CROSS BORDER TAXATION OF ENTERTAINERS AND SPORTSMEN NATIONAL WORKSHOP ON MEDIA AND ENTERTAINMENT BY AND ENTERTAINMENT BY COMMITTEE FOR MEMBERS IN INDUSTRY OF ICAI, WIRC MUMBAI 2 JUNE 2012 Isha Sekhri

Transcript

CROSS BORDER TAXATION OF

ENTERTAINERS AND SPORTSMEN

NATIONAL WORKSHOP ON MEDIA

AND ENTERTAINMENT BY AND ENTERTAINMENT BY

COMMITTEE FOR MEMBERS IN

INDUSTRY OF ICAI, WIRC

MUMBAI

2 JUNE 2012

Isha Sekhri

2

� Taxation of Resident

Entertainers and

Sportsmen outside India

Road Map

Cross Border Taxation of Entertainers and Sportsmen

� Taxation of Non-Resident

Entertainers and

Sportsmen in India

Resident Entertainers and Sportsmen

Performance outside India3

Cross Border Taxation of Entertainers and Sportsmen

Resident Entertainers and Sportsmen

performing outside India

� A large number of Bollywood and Tollywood Films are shot outside India

� Live concerts by Resident Entertainers outside India (recently Indian Singer, Sonu

Nigam, performed at Sydney)

� Sports - Cricket, Football, Hockey matches played around the globe

� Earlier, ‘Artist’ was used to denote Performers (does not include Painters, Sculptors)

Term “Entertainer” different from “Artiste” - Not defined in the Act

4

� Term “Entertainer” different from “Artiste” - Not defined in the Act

� New Genre of Individuals, “Entertainers”, who may or may not act

� Common parlance, “Entertainer” means:

� One who amuses people, such as a singer, dancer, comedian, magician, etc., especially

one who does so as a profession

� One who entertains; a host

� Entertain - To engage the attention of agreeably; to amuse with that which makes the time

pass pleasantly; to divert; as, to entertain friends with conversation, etc

� Article 17 and amendment to Section 115BBA as “Entertainers” in India

Cross Border Taxation of Entertainers and Sportsmen

Judicial Precedents on Section 80RR -

Artist, Actor, Entertainer

� Amitabh Bachchan vs DCIT (106 TTJ 925) - In the context of erstwhile Section

80RR, ( which provided a deduction to income of artists, actors etc earned in

foreign exchange), on whether Mr. Amitabh Bachchan’s performance in KBC

was as an “Actor” - Held “Yes” by Mumbai Tribunal, stating:“The various meanings assigned to the term ‘artist’ by different standard dictionaries clearly show

that the term "artist" is a term which has a wide meaning not merely restricted to the meaning of

fine arts but encompasses within its scope, a skilled performer.”

5

fine arts but encompasses within its scope, a skilled performer.”

� Similar issue, Mr. Sachin Tendulkar’s argument upheld that he was an “Actor”

while appearing in commercials (2011-TIOL-327-ITAT-MUM).

� CIT vs Tarun R Tahiliani (2010-TIOL-446-HC-MUM-IT) : A Designer was held to

be an “Artist”

� Harsha Bhogle vs ITO (2003-TIOL-46-ITAT-MUM) : A presenter, commentator

and programme compere of sports on television was held to be not an “artist”

Cross Border Taxation of Entertainers and Sportsmen

Judicial Precedents - Artist, Actor,

Entertainer

� Canadian Case Law - Cheek vs the Queen: The Court has provided detailed reasoning why a

radio broadcaster cannot be considered as a ‘radio artiste’ as per 1980 US-Canada Tax

Treaty stating:

“…It is obvious that athletes and sportsmen "perform" in their chosen athletic avocation; and their

performance is inherently entertaining. The fans who turn on the radio to hear a particular

Baseball game want to know how the team is performing on the field. While he may be able to

hold the attention and interest of the fans with his "down time" commentary but he is not the

6

hold the attention and interest of the fans with his "down time" commentary but he is not the

reason why the fan turns on the radio.”

� Pilcom vs Income-tax Officer (2003-TII-86-ITAT-KOL-INTL) : Held that the players of the

cricket associations of the participating countries in the World Cup Cricket Tournament,

1996, should be considered as Entertainers.

� Issue : Whether the IPL can be considered has having more entertainment value than actually

being a sport? Artificially crafted teams and not all the players of Mumbai Indians are

actually from Mumbai? Rajasthan Royals? CSK?

� Article 17 of OECD Model Convention, various tax treaties and Section115BBA of the Act

apply in equal measure to both Sportspersons and Entertainers

Cross Border Taxation of Entertainers and Sportsmen

Taxability of Resident Entertainers and

Sportsmen performing outside India

� Article 17 of Tax Treaties and OECD Model Tax Convention

� Main reason for this special treatment is that top artistes and sportsmen are very mobile and

can easily move their residency to a tax havens, which levies no income tax. The OECD

believes that without Art. 17 (and the taxing right for the source country) these top artistes

and sportsmen would escape from taxation under Art. 7

“1. Notwithstanding the provisions of Articles 7 and 15, income derived by a resident of a

Contracting State as an entertainer, such as a theatre, motion picture, radio or television artiste,

7

Contracting State as an entertainer, such as a theatre, motion picture, radio or television artiste,

or a musician, or as a sportsman, from his personal activities as such exercised in the other

Contracting State, may be taxed in that other State.

2. Where income in respect of personal activities exercised by an entertainer or a sportsman in his

capacity as such accrues not to the entertainer or sportsman himself but to another person, that

income may, notwithstanding the provisions of Articles 7 and 15, be taxed in the Contracting

State in which the activities of the entertainer or sportsman are exercised.”

� Discussion draft on Article 17 Revised Commentary(issued for public comments in April 2010)

(changes proposed in red) - Recommended to substitute the term “Artiste” with the term

“Entertainer” and the term “Appearances” with “Performances”

Cross Border Taxation of Entertainers and Sportsmen

Preliminary Conditions

� Income derived from personal activities would be taxable in Country of

Performance (‘Country P’) irrespective of number of days stay in Country P.

Conditions for applicability:

� Resident of one of the contracting states (‘Country R’);

� From Performance of Personal Activities in Country P.

� As per the thesis of Mr. Milan Matijevic, set of criteria:

8

� As per the thesis of Mr. Milan Matijevic, set of criteria:

� Must be a performance;

� Performance should be in public, i.e. directly before an audience or recorded and

later reproduced for an audience;

� Predominant element of the performance must be artistic and entertaining (level is

irrelevant);

� Performer by himself / herself should be the direct or indirect reason why the

audience is listening to or watching the performance.

Cross Border Taxation of Entertainers and Sportsmen

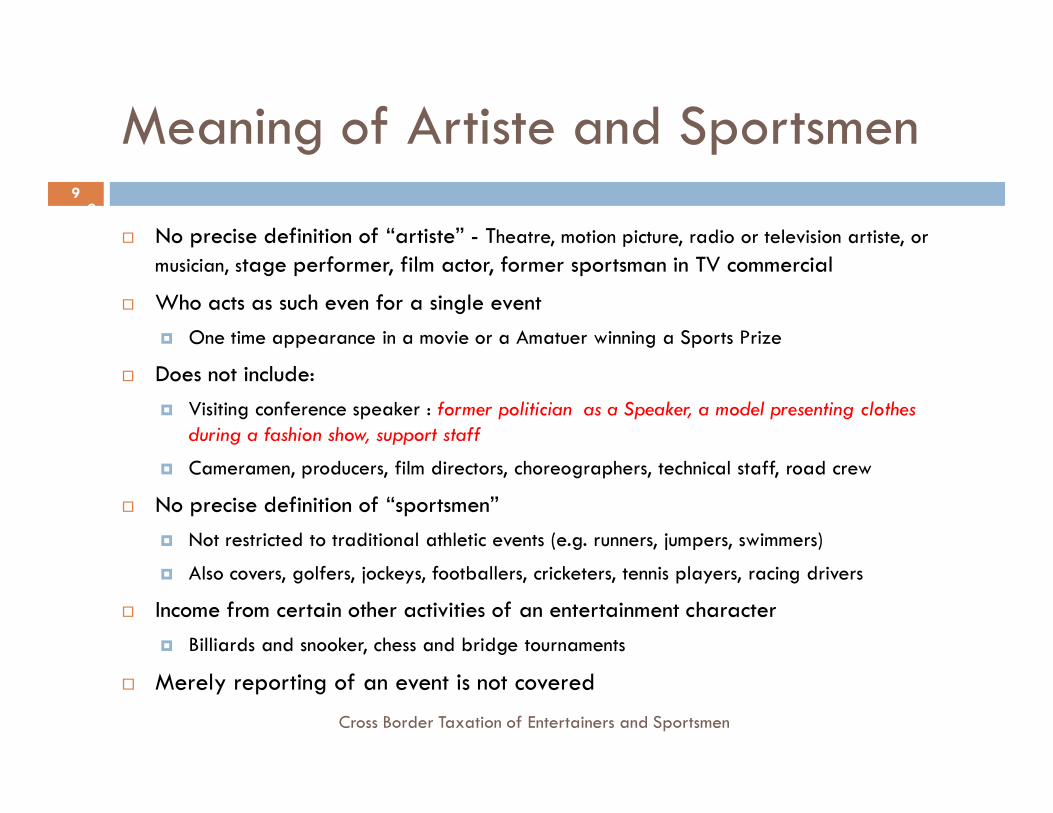

Meaning of Artiste and Sportsmen

� No precise definition of “artiste” - Theatre, motion picture, radio or television artiste, or

musician, stage performer, film actor, former sportsman in TV commercial

� Who acts as such even for a single event

� One time appearance in a movie or a Amatuer winning a Sports Prize

� Does not include:

� Visiting conference speaker : former politician as a Speaker, a model presenting clothes

9

9

� Visiting conference speaker : former politician as a Speaker, a model presenting clothes

during a fashion show, support staff

� Cameramen, producers, film directors, choreographers, technical staff, road crew

� No precise definition of “sportsmen”

� Not restricted to traditional athletic events (e.g. runners, jumpers, swimmers)

� Also covers, golfers, jockeys, footballers, cricketers, tennis players, racing drivers

� Income from certain other activities of an entertainment character

� Billiards and snooker, chess and bridge tournaments

� Merely reporting of an event is not covered

Cross Border Taxation of Entertainers and Sportsmen

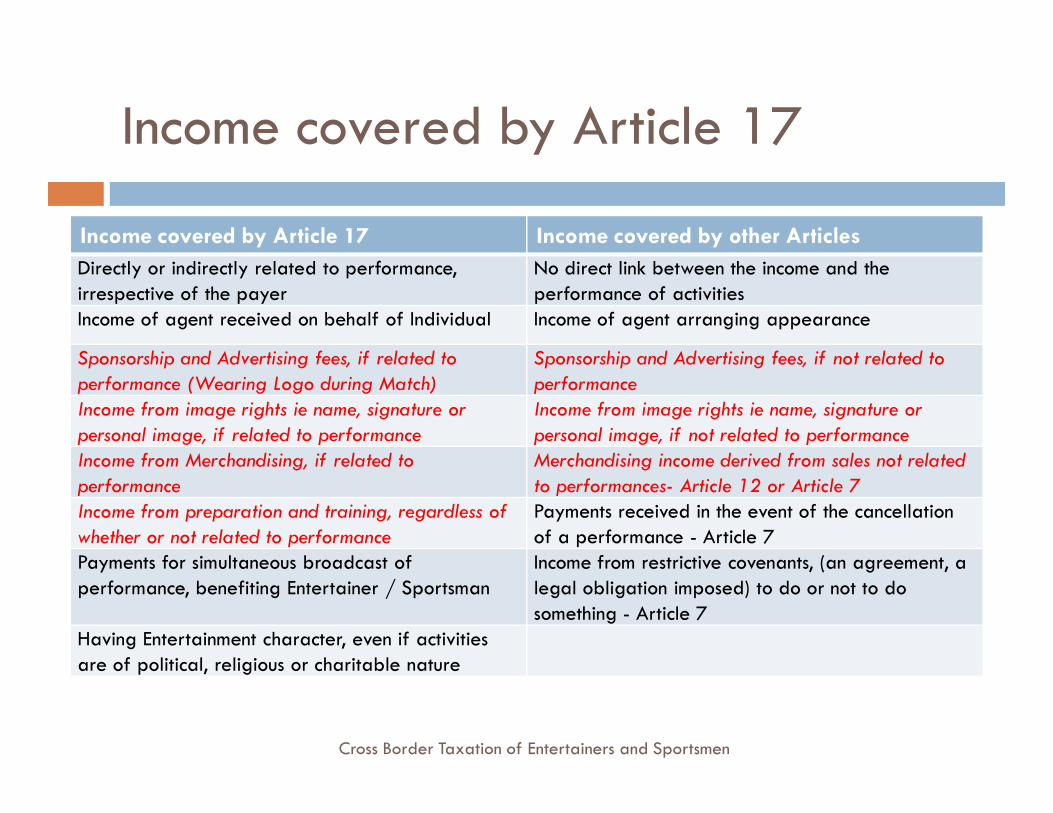

Income covered by Article 17

Income covered by Article 17 Income covered by other Articles

Directly or indirectly related to performance,

irrespective of the payer

No direct link between the income and the

performance of activities

Income of agent received on behalf of Individual Income of agent arranging appearance

Sponsorship and Advertising fees, if related to

performance (Wearing Logo during Match)

Sponsorship and Advertising fees, if not related to

performance

Income from image rights ie name, signature or Income from image rights ie name, signature or Income from image rights ie name, signature or

personal image, if related to performance

Income from image rights ie name, signature or

personal image, if not related to performance

Income from Merchandising, if related to

performance

Merchandising income derived from sales not related

to performances- Article 12 or Article 7

Income from preparation and training, regardless of

whether or not related to performance

Payments received in the event of the cancellation

of a performance - Article 7

Payments for simultaneous broadcast of

performance, benefiting Entertainer / Sportsman

Income from restrictive covenants, (an agreement, a

legal obligation imposed) to do or not to do

something - Article 7

Having Entertainment character, even if activities

are of political, religious or charitable nature

Cross Border Taxation of Entertainers and Sportsmen

Other provisions

� Dual Role : Mr. Subhash Ghai - appearance in most of his movies

� Actual nature of activities

� Activities predominantly of performing nature, apply to all resulting income

� Performing element is a negligible part, whole income will fall outside the Article

� In other cases ,an apportionment should be necessary

� Applicable regardless of the Payer

11

� Applicable regardless of the Payer

� Performance as an Employee of the Company, receiving annual salary

� Country P entitled to tax proportionate salary corresponding to the performance

� Member of orchestra paid salary and not payment for each separate performance

� Tax proportion of musician's salary which corresponds to performance

� Employed by one person company, Country P may tax proportionate remuneration

� Domestic laws “look through” entities and treat income accruing to individual: Country P

can tax income accruing in the entity for individual's benefit, even if not actually paid

as remuneration to the individual (eg Brad Pitt’s company receiving income for his benefit)

Cross Border Taxation of Entertainers and Sportsmen

Examples

� A cyclist employed by a Team, required to travel with the team, appear in public press

conferences , participate in training activities and races in different countries. Paid

fixed annual salary plus bonuses based on race results.

� Allocate the salary based on number of working days during which he is present in each State

performing employment-related activities (e.g. travel, training, races, public appearances)

and allocate bonuses to where the relevant races took place.

Organiser of a football tournament holds all IPR in the event and receives payments

12

� Organiser of a football tournament holds all IPR in the event and receives payments

for broadcasting rights - Article 17 is not applicable to income and also to any share

of these payments distributed to participating teams. Depending on legal nature, may

constitute royalties covered by Article 12.

� Indian Cricket Team goes to Australia to play a series and fly in 3 weeks in

advance to practice on the ground- Taxability of income from practice sessions?

� It will be appropriate to allocate that salary or remuneration on the basis of the

working days spent in each State in which the entertainer or sportsman has been

required, under his employment contract, to perform these activities

Cross Border Taxation of Entertainers and Sportsmen

Computation of Income

� Computation of Income under Article 17

� Article does not provide for Computation of income

� Country P’s domestic law - deductions for expenses

� Domestic laws differ - Taxation at source, gross based taxation, low rate

13

Cross Border Taxation of Entertainers and Sportsmen

Income accruing to other persons

� Income accrues to another person and Country P does not look through the person

receiving the income to tax it as income of the Individual, as per Paragraph 2,

portion of income which cannot be taxed in the hands of the Individual, may be

taxed in the hands of the other person receiving it

� Business Income may be taxable even in the absence of a PE in Country P

� Three situations:

14

� Management company receives income for appearance of a group (not constituted as a

legal entity)

� Team, team, troupe, orchestra, etc., constituted as a legal entity

� Income for performances may be paid to entity

� Individual members liable to tax under Paragraph 1

� Profit element of legal entity under Paragraph 2

� Entertainer / Sportsman Company (Neither as personal activities or business income)

� Taxable under Paragraph 2 (Individual and Star Company may be residents of different States)

� If Country P Looks Through, taxable under Paragraph 1

Cross Border Taxation of Entertainers and Sportsmen

Article 17(2)

� Article 17(2) not applicable :

� Prize money of owner of horse or race car since not related to personal activities of the

jockey or race car driver

� Income of enterprises involved in production of entertainment or sports events.

� Income of independent promoter of concert from sale of tickets and allocation of advertising space

� Same income should not be taxed twice through application of these two paragraphs

15

Same income should not be taxed twice through application of these two paragraphs

� Paragraph 2 : Star-company on payment with respect to activities performed by the

Individual; and

� Paragraph 1 : Part of remuneration paid by Company to the Individual, attributed to

activities.

� Depending on domestic law of Country P, tax only the company or Individual on the whole

income attributable to activities or tax each of them on part of the income, e.g. by taxing the

income received by the company but allowing a deduction for the relevant part of the

remuneration paid to the Individual and taxing that part in the hands of the Individual

Cross Border Taxation of Entertainers and Sportsmen

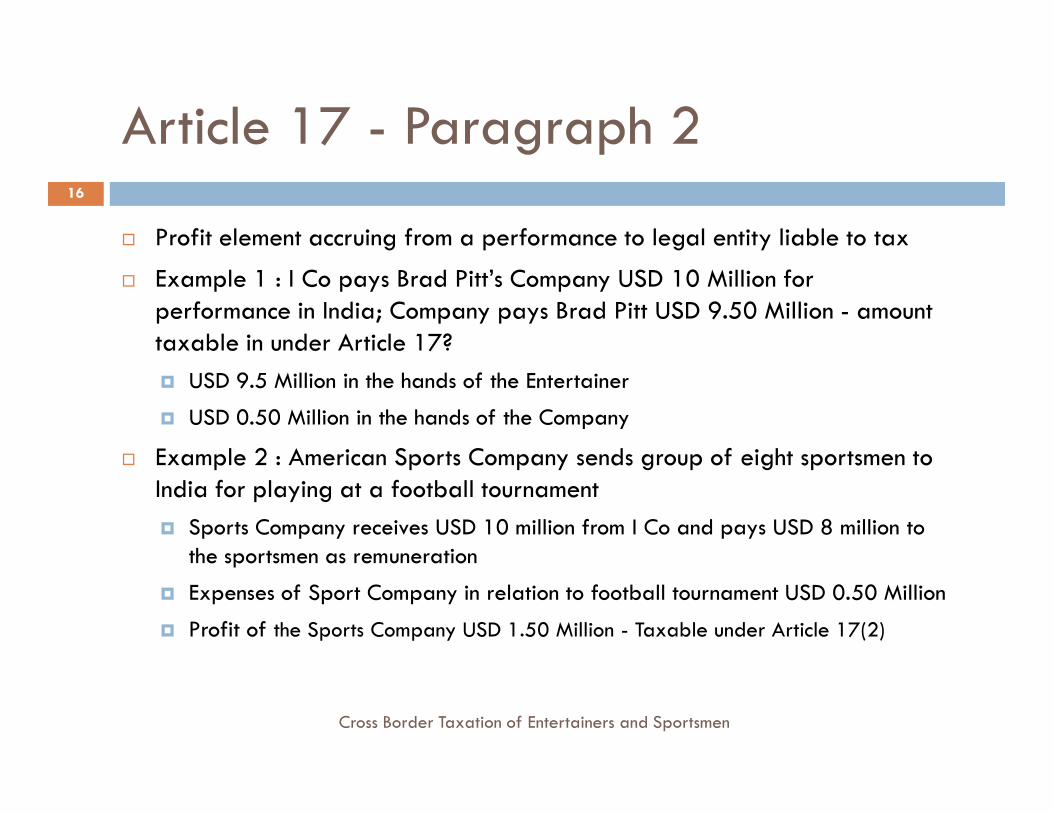

Article 17 - Paragraph 2

� Profit element accruing from a performance to legal entity liable to tax

� Example 1 : I Co pays Brad Pitt’s Company USD 10 Million for

performance in India; Company pays Brad Pitt USD 9.50 Million - amount

taxable in under Article 17?

� USD 9.5 Million in the hands of the Entertainer

USD 0.50 Million in the hands of the Company

16

� USD 0.50 Million in the hands of the Company

� Example 2 : American Sports Company sends group of eight sportsmen to

India for playing at a football tournament

� Sports Company receives USD 10 million from I Co and pays USD 8 million to

the sportsmen as remuneration

� Expenses of Sport Company in relation to football tournament USD 0.50 Million

� Profit of the Sports Company USD 1.50 Million - Taxable under Article 17(2)

Cross Border Taxation of Entertainers and Sportsmen

Article 17(2)

� Peculiar India-Australia Treaty

� Australian Cricketer’s Management Company receives the income on his behalf

� Article 17(2) gives the impression that Management Companies of only

Entertainers are covered ie Management Companies of Sportsmen may not

covered by Article 17(2) and hence not taxable

“ARTICLE XVII - Entertainers - 1. Notwithstanding the provisions of Articles 14 and 15,

17

“ARTICLE XVII - Entertainers - 1. Notwithstanding the provisions of Articles 14 and 15,

income derived by residents of one of the Contracting States as entertainers, such as

theatre, motion picture, radio or television artists, musicians and athletes, from their

personal activities as such exercised in the other Contracting State, may be taxed in

that other State.

2. Where income in respect of the personal activities of an entertainer as such accrues

not to that entertainer but to another person, that income may, notwithstanding the

provisions of Articles 7, 14 and 15, be taxed in the Contracting State in which the

activities of the entertainer are exercised

Cross Border Taxation of Entertainers and Sportsmen

Non-Resident Entertainers and Sportsmen

Performance in India18

Cross Border Taxation of Entertainers and Sportsmen

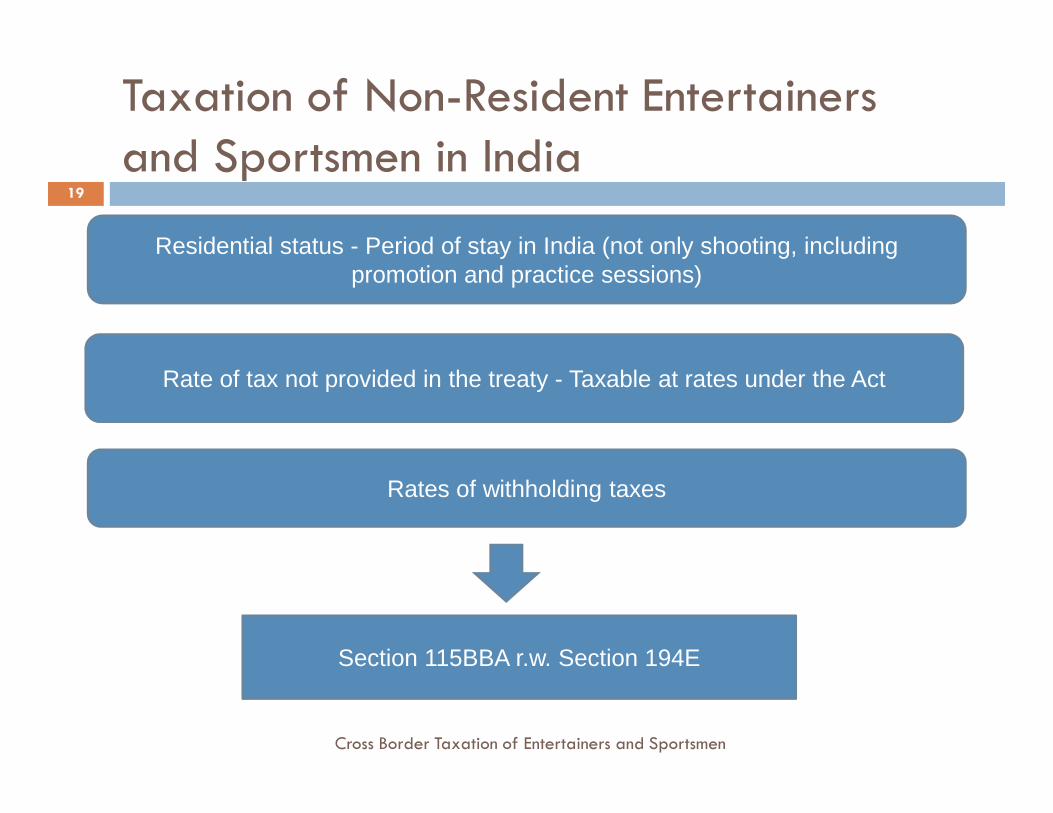

19

Residential status - Period of stay in India (not only shooting, including promotion and practice sessions)

Taxation of Non-Resident Entertainers

and Sportsmen in India

Rate of tax not provided in the treaty - Taxable at rates under the Act

Cross Border Taxation of Entertainers and Sportsmen

Rates of withholding taxes

Section 115BBA r.w. Section 194E

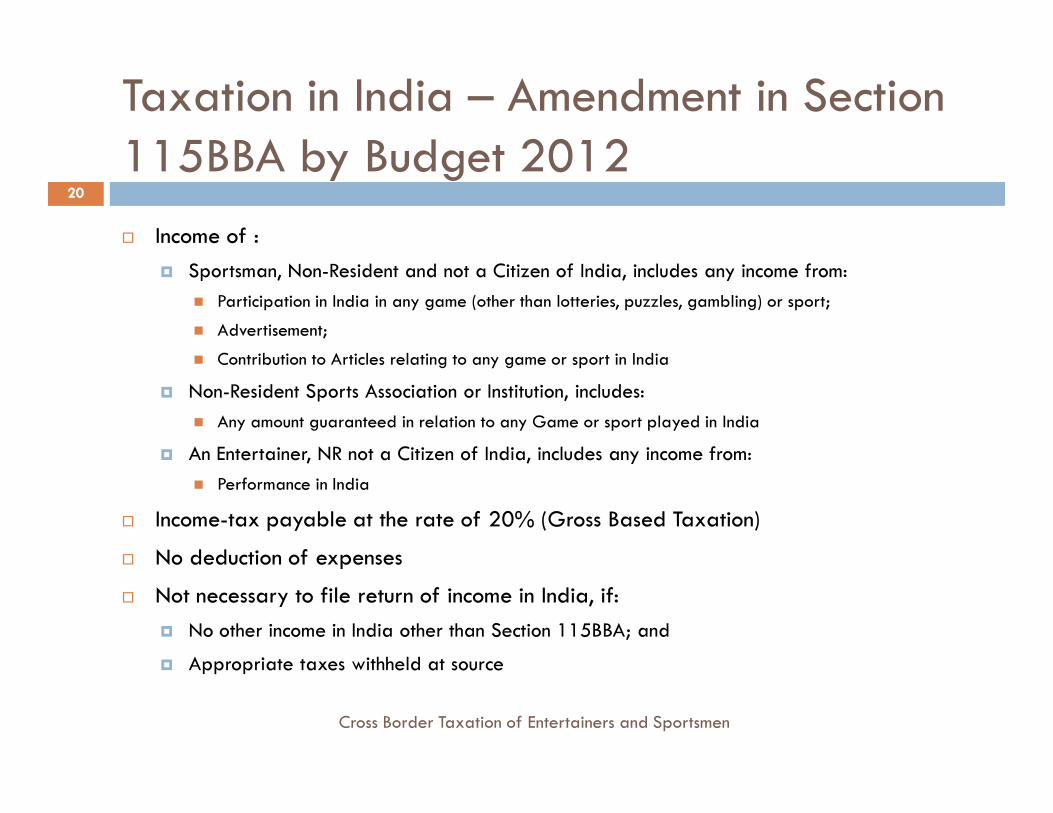

Taxation in India – Amendment in Section

115BBA by Budget 201220

� Income of :

� Sportsman, Non-Resident and not a Citizen of India, includes any income from:

� Participation in India in any game (other than lotteries, puzzles, gambling) or sport;

� Advertisement;

� Contribution to Articles relating to any game or sport in India

� Non-Resident Sports Association or Institution, includes:

Cross Border Taxation of Entertainers and Sportsmen

� Any amount guaranteed in relation to any Game or sport played in India

� An Entertainer, NR not a Citizen of India, includes any income from:

� Performance in India

� Income-tax payable at the rate of 20% (Gross Based Taxation)

� No deduction of expenses

� Not necessary to file return of income in India, if:

� No other income in India other than Section 115BBA; and

� Appropriate taxes withheld at source

Amendment Impact

21

� Does not cover cases of when income accrues to a person other than the

Entertainer / Sportsman as per Article 17(2)

� Continue to be taxed as per normal income tax provisions

� Withholding taxes - Section 194E

� With respect to Income specified in Section 115BBA, taxes to be withheld at the rate

of 20%

Cross Border Taxation of Entertainers and Sportsmen

of 20%

� Section 115BBA applicable from 1 April 2012

� Section 194E applicable from 1 July 2012

� Withholding taxes in the interim for one month

� Better view at the rate of 20%

Circular 787 dated 10.02.2000

Scenario Taxability

i. If the artist performs in India gratuitously, without any

consideration, or performs in India to promote sale of his records

but no consideration is paid for the performances by anyone.

ii. Consideration received by artist for live performance and/or

simultaneous live telecast or broadcast in India.

iii. Consideration received to acquire copyrights of performance in

No Tax

Taxable in India / Article

17

22

iii. Consideration received to acquire copyrights of performance in

India for subsequent sale abroad (of records, CDs etc) or

consideration to acquire license for broadcast or telecast

overseas.

iv. Consideration to acquire copyright of performance in India for

subsequent sale in India or consideration to acquire license for

broadcast or telecast in India.

v. Endorsement fees which relates to artist’s performance in India.

Not taxable in India u/s.

9(1)(vi)

Taxable in India u/s. 9(1)(vi)

/ Article 12 - Royalties

Taxable in India u/s. 5 /

Article 17

Cross Border Taxation of Entertainers and Sportsmen

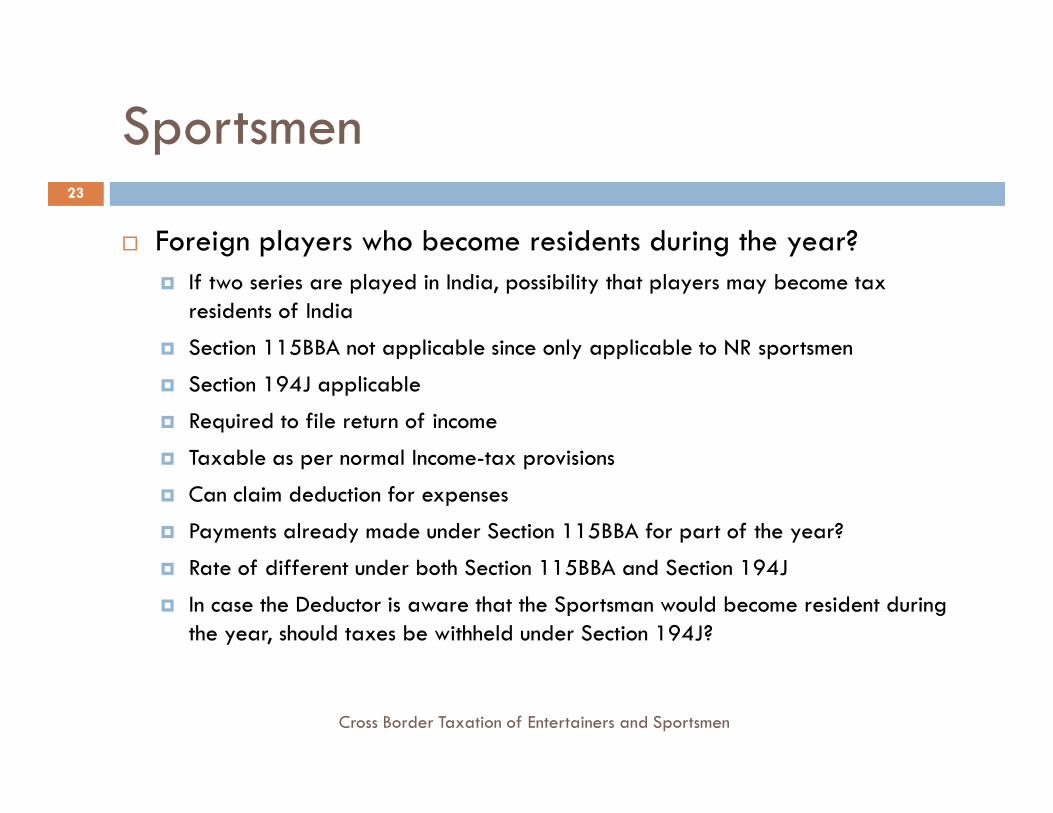

Sportsmen

� Foreign players who become residents during the year?

� If two series are played in India, possibility that players may become tax

residents of India

� Section 115BBA not applicable since only applicable to NR sportsmen

� Section 194J applicable

Required to file return of income

23

� Required to file return of income

� Taxable as per normal Income-tax provisions

� Can claim deduction for expenses

� Payments already made under Section 115BBA for part of the year?

� Rate of different under both Section 115BBA and Section 194J

� In case the Deductor is aware that the Sportsman would become resident during

the year, should taxes be withheld under Section 194J?

Cross Border Taxation of Entertainers and Sportsmen

Case Study - 1

� Akon, an American singer visited India for live stage performances, hosted in 3 cities

in a span of 15 days, organised by a Foreign Management Company (‘F Co’) and

in India by Indian Event management Company (‘I Co’)

� Remuneration - Rs. 2 crores paid by I Co

� I Co released a compilation of audio and video CDs / DVDs the Concert, released

globally by an XYZ Music Company, an Indian Company and remuneration paid

24

globally by an XYZ Music Company, an Indian Company and remuneration paid

was Rs 1 crore on acquiring rights by XYZ Music

� Guest Appearance on Indian Idol, remuneration of Rs 50 lakhs

� Payment of Commission to F Co - Rs 20 lakhs

� Taxability if I Co directly made the entire payment to F Co

Cross Border Taxation of Entertainers and Sportsmen

Case Study - 1

� Remuneration for performance

� Section 115BBA

� Acquiring rights by XYZ Music

� Circular 787 - Subsequent Sale abroad not taxable and subsequent Sale in

India taxable

XYZ Music Company to release it globally

25

� XYZ Music Company to release it globally

� Rs 1 crore to be apportioned between India and other than India

� Guest Appearance on Indian Idol, remuneration of Rs 50 lakhs

� Section 115BBA

� F Co’s income not taxable in India (Wizcraft decision)

� If I Co made the entire payment to F Co:

� F Co could be taxable on portion of Akon’s remuneration in India under Article

17 and not covered by Section 115BBA

Cross Border Taxation of Entertainers and Sportsmen

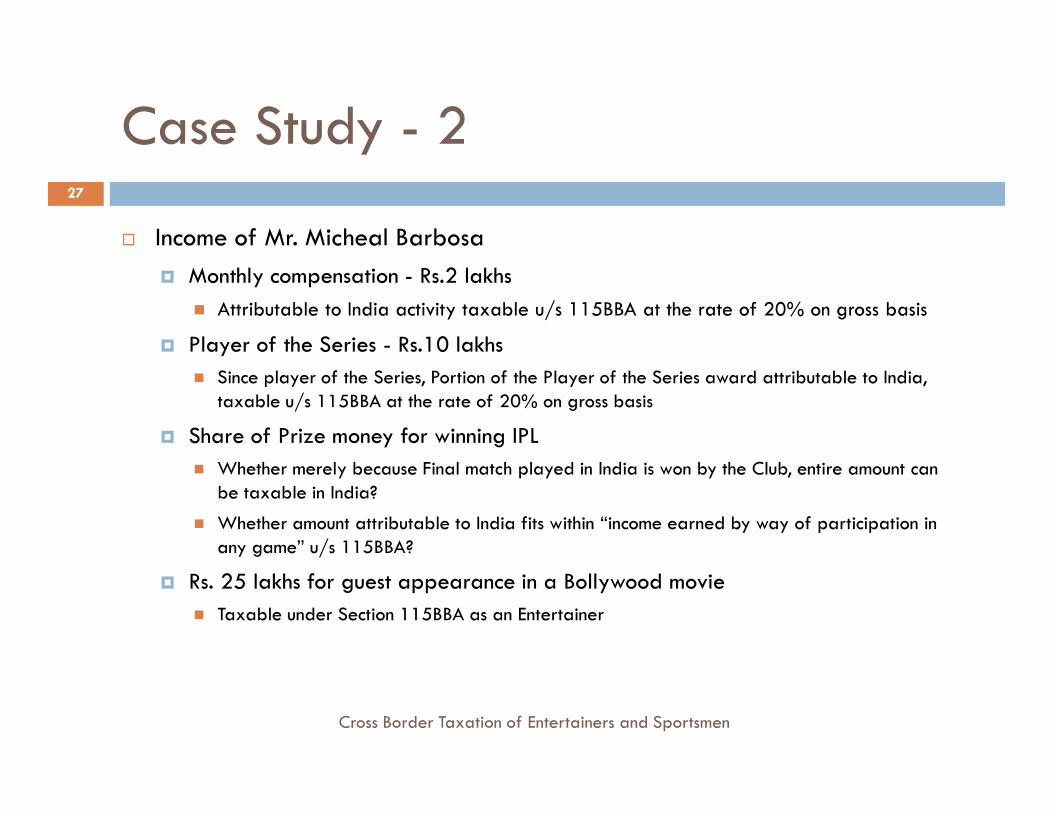

Case Study - 2

� Mr. Micheal Barboza (Brazil Resident), contracted by UK Club to play in IPL in India,

Sri lanka and China

� Play-off matches in India, Sri Lanka and China (to be played over 3 weeks) and

final match in India, with two matches played in a week, training only in India

� Income of the Club - Prize money for winning IFL- Rs. 50 lakhs (50% to be

distributed among players)

26

distributed among players)

� Income of Mr. Micheal Barbosa

� Monthly compensation - Rs.2 lakhs (including time spent in training)

� Player of the Series - Rs.10 lakhs

� Share of Prize money for winning IFL (50%) Rs 25 lakhs

� Nike promotion fees for wearing gear:

� Rs. 2 lakhs: during matches

� Rs. 5 lakhs: during public appearances

� Rs. 25 lakhs for guest appearance in a Bollywood movie

Cross Border Taxation of Entertainers and Sportsmen

Case Study - 2

� Income of Mr. Micheal Barbosa

� Monthly compensation - Rs.2 lakhs

� Attributable to India activity taxable u/s 115BBA at the rate of 20% on gross basis

� Player of the Series - Rs.10 lakhs

� Since player of the Series, Portion of the Player of the Series award attributable to India,

taxable u/s 115BBA at the rate of 20% on gross basis

27

taxable u/s 115BBA at the rate of 20% on gross basis

� Share of Prize money for winning IPL

� Whether merely because Final match played in India is won by the Club, entire amount can

be taxable in India?

� Whether amount attributable to India fits within “income earned by way of participation in

any game” u/s 115BBA?

� Rs. 25 lakhs for guest appearance in a Bollywood movie

� Taxable under Section 115BBA as an Entertainer

Cross Border Taxation of Entertainers and Sportsmen

Case Study - 2

� Income of Mr. Micheal Barbosa

� Nike promotion fees for wearing gear:

� Rs. 2 lakhs: during matches

� Directly related to performance and hence taxable under Section 115BBA

� Rs. 5 lakhs: during public appearances

� Taxable as Income from Advertisement under Section 115BBA

28

Taxable as Income from Advertisement under Section 115BBA

� Income of Club

� Prize money attributable to Players would be taxable under Article 17(2)

� Prize of the Club (50%) Rs 25 lakhs payment under Article 7

� The Club is not a Sports Association, prize money not covered u/s 115BBA

� Taxable in India on net basis under normal provisions

� Other views?

Cross Border Taxation of Entertainers and Sportsmen

Case Study - 3

� Mr. LB, a South African cricketer

� During FY 2011-12, played matches in Indian Premier League 2012

� Participating in FY 2012-13, as a fielding coach

� Dashing Sports Ltd - a US Company, acquires world-wide rights from LB to

use his face, name and character in “Indian Premier Gaming League 2012”

animation game

29

animation game

� LB has advertisement agreement with I Co.

� Advertisement would be for Indian products

Cross Border Taxation of Entertainers and Sportsmen

Case Study - 3

� Taxability of Income from IPL

� Same as per principles outlined in Case Study 2

� Income as a player covered under Art. 17

� Income as a coach

� Covered under Art. 14

May not be taxable if threshold period not crossed

30

� May not be taxable if threshold period not crossed

� Taxability of Advertisement Income

� Section 115BBA

� Taxability of Gaming Rights

� Whether celebrity rights covered under IPR?

� Whether taxable under Article 17 or 12?

� Applicability of Section 115BBA

Cross Border Taxation of Entertainers and Sportsmen

Case Study - 4

� I Co engaged in entertainment event management and marketing

� Organised events/performances of renowned foreign artists/groups in India

� For performances of international artists in India, I Co entered into agreement

with UK agent, also acting as agent for various event management companies

� As per agreement, I Co granted limited authority to UK agent

To act on its behalf; enter into contract with artists; and ancillary acts required to be

31

� To act on its behalf; enter into contract with artists; and ancillary acts required to be

performed outside India

� Apart from payment of fees to artists, I Co paid commission to UK agent and

reimbursed expenses incurred in connection with performances of artists in India

� Fee paid to artist - I Co deducted tax under Article 18 of India-UK DTAA

� Reimbursement of artist’s expenses - I Co did not deduct tax

� Commission and reimbursement to UK Agent – I Co did not deduct any tax since

UK agent had rendered services outside India and it did not have PE in India

Cross Border Taxation of Entertainers and Sportsmen

Case Study - 4

� Commission paid to the UK agent was not for services of entertainers/artists.

� The UK agent had not taken any part in the events, nor performed any activities in India.

Hence, it was not covered by Article 18 of India-UK DTAA.

� The UK agent did not have any PE in India [Carborandum Co. v. CIT, (1977)

108 ITR 335 (SC) and CBDT Circular Nos. 17 (XXXVII) dated 17.07.1953 and

786 dated 07.02.2000], commission paid to the UK agent was not taxable in

32

786 dated 07.02.2000], commission paid to the UK agent was not taxable in

India and no obligation on ICo to deduct tax at source

� Reimbursement of expenses - The law is well settled that reimbursement of

expense not chargeable to tax and hence, no obligation to deduct tax at

source [DIT (IT) Vs. Krupp UDHE Gmbh (2010) 38 DTR (Bom) 251 following own

decision in CIT Vs. Siemens Aktiongesellschaft 220 CTR (Bom) 425]

� ACIT vs Wizcraft International Entertainment Pvt Ltd I.T.A.No. 3208/Mum/2003

� Reliance placed on Circular No. 786 dated 7 February 2000, which is

withdrawn on 22 October 2009 - Implications?

Cross Border Taxation of Entertainers and Sportsmen

Case Study - Marathon

� Every year Mumbai Marathon - Matter of pride to run the Marathon

� Celebrities, industrialists running for a cause

� Almost a social event

33

Cross Border Taxation of Entertainers and Sportsmen

Marathon

� Winner of Mumbai Marathon 2012?

Laban Moiben, from Kenya

34

� Not an Indian

Laban Moiben, from Kenya

Cross Border Taxation of Entertainers and Sportsmen

Marathon

� Africans come to India to run the Marathon

� Invited by the sponsors to run the Marathon, three situations:

� Directly - Payment made directly to the Athletes

� Through a sports association

� Through a management company� Through a management company

� Income of the athletes in India

� Participation fees

� Prize money

� Advertisement, if any

� Contribution to articles, if any

� Reimbursement of expenses

Cross Border Taxation of Entertainers and Sportsmen

Taxability in India

� Directly by Organisers

� Section 115BBA at the rate of 20 percent (plus surcharge and cess)

� Reimbursement of expenses - Discussed in Wizcraft

� Through a Sports Association

� If amount is not guaranteed?

36

� If amount is not guaranteed?

� Covered by Section 115BBA?

� Through a Management Company

� Two situations:

� Own Company ie Star-Company; and

� Sports Companies

Cross Border Taxation of Entertainers and Sportsmen

Marathon

� Through a Star company

� Star company charges Organiser consolidated amount

� Makes the payment to the athlete on its own account

� One agreement between Organiser and Star Company

� Taxability

37

� Star company not covered under Section 115BBA

� However, covered under Article 17(2)

� Article 17 does not provide computation or rate of taxation

� Reference to domestic law

� Payment to Star Company taxable as per domestic law in India

� No special rate or method provided, taxable as per normal provisions

� Taxability of athlete in India?

� Can a view be taken that since ultimate beneficiary is the athlete, Section

115BBA should be applicable?

Cross Border Taxation of Entertainers and Sportsmen

Marathon - Through a Sports management

company (‘SMC’)

� Model 1 - Mechanics

� SMC charges commission and makes payment to the athlete

� Agreement on Principal-Principal basis

� Taxability

� Athlete’s remuneration - SMC covered under Article 17(2) and not under Section 115BBA,

taxable as per normal income tax provisions

38

taxable as per normal income tax provisions

� Commission taxable as business income - No PE, not taxable

� Model 2 - Mechanics

� SMC charges Organiser commission and receives payment on behalf of the Athlete

� Agreement on Principal-Agent Basis

� Taxability

� Commission taxable as business income - No PE, not taxable

� Can a view be taken that since ultimate beneficiary is the athlete, Article 17(1) r.w. Section

115BBA applicable?

Cross Border Taxation of Entertainers and Sportsmen

Way Forward

� Need of a single code for Taxation of Entertainers and Sportsmen

� Section 115BBA and Circular 787

� Article 17 changes proposed in discussion draft could be

incorporated

� Radical Changes to Article 17

39

� Radical Changes to Article 17

Cross Border Taxation of Entertainers and Sportsmen

YOUR

40

Queries

YOUR

QUESTIONS

PLEASE !!!

Cross Border Taxation of Entertainers and Sportsmen

Source

41

Cross Border Taxation of Entertainers and Sportsmen

Thank you!!!42

Isha Sekhri

Cross Border Taxation of Entertainers and Sportsmen