90

Crnogorski Telekom 2013 AnnuAl RepoRt

Crnogorski Telekom2013 AnnuAl RepoRt

1our mission / our Vision

ConTenTs: to ouR ShAReholdeRSAbout Crnogorski TelekomSelected Financial and Operational Data of Crnogorski TelekomLetter to Our Shareholders

MAnAgeMent RepoRtManagement Report for the Financial Year 2013Crnogorski Telekom’s Management Board of Directors Executive Management BoardVision and StrategyRegulatory EnvironmentPromotions and Offers

huMAn ReSouRceS

coRpoRAte ReSponSibility

FinAnciAl StAteMentSIndependent Auditor’s ReportStatement of Financial PositionStatement of Comprehensive IncomeStatement of Cash FlowsStatements of Changes in EquityNotes to the Financial Statements

FuRtheR inFoRMAtion

3our mission / our Vision

To our shareholdersAbout cRnogoRSki telekoM

Crnogorski Telekom (CT) is the largest telecommunications company in Montenegro. It provides a full range of fixed and mobile telecommunica-tion services (voice, messaging, internet, TV, leased-line circuits, data networks and ICT solutions).

Crnogorski Telekom fully digitalised the fixed-line network in 2007 and brought ADSL coverage of PSTN customers close to a 100% base by the end of 2012. In December 2007, Crnogorski Telekom started an IPTV service. At the end of 2011 CT started offering ICT solutions, promoted under the name “Integris”.

CT was the second entrant into the mobile market in Montenegro. From its founding in 2000, it has always offered innovative and advanced services to the Montenegrin market and has been experiencing dynamic growth. Telekom uses mobile technologies such as UMTS, HSDPA, GPRS and EDGE. A 3G network was launched in the summer of 2007. A 4G service was softly launched in 2012, while wider coverage was brought to the market in 2013.

In 2006, the T-Com and T-Mobile brands were launched.

In May 2009, Crnogorski Telekom a.d., T-Mobile Crna Gora d.o.o and Internet Crna Gora d.o.o were merged into one legal entity, Crnogorski Telekom a.d.

In 2012, the T-Com and T-Mobile brands were replaced by the Telekom brand, under which all products are now marketed.

On 1 April 2005, Magyar Telekom obtained a 76.53% interest in Crno-gorski Telekom. Deutsche Telekom AG holds 59.21% of the Magyar Telekom shares. Deutsche Telekom and Magyar Telekom have a number of subsidiaries worldwide, with which Crnogorski Telekom has regular transactions. Details of related party transactions are given in the com-pany’s Financial Statements, Note 28.

5our mission / our Vision

odabrani finansijski i operaTiVni podaCi Crnogorskog Telekoma

Main financial KPIs (€ million) 2012 2013 Δ Δ%

Revenues and Other income 114,3 110,2 -4,1 -4

EBITDA w/o SI 44,1 43,3 -0,8 -2

EBITDA w/o SI margin (%) 38,6 39,3 0,7

EBITDA 42,7 39,8 -2,9 -7

EBITDA margin (%) 37,3 36,1 -1,2

Operating profit 21,1 20,1 -1,0 -5

Net profit 19,9 18,8 -1,1 -5

Total Assets 200,7 198,2 -2,5 -1

CAPEX 14,5 14,5 -0,1 -1

Number of employees (closing FTE) 729 651 -78 -11

Fixed line operation KPIs (in thousands)* 31 Dec 2012 31 Dec 2013 Δ Δ%

Fixed-voice customers, Total 167.8 167.2 −0.7 0

Fixed-voice market share (%) 98.1 98.3 0.1

ADSL customers, Total 69.6 74.4 4.7 7

BB internet market share (%) 82.6 81.8 −0.8

IPTV customers, Total 56.3 61.8 5.5 10

Pay TV market share (%) 42.0 41.6 −0.4

Mobile line operation KPIs (in thousands)* 31 Dec 2012 31 Dec 2013 Δ Δ%

Number of customers, Total 340.0 352.8 12.8 4

Prepaid 203.4 214.8 11.4 6

Postpaid 136.7 138.1 1.4 1

Mobile customers market share (%) 34.3 35.5 1.2

Mobile internet customer numbers 87.1 96.9 9.8 11

Mobile internet customers market share (%) 39.6 40.6 1.0

Mobile penetration (%) 160 160 0.5

* Source: Montenegro Agency for Electronic Communications and Postal Services

6

dear shareholders,

As always at this time of the year, I have the pleasure of sharing with you our view about Crnogorski Telekom’s most significant moments in 2013 when it comes to business developments. This year can be summarised in a few words: facing remarkable challenges, we achieved remarkable success. I am happy to report that, despite negative macroeconomic developments, characterised by constant state budget deficits, failure to achieve the projected growth rate, risks caused by social pressure, high economic illiquidity, decreased FDI inflow, still causing additional pres-sure on economic stability in 2013, Crnogorski Telekom has managed to preserve its market superiority, stable financial performance and has had significant achievements on its transformational path. Speaking of financial achievements, let me inform you that our revenues, amounting to €110.2 million, exceeded the Budget by €8.2 million (8%), driven by Wholesale revenues, equipment/handset sales and ICT revenues, while service revenues deteriorated (€−2.2million). Furthermore, EBITDA was €0.25 million higher and solid oFCF performance was successfully maintained.

The business year 2013 was fairly successful and pretty much in line with our expectations, which, in our view, results from the full commit-ment of our management to the already proclaimed strategic framework based on three strategic layers (Stand 4 Broadband – capturing and retaining customers and outperform competition; Transform 2 Out-perform – full focus on e-Business, e-Company, One Billing/CRM and

Save2Invest initiatives and New Way 2 Play – growing revenue streams in ICT/Cloud and Retailer No.1 initiatives, new business development and exploring partnering concepts, and the transformation program DELFIN, in order to achieve operational, financial and market excellence.

Not surprisingly, the year 2014 will be full of challenges for all industries, particularly for such fast-developing and changing ones such as tele-communications, in which operators are under high pressure in today’s business climate and facing revenue decline every year. The fact is that these changes create opportunities but there is also increasing competi-tion in every market segment, especially in fixed-line telephony, driven by aggressive rollout, lower broadband prices and content advantages compared to CT. Tension also comes from operators’ pressure to provide services which are attractive enough, in terms of both price and quality, to keep the existing customers and acquire new ones, smartly targeting different customer segments with adequate and unique proposals. It is unbelievable how quickly technological disruptions change customers’ behaviour and expectations, as they see operators as the means for con-nectivity and a convenient lifestyle, providing them with everything on demand and on whichever device. At the same time, operating costs need to be brought under control and all operators are planning efficiency improvements. As you well know, we have been very active and innovative in that regard for years, constantly thinking about how we can simplify our daily operations in order to increase efficiency and save at all levels, so that we can provide funds to invest in our resources in new products and services. Our newest invention when it comes to efficiency improvement is so called the Save to Invest (S2I) program, through which saving initiatives were developed and executed, aimed at reaching financial and indirect cost targets. Our cost saving target was defined at the level of €2.4 million and almost the entire amount has already been covered by our initiatives. But we will not stop there. We will be constantly looking for additional saving opportuni-ties, and cost control will definitely remain one of our watchwords in the upcoming period. We must tightly manage our cost base to ensure we are efficient and focused only on delivering what matters to our custom-ers. However, we must also have an ambitious plan for long-term growth. We as a company have never been interested in improving our efficiency simply through cutting costs. What we need is to be winning in key markets and being innovative enough to deliver growth through the rev-enue base as well. I am also very focused on ensuring we have the right leadership capability across the organisation. This company has many talented and passionate people who are keen to deliver great solutions and service to our customers. It is also being proved through numerous transfers of knowledge that we introduced in 2013, and through which a constantly increasing number of our colleagues are being recognised as the most qualified and most preferred people for demanding positions at DT Headquarters. Hard and dedicated work always pays dividends.

As I said, a very demanding year is again ahead of us, also due to unpre-dictable new taxes and fees creating an additional financial burden and legal issues (local taxes, the new method of VAT treatment, new personal income tax, VAT increase, tourist tax increase, etc.) and constantly increasing regulatory requirements. However, we are confident that, with our customer focus, constant innovations, investments in both fixed-line and mobile networks searching for new revenue potentials, we will improve our performance at all levels, develop to be stronger and better able to serve customers and maintain solid profitability.

As in previous years, we continued to maintain a very substantial volume of investments of €14.5 million. We achieved good business results

7dear shareholders

and invested significantly in the latest technology. Crnogorski Telekom further improved substantially the technological basis of the company and continued modernisation of the fixed-line and mobile network with state-of-the-art technology, with special emphasis on the IT infrastructure and access to the broadband network (One Billing &CRM system, FTTH rollout, IPTV, IMS etc.)

Speaking of other 2013 achievements, last year provided a good response to our efforts aimed at development of new markets and new products. We were focused on launching the LTE network, intensive FTTH rollout, expanding ICT business, One Billing project implementa-tion, launching the Hybrid Access project, the IPTV Upgrade project, minimising negative effects of the extensive regulatory changes and continuation of the Delfin transformation program. With regards to Crnogorski Telekom as an ICT company, I am happy to inform you that the positive trend launched in 2012 is continuing also in 2013 and that we are exceeding a 100% revenue growth rate compared to 2012, sig-nificantly contributed to by the hotel and resort segment, securing also strong potential for the years to come. In that particular area we targeted €4 million of ICT revenues for 2014.

Our wholesale business, despite huge challenges, delivered good results in 2013. Revenue plans have been exceeded in all business seg-ments. Mitigated regulation of international voice termination and good roaming results marked this year of wholesale business. Just before the end of the year a deal worth €2. 3 million for the long-term lease of opti-cal fibres with Telenor was signed.

Working in such a challenging environment, we at Crnogorski Telekom are continuously looking for new revenue opportunities. One of them that has proved to be successful is selling devices. Compared to our ini-tial 2013 plans for equipment revenue in the consumer segment (€820 thousand), we can report nearly 100% overachievement (€1.63 million). The most significant contribution to consumer financing revenue in 2013 comes from laptop and TV sales (76%). Sales results in this segment place Crnogorski Telekom as a significant market player in retail in Montenegro.

Regarding development of the fibre story, I point out that our teams have already provided access to fibre optic data transfer for almost 28 households in Montenegro. We gained 3,400 new fibre users, and 7,000 users in total, which means that in 2013 we almost doubled the number of fibre users in 2012 + 2011, since at the end of 2012 we had around 3,600 customers! At the end of 2013 the utilisation rate amounted to 25%, i.e. every fourth user in the zones covered by the fibre network uses some of our services. Speaking of the LTE Rollout (4G), this year eighteen 4G base stations were installed in seven cities. Over the next four years in our develop-ment plans we have foreseen installation of one hundred 4G base stations, hoping thereby to increase customer satisfaction by fulfilling growing demand for quality, coverage and speed. In that regard we have also offered them a wide selection of devices supporting 4G. Our 4G implementation offers superior features and, combined with our superior mobile hardware portfolio, this allows us to offer the best broadband experience on the move.

Let me continue the story of our success with a short reminder of the outcome of the second benchmark survey “The best company to work for in Montenegro” 2013/2014, according to which Crnogorski Telekom received an award for the Best Company to Work for in Montenegro –

first place in the large companies category (Main Award) and The Most Attractive Employer – first place in the survey among university students, which I particularly like, since it indicates that young people consider that our company meets the challenges of the modern business environ-ment in the best possible way.These prestigious awards belong to all of us because we deserved it through our joint efforts, personal, professional and business values that we have embedded in our company culture, as well as through fighting for high quality in each and every segment of our business operations.

We have been investing significant effort in increasing employee satisfaction, seeing our employees as a key factor in our success. In that regard I am happy to inform you about the closing of the housing loan distribution process, enabling 148 employees to permanently resolve this particularly important issue for themselves and their family mem-bers. I am also very happy that we further improved cooperation with the Trade Union, which also resulted in a successfully organised and implemented Voluntary Leave Program (VLP).

We have also been investing significant efforts in increasing customer satisfaction. Crnogorski Telekom’s strong commitment to continuously improve customer service is reflected in positive development of cus-tomer loyalty indices. Special attention in 2013 was paid to the TRI*M (customer satisfaction) index, which resulted in the first increase of fixed and mobile line TRI*M results after 2 years of decline, with special em-phasis on the fact that those exceeded the main competitor’s average. But this is only the beginning. We already developed the main recom-mendation for improving results in 2014 for both segments.

Crnogorski Telekom experienced a limited YoY decrease of Earnings before Interest, Tax and Depreciation (EBITDA) before special impacts of €0.8 million (−2%) to a level of €43.3 million. The Net Profit achieved by Crnogorski Telekom in 2013 amounted to €18.8 million, which represents a YoY decrease of €1.1 million (−5%). In 2013 the company paid out dividends of €22.9 million and the dividend yield amounted to 10.9%.

I would like to take the opportunity to thank all of our employees for their dedicated and skilled efforts in 2013, which are the basis on which we can achieve our objectives during the coming years.

Finally, dear shareholders, let me also thank you, for the third time already, for your contribution to the success of our company. Your trust and confidence have always been a great support for us and we will feel free to keep counting on it.

Rüdiger J. SchulzChief Executive Director

8

managemenT reporTMAnAgeMent RepoRt FoR the FinAnciAl yeAR 2013

Highlights

The decrease in revenue was limited to 3.6%, with a total revenue of €110.2 million mainly driven by the development of voice revenues, both retail and wholesale, and partly offset by the increase in internet, TV, ICT and equipment sales revenues.

EBITDA excluding special influences decreased by 1.9% to €43.3 million, with an achieved margin of 39.3%. Net profit decreased YoY, by €1.1 million, or 5.5%, to €18.8 million. Capital expenditure was €14.5 million. It mainly related to: One Billing & CRM, fibre-optic network roll-out, IPTV and IMS. Dividends of the amount of €22.9 million were paid out.

Revenues and profitability Although 2013 was operationally and financially very challenging, due to the economic downturn and the difficult market conditions, Crnogorski Telekom was focused on expanding its broadband services, on fibre-optic access roll-out, on expansion of the ICT service (Integris) and on the im-provement of voice services. In the fixed-line voice segment, CT kept a stable customer base, while ADSL and Extra TV customer numbers increased. In the mobile segment CT retained both total postpaid and business segment postpaid leadership and further strengthened its leadership position regarding the mobile internet market.

Even though the development in the number of customers was mainly positive, CT experienced a moderate revenue decline. By limiting the YoY de-crease to only 3.6%, CT performed better than most of its peers. Revenues reached €110.2 million. The retail revenue decrease was limited to 1.7%, while wholesale revenues decreased by 11%. Major revenue downsides, compared to 2012, related to: interconnection revenues (−14%), which was a consequence of decreased mobile termination rates and lower incoming traffic, fixed-line voice retail revenues (−7%), influenced by decreasing usage, and mobile prepaid revenues (−11%), influenced by the 1EUR Tax, introduced in 2012, and generally lower usage.Such development was partly compensated by higher: ADSL revenues (+3%), driven by higher customer numbers, IPTV revenues (+8%), driven by higher customer numbers, data services revenues (+6%), driven by the growth of CT’s Integris service, and equipment sales revenues (+51%), boosted by sales of TVs/laptops and handsets sale.

As a result of continuous successful efforts to increase efficiency and improve the cost base, operating expenses excluding special effects at the same time decreased YoY by €3.3 million (−5%), to the level of €66.9 million.

The limited YoY revenue decrease and cost efficiency resulted in a moderate YoY decrease of EBITDA excluding special influences of 1.9%, to the amount of €43.3 million.

Operating profit (EBIT) decreased YoY by €1.0 million to €20.1 million, mainly due to higher severance payments in 2013. Net profit decreased by €1.1 million to €18.8 million.

9dear shareholders

Main Non-Financial KPIs In 2013, the fixed-line voice customer number was stable. The ADSL revenue increase was driven by a customer base increase of 4,700 or 7%. IPTV revenues also increased due to a customer number increase of 5,500 YoY or 10%.

Fixed-line operations KPIs (in thousands)* 31 Dec 2012 31 Dec 2013 Δ Δ%

Fixed-voice customers, Total 167.8 167.2 −0.7 0

Residential 145.8 145.5 −0.3 0

Business 22.0 21.7 −0.4 −2

Fixed-voice market share (%) 98.1 98.3 0.1

ADSL customers, Total 69.6 74.4 4.7 7

Residential 62.4 66.7 4.3 7

Business 7.2 7.7 0.4 6

BB internet market share (%) 82.6 81.8 −0.8

IPTV customers, Total 56.3 61.8 5.5 10

Residential 54.4 59.7 5.3 10

Business 1.8 2.0 0.2 11

Pay TV market share (%) 42.0 41.6 −0.4

By the year end of 2013, 352,800 customers were using Telekom’s mobile services, 12,800 more than at the end of 2012, an increase of 4%, whereas both Prepaid and Postpaid segments were growing. The main driver of such development is an increase of the Prepaid customer base of 11,400 or 1%. At the same time, the Prepaid SIM market share increased by 2pp, to 32.1%. Although Postpaid customer numbers increased by 1%, to 138,100, the Postpaid SIM market share decreased by 0.8pp, to 42.5%. Still, Crnogorski Telekom remains the market leader in that segment. Consequently, the total SIM market share increased by 1.2pp, to 32.1%. The number of mobile customers using the internet at YE 2013 increased by 9,800 or 11% YoY.

Mobile line operation KPIs (in thousands)* 31 Dec 2012 31 Dec 2013 Δ Δ%

Number of customers, Total 340.0 352.8 12.8 4

Prepaid 203.4 214.8 11.4 6

Postpaid, Total 136.7 138.1 1.4 1

Postpaid Residential 34.1 36.7 2.6 8

Postpaid Business 102.6 101.4 −1.2 −1

Mobile customers market share (%) 34.3 35.5 1.2

Mobile internet customer number 87.1 96.9 9.8 11

Mobile internet customers market share (%) 39.6 40.6 1.0

Mobile penetration (%) 160 160 0.5

* Source: Montenegro Agency for Electronic Communications and Postal Services

10

Main investments In 2013, CT started major investment in One Billing/CRM (Customer Relations Management), with total budget of €12.2 million, of which €3.2 million was spent in 2013 (22% of total CAPEX spent). The new billing system will replace the current three separate billing systems. It will increase market competitiveness, by enabling fully convergent offers to the market (prepaid/postpaid and fixed/mobile) and it will enable real-time rating, which will fulfil certain regulatory requirements (“bill shock” prevention). It will also support CT’s way towards becoming an e-company, which is DT Group’s strategic direction.

Following its Mobile Access Strategy, after successful RAN Modernisation, in 2013 investments in the mobile network were focused on new technolo-gies. The major project finished in 2013 was the LTE commercial launch. After the successful LTE soft launch in Podgorica and Kotor in November 2012, roll-out of eighteen new base stations in seven cities, implementation of the new Evolved Packet Core (EPC) and its integration with the billing and provisioning system were completed in the first half of 2013. With this, the LTE network reached a coverage of 38% of the population providing download speeds of up to 100 Mbps and upload speeds of up to 50 Mbps. LTE technology supports packet-based services, however in CT’s LTE architecture, implemented CSFB (circuit switched fall back) function-ality enables continuous voice services on LTE.

In 2013, a major upgrade of the IPTV platform, which started in 2012, was successfully finished in July 2013. Besides the improvement in stability and performance, this upgrade brought some new features: TVTeka offers content from 10 local channels available for the past 48 hours without manual recording, the VOD storefront offers a completely new look & feel. All of this gives us a competitive advantage in the area of TV. On the content side, the number of channels in 2013 was increased to 115 channels with standard definition and 6 channels with high definition. Also, the TV Shared Service Centre hosted by Magyar Telekom has been up and running since 2013 as a joint Deutsche Telekom Europe operators initiative to consoli-date TV expertise and bring an additional decrease in costs and accelerated time-to-market for TV products. Crnogorski Telekom was involved in its establishment and starts participation from 2014. Following the Fixed Access Strategy, we continued with investments in the FTTH network during 2013. The focus was on new zones. Plans for 2013 were exceeded. Year end results were as follows: 27,642 households covered by the fibre network and 6,971 homes actually connected to the net-work, which gives a utilisation rate of 25%. After the successful implementations of the IMS platform in 2011, in 2013 we have continued with customer migration, in parallel with a platform upgrade. We have exceeded our 2013 target and finished the year with more than 48 thousand IMS customers, or more than 30% of active voice customers were using IP-based voice technology.

The changeover of the existing Mobile Packet Core Network to the Evolved Packet Core (EPC) was executed. The main reasons for the changeover were: to support mobile data traffic growth, to make the network LTE-ready and update HW/SW. The project was successfully finished in July 2013. All users were migrated without any problem. This project was a precondition for LTE implementation in the CT mobile network.

Last but not least, CT is first operator in the country to introduce HD voice technology. Mobile HD voice, based on AMR (Adaptive Multi Rate) Wide-band technology (W–AMR) enables high-quality voice calls in mobile 2G and 3G networks and an improved user experience. It provides significantly higher voice quality for calls between mobile phones supporting the feature.

11dear shareholders

12

Crnogorski Telekom’s board of direCTors János Szabo - Chairman, Susanne KrogmannMelinda Szabo, Tripko KrgovićPéter ZsomThilo KuschMihály Németh

jános szabóJános Szabó was born in Hódmezovásárhely (Hungary) in 1961. He graduated at the Budapest University of Economics in 1986, majoring in international relations.After working in foreign affairs for three years, he continued in various finance and consultant positions in the private business sector. He became Director of Finance at Delco Remy Hungary (a subsidiary of the US-based automotive supplier) in 1995. Later he became Deputy General Manager of the operation, responsible for sales, purchasing and operations. In 1998 he moved to the position of Director of Finance for Europe, in charge of the finance activities and acquisitions of European operations. Later he became CFO and Managing Director of a joint venture between Delco Remy and Hitachi. From April 2003 he was the Finance Director of the Wireline Services LOB of Magyar Telekom (later T-Com). The role was extended to the fixed-line network and IT opera-tions in 2006. Since January 2008, he has been the Director of Group Planning & Controlling of the Magyar Telekom Group. He is a member of the BoD of Crnogorski Telekom, MakTel and TMMK.

susanne krogmannSusanne Krogmann, born in 1964, holds a diploma in economics from Georg-August-University in Göttingen, Germany. After graduating, she went on to study European Integration at the College of Europe, Bruges, Belgium. She started her career at the Treuhandanstalt, the state-owned agency responsible for the privatisation of the enterprises and assets of the former Democratic Republic of Germany. During her five years at the Treuhandanstalt, Susanne Krogmann worked in the controlling and con-tract management departments. For the last 2 years there she held the position of Key Account Manager for several companies in the chemical industry. Susanne Krogmann joined Deutsche Telekom in 1999. For more than 8 years she worked in different positions in the Regulatory and Public Affairs division, especially in the field of regulatory econom-ics and regulatory strategy. She then took over the position as head of the Corporate Responsibility Strategy and Controlling group, where she developed a new Corporate Responsibility strategy for the DT group. Following increasing awareness of data security and data protection at Deutsche Telekom, she then worked on a data security project with a personal focus on customer data security. Since the end of 2009 she has held the position of Vice President of Corporate Governance Europe within Board Area Europe at Deutsche Telekom. Since 2011 she has been a member of the Board of Directors of Crnogorski Telekom.

melinda szaboMelinda Szabo was born in Budapest, 1971. She graduated from the College of Trade & Catering in 1994, followed by a second Bachelor’s degree in marketing at the College of Foreign Trade in 1997. She com-pleted a Masters in Business Administration at WEBSTMBA in 2007.She started to work for Westel Mobile Co. Ltd. in 1999 as a marketing manager. During the past 10 years she has managed different projects in the area of consumer marketing. After several career steps she was promoted to Deputy Marketing Director in 2005. From January 2008, she was Deputy Marketing Director of the Consumer Segment Market-ing Unit of Magyar Telekom, responsible for the T-Home and T-Mobile brands. She was appointed as Director of Consumer Segment Marketing Directorate effective from 1 July 2010.She has been a member of the Supervisory Board of Origo Media and Communication Services Provider Co. Ltd. (member of the Telekom Group) since August 2010.

13dear shareholders

péTer zsomPeter Zsom was born in Budapest, Hungary in 1973. He gained his first degree in Germanic Studies at ELTE University in 1999. Afterwards he received a second degree in economics at the College of Foreign Trade in Budapest in 2003. He started his career working for the Hungarian Tax Authorities in the PR department. He joined Westel in 1999 and first worked in customer relations. From 2002, he led various sales and product development projects as Project Manager, participated in the T-Mobile re-branding project in 2005 and was the head of the Integrated Sales Campaign Management Department in 2008. After that he worked for Deutsche Telekom in Germany as Senior Launch & Lifecycle Manager responsible for international product management within the DT Group. After returning to Magyar Telekom in 2010, Peter led various strategic projects. In April 2011 he joined Area Management MT at Deutsche Telekom and has been responsible for Magyar Telekom ever since.

Thilo kusChThilo Kusch (born in 1965) graduated from the Technische Universität Berlin in Business Administration and Electrical Engineering, specialis-ing in corporate finance and communication engineering. At the begin-ning of his career he worked as consultant/manager at Arthur D. Little Ltd. in London, then from 1998–2001 at Dresdner Kleinwort Wasserstein in London, first as a Telecom Equity Analyst in the position of Assistant Director, then as an Telecom Marketing Analyst in the position of Direc-tor.In 2001 he joined Deutsche Telekom, T-Mobile International where he held the position of Head of Investor Relations. In 2002 he became Head of Investor Relations in Headquarters of Deutsche Telekom in Bonn where he was responsible for communications with equity markets and in 2006 became Chief Financial Officer and a member of the Board of Directors in Magyar Telekom Nyrt. In his current position, he is responsible for group finance (controlling, accounting, tax, treasury, M&A, IR, procurement, real estate, shared ser-vices). In 2008 and 2009 he received an award for best investor relations and as the best corporate governance officer.

mihály némeThMihály Németh (born in 1974) graduated as a certified economist at the Budapest University of Economy, then as a certified lawyer at the ELTE Law Institute of Higher Education. In 2005 he became a CFA charterholder (certified financial analyst), which is a highly recognised designation in the field of investment profession. At the beginning of his career he worked as an equity analyst at BudaCash, then at the K&H Brokerage Company in Hungary. He joined MATÁV Rt., the predecessor of Magyar Telekom, in 1998. Initially he worked in the telecommunica-tions company as a business analyst, then from 2000 as Head of the Business Planning Department and from 2004 as Deputy Controlling Di-rector. In 2008 he was appointed as Director of Magyar Telekom Group Headquarters, Finance Directorate. Between 2010 and 2012 he worked as the director of the company’s Central Services Directorate. This organ-isation operated as the multifunctional service centre of the holding. Since January 2013 he has held the position of Strategic Asset Manage-ment Director. In this function he is responsible for subsidiary portfolio management, M&A, Treasury, Working Capital management and Partner Settlement functions of Magyar Telekom. In recent years he has taken various positions in the boards of directors and supervisory boards of various companies. He is currently the Chairman of Origo Zrt’s Supervi-sory Board and a member of the Board of Directors of Vidanet Zrt.

Tripko krgoVićTripko Krgović was born in 1977 in Belgrade. He finished his undergrad-uate and Master’s studies at the Faculty of Economics in Podgorica. His professional career began in 1996 at his family business. From 2004 he worked in the Securities Commission, in the Market Supervision Depart-ment. In 2005, he held the position of Investment Manager in Moneta Investment Fund. From 2006 to 2008, he was the Chief Executive Officer of Moneta Broker–Diler AD, Podgorica. From 2008 to 2011, he was a member of the Board of Directors of the Moneta privatisation fund and of Otrantkomerc AD, Ulcinj. He is a representative of the minority share-holders in some of Montenegro’s largest companies. He was elected a member of Crnogorski Telekom’s Board of Directors, Audit Committee and Compensation Committee in 2008.

14

The exeCuTiVe managemenT board of Crnogorski Telekom

15dear shareholders

Rüdiger Schulz, Chief Executive Officer and Chairman of the Executive Management BoardDr. Gabor Altmann, Chief Commercial Officer Residential Endre Horanyi, Chief Human Resources OfficerVladan Peković, Chief Technology and Information OfficerManfred Knapp, Chief Financial OfficerVladimir Beratović, Chief Corporate Affairs Officer Milija Zeković, Chief Commercial Officer Business

16

endre horanyiChief Human Resources Officer Endre Horanyi was previously an HR Partner of the Consumer Business Unit at Magyar Telekom. According to the MT organisational model, he was in charge of more than 4 000 people. From that position Mr. Horanyi joined Magyar Telekom in 2003. His professional development in the field of HR management mainly relates to his career path within MT. From 2003 until now, he has covered several positions related to HR functions such as: Senior HR Operational Development Manager, Head of HR Operational Development, HR Director of the Mobile Business Unit and most recently: HR Partner of the Customer Business Unit. Since June 2010, he has been working as Chief Human Resources Officer at Crnogorski Telekom.

Vladan pekoVićChief Technology and Information Officer

Vladan Peković took over the position of Chief Technology and Informa-tion Officer in January 2014. He came from T-Mobile Poland, where he was Technology and Platforms Director and Chairman of the Supervi-sory Board of Networks.Before joining DT group in 2009, he gained vast experience during long-lasting international carrier working for major telco companies on projects of development, implementation and management of telecom-munications networks in the Czech Republic, Mexico and the USA.

rüdiger sChulz Chief Executive Officer and Chairman of the Executive Management Board

Rüdiger Schulz, who is an internationally experienced business leader, completed his studies in electrical engineering at the University of Ham-burg and business management studies at the University of Koblenz. His professional career began with service in the German Navy as Chief Engineer on Vessels, after which he joined Deutsche Telekom Group in 1991. To begin with, he was responsible for technology platforms, and later became responsible for marketing and sales in the residential and corporate segment. In 2005, he began working for T-Systems as Senior Executive Vice President of Business Customers and Large Enterprises in the north-eastern region of Germany, one of six in the country and de-veloped his experience in the area of IT. He joined Slovak Telekom in No-vember 2006, taking over the position of Senior Executive Vice President for Marketing, Sales and Technology/COO and was a member of the Executive Management Board being responsible for T-Com’s product and service portfolio in the business, residential and wholesale segment. In July 2010 he was appointed Chief Operating Officer for Networks and IT of Slovak Telekom. From October 2011 he joined Crnogorski Telekom in his current position.

dr gabor alTmannChief Commercial Officer for Residential Area Dr. Gabor Altman joined Crnogorski Telekom in January 2013, when he took over the position of Chief Commercial Officer for Residential Area. He came from Makedonski Telekom, from the position of Chief Sales Officer.In the last 10 years he has covered different positions within Magyar Telekom Group including Makedonski Telekom, T-Mobile Macedonia, T Systems and T-Mobile Hungary. His professional experience at previous positions mainly relate to sales and customer service activities, market-ing, portfolio management and strategy.

17dear shareholders

manfred knapp Chief Financial Officer Born in 1955 in Frankfurt am Main, Germany. He holds a degree in Busi-ness Administration and Management. Before joining Deutsche Telekom Group in 1997, Manfred Knapp covered several senior controlling and finance management positions in different industries where he gained broad experience in all areas of finance management, mergers and acquisitions and turnaround management. In 1998, Manfred Knapp was assigned to the mobile operator Wind, in Italy, as Controlling Director. From 1999, he managed the controlling department of the Deutsche Telekom Carrier Services Business. In 2001, he joined Slovak Telekom as Controlling Director and Deputy CFO. Since May 2009, he has been responsible for the Finance Department of Crnogorski Telekom as CFO.

Vladimir beraToVićChief Corporate Affairs Officer

Born in 1970 in Podgorica, he graduated in international management, and is currently undertaking postgraduate studies. His 17-year-long ca-reer in telecommunications started in the Montenegrin mobile operator Promonte (today’s Telenor). During his last 10 years at Telenor, he held various directorial positions and was a member of the top-level manage-ment. He left Telenor as Chief Corporate Affairs Officer, in charge of government relations, legal, regulatory, interconnection and wholesale and corporate communication departments. His career at Crnogorski Telekom started in September 2010 as advisor to the Chairman of the Board. He was appointed Corporate Affairs Officer in November 2010. He currently holds the position of Chief Corporate Affairs Officer, which includes the wholesale area.

milija zekoVićChief Commercial Officer for Business Area

Born in 1971, he holds a degree in economics from the University of Montenegro. After completing his studies in 1995, he started his career at “Kartonka”, Podgorica as Production and Sales Manager. He started working as Sales Manager in T-Mobile (formerly Monet) in 2000. In 2006, he became the Director of Sales for residential customers and small and medium enterprises. In July 2008, he was appointed as the CSO of Crnogorski Telekom. He currently holds the position of Chief Commercial Officer for Business customers.

18

our Vision

In a fast changing world,we are your first choice to live in a fully digital lifestyle wherever you are, whatever you do; by aspiring to be the best in class.

our sTraTegy CT continues with the successful implementation of our corporative strategy based on three strategic layers: Broadband, Transformation and Innovation.

StAnd FoR bRoAdbAndIn order to offer unique customer experience of ultrafast internet and to keep our position of the technology leader, we continue with progres-sive migration of customers to the IMS platform, while at the same time improving the mobile network through 3G and 4G technologies and spreading the coverage of our fibre network. Our goal is to keep and to improve our competitive advantage in ADSL, Extra TV, Extra Trio and mobile internet and to respond effectively to the increasing demands of customers in terms of multimedia content and digital services.

19inTroduCTion

tRAnSFoRM to outpeRFoRMAt the centre of the transformation program is the process of developing a modern e-company with simplified internal operations for our employ-ees and establishing e-business operations, with more effective online channels and e-care services for our customers. Transformation initiatives and consolidation strategies should enable All-IP cost-effective network architecture, cost optimisation, service convergence, a multichannel business model and a faster and flexible Go-2-Market.

new wAy to plAyAs a result of increasing regulatory requirements and competitive pres-sure, we are facing a decline in revenues, particularly for traditional fixed and mobile services. Because of that we are intensively exploring new market possibilities and new business models. Through customised ICT and cloud solutions, CT meets the demands of modern businesses. Fur-ther extension of our content offer and interactivity features will ensure added value for evolving customer needs. Successful customer financing model enables further broadening of our business portfolio and opens up partnering possibilities.

21inTroduCTion

RegulAtoRy enviRonMent

The recent regulatory environment has been characterised by imple-mentation of the new Law on Electronic Communications based on the EU regulatory 2009 framework, which is dedicated to ensuring competi-tiveness in the market. In 2013, the new products placed in the market, based on the resolutions on SMP operators from 2010 and 2013, had still not been put into operation due to a lack of interest from other par-ties. The only interest was shown for duct rental. The Cost Accounting and Accounting Separation Methodology for the fixed network was implemented in 2012 and the National Regulatory Agency (NRA) approved the 2012 regulatory reports in September 2013. Additionally, the Cost Accounting and Accounting Separation Methodol-ogy was also applied in mobile and the first Mobile Regulatory revised reports (for 2012) were approved also in September 2013.

In 2012, the NRA completed second round of market analysis of seven standard EU relevant markets already analysed in 2010. CT was identi-fied as an SMP in all seven markets again. Additionally the NRA applied three criteria test on two retail markets: broadband and mobile service as to find out if those markets are susceptible for ex ante regulation. Retail market of mobile services was found sufficiently competitive, which was not the case with retail BB, where CT was designated as SMP. Upon approval of 2013 Regulatory reports for fixed network the NRA is going to enter in retail price regulation of BB service on cost orientation basis. Based on three SMP resolutions (from 2012 and 2013) the NRA entered, at the end of 2013, in retail price regulation of access to the fixed network, as well as fixed voice service (local, national and international calls). Price adjustment based on cost model implies price decrease in voice services.

Universal service

Universal service (US) was commercially launched in December 2011, but without significant interest from the customers’ side for the US service (especially for voice services and Internet access). Interest for US Inquiry and Directory Service is also not so remarkable; therefore Mon-tenegrin operators compensated a rather significant net cost to USO) for the years 2011 and 2012.

The Number Portability service was commercially launched on 1 De-cember 2011. The first years of implementation of the service showed that around 50% of numbers are ported in the CT network (while there was limited interest for porting numbers in the fixed-line segment). The new Rulebook on Number Portability adopted in 2013 provides for fewer restrictions for the porting of numbers.

Regulatory fees

Under the regulations currently in effect, Crnogorski Telekom pays fees for market supervision, numeration and the usage of radio frequencies.

Carrier Selection

Carrier Selection was already included in the Reference Interconnection Offer (RIO) published in 2008. In accordance with the NRA’s Resolution on Designating CT as an SMP in the relevant market, the updated RIO also includes Carrier Pre-selection. Only two operators have signed inter-connection agreements with Crnogorski Telekom with Carrier Selection included.

Sharing of infrastructure

The RIO also defines the terms and conditions of collocation, for the purpose of interconnection realised in Crnogorski Telekom’s premises. This includes renting of space in buildings, masts and ducts. The RIO’s conditions are valid only for operators looking for interconnection/ac-cess, while usage of infrastructure by operators for other purposes is subject to commercial negotiations. Apart from the RIO, the Reference Unbundling Offer defines the terms and conditions of collocation for the purpose of local loop unbundling, including also rental of collocation space in CT premises and ducts. Regulated prices for duct rental do not encourage investments in new duct deployment.

Termination of calls

The mobile termination rate (MTR) for voice traffic was decreased to 4 cents as of 1 January 2013, down from 7.06 cents in 2012. The decrease was based on the international benchmark results of the National Regu-latory Agency. Fixed termination rates did not change during 2013.

Future regulatory developments

In the process of implementation of the new Law on Electronic Commu-nications the NRA and the responsible ministry are supposed to adopt 45 bylaws by the end of August 2014. The bylaws will be subject to a public consultation process.

23inTroduCTion

promoTions and offersReSidentiAl cuStoMeRS

Postpaid The beginning of the year was marked by a campaign in which all new and existing customers had the possibility to buy a mobile device in instalments, along with three months free subscription. In Q1, CT introduced postpaid Duets, targeted at customers buying Smart pack-ages for two subscribers, with special benefits. Promotions continued in May, with a campaign offering three months free subscription to all new customers, accompanied by new smartphones on offer. In October 2013, CT introduced a new campaign offering additional benefits for all new customers. Benefits included free calls and SMSs, along with free internet for a three-month period.

PrepaidIn order to better match the needs of its younger customers, CT launched NRG, a new prepaid tariff. NRG is specifically designed to sat-isfy the needs of the young population and is offering relevant benefits: free internet, music streaming access and favourable SMS prices avail-able to the customer with each top-up. Mobile internet customers had access to the best offer on the market: an MI USB Stick, along with 10 GB of data for only €9.

Fixed telephonyIMS (IP Multimedia Subsystem) migration, a key technical transformation project, continued in 2013. The new system is based on IP protocols and will set the stage for the new generation of fixed services, with new functionalities for customers. At the end of 2013 48.000 customers had been migrated to the new system.

Extra TVExtra TV customers had an exciting year in 2013, with new promotions throughout the year, along with new product and content offers. Extra TV was available as a bundle with free minutes in the fixed network, enabling customers to call their loved ones for free during the promotion. The number of channels on Extra TV was increased significantly with inclusion of the new Pink package, with over 35 channels available to customers. A major new feature was TVTeka, enabling customers to ac-cess the previous 48 hours of the most popular channels as part of their regular subscription.

At the end of 2013, there were 61,800 customers, which is an increase of 5.5% compared to the previous year. The company maintained its leading position in the market with a market share of 41.6%.

ADSLStrong marketing campaigns marked the entire year helping to increase the ADSL customer base to 74,400 customers, which is an increase of 7% compared to the previous year base. As a result of the various marketing and promotional activities, CT holds a 81.8% market share in the broadband internet market.

Fibre to the home (FTTH) project Crnogorski Telekom continued its strong development of its fibre infra-structure resulting in utilisation reaching 25%. The number of customers of fibre networks doubled, increasing for 3,400 to almost 7,000 in 2013. In addition to the existing benefits available to fibre customers, such as very high internet speeds, the possibility of connecting up to five TV sets to the IPTV service, and a free additional phone line, fibre customers can now also enjoy full HD channels.

Sales of consumer goods

In 2013, Crnogorski Telekom continued the development and expan-sion of partnership with major retail chains. A wide portfolio of electronic consumer goods is offered.

Loyalty program

Premium program activities in 2013 were focused on expanding the number of partners and companies supporting the program. From initially 35 companies that gave discounts to Telekom customers, more than 70 companies were added to the list by December 2013. The total number of T-Cards issued at the end of 2013 was around 10,000.

24

buSineSS cuStoMeRS

Postpaid

The promotional offer for SMEs was launched in March 2013, in order to improve CT’s position in this segment. The offer consisted of three months free subscription for 24-month contracts, free-of-charge CUG calls, handsets purchased in instalments with internet options included in order to push data usage. In September, CT launched its ATL campaign with the main focus on the SME and SOHO segment with a postpaid offer as one of the main drivers for boosting revenues. Key elements were additional discounts for services bundled with HW in instalments. In order to push revenues and increase market share in SOHO segment, the “DoorToDoor” sales channel was introduced.

Roaming

In order to protect customers using services in roaming we continued with internet roaming cards for data usage throughout 2013. The number of activated daily and weekly roaming cards increased by 138% compared to 2012.

Convergent offers The Business Calculator as a promotional offer was continued during 2013. It presented CT as a full telecommunication provider for business customers by integrating all services and equipment into one offer with a shorter sale cycle. The campaign was accompanied by a web calcula-tor, a special web tool that enables customers to combine services and choose the best offer on their own.

The Business Summer Offer was launched in April 2013 and targets SMEs that are oriented towards summer-season business and have no need for internet connections for the entire year. It consists of fixed/mo-bile data services with a minimal contract duration of three months. Also, purchase of HW (TVs, laptops, mobile phones) in instalments was a part of the promotional offer.

Integris (ICT)

Integris continued its successful story during 2013. Great progress in the hotel/resort segment and retail area is helping us to achieve YoY revenue growth of more than 100%. In November 2013, CT signed the largest ICT contract, with the investor for the Hilton Hotel in Podgorica, the value of which is €1.4 million and will be implemented in the next two years. Also one of the important achievements is a pilot project with the Ministry of Justice for home detention monitoring which should be monetised in years to come.

25human resourCes

huMAn ReSouRceS

HR strategy development

In line with Crnogorski Telekom’s renewed corporate strategy and three-year-long business transformation, the HR Area decided to redefine its HR mission and strategic priorities. The ambition of the three-year-based HR strategy (2013–2016) is to align the organisation with new business challenges, to accelerate the changes in workforce alloca-tion, to strengthen the adaptability of business mindset and to create a performance-based culture. Consequently, the main HR focuses in 2013 have been the following: To fortify the strengths and competitive advantages of our human

resources Performance and leadership culture New training and development landscape A lean company – using simplicity, standardisation and lean manage-

ment principles to achieve MORE with LESS.

Survey management & employer positioning The most valuable outcome of the survey management in the last several years is a strong consequence management which implies different kinds of improvement measures. We are creating a liveable and likeable workplace, which is satisfactory for our employees and attractive to the labour market, continuously mak-ing efforts to be among the top three employers in Montenegro. Finally this has been proved by the outcomes of the second benchmark survey “The best company to work for in Montenegro” in 2013/2014, in which Crnogorski Telekom won three prizes:

Best Company to work for in Montenegro – main award The Most Attractive Employer – first place in the survey among uni-

versity students Special prize: Fair Play Award

Commitment to ONE Deutsche Telekom Europe (ONE DT EU) CT has actively used its employee survey results to leverage employee satisfaction, engagement, motivation, strategy awareness and com-mitment to ONE DT EU. According to Pulse Check in 2013, we have recorded the best results in the Group relating to: Collaboration – 80%; Heard about ONE DT/EU – 72%; Connected with DT Group – 67%.

Social dialogue & employee benefits Following the Agreement with the Trade Union, HR started to implement programs for resolving the housing needs of the employees. 148 em-ployees (20% of the overall number) gained the right to take out housing loans. Other benefits realised in cooperation with our social partners are numerous sport and recreation offers for employees; medical checkups for employees and their children including annual systematic checkups while advanced health insurance is under negotiation. Both the quality and quantity of extended offers of employee benefits in 2013 have been highly appreciated by our employees. Performance-based culture Following our intention to extend the Performance Management System, we made a decisive step ahead in 2013 in comparison with the previ-ous year (only 16% of employees, i.e. managers, were covered by the bonus system). By introducing the Employee Bonus Scheme and Shop Incentive Scheme, all employees of Crnogorski Telekom are covered by adequate financial motivation schemes. Finally, we created preconditions for performance-based remuneration for all employees in the company. Optimisation of training and development offer The leadership development programs offered through the Manage-ment Academy in 2013 were targeted at increasing knowledge and skills related to competence management and collaboration and at increasing the capabilities for self-driven development and self-assessment. Since the Employee Training Catalogue which was accepted extraordi-narily well – we have continued to meet the expectations and the needs of our employees related to project management, finance for non-finance, communication skills, time management, etc. In 2013, for the first time, HR introduced its Expert Excellence Program as the third pillar in the Training and Development Landscape. The Sales Academy which is entering the third year of its lifecycle is still supported to a high extent by HR.

Lean company

To support the implementation of leaner organisation and efficient business operations, HR has started to create a framework for further reduction of the complexity and pressure of work: regulation and process review, standardisation of HR processes, and primarily e-initiatives which enable provision of traditional HR services on-line. The E-HR Archive, the most strategic guided project, has been started up as an example of extraordinary cooperation with Magyar Telekom. The aim of the project is to automate and digitalise handling of paper-based documents prescribed by the law.To support and enhance the idea of simplicity in our day-to-day work, HR also developed a unique application (Leave Your Mark!) to collect the strategic-related ideas coming from employees. In this way HR has contributed to business transformation into an e-company.

27Corp. soCial responsibiliTy

coRpoRAte ReSponSibility

Corporate responsibility has been part of our corporate culture for many years; it involves and is an integral component of all our business activities. As one of the leading companies in the country, Crnogorski Telekom aims to be involved in all areas that are important to Montene-grin society. Besides striving to offer the most advanced telecommuni-cation services for our customers, we wish to actively contribute to the development of the community in which we do business and of which we are a part.

In April 2013 the Montenegrin Chamber of Commerce awarded Crnogo-rski Telekom the Annual Award for Social Responsibility in 2012.

At the traditional Iskra Annual Award Ceremony for Philanthropy in December 2013, Telekom received special recognition for corporate philanthropy. The Iskra Award Ceremony for Philanthropy is organised in cooperation with the Active Citizenship Fund, the Montenegrin Chamber of Commerce, the Ministry of Sustainable Growth and Tourism and the Diaspora Administration in the Ministry of Foreign Affairs and European Integration.

Telekom is a company that has always maintained a balance between economic and social goals while being accountable to the community and positioning itself in a socially responsible manner. The areas on which we are focusing are education, health and the environment, culture and community support.

Development of an information society in MontenegroBeing the leading broadband provider in the country, Crnogorski Tele-kom has the responsibility of being the country’s first partner on its way to becoming an information society.

For the seventh year in a row, Crnogorski Telekom is enabling free inter-net access via ADSL to all elementary and high schools in the country. During 2013, around 150 Montenegrin schools benefitted from this. The project was implemented together with the Ministry of Education and Science.

For two consecutive years, Telekom has supported the organisation of Hakaton, a competition for young developers. In 2013 the company supported the National Electronics Competition for high school students in Podgorica.

Sports, music and culture move people Our sponsoring platform focuses on sports, music and culture – which is perfect for underlining our brand promise “Life is for sharing” and giving a wide range of memorable moments to share.

Within the company’s sponsorship strategy, sports have a special place since this is an important area for developing a healthy, modern and ad-

vanced society. The company is the golden sponsor of the Montenegrin national football team and general sponsor of the Telekom Montenegrin Football First League. Additionally, in 2013 Telekom supported and sponsored Budućnost Basketball Club.

Regarding music as one of the main areas within the sponsorship strategy, as every year, we sponsored numerous musical events and activities, since music is considered to be the universal language for all generations. We partnered with organisations across Montenegro and supported the Asfaltiranje Hip-Hop Festival in Podgorica, the Southern Soul Festival in Ulcinj as well as the Sergej Ćetković concert tour.

In the field of culture, Crnogorski Telekom partnered with several organisations in order to support different projects, with the focus being on youth and education. The activities of these organisations were vital to the Montenegrin art scene.

In 2013, the company continued to support the City Theatre in Pod-gorica and thus was the sponsor of the theatre season 2013/2014. The company was also the sponsor of the Telekom Underhill Fest, an international documentary film festival which featured a series of concerts, film projects and lectures in Podgorica. Telekom supported the International TV Festival in Bar, the International Fashion Festival in Kotor, the International Puppetry Festival in Podgorica and the Durmitor Eko Festival in Žabljak.

Environment protection and energy efficiency In 2013, Crnogorski Telekom continued implementing a range of mea-sures to save energy and make their operations more energy-efficient. Energy consumption was reduced through a number of different mea-sures in the reporting period.

In March 2013, the company participated in the Earth Hour and Earth Day global campaigns with the aim of raising awareness about climate change issues. The company is constantly promoting usage of sustain-able solutions among its customers and employees, e.g. promoting e-mail bills, online registration, etc.

Crnogorski Telekom owns three base stations that use renewable energy sources. These are state-of-the art equipment that use the power of the sun and wind. The project is part of a broader company initiative to ad-dress global warming issues and protect the environment.

Community supportIn 2013 Telekom supported a number of NGOs and other organisations dealing with problems of socially vulnerable groups or promoting good causes and initiatives for society. Some of the main donations in 2013 were: donating two fully equipped vehicles to the Institute for Urgent Healthcare of Montenegro, donation of TV sets and free-of-charge IPTV subscription for kindergartens in cooperation with the NGO Roditelji, joining the fundraising campaign for the purchase of a mammography device for the public hospital in Cetinje, supporting the project for test-ing blood-sugar levels among kids in the elementary schools in several municipalities (in cooperation with the Association of Diabetes and Heart Disease patients), supporting the Food Bank of Montenegro initiatives, joining the campaign for early diagnosis and preventive examinations initiated by the Ministry of Health and supporting the national Breast Cancer Awareness Month Campaign in Montenegro.

28

This version of our report/ the accompanying documents is a translation from the original, which was prepared in Montenegrin. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version of our report takes precedence over this translation.

Crnogorski Telekom a.d. podgoriCaInternational Financial Reporting StandardsFinancial Statements For the year ended 31 December 2013

This version of our report/ the accompanying documents is a translation from the original, which was prepared in Montenegrin. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version of our report takes precedence over this translation.

30

This version of our report/ the accompanying documents is a translation from the original, which was prepared in Montenegrin. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version of our report takes precedence over this translation.

contentS

PageIndependent Auditor’s Report 29Statement of Financial Position 31Statement of Comprehensive Income 32Statement of Cash Flow 33Statement of Changes in Equity 34 Notes to the Financial Statements 35-85

31The finanCial year 2013

This version of our report/ the accompanying documents is a translation from the original, which was prepared in Montenegrin. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version of our report takes precedence over this translation.

sTaTemenT of finanCial posiTion

As atNotes 31. decembar 2013. 31. decembar 2012.

ASSETS Non current assets Property, plant and equipment 5 88,326,493 96,161,284Intangible assets 6 17,517,186 14,894,183Long term loans and other receivables 7 8,420,618 6,686,993 Total non current assets 114,264,297 117,742,460

Current assets Inventories 8 2,277,817 2,615,203Trade and other receivables 9 23,940,228 21,906,579Short term investments 10 54,000,000 32,000,000Cash and cash equivalents 11 3,684,312 26,438,865Total current assets 83,902,357 82,960,647Total assets 198,166,654 200,703,107

EQUITY AND LIABILITIESEquity and reserves attributable to the equity holders of the companyShare capital 13 140,996,394 140,996,394Retained earnings 24,823,321 28,878,790Total shareholders’ equity 165,819,715 169,875,184

LIABILITIESNon-current liabilitiesDeferred income tax liability 17 2,076,700 2,105,814Provision for liabilities and charges 16 757,642 635,382Total non-current liabilities 2,834,342 2,741,196Total liabilities 32,346,939 30,827,923

Current liabilities Trade and other payables 15 26,270,623 22,868,789Current income tax payable 2,315,364 2,615,564Provision for liabilities and charges 16 926,610 2,602,374Total current liabilities 29,512,597 28,086,727

Total equity and liabilities 198,166,654 200,703,107

The notes on pages 35 do 85 are an integral part of these financial statements.

These financial statements were authorised for issue by the Board of Directors of Crnogorski Telekom A.D. on April 19, 2014 and were signed on its behalf by

Ruediger Schulz Manfred KnappChief Executive Officer Chief Financial Officer

32

This version of our report/ the accompanying documents is a translation from the original, which was prepared in Montenegrin. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version of our report takes precedence over this translation.

sTaTemenT of ComprehesiVe inCome

For the year ended 31 DecemberNote 2013 2012

Revenue

Revenue from fixed lines and Internet 18 a 61,721,861 63,123,809 Revenue from mobile lines 18 b 47,227,529 50,953,125 Total revenue 108,949,390 114,076,934

Other operating income 19 1,241,336 249,665

Operating expensesEmployee related expenses 20 (22,671,829) (20,674,655)Depreciation, amortization and impairment 21 (19,491,584) (21,432,308)Payments to other network operators 22 (14,972,947) (18,237,414)Cost of equipment sold (6,779,225) (5,784,610)Other operating expenses 23 (26,136,462) (27,097,037)Total operating expenses (90,052,047) (93,226,024)

Operating profit 20,138,679 21,100,575

Finance income 24 1,290,640 2,855,494Finance costs 24 (298,536) (845,260)Finance income – net 992,104 2,010,234

Profit before income tax 21,130,783 23,110,809

Income tax expense 25 (2,286,252) (3,170,805)

Profit for the year 18,844,531 19,940,004

Other comprehensive income for the year - -Total comprehensive income for the year 18,844,531 19,940,004

Attributable to:

Equity holders of the company 18,844,531 19,940,004

Earnings per share of the Company during the year (expressed in EUR per share)

- basic and diluted 26 0.40 0.42

The notes on pages 35 do 85 are an integral part of these financial statements.

33The finanCial year 2013

This version of our report/ the accompanying documents is a translation from the original, which was prepared in Montenegrin. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version of our report takes precedence over this translation.

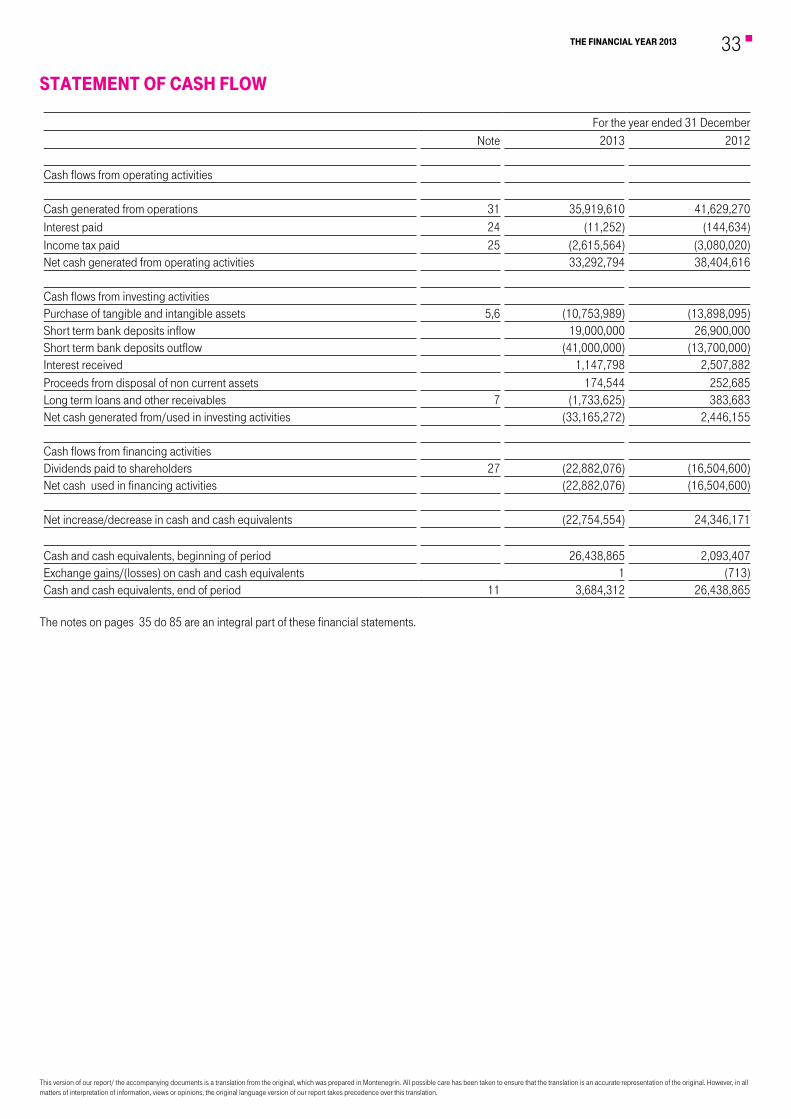

sTaTemenT of Cash floW

For the year ended 31 DecemberNote 2013 2012

Cash flows from operating activities

Cash generated from operations 31 35,919,610 41,629,270Interest paid 24 (11,252) (144,634)Income tax paid 25 (2,615,564) (3,080,020)Net cash generated from operating activities 33,292,794 38,404,616

Cash flows from investing activitiesPurchase of tangible and intangible assets 5,6 (10,753,989) (13,898,095)Short term bank deposits inflow 19,000,000 26,900,000Short term bank deposits outflow (41,000,000) (13,700,000)Interest received 1,147,798 2,507,882Proceeds from disposal of non current assets 174,544 252,685Long term loans and other receivables 7 (1,733,625) 383,683Net cash generated from/used in investing activities (33,165,272) 2,446,155

Cash flows from financing activitiesDividends paid to shareholders 27 (22,882,076) (16,504,600)Net cash used in financing activities (22,882,076) (16,504,600)

Net increase/decrease in cash and cash equivalents (22,754,554) 24,346,171

Cash and cash equivalents, beginning of period 26,438,865 2,093,407Exchange gains/(losses) on cash and cash equivalents 1 (713)Cash and cash equivalents, end of period 11 3,684,312 26,438,865

The notes on pages 35 do 85 are an integral part of these financial statements.

34

This version of our report/ the accompanying documents is a translation from the original, which was prepared in Montenegrin. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version of our report takes precedence over this translation.

sTaTemenT of Changes in eQuiTy

Share Capital Statutory reserves Retained earnings Total

Balance at January 1, 2012 140,996,394 8,046,359 17,392,427 166,435,180

Dividends - - (16,500,000) (16,500,000)

Allocation of statutory reserves (Note 14) - (8,046,359) 8,046,359 -

Profit for the year - - 19,940,004 19,940,004

Other comprehensive income for the year - - - -

Balance at December 31, 2012 140,996,394 - 28,878,790 169,875,184

Balance at January 1, 2013 140,996,394 - 28,878,790 169,875,184Dividends (Note 27) - (22,900,000) (22,900,000)Profit for the year - 18,844,531 18,844,531Other comprehensive income for the year - - -

Balance at December 31, 2013 140,996,394 - 24,823,321 165,819,715

The notes on pages 35 do 85 are an integral part of these financial statements.

35The finanCial year 2013

This version of our report/ the accompanying documents is a translation from the original, which was prepared in Montenegrin. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version of our report takes precedence over this translation.

1. general informaTion

Crnogorski Telekom A.D. Podgorica (also referred to as “Telekom” or the “Company”) is a principal provider of fixed telephony services in Montene-gro, as well as of local, national and international telephony services, in addition to a wide range of other telecommunication services involving mobile network, internet, leased circuits, data networks, cable television services and other telecommunication services in Montenegro.

The Company is a shareholding company listed on the Montenegro Stock Exchange (TECG). The Company was acquired in 2005 by Magyar Telekom Nyrt. (hereinafter referred to as “Magyar Telekom”) with 76.53% of ownership interest. On April 30, 2009, the General Assembly of Crnogorski Tele-kom A.D decided to merge T Mobile d.o.o. and Internet Crna Gora d.o.o., into Crnogorski Telekom A.D..

Deutsche Telekom AG (“DTAG”) is the ultimate controlling owner of Magyar Telekom Plc. holding 59.21% of the issued shares. Deutsche Telekom (“DT”) Group has a number of fixed lines, mobile and IT service provider subsidiaries worldwide, with whom Magyar Telekom Group has regular transactions.

Telekom is domiciled in Montenegro at the following address: Moskovska 29, Podgorica. As at December 31, 2013 the Company had 687 employees (774 employees as at 31 December 2012).

Investigation into certain consultancy contracts

As previously disclosed, in the course of conducting their audit of Magyar Telekom’s 2005 financial statements, PricewaterhouseCoopers Könyv-vizsgáló és Gazdasági Tanácsadó Kft. (“PwC”) identified two contracts the nature and business purposes of which were not readily apparent to them. In February 2006, Magyar Telekom’s Audit Committee retained White & Case LLP (the “independent investigators” or “White & Case”), as its independent legal counsel, to conduct an internal investigation into whether Magyar Telekom and/or any of its affiliates had made payments under those, or other contracts, potentially prohibited by U.S. laws or regulations, including the Foreign Corrupt Practices Act (“FCPA”), or internal company policy. The Audit Committee also informed the U.S. Department of Justice (“DOJ”) and the U.S. Securities and Exchange Commission (“SEC”), and the Hungarian Financial Supervisory Authority of the internal investigation.

On December 2, 2009, the Audit Committee provided Magyar Telekom’s Board of Directors with a “Report of Investigation to the Audit Committee of Magyar Telekom Nyrt.” dated November 30, 2009 (the “Final Report”). The Audit Committee indicated that it considers that, with the delivery of the Final Report based on currently available facts, White & Case has completed its independent internal investigation.

36

This version of our report/ the accompanying documents is a translation from the original, which was prepared in Montenegrin. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version of our report takes precedence over this translation.

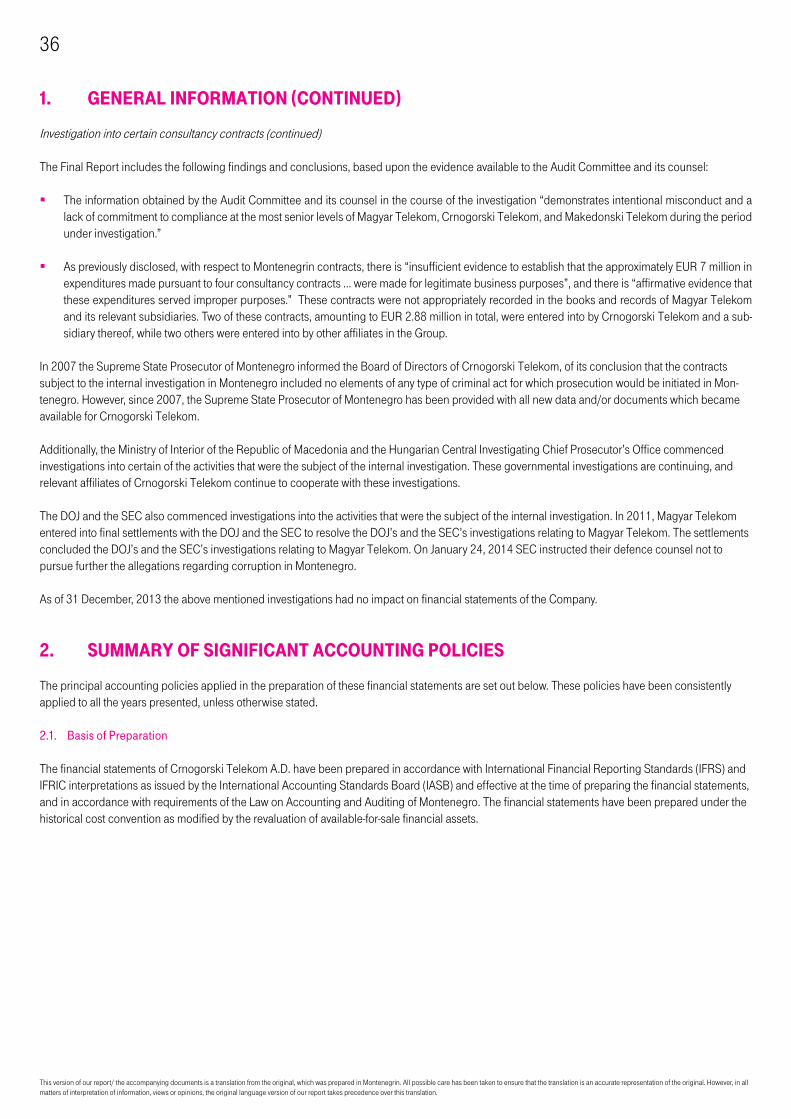

1. general informaTion (ConTinued)

Investigation into certain consultancy contracts (continued)

The Final Report includes the following findings and conclusions, based upon the evidence available to the Audit Committee and its counsel:

The information obtained by the Audit Committee and its counsel in the course of the investigation “demonstrates intentional misconduct and a lack of commitment to compliance at the most senior levels of Magyar Telekom, Crnogorski Telekom, and Makedonski Telekom during the period under investigation.”

As previously disclosed, with respect to Montenegrin contracts, there is “insufficient evidence to establish that the approximately EUR 7 million in expenditures made pursuant to four consultancy contracts ... were made for legitimate business purposes”, and there is “affirmative evidence that these expenditures served improper purposes.” These contracts were not appropriately recorded in the books and records of Magyar Telekom and its relevant subsidiaries. Two of these contracts, amounting to EUR 2.88 million in total, were entered into by Crnogorski Telekom and a sub-sidiary thereof, while two others were entered into by other affiliates in the Group.

In 2007 the Supreme State Prosecutor of Montenegro informed the Board of Directors of Crnogorski Telekom, of its conclusion that the contracts subject to the internal investigation in Montenegro included no elements of any type of criminal act for which prosecution would be initiated in Mon-tenegro. However, since 2007, the Supreme State Prosecutor of Montenegro has been provided with all new data and/or documents which became available for Crnogorski Telekom.

Additionally, the Ministry of Interior of the Republic of Macedonia and the Hungarian Central Investigating Chief Prosecutor’s Office commenced investigations into certain of the activities that were the subject of the internal investigation. These governmental investigations are continuing, and relevant affiliates of Crnogorski Telekom continue to cooperate with these investigations.

The DOJ and the SEC also commenced investigations into the activities that were the subject of the internal investigation. In 2011, Magyar Telekom entered into final settlements with the DOJ and the SEC to resolve the DOJ’s and the SEC’s investigations relating to Magyar Telekom. The settlements concluded the DOJ’s and the SEC’s investigations relating to Magyar Telekom. On January 24, 2014 SEC instructed their defence counsel not to pursue further the allegations regarding corruption in Montenegro.

As of 31 December, 2013 the above mentioned investigations had no impact on financial statements of the Company.

2. summary of signifiCanT aCCounTing poliCies

The principal accounting policies applied in the preparation of these financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated.

2.1. Basis of Preparation

The financial statements of Crnogorski Telekom A.D. have been prepared in accordance with International Financial Reporting Standards (IFRS) and IFRIC interpretations as issued by the International Accounting Standards Board (IASB) and effective at the time of preparing the financial statements, and in accordance with requirements of the Law on Accounting and Auditing of Montenegro. The financial statements have been prepared under the historical cost convention as modified by the revaluation of available-for-sale financial assets.

37The finanCial year 2013

This version of our report/ the accompanying documents is a translation from the original, which was prepared in Montenegrin. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version of our report takes precedence over this translation.

2. summary of signifiCanT aCCounTing poliCies (ConTinued)

2.1. Basis of Preparation (continued)

The preparation of financial statements in conformity with IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the Company’s accounting policies. The areas involving a higher degree of judgement or com-plexity, or areas where assumptions and estimates are significant to the financial statements are disclosed in note 4.

The Company maintains its accounting records in accordance with the Accounting and Auditing Law of Montenegro (“Official Gazette of the Republic of Montenegro”, No. 69/2005 and “Official Gazette of Montenegro”, no. 80/08 and 32/11) and in particular, based on the relevant legal decision defining the mandatory application of IFRS in the Republic of Montenegro (“Official Gazette of the Republic of Montenegro”, No. 69/2002).