24

Current Economic Climate of the Cattle Business Derrell S. Peel Breedlove Professor of Agribusiness and Extension Livestock Marketing Specialist

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| View: | 216 times |

| Download: | 0 times |

Current Economic Climate of the Cattle Business

Derrell S. PeelBreedlove Professor of Agribusiness and Extension Livestock Marketing Specialist

Oklahoma State University

Current Economic Climate

• Short and Medium Term– Current market situation– Industry and external factors

• Long Term– Industry structural change

Major Market Factors

• Cattle Inventory and Beef Production• Beef Demand• International Trade• Feed and Input Markets• Forage Conditions

BOXED BEEF CUTOUT VALUEChoice 600-900 Lbs. Carcass, Weekly

135

145

155

165

175

185

195

JAN APR JUL OCT

$ Per Cwt.

Avg.2005-09

2010

2011

C-P-6210/31/11Livestock Marketing Information Center

Data Source: USDA-AMS

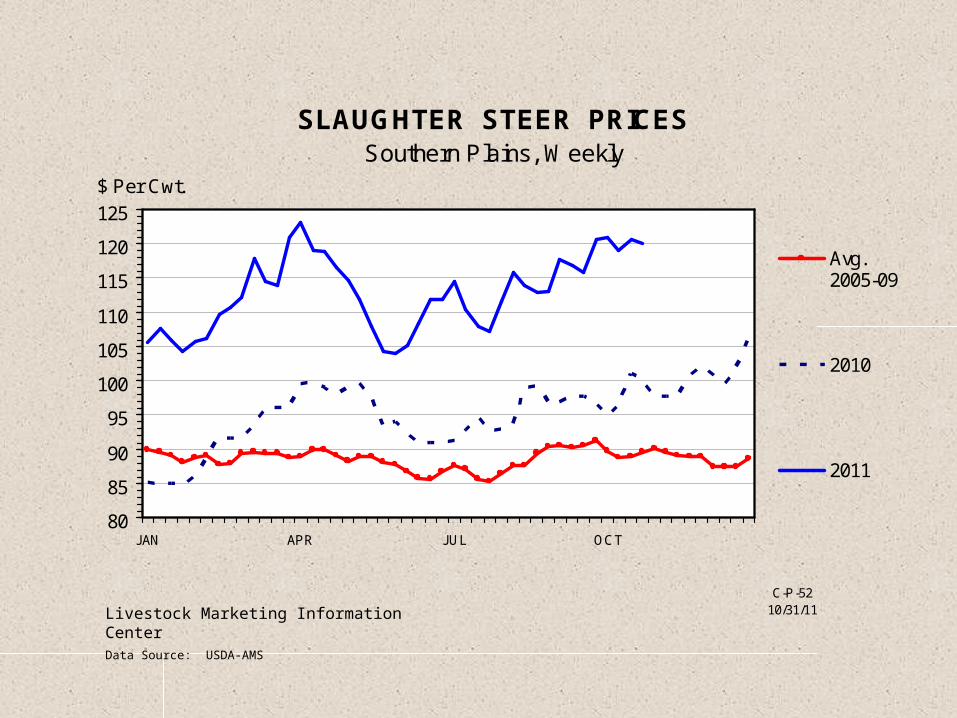

SLAUGHTER STEER PRICESSouthern Plains, Weekly

80

85

90

95

100

105

110

115

120

125

JAN APR JUL OCT

$ Per Cwt.

Avg.2005-09

2010

2011

C-P-5210/31/11Livestock Marketing Information Center

Data Source: USDA-AMS

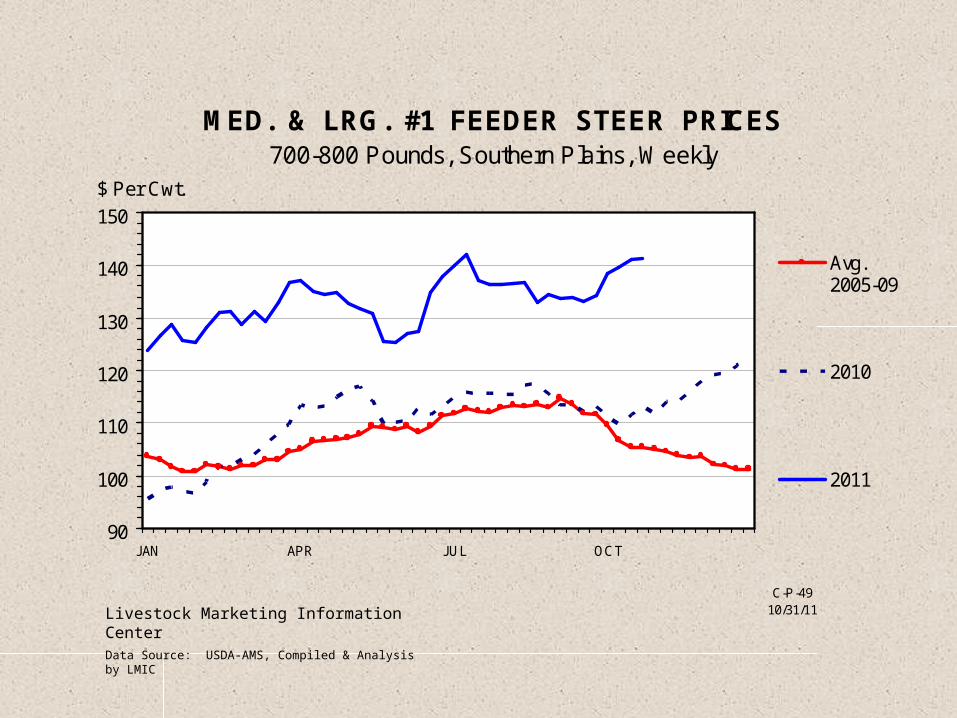

MED. & LRG. #1 FEEDER STEER PRICES700-800 Pounds, Southern Plains, Weekly

90

100

110

120

130

140

150

JAN APR JUL OCT

$ Per Cwt.

Avg.2005-09

2010

2011

C-P-4910/31/11Livestock Marketing Information Center

Data Source: USDA-AMS, Compiled & Analysis by LMIC

MED. & LRG. #1 STEER CALF PRICES400-500 Pounds, Southern Plains, Weekly

115

125

135

145

155

165

175

JAN APR JUL OCT

$ Per Cwt.

Avg.2005-09

2010

2011

C-P-49A10/31/11Livestock Marketing Information Center

Data Source: USDA-AMS, Compiled & Analysis by LMIC

SLAUGHTER COW PRICESSouthern Plains, 85-90% Lean, Weekly

40

45

50

55

60

65

70

75

80

85

JAN APR JUL OCT

$ Per Cwt.

Avg.2005-09

2010

2011

C-P-3510/31/11Livestock Marketing Information Center

Data Source: USDA-AMS

Oklahoma Cattle Inventory, January 12012 Forecast

2011 2012 %

Head Head Change Change

Beef Cows 2,036,000 1,780,000 -256,000 -12.6%

Beef Heifers 355,000 239,000 -116,000 -32.7%

Feeder Supply 2,120,000 1,102,000 -1,018,000 -48.0%All Cattle and Calves 5,100,000 3,723,000 -1,377,000 -27.0%

Oklahoma and U.S. Cattle Cycles: Beef Cow Inventory, January 1

1500

1700

1900

2100

2300

2500

2700

2900

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

29000

31000

33000

35000

37000

39000

41000

43000

45000

47000

OKLA US

Oklahoma All Cattle and Calves

1000

2000

3000

4000

5000

6000

7000

1920

1930

1940

1950

1960

1970

1980

1990

2000

2010

1000

Hea

d

Oklahoma Cattle Inventory by Agricultural Statistics District, January 1, 2012 Forecast

All Cattle and Calves Beef Cows % %

2011 2012 Change 2011 2012 ChangePANHANDLE 629,000 452,000 -28.1% 88,500 69,000 -22.0%WEST CENTRAL 443,500 248,500 -44.0% 167,000 129,000 -22.8%SOUTHWEST 495,000 251,000 -49.3% 180,000 137,500 -23.6%NORTH CENTRAL 572,000 305,000 -46.7% 177,000 143,500 -18.9%CENTRAL 758,400 526,000 -30.6% 324,000 273,000 -15.7%SOUTH CENTRAL 675,700 447,000 -33.8% 319,000 276,500 -13.3%NORTHEAST 750,900 755,500 0.6% 353,500 345,000 -2.4%EAST CENTRAL 499,500 498,500 -0.2% 280,000 266,000 -5.0%SOUTHEAST 276,000 239,500 -13.2% 147,000 140,500 -4.4%Total 5,100,000 3,723,000 -27.0% 2,036,000 1,780,000 -12.6%

Estimated Change in Grazing Animal Density, Head/Sq. mile, Jan. 1,2011 to 2012

State Ave. 130 => 91

Panhandle 70 => 29

W. Cent. 112 => 58

S. W. 143 => 71

N. Cent. 136 => 70

Central 147 => 100

N. East. 150 => 150

E. Cent. 155 => 155

S. East. 155 => 135

S. Cent. 127 => 84

OKLAHOMA

NATIONAL AVERAGE CORN PRICECrop Year, Received by Farmers

1.00

2.00

3.00

4.00

5.00

6.00

7.00

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

$ Per Bushel

G-NP-0310/12/11Livestock Marketing Information Center

Data Source: USDA-NASS, Compiled & Forecasts by LMIC

Feedlot Cost of GainKansas, $/cwt.

Jan-

90

Jan-

92

Jan-

94

Jan-

96

Jan-

98

Jan-

00

Jan-

02

Jan-

04

Jan-

06

Jan-

08

Jan-

10

40.00

50.00

60.00

70.00

80.00

90.00

100.00

110.00

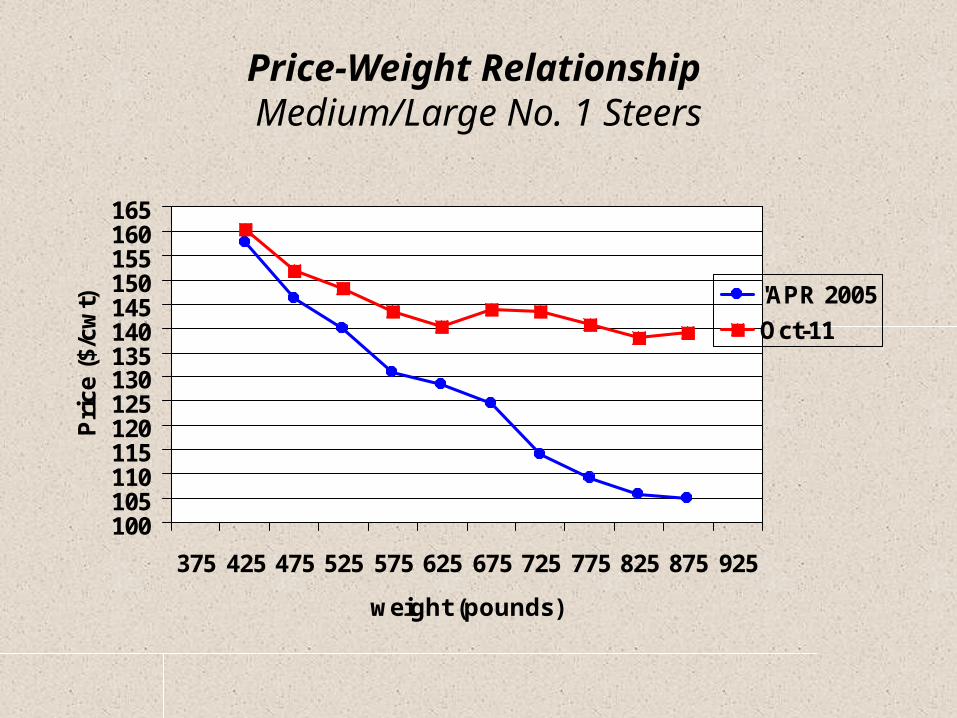

Price-Weight Relationship Medium/Large No. 1 Steers

100105110115120125130135140145150155160165

375 425 475 525 575 625 675 725 775 825 875 925

weight (pounds)

Pri

ce (

$/cw

t) 'APR 2005

Oct-11

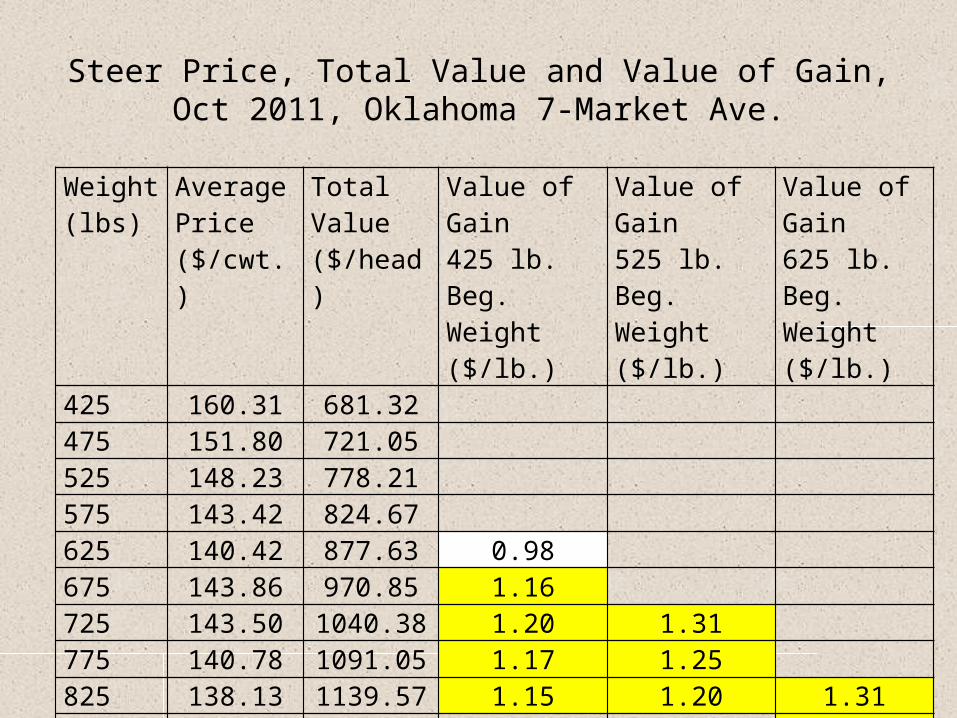

Steer Price, Total Value and Value of Gain, Oct 2011, Oklahoma 7-Market Ave.

Weight (lbs)

Average Price ($/cwt.)

Total Value ($/head)

Value of Gain425 lb. Beg. Weight($/lb.)

Value of Gain525 lb. Beg. Weight($/lb.)

Value of Gain625 lb. Beg. Weight($/lb.)

425 160.31 681.32475 151.80 721.05525 148.23 778.21575 143.42 824.67625 140.42 877.63 0.98675 143.86 970.85 1.16725 143.50 1040.38 1.20 1.31775 140.78 1091.05 1.17 1.25825 138.13 1139.57 1.15 1.20 1.31875 139.03 1216.51 1.36925 134.65 1245.51 1.23

Cattle Markets are Providing Twin Signals to Producers

• Increase Calf Production– Herd Expansion

• More Stocker Production– Keep feeder cattle on forage longer

• Both Signals Imply Increased Demand for Forage

• Different From History When Cow-Calf and Stocker Production was a Tradeoff

Total Meat Supplies Down in 2012

2011 2012• Beef ↓0.25% ↓3.5%• Pork ↑1.5% ↑0.5%• Broilers ↑0.8% ↓2.5%• Total Meat ↑0.8% ↓1.9%

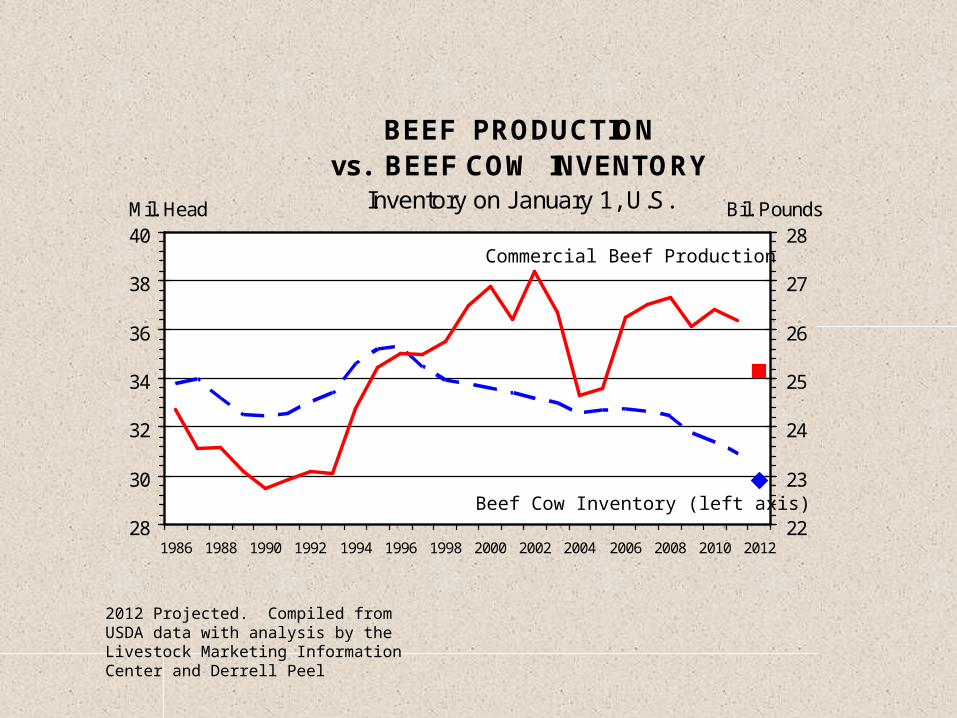

BEEF PRODUCTION vs. BEEF COW INVENTORY

Inventory on January 1, U.S.

28

30

32

34

36

38

40

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Mil. Head

22

23

24

25

26

27

28Bil. Pounds

Commercial Beef Production

Beef Cow Inventory (left axis)

2012 Projected. Compiled from USDA data with analysis by the Livestock Marketing Information Center and Derrell Peel

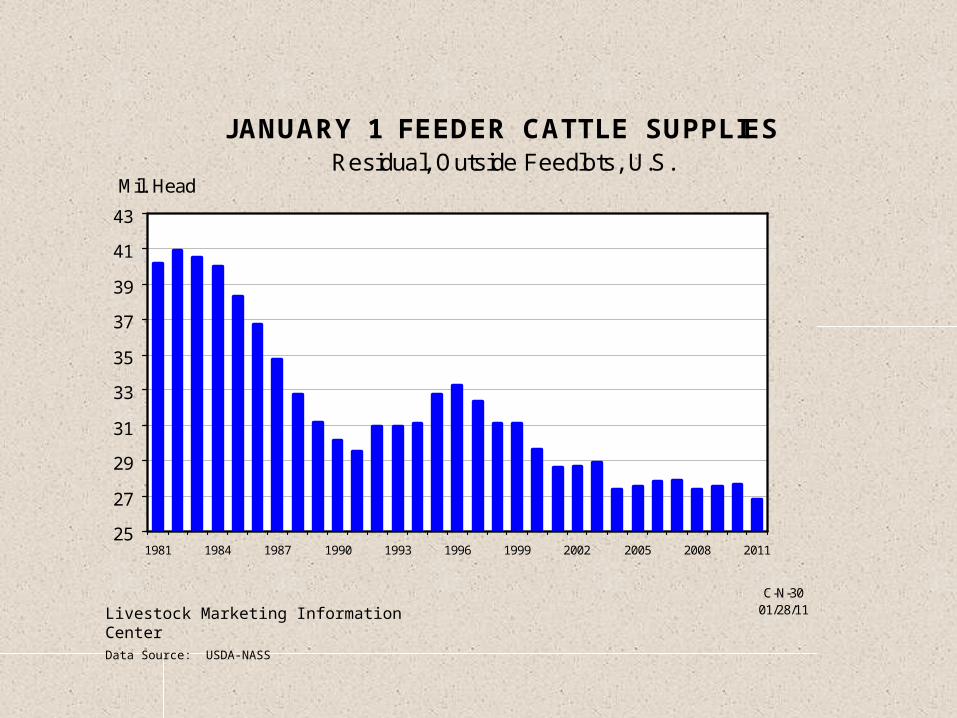

JANUARY 1 FEEDER CATTLE SUPPLIESResidual, Outside Feedlots, U.S.

25

27

29

31

33

35

37

39

41

43

1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011

Mil. Head

C-N-3001/28/11Livestock Marketing Information Center

Data Source: USDA-NASS

ANNUAL AVERAGE CATTLE PRICESSouthern Plains

55

75

95

115

135

155

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

$ Per Cwt

500-600lbSteerCalves

700-800lbFeederSteers

FedSteers

C-P-0610/05/11Livestock Marketing Information Center

Data Source: USDA-AMS, Compiled & Analysis by LMIC

The Weekly Email NewsletterFrom OSU Animal Science and Agricultural Economics

Send Email to [email protected]

THANK YOU!