Page 1

CRU Consulting Steelmaking raw materials – key trends

Prepared for the 82nd Session of the OECD Steel Committee

Prepared by CRU Consulting

Laura Brooks, Principal Consultant

e: [email protected]

t: +44 (0) 20 7903 2239

23rd March 2017

Page 2

2

Agenda

• Recent trends for the bulks

• Snapshot of base case long-run forecasts

• 4 key trends to watch

• Why are these trends important?

• Conclusion

OECD Steel Committee

Page 3

3

2014 - 2015: prices crashed due to over-investment in supply

CRU uses super cycles to justify expectations for long-run price trends

1. Super cycles typically take about 25 years peak to peak or trough to trough

2. High capital cost commodities (hard rock or bulks) have a wide amplitude, while less capital- intensive

industries have a narrow amplitude

3. Super cycles come about because of an overreaction of investment following a price spike

-150

-100

-50

0

50

100% Price 2015/2011 % Volume 2015/2011

Price versus volume change

Upstream steel market

OECD Steel Committee

Source: CRU

Page 4

4

Lower costs also helped to drive prices down

CRU Business Cost Curve

x axis: cumulative production, Mt

y axis: Business Cost (normalised to 62% Fe fines, CFR China, $/t

Downwards pressure from lower oil prices, currency depreciation, lower

contractor costs, reduction in headcounts, change in mine plans etc.

Are the cost reductions sustainable?

….this is critical for CRU’s price forecasts

OECD Steel Committee

Source: CRU

Page 5

5

A recovery ensued in 2016, followed by sharp gains in 2017. Why?

0

50

100

150

200

250

Ja

n-0

8

Apr-

08

Ju

l-0

8

Oct-

08

Ja

n-0

9

Apr-

09

Ju

l-0

9

Oct-

09

Ja

n-1

0

Apr-

10

Ju

l-1

0

Oct-

10

Ja

n-1

1

Apr-

11

Ju

l-1

1

Oct-

11

Ja

n-1

2

Apr-

12

Ju

l-1

2

Oct-

12

Ja

n-1

3

Apr-

13

Ju

l-1

3

Oct-

13

Ja

n-1

4

Apr-

14

Ju

l-1

4

Oct-

14

Ja

n-1

5

Apr-

15

Ju

l-1

5

Oct-

15

Ja

n-1

6

Apr-

16

Ju

l-1

6

Oct-

16

Ja

n-1

7

Monthly price, 62% Fe fines, CFR China Average monthly price

0

50

100

150

200

250

300

350

Ja

n-0

8

Apr-

08

Ju

l-0

8

Oct-

08

Ja

n-0

9

Apr-

09

Ju

l-0

9

Oct-

09

Ja

n-1

0

Apr-

10

Ju

l-1

0

Oct-

10

Ja

n-1

1

Apr-

11

Ju

l-1

1

Oct-

11

Ja

n-1

2

Apr-

12

Ju

l-1

2

Oct-

12

Ja

n-1

3

Apr-

13

Ju

l-1

3

Oct-

13

Ja

n-1

4

Apr-

14

Ju

l-1

4

Oct-

14

Ja

n-1

5

Apr-

15

Ju

l-1

5

Oct-

15

Ja

n-1

6

Apr-

16

Ju

l-1

6

Oct-

16

Ja

n-1

7

Australian quarterly contract HCC Average quarterly price

Iron ore price

Hard coking coal price

OECD Steel Committee

Source: CRU

Page 6

6

An improved demand side picture stabilisation in global crude steel production…

0

500

1000

1500

2000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

ROW

China

Global crude steel production

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Q12014

Q32014

Q12015

Q32015

Q12016

Q32016

Rest of world China

Carbon crude steel production growth, y/y %

-30%

-20%

-10%

0%

10%

20%

China North America Europe

HR coil EBITDA margin for Chinese producers, %

A slight increase in demand and expectations of production cuts in China drove steel prices higher

Steel margins fattened despite the increases in iron ore and coking coal prices

…and higher steel prices and margins

OECD Steel Committee

Source: CRU, WSA

Page 7

7

For iron ore = a Chinese import boom, not a demand boom, drove prices higher

-4 -4 -9

78

-20

5

30

55

80

Crude steel Hot metal Iron ore consumption Iron ore imports

Chinese crude steel production and iron ore consumption, 2016, y/y change, Mt

The result of a

sharper cut in

Chinese

domestic iron

ore production

OECD Steel Committee

Source: CRU, WSA

Page 8

8

For coking coal = the Chinese government’s policies played a central role in price movements

China coal capacity, annualised, bn t

NB. Total capacity figures exclude idled capacity.

3

4

2

1

0

5

16 Q3 16 Q4 16 Q2 15 16 Q1 17 Q1

+13%

Operating new capacity Permanently closed capacity Operating capacity

276 working day policy in China Implementation Relaxation

Global prices Global prices

OECD Steel Committee

Source: CRU

Page 9

9

Agenda

• Recent trends for the bulks

• Snapshot of base case long-run forecasts

• 4 key trends to watch

• Why are these trends important?

• Conclusion

OECD Steel Committee

Page 10

India will be the largest driver of steel demand growth

-5%

0%

5%

10%

15%

20%

25%

30%

0

100

200

300

400

500

600

700

800

900

China has not yet hit peak steel but it will no longer drive growth LHS: finished steel consumption, Mt (bars)

RHS: growth in apparent demand, % (line)

10

0

500

1000

1500

2000

2500

2015 2020 2025 2030 2035North America Europe Asia-Pacific advanced Latin America

Russia & CIS China Asia-Pacific, developing India

Middle East Africa

Global finished steel demand, Mt

OECD Steel Committee

Source: CRU, WSA

Page 11

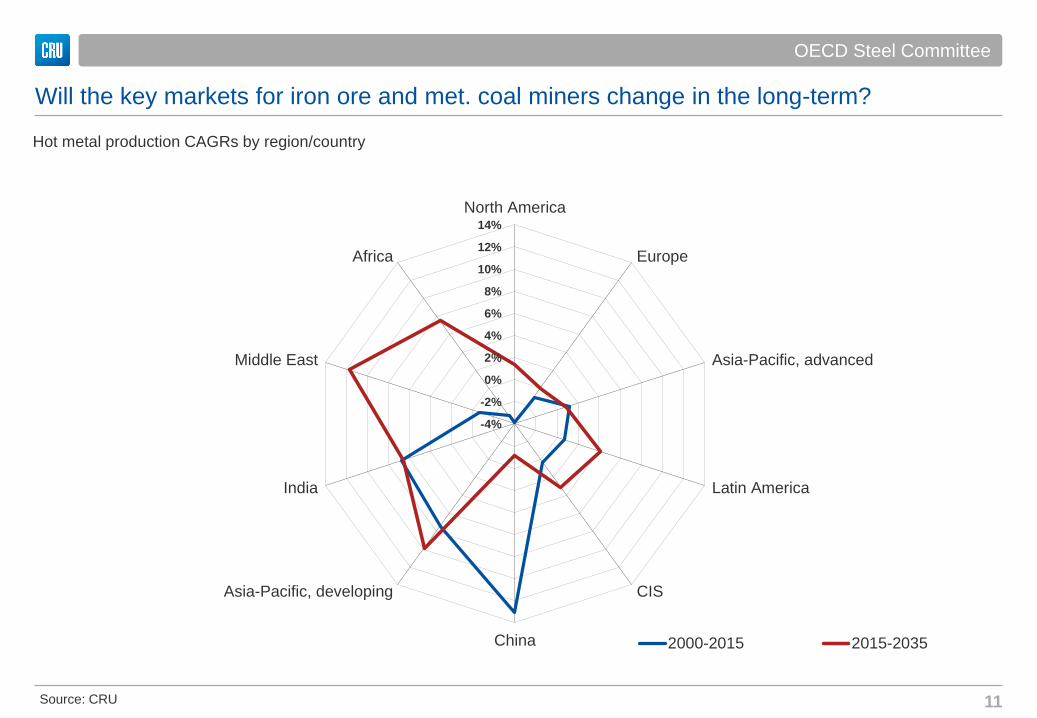

Will the key markets for iron ore and met. coal miners change in the long-term?

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

North America

Europe

Asia-Pacific, advanced

Latin America

CIS

China

Asia-Pacific, developing

India

Middle East

Africa

Hot metal production CAGRs by region/country

2000-2015 2015-2035

11

OECD Steel Committee

Source: CRU

Page 12

Supply/demand “gap” is very different when comparing the bulks

12

800

900

1,000

1,100

1,200

1,300

1,400

16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35

Possible Probable Idled Committed Demand

Gap analysis: met. coal market, demand and potential supply, Mt

Met. coal

S/D “gap” to be filled

by new projects

• IRON ORE - no new greenfield investment is

required in iron ore in the long term, i.e. there is

no gap between supply and demand.

• This does not mean that no new projects will

enter the market.

OECD Steel Committee

Source: CRU

Page 13

13

Agenda

• Recent trends for the bulks

• Snapshot of base case long-run forecasts

• 4 key trends to watch: scrap generation and usage in China

• Why are these trends important?

• Conclusion

OECD Steel Committee

Page 14

China’s construction industry has evolved dramatically over the past 20-30 years

The Shanghai skyline highlights one of many examples of the transition to modern construction methods:

OECD Steel Committee

Page 15

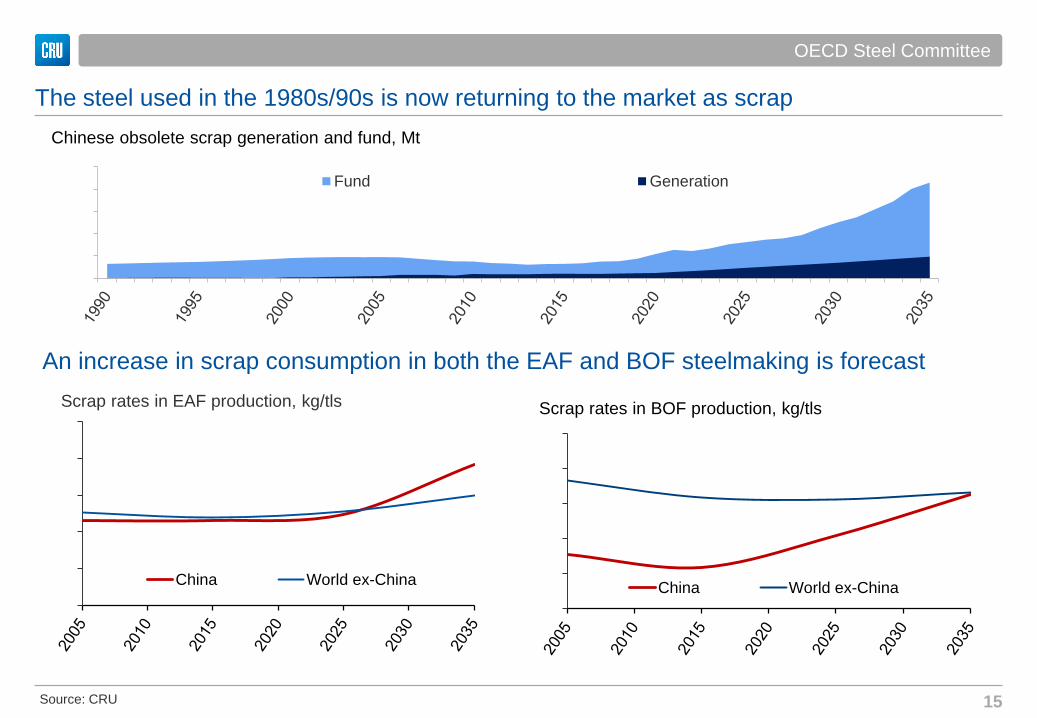

15

The steel used in the 1980s/90s is now returning to the market as scrap

0

300

600

900

1,200

1,500Fund Generation

Chinese obsolete scrap generation and fund, Mt

500

650

800

950

1,100

1,250

China World ex-China

Scrap rates in EAF production, kg/tls

0

60

120

180

240

300

China World ex-China

Scrap rates in BOF production, kg/tls

An increase in scrap consumption in both the EAF and BOF steelmaking is forecast

OECD Steel Committee

Source: CRU

Page 16

16

End of boom times for hot metal production and iron ore and met. coal demand

0

240

480

720

960

1,200

1,440

1,680

RoW India China

Global hot metal production, Mt

This is a negative for the miners

What does this mean for steel

producers?

China’s hot metal production falls at a faster rate

than crude steel due to increasing scrap use

OECD Steel Committee

Source: CRU, WSA

Page 17

17

Agenda

• Recent trends for the bulks

• Snapshot of base case long-run forecasts

• 4 key trends to watch: influence of Chinese government on supply

• Why are these trends important?

• Conclusion

OECD Steel Committee

Page 18

18

Chinese domestic production is critical for the market balance (and price) for both bulks

0

50

100

150

200

250

300

350

400

450

500

0

20

40

60

80

100

120

140

160

180

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Iron ore price Chinese domestic iron ore production

Historical relationship between price and Chinese domestic production

Chin

ese

do

me

stic

iron

ore

pro

du

ctio

n, M

t Iron

ore

price

, $

/t

0 50 100 150 200 250

China

Indonesia

Iran

Mexico

Other Africa

Russia

South Africa

Ukraine

USA

Iron ore supply exits by country, 2013 -2016

Production idled in Australia and Brazil

(combined) in 2016 was well below China’s

volume of exits

OECD Steel Committee

Source: CRU

Page 19

(3)

(2)

(1)

0

1

2

0

2

4

6

8

Production m/m change

LHS: Yangquan coal production, Mt

RHS: Yangquan coal production, m/m change, Mt

(3)

(2)

(1)

0

1

0

2

4

6

8

10

Production m/m change

LHS: Shanxi Coking Coal Group coal production, Mt

RHS: Shanxi Coking Coal Group coal production, m/m change, Mt

Policies to reduce coal production lately have had a dramatic impact on coking coal prices

There is high uncertainty over future policies. Met. coal is likely to be more impacted than iron ore.

OECD Steel Committee

Page 20

20

Agenda

• Recent trends for the bulks

• Snapshot of base case long-run forecasts

• 4 key trends to watch: steel industry restructuring in China

• Why are these trends important?

• Conclusion

OECD Steel Committee

Page 21

21

Restructuring of the Chinese steel industry means a switch to medium-sized blast furnaces

0

100

200

300

400

500

600

700

800

900

1,000Number of blast furnaces in China by size

>4,000 m3 3,000-4,000 m3 2,000-3,000 m3

1,000-2,000 m3 <1,000 m3

0

50

100

150

200

250

300

350

400

450

Pellet rate in China, kg/thm

Outdated

Environmentally un-friendly

Inefficient

….steel capacity is being, and will continue to be, closed

• A focus on productivity drives greater demand

for higher quality blast furnace inputs

• This is a positive for producers of high grade

iron ore products

OECD Steel Committee

Source: CRU

Page 22

22

European blast furnace data demonstrates increased pellet rates aiding higher PCI use

0

50

100

150

200

250

300

0 100 200 300 400 500 600 700 800

Working Volume

x-axis: pellet rate, kg/thm y-axis: PCI rate, kg/thm Bubble size: working volume, m3

OECD Steel Committee

Source: CRU

Page 23

23

Agenda

• Recent trends for the bulks

• Snapshot of base case long-run forecasts

• 4 key trends to watch: flattening and lower of industry cost curves

• Why are these trends important?

• Conclusion

OECD Steel Committee

Page 24

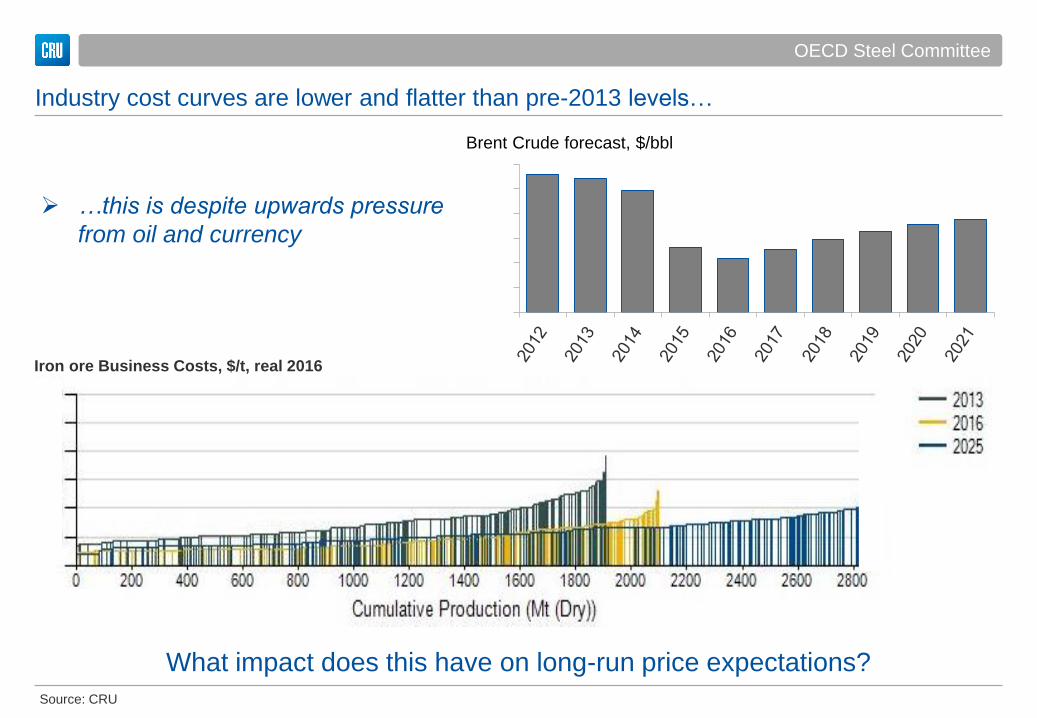

Industry cost curves are lower and flatter than pre-2013 levels…

Iron ore Business Costs, $/t, real 2016

0

20

40

60

80

100

120

Brent Crude forecast, $/bbl

…this is despite upwards pressure

from oil and currency

What impact does this have on long-run price expectations?

OECD Steel Committee

Source: CRU

Page 25

25

Agenda

• Recent trends for the bulks

• Snapshot of base case long-run forecasts

• 4 key trends to watch

• Why are these trends important?

• Conclusion

OECD Steel Committee

Page 26

26

Summary: what do these key trends mean for the bulks markets and for steel?

• Scrap lower demand for raw materials, lower prices

for raw materials, lower input costs for steel

• Chinese domestic mining industry volatility

(scenario analysis!)

• Rationalisation of Chinese steel sector (environmental

trigger) change in demand for different raw

materials product segments

• Lower industry costs and a flatter curve lower

steady-state prices, an end to 70% EBITDA margins

(iron ore), slower supply response, lower input costs

for steel compared to early 2010s levels

OECD Steel Committee

Page 27

27

Our value proposition

Recognition We have a reputation as the foremost name in metals, minerals

and fertilizers consulting and analysis

Independence

We are privately owned and not associated with any producer, consumer, financial community or other stakeholder interest in the industry.

Industry knowledge

Our business is mining, metals and fertilizers and we have been active in this field for over 45 years. You do not pay us to ascend the industry learning curve.

Our people

Our consultants and analysts are subject matter experts within your industry, supported by rigorous economic analysis.

Speed of response

Through CRU Analysis we have existing data and models that can rapidly be customised. Our team is dedicated to single client work

Global presence

We have offices in the key regions – Europe, North & South America, China, India, and Australia

OECD Steel Committee

Page 28

Thank you for listening

28

If you have any questions, please don’t hesitate to contact us:

Laura Brooks

Principal Consultant, CRU Consulting

e: [email protected]

t: +44 (0) 20 7903 2239

Matthew Poole

Head of Ferrous, CRU Consulting

e: [email protected]

t: +44 (0) 20 7903 2179

OECD Steel Committee