Charlie Wellins Senior Vice President, Supply Chain Solu7ons, CEVA Logis7cs October 18 2012 TransPacific Mari7me Asia Conference Shenzhen, China Cu$ng costs out of the supply chain: what works and what doesn't?

Transcript

Charlie Wellins Senior Vice President, Supply Chain Solu7ons, CEVA Logis7cs

October 18 2012 Trans-‐Pacific Mari7me Asia Conference Shenzhen, China

Cu$ng costs out of the supply chain: what works and what doesn't?

Driving out cost: What we see in the market in 2012 • Customers focusing on driving more value and cost savings through 3&4PL Partnerships, rather than only looking at transac7onal freight forwarding costs

• More interest in End to End Visibility -‐ having access to end to end informa7on/KPIs and incen7vizing con7nuous cost improvement

• Outsourcing decision of op7mal transport mode based on required IN-‐DC date -‐ planning effec7vely to enable balancing of service vs cost

• A shiW to Increasing raHos of oceanfreight from clients with a historic reliance on airfreight (e.g. tech)

• Cost down origin solu7ons : Milkruns, FCA conversion, ConsolidaHons

• OpHmizing Packaging to reduce cost/waste and support green ini7a7ves

• ShiW toward Global DC’s in Asia 2 Cutting costs out of the supply chain: what works and what doesn't?

ShiPing to a Global DC in Asia

• Building DCs and MCC hubs in Asia to bypass more expensive des7na7on DCs while also being able to serve growing local markets

3

Before • High transporta7on costs

• Longer lead 7mes

• Distribu7on network under-‐ servicing major markets, i.e. West Coast USA

APer • More flexible supply chain

• Improved service levels

• Ability to also serve local markets

Cutting costs out of the supply chain: what works and what doesn't?

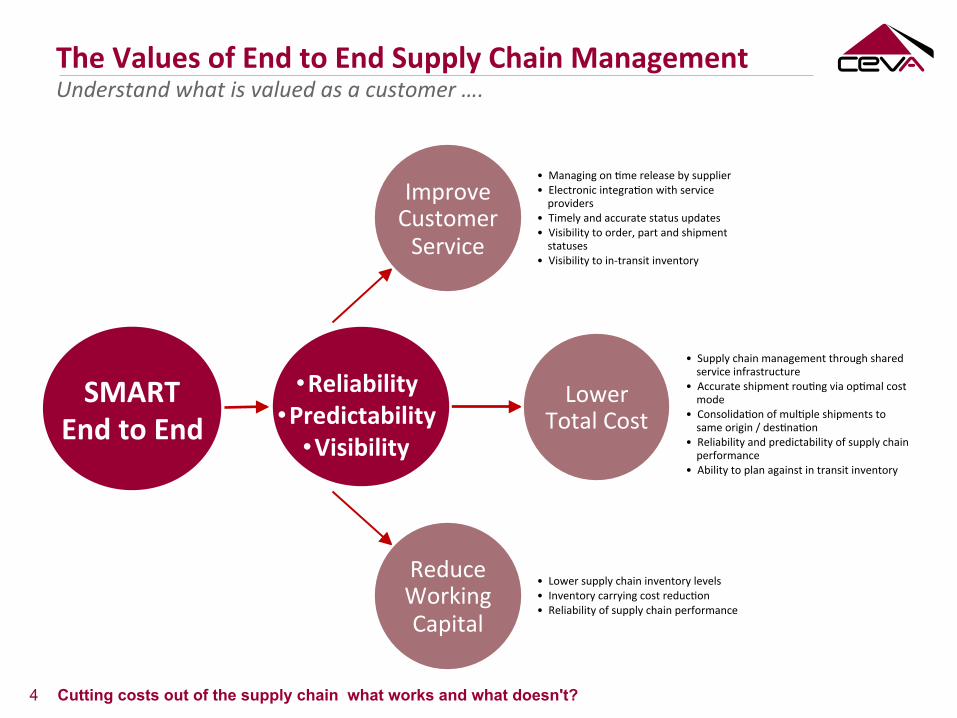

Improve Customer Service

• Managing on 7me release by supplier • Electronic integra7on with service providers

• Timely and accurate status updates • Visibility to order, part and shipment statuses

• Visibility to in-‐transit inventory

Lower Total Cost

• Supply chain management through shared service infrastructure

• Accurate shipment rou7ng via op7mal cost mode

• Consolida7on of mul7ple shipments to same origin / des7na7on

• Reliability and predictability of supply chain performance

The Values of End to End Supply Chain Management Understand what is valued as a customer ….

4 Cutting costs out of the supply chain what works and what doesn't?

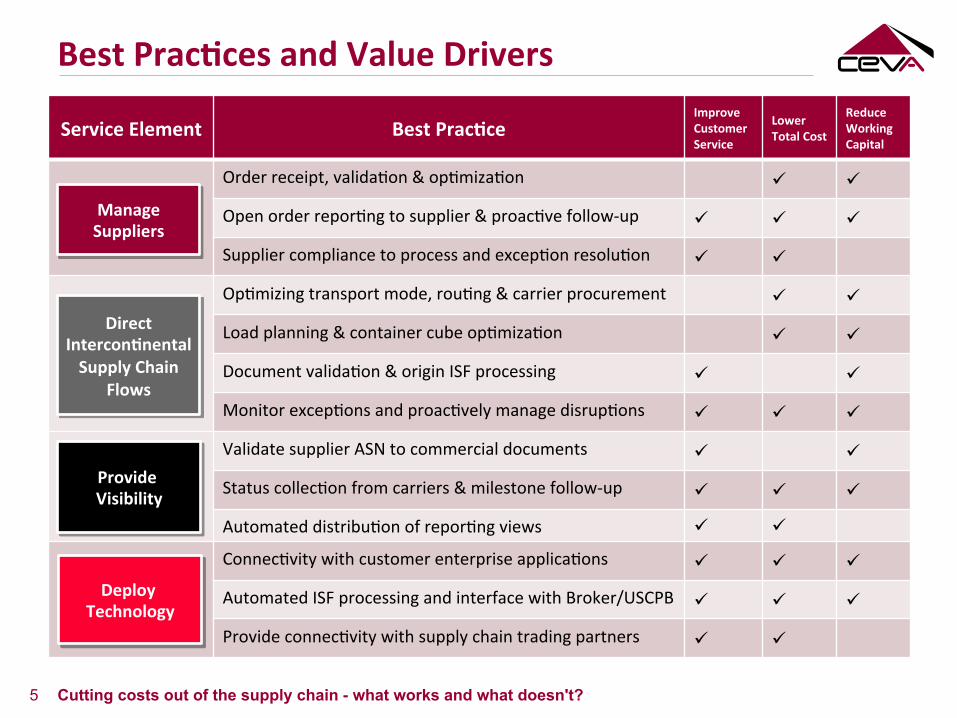

Best PracHces and Value Drivers

5 Cutting costs out of the supply chain - what works and what doesn't?

Service Element Best PracHce Improve Customer Service

Lower Total Cost

Reduce Working Capital

Order receipt, valida7on & op7miza7on ü ü

Open order repor7ng to supplier & proac7ve follow-‐up ü ü ü

Supplier compliance to process and excep7on resolu7on ü ü

Op7mizing transport mode, rou7ng & carrier procurement ü ü

Load planning & container cube op7miza7on ü ü

Document valida7on & origin ISF processing ü ü

Monitor excep7ons and proac7vely manage disrup7ons ü ü ü

Validate supplier ASN to commercial documents ü ü

Status collec7on from carriers & milestone follow-‐up ü ü ü

Automated distribu7on of repor7ng views ü ü

Connec7vity with customer enterprise applica7ons ü ü ü

Automated ISF processing and interface with Broker/USCPB ü ü ü

Provide connec7vity with supply chain trading partners ü ü

Manage Suppliers

Direct InterconHnental Supply Chain

Flows

Provide Visibility

Deploy Technology

6 Cutting costs out of the supply chain: what works and what doesn't?

24/10/12 p. 7 TPM Asia 2012

From Air to Ocean

TPM Asia 2012 Alfred Hofmann Go clean go Green

Containershipping : the most energy efficient way of transporting goods

24/10/12 p. 8 TPM Asia 2012

Agenda

� Key event influencing change � Cost of airfreight versus seafreight � Industries at forefront of the trend

� Challenges to the supply chain

� Solutions and Result

24/10/12 p. 9 TPM Asia 2012

From Air to Ocean Key event influencing change � Collapse of Lehman Brothers and the economic crisis � Consumer demand at lowest level � Airfreight was a “no” in most companies and only used in emergencies � Re-examing the supply chain � Re-stocking of 2010 did not change the long term fundamentals

24/10/12 p. 10 TPM Asia 2012

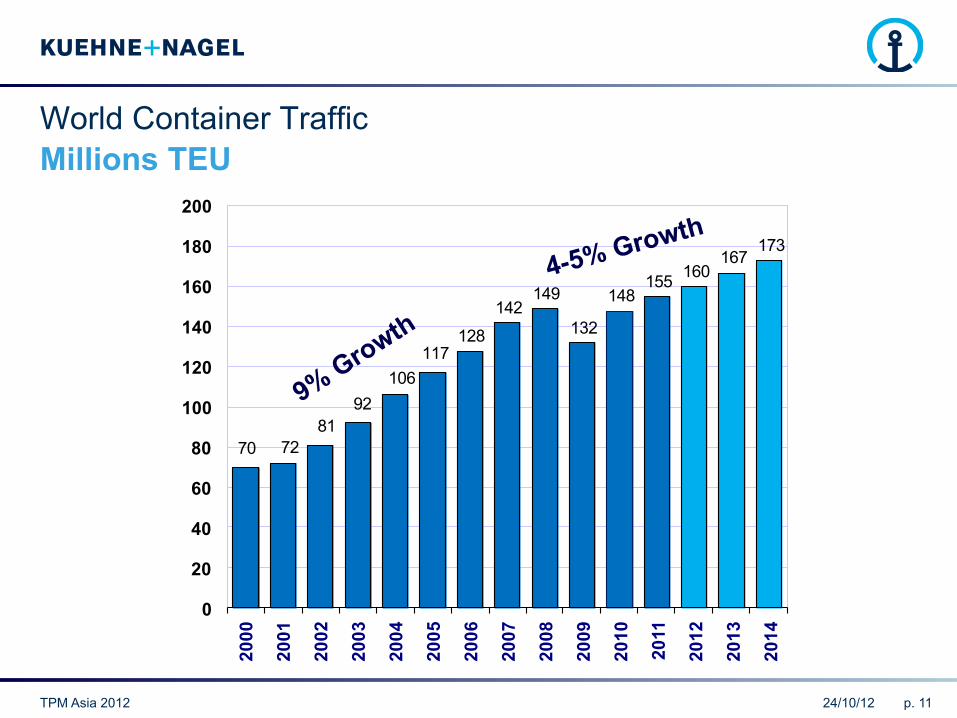

Growth in Global Air Travel (RPK) and Air Freight (FTK)

24/10/12 p. 11 TPM Asia 2012

70 7281

92106

117128

142149

132

148155 160

167173

0

20

40

60

80

100

120

140

160

180

200

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Millions TEU World Container Traffic

4-5% Growth

24/10/12 p. 12

From Air to Ocean

TPM Asia 2012

Cost of airfreight versus seafreight • 1x40‘ with 10tons from SHA/LAX

US$ 2,600 US$ 46,000

• 1x40‘ with 10 tons from SHA/HAM US$ 2,200 US$ 33,500

24/10/12 p. 13

From Air to Ocean

TPM Asia 2012

Industries at forefront of the trend • Pharmaceutical Industry

• Extremely high value cargo • Temperature controlled products which could be converted • Natural choice – Reefer Containers

• Hi-Tech Industy • Seriously started to convert notebooks 3 years ago • Industry aim is to convert over 50% of notebook shipments to ocean • Tablets go ocean after first wave of consumer demand has been satisfied

24/10/12 p. 14

From Air to Ocean

TPM Asia 2012

Challenges to the supply chain • Notoriously bad in forcasting of volumes • Cancellation of bookings versus actually shipped challenged promise to deliver to customers on time • Inadaquate communication between planers, ODM‘s and logistics departments • Insufficient visibility to manage flow of cargo • Re-examine security issues while cargo is in transit

24/10/12 p. 15

From Air to Ocean

TPM Asia 2012

Solution and Result • Ensure collaboration of all participants in the supply chain

• Planers, ODM‘s, Logistics Management, 3PL, Truckers, Carriers, Rail and Barge Operators • Provide excellent visibility • Reduce risk of unwanted surprises • Establish clear handling and security procedures

• Move to E2E with 3PL‘s managing process(Control Tower) • Reliable transit times – Reduction in overall leadtime • Assurance in the supply chain and availability of products in time • Cost reduction through better inventory control and increased cash flow

" Ian Richardson has been a resident of Asia for 20 years. Ian has adapted to the Chinese culture, Lifestyles and ways of business, building up an extensive Asian Network during this time.

" Ian boasts over 30 years experience within the logistics industry.

" With Ian’s knowledge and professionalism he was appointed to Managing Director and Partner of SEKO Synergy Hong Kong in 2008. Recently the company started its structural expansion and changed its name to SEKO Logistics (HK) Limited.

" Ian has worked with various Fortune 500 companies such as IKEA, Costco and Wal-Mart, and more latterly with fast-growing SME brands, all eager to expand their businesses in China and Asia. Ian enjoys building the business and encouraging his team of enthusiastic young professionals to greater success.

Ian Richardson – Director/Partner of SEKO Logis7cs (HK) Limited