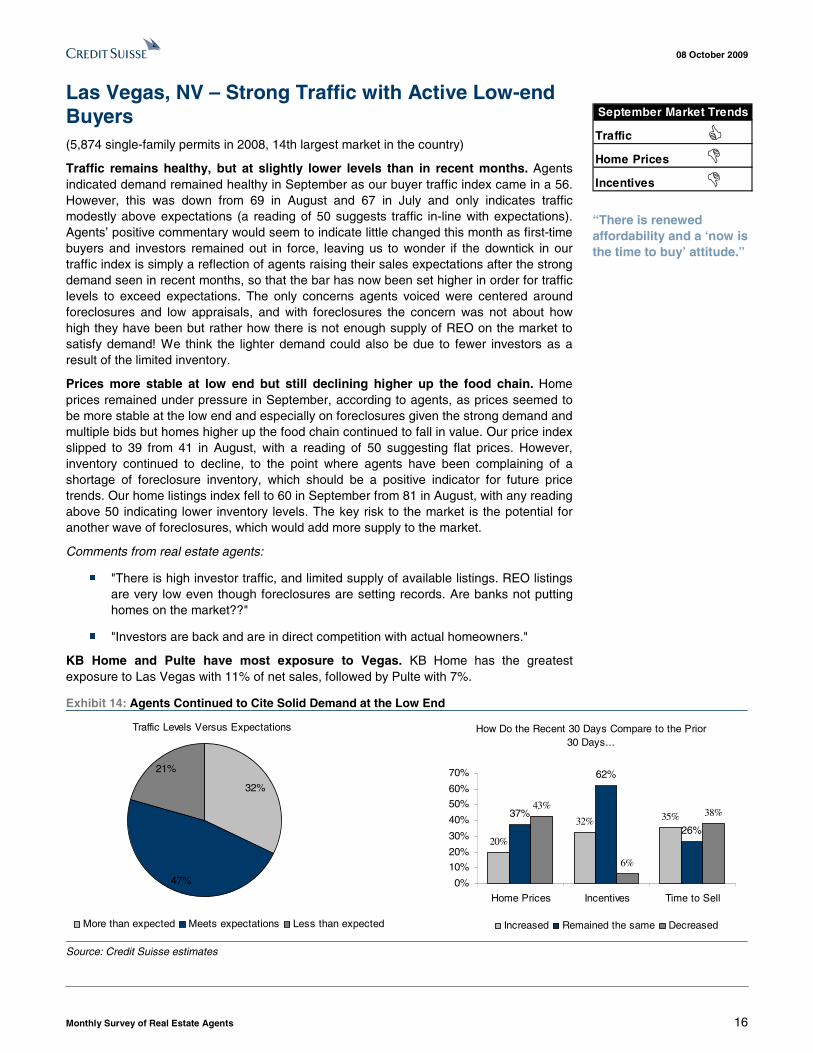

Las Vegas, NV – Strong Traffic with Active Low-end Buyers (5,874 single-family permits in 2008, 14th largest market in the country)

Traffic remains healthy, but at slightly lower levels than in recent months. Agents indicated demand remained healthy in September as our buyer traffic index came in a 56. However, this was down from 69 in August and 67 in July and only indicates traffic modestly above expectations (a reading of 50 suggests traffic in-line with expectations). Agents’ positive commentary would seem to indicate little changed this month as first-time buyers and investors remained out in force, leaving us to wonder if the downtick in our traffic index is simply a reflection of agents raising their sales expectations after the strong demand seen in recent months, so that the bar has now been set higher in order for traffic levels to exceed expectations. The only concerns agents voiced were centered around foreclosures and low appraisals, and with foreclosures the concern was not about how high they have been but rather how there is not enough supply of REO on the market to satisfy demand! We think the lighter demand could also be due to fewer investors as a result of the limited inventory.

Prices more stable at low end but still declining higher up the food chain. Home prices remained under pressure in September, according to agents, as prices seemed to be more stable at the low end and especially on foreclosures given the strong demand and multiple bids but homes higher up the food chain continued to fall in value. Our price index slipped to 39 from 41 in August, with a reading of 50 suggesting flat prices. However, inventory continued to decline, to the point where agents have been complaining of a shortage of foreclosure inventory, which should be a positive indicator for future price trends. Our home listings index fell to 60 in September from 81 in August, with any reading above 50 indicating lower inventory levels. The key risk to the market is the potential for another wave of foreclosures, which would add more supply to the market.

Comments from real estate agents:

■ "There is high investor traffic, and limited supply of available listings. REO listings are very low even though foreclosures are setting records. Are banks not putting homes on the market??"

■ "Investors are back and are in direct competition with actual homeowners."

KB Home and Pulte have most exposure to Vegas. KB Home has the greatest exposure to Las Vegas with 11% of net sales, followed by Pulte with 7%.

Exhibit 14: Agents Continued to Cite Solid Demand at the Low End

Traffic Levels Versus Expectations

47%

32%

21%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

20%

32% 35%37%

62%

26%

43%

6%

38%

0%

10%

20%

30%

40%

50%

60%

70%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!

!

“There is renewed affordability and a ‘now is the time to buy’ attitude.”

08 October 2009

Monthly Survey of Real Estate Agents 17

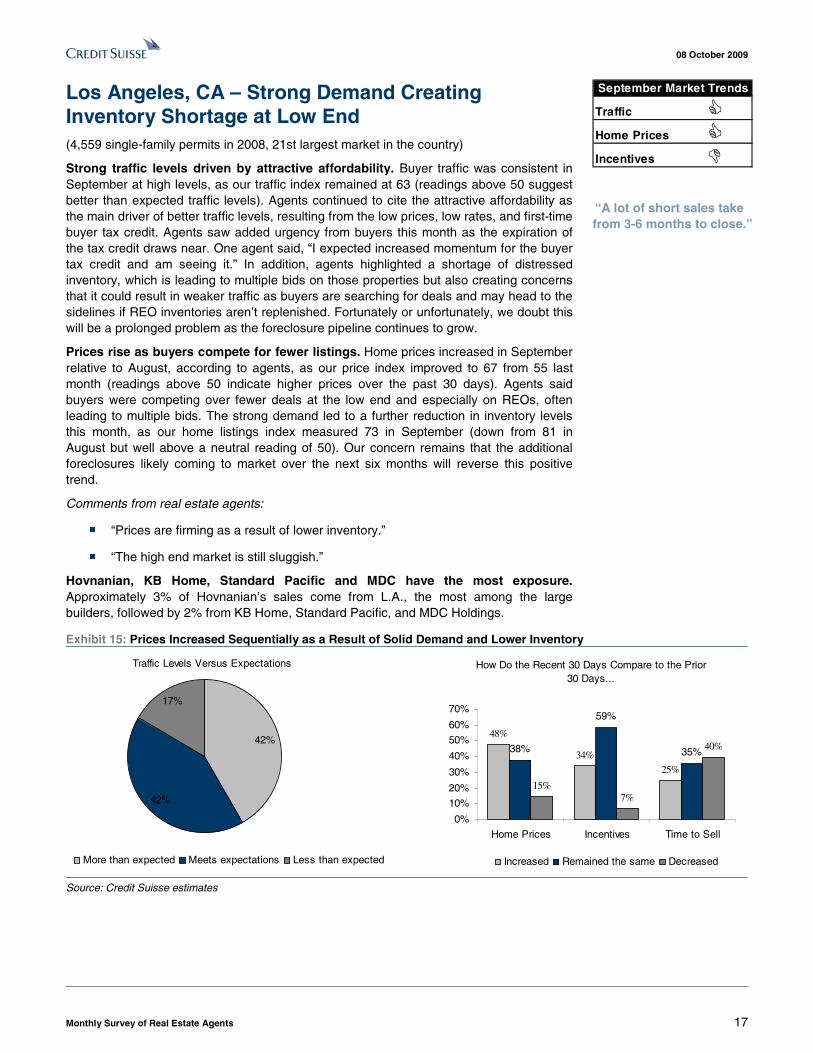

Los Angeles, CA – Strong Demand Creating Inventory Shortage at Low End (4,559 single-family permits in 2008, 21st largest market in the country)

Strong traffic levels driven by attractive affordability. Buyer traffic was consistent in September at high levels, as our traffic index remained at 63 (readings above 50 suggest better than expected traffic levels). Agents continued to cite the attractive affordability as the main driver of better traffic levels, resulting from the low prices, low rates, and first-time buyer tax credit. Agents saw added urgency from buyers this month as the expiration of the tax credit draws near. One agent said, “I expected increased momentum for the buyer tax credit and am seeing it.” In addition, agents highlighted a shortage of distressed inventory, which is leading to multiple bids on those properties but also creating concerns that it could result in weaker traffic as buyers are searching for deals and may head to the sidelines if REO inventories aren’t replenished. Fortunately or unfortunately, we doubt this will be a prolonged problem as the foreclosure pipeline continues to grow.

Prices rise as buyers compete for fewer listings. Home prices increased in September relative to August, according to agents, as our price index improved to 67 from 55 last month (readings above 50 indicate higher prices over the past 30 days). Agents said buyers were competing over fewer deals at the low end and especially on REOs, often leading to multiple bids. The strong demand led to a further reduction in inventory levels this month, as our home listings index measured 73 in September (down from 81 in August but well above a neutral reading of 50). Our concern remains that the additional foreclosures likely coming to market over the next six months will reverse this positive trend.

Comments from real estate agents:

■ “Prices are firming as a result of lower inventory.”

■ “The high end market is still sluggish.”

Hovnanian, KB Home, Standard Pacific and MDC have the most exposure. Approximately 3% of Hovnanian’s sales come from L.A., the most among the large builders, followed by 2% from KB Home, Standard Pacific, and MDC Holdings.

Exhibit 15: Prices Increased Sequentially as a Result of Solid Demand and Lower Inventory

Traffic Levels Versus Expectations

42%

17%

42%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

48%

34%

25%

38%

59%

35%

15%7%

40%

0%

10%

20%

30%

40%

50%

60%

70%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!

“A lot of short sales take from 3-6 months to close.”

08 October 2009

Monthly Survey of Real Estate Agents 18

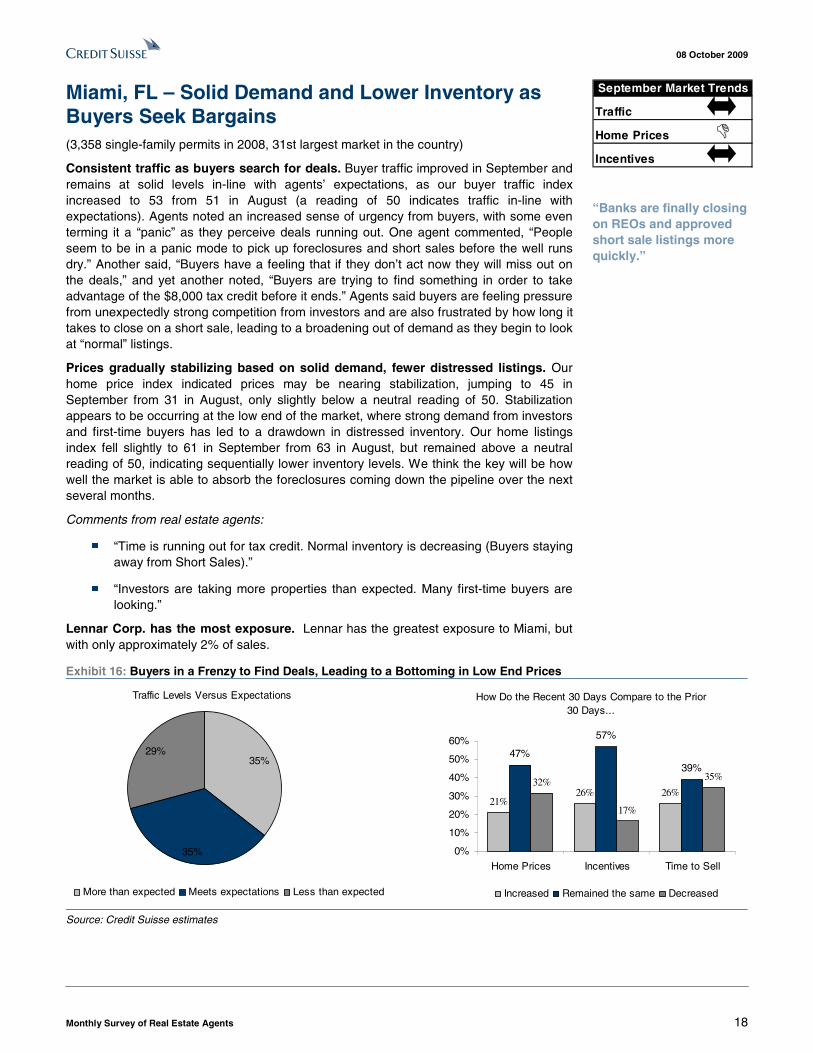

Miami, FL – Solid Demand and Lower Inventory as Buyers Seek Bargains (3,358 single-family permits in 2008, 31st largest market in the country)

Consistent traffic as buyers search for deals. Buyer traffic improved in September and remains at solid levels in-line with agents’ expectations, as our buyer traffic index increased to 53 from 51 in August (a reading of 50 indicates traffic in-line with expectations). Agents noted an increased sense of urgency from buyers, with some even terming it a “panic” as they perceive deals running out. One agent commented, “People seem to be in a panic mode to pick up foreclosures and short sales before the well runs dry.” Another said, “Buyers have a feeling that if they don’t act now they will miss out on the deals,” and yet another noted, “Buyers are trying to find something in order to take advantage of the $8,000 tax credit before it ends.” Agents said buyers are feeling pressure from unexpectedly strong competition from investors and are also frustrated by how long it takes to close on a short sale, leading to a broadening out of demand as they begin to look at “normal” listings.

Prices gradually stabilizing based on solid demand, fewer distressed listings. Our home price index indicated prices may be nearing stabilization, jumping to 45 in September from 31 in August, only slightly below a neutral reading of 50. Stabilization appears to be occurring at the low end of the market, where strong demand from investors and first-time buyers has led to a drawdown in distressed inventory. Our home listings index fell slightly to 61 in September from 63 in August, but remained above a neutral reading of 50, indicating sequentially lower inventory levels. We think the key will be how well the market is able to absorb the foreclosures coming down the pipeline over the next several months.

Comments from real estate agents:

■ “Time is running out for tax credit. Normal inventory is decreasing (Buyers staying away from Short Sales).”

■ “Investors are taking more properties than expected. Many first-time buyers are looking.”

Lennar Corp. has the most exposure. Lennar has the greatest exposure to Miami, but with only approximately 2% of sales.

Exhibit 16: Buyers in a Frenzy to Find Deals, Leading to a Bottoming in Low End Prices

Traffic Levels Versus Expectations

35%

35%29%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

21%26% 26%

47%

57%

39%32%

17%

35%

0%

10%

20%

30%

40%

50%

60%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!

“Banks are finally closing on REOs and approved short sale listings more quickly.”

08 October 2009

Monthly Survey of Real Estate Agents 19

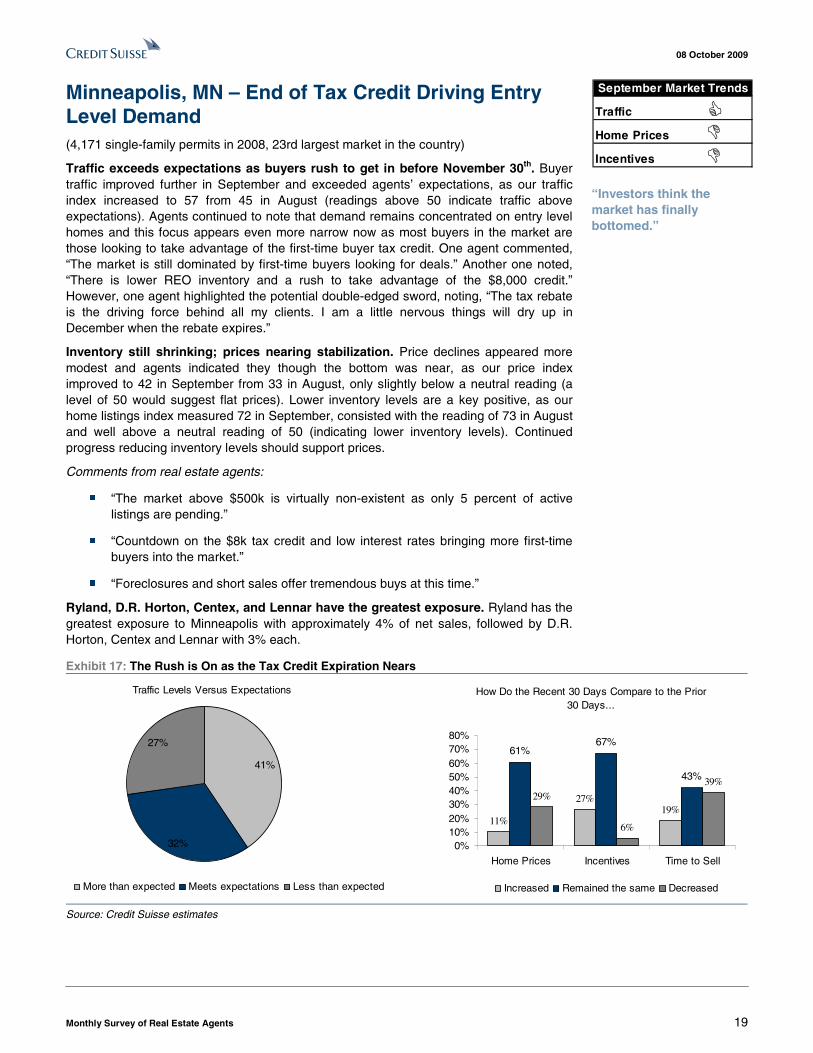

Minneapolis, MN – End of Tax Credit Driving Entry Level Demand (4,171 single-family permits in 2008, 23rd largest market in the country)

Traffic exceeds expectations as buyers rush to get in before November 30th. Buyer traffic improved further in September and exceeded agents’ expectations, as our traffic index increased to 57 from 45 in August (readings above 50 indicate traffic above expectations). Agents continued to note that demand remains concentrated on entry level homes and this focus appears even more narrow now as most buyers in the market are those looking to take advantage of the first-time buyer tax credit. One agent commented, “The market is still dominated by first-time buyers looking for deals.” Another one noted, “There is lower REO inventory and a rush to take advantage of the $8,000 credit.” However, one agent highlighted the potential double-edged sword, noting, “The tax rebate is the driving force behind all my clients. I am a little nervous things will dry up in December when the rebate expires.”

Inventory still shrinking; prices nearing stabilization. Price declines appeared more modest and agents indicated they though the bottom was near, as our price index improved to 42 in September from 33 in August, only slightly below a neutral reading (a level of 50 would suggest flat prices). Lower inventory levels are a key positive, as our home listings index measured 72 in September, consisted with the reading of 73 in August and well above a neutral reading of 50 (indicating lower inventory levels). Continued progress reducing inventory levels should support prices.

Comments from real estate agents:

■ “The market above $500k is virtually non-existent as only 5 percent of active listings are pending.”

■ “Countdown on the $8k tax credit and low interest rates bringing more first-time buyers into the market.”

■ “Foreclosures and short sales offer tremendous buys at this time.”

Ryland, D.R. Horton, Centex, and Lennar have the greatest exposure. Ryland has the greatest exposure to Minneapolis with approximately 4% of net sales, followed by D.R. Horton, Centex and Lennar with 3% each.

Exhibit 17: The Rush is On as the Tax Credit Expiration Nears

Traffic Levels Versus Expectations

32%

27%

41%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

11%

27%19%

61%67%

43%

29%

6%

39%

0%10%20%30%40%50%60%70%80%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!

!

“Investors think the market has finally bottomed.”

08 October 2009

Monthly Survey of Real Estate Agents 20

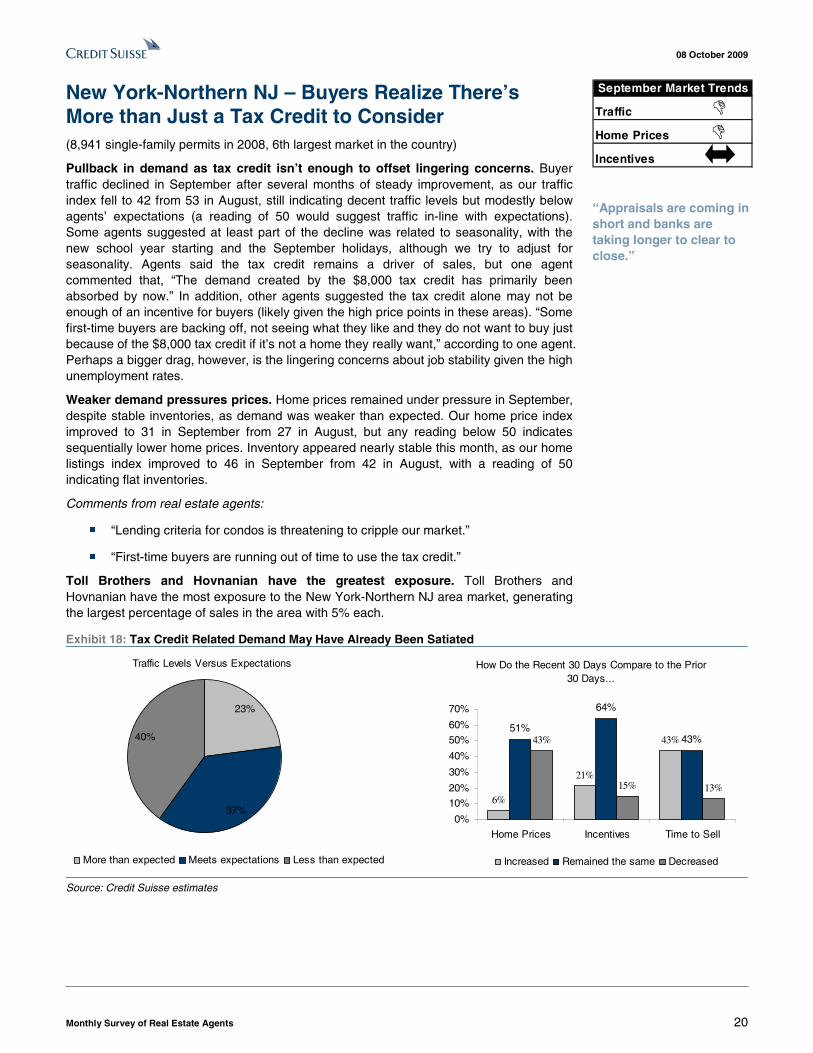

New York-Northern NJ – Buyers Realize There’s More than Just a Tax Credit to Consider (8,941 single-family permits in 2008, 6th largest market in the country)

Pullback in demand as tax credit isn’t enough to offset lingering concerns. Buyer traffic declined in September after several months of steady improvement, as our traffic index fell to 42 from 53 in August, still indicating decent traffic levels but modestly below agents’ expectations (a reading of 50 would suggest traffic in-line with expectations). Some agents suggested at least part of the decline was related to seasonality, with the new school year starting and the September holidays, although we try to adjust for seasonality. Agents said the tax credit remains a driver of sales, but one agent commented that, “The demand created by the $8,000 tax credit has primarily been absorbed by now.” In addition, other agents suggested the tax credit alone may not be enough of an incentive for buyers (likely given the high price points in these areas). “Some first-time buyers are backing off, not seeing what they like and they do not want to buy just because of the $8,000 tax credit if it’s not a home they really want,” according to one agent. Perhaps a bigger drag, however, is the lingering concerns about job stability given the high unemployment rates.

Weaker demand pressures prices. Home prices remained under pressure in September, despite stable inventories, as demand was weaker than expected. Our home price index improved to 31 in September from 27 in August, but any reading below 50 indicates sequentially lower home prices. Inventory appeared nearly stable this month, as our home listings index improved to 46 in September from 42 in August, with a reading of 50 indicating flat inventories.

Comments from real estate agents:

■ “Lending criteria for condos is threatening to cripple our market.”

■ “First-time buyers are running out of time to use the tax credit.”

Toll Brothers and Hovnanian have the greatest exposure. Toll Brothers and Hovnanian have the most exposure to the New York-Northern NJ area market, generating the largest percentage of sales in the area with 5% each.

Exhibit 18: Tax Credit Related Demand May Have Already Been Satiated

Traffic Levels Versus Expectations

37%

23%

40%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

6%

21%

43%51%

64%

43%43%

15% 13%

0%

10%

20%

30%

40%

50%

60%

70%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!!

“Appraisals are coming in short and banks are taking longer to clear to close.”

08 October 2009

Monthly Survey of Real Estate Agents 21

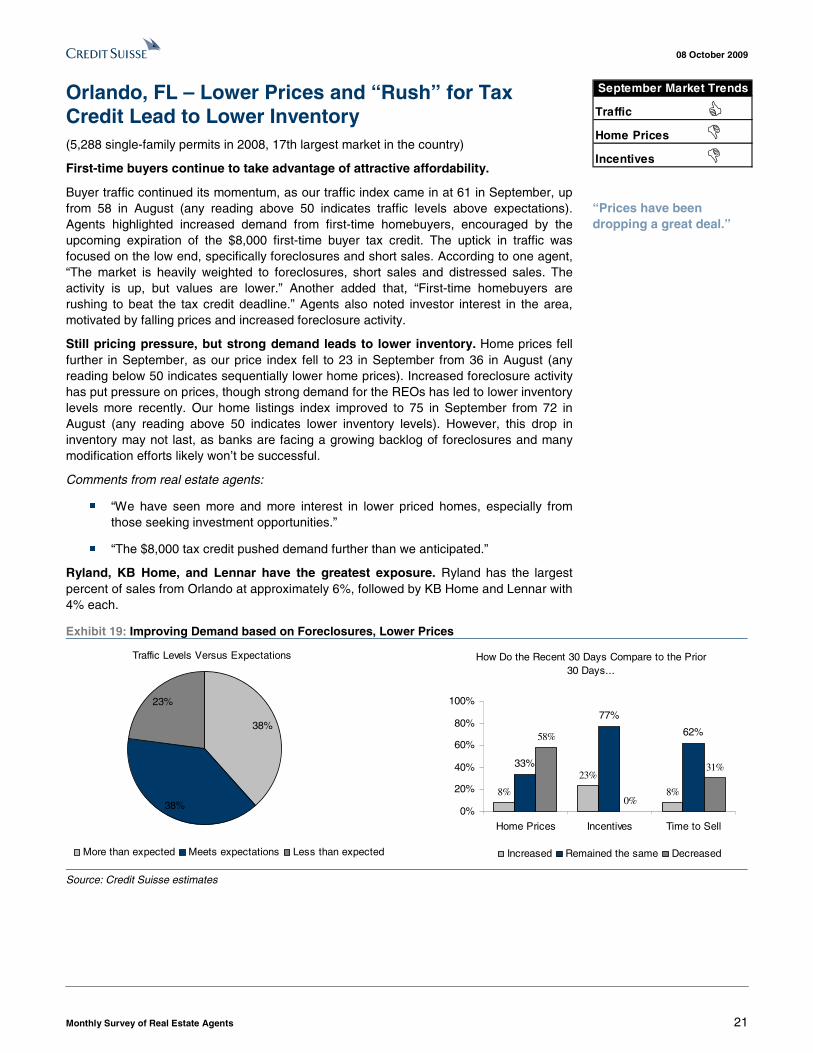

Orlando, FL – Lower Prices and “Rush” for Tax Credit Lead to Lower Inventory (5,288 single-family permits in 2008, 17th largest market in the country)

First-time buyers continue to take advantage of attractive affordability.

Buyer traffic continued its momentum, as our traffic index came in at 61 in September, up from 58 in August (any reading above 50 indicates traffic levels above expectations). Agents highlighted increased demand from first-time homebuyers, encouraged by the upcoming expiration of the $8,000 first-time buyer tax credit. The uptick in traffic was focused on the low end, specifically foreclosures and short sales. According to one agent, “The market is heavily weighted to foreclosures, short sales and distressed sales. The activity is up, but values are lower.” Another added that, “First-time homebuyers are rushing to beat the tax credit deadline.” Agents also noted investor interest in the area, motivated by falling prices and increased foreclosure activity.

Still pricing pressure, but strong demand leads to lower inventory. Home prices fell further in September, as our price index fell to 23 in September from 36 in August (any reading below 50 indicates sequentially lower home prices). Increased foreclosure activity has put pressure on prices, though strong demand for the REOs has led to lower inventory levels more recently. Our home listings index improved to 75 in September from 72 in August (any reading above 50 indicates lower inventory levels). However, this drop in inventory may not last, as banks are facing a growing backlog of foreclosures and many modification efforts likely won’t be successful.

Comments from real estate agents:

■ “We have seen more and more interest in lower priced homes, especially from those seeking investment opportunities.”

■ “The $8,000 tax credit pushed demand further than we anticipated.”

Ryland, KB Home, and Lennar have the greatest exposure. Ryland has the largest percent of sales from Orlando at approximately 6%, followed by KB Home and Lennar with 4% each.

Exhibit 19: Improving Demand based on Foreclosures, Lower Prices

Traffic Levels Versus Expectations

38%

38%

23%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

8%

23%

8%

33%

77%

62%58%

0%

31%

0%

20%

40%

60%

80%

100%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!

!

“Prices have been dropping a great deal.”

08 October 2009

Monthly Survey of Real Estate Agents 22

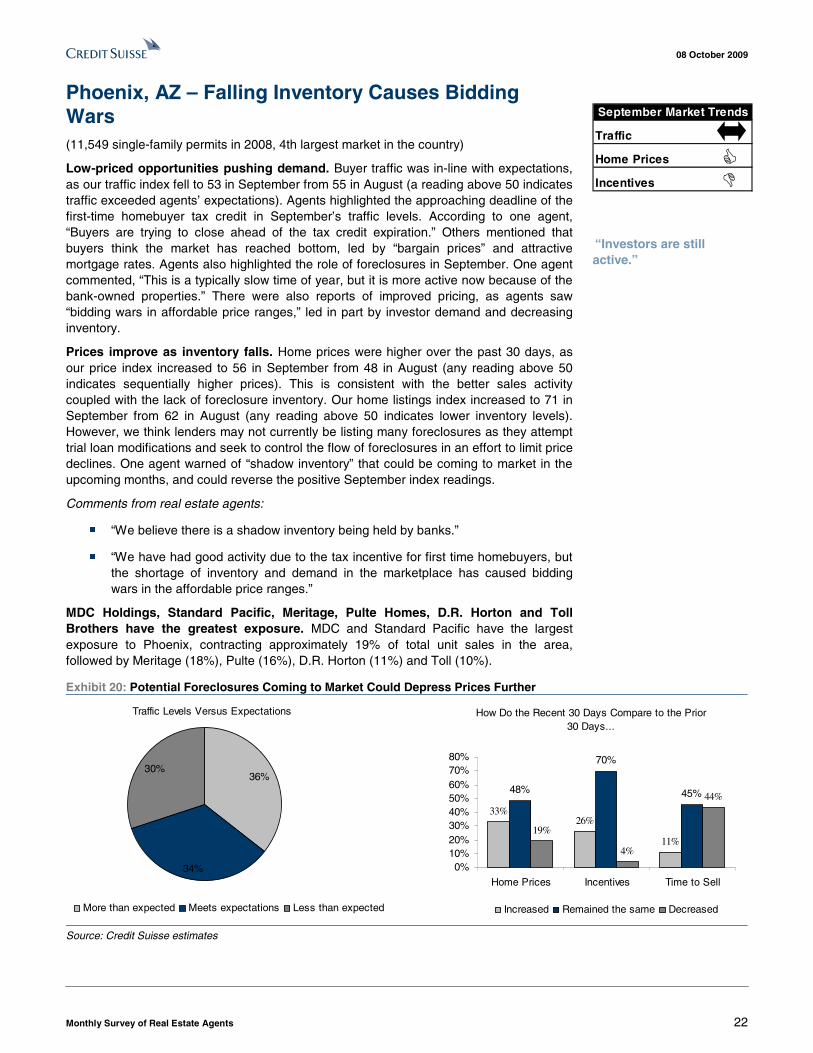

Phoenix, AZ – Falling Inventory Causes Bidding Wars (11,549 single-family permits in 2008, 4th largest market in the country)

Low-priced opportunities pushing demand. Buyer traffic was in-line with expectations, as our traffic index fell to 53 in September from 55 in August (a reading above 50 indicates traffic exceeded agents’ expectations). Agents highlighted the approaching deadline of the first-time homebuyer tax credit in September’s traffic levels. According to one agent, “Buyers are trying to close ahead of the tax credit expiration.” Others mentioned that buyers think the market has reached bottom, led by “bargain prices” and attractive mortgage rates. Agents also highlighted the role of foreclosures in September. One agent commented, “This is a typically slow time of year, but it is more active now because of the bank-owned properties.” There were also reports of improved pricing, as agents saw “bidding wars in affordable price ranges,” led in part by investor demand and decreasing inventory.

Prices improve as inventory falls. Home prices were higher over the past 30 days, as our price index increased to 56 in September from 48 in August (any reading above 50 indicates sequentially higher prices). This is consistent with the better sales activity coupled with the lack of foreclosure inventory. Our home listings index increased to 71 in September from 62 in August (any reading above 50 indicates lower inventory levels). However, we think lenders may not currently be listing many foreclosures as they attempt trial loan modifications and seek to control the flow of foreclosures in an effort to limit price declines. One agent warned of “shadow inventory” that could be coming to market in the upcoming months, and could reverse the positive September index readings.

Comments from real estate agents:

■ “We believe there is a shadow inventory being held by banks.”

■ “We have had good activity due to the tax incentive for first time homebuyers, but the shortage of inventory and demand in the marketplace has caused bidding wars in the affordable price ranges.”

MDC Holdings, Standard Pacific, Meritage, Pulte Homes, D.R. Horton and Toll Brothers have the greatest exposure. MDC and Standard Pacific have the largest exposure to Phoenix, contracting approximately 19% of total unit sales in the area, followed by Meritage (18%), Pulte (16%), D.R. Horton (11%) and Toll (10%).

Exhibit 20: Potential Foreclosures Coming to Market Could Depress Prices Further

Traffic Levels Versus Expectations

34%

30%36%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

33%26%

11%

48%

70%

45%

19%

4%

44%

0%10%20%30%40%50%60%70%80%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!

“Investors are still active.”

08 October 2009

Monthly Survey of Real Estate Agents 23

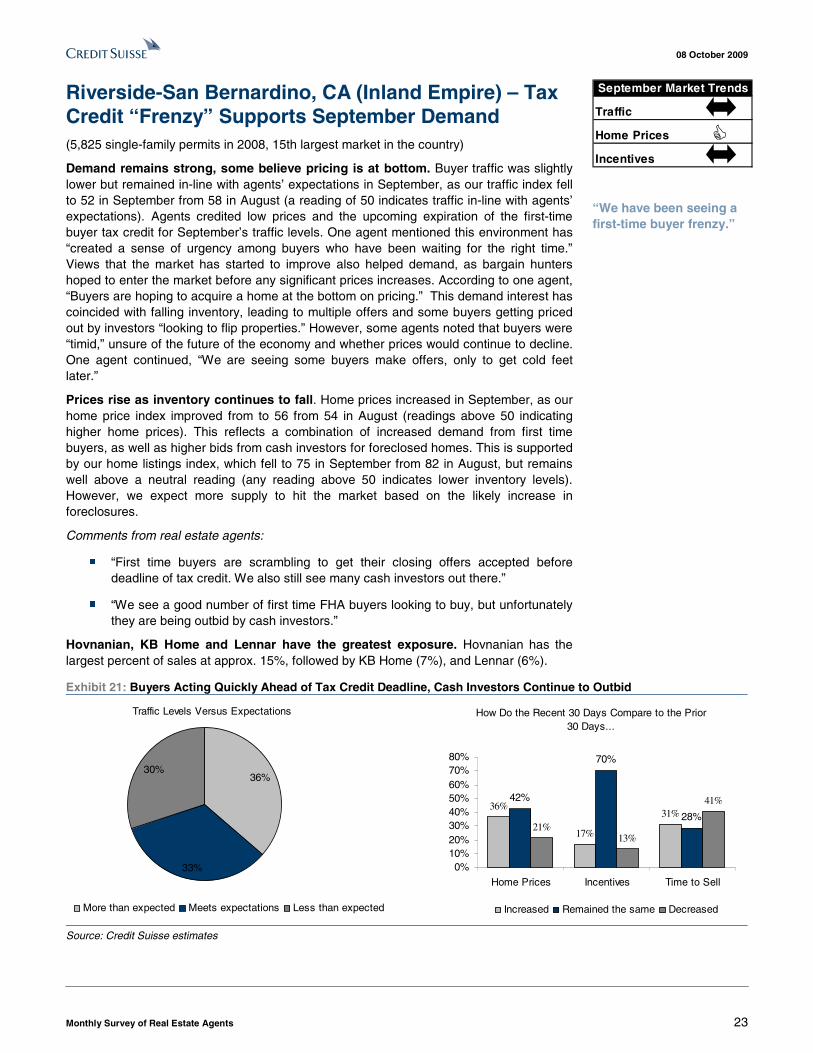

Riverside-San Bernardino, CA (Inland Empire) – Tax Credit “Frenzy” Supports September Demand (5,825 single-family permits in 2008, 15th largest market in the country)

Demand remains strong, some believe pricing is at bottom. Buyer traffic was slightly lower but remained in-line with agents’ expectations in September, as our traffic index fell to 52 in September from 58 in August (a reading of 50 indicates traffic in-line with agents’ expectations). Agents credited low prices and the upcoming expiration of the first-time buyer tax credit for September’s traffic levels. One agent mentioned this environment has “created a sense of urgency among buyers who have been waiting for the right time.” Views that the market has started to improve also helped demand, as bargain hunters hoped to enter the market before any significant prices increases. According to one agent, “Buyers are hoping to acquire a home at the bottom on pricing.” This demand interest has coincided with falling inventory, leading to multiple offers and some buyers getting priced out by investors “looking to flip properties.” However, some agents noted that buyers were “timid,” unsure of the future of the economy and whether prices would continue to decline. One agent continued, “We are seeing some buyers make offers, only to get cold feet later.”

Prices rise as inventory continues to fall. Home prices increased in September, as our home price index improved from to 56 from 54 in August (readings above 50 indicating higher home prices). This reflects a combination of increased demand from first time buyers, as well as higher bids from cash investors for foreclosed homes. This is supported by our home listings index, which fell to 75 in September from 82 in August, but remains well above a neutral reading (any reading above 50 indicates lower inventory levels). However, we expect more supply to hit the market based on the likely increase in foreclosures.

Comments from real estate agents:

■ “First time buyers are scrambling to get their closing offers accepted before deadline of tax credit. We also still see many cash investors out there.”

■ “We see a good number of first time FHA buyers looking to buy, but unfortunately they are being outbid by cash investors.”

Hovnanian, KB Home and Lennar have the greatest exposure. Hovnanian has the largest percent of sales at approx. 15%, followed by KB Home (7%), and Lennar (6%).

Exhibit 21: Buyers Acting Quickly Ahead of Tax Credit Deadline, Cash Investors Continue to Outbid

Traffic Levels Versus Expectations

33%

36%30%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

36%

17%

31%

42%

70%

28%21%

13%

41%

0%10%20%30%40%50%60%70%80%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

“We have been seeing a first-time buyer frenzy.”

08 October 2009

Monthly Survey of Real Estate Agents 24

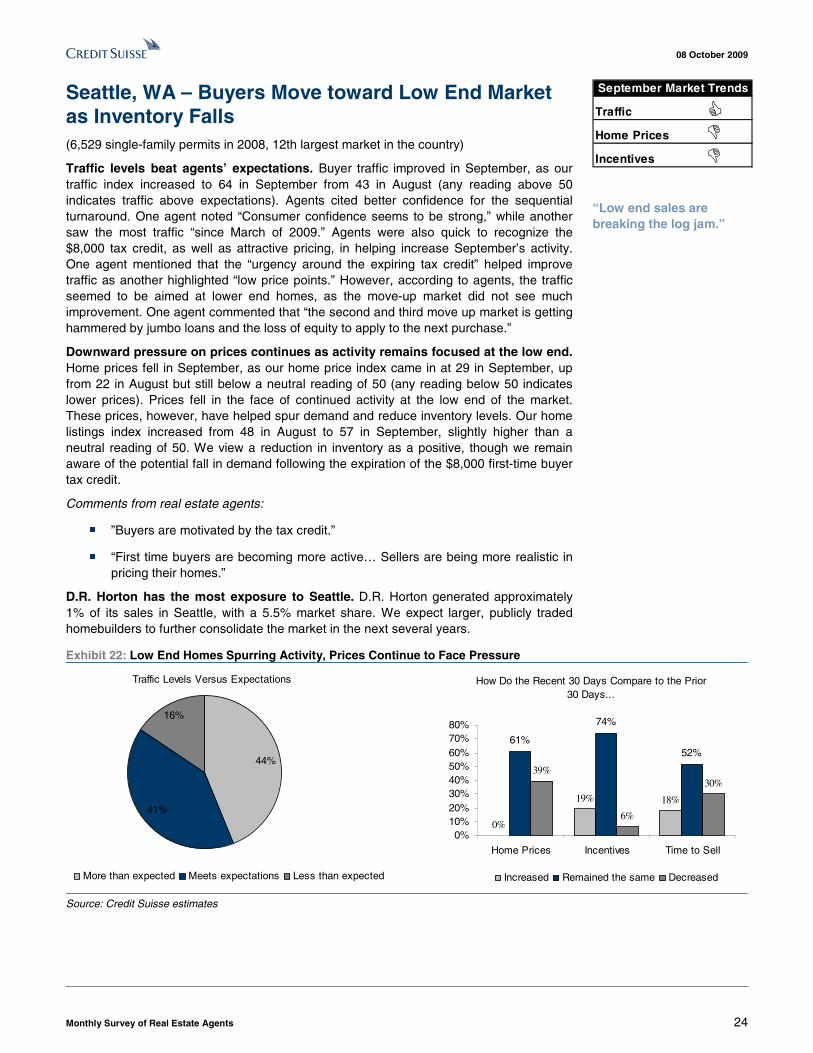

Seattle, WA – Buyers Move toward Low End Market as Inventory Falls (6,529 single-family permits in 2008, 12th largest market in the country)

Traffic levels beat agents’ expectations. Buyer traffic improved in September, as our traffic index increased to 64 in September from 43 in August (any reading above 50 indicates traffic above expectations). Agents cited better confidence for the sequential turnaround. One agent noted “Consumer confidence seems to be strong,” while another saw the most traffic “since March of 2009.” Agents were also quick to recognize the $8,000 tax credit, as well as attractive pricing, in helping increase September’s activity. One agent mentioned that the “urgency around the expiring tax credit” helped improve traffic as another highlighted “low price points.” However, according to agents, the traffic seemed to be aimed at lower end homes, as the move-up market did not see much improvement. One agent commented that “the second and third move up market is getting hammered by jumbo loans and the loss of equity to apply to the next purchase.”

Downward pressure on prices continues as activity remains focused at the low end. Home prices fell in September, as our home price index came in at 29 in September, up from 22 in August but still below a neutral reading of 50 (any reading below 50 indicates lower prices). Prices fell in the face of continued activity at the low end of the market. These prices, however, have helped spur demand and reduce inventory levels. Our home listings index increased from 48 in August to 57 in September, slightly higher than a neutral reading of 50. We view a reduction in inventory as a positive, though we remain aware of the potential fall in demand following the expiration of the $8,000 first-time buyer tax credit.

Comments from real estate agents:

■ ”Buyers are motivated by the tax credit.”

■ “First time buyers are becoming more active… Sellers are being more realistic in pricing their homes.”

D.R. Horton has the most exposure to Seattle. D.R. Horton generated approximately 1% of its sales in Seattle, with a 5.5% market share. We expect larger, publicly traded homebuilders to further consolidate the market in the next several years.

Exhibit 22: Low End Homes Spurring Activity, Prices Continue to Face Pressure

Traffic Levels Versus Expectations

41%

44%

16%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

0%

19% 18%

61%

74%

52%

39%

6%

30%

0%10%20%30%40%50%60%70%80%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!

!

“Low end sales are breaking the log jam.”

08 October 2009

Monthly Survey of Real Estate Agents 25

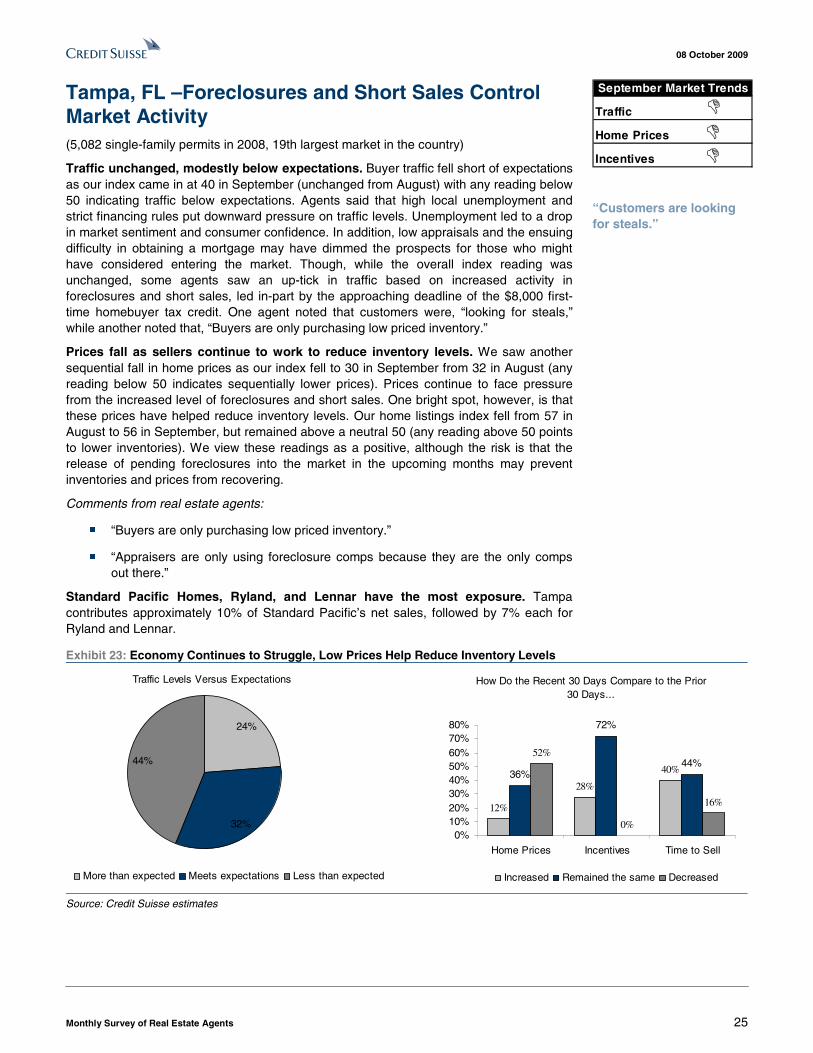

Tampa, FL –Foreclosures and Short Sales Control Market Activity (5,082 single-family permits in 2008, 19th largest market in the country)

Traffic unchanged, modestly below expectations. Buyer traffic fell short of expectations as our index came in at 40 in September (unchanged from August) with any reading below 50 indicating traffic below expectations. Agents said that high local unemployment and strict financing rules put downward pressure on traffic levels. Unemployment led to a drop in market sentiment and consumer confidence. In addition, low appraisals and the ensuing difficulty in obtaining a mortgage may have dimmed the prospects for those who might have considered entering the market. Though, while the overall index reading was unchanged, some agents saw an up-tick in traffic based on increased activity in foreclosures and short sales, led in-part by the approaching deadline of the $8,000 first-time homebuyer tax credit. One agent noted that customers were, “looking for steals,” while another noted that, “Buyers are only purchasing low priced inventory.”

Prices fall as sellers continue to work to reduce inventory levels. We saw another sequential fall in home prices as our index fell to 30 in September from 32 in August (any reading below 50 indicates sequentially lower prices). Prices continue to face pressure from the increased level of foreclosures and short sales. One bright spot, however, is that these prices have helped reduce inventory levels. Our home listings index fell from 57 in August to 56 in September, but remained above a neutral 50 (any reading above 50 points to lower inventories). We view these readings as a positive, although the risk is that the release of pending foreclosures into the market in the upcoming months may prevent inventories and prices from recovering.

Comments from real estate agents:

■ “Buyers are only purchasing low priced inventory.”

■ “Appraisers are only using foreclosure comps because they are the only comps out there.”

Standard Pacific Homes, Ryland, and Lennar have the most exposure. Tampa contributes approximately 10% of Standard Pacific’s net sales, followed by 7% each for Ryland and Lennar.

Exhibit 23: Economy Continues to Struggle, Low Prices Help Reduce Inventory Levels

Traffic Levels Versus Expectations

32%

44%

24%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

12%

28%

40%36%

72%

44%52%

0%

16%

0%10%20%30%40%50%60%70%80%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

!!!

“Customers are looking for steals.”

08 October 2009

Monthly Survey of Real Estate Agents 26

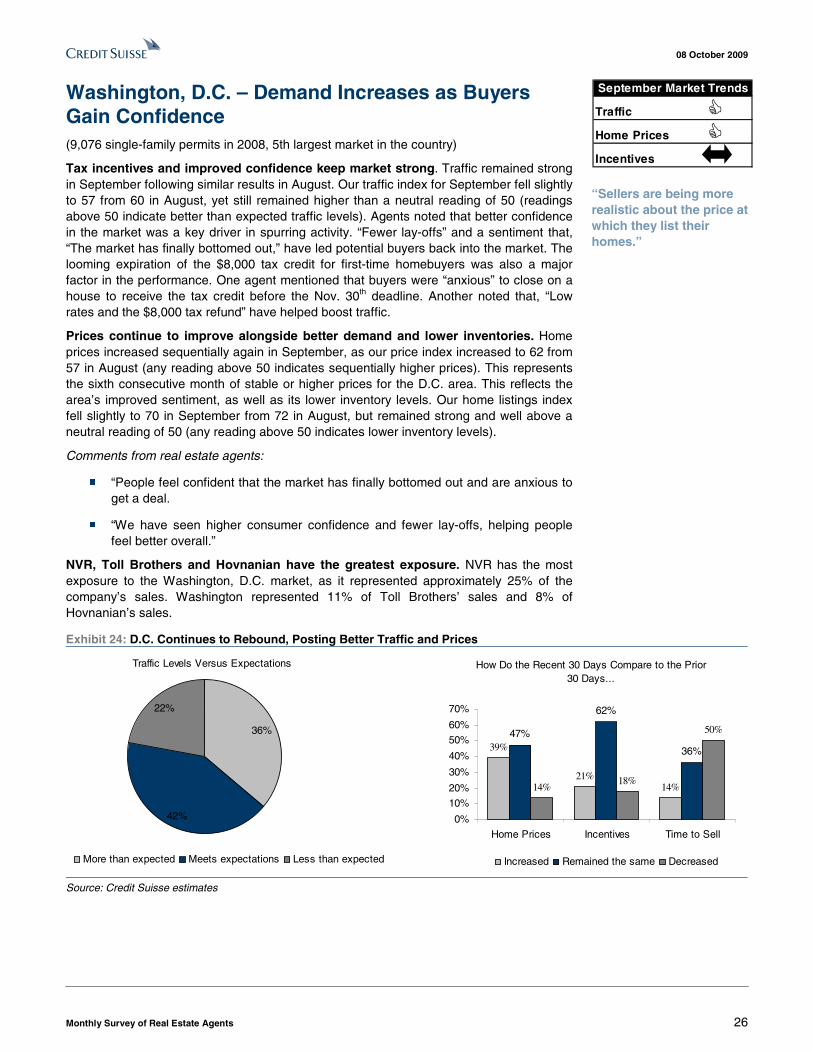

Washington, D.C. – Demand Increases as Buyers Gain Confidence (9,076 single-family permits in 2008, 5th largest market in the country)

Tax incentives and improved confidence keep market strong. Traffic remained strong in September following similar results in August. Our traffic index for September fell slightly to 57 from 60 in August, yet still remained higher than a neutral reading of 50 (readings above 50 indicate better than expected traffic levels). Agents noted that better confidence in the market was a key driver in spurring activity. “Fewer lay-offs” and a sentiment that, “The market has finally bottomed out,” have led potential buyers back into the market. The looming expiration of the $8,000 tax credit for first-time homebuyers was also a major factor in the performance. One agent mentioned that buyers were “anxious” to close on a house to receive the tax credit before the Nov. 30th deadline. Another noted that, “Low rates and the $8,000 tax refund” have helped boost traffic.

Prices continue to improve alongside better demand and lower inventories. Home prices increased sequentially again in September, as our price index increased to 62 from 57 in August (any reading above 50 indicates sequentially higher prices). This represents the sixth consecutive month of stable or higher prices for the D.C. area. This reflects the area’s improved sentiment, as well as its lower inventory levels. Our home listings index fell slightly to 70 in September from 72 in August, but remained strong and well above a neutral reading of 50 (any reading above 50 indicates lower inventory levels).

Comments from real estate agents:

■ “People feel confident that the market has finally bottomed out and are anxious to get a deal.

■ “We have seen higher consumer confidence and fewer lay-offs, helping people feel better overall.”

NVR, Toll Brothers and Hovnanian have the greatest exposure. NVR has the most exposure to the Washington, D.C. market, as it represented approximately 25% of the company’s sales. Washington represented 11% of Toll Brothers’ sales and 8% of Hovnanian’s sales.

Exhibit 24: D.C. Continues to Rebound, Posting Better Traffic and Prices

Traffic Levels Versus Expectations

42%

36%

22%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

39%

21%14%

47%

62%

36%

14%18%

50%

0%

10%

20%

30%

40%

50%

60%

70%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

“Sellers are being more realistic about the price at which they list their homes.”

08 October 2009

Monthly Survey of Real Estate Agents 27

Additional Key Housing Markets

08 October 2009

Monthly Survey of Real Estate Agents 28

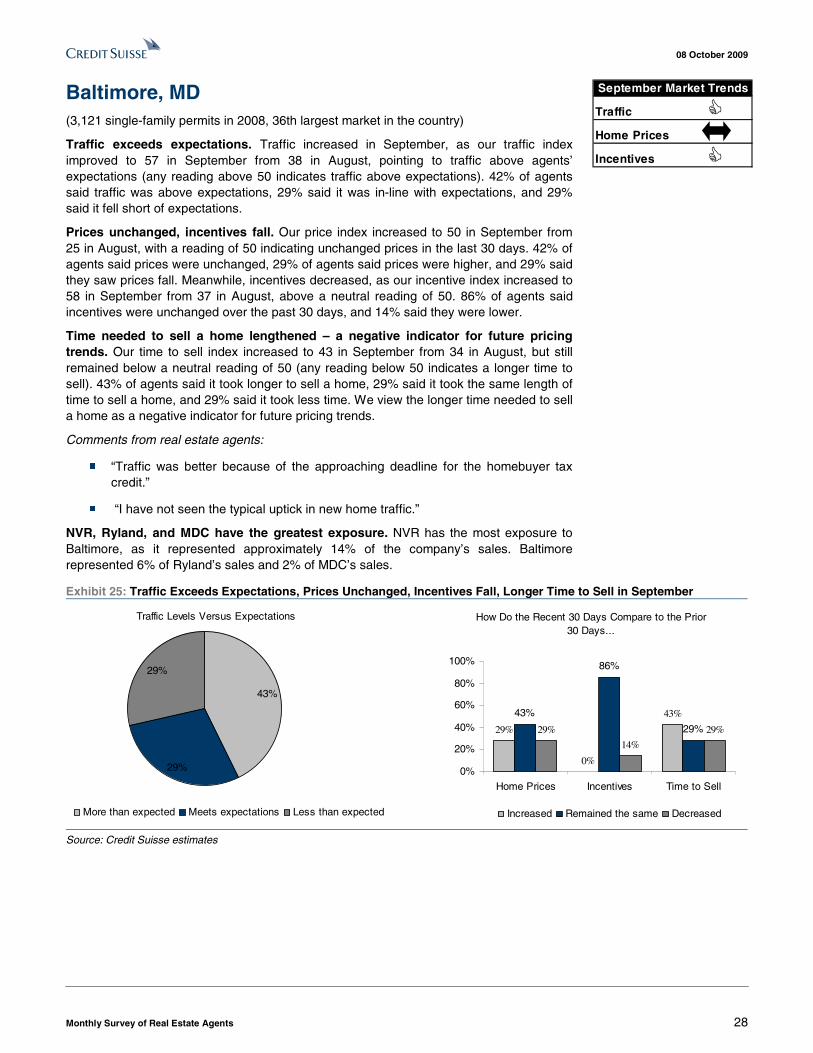

Baltimore, MD (3,121 single-family permits in 2008, 36th largest market in the country)

Traffic exceeds expectations. Traffic increased in September, as our traffic index improved to 57 in September from 38 in August, pointing to traffic above agents’ expectations (any reading above 50 indicates traffic above expectations). 42% of agents said traffic was above expectations, 29% said it was in-line with expectations, and 29% said it fell short of expectations.

Prices unchanged, incentives fall. Our price index increased to 50 in September from 25 in August, with a reading of 50 indicating unchanged prices in the last 30 days. 42% of agents said prices were unchanged, 29% of agents said prices were higher, and 29% said they saw prices fall. Meanwhile, incentives decreased, as our incentive index increased to 58 in September from 37 in August, above a neutral reading of 50. 86% of agents said incentives were unchanged over the past 30 days, and 14% said they were lower.

Time needed to sell a home lengthened – a negative indicator for future pricing trends. Our time to sell index increased to 43 in September from 34 in August, but still remained below a neutral reading of 50 (any reading below 50 indicates a longer time to sell). 43% of agents said it took longer to sell a home, 29% said it took the same length of time to sell a home, and 29% said it took less time. We view the longer time needed to sell a home as a negative indicator for future pricing trends.

Comments from real estate agents:

■ “Traffic was better because of the approaching deadline for the homebuyer tax credit.”

■ “I have not seen the typical uptick in new home traffic.”

NVR, Ryland, and MDC have the greatest exposure. NVR has the most exposure to Baltimore, as it represented approximately 14% of the company’s sales. Baltimore represented 6% of Ryland’s sales and 2% of MDC’s sales.

Exhibit 25: Traffic Exceeds Expectations, Prices Unchanged, Incentives Fall, Longer Time to Sell in September

Traffic Levels Versus Expectations

29%

29%

43%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

29%

0%

43%43%

86%

29%29%

14%

29%

0%

20%

40%

60%

80%

100%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

08 October 2009

Monthly Survey of Real Estate Agents 29

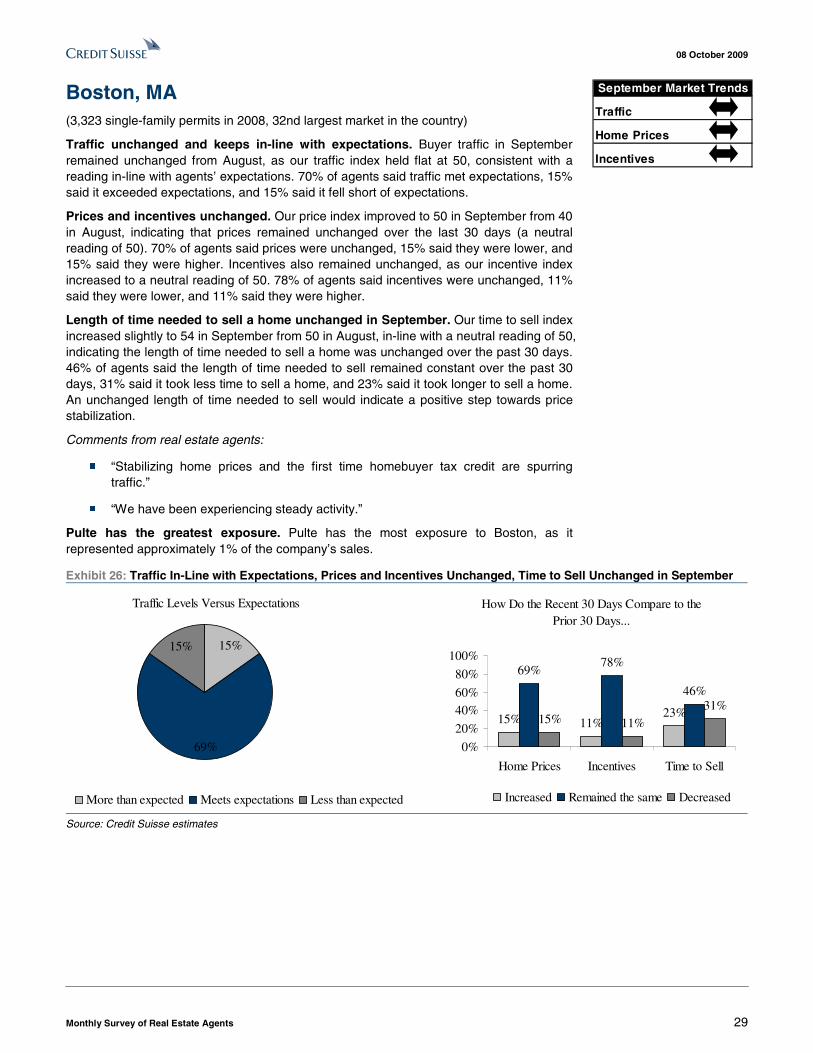

Boston, MA (3,323 single-family permits in 2008, 32nd largest market in the country)

Traffic unchanged and keeps in-line with expectations. Buyer traffic in September remained unchanged from August, as our traffic index held flat at 50, consistent with a reading in-line with agents’ expectations. 70% of agents said traffic met expectations, 15% said it exceeded expectations, and 15% said it fell short of expectations.

Prices and incentives unchanged. Our price index improved to 50 in September from 40 in August, indicating that prices remained unchanged over the last 30 days (a neutral reading of 50). 70% of agents said prices were unchanged, 15% said they were lower, and 15% said they were higher. Incentives also remained unchanged, as our incentive index increased to a neutral reading of 50. 78% of agents said incentives were unchanged, 11% said they were lower, and 11% said they were higher.

Length of time needed to sell a home unchanged in September. Our time to sell index increased slightly to 54 in September from 50 in August, in-line with a neutral reading of 50, indicating the length of time needed to sell a home was unchanged over the past 30 days. 46% of agents said the length of time needed to sell remained constant over the past 30 days, 31% said it took less time to sell a home, and 23% said it took longer to sell a home. An unchanged length of time needed to sell would indicate a positive step towards price stabilization.

Comments from real estate agents:

■ “Stabilizing home prices and the first time homebuyer tax credit are spurring traffic.”

■ “We have been experiencing steady activity.”

Pulte has the greatest exposure. Pulte has the most exposure to Boston, as it represented approximately 1% of the company’s sales.

Exhibit 26: Traffic In-Line with Expectations, Prices and Incentives Unchanged, Time to Sell Unchanged in September

Traffic Levels Versus Expectations

69%

15%15%

More than expected Meets expectations Less than expected

How Do the Recent 30 Days Compare to the Prior 30 Days...

15% 11%23%

69%78%

46%

15% 11%31%

0%

20%

40%60%

80%

100%

Home Prices Incentives Time to Sell

Increased Remained the same Decreased

Source: Credit Suisse estimates

Traffic

Home Prices

Incentives

September Market Trends

08 October 2009