Country Profile 2002 Cuba This Country Profile is a reference work, analysing the countrys history, politics, infrastructure and economy. It is revised and updated annually. The Economist Intelligence Units Country Reports analyse current trends and provide a two-year forecast. The full publishing schedule for Country Profiles is now available on our website at http://www.eiu.com/schedule The Economist Intelligence Unit 15 Regent St, London SW1Y 4LR United Kingdom

Transcript

Country Profile 2002

CubaThis Country Profile is a reference work, analysing thecountry�s history, politics, infrastructure and economy. It isrevised and updated annually. The Economist IntelligenceUnit�s Country Reports analyse current trends and provide atwo-year forecast.

The full publishing schedule for Country Profiles is nowavailable on our website at http://www.eiu.com/schedule

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where itslatest analysis is updated daily; through printed subscription products ranging from newsletters to annualreference works; through research reports; and by organising seminars and presentations. The firm is amember of The Economist Group.

Hong KongThe Economist Intelligence Unit60/F, Central Plaza18 Harbour RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

Website: www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, on-line databasesand as direct feeds to corporate intranets. For further information, please contact your nearest EconomistIntelligence Unit office

All information in this report is verified to the best of the author's and the publisher's ability. However, theEconomist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-5111

Symbols for tables�n/a� means not available; ��� means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

4 Politics4 Political background5 Recent political developments7 Constitution, institutions and administration7 Political forces8 International relations and defence

11 Resources and infrastructure11 Population13 Education14 Health15 Natural resources and the environment15 Transport, communications and the Internet18 Energy provision

26 Economic sectors26 Agriculture28 Mining and semi-processing28 Manufacturing29 Construction29 Financial services30 Other services

31 The external sector31 Trade in goods33 Invisibles and the current account34 Capital flows and foreign debt35 Foreign reserves and the exchange rate

36 Appendices36 Membership of regional organisations36 Sources of information37 Reference tables37 Population37 Oil and gas production37 State finances38 Money supply38 Gross domestic product39 Gross domestic product by expenditure, current prices39 Gross domestic product by expenditure, constant prices40 Gross domestic product by sector40 Prices and earnings40 Sugar production

41 Non-sugar agricultural production41 Fishing41 Selected industrial production42 Tourist arrivals and earnings42 Main trading partners42 Main exports42 Import composition43 Balance of payments: current account43 Balance of payments: capital flows43 Official development assistance44 Hard-currency external debt, national series44 Exchange rates

Hottest month, August, 24-32°C (average monthly minimum); coldest months,January and February, 18-27°C; driest months, February and March, 46 mmaverage rainfall; wettest month, October, 173 mm average rainfall

Metric system; also old Spanish units. Sugar is often measured in Spanish tonnesof 2,271 lb and there is a Cuban quintal of 101.4 lb made up of 4 arrobas. Forarea measurement one Cuban caballería equals 13.4 ha or 33.16 acres

Peso (Ps); 1 Peso=100 centavos. Official fixed exchange rate: Ps1:US$1. �Unofficial�exchange rate (floating domestic rate, only available for personal transactions):Ps26:US$1 (2001, year-end). A �convertible peso� (Pc) also circulates domestically,with a value of Pc1:US$1. Tourists and foreign business visitors use US dollars,which are readily accepted; in 2002 euros also began to be accepted in sometourist resorts

Cuba has been governed by the Partido Comunista de Cuba (PCC) since 1965; itis the only legal political party, and exercises de facto control over governmentpolicies. Elections to the People�s Power National Assembly take place every fiveyears (see Constitution, institutions and administration). Fidel Castro Ruz, wholed the revolt that overthrew the US-backed Batista government in 1959, hasbeen the head of the government since that year. He was formally electedpresident for the first time in 1976.

Political background

Settled by Spain in the 16th and 17th centuries, Cuba was used largely as a navalbase before the British occupation in 1762-63. Following the introduction of sugarplantations worked by African slave labour, Cuba became a prosperous sugar-based export economy with the US as its main market. A crisis in the sugarindustry in the 1840s and 1850s, compounded by the weakness of the Spanishcolonial government, fuelled Cuba�s first war of independence (1868-78).Increasingly strained relations between Spain and the US, the dominanteconomic power in the region, culminated in US intervention in the final stageof the second independence war (1895-98).

Emerging victorious from this brief Spanish-Cuban-American war, the USimposed military government on the devastated island from 1899 to 1902. Underthe Platt amendment, which was incorporated into the new Cuban constitutionof 1901, the US retained the right to intervene in the republic�s affairs, andexercised it on a number of occasions (1906-09, 1917 and 1921). The US also woncontrol of the Guantánamo naval base in eastern Cuba, which it still retains.

Instability and rising authoritarianism marked the period from independence tothe 1930s. In 1933 a rebellion by students and junior army officers broughtGeneral Fulgencio Batista Zaldívar to political prominence. General Batistastepped down as president in 1944, but seized power again in a military coupbefore the elections in 1952 could take place.

Opposition to General Batista�s authoritarian and corrupt rule in the 1950s camemainly from student and guerrilla organisations. One such group, led byMr Castro, attacked the Moncada army barracks in Santiago de Cuba in 1953.Mr Castro was captured, tried and imprisoned, but was released into exile in1955. He and 81 of his followers returned to Cuba in December 1956 on a boat,Granma, to initiate a guerrilla campaign from the eastern Sierra Maestramountains, with the support of some urban groups. By late 1958 the guerrillashad advanced into the populated lowlands, and following the collapse ofresistance from the demoralised army, General Batista fled the country onJanuary 1st 1959.

Mr Castro united various political groups to form the OrganizacionesRevolucionarias Integradas (ORI, the Integrated Revolutionary Organisations) toinitiate a transformation of Cuban society. Waves of Cubans fled to the US: first

those associated closely with General Batista�s regime, then the business andprofessional classes. Relations with the US quickly deteriorated, and a partialembargo on Cuban imports was imposed in 1960. In January 1961, in response tothe government�s expropriation of assets worth over US$1bn belonging to USenterprises, the US severed relations. Anti-Castro Cuban emigrés, backed by theCIA, botched an invasion of Cuba at the Bay of Pigs in April 1961. The US thenextended its partial embargo to include all goods.

Cuba turned to a welcoming Soviet Union for military and trade protection.Cuba�s protection from military attack by the US was assured in 1962, in a US-Soviet agreement which ended the Cuban missile crisis (sparked by an attemptby the Soviet Union to install nuclear missiles in Cuba). The new tradedependence was formally acknowledged in 1972, when it became a member ofthe Council for Mutual Economic Assistance (CMEA). Cuba thus became anenemy state to the US in the cold war.

In the late 1980s Cuba rejected the liberalisation policies adopted by othersocialist countries, and its communist government survived after 1990 whileother governments in the socialist bloc collapsed. Relations with most foreigngovernments were normalised in the 1990s, but relations with the US are stillhostile. The US continues to apply economic sanctions against Cuba, althoughpressure for their relaxation has increased over the past few years.

Recent political developments

Cuba is almost alone among the countries of the former Soviet bloc in havingretained its one-party communist political system. However, there have beensome changes to the political system in the past decade. In the constitutionalreform of 1993, direct elections were introduced for the legislature (known as theAsemblea Nacional de Poder Popular�ANPP, National Assembly of PopularPower), and there have been several amendments to the procedures for selectingpolitical representatives at local and national level. The system of broadconsultation, through mass organisations and workers� assemblies, has alsodeveloped, increasing the level of participation in national policy debates.Restrictions on religious organisations have been relaxed, and party member-ship has been opened to religious worshippers. There has been an increasedpolitical emphasis on the role of youth in national political life over the past fewyears, in response to an increase in alienation of the younger generation duringthe economic slump of the 1990s. And as the president, Fidel Castro, weakens(he reached 76 in August 2002), there has been a deliberate effort to replaceolder members of the government with a new generation. Mr Castro continuesto play a central role as leader of political campaigns and arbiter of policy, butthere are some signs that he has allowed an increase in the authority of a groupof political figures around him.

The country�s leader since 1959, Mr Castro presides over the Council of State andCouncil of Ministers, and is the commander-in-chief of the armed forces and thechairman of the Partido Comunista de Cuba (PCC). In 2001 he fainted in a publicmeeting, raising concern that he was weakening, but he reached the age of 76 inAugust 2002, apparently in good health.

Raúl Castro Ruz

First vice-president and defence minister; has been designated by his brother as hisimmediate successor as president.

Carlos Lage Dávila

Vice-president and de facto prime minister; in effect in charge of the government�seconomic team.

José Luis Rodríguez García

Economy and planning minister, an academic brought into government after 1993 tohelp formulate a new economic strategy.

Francisco Soberón Valdés

Head of the Banco Central de Cuba (BCC, the central bank), he brought overseasbusiness experience to the restructuring of the banking system.

Ricardo Alarcón de Quesada

Ex-Cuban ambassador to the UN and now president of the National Assembly; ledthe Cuban side in negotiations with the US in the mid-1990s, which improved co-operation over migratory issues.

Felipe Pérez Roque

A close aide of Mr Castro, he was appointed minister of foreign affairs at the age of34 in 1999.

Other key government figures include the ex-foreign investment minister and nowtourism minister, Ibrahim Ferradaz García; the minister for basic industry, MarcosPortal León; and the ex-foreign trade minister and now minister-without-portfolio,Ricardo Cabrisas Ruiz. Emerging young leaders include Hassan Pérez, leader of theFederación de Estudiantes Universitarios (FEU, the university students� federation)and Otto Rivero, leader of the Unión de Jóvenes Comunistas (UJC).

The head of the Catholic Church in Cuba, Cardinal Jaime Ortega, has assumed ahigher profile since the pope�s visit in 1998, but does not represent himself as anopposition figure.

The domestic opposition includes over 100 small groups, of which some of the mostprominent leaders are: Elizardo Sánchez of the Comisión Cubana de DerechosHumanos y Reconciliación Nacional (the Cuban Commission of Human Rights andNational Conciliation); Osvaldo Paya of the Movimiento Cristiano por la Liberación(the Christian Liberation Movement); Marta Beatriz Roque of the Instituto Cubano

de Economistas Independientes (Cuban Institute of Independent Economists);Hector Palacios of the Partido Liberal; and Raúl Rivero of Cuba Press.

Constitution, institutions and administration

The current constitution, approved by referendum in 1976 to replace thatsuspended when General Batista fled in 1959, describes Cuba as a socialistworkers� state in which the entire people own the basic means of production. Itestablished the Poder Popular (People�s Power) system of deliberative andadministrative assemblies, consisting of a 601-member National Assembly alongwith 14 provincial and 169 municipal assemblies. Establishment of an additionalbottom tier of local government, the Consejos Populares (People�s Councils), wasapproved in a constitutional reform in 1992.

The National Assembly normally meets twice a year, although special sessionsmay be called. Since 1992 parliamentary commissions have monitored crucialissues and debated legislation in advance of National Assembly plenarysessions. The 30-member Council of State has legislative powers and theCouncil of Ministers and the Executive Council (comprising the president, thefirst vice-president and five other vice-presidents) exercise executive andadministrative functions. The president, Mr Castro, is simultaneously head ofstate and head of the government.

A National Assembly election takes place every five years and provincial andmunicipal elections every two-and-a-half years. Following a constitutionalamendment in 1992, national and provincial as well as municipal assemblymembers are directly elected. Two to eight candidates per constituency arenominated through a process of commissions and public meetings. There is onlyone candidate per seat. Voters choose either to approve or reject the candidatesfinally selected, who must obtain 50% of valid votes. Although candidates arenot required to be members of the PCC, in practice the procedures give the partyextensive influence over the selection of candidates.

Political forces

The PCC was formed in 1965 from a merger of the Partido Popular Socialista andthe Castro-led Movimiento 26 Julio (July 26th Movement) and has held powerever since. It is the island�s only legal political party. Grassroots involvement inpolicymaking has been institutionalised through a range of approved nationalorganisations representing various groups, including small farmers, women,students and industrial workers. However, the PCC and its youth wing, theUnión de Jóvenes Comunistas (UJC, the Union of Young Communists), havespecial constitutional status and exercise indirect control over the NationalAssembly (see Constitution and institutions).

The economic crisis triggered by the collapse of the socialist bloc in 1989-90created serious hardship, open unemployment and growing inequality, erodingsupport for the communist government. However, this did not create a climateof rebellion. There was just one significant anti-government outburst, a

spontaneous riot in central Havana in August 1994, when living conditions wereat their worst for decades. The discontent was defused and there have been nofurther major incidents. The organised domestic opposition has been limited tosome small human rights groups and proto-parties. The number of politicalprisoners in Cuba is currently estimated to be between 200 and 1,000. Thelower estimate includes only those deemed to be prisoners of conscience serv-ing custodial sentences; the higher figure includes those who have committedother politically motivated crimes and those detained for short periods by thepolice. All estimates are well below those of the first decade of the Castrogovernment, when the range was between 2,000 (a Cuban government figure)and 20,000 (a CIA estimate). Many of the dissident organisations have links toemigré organisations, mainly in the US. These links increase their financial andlogistical strength but undermine their credibility within Cuba.

Most emigré organisations are small, with the exception of the Miami-basedCuban-American National Foundation (CANF). This group has been weakenedin the past few years, although it remains powerful. Following the death of itsfounder, Jorge Mas Canosa, in 1997, the organisation has split, leaving it weaker.A visit to Cuba by the head of the Roman Catholic Church, Pope John Paul II, inJanuary 1998 caused divisions within the emigré community over the issue ofeconomic sanctions; and the group�s support of claims for the custody of a six-year-old boy, Elián González, by his relatives in Miami, which ended in June2000 with the boy�s return to live with his father in Cuba, turned US publicopinion against the group. However, despite the schisms, the CANF retainssignificant influence. The administration of George W Bush has shown itself tobe particularly receptive to the lobby�s demands and has appointed a significantnumber of Cuban-Americans to federal government positions.

International relations and defence

Relations with the US overshadow all political, economic and internationalissues. The US classes Cuba as an enemy state. US trade sanctions have been inplace since 1960, and there have been no formal diplomatic relations since 1961.The US and Cuban governments maintain an Interests Section in the other�scapital, in the embassy of another country.

Efforts at détente during the 1970s and 1980s foundered on issues such as Cubanaid to third world revolutionaries, the special status granted to Cuban migrantsto the US and US control of the Guantánamo naval base in eastern Cuba. Sincethe end of the cold war, US hostility has centred less on Cuba�s potentialmilitary threat and more on the lack of political and economic freedom and onoutstanding claims for compensation for property expropriated from US citizensand Cuban-Americans in the 1960s. However, successive US administrationshave been torn between conflicting pressures. On the one hand, the anti-Castrolobby, which is in favour of a hard line on economic sanctions and support forpolitical change in Cuba, remains an effective political force; on the other, agrowing number of US political analysts have argued that sanctions have beenineffective, and there is a growing business lobby in favour of greater access tothe Cuban market.

These conflicting pressures have resulted in contradictory signals from the US. In1992 it tightened economic sanctions against Cuba with the so-called TorricelliLaw, but by 1994 tensions had eased sufficiently to allow successful negotiationson a new migration accord. However, in February 1996 relations deterioratedsharply once more when two small planes belonging to the Cuban émigrégroup Brothers to the Rescue were shot down by the Cuban military. Inresponse, the US president, Bill Clinton, halted all direct flights and remittancesto Cuba and signed the controversial Cuban Liberty and Democratic Solidarity(Libertad) Act of 1996�the Helms-Burton Law.

The pope�s visit to Cuba in January 1998 was followed by mounting pressure inthe US to relax sanctions. Direct flights to Cuba for certain approved travellersand direct mail services were restored and remittances of up to US$1,200 peryear allowed. Bilateral co-operation against drug-trafficking has also beencautiously extended. The business lobby�s campaign against sanctions hasyielded results, with the approval in 2000 of a bill making food and medicinesales possible. This resulted in the first sales of food to Cuba in 40 years inJanuary 2002. Further bills have been proposed in 2002 to allow financing offood sales and to lift the restrictions on travel to Cuba. But even if the latest billsto relax sanctions are approved by both houses of Congress, the US president,George W Bush, under heavy pressure from the Florida lobby, has said he willrefuse to sign them into law.

In political terms, Mr Bush�s close ties with the Miami-based Cuban-Americanlobby and the events of September 11th 2001 have considerably worsened theclimate between the US and Cuba. Soon after his inauguration in early 2001Mr Bush sought to assuage the hardline lobby in Florida by pledging to increaseUS aid to dissidents within the island and to stem the increasing flow of UStourists travelling to Cuba without licences (an estimated 80,000 in 2000). Inspite of Mr Castro�s immediate and unequivocal condemnation of the attack onthe US in September 2001, the US president included Cuba among the nationsbelonging to an �axis of evil� and in a list of potential biological warfare threatsto the US (on the grounds that it has an advanced biotechnology industry). Theappointment of Otto Reich, a prominent anti-Castro Cuban-American, to thepost of Under Secretary of State for Latin American Affairs�against the wishesof the influential Senate Foreign Relations Committee�has also contributed tohostile relations. However, the threat of a confrontation with the EuropeanUnion has persuaded Mr Bush to extend the presidential veto of Title III of theHelms-Burton Law, which would allow for claims by ex-owners of nationalisedproperties against third-country investors in Cuba. This decision has dis-appointed the emigré lobby.

Cuba�s bilateral relations with individual EU countries have generally improvedconsiderably over the past decade, with trade and investment relations beingcultivated and diplomatic activity substantially increased. Relations at the EUlevel were soured by an EU demand in 1996 for democratic reforms in Cuba,and despite several attempts to bridge the differences, a co-operation agreementis still unsigned because Cuba will not accept the political conditionality impliedby the EU policy of constructive engagement, known as the �common position�,which distances itself from the policy of economic sanctions but makes closer

economic and political ties conditional on political reform. The African,Caribbean and Pacific (ACP) signatories to the EU Cotonou (formerly Lomé)preferential trade agreement supported Cuba�s application for membership ofthe accord in 1999, but Cuba withdrew its application in 2000 when it perceivedthat the EU would attempt to attach political and economic conditions.However, the ACP group then voted to formally accept Cuba as a full member,granting it the curious status of being in on the negotiations for the renewedCotonou accord, but without being party to its outcome. In 2002 Cuba wasreaffirmed as a member of the ACP and will form part of the negotiatingmachinery for the renewed Cotonou accord with the EU. However, membershipof the renewed accord is still in doubt because of the opposition from some EUmember states.

Despite these difficulties the EU has remained committed in principle tonormalising economic relations and has objected strongly to the extraterritorialprovisions of the 1996 Helms-Burton law, which include the denial of US visasto executives of foreign companies doing business with Cuba and the threat oflegal action against US branches of such companies. In 1997 the EU requested aWorld Trade Organisation (WTO) dispute panel on the issue, but under pressurefrom the US it agreed in 1998 to suspend the panel in return for a UScommitment that sanctions against European companies doing business in Cubawould be waived. However, the EU could restart WTO proceedings if any actionwere taken against EU companies under the Helms-Burton Law.

Relations with former partners in the Soviet bloc were suddenly curtailed in1990-91, but they have since improved. Economic and diplomatic relations havebeen restored with most of the East European and Commonwealth ofIndependent States (CIS) countries, although strains have emerged over politicalissues. The sponsorship in 2001 of a UN resolution condemning Cuba�s humanrights record by Poland and the Czech Republic caused tension, although thisdoes not seem to have hindered the development of trade and investment ties.Relations with Russia have been cool since an October 2001 announcement bythe Russian president, Vladimir Putin, that Russia would close its listening basein Cuba.

Diplomatic relations have been reopened with most nations in the region since1990 and trade is growing, particularly with two North American Free-TradeAgreement (NAFTA) members, Canada and Mexico. Relations with Canadadeteriorated in the first half of 2001, but this did not affect commercial ties, andby the end of 2002 they had started to improve once more. In 2002 relationswith Mexico and Uruguay cooled because both countries criticised Cuba for itshuman rights record. Ties with Venezuela have become much closer followingthe election of Hugo Chávez to the Venezuelan presidency in 1999.

Cuban membership of regional institutions is limited to those organisations notsubject to a US veto. This means that Cuba is excluded from the AmericasSummit, the Organisation of American States (OAS), the Inter-AmericanDevelopment Bank (IDB) and negotiations over the Free-Trade Area of theAmericas (FTAA). Cuba was a founder member of the Association of CaribbeanStates in 1995 and joined the Latin American Integration Association (LAIA) in

1999. It is a full member of the ACP group for negotiations with the EU andjoined Cariforum as a full member in October 2001. It has indicated its desire tostart negotiations with Mercosur and the Andean Community.

Cuba has maintained its social and economic aid programmes to developingcountries. The focus of these programmes has become more commerciallybased over the past decade, although substantial healthcare aid is still donated,particularly in Central America and the Caribbean. Since the late 1990s Cubahas negotiated trilateral medical aid programmes, in which financial assistancefrom France, Belgium, Germany and the United Kingdom has been used tosupport work carried out by Cuban medical personnel in Haiti and Africa.Within Africa, relations with South Africa are particularly strong. Cuba hasactively sought new commercial partners in Asia, and the rescheduling of debtowed to Japan has paved the way for greater bilateral trade since 1998.

State spending on defence was cut from 9.6% of GDP in 1985 to 2.8% of GDP in1995, and has remained under 3% of GDP since then. Military leaders play animportant political role, and occupy several ministerial posts in civilian sectors,including sugar, fisheries and transport. The armed forces have becomeincreasingly involved in business activities, including farming, tourism andmanufacturing. These businesses led the development of enterprise reformsduring the 1990s, moving away from centralised state direction towards greaterautonomy, efficiency and market orientation.

Cuban defence forces2001

Active armed forces 46,000 Armya 35,000 Navya 3,000 Air forcea 8,000Other security services 1,076,500 Civil defence force 50,000 Territorial militiaa 1,000,000 State securityb 20,000 Border guardsb 6,500OthersArmy of Working Youthc 70,000

a Estimate. b Ministry of the Interior. c Conscripts doing their national service in agriculture.

Source: International Institute for Strategic Studies, The Military Balance, 2001/02.

Resources and infrastructure

Population

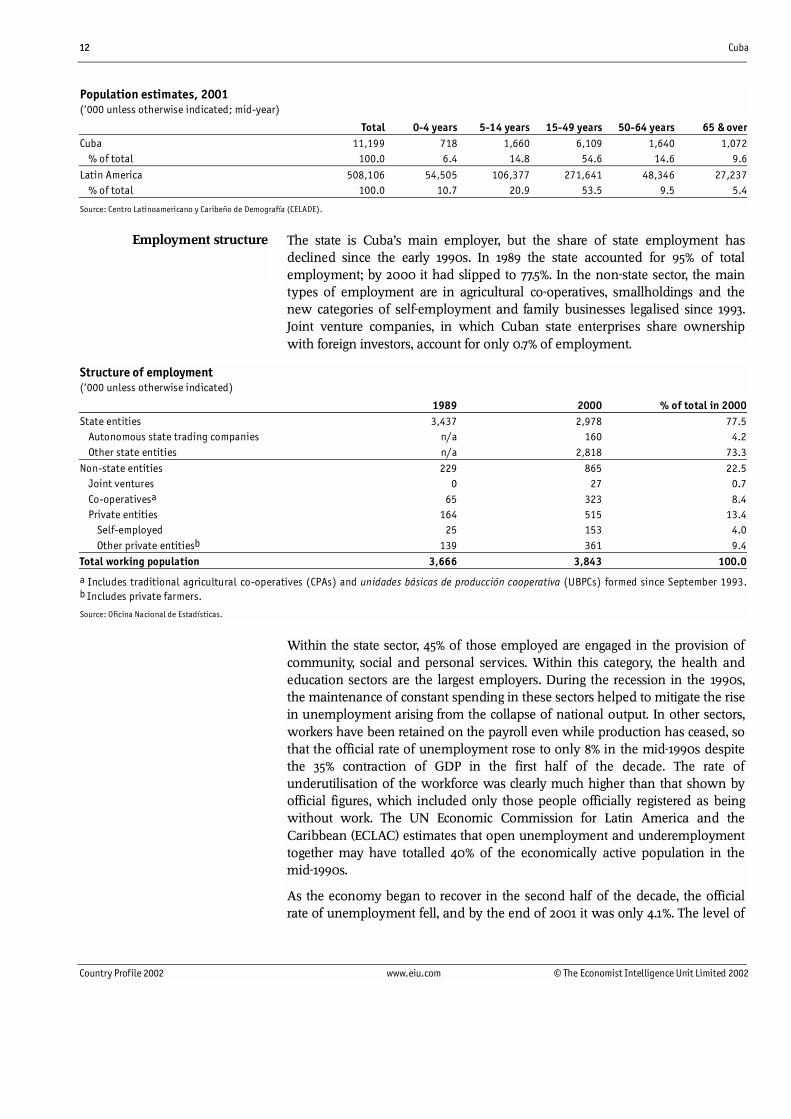

Cuba�s population, estimated at 11.2m at end-2000, grew by an average of lessthan 0.5% per year in the 1990s, well below the Latin American average of 1.6%.The low birth and death rates have given the country an ageing population incomparison with the rest of Latin America. The results of a new census, carriedout in late 2002, are not yet available; the last full national census wascompleted in 1981. (See Reference table 1 for historical data on population.)

Population estimates, 2001(�000 unless otherwise indicated; mid-year)

Total 0-4 years 5-14 years 15-49 years 50-64 years 65 & overCuba 11,199 718 1,660 6,109 1,640 1,072 % of total 100.0 6.4 14.8 54.6 14.6 9.6

Latin America 508,106 54,505 106,377 271,641 48,346 27,237 % of total 100.0 10.7 20.9 53.5 9.5 5.4

Source: Centro Latinoamericano y Caribeño de Demografía (CELADE).

The state is Cuba�s main employer, but the share of state employment hasdeclined since the early 1990s. In 1989 the state accounted for 95% of totalemployment; by 2000 it had slipped to 77.5%. In the non-state sector, the maintypes of employment are in agricultural co-operatives, smallholdings and thenew categories of self-employment and family businesses legalised since 1993.Joint venture companies, in which Cuban state enterprises share ownershipwith foreign investors, account for only 0.7% of employment.

Structure of employment(�000 unless otherwise indicated)

1989 2000 % of total in 2000State entities 3,437 2,978 77.5 Autonomous state trading companies n/a 160 4.2 Other state entities n/a 2,818 73.3Non-state entities 229 865 22.5 Joint ventures 0 27 0.7 Co-operativesa 65 323 8.4 Private entities 164 515 13.4 Self-employed 25 153 4.0 Other private entitiesb 139 361 9.4Total working population 3,666 3,843 100.0

a Includes traditional agricultural co-operatives (CPAs) and unidades básicas de producción cooperativa (UBPCs) formed since September 1993.b Includes private farmers.

Source: Oficina Nacional de Estadísticas.

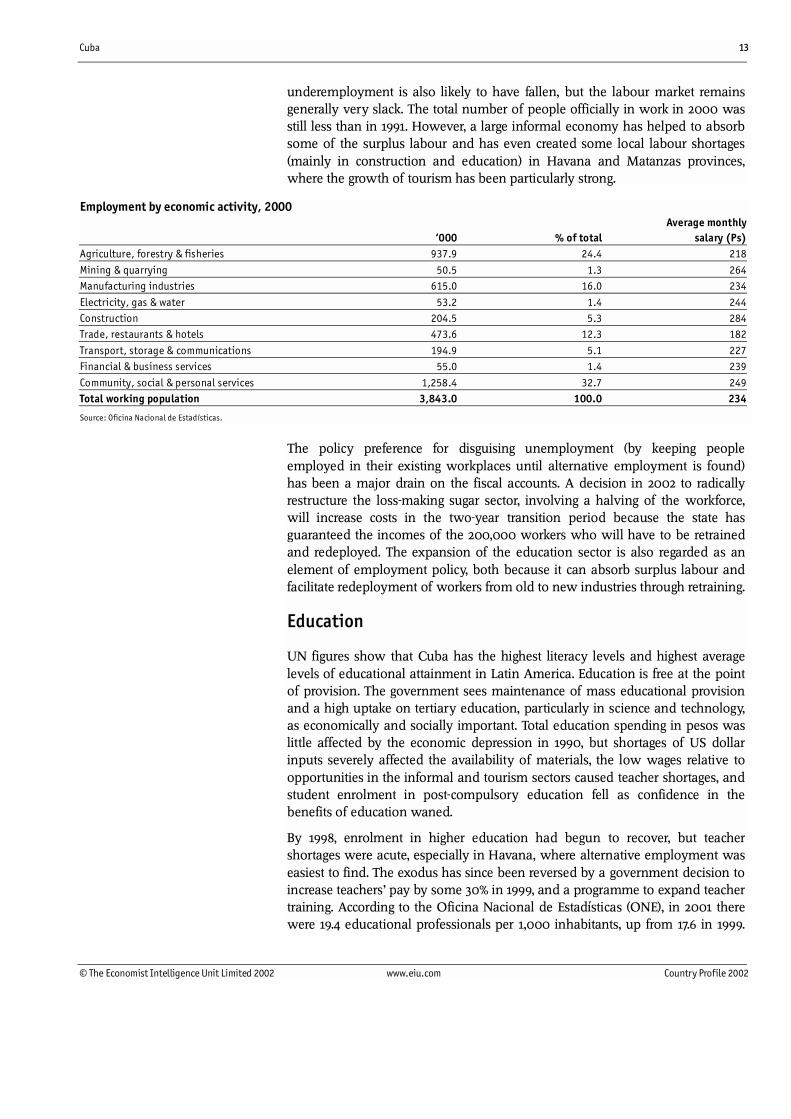

Within the state sector, 45% of those employed are engaged in the provision ofcommunity, social and personal services. Within this category, the health andeducation sectors are the largest employers. During the recession in the 1990s,the maintenance of constant spending in these sectors helped to mitigate the risein unemployment arising from the collapse of national output. In other sectors,workers have been retained on the payroll even while production has ceased, sothat the official rate of unemployment rose to only 8% in the mid-1990s despitethe 35% contraction of GDP in the first half of the decade. The rate ofunderutilisation of the workforce was clearly much higher than that shown byofficial figures, which included only those people officially registered as beingwithout work. The UN Economic Commission for Latin America and theCaribbean (ECLAC) estimates that open unemployment and underemploymenttogether may have totalled 40% of the economically active population in themid-1990s.

As the economy began to recover in the second half of the decade, the officialrate of unemployment fell, and by the end of 2001 it was only 4.1%. The level of

underemployment is also likely to have fallen, but the labour market remainsgenerally very slack. The total number of people officially in work in 2000 wasstill less than in 1991. However, a large informal economy has helped to absorbsome of the surplus labour and has even created some local labour shortages(mainly in construction and education) in Havana and Matanzas provinces,where the growth of tourism has been particularly strong.

Employment by economic activity, 2000Average monthly

�000 % of total salary (Ps)Agriculture, forestry & fisheries 937.9 24.4 218

Community, social & personal services 1,258.4 32.7 249Total working population 3,843.0 100.0 234

Source: Oficina Nacional de Estadísticas.

The policy preference for disguising unemployment (by keeping peopleemployed in their existing workplaces until alternative employment is found)has been a major drain on the fiscal accounts. A decision in 2002 to radicallyrestructure the loss-making sugar sector, involving a halving of the workforce,will increase costs in the two-year transition period because the state hasguaranteed the incomes of the 200,000 workers who will have to be retrainedand redeployed. The expansion of the education sector is also regarded as anelement of employment policy, both because it can absorb surplus labour andfacilitate redeployment of workers from old to new industries through retraining.

Education

UN figures show that Cuba has the highest literacy levels and highest averagelevels of educational attainment in Latin America. Education is free at the pointof provision. The government sees maintenance of mass educational provisionand a high uptake on tertiary education, particularly in science and technology,as economically and socially important. Total education spending in pesos waslittle affected by the economic depression in 1990, but shortages of US dollarinputs severely affected the availability of materials, the low wages relative toopportunities in the informal and tourism sectors caused teacher shortages, andstudent enrolment in post-compulsory education fell as confidence in thebenefits of education waned.

By 1998, enrolment in higher education had begun to recover, but teachershortages were acute, especially in Havana, where alternative employment waseasiest to find. The exodus has since been reversed by a government decision toincrease teachers� pay by some 30% in 1999, and a programme to expand teachertraining. According to the Oficina Nacional de Estadísticas (ONE), in 2001 therewere 19.4 educational professionals per 1,000 inhabitants, up from 17.6 in 1999.

These initiatives were followed in 2002 by a drive to modernise and renovatethe school infrastructure and to focus on education as a national priority.Education spending was increased from 7.5% of GDP to 9.2%, allowing schoolclass sizes to be reduced to a maximum of 20 and new schools and highereducation institutions to be added. Computers have been installed in schoolsand televisions are being used to broadcast cultural and educational pro-gramming provided in a new third television channel.

Health

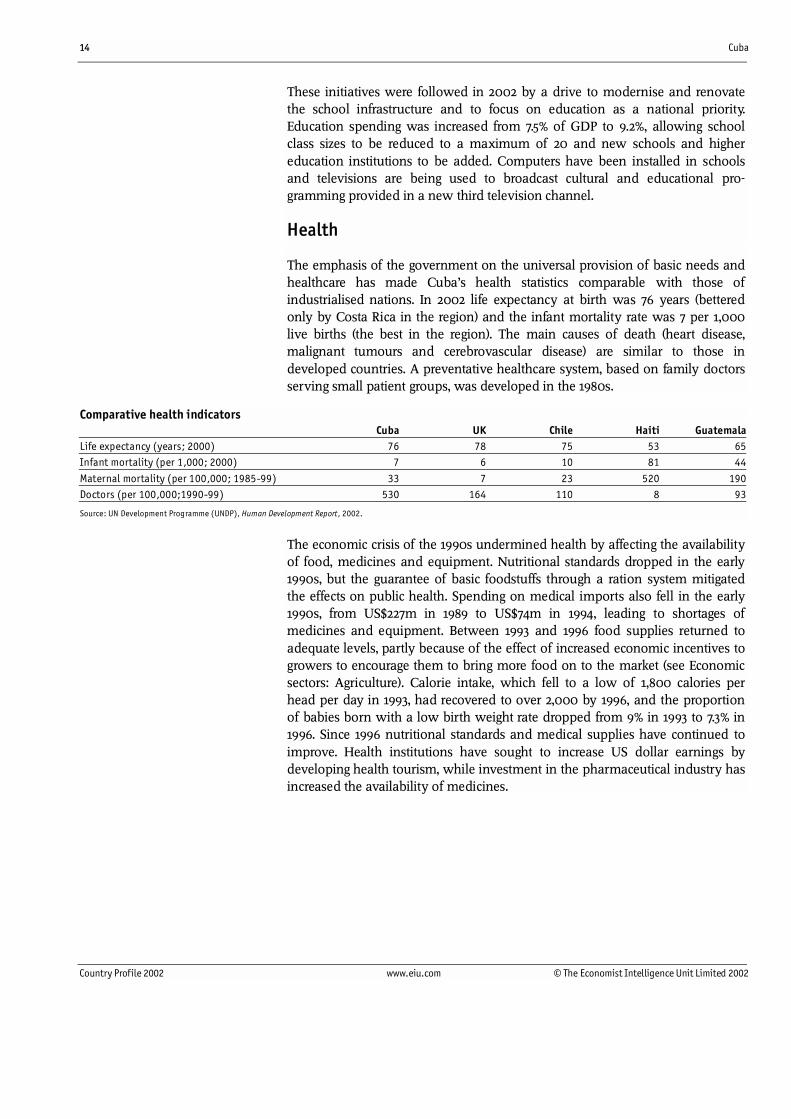

The emphasis of the government on the universal provision of basic needs andhealthcare has made Cuba�s health statistics comparable with those ofindustrialised nations. In 2002 life expectancy at birth was 76 years (betteredonly by Costa Rica in the region) and the infant mortality rate was 7 per 1,000live births (the best in the region). The main causes of death (heart disease,malignant tumours and cerebrovascular disease) are similar to those indeveloped countries. A preventative healthcare system, based on family doctorsserving small patient groups, was developed in the 1980s.

Comparative health indicatorsCuba UK Chile Haiti Guatemala

Source: UN Development Programme (UNDP), Human Development Report, 2002.

The economic crisis of the 1990s undermined health by affecting the availabilityof food, medicines and equipment. Nutritional standards dropped in the early1990s, but the guarantee of basic foodstuffs through a ration system mitigatedthe effects on public health. Spending on medical imports also fell in the early1990s, from US$227m in 1989 to US$74m in 1994, leading to shortages ofmedicines and equipment. Between 1993 and 1996 food supplies returned toadequate levels, partly because of the effect of increased economic incentives togrowers to encourage them to bring more food on to the market (see Economicsectors: Agriculture). Calorie intake, which fell to a low of 1,800 calories perhead per day in 1993, had recovered to over 2,000 by 1996, and the proportionof babies born with a low birth weight rate dropped from 9% in 1993 to 7.3% in1996. Since 1996 nutritional standards and medical supplies have continued toimprove. Health institutions have sought to increase US dollar earnings bydeveloping health tourism, while investment in the pharmaceutical industry hasincreased the availability of medicines.

Public health service statistics, 2001Health spending (% of GDP) 6.3Total no. of doctors 66,285Family doctors 30,726

Population per doctor 169Population covered by family doctor service (%) 99.1

Service facilities Hospitals 270a

Polyclinics 440a

a 2000.

Sources: Ministry of Public Health; Oficina Nacional de Estadísticas.

Natural resources and the environment

Cuba is the largest island in the Greater Antilles, 1,250 km long and 31 km to191 km wide. The national territory, including offshore islands and keys,covers 110,860 sq km. Rainfall is comparatively high, with a dry season fromNovember to April and hurricanes in June-October. A limestone plain coversalmost three-quarters of the island. There are three mountain ranges: theSierra Maestra, which dominates the south-eastern part of the island, theGuaniguanico range in the west, which rises to just over 700 metres, and thecentral Guamohaya (Escambray) range. Few of Cuba�s 200 rivers are suitablefor electricity generation. Over 300 beaches provide potential for tourism.

Although protection of the environment is written into the constitution,methods used in agriculture (particularly in the sugar sector) have oftendamaged soil, and dilapidated and polluting industrial plant and machineryhave been tolerated. A new environmental law was introduced in 1997establishing a regulatory framework, including fines and the principle ofenvironmental taxation. Organic agriculture and alternative energy sources(particularly solar energy) are now being promoted. Plans for reforestationenvisage an increase in coverage from the current level of 22% of the land area toup to 28% by 2015, and improvements in water treatment are under way. In thepast decade the number of environmental projects supported by internationalco-operation has grown.

Transport, communications and the Internet

Cuba�s 10,990-km network of paved roads, of which 682 km are highways, iswell integrated with cities, towns and ports. However, a decade of neglect in the1990s has left the network in poor condition. A repair programme is under way,although government funding for road works has prioritised tourist areas. Theeastern tunnel under Havana bay was reopened after extensive renovation in2001. Discussions about widening the scope for road concessions have thus farcome to nought as foreign capital has shown scant interest. Shortages of fuel andspare parts sharply reduced all forms of road transport in the early 1990s, buteconomic recovery since 1994 has been accompanied by rising traffic. Fleetimprovements, helped by a joint venture bus assembly contract with a Braziliancompany, Busscar, have allowed the number of bus passenger journeys to

increase by 38% between 1998 and 2001, and inland road freight distribution isimproving as old, fuel-inefficient trucks are being replaced by imported newvehicles for prioritised sectors. Private car ownership and road traffic remainlow by international standards, but increases are anticipated in an integratedtransport plan for Havana, now under discussion.

Road and rail transport, 2001Passenger transport (m passenger journeys)Bus services 623Railways 15

Freight transport ('000 km tonnes)Road 42,450Rail 5,380

Source: Oficina Nacional de Estadísticas.

Over half the railway system of over 11,000 km serves the sugar industry. Thedecline in the sugar harvest during the 1990s and closure of mills have hit freightlevels, and a severe lack of investment has led to depreciation of the networkand rolling stock. Railways serving tourist areas have attracted some foreigninvestor interest. But although foreign investment has contributed to themodernisation of a passenger service for the 750-km main arterial routebetween Havana and the second largest city, Santiago, and a new rail linkbetween Havana�s José Martí International airport and the tourist resort ofVaradero is being planned, the level of investment is insufficient to reverse thedeterioration in the network.

Both air freight and air passenger transport volumes increased sharply between1992 and 1999, as Cuba opened to international tourism and rebuilt traderelations. High oil prices, financing difficulties experienced by the nationalairline, and a slump in visitors following the September 11th 2001 attacks onthe US, have interrupted growth since then. Civil aviation was restructured in1997, when the national airline, Cubana de Aviación, and the services companyEmpresa de Aeropuertos y Servicios Aeronáuticos, together with smallerairlines providing domestic and regional services, were brought under theumbrella of the Corporación de la Aviación Cubana.

Tourism revenue is driving expansion of air services. The opening of a newinternational airport on Cayo Coco off the northern coast of Ciego de Avílaprovince in 2002 brought the total number of airports to 20, of which 11 serveinternational traffic. Seven of the international airports have been upgradedsince 1995, and there is now air transport capacity for more than 8m tourists ayear, compared with the current inflow of still under 2m. The Havana andVaradero airports deal with 70% of international arrivals, and projects currentlyin progress will lift capacity in the two airports to 3m and 1.25m respectively.Freight capacity was improved with the opening of a new cargo terminal at JoséMartí airport in Havana in 2002.

Cuba has seven major sea ports and 20 sea terminals. The merchant marine,which was the Caribbean�s largest at the end of the 1980s, suffered from thecollapse of Soviet-bloc trade. Total cargo handled fell by over one-half in theearly 1990s. Maritime transport was decentralised in the 1990s and is expandingwith the help of some foreign capital and the entry of overseas shippers. In 1999the industry comprised six shipping companies with a total of around 100vessels and a total deadweight of 1.2m tonnes.

The problem of chronic under-investment in Cuban telecommunications beganto be addressed with the formation of Etecsa in 1994, a joint venture betweenthe state telecoms enterprise and a Mexican company, Grupo Domos. An Italiancompany, Stet, has since replaced Grupo Domos as Etecsa�s partner, but theupgrading programme has continued. A US decision in 1994 to authorisepayments to Cuban operators for a share of revenue from US-Cuban serviceshelped to finance the investment, and a further boost was given to developmentof the sector by the establishment of a new Ministry of Information Technologyand Communications in January 2000. The new ministry has a mandate tospeed the development of trade and e-business using information technology tomake Cuba an �information society�. It has a range of autonomous subsidiaryenterprises focusing on separate information technology (IT) industries such astelecoms, software, hardware, wireless, training, and e-commerce. Each of theseis actively seeking foreign partners. Communications activity increased by 14%in 2001, making it the most dynamic sector in the economy.

The surge in investment included the digitalisation of the country�s telephonenetwork, replacing the archaic analogue telephone system with wirelessapplication protocol (WAP). By the end of 2001 67% of telephone exchanges�and 90% of those in Havana�had been digitalised, compared with only 23% ayear before. In 2002 digitalisation coverage is expected to rise to 80%. Telephonedensity is low. The Oficina Nacional de Estadísticas (ONE, national statisticsoffice) reports that there are only 5.1 lines per 100 inhabitants in 2001; thetelecommunications ministry�s figure is slightly higher but still small, at 7.1. Aprogramme for expansion added some 80,000 new lines in 2001, and a further100,000 are scheduled to be completed by the end of 2002. Work on a nationalfibre-optic network has begun, and the main cable from west to east expected tobe completed by the end of 2002. A joint venture between Cubacel (Cuba) andan Italian company, Sirti, is carrying out the work.

The Ministry of Communications and Informatics has indicated that there areplans to extend cellular telephone services�which are currently available only tobusiness and tourist users�to Cubans for personal use by the end of 2003. Theservice will be available for payment in US dollars only. Since mid-2001 therehave been two mobile service providers Cubacel and C-Com.

Official policy is to seek to maximise access to information technology. To thisend, a nationwide network of public access computer clubs, equipped withPentium computers, has been established. These clubs give free lessons andaccess to computers. New computers have also been installed in all schools. In2001 a programme was launched to install Internet terminals in every local postoffice, to provide universal access to e-mail facilities. Few people have access to

the Internet from home, but government offices, universities, and businesses allhave wireless Internet access. Satellite earth stations are being built across theisland. Fibre-optic cable is being laid throughout Havana, connecting to a �fibrering� around the capital city, and in October 2001 work started on a link toMatanzas. A fibre-optic cable has been laid between Cuba and Florida, althoughUS legislation prevents it being connected to a US terminal, and a link with thenetwork linking the Americas is scheduled for completion by the end of 2004.

Cuban planners hope that its investment in information technology will help toboost Cuba�s competitiveness in international markets. To improve the level ofskills, a new university specialising in informatics opened in September 2002 atthe former Russian listening base at Lourdes, outside Havana. This facility willprovide future recruits for a new software export industry, which wasinaugurated with the opening of a new IT software production facility at Tarará,East of Havana, with 150 software engineers, in 2002.

Energy provision

Until 1990 Cuba imported 12m-13m tonnes of oil per year from the Soviet Unionin exchange for sugar at favourable terms of trade. When Soviet supplies fell tolittle more than 1m tonnes/year (t/y), Cuba had to source oil on the world market.Oil imports fell steeply, from 13.1m tonnes in 1989 to 5.5m tonnes in 1993. Sincethen imports have recovered, but an increase in domestic oil and gas production,improvements in energy efficiency and the use of alternative energy sources,have also served to moderate Cuba�s energy import needs.

Domestic crude production has increased over sixfold since 1991, to reach anestimated 3.4m tonnes in 2002, around 40% of total oil consumption. Thisexpansion has been facilitated by over US$500m in foreign investment in thesector since the early 1990s. Until now, the oil has come from wells close to thenorth coast of Matanzas province, but Cuba also has unexplored deep seaterritory in the Mexican Gulf. In 1999, 59 oil exploration blocks in Cuba�sMexican Gulf territory were made available to foreign partners for the first time;in 2002 it was reported that 17 of these had been taken up. Foreign partners havealso been sought for the modernisation of a large Soviet-built oil refinery atCienfuegos (with a capacity of 11m t/y, or 220,000 barrels/day). In late 2002 aSwiss-based, Russian-owned company, Crown Resources, announced its interestin the project, involving investment of US$40m. (See Reference table 2 forhistorical data on oil production.)

With oil import costs amounting to US$1bn in 2001, or 20% of total importspending, Cuba remains vulnerable to oil price or supply shocks. It wasanticipated that an October 2000 deal to purchase a third of national oil needsfrom Venezuela, on preferential financing terms, would help to reduce Cuba�svulnerability, but political disputes within the Venezuelan state oil company,Pdvsa, interrupted these supplies between April and September 2002.

a Input basis. b Input to transformation processes (electricity generation, gas manufacture, liquids from coal, etc) plus energy industry fuel andlosses. Primary electricity output and imports/exports of electricity are expressed as input equivalents, on an assumed generating efficiency of33%. c Output basis.

Source: Energy Data Associates.

Electricity generation is mainly oil-fired, but the sugar industry generates its ownpower using cane waste, and other sources (including hydroelectric plants andsolar power) are used on a small scale. Fuel shortages and a deterioration in thecondition of power plants and distribution networks led to power rationing andfrequent supply interruptions in the mid-1990s, but since then more reliable fuelsupplies, repairs and new investments in electricity generation and distributionhave increased reliability. By the end of 2002, 90% of Cuba�s electricity wasgenerated from Cuban crude, following the completion of investments to replaceSoviet generating plants with new technology. Plans for the completion of aSoviet-built nuclear power station, which was mothballed after 1990 for lack ofcapital, were abandoned in late 2000.

Current-account balance (US$ m) -552.7Exports of goods fob (US$ m) 1,762.1Imports of goods fob (US$ m) 4,838.3

External debt stock (US$ m) 10,893.0 a

Population (year-end; m) 11.2

a Hard-currency debt only.

Sources: Banco Central de Cuba; Oficina Nacional de Estadísticas.

According to the latest national sources, services accounted for 66% of GDP in2001, agriculture for 7% and industry for 28%. The services sector consists of avery large welfare state on the one hand, and a rapidly growing tourismindustry on the other. Within the agricultural sector, sugar has traditionally beenthe dominant crop, accounting for around half the land area under cultivation.Low world prices and low Cuban yields have resulted in large losses in thesugar industry in recent years, prompting the initiation of a radical restructuringprogramme in 2002. This is expected to halve the area under sugar by 2004,

allowing for an expansion of food crops and other export agriculture (mainlycitrus and tropical fruit). The sugar processing industry will also contract, alteringthe structure of the industrial sector. Industrial production contracted sharply inthe early 1990s. New investment has brought a recovery in some industries�particularly nickel mining, steel production and light industries supplying thetourism sector�but many plants remain under-utilised or idle.

Comparative economic indicators, 2001Dominican

Cuba Guatemala Republic Mexico JamaicaGDP (US$ bn) 25.5 a 20.5 21.3 617.8 7.8

GDP per head (US$) 2,275 a 1,759 2,473 6,155 2,966Consumer price inflation (av; %) -4.1 7.6 8.9 6.4 6.9

a Economist Intelligence Unit estimates; there are no official figures. b Hard-currency debt only.

Source: Economist Intelligence Unit.

Economic policy

Following the 1959 revolution, the economy was transformed from a capitalist toa centrally planned system. Membership of the Soviet trading bloc, the Councilfor Mutual Economic Assistance (CMEA), which Cuba joined in 1972, providedterms of trade that favoured sugar-led development and generous loans andtransfers to finance large current-account deficits. Following the dissolution ofthe CMEA in 1990, Cuba has not followed other CMEA countries in making atransition to a full market economy. Instead, the initial policy response in theearly 1990s was emergency planning, and this has been followed byretrenchment and reform.

When the economy began to slide in 1990-91, economic planners halted non-essential imports and channelled all available resources into essential services.But by 1993, the decline in economic activity and acute imbalances forced anadjustment as it became apparent that the state was becoming unable to fulfil itsguarantee of universal provision of minimum basic needs. Shortages andsuppressed inflation had caused a collapse of the black market exchange rateand stimulated a boom in black-market activity, while the fiscal deficit reachedan estimated 33% of GDP. In 1994 the government implemented an initialstabilisation package. Increases in tax rates, together with new taxes, usercharges and price increases on non-essential goods, were introduced to mop upexcess liquidity. On the spending side, the sharpest cuts were made in defencespending and state investment, while social spending remained steady. The statedeficit was reduced to 7.4% of GDP in 1994 and 3.2% in 1995, the money supply,which had more than doubled between 1990 and 1993, stabilised, and theunofficial exchange rate recovered from around Ps140:US$1 to Ps25:US$1. (SeeReference table 3 for historical data on state finances and Reference table 4 fordata on money supply.)

Possession of foreign currency depenalised; self-employment widened; a new kindof agricultural co-operative, the unidad básica de producción cooperativa (UBPC, basicunit of co-operative production), was established, to replace many state farms.

1994

User charges introduced and prices of non-essential goods raised; new taxationsystem established; 15 ministries abolished in radical restructuring of stateadministration; convertible peso introduced, at par with the US dollar and with fullhard-currency backing; foreign trade decentralised; banking reform begun; free retailmarkets established for agricultural produce, crafts and manufactured goods; 100new categories of legal self-employment introduced.

1995

New foreign investment law passed and new ministry established; self-employmentallowed for university graduates in restricted activities; sight and time deposits inhard currency authorised for nationals; bureaux de change set up to handle personalcurrency purchases; automation of banking network commenced.

In order to stimulate trade, reduce black market activity and improve economicefficiency, some liberalising reforms were introduced in 1993-95. They includedthe depenalisation of possession of hard currency and establishment of a new�unofficial� exchange market to replace the black market, transformation ofmany state farms into co-operatives, and the first steps towards decentralisationof economic management.

Since 1995, there has been no major change in the government�s approach toeconomic policy. The fiscal deficit has been held below 3% of GDP and thesystem of economic management has become gradually more decentralised,with government seeking to adapt and strengthen the institutional framework.The free agricultural markets have increased the supply of food to the cities, andhave become an important source of income for farmers. The domesticcirculation of foreign exchange opened the way for the establishment of anationwide network of hard currency state retail outlets, which have made itpossible to begin to develop a free market for consumer goods. The shops havealso provided the government with an important source of foreign exchange, aspart of the retail mark-up is paid to the state. The tax system has continued toevolve since 1995. Direct taxes, which were almost eliminated in 1967, have sincereturned.

New forms of quasi-autonomous state companies introduced in the first half ofthe 1990s heralded the start of a long process of decentralisation of enterprisemanagement, using profit and loss accounts, and wider use of incentives andbonuses. This process has been accompanied by reforms to create a financialsystem to replace the previous centralised system for the allocation of finance.Since 1995 a set of state-owned financial institutions have been created underthe supervision of the Banco Central de Cuba (BCC, the central bank). Theregulation of the various forms of more autonomous enterprise, from the

expanded self-employed sector to multinational joint enterprises, has evolvedwith the development of new legislation and institutions. However, the pricesystem is not yet able to operate as an efficient allocator of resources, asdomestic prices and the official exchange rate (used for enterprise accounts) arefixed by the state.

Reforms evolve, 1996-2002

1996

Free-trade zones and industrial parks law passed; new banks opened and 71% ofbank branches automated.

1997

A new central bank (the Banco Central de Cuba) established; first free-trade zonesopened; registration and taxation of private rental activity introduced.

1998

Tax reforms introduced; enterprise management systems reviewed.

1999

Monetary policy committee set up; consumer credit established; further progress inreform of enterprise management.

2000

Introduction of interest-bearing savings accounts, factoring and promissory notes;real estate developments financed by foreign investors repurchased by the Cubanstate.

2001

Decentralisation of enterprise management continues; a new Ministry of Audit andControl takes charge of regulation and supervision of state and private enterprises.

2002

Radical restructuring of the sugar industry begins; a new law enables members ofsmall farmers� co-operatives to keep 75% of their profits rather than the 50%previously allowed.

Most sectors of the economy have been opened to foreign businessparticipation, although the Ministry for Foreign Investment and Economic Co-operation (Minvec), created in 1995, continues to vet all applications. Permissionsare granted only if Minvec can be convinced that the foreign partner can offercapital, technology or markets that would otherwise be unavailable to theCuban counterpart.

Although the reforms and adjustments have brought profound changes ineconomic management and increased the role of the market, expectations of afull transition to a market economy have not been met. The state still centrallydirects the allocation of finance in many areas, and its tight regulation andcontrol of prices, the labour market and foreign investment severely restricts therole of the free market. Private ownership of land and productive capital byCuban citizens is still limited to farming and self-employment, and at present thegovernment is unwilling to contemplate a mass privatisation programme. The

sale of assets to foreign investors is not only resisted by the government, but alsodiscouraged by US legislation, which threatens action against investors inproperty nationalised since 1959. The lack of access to the US market has alsomeant that free-trade zones and industrial parks, which were opened under a1996 law to attract investors in manufacturing and stimulate employment, haveso far attracted little manufacturing activity.

Economic performance

The only data available for Cuban GDP trends are the official national data.Statistics are not verified by the IMF, but the UN Economic Commission for LatinAmerica and the Caribbean (ECLAC) has accepted the Cuban data as the bestavailable.

Until 1989 the national income series was based on the material balances system,in line with practice among CMEA countries. Economic growth was measured interms of global social product (GSP), which is not directly comparable with GDP.The main difference was the exclusion of most services from the accounts. In1990, following the collapse of the CMEA, the series was suspended. In 1995 theCuban national statistics office presented new GDP figures, to comply withstandard UN macroeconomic accounting practices.

Until 2002 the data for GDP were expressed only in 1981 constant prices; a newseries, using 1997 prices, has been prepared but only part of this series�the years2000 and 2001�has so far been published. Economist Intelligence Unit estimatesfor data before 2000 are based on the previous series.

There are no estimates for the GDP deflator, no reliable current price series andno US dollar GDP estimates (see The external sector: Foreign reserves and theexchange rate). The persistence of major price distortions and lack of a singleexchange rate will remain difficulties for the treatment of Cuban economic data.

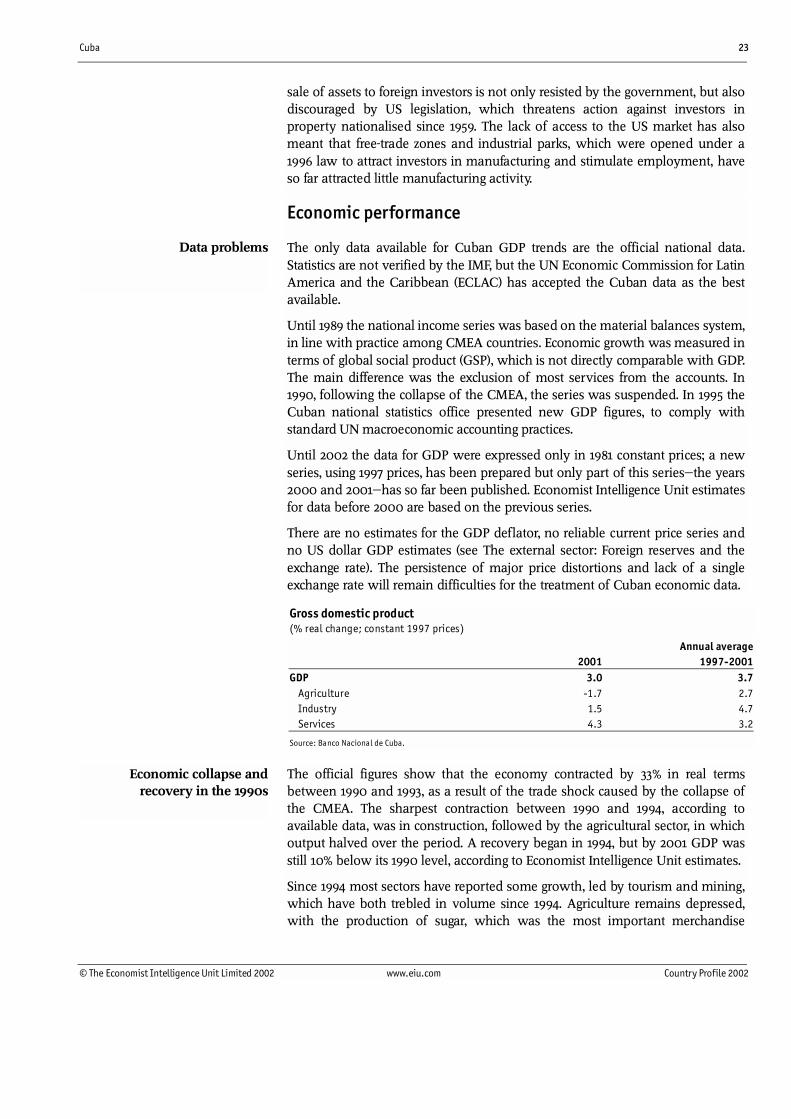

Gross domestic product(% real change; constant 1997 prices)

Annual average2001 1997-2001

GDP 3.0 3.7 Agriculture -1.7 2.7 Industry 1.5 4.7 Services 4.3 3.2

Source: Banco Nacional de Cuba.

The official figures show that the economy contracted by 33% in real termsbetween 1990 and 1993, as a result of the trade shock caused by the collapse ofthe CMEA. The sharpest contraction between 1990 and 1994, according toavailable data, was in construction, followed by the agricultural sector, in whichoutput halved over the period. A recovery began in 1994, but by 2001 GDP wasstill 10% below its 1990 level, according to Economist Intelligence Unit estimates.

Since 1994 most sectors have reported some growth, led by tourism and mining,which have both trebled in volume since 1994. Agriculture remains depressed,with the production of sugar, which was the most important merchandise

export in 1990, less than half the 1990 level (see Economic sectors: Agriculture).The level of activity in community, social and personal services has remainedalmost unchanged throughout the decade, reflecting the government�s policy ofmaintaining the level of health, education and social services provision. (SeeReference tables 5-8 for historical data on GDP growth.)

The priority given to welfare spending is also reflected on the demand side:official figures using constant prices show the fall in government currentspending between 1990 and 1993 was only 20% (most of which was achieved bycuts in defence and central government administration), while consumerspending contracted by 32% in the same period and state investment by a full80%. By 2001, consumer spending had recovered to 75% of its 1990 level,government current spending to 5% higher than in 1990, and investment wasstill 50% lower.

Although overall real output is reported to have contracted by one-thirdbetween 1990 and 1993, the decline in employment was only 2% over theperiod. Official policy was to leave people in jobs until alternative employmentcould be found. The result was a dramatic decline in labour productivity and ahigh level of disguised unemployment. Labour productivity has improved since1993, but the national average is still low by historical standards.

The measurement of inflation is difficult, because retail spending is dividedbetween a number of markets (US dollar and peso, state and private, legal andillegal). Price behaviour varies widely between these outlets. In the state-runpeso shops, rationed basic goods are sold at highly subsidised fixed prices. Thepeso cost of purchases in the state-owned US dollar shops is inflated by thedistorted domestic �unofficial� exchange rate (which was Ps26:US$1 in mid-2002). Prices in the free markets for domestically produced agricultural andindustrial products are determined by market conditions, and have tended to fallas availability has improved since the markets were established in 1994. Priceson the black market, which operates in both US dollars and pesos, fluctuatemost widely, but there are no published data series.

Inflation(% change)

Annual average2001 1997-2001

Consumer prices (av) -4.1a -1.2a

a Economist Intelligence Unit estimates, based on official year-end figures.

Source: Banco Central de Cuba.

The Ministry of Finance and Prices has made inflation estimates by using aweighted index of price changes in the various markets. The appreciation of theunofficial exchange rate accounted for some of the negative inflation reportedfor 1995 and 1996 (-11% and -4.9% respectively). This followed several years inwhich the cost of living grew rapidly, with the unofficial (and not yet legalised)exchange rate weakening to over Ps120:US$1 in 1994 and shortages reflected inhigh inflation in black markets. Year-end inflation was mildly negative in1999-2001, but the downward trend was reversed in the final months of 2001 asthe depreciation of the exchange rate pushed up the peso cost of dollar goods

and a severe hurricane reduced supplies to agricultural markets. (See Referencetable 9 for historical data on prices and earnings.)

Regional trends

Cuba is divided into 15 administrative regions: 13 provinces, each with apopulation of between 400,000 and one million; the City of Havana, with apopulation of 2.2m and the �special municipality� of the Isle of Youth, withonly 81,000. Over 75% of Cubans live in urban areas, reflecting the low share ofGDP accounted for by agriculture. Sugar is cultivated in most of the provinces,tobacco mainly in the west, coffee mainly in the east and citrus in the centre andon the Isle of Youth. Nickel extraction is concentrated in the eastern province ofHolguín, and most of the oil wells are in Matanzas province, close to Havana.The tourism industry, which has shown the strongest growth in the 1990s, hasdeveloped fastest in the City of Havana and the resorts on the northern coast ofMatanzas and Ciego de Avila provinces. The cities of Santiago de Cuba andTrinidad (in the province of Sancti Spíritus) have also become important tourismdestinations. Activity in the trading ports of Havana, Cienfuegos and Santiagode Cuba has been depressed since the contraction of shipping in the early 1990s.

Population by province, 2001(year-end)

% change�000 % of total 2001/1996

Pinar del Río 739 6.6 2.3Havana 712 6.3 5.0Havana City 2,182 19.4 0.3

Santiago de Cuba 1,041 9.3 2.3Guantánamo 516 4.6 0.1Isle of Youtha 81 0.7 4.1

Total 11,243 100.0 2.2

a Special municipality.

Source: Oficina Nacional de Estadísticas.

Havana contains around one-fifth of the total population. Migration to thecapital was slower than elsewhere in Latin America between 1959 and 1990,thanks to a deliberate policy of promoting development in the regions: Havana�spopulation grew by a modest average of 0.7% a year in that period, comparedwith 3-5% in other Latin American capitals. However, the onset of the economiccrisis in 1990 raised the pace of internal migration towards the capital, which hasattracted much of the tourism trade and foreign investment activity. Althoughlegislation introduced in 1997 provided the authorities with the power to limit

internal migration, slowing the flow, there is still a marked populationmovement from the poorer eastern provinces, where unemployment has beenhighest, towards those in the west, where economic dynamism is strongest.

Economic sectors

Agriculture

Despite some recovery since 1995, agricultural output in 2001 was still some 35%below its 1989 level. Agriculture employs around one-fifth of the workforce andaccounts for around one-third of merchandise export earnings. The largestagricultural export earner is still sugar, although the industry has contractedsharply since 1990 and is set to be further reduced in size in the next two years.

Reforms of the agricultural sector have had some success since 1990, butagricultural productivity remains generally low. A food programme introducedin 1991, which placed emphasis on voluntary labour and import-substitutingproduction, failed to halt the decline in output. From September 1993 a newform of enterprise, the unidades básicas de producción cooperativa (UBPCs, basicunits of co-operative production), began to take over land previouslyadministered by state farms. This transformed the structure of land tenure, but asystem of quotas and fixed prices continues to dampen incentives.

Land tenure(%; year-end)

1989 1998State 78 33UBPCs 0 41

Other co-operative ownership 10 9Private farmersa 12 16

a Includes service co-operatives.

Source: Oficina Nacional de Estadísticas.

One of the most dynamic sub-sectors over the past decade has been foodproduction in the non-state sector. Private farmers have responded to theopportunities offered by free agricultural markets, which have been operatingsince 1994, and local communities have set up successful urban farms toimprove food security. In the absence of finance for imported inputs over thepast decade, many crops have been produced organically. Growers have begunto win international certification for some of these crops, to secure a premiumprice for exports.

Agriculture was opened to foreign investment in 1994, but take-up has beenslow. Foreign involvement has been mainly in the financing, management andmarketing of export commodities and of by-products such as rum and cigars,although there have also been major investments in citrus production andprocessing. The pace of inward investment has been inhibited not only by thethreat of US sanctions against companies deemed to be �trafficking� innationalised land or property, but also by the authorities� unwillingness tosurrender control of agricultural land to foreign interests.

Sugar has traditionally dominated the agricultural sector, but the dominance isset to be ended by a decision in 2002 to restructure the industry. Since 1990,when Cuban producers lost the generous terms offered by the Council forMutual Economic Assistance (CMEA), the industry has faced severe difficulties.Output plummeted, from over 8m to around 4m tonnes between 1990 and 1994,and it has since remained around that level. The appointment of General UlisesRosales del Toro as sugar minister in late 1997 heralded a rationalisation process,in which quantitative targets were replaced by an emphasis on economicefficiency and the incentives structure was overhauled. The least efficient millswere closed, the price paid to farmers was increased and the decision was madeto leave more young cane in the ground to improve future yields. These changessucceeded in reducing costs and increasing awareness of the low returns in theindustry, but failed to increase the harvest (which was only 3.6m tonnes in2002). (See Reference table 10 for historical data on sugar production.)

In the restructuring plans announced in 2002, it is envisaged that around half ofthe mills will be permanently closed and half of the agricultural land undersugar will be transferred to other uses within two years. The state has promisedto maintain the salaries of the workforce during retraining and redeployment.The restructuring was announced soon after the inauguration of two newcompanies in the sector: a state finance company, Corporación FinancieraAzucarera (Arcaz), with initial capital of US$50m; and a trading company,Compania Azucarera Internacional (Caisa), a joint venture between the SugarMinistry and an unknown foreign partner. The industry plan prioritises thedevelopment of higher-value-added sugar products, including organic sugar,alcohol and other by-products.

The production of fruit and vegetables for domestic consumption has picked upstrongly since 1994, when free agricultural markets were introduced andcommunity gardens started, and are now higher than before the economic crisisof the early 1990s, despite a lower level of imported inputs. The success ofdomestic food cultivation is reflected in a decline in food import dependencysince 1997: spending on food imports has remained steady at around US$800msince 1997, despite an increase in total food consumption. This compares withfood import spending of over US$1bn in 1989, before the economic crisis hit.However, there are still some staple crops�particularly rice, beans and wheat�for which import dependency remains high. In recent years, rice is importedmainly from China and Vietnam, while France has been a leading supplier ofwheat, but the restoration of US food exports to Cuba since the end of 2001 hasbegun to divert this trade to the US. The once successful dairy industry is alsostill performing well below pre-1990 levels, and rations of milk are prioritised foryoung children and those with special medical needs. (See Reference table 11 forhistorical data on non-sugar agricultural production.)

Non-sugar export crops are gradually securing external and domestic financingto restore production. Citrus production has recovered to precrisis levels, afterfalling by over 40% between 1990 and 1994. Tobacco production fell by 60%from 1989 to 1993, but has also returned to its 1990 level, with the help ofharvest pre-financing from Europe. In 1999 a Franco-Spanish company, Altadis,agreed to purchase 50% of Habanos, the state company responsible for

marketing cigars internationally. The deal has been followed by a reorientationof policy, with the emphasis placed on maintaining the premium for Cubancigars rather than maximising output growth.

A lack of investment and working capital reduced deep-sea fish catches byaround one-half between 1990 and 1993. Although the sea catch is still 20%below its precrisis level, the development of fish farming since the mid-1990shas made up the shortfall. With output now exceeding the 1989 level, theindustry provides over one-half of domestic fish consumption, as well asproviding annual export income of almost US$100m. Lobster-processing plantshave been remodelled to international standards to handle growing export andtourist demand. (See Reference table 12 for historical data on fishing.)

Mining and semi-processing

Nickel plus cobalt reserves in the north-east of the island are among the world�slargest. Gold, copper and chromium are being extracted on a small scale, as areindustrial minerals, particularly zeolite. Nickel output more than doubled to61,600 tonnes over the four years to 1997, and has continued to rise since then,albeit at a slower pace. In 2002 output is expected to reach 80,000 tonnes. Adeal made in 1994 with Sherritt International of Canada has been the biggestsingle factor in reactivating nickel and cobalt output. Capacity will increase by afurther 60,000 tonnes in the medium term if two further plants, currently beingplanned, come on stream.

Manufacturing

The loss of the CMEA markets from 1989 caused a sharp contraction in themanufacturing sector. Cuban economists have estimated that non-sugar industrywas operating at only 35% of capacity in 1995. An enterprise restructuringprogramme has divided large firms into smaller units, and financial control isbeing gradually devolved from the ministerial to the enterprise level. Profit andloss accounting is playing a growing role, while subsidies are being cut back andfinancing is increasingly being allocated on the basis of projected future returns.Price reforms are being introduced cautiously along with enterprise reform, butthe continued lack of a single exchange rate continues to limit the use of profitand loss accounting.

The limited official data suggest that overall manufacturing output has returnedto its 1990 level, although recovery is uneven. The growth has been strongest inthose industries that can generate hard currency earnings. (See Reference table 13for historical data on selected industrial production.) These include enterprisessupplying the tourism sector, including drinks, food processing, furniture andelectrical appliances, which have been able to secure financing and marketsthrough joint ventures.

State investment has been concentrated in the development of biotechnologyand pharmaceuticals, both to ensure supplies for the national healthcare system(which has experienced shortages of medicines due to a lack of foreign exchangeand as a result of the US embargo) and in the expectation that they will become

important export earners in the medium term. As well as providing most of thefinance (over US$1bn since the late 1980s), the state sets the research agendas inbiotechnology and pharmaceuticals. Most of the research facilities areaccountable to the Ministry of Health, although the leading institutes are directlyaccountable to the Council of State. The industry�s institutions, which oftencombine research and production on the same site, are concentrated in theWestern Havana Science Park with 41 key research institutes, but there is also anationwide network of biotechnology centres, including scientific parks in SanctiSpíritus and Camagüey.

Construction

Total construction activity contracted by some 75% between 1990 and 1993, anddespite a recovery since then, activity was still less than 50% of the 1990 level in2000. Hotel building has made an important contribution to the recovery, anddespite slower growth in tourism in 2001-02, it has continued apace with threenew hotels in Varadero, two in Havana and two on the northern coast ofHolguín province under construction in 2002. Building work on housing andpublic buildings had almost halted between 1990 and 1995, leading to adeterioration in the stock, but since then public investment in these areas hasincreased. There have also been major construction projects in the mining andenergy sectors.

Property was opened to foreign investment and ownership in 1995, but policytowards the sector has vacillated since then. Consultations in preparation for theintroduction of a new law codifying real estate investment were launched in 1996,but they appear to have become bogged down, as the issues of ownership raisedby the discussions have proved to be intractable. After the opening of the sector in1995 foreign business interest was initially slow, but just as it started to surge in1998-99, raising the number of joint ventures from four to 18, officials began tolose enthusiasm. In April 2000 the opening of the sector was abruptly sus-pended and Cuban partners in existing projects in Havana bought back unsoldunits from their foreign partners. The move was described by the Cubanauthorities as �a pause� in the development pending a review of infrastructuralcapacity in Havana, but there has been no sign of a reopening of the sector sincethat time.

Financial services

A reform of the financial system, involving restructuring, modernisation andexpansion, was initiated in 1994. A new central bank, the Banco Central de Cuba(BCC), was established in 1997, removing central bank functions from the BancoNacional de Cuba (BNC). The BNC has become one of the set of new state-owned banks that have been established. A chain of bureaux de change (casasde cambio, or cadecas), for changing Cuban pesos for US dollars at the�unofficial� rate (see Foreign reserves and the exchange rate) has also beencreated. Over a dozen foreign banks have opened representative offices. Thedomestic banking system has been computerised, a clearing system is being putin place and automatic cash dispensing terminals are being installed for holders

of local and international credit cards and Cubans receiving social securitypayments.